AML (Anti-Money Laundering) compliance is one of the toughest responsibilities for any large organization that handles regulated money. Financial institutions, fintechs, and other businesses face an increasing challenge, which is that manual processes, scattered monitoring tools, and slow reporting are creating real risks.

At the same time, regulators in the US, EU, and APAC are stepping up their oversight. The pressure is greatest on organizations that still rely on outdated systems. It is because these systems cannot keep up with the pace and complexity of today’s financial crime. Building a RegTech platform for AML automation requires a complete system where transaction monitoring, risk scoring, regulatory reporting, and case management are designed to work together from the beginning, rather than being pieced together under audit deadlines.

At Intellivon, RegTech platforms are designed to make compliance a strength, not just a cost. This blog discusses how we build a modern AML automation system, from collecting data and detecting risks to reporting and scaling across borders.

Why Fintech Enterprises Are Investing in RegTech Platforms

Fintech enterprises are investing in RegTech platforms to automate compliance as regulations grow more complex. At the same time, cyber threats and digital transactions continue to rise.

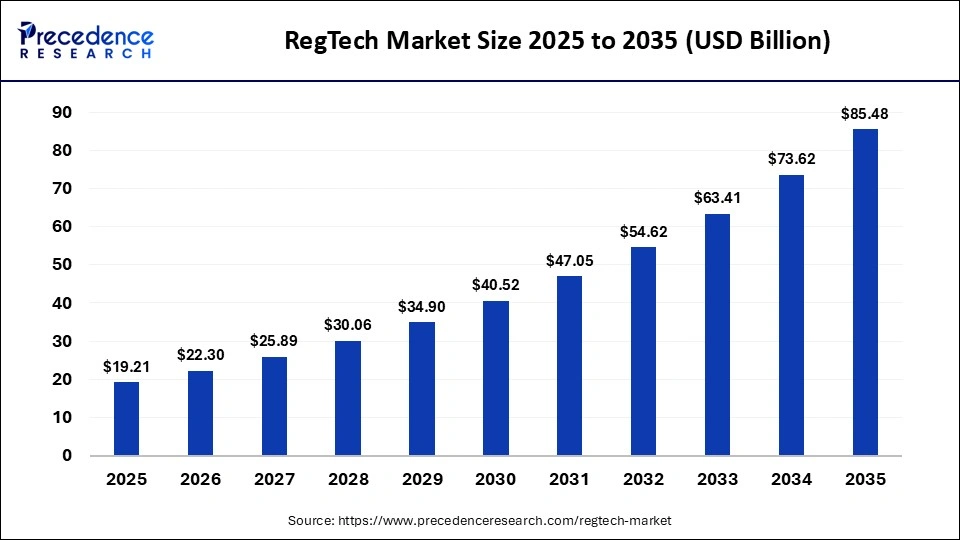

As a result, many organizations are adopting RegTech infrastructure alongside systems for KYC, KYB, and fraud detection. The global RegTech market reached $19.21 billion in 2025. It is expected to grow to $22.30 billion in 2026. By 2035, the market could reach $85.48 billion, expanding at a 16.10% CAGR between 2026 and 2035.

1. Compliance complexity in fintech ecosystems

Global financial regulations evolve at a staggering pace, often changing daily across different jurisdictions. Maintaining a consistent posture requires sophisticated logic that can interpret these shifts without disrupting core services.

Therefore, specialized platforms act as a dynamic shield, translating legal requirements into executable technical protocols automatically.

2. Explosion of ML monitoring needs

The sheer volume of digital payments makes manual oversight physically impossible for growing enterprises. Robust Anti-Money Laundering (AML) tools utilize advanced pattern recognition to flag suspicious behavior in milliseconds.

This real-time visibility ensures that high-velocity platforms remain secure while maintaining the fluid user experience customers expect today.

3. Limitations of manual compliance workflows

Human-led verification processes are inherently slow and prone to expensive clerical errors. These legacy methods create friction during customer onboarding, which directly leads to high abandonment rates and lost revenue.

By contrast, moving away from manual entry allows your specialized talent to focus on high-level strategy rather than repetitive data validation.

Why fintech infrastructure requires RegTech automation

Scalability in the financial sector is strictly tethered to the efficiency of your underlying compliance engine. Automation allows a platform to handle millions of users across diverse markets without a linear increase in headcount.

Furthermore, it provides the verifiable audit trails necessary to satisfy the most stringent international banking standards and partners.

In summary, the transition to automated regulatory technology is no longer optional for firms chasing global scale. It provides the necessary foundation for sustainable growth and long-term institutional trust in an increasingly scrutinized digital economy.

What Is a RegTech Platform for AML Compliance Automation?

A RegTech platform for AML compliance automation is a specialized software ecosystem that digitizes the oversight of financial transactions. This technology integrates directly into existing banking or enterprise workflows to monitor for money laundering.

It replaces manual verification with real-time data processing and automated screening. Consequently, organizations can detect suspicious activity instantly without human intervention.

These systems provide the technical foundation for scalable risk management in high-volume environments.

How RegTech Platforms Automate Fintech Compliance

Fintech companies operate in highly regulated environments. As transaction volumes grow, manual compliance processes become difficult to manage. Teams must monitor transactions, verify customer identities, and report suspicious activity while maintaining regulatory accuracy.

RegTech platforms solve this challenge by automating core compliance workflows. They combine data integration, monitoring engines, and regulatory reporting systems into one coordinated infrastructure. As a result, fintech enterprises can scale operations while maintaining strong compliance oversight.

1. Automated Transaction Monitoring

RegTech platforms continuously analyze financial transactions across payment systems, wallets, and banking infrastructure. The system applies risk rules and behavioral models to identify unusual activity.

When suspicious patterns appear, alerts are generated automatically. At the same time, compliance teams can then review the cases instead of manually scanning thousands of transactions.

2. Risk-Based Customer Monitoring

Customer risk levels change over time. RegTech platforms, therefore, track user behavior, transaction activity, and geographic exposure to update risk scores dynamically.

This risk-based monitoring helps fintech companies focus attention on high-risk accounts. As a result, compliance teams allocate resources more efficiently.

3. Automated Sanctions and Watchlist Screening

Financial institutions must screen customers against sanctions lists, politically exposed person (PEP) databases, and global watchlists. RegTech platforms automate this screening process during onboarding and throughout the customer lifecycle.

The system performs real-time checks and flags potential matches for review. This reduces the risk of processing transactions linked to restricted entities.

4. Regulatory Reporting Automation

Compliance reporting is one of the most time-consuming regulatory tasks. RegTech platforms simplify this process by automatically collecting investigation data, alert histories, and case outcomes.

These systems then generate regulatory reports such as suspicious activity reports (SARs). As a result, fintech companies can meet reporting obligations without manual data compilation.

RegTech platforms transform compliance from a manual process into an automated operational system. By combining monitoring, risk analysis, and reporting workflows, fintech enterprises can maintain regulatory compliance while continuing to scale digital financial services.

Core Modules Inside a RegTech Platform

A RegTech platform works as a coordinated compliance infrastructure. Instead of relying on separate tools, fintech enterprises use one system to manage monitoring, risk analysis, and regulatory reporting.

Each module performs a specific compliance function, but all components share data and workflows. As a result, compliance teams gain better visibility across operations.

Most enterprise RegTech platforms include the following core modules:

- Customer identity verification module: This module supports KYC and KYB checks during onboarding. It verifies identities, validates documents, and confirms beneficial ownership information.

- Transaction monitoring engine: The monitoring system analyzes transactions in real time. It detects unusual behavior patterns and generates alerts when activity exceeds predefined risk thresholds.

- Sanctions and watchlist screening module: This component screens customers and transactions against global sanctions lists, politically exposed person databases, and regulatory watchlists.

- Risk scoring and analytics engine: The platform calculates risk scores based on customer activity, geography, transaction patterns, and behavioral signals. These scores guide compliance investigations.

- Case management and investigation workflow: Compliance teams use this module to review alerts, document investigations, and track suspicious activity cases from detection to resolution.

- Regulatory reporting system: The reporting module compiles investigation data and automatically generates reports required by regulators, such as suspicious activity reports.

Together, these modules create a unified compliance system. By integrating monitoring, risk assessment, and reporting workflows, RegTech platforms help fintech enterprises manage regulatory obligations more efficiently.

How AML Automation Fits into RegTech Architecture

AML automation works as a core capability inside a RegTech platform. The RegTech layer manages compliance infrastructure, governance, and reporting. Meanwhile, AML systems focus on detecting suspicious financial activity. Together, they create a structured compliance environment for fintech enterprises.

In practice, AML automation connects several operational layers within the platform. It monitors transactions, evaluates customer risk, and supports compliance investigations.

As a result, fintech companies can manage AML obligations without relying on fragmented systems.

Within a RegTech architecture, AML automation supports the following functions:

- Transaction Monitoring Integration: AML engines analyze payment activity, transfers, and account behavior. When unusual patterns appear, the system generates alerts for investigation.

- Customer Risk Intelligence: AML monitoring evaluates customer behavior, geographic exposure, and transaction patterns. These signals contribute to dynamic risk scoring across the platform.

- Case Management Coordination: Once alerts are triggered, they move into investigation workflows. Compliance teams review cases, document findings, and track outcomes.

- Regulatory Reporting Automation: AML systems collect investigation data and prepare suspicious activity reports. The RegTech platform manages submission and audit documentation.

AML automation acts as the detection and investigation engine within a RegTech platform. By connecting monitoring, risk analysis, and reporting workflows, fintech enterprises can manage compliance at scale while maintaining regulatory oversight.

Why AML Automation Is a Core RegTech Capability

AML compliance is no longer periodic or reactive. For enterprises running BNPL programs, it is a continuous, data-intensive obligation. Manual review cannot keep pace with transaction volumes, customer diversity, and cross-border complexity. Therefore, AML automation must be a foundational platform capability, and not an afterthought.

Regulators across the US, EU, and Asia-Pacific hold BNPL providers to the same AML standards as traditional lenders. Enforcement actions in this space are increasing. At the same time, the cost of non-compliance compounds fast, financially, operationally, and reputationally.

1. AML Monitoring as a Regulatory Obligation

Enterprises offering BNPL credit operate within defined regulatory perimeters, like the Bank Secrecy Act, the EU’s AMLD6, or equivalent frameworks across GCC and Southeast Asia. Each demands active monitoring, not passive response.

BNPL-specific risk typologies, like synthetic identity fraud, merchant-borrower collusion, and structured payment abuse, differ from traditional banking risks. Therefore, generic AML rule sets borrowed from retail banking will miss what matters most. Monitoring logic must reflect the product, the customer segment, and the geography.

2. Transaction Monitoring at Enterprise Scale

Volume changes everything. Monitoring tens of thousands of daily transactions requires near real-time processing across multiple data streams simultaneously. Batch-processing architectures simply cannot support this.

Effective platforms combine rule-based logic with machine learning. Rules catch known patterns precisely. Models’ surface emerging anomalies rules haven’t yet been written for. Together, they create adaptive monitoring that evolves alongside fraud typologies.

Compliance teams also need granular control over alert thresholds, tunable by segment, product type, and channel. Rigid sensitivity settings either flood teams with false positives or miss genuine risk entirely.

3. Regulatory Reporting Requirements

Automating SAR and CTR filing reduces analyst burden significantly. A mature platform pulls structured data from the monitoring layer, formats it per jurisdiction requirements, and routes filings through the correct submission channel, accurately and on time.

4. Integration with KYC and Onboarding Systems

AML effectiveness depends directly on KYC data quality. When both systems share real-time data pipelines, updated customer risk profiles immediately inform transaction monitoring.

This bidirectional flow shortens investigation cycles and strengthens the overall compliance architecture.

AML automation is the operational backbone of any enterprise BNPL program built to scale responsibly. Enterprises that embed it at the infrastructure level move faster, stay cleaner, and stand on far stronger regulatory ground.

Core Components of an AML Automation Platform

A RegTech platform for AML compliance automation is a specialized software ecosystem that digitizes the oversight of financial transactions. This technology integrates directly into existing banking or enterprise workflows to monitor for money laundering.

Consequently, organizations can detect suspicious activity instantly without human intervention. These systems provide the technical foundation for scalable risk management in high-volume environments.

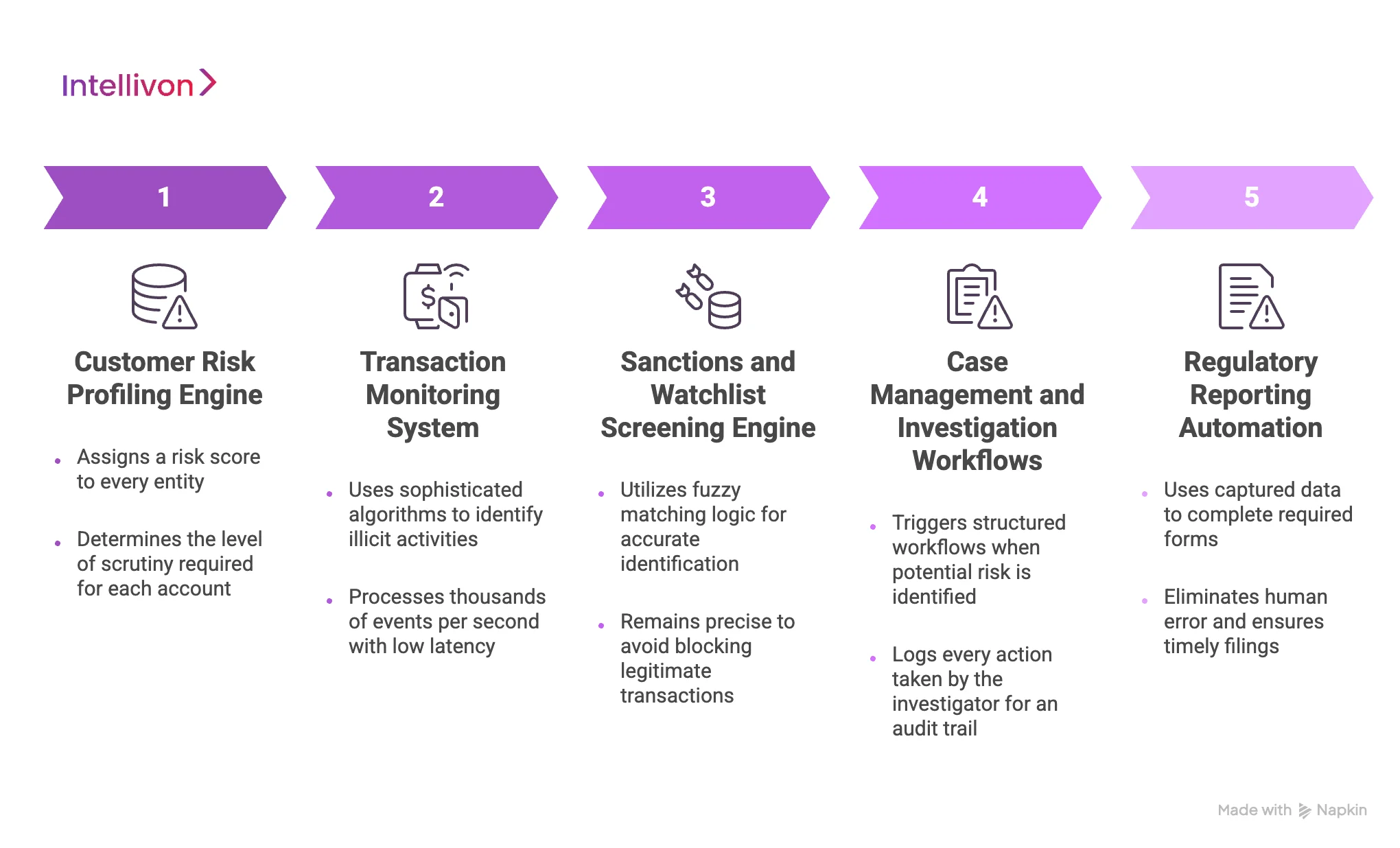

1. Customer Risk Profiling Engine

The customer risk profiling engine serves as the intelligence hub for initial and ongoing due diligence. It automatically assigns a risk score to every entity based on geographic location, business type, and historical behavior.

Therefore, the system determines the level of scrutiny required for each account without manual intervention.

2. Transaction Monitoring System

A high-performance transaction monitoring system analyzes every movement of funds in real-time to detect suspicious patterns. It uses sophisticated algorithms to identify layering, structuring, or rapid movement of capital across multiple jurisdictions.

Because this system processes thousands of events per second, it must maintain low latency while checking against complex rule sets.

3. Sanctions and Watchlist Screening Engine

This engine scans all involved parties against global databases like OFAC, the UN, and various national PEP lists. It utilizes fuzzy matching logic to account for spelling variations, aliases, and phonetic similarities across different languages.

However, the system must remain precise to avoid blocking legitimate transactions unnecessarily.

4. Case Management and Investigation Workflows

When the automation identifies a potential risk, it triggers a structured workflow within the case management module. This interface provides compliance officers with a unified view of all relevant data, including linked accounts and flagged documents.

Furthermore, the system logs every action taken by the investigator to create a tamper-proof audit trail.

5. Regulatory Reporting Automation

The final stage of the compliance lifecycle involves filing Suspicious Activity Reports (SARs) with the appropriate authorities. This module automatically populates the required forms using the data captured during the investigation.

Consequently, the enterprise eliminates the risk of human error and ensures that filings are submitted within mandatory deadlines.

Solving these technical hurdles requires a blend of engineering excellence and regulatory expertise. Ultimately, the goal is to create a seamless system that identifies risk without hindering legitimate business operations.

AML Regulations Your RegTech Platform Must Support

A globally effective RegTech platform for AML compliance automation must adhere to a complex web of international and local mandates. Consequently, the architecture needs to be flexible enough to incorporate regional nuances without requiring a complete code overhaul.

This ensures that your enterprise remains protected across every jurisdiction where you operate.

1. FATF global AML standards

The Financial Action Task Force sets the international benchmark for combating money laundering and terrorist financing. Your platform must implement the FATF “Risk-Based Approach” to allocate resources where threats are highest.

Therefore, the software should automatically adjust monitoring intensity based on the latest FATF Mutual Evaluation Reports.

2. Bank Secrecy Act (BSA) compliance

For entities operating in the United States, adhering to the BSA is a fundamental requirement for maintaining a banking license. The platform must automate the recording of cash transactions and the maintenance of detailed customer identification programs.

Consequently, this prevents the heavy fines associated with record-keeping failures and inadequate internal controls.

3. EU Anti-Money Laundering Directives

European markets follow the evolving AMLD framework, which emphasizes the identification of ultimate beneficial owners and crypto-asset transparency.

Your system must handle the stringent data privacy requirements of GDPR while performing these mandatory checks. This balance ensures that you meet European transparency standards without compromising user data rights.

4. FinCEN Regulatory Reporting Requirements

FinCEN demands precise electronic filing for large currency transactions and complex financial crimes. The platform should include a direct gateway for submitting these reports in the required XML formats.

Furthermore, it must track acknowledgment receipts from the agency to ensure every filing is officially logged and verified.

5. Suspicious Activity Reporting Frameworks

Every jurisdiction has a unique threshold and timeline for filing a Suspicious Activity Report (SAR). The system must trigger automated alerts when internal thresholds are crossed, such as sudden large-value transfers.

This ensures that your compliance team submits high-quality, actionable intelligence to authorities within the mandatory 30-day window.

The complex nature of global mandates means that manual updates are no longer feasible for a growing enterprise. Therefore, a RegTech platform for AML compliance automation acts as a digital safeguard that evolves alongside international law.

Architecture of a RegTech Platform for AML Automation

Designing a high-performance RegTech platform for AML compliance automation requires a decoupled architecture capable of processing massive datasets. This technical foundation must support high availability and fault tolerance to prevent gaps in regulatory oversight.

Consequently, a microservices-based approach allows each functional component to scale independently as transaction volumes grow.

1. Data ingestion and integration layer

This layer acts as the entry point for all structured and unstructured data from core banking systems and external APIs. It utilizes Kafka or similar message brokers to handle high-frequency data streams without loss.

Furthermore, the ingestion process normalizes disparate data formats into a standardized schema for downstream analysis.

2. Risk scoring and analytics engine

The analytics engine applies complex mathematical models to assess the risk level of every entity and transaction. It calculates scores based on hundreds of variables, including geographic risk and behavioral history.

Consequently, the system can flag high-risk activities in milliseconds to prevent illicit funds from moving through the network.

3. Real-time monitoring infrastructure

Real-time infrastructure provides the “always-on” surveillance required to identify suspicious patterns as they happen. It runs continuous checks against predefined rule sets and machine learning models to detect anomalies.

This setup ensures that the enterprise meets the immediate notification requirements of modern regulatory bodies.

4. Case investigation workflow system

This system translates raw alerts into a structured environment for human review and decision-making. It provides investigators with a comprehensive dashboard that consolidates all relevant evidence and historical context.

Therefore, the team can resolve cases faster while maintaining a detailed audit trail of every investigative step.

5. Compliance reporting infrastructure

The reporting infrastructure automates the generation and submission of regulatory filings to national financial intelligence units. It maps internal data to specific jurisdictional templates to ensure 100% accuracy in every submission.

This automation significantly reduces the time between detection and reporting, which is a key metric for regulators.

A robust architecture serves as the definitive bridge between technical stability and regulatory reliability. This structural integrity ultimately safeguards the organization against both financial crime and operational failure.

Governance Framework for AML Automation Platforms

A robust governance framework ensures that a RegTech platform for AML compliance automation operates within defined legal and ethical boundaries. This structure provides the necessary oversight to align automated decision-making with corporate risk appetite.

Consequently, it creates a transparent environment where every automated action is justifiable to internal stakeholders and external regulators.

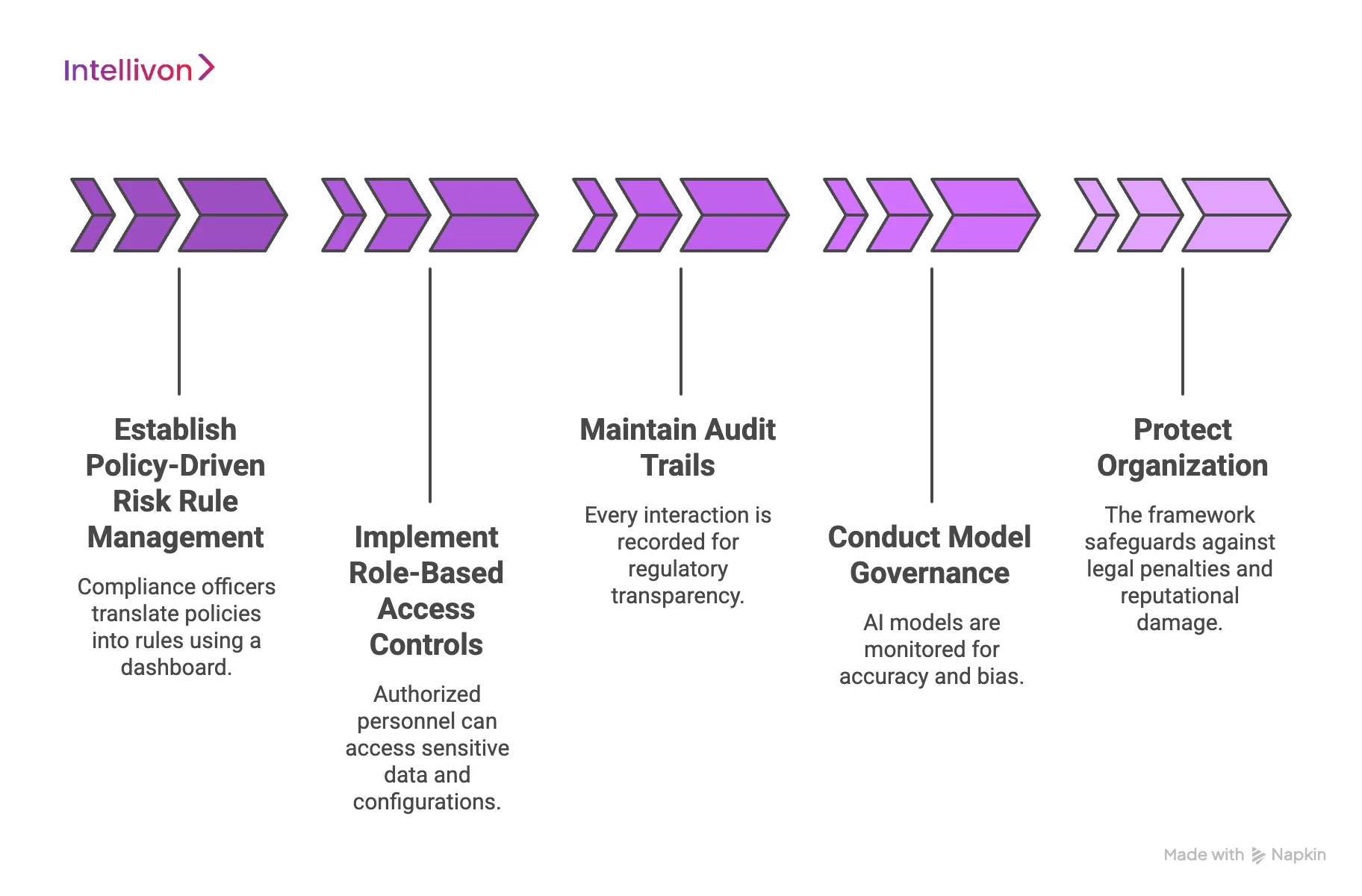

1. Policy-Driven Risk Rule Management

The governance layer allows compliance officers to translate high-level legal policies into executable technical rules without writing code. It utilizes a centralized dashboard to update risk thresholds and screening criteria across the entire organization instantly.

Therefore, the enterprise can react to new threats or regulatory changes with unprecedented speed and precision.

2. Role-Based Access and Approval Controls

Strict access controls ensure that only authorized personnel can modify sensitive compliance configurations or view private customer data. The platform implements multi-factor authentication and granular permissions to prevent internal fraud or accidental data exposure.

Furthermore, significant changes to the system require dual-approval workflows to maintain a high level of operational integrity.

3. Audit Trails for Regulatory Transparency

Every interaction within the platform is recorded in a tamper-proof ledger to provide a complete history of the compliance lifecycle. These logs capture the data inputs, the specific rules applied, and the final decision reached by the automation engine.

Consequently, during a regulatory audit, the enterprise can demonstrate exactly why a specific transaction was flagged or cleared.

4. Model Governance for AI Monitoring Systems

As machine learning becomes central to detection, model governance ensures these algorithms remain accurate and free from unintended bias. The framework includes regular “back-testing” and performance monitoring to detect any drift in the model’s effectiveness over time.

This continuous validation process is essential for maintaining the trust of regulators who scrutinize AI-driven decision-making.

A well-defined governance framework transforms a complex technical tool into a reliable corporate asset. This alignment between technology and policy ultimately protects the organization from both legal penalties and reputational damage.

Data Sources That An AML RegTech Platform Must Integrate

A sophisticated RegTech platform for AML compliance automation depends entirely on the quality and variety of its data inputs. Integrating diverse streams allows the system to build a comprehensive picture of financial movement and entity risk.

Consequently, the platform acts as a central nervous system that synthesizes information from across the entire enterprise ecosystem.

1. Core Banking and Payment Systems

The platform must connect directly to the ledgers that record every deposit, withdrawal, and transfer in real-time. This integration provides the raw transaction data necessary for the monitoring engine to identify suspicious patterns or velocity spikes.

Furthermore, it allows the system to track the movement of funds across different account types and geographical borders.

2. Customer Identity and Onboarding Systems

Integrating with identity management tools ensures that the compliance engine has access to verified government IDs and biometric data.

This connection allows the platform to verify that the person performing a transaction is the same individual cleared during onboarding. Therefore, it creates a consistent link between a physical identity and its digital financial footprint.

3. Sanctions and PEP Databases

A reliable platform maintains constant synchronization with international watchlists such as OFAC, the UN, and various national sanctions records. The system automatically cross-references every involved party against these databases to flag prohibited individuals or high-risk political figures.

Consequently, the enterprise remains compliant with global laws that forbid transacting with sanctioned entities.

4. External Fraud and Risk Intelligence Data

Beyond standard lists, integrating third-party risk intelligence provides deeper insights into emerging criminal trends and “dark web” activity. These data feeds alert the system to compromised credentials or known fraudulent wallet addresses before they interact with your network.

This proactive integration significantly strengthens the organization’s defensive posture against sophisticated cyber-financial threats.

Strategic data integration ensures that the automation engine never operates in a vacuum. This comprehensive visibility is the primary driver of both operational efficiency and long-term regulatory safety.

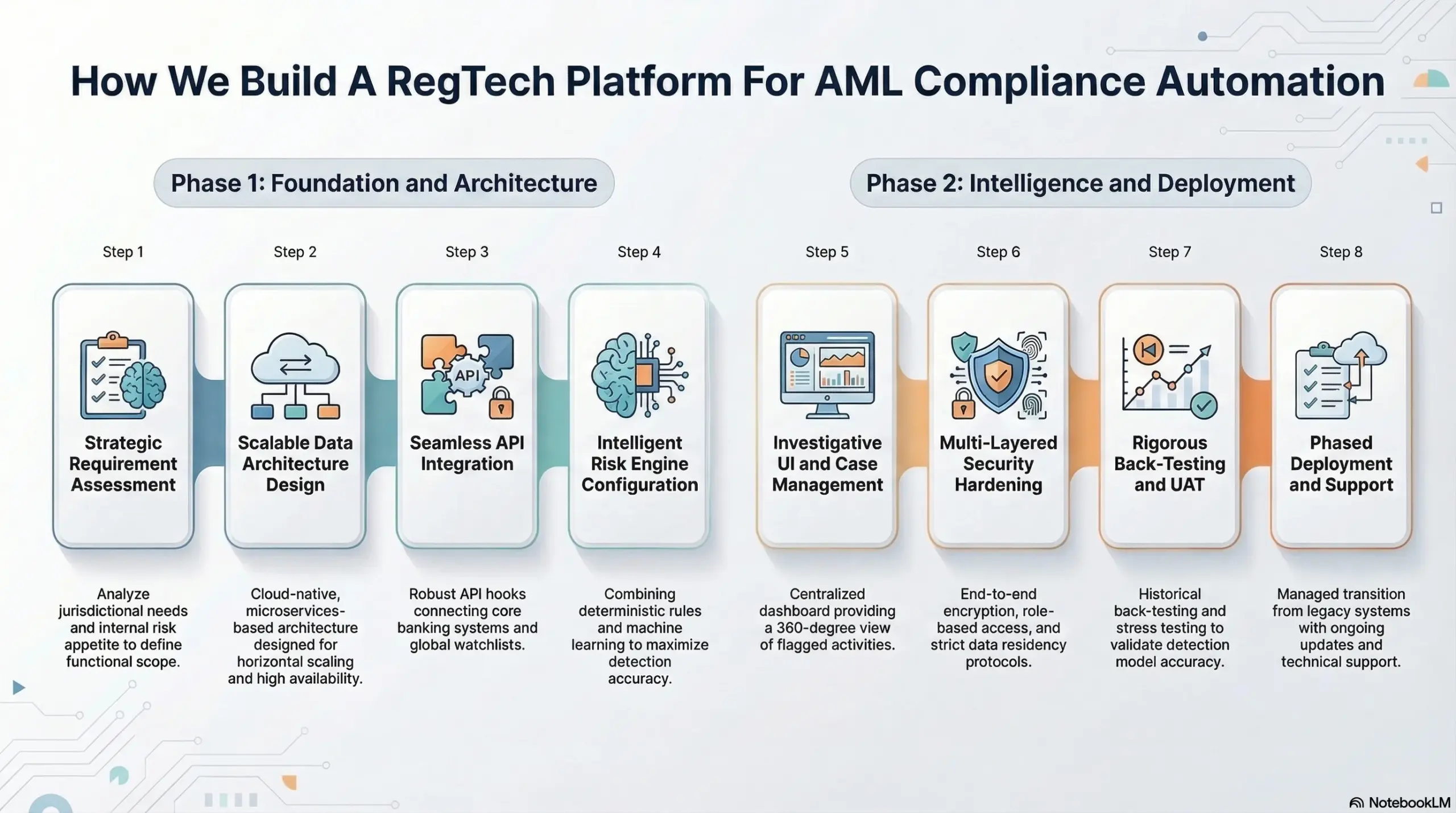

How We Build A RegTech Platform For AML Compliance Automation

Constructing a high-grade RegTech platform for AML compliance automation requires a systematic approach that bridges the gap between raw data and regulatory readiness.

At Intellivon, we follow a rigorous deployment lifecycle that prioritizes security, speed, and seamless integration with your existing core banking infrastructure. Consequently, the result is a custom-tailored ecosystem that evolves alongside your enterprise growth.

Step 1: Strategic Requirement Assessment

We begin by analyzing your specific jurisdictional needs and internal risk appetite to define the platform’s functional scope. Our team evaluates your current compliance gaps to ensure the new architecture addresses your most pressing operational challenges.

Therefore, this phase sets a clear roadmap for a solution that is both legally compliant and commercially viable.

Step 2: Scalable Data Architecture Design

Our engineers design a decoupled, microservices-based architecture that can handle millions of events with near-zero latency. We prioritize a cloud-native approach to ensure that your platform can scale horizontally as your transaction volumes increase globally.

This structural foundation prevents future bottlenecks and ensures high availability for critical real-time monitoring functions.

Step 3: Seamless API Integration

We build robust API hooks to connect the platform directly with your core banking systems, identity providers, and global watchlists. This ensures a continuous flow of high-fidelity data between your transaction ledgers and the automated screening engines.

Furthermore, our integration strategy minimizes disruption to your live environment while maximizing data throughput for the intelligence layer.

Step 4: Intelligent Risk Engine Configuration

Our data scientists configure the core intelligence engine using a combination of deterministic rules and advanced machine learning models.

We tune these algorithms to your specific customer base to maximize detection accuracy while minimizing the operational burden of false positives. Consequently, the system learns to recognize legitimate behavior patterns unique to your enterprise’s market segment.

Step 5: Investigative UI and Case Management

We develop a centralized dashboard that provides your compliance team with a high-density, 360-degree view of all flagged activities. This interface organizes complex data into intuitive narratives to help investigators make faster, more informed decisions during the review process.

Therefore, your staff can focus on high-risk cases without being bogged down by fragmented data silos.

Step 6: Multi-Layered Security Hardening

Security is baked into the development process through end-to-end encryption, role-based access controls, and regular vulnerability scanning.

We implement strict data residency and privacy protocols to ensure your platform remains compliant with international standards like GDPR or CCPA. This proactive hardening protects your sensitive customer data from unauthorized access or external cyber threats.

Step 7: Rigorous Back-Testing and UAT

Before going live, we subject the platform to extensive stress testing and historical back-testing to validate the accuracy of the detection models. Our team works closely with your stakeholders during User Acceptance Testing to ensure the workflows align with your internal compliance policies.

This ensures that the platform is fully optimized and ready for the pressures of a production environment.

Step 8: Phased Deployment and Support

We manage the rollout in phases to ensure a smooth transition from your legacy systems to the new automated infrastructure. Our team provides ongoing technical support and periodic model updates to keep your platform at the cutting edge of regulatory technology.

Consequently, your enterprise remains protected against both emerging financial crimes and evolving global mandates.

A structured, step-by-step methodology is the only way to ensure an enterprise-grade solution that stands up to regulatory scrutiny. This disciplined approach ultimately guarantees a seamless transition into the future of automated compliance.

Cost to Build an AML RegTech Compliance Platform

At Intellivon, AML RegTech platforms are built as enterprise compliance infrastructure, not as monitoring tools layered onto existing fintech systems. The goal is to create platforms that continuously monitor transactions, evaluate risk, and support regulatory reporting across financial operations.

However, AML compliance cannot be simplified without introducing regulatory risk. Monitoring engines, audit trails, governance controls, and reporting systems must operate reliably under high transaction volumes. As a result, enterprises avoid compliance failures, regulatory penalties, and costly remediation after launch.

Estimated Phase-Wise Cost Breakdown

| Phase | Description | Estimated Cost Range (USD) |

| Discovery & Regulatory Alignment | Compliance scope definition, AML obligations, jurisdiction mapping | $8,000 – $15,000 |

| Compliance Architecture Design | Risk engines, monitoring infrastructure, reporting framework | $12,000 – $20,000 |

| Governance & Policy Framework | Risk thresholds, alert policies, and approval workflows | $10,000 – $18,000 |

| Data & Financial Integrations | Payment systems, banking APIs, compliance data providers | $18,000 – $35,000 |

| Investigation & Compliance Interfaces | Case management dashboards, compliance analyst tools | $12,000 – $20,000 |

| Transaction Monitoring Engine | Behavioral monitoring logic, alert generation systems | $12,000 – $20,000 |

| Security & Compliance Controls | Encryption, access governance, and audit logging systems | $12,000 – $20,000 |

| Testing & Regulatory Validation | Monitoring accuracy testing, regulatory workflow validation | $8,000 – $14,000 |

| Deployment & Infrastructure Setup | Cloud infrastructure, monitoring tools, and performance optimization | $10,000 – $16,000 |

Total initial investment: $100,000 – $200,000

Ongoing maintenance and optimization:

Approximately 15–20% of the initial development cost per year.

Hidden Costs Enterprises Should Plan For

Even well-planned compliance platforms experience pressure when indirect costs are ignored.

- Integration complexity grows as payment systems, banking infrastructure, and external data providers expand.

- Compliance overhead increases due to regulatory updates, reporting changes, and audit requirements.

- Governance management requires continuous updates to monitoring rules, thresholds, and compliance workflows.

- Infrastructure costs rise as transaction volumes and analytics workloads increase.

- Operational training becomes necessary for compliance analysts, investigators, and risk teams.

- Monitoring expansion is required as fraud patterns and financial crime tactics evolve.

Best Practices to Avoid Budget Overruns

Based on Intellivon’s experience building enterprise fintech platforms, several practices help organizations control costs.

- Define the AML monitoring scope clearly before expanding regulatory coverage.

- Embed governance, auditability, and reporting controls directly into the platform architecture.

- Use modular infrastructure so monitoring engines and data integrations scale independently.

- Plan financial system integrations early to avoid costly retrofitting later.

- Maintain observability across transaction monitoring, compliance alerts, and reporting workflows.

- Design the platform to adapt to regulatory changes instead of relying on one-time certification.

Organizations planning to build an AML RegTech compliance platform can work with Intellivon’s fintech experts to define a delivery roadmap aligned with regulatory exposure, operational scale, and long-term compliance strategy.

Operational Challenges in AML Platform Development

Developing a RegTech platform for AML compliance automation introduces several friction points that can disrupt enterprise workflows if not managed proactively. These hurdles often stem from the tension between maintaining high-speed operations and meeting rigid regulatory demands.

Consequently, a successful implementation requires a strategy that balances technical performance with the precision of specialized AI.

1. Managing false positives at scale

High false-positive rates remain a primary source of operational noise that can overwhelm even the most sophisticated compliance teams. To mitigate this, platforms must utilize secondary identifiers like date of birth or geographic context during the matching process.

How We Solve It: Intellivon utilizes proprietary noise-reduction algorithms that filter out low-risk alerts before they reach your investigators. Our AI learns from your team’s past decisions to refine its matching precision over time. Consequently, your compliance officers spend their energy on high-value investigations rather than clearing repetitive, false alarms.

2. Handling large transaction datasets

Modern enterprises generate massive volumes of data that require sub-second processing to maintain a seamless user experience. The platform must utilize elastic cloud infrastructure and parallel processing to ensure that monitoring does not become a bottleneck.

How We Solve It: Our infrastructure leverages high-throughput event streaming to process millions of transactions with near-zero latency. Intellivon builds custom data pipelines that scale horizontally based on your real-time traffic demands. This ensures that your compliance checks never slow down the customer journey, even during peak global shopping periods.

3. Maintaining regulatory reporting accuracy

Regulatory bodies have zero tolerance for reporting errors, yet manual data entry is inherently prone to mistakes. An automated platform solves this by mapping internal data directly to jurisdictional templates like FinCEN’s XML formats.

How We Solve It: Intellivon automates the entire filing lifecycle by pre-populating regulatory forms with verified transaction data and investigation notes. Our system performs automated validation checks to ensure every field meets the technical requirements of the receiving agency. Therefore, your organization eliminates the risk of “failure-to-file” penalties caused by human oversight.

4. Ensuring explainable AI decisions

As machine learning takes a larger role in detection, regulators are increasingly demanding to know exactly why an algorithm flagged a specific transaction. The platform must avoid “black-box” models and instead provide clear reason codes for every automated decision.

How We Solve It: We implement “Explainable AI” (XAI) frameworks that provide human-readable justifications for every risk score generated. Intellivon ensures that your team can justify any automated action during a regulatory audit or internal review. This transparency transforms complex AI outputs into actionable insights that withstand the highest levels of legal scrutiny.

Solving these operational hurdles requires a partner who understands both the engineering and the ethics of financial technology. This technical resilience ultimately ensures that compliance remains a facilitator of growth rather than a barrier to entry

Conclusion

Building a RegTech platform for AML compliance automation is a strategic investment in long-term enterprise resilience. Modern automation transforms regulatory obligations from a cost center into a powerful engine for scalable growth.

By integrating advanced AI and robust data architectures, organizations protect their reputation while streamlining global operations. Consequently, the transition to automated oversight ensures your business remains competitive and compliant in an increasingly complex financial landscape.

Build a RegTech AML Compliance Platform With Intellivon

At Intellivon, RegTech platforms are engineered as enterprise compliance infrastructure, not as monitoring tools layered onto existing fintech systems. Each platform is designed to automate AML monitoring, risk analysis, and regulatory reporting across complex financial environments.

Every solution is built for regulated fintech ecosystems. RegTech platforms must process large transaction volumes, integrate with financial systems, and maintain regulatory accuracy through governed monitoring engines, audit trails, and compliance-ready infrastructure.

Why Partner With Intellivon?

- Governance-First Compliance Architecture: RegTech platforms are designed with embedded policy controls, investigation workflows, and role-based access governance to ensure regulatory accountability across compliance operations.

- AI-Driven AML Monitoring Systems: Our platforms include real-time transaction monitoring engines, behavioral analytics models, and automated alert generation to identify suspicious activity across financial networks.

- Integrated Risk and Investigation Workflows: Compliance teams can review alerts, document investigations, and manage suspicious activity cases through centralized case management systems.

- Provider-Agnostic Compliance Integrations: RegTech platforms integrate with banking systems, payment networks, sanctions databases, identity verification providers, and regulatory data sources.

- Compliance-Ready Reporting Infrastructure: AML reporting frameworks, audit logs, and investigation records are embedded directly into the platform to support regulatory transparency and documentation.

- Scalable Infrastructure for Fintech Growth: Architecture supports increasing transaction volumes, expanding regulatory requirements, and new financial integrations without compromising monitoring accuracy or operational performance.

Organizations exploring RegTech platform development for AML compliance automation can work with Intellivon’s fintech experts to design and deploy a secure, scalable, and compliance-ready system built for long-term regulatory operations.

FAQs

Q1. What is the primary purpose of a RegTech platform?

A1. A RegTech platform helps financial institutions manage regulatory compliance more efficiently. It automates monitoring, reporting, and risk analysis across financial operations. By using technologies such as AI, machine learning, and workflow automation, the platform reduces manual compliance work. As a result, organizations can meet regulatory requirements while operating at scale.

Q2. What features are important when building a RegTech platform?

A2. A strong RegTech platform should combine security, automation, and integration capabilities. First, it must protect sensitive compliance data through encryption and access controls. Second, the platform should integrate easily with banking systems, payment infrastructure, and compliance data providers. In addition, automated monitoring and reporting tools help organizations track regulatory risks and generate required reports.

Q3. How do RegTech platforms adapt to changing regulations?

A3. Financial regulations evolve frequently across different regions. RegTech platforms address this challenge by supporting configurable compliance workflows and monitoring rules. Compliance teams can update policies, risk thresholds, and reporting logic without rebuilding the system. This flexibility allows organizations to respond quickly to new regulatory requirements.

Q4. Why is data security critical in RegTech platforms?

A4. RegTech platforms process highly sensitive financial and compliance information. Therefore, strong data protection is essential. These systems typically use encryption, secure data storage, and strict access controls to protect information. In addition, audit logs track system activity and help organizations demonstrate accountability during regulatory reviews.

Q5. How do RegTech platforms support compliance reporting?

A5. Regulatory reporting is a key responsibility for financial institutions. RegTech platforms simplify this process by collecting investigation data, monitoring alerts, and case outcomes in one system. The platform can then generate the required reports automatically. As a result, organizations can maintain accurate documentation while reducing manual reporting work.