Enterprise leaders feel increasing pressure to deliver financial services faster, cheaper, and with much better control than traditional development cycles allow. This is because users want seamless payments, lending, insurance, and investment features in one experience, and they want it immediately.

Building that from the ground up is costly, slow, and risky for many organizations. That is why white-label fintech is becoming popular among businesses that want to move quickly without sacrificing quality, compliance, or brand ownership. The main question for most decision-makers is not whether to use a white-label fintech super app, but what it truly costs to do it properly and where the hidden costs are.

Intellivon has helped enterprise teams make this decision, guiding them to understand real platform costs, avoid costly architectural mistakes, and launch faster than their competitors anticipated. This blog outlines every important cost factor, allowing your team to plan, budget, and build with clarity.

Why Enterprises Are Building Fintech Super Apps

Enterprises build fintech super apps to consolidate services into a single ecosystem, which significantly enhances user retention and data ownership.

This strategic move allows for personalized financial experiences while reducing the high costs associated with custom, ground-up development.

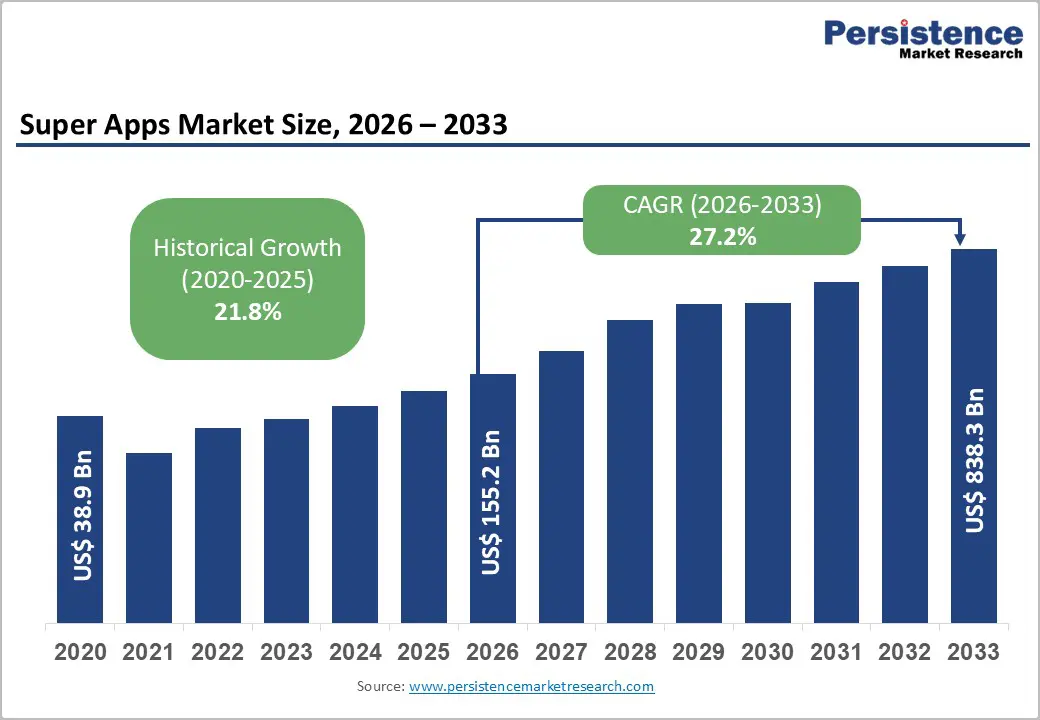

The global super apps market is expected to reach $155.2 billion in 2026. It is projected to grow significantly and reach $838.3 billion by 2033, expanding at a 27.2% CAGR between 2026 and 2033.

This growth is driven by the rapid convergence of digital payments, embedded finance, mobility platforms, and platform-based commerce into unified digital ecosystems.

Modern organizations now seek to own the entire financial lifecycle of their users to prevent fragmented data. By centralizing services, these firms reduce operational silos and capture higher lifetime value from every customer interaction.

1. Financial Services Consolidation

Traditional banking requires jumping between apps for payments, lending, or investments, which creates friction. A unified platform eliminates this hurdle, positioning the enterprise as the primary touchpoint for a user’s daily economic life.

Consequently, businesses gain a holistic view of consumer behavior. This visibility allows for better-timed product offers based on the full financial context. Therefore, the brand becomes an indispensable utility rather than a secondary tool.

2. Super Apps Increase Customer Engagement

Sticky ecosystems thrive because they offer immediate convenience through integrated rewards and seamless workflows. When users can pay bills and apply for credit in one place, they return more frequently.

This high-frequency interaction generates rich behavioral data for future strategies. Moreover, the proximity of services encourages cross-selling that feels helpful rather than intrusive. Engagement levels skyrocket when an app becomes a daily necessity for the user.

3. Why Choose White-Label Fintech Apps

Building a core financial engine from scratch requires immense capital and years of development. Most leaders choose white-label fintech solutions because they provide a battle-tested foundation ready for immediate deployment.

This allows internal teams to focus on branding instead of complex ledger mechanics. Additionally, these platforms typically include built-in compliance frameworks and security protocols. As a result, the time-to-market is drastically reduced.

4. Market growth of fintech super app ecosystems

The global appetite for all-in-one hubs is expanding as mobile-first generations become the primary economic drivers. Market data indicates a clear preference for integrated experiences over single-purpose applications.

Because of this, massive capital is flowing into regional super apps that cater to specific cultural needs. Furthermore, open banking regulations have lowered entry barriers for non-financial corporations. This expansion suggests that the super app model will soon be the standard for digital commerce.

Adopting this integrated model ensures enterprises remain relevant in an increasingly competitive digital landscape. This strategy provides a clear path to market leadership and sustained revenue growth.

What Is a White-Label Fintech Super App?

A white-label fintech super app is a pre-built, customizable mobile platform that allows enterprises to offer multiple financial services under their own brand.

Instead of building from scratch, companies license this sophisticated infrastructure to provide payments, lending, insurance, and investments within one ecosystem.

This turnkey solution integrates seamlessly with existing workflows. Consequently, it enables rapid market entry while ensuring enterprise-grade security and full regulatory compliance.

Difference Between Fintech Apps and Super Apps

Fintech apps and super apps both deliver digital financial services, but their scope is very different. A fintech app usually focuses on one financial product, such as payments, lending, or investing.

In contrast, a super app combines multiple financial and lifestyle services within a single platform. Understanding this difference is important for enterprises planning large digital ecosystems.

Fintech Apps vs Super Apps

| Aspect | Fintech Apps | Super Apps |

| Core Purpose | Provide a single financial service such as payments, lending, or investments. | Combine multiple financial and non-financial services in one platform. |

| Product Scope | Focused on one or two financial functions. | Integrates payments, lending, commerce, mobility, and other services. |

| User Experience | Users switch between different apps for different services. | Users access many services within one unified application. |

| Platform Complexity | Simpler architecture with limited integrations. | Complex architecture that connects multiple services and ecosystems. |

| Revenue Streams | Revenue typically comes from one financial product. | Revenue comes from multiple services across a digital ecosystem. |

| Ecosystem Role | Operates as a standalone financial product. | Operates as a digital ecosystem connecting many services and partners. |

Fintech apps solve specific financial problems through focused products. Super apps take a broader approach by integrating many services into a single platform.

For enterprises building digital ecosystems, super apps create stronger engagement because users can access multiple services without leaving the platform.

How White-Label Fintech Platforms Operate

White-label fintech platforms operate through a model where technology infrastructure and customer branding are separated. The platform provider manages the financial system, while the enterprise delivers the services under its own brand.

1. Enterprise Licenses the Platform

The enterprise adopts a ready-built fintech platform that already includes core financial capabilities such as payments, wallets, lending, or investments.

2. Platform Branded for the Enterprise

The interface is customized with the enterprise’s logo, colors, and user experience. Customers interact only with the enterprise brand.

3. Financial Services are Activated

The enterprise enables specific services such as payments, credit, insurance, or investments, depending on its business model.

4. Customers use the Enterprise App

End users access financial services through the enterprise’s branded application, which appears as the company’s own product.

5. Infrastructure Processes Transactions

The platform’s backend handles payments, credit decisions, compliance checks, and transaction records in the background.

6. Provider Maintains the Platform

The infrastructure provider manages system reliability, security, updates, and integrations with financial networks.

White-label fintech platforms allow enterprises to launch financial services under their own brand while relying on specialized infrastructure providers to operate the technology behind the scenes.

Core Modules That Influence Super App Development Cost

Development costs for fintech super apps are driven by modular complexity, including high-stakes components like digital wallets, KYC engines, and lending modules. Integrating these diverse financial services into a single architecture requires sophisticated middleware and robust security frameworks to ensure seamless interoperability.

The total investment for a fintech ecosystem depends heavily on the complexity of its underlying functional blocks. Each module requires specific API integrations, security protocols, and compliance logic that dictate the final development timeline.

1. Digital wallet and payment infrastructure

The digital wallet serves as the central nervous system for any super app. It handles fund storage, peer-to-peer transfers, and bill payments through secure gateway integrations.

Developing this requires high-grade encryption and real-time transaction processing capabilities. Furthermore, adding support for multiple currencies or cross-border remittances increases the technical overhead.

Therefore, this module often represents the largest portion of the initial core investment.

2. Lending and credit services module

Integrating credit features adds layers of complexity regarding risk assessment and automated underwriting. This module must connect to credit bureaus and employment verification systems to evaluate borrower profiles instantly.

In addition, developers must build flexible repayment schedules and automated collection workflows. Because lending involves high regulatory scrutiny, the cost includes rigorous testing for interest rate calculations.

Consequently, businesses should prioritize a scalable credit engine that grows with their user base.

3. Investment and wealth management module

Wealth management tools allow users to trade stocks, ETFs, or mutual funds directly within the interface. Building this requires low-latency connections to brokerage houses and real-time market data feeds.

Developers must also implement portfolio tracking and automated rebalancing logic for a premium user experience. Moreover, the UI must simplify complex financial data into digestible charts for non-professional investors.

As a result, the cost reflects the need for both back-end precision and front-end clarity.

3. Insurance and protection services module

Embedding insurance allows the enterprise to offer “point-of-sale” protection for travel, health, or electronics. This module necessitates a robust claims management system and a seamless policy issuance engine.

It often involves complex partnerships with third-party underwriters through specialized APIs. Additionally, the app must handle premium renewals and document storage securely.

Therefore, the development focus remains on creating a friction-free bridge between the user and the insurance provider.

4. User identity and KYC infrastructure

Security starts with a foolproof “Know Your Customer” (KYC) and identity verification process. This infrastructure must include biometric scanning, document OCR, and anti-money laundering (AML) screening.

Automated verification speeds up user onboarding while reducing the risk of fraudulent accounts. Furthermore, the system must adhere to global data privacy standards like GDPR or CCPA.

Investing in a high-quality KYC module prevents future legal liabilities and builds immediate user trust.

5. Merchant and partner ecosystem module

A true super app thrives on its ability to host third-party merchants and service providers. This module requires a dedicated portal for partners to manage their offerings and view transaction analytics.

It also involves building a standardized SDK or API set that allows external vendors to plug into the ecosystem.

In addition, a centralized settlement system ensures that all parties are paid accurately and on time. Consequently, this creates a scalable marketplace that drives long-term platform value.

Each module adds specific value but also introduces unique technical challenges that influence the budget. Selecting the right combination of these features ensures the platform meets current market needs while remaining cost-effective.

Major Cost Drivers in Fintech Super App Development

Fintech super app costs are driven by architectural complexity, regulatory compliance, and multi-service integration. Engineering focus centers on microservices and security layers like PCI DSS to protect enterprise-grade data and ensure 99.9% uptime for global users.

Strategic budgeting requires understanding that most investment flows into the invisible infrastructure. High-performance systems demand robust backends that ensure stability under massive transaction loads and peak usage periods.

Key Cost Drivers in Fintech Super App Development

| Cost Driver | Why It Increases Development Cost | Impact on Platform Development |

| Number of Financial Services | Each service, such as lending, insurance, or investments, requires its own business logic, rules, and workflows. | Expands engineering scope and increases system complexity across multiple financial products. |

| Platform Architecture Complexity | Super apps often rely on microservices to ensure stability and modular scalability. | Requires advanced backend engineering, DevOps expertise, and sophisticated cloud infrastructure. |

| Security and Regulatory Compliance | Fintech platforms must comply with standards such as PCI DSS, GDPR, and financial regulations. | Adds costs for encryption systems, fraud monitoring tools, and ongoing compliance audits. |

| Third-Party Financial Integrations | Platforms integrate with payment processors, credit bureaus, and identity verification services. | Integration development, testing, and ongoing API maintenance increase operational expenses. |

| User Experience and Interface Design | A super app must keep a simple interface while supporting many services. | Requires extensive UX design, testing cycles, and consistent mobile experiences across platforms. |

1. Number of Financial Services Integrated

Each new service, such as lending or insurance, multiplies the development effort significantly. You are building entire logic layers and business rules for every unique product added. Every vertical requires specific calculation engines and edge-case handling.

Consequently, a multi-service platform costs more than a simple wallet. Therefore, enterprises must prioritize modules that offer the highest immediate ROI.

2. Platform Architecture Complexity

High-performance apps rely on microservices to ensure one module’s failure doesn’t crash the entire system. This approach increases initial setup costs but provides vital flexibility for long-term growth.

Furthermore, the infrastructure must support real-time data synchronization across different geographical regions.

This complexity demands senior DevOps expertise and robust cloud orchestration. As a result, the backend engine often becomes the most expensive budget item.

3. Regulatory Compliance Requirements

Fintech platforms operate under extreme scrutiny, making security a non-negotiable and recurring expense. You must account for data encryption, multi-factor authentication, and continuous fraud monitoring.

Additionally, compliance with standards like PCI DSS and GDPR requires specialized technical audits. Skipping these steps leads to catastrophic fines and lost user trust. Consequently, security is a foundational investment rather than an optional feature.

4. Third-party Financial Service Integrations

Most enterprises rely on a web of third-party APIs for credit bureaus and payment gateways. Integrating these involves complex data mapping and rigorous testing to ensure seamless data flow.

Each integration requires extensive maintenance to handle external updates or downtime. Moreover, these providers often charge per-transaction fees that impact operational budgets. Therefore, managing these technical partnerships is a significant cost driver.

5. User Experience and Mobile Interface Complexity

The interface must remain clean despite the massive amount of underlying functionality. Designing a journey from a payment screen to an investment dashboard is a high-level UX challenge.

This requires multiple rounds of prototyping and usability testing to ensure simplicity. In addition, supporting both iOS and Android consistently adds to the design overhead. Ultimately, a superior experience determines if the app is adopted or ignored.

Understanding these drivers allows leaders to allocate capital for maximum impact. Balancing feature richness with infrastructure stability is the key to a sustainable fintech strategy.

Estimated Cost to Build a Fintech Super App

Fintech super app development costs depend on platform scope, infrastructure design, and the number of financial services offered. Enterprises often begin with a focused MVP and expand the ecosystem gradually.

The table below shows the typical cost ranges for different development stages.

Fintech Super App Development Cost Comparison

| Platform Stage | Typical Features | Development Complexity | Estimated Cost |

| MVP Fintech Super App | User onboarding, digital wallet, payments, basic dashboard | Low to moderate complexity | $60,000 – $100,000 |

| Mid-Scale Fintech Super App | Payments, lending modules, investment tools, and stronger APIs | Moderate complexity with multiple services | $100,000 – $180,000 |

| Full Financial Ecosystem Platform | Payments, lending, insurance, investments, partner marketplace | High complexity with enterprise infrastructure | $180,000 – $300,000 |

| Infrastructure & Cloud Deployment | Hosting, databases, monitoring systems, security layers | Ongoing infrastructure scaling | $15,000 – $60,000 annually |

| Maintenance & Operations | Updates, bug fixes, compliance monitoring, performance tuning | Continuous operational support | $20,000 – $70,000 annually |

Understanding these stages helps enterprises plan development budgets more effectively. Most organizations launch with a focused platform and scale services as the ecosystem grows.

Fintech Super App Development Cost Breakdown

The total cost of building a fintech super app comes from several technical components. Each layer of the platform requires specialized engineering, infrastructure, and compliance systems.

Fintech Super App Development Cost Breakdown

| Development Component | Estimated Cost |

| Product Design and UX Research | $8,000 – $20,000 |

| Mobile App Development (iOS and Android) | $20,000 – $80,000 |

| Backend Infrastructure Development | $15,000 – $70,000 |

| Payment and Financial Integrations | $8,000 – $35,000 |

| Security and Compliance Systems | $5,000 – $25,000 |

| Testing and Quality Assurance | $4,000 – $20,000 |

| Total Estimated Cost | $60,000 – $300,000 |

This breakdown highlights how costs are distributed across design, engineering, infrastructure, and compliance. Enterprises that prioritize essential modules first can control budgets while building a scalable fintech ecosystem.

Technology Decisions That Affect Development Cost

Technology choices directly influence the cost of building a fintech super app. Some architectures require more engineering effort at the beginning, but reduce long-term operational costs. Others allow faster development but may limit scalability later.

Enterprises must balance speed, flexibility, and long-term platform stability when selecting the right technology stack.

1. Native vs Cross-Platform Mobile Development

Mobile development strategy significantly affects the overall development budget. Enterprises must decide whether to build native applications for each platform or use cross-platform frameworks that share code across devices.

Native development creates separate apps for iOS and Android. This approach offers strong performance and better integration with device features. However, it increases development time and engineering costs.

Cross-platform development uses a single codebase to build apps for multiple platforms. This approach reduces development costs and accelerates launch timelines. However, performance and customization may sometimes be limited compared to native applications.

Native vs Cross-Platform Development Comparison

| Factor | Native Development | Cross-Platform Development |

| Development Cost | Higher due to separate iOS and Android development | Lower due to shared codebase |

| Performance | Optimized performance and smoother user experience | Slightly lower performance in complex apps |

| Development Time | Longer development cycle | Faster development and deployment |

| Maintenance | Requires updates for each platform separately | Single codebase simplifies maintenance |

| Best Use Case | High-performance apps with complex features | Faster launch for multi-platform apps |

2. Microservices vs Monolithic Architecture

Platform architecture determines how the system handles growth and complexity. Fintech super apps often manage multiple services such as payments, lending, and investments. The architectural approach affects both development cost and system flexibility.

Monolithic architecture builds the entire platform as a single unified application. This structure is simpler to develop at the beginning. However, it becomes harder to scale as more services are added.

Microservices architecture divides the platform into independent services. Each service operates separately and communicates through APIs. This design increases initial engineering effort but improves scalability and reliability.

Microservices vs Monolithic Architecture Comparison

| Factor | Monolithic Architecture | Microservices Architecture |

| Development Cost | Lower initial development cost | Higher upfront engineering investment |

| Scalability | Limited scalability as the platform grows | High scalability with independent services |

| System Reliability | One failure can affect the entire system | Failures remain isolated to specific services |

| Development Speed | Faster early development | Slower initial setup but faster feature expansion |

| Best Use Case | Small platforms with limited services | Complex platforms with multiple financial modules |

3. Cloud-Native vs Hybrid Infrastructure

Infrastructure decisions influence both development costs and long-term operational expenses. Fintech platforms must support high transaction volumes and maintain reliable uptime.

Cloud-native infrastructure runs entirely on cloud platforms. This approach enables automatic scaling and reduces the need for physical infrastructure management.

Hybrid infrastructure combines cloud services with on-premise systems. Some enterprises choose this model to maintain control over sensitive financial data or meet regulatory requirements.

Cloud-Native vs Hybrid Infrastructure Comparison

| Factor | Cloud-Native Infrastructure | Hybrid Infrastructure |

| Setup Cost | Lower initial infrastructure investment | Higher setup cost due to mixed environments |

| Scalability | Automatic scaling through cloud resources | Scaling requires coordination across systems |

| Maintenance | Managed cloud services reduce operational effort | Requires internal infrastructure management |

| Compliance Flexibility | Suitable for global fintech platforms | Useful for regulated financial institutions |

| Best Use Case | Rapidly growing fintech platforms | Enterprises with strict regulatory requirements |

-

API-First Financial Service Architecture

Fintech super apps rely heavily on integrations with external financial systems. An API-first architecture designs the platform so that every service communicates through standardized APIs.

This approach simplifies integration with payment networks, banking systems, and financial data providers. It also allows enterprises to add new services without rebuilding the entire platform.

Although API-first design requires careful planning and engineering, it improves long-term flexibility and scalability.

API-First vs Traditional Integration Comparison

| Factor | Traditional Integration | API-First Architecture |

| Integration Flexibility | Limited integration options | Highly flexible integrations |

| Development Speed | Slower when adding new services | Faster service expansion |

| Platform Scalability | Difficult to expand integrations | Easy to integrate new partners |

| Maintenance | Changes often require system updates | APIs allow modular updates |

| Best Use Case | Smaller platforms with few integrations | Multi-service fintech ecosystems |

5. Data Infrastructure for Financial Analytics

Data infrastructure enables fintech platforms to process financial transactions, analyze user behavior, and monitor risks. Super apps generate large volumes of financial data across multiple services.

Basic data systems store transaction records and user activity logs. However, advanced fintech platforms require real-time analytics, fraud detection systems, and predictive financial insights.

Building a strong data infrastructure increases development costs but provides valuable insights for risk management and customer personalization.

Basic Data Systems vs Advanced Financial Data Infrastructure

| Factor | Basic Data Infrastructure | Advanced Financial Data Infrastructure |

| Data Processing | Stores transaction records | Processes data in real time |

| Analytics Capability | Limited reporting features | Advanced analytics and insights |

| Fraud Detection | Basic monitoring tools | AI-driven fraud detection systems |

| Infrastructure Cost | Lower infrastructure cost | Higher infrastructure investment |

| Best Use Case | Early-stage fintech platforms | Large-scale financial ecosystems |

Technology decisions play a major role in determining development costs. Choices around architecture, infrastructure, and data systems affect both the initial investment and long-term scalability. Enterprises that prioritize scalable architecture early can reduce future platform redesign costs.

Third-Party Integrations That Increase Development Cost

Third-party integrations typically account for 25-40% of a fintech super app’s budget. Key cost drivers include BaaS infrastructure, KYC automation, and specialized credit data feeds.

In 2026, enterprises prioritize API-first providers that offer pre-certified compliance layers to reduce long-term auditing expenses and speed up regional deployments.

1. Banking infrastructure and payment processors

Connecting to the global financial grid requires robust Banking-as-a-Service (BaaS) and payment gateway integrations. Providers like Stripe or Adyen handle fund movement and settlement processes.

Setting up these secure handshakes involves backend engineering to manage webhooks and transaction status syncing. Most processors charge a mix of monthly platform fees and per-transaction commissions.

Consequently, the cost reflects the need for high-availability connections that ensure every payment is processed successfully.

2. Credit bureaus and financial data providers

To offer lending or personalized advice, your app must pull data from bureaus like Equifax or Experian. Integrating these APIs allows for real-time credit scoring and financial health monitoring for your users.

Each data pull incurs a fee, and the initial integration requires strict data mapping to ensure accuracy. Additionally, developers must build secure vaults to store sensitive information in compliance with local laws.

Therefore, these integrations are vital for apps aiming to offer sophisticated credit products.

3. Identity verification and KYC providers

Onboarding users securely is a legal mandate requiring integration with specialized identity verification services. These providers use AI to verify passports, scan biometrics, and check global watchlists for AML compliance.

Costs vary based on whether you require manual review backups or fully automated instant approvals. Maintaining these digital gates involves recurring costs per new user verified.

Investing in a top-tier KYC provider reduces fraud and ensures your enterprise remains compliant with regulators.

4. Investment and wealth management integrations

Allowing users to trade stocks requires a bridge to brokerage houses and market data aggregators. These integrations are technically demanding due to low-latency data feeds and complex order-routing logic.

You must ensure that fractional shares and dividends are tracked with absolute precision in the ledger. Moreover, these partners often require their own compliance audits before allowing a third-party app to connect.

As a result, wealth management features often sit in the higher tier of development costs.

5. Insurance provider integrations

Embedding insurance involves connecting your app to an underwriter’s policy management system. This allows for instant quote generation and digital policy issuance directly within your interface.

The technical challenge lies in syncing claims data and premium schedules across two different enterprise systems. You may also need custom workflows for specific insurance types, such as travel or health protection.

While these integrations offer lucrative revenue streams, they require thoughtful and well-tested technical implementation.

Strategic selection of these partners ensures your super app provides a comprehensive experience without ballooning the budget. Focusing on high-impact integrations first allows enterprises to manage capital while building a foundation for growth.

Deployment Models and Their Cost Impact On Building Fintech Super Apps

Deployment strategy plays a major role in the total cost of a fintech super app. The infrastructure model determines how the platform handles security, scalability, and regulatory compliance.

Some deployment models reduce upfront infrastructure costs but increase long-term operational expenses. Others require a higher initial investment but offer stronger control over sensitive financial data.

Enterprises must select a deployment strategy that balances cost, performance, and regulatory requirements.

1. Cloud-Based Fintech Super App Deployment

Cloud deployment is the most common infrastructure model for fintech platforms. The entire application runs on cloud environments managed by providers such as AWS, Azure, or Google Cloud.

This model reduces the need for physical infrastructure and allows platforms to scale automatically as user activity grows. As a result, many fintech startups and digital platforms prefer cloud-based deployment.

However, long-term costs can increase as the platform grows and processes larger transaction volumes.

Cloud-Based vs Traditional Infrastructure Comparison

| Factor | Cloud-Based Deployment | Traditional Infrastructure |

| Initial Setup Cost | Lower upfront infrastructure investment | High hardware and infrastructure costs |

| Scalability | Automatic scaling based on demand | Scaling requires additional hardware |

| Deployment Speed | Faster deployment and updates | Slower deployment cycles |

| Maintenance | Managed by a cloud provider | Managed internally by the organization |

| Best Use Case | Rapidly growing fintech platforms | Organizations with fixed infrastructure |

2. Hybrid Infrastructure for Financial Institutions

Hybrid infrastructure combines cloud environments with on-premise systems. Sensitive financial data or core systems remain within internal servers, while customer-facing services run on the cloud.

This model helps financial institutions meet regulatory requirements while still benefiting from cloud scalability. Many large banks adopt hybrid systems to maintain control over sensitive operations.

However, managing two infrastructure environments increases engineering complexity and operational costs.

Hybrid vs Cloud Infrastructure Comparison

| Factor | Hybrid Infrastructure | Cloud-Only Infrastructure |

| Data Control | Sensitive data stored internally | Data managed within cloud systems |

| Infrastructure Cost | Higher due to dual environments | Lower infrastructure complexity |

| Scalability | Moderate scalability | High scalability |

| Compliance Flexibility | Easier to meet regulatory requirements | Depends on the regulatory framework |

| Best Use Case | Banks and regulated institutions | Digital fintech platforms |

3. On-Premise Deployment for Regulated Enterprises

On-premise deployment hosts the entire platform within the internal enterprise infrastructure. Organizations maintain full control over servers, networks, and data storage.

This approach is often used by highly regulated financial institutions that must comply with strict data residency or security rules. It provides strong control over sensitive financial systems.

However, on-premise deployment requires significant investment in infrastructure, maintenance, and technical teams.

On-Premise vs Cloud Deployment Comparison

| Factor | On-Premise Deployment | Cloud Deployment |

| Infrastructure Control | Full control over systems and data | Managed by cloud providers |

| Setup Cost | High initial infrastructure investment | Lower upfront cost |

| Maintenance | Requires internal IT teams | Managed cloud services |

| Scalability | Limited scalability | Flexible and scalable |

| Best Use Case | Highly regulated enterprises | Modern fintech platforms |

4. Multi-Region Deployment for Global Fintech Platforms

Fintech super apps operating across multiple countries often require multi-region infrastructure. This model distributes servers across different geographic regions to support local users.

Multi-region deployment improves performance and reduces latency for global users. It also helps platforms comply with regional data protection laws.

However, maintaining infrastructure across multiple regions increases operational complexity and cloud costs.

Single-Region vs Multi-Region Deployment Comparison

| Factor | Single-Region Deployment | Multi-Region Deployment |

| Infrastructure Cost | Lower infrastructure cost | Higher infrastructure expenses |

| Platform Performance | Slower response times for distant users | Faster global performance |

| Compliance | Limited support for regional data rules | Easier compliance with regional laws |

| Operational Complexity | Easier to manage infrastructure | More complex infrastructure management |

| Best Use Case | Regional fintech platforms | Global financial ecosystems |

Deployment strategy significantly affects both development cost and long-term platform operations. Cloud infrastructure offers flexibility and faster deployment, while hybrid and on-premise models provide stronger control over financial data.

Enterprises expanding globally often adopt multi-region infrastructure to support performance and regulatory compliance across markets.

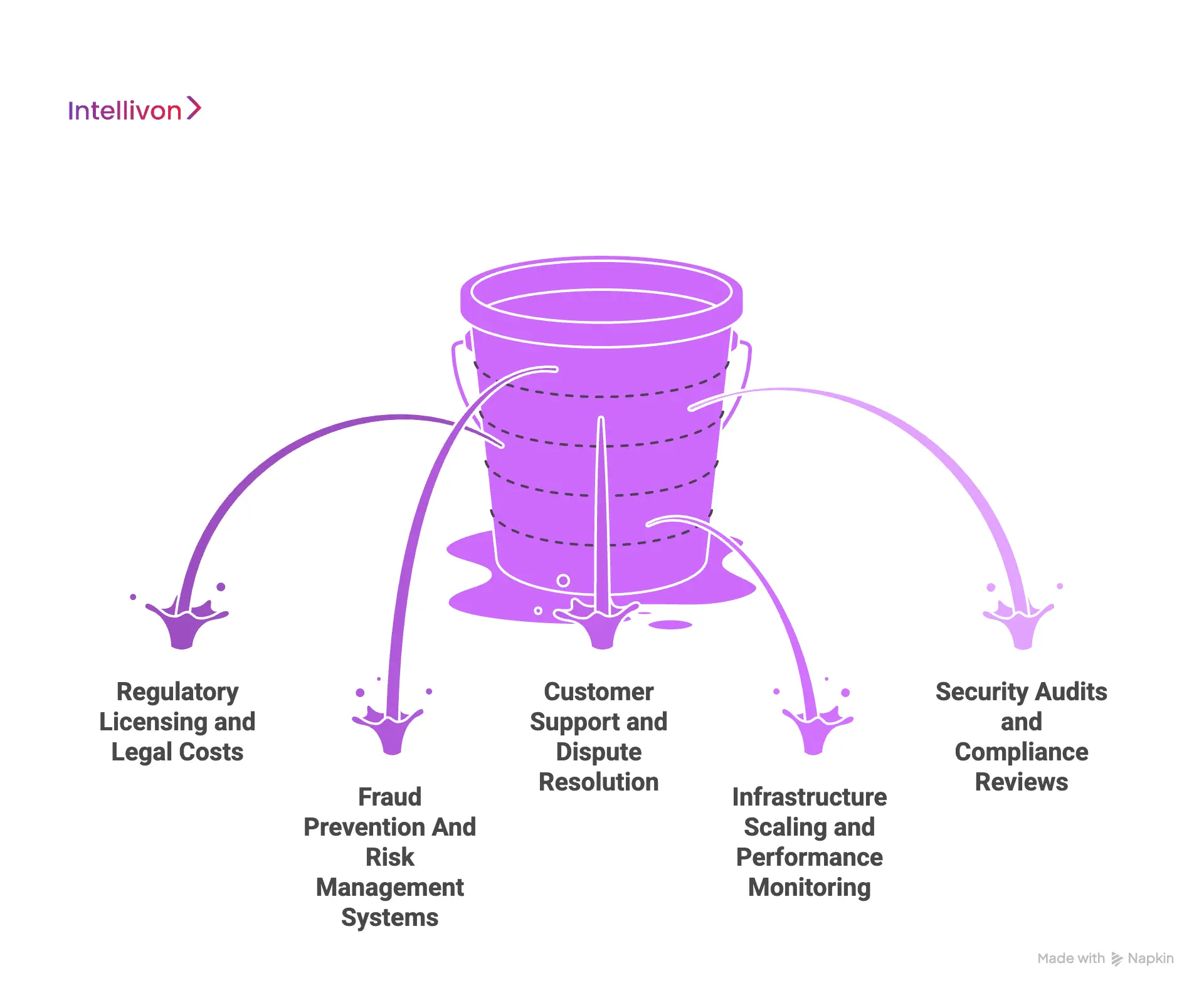

Hidden Costs of Building a Fintech Super App

Hidden costs in fintech development frequently stem from regulatory licensing and advanced fraud detection.

For an enterprise super app, these non-development expenses can account for 20% to 30% of the total cost of ownership, ensuring the platform remains resilient against financial crime.

1. Regulatory licensing and legal costs

Operating a financial platform requires specific licenses that vary by jurisdiction. Obtaining these permits involves significant application fees and months of specialized legal work.

You must hire experts to draft user agreements that withstand local scrutiny. Therefore, navigating the regulatory landscape is often the most time-consuming hidden expense.

2. Fraud prevention and risk management systems

As transaction volume grows, your platform becomes a target for sophisticated financial criminals. You need AI-driven fraud detection systems that analyze behavior in real-time to flag suspicious activities.

In addition, you must account for the cost of a specialized risk team to review these alerts. Consequently, investing in robust prevention tools is far cheaper than the cost of a major breach.

3. Customer Support and Dispute Resolution

Financial services demand a 24/7 support infrastructure, including secure chat systems and trained human agents. You also need a formal process for handling chargebacks and transaction disputes to comply with banking regulations.

Moreover, a slow response to a financial issue can permanently destroy user trust. As a result, operationalizing support is a significant recurring expense.

4. Infrastructure Scaling and Performance Monitoring

An enterprise-grade app must remain functional during sudden traffic spikes. Scaling infrastructure requires advanced monitoring tools and automated server management to ensure zero latency.

Furthermore, you must budget for the engineering time needed to optimize code as the user base grows. Therefore, maintaining a high-performance environment is a continuous financial commitment.

5. Security Audits and Compliance Reviews

To maintain licenses, you must undergo regular third-party security audits like SOC2 or PCI DSS certifications. These reviews involve deep technical inspections of your code and internal processes.

In addition, internal compliance officers must regularly review data handling practices. Consequently, these recurring audits serve as a necessary “tax” to prove your platform’s integrity.

Identifying these hidden costs early allows leadership to build a more realistic financial model. Proactive planning for legal and security requirements prevents expensive pivots and ensures long-term operational stability.

Cost Optimization Strategies for Super App Development

To optimize fintech development costs, enterprises should prioritize modular architectures and API-first designs.

Utilizing white-label modules can reduce initial R&D expenses by up to 60%, while a staggered rollout of features allows for self-funding growth through immediate transaction revenue.

1. Modular financial service architecture

A modular approach allows you to develop, deploy, and update specific features without affecting the entire system. Instead of a monolithic codebase, each financial service operates as an independent unit.

This isolation simplifies the testing process and reduces the time required for bug fixes. Furthermore, it allows you to scale specific high-traffic modules independently to save on cloud costs.

Therefore, modularity acts as a safeguard against expensive system-wide failures.

2. API-first infrastructure approach

An API-first strategy ensures that every component of your super app can communicate seamlessly with internal and external services. This standardized connectivity reduces the complexity of adding new third-party partners later.

Moreover, it allows your internal teams to build new front-end experiences without rebuilding the core backend logic. In addition, well-documented APIs make it easier for future developers to maintain the platform.

Consequently, this approach dramatically lowers long-term integration and maintenance costs.

3. Gradual rollout of financial services

Launching all services at once increases risk and puts immense strain on your initial budget. Instead, start with a core utility, like a digital wallet, and add services based on actual user demand.

This phased approach allows you to use revenue from the first module to fund the development of the next. Additionally, you can refine your user experience based on real-world feedback before scaling.

As a result, you avoid investing in features that your users might not actually need.

4. White-label fintech modules

Leveraging white-label modules allows you to skip the expensive R&D phase for standard financial utilities. Components like ledger management, KYC engines, and payment gateways are already battle-tested and compliant.

By licensing these building blocks, you can redirect your budget toward unique features that differentiate your brand. Furthermore, white-label solutions often come with ongoing security updates included in the license.

Therefore, this choice provides a faster, safer, and more cost-effective route to market.

5. Automated compliance and monitoring

Manual compliance checks are slow, prone to error, and require a large headcount. Integrating automated monitoring tools allows for real-time tracking of transactions and regulatory reporting.

These systems instantly flag suspicious activity, reducing the need for constant manual oversight. Moreover, automation ensures that your platform remains compliant with evolving laws without requiring a massive legal team.

Consequently, the initial investment in automation pays for itself by lowering long-term operational overhead.

By implementing these strategies, enterprises can build a sophisticated financial ecosystem that remains financially sustainable. Balancing custom innovation with proven infrastructure is the most efficient way to achieve long-term platform growth

Conclusion

Building a fintech super app is a strategic investment in long-term customer ownership. By choosing a modular, white-label approach, enterprises can balance sophisticated functionality with controlled development costs. This path ensures rapid market entry without compromising security.

Consequently, your organization gains a scalable, future-proof ecosystem. To build a cutting-edge, AI-powered financial solution, partner with Intellivon. We provide the expertise to transform your vision into a dominant market reality.

Build a White-Label Fintech Super App With Intellivon

At Intellivon, fintech super apps are engineered as financial ecosystem platforms, not as standalone mobile applications. Each platform is designed to integrate multiple financial services such as payments, lending, investments, and insurance within a unified digital environment.

Every solution is built for enterprise-scale financial operations. Super apps must support high transaction volumes, manage complex service integrations, and maintain strong governance across financial workflows. Our platforms are designed to deliver stability, security, and scalability across global fintech ecosystems.

Why Partner With Intellivon?

- Governance-First Super App Architecture: Platforms are designed with embedded policy controls, role-based access frameworks, and financial governance systems to maintain operational oversight across services.

- Multi-Service Financial Infrastructure: Our super apps support payments, wallets, lending, investments, insurance, and partner services within a unified platform architecture.

- AI-Driven Financial Intelligence Systems: We integrate advanced analytics and AI models to support fraud detection, financial insights, and personalized user experiences across the ecosystem.

- Provider-Agnostic Financial Integrations: Super apps integrate with payment gateways, banking APIs, credit bureaus, identity verification providers, and financial data sources without vendor lock-in.

- Scalable Architecture for Financial Ecosystems: The infrastructure supports growing user bases, expanding partner networks, and increasing transaction volumes while maintaining system performance.

- Secure Infrastructure for Regulated Environments: Platforms are built with strong encryption, authentication frameworks, and compliance-ready systems aligned with financial security standards.

Organizations exploring white-label fintech super app development can work with Intellivon’s fintech specialists to design and deploy a secure, scalable, and ecosystem-ready financial platform built for modern digital finance.

FAQs

Q1. How much does it cost to build a fintech super app?

A1. The cost of building a fintech super app usually ranges between $60,000 and $300,000. The final cost depends on the number of financial services included, platform architecture, security requirements, and third-party integrations. Enterprises often begin with a focused MVP and expand the platform gradually as new services are added.

Q2. What features affect fintech super app development cost?

A2. Several features influence the development cost of a fintech super app. These include digital wallets, payment systems, lending modules, investment services, KYC verification, and financial analytics tools. The more financial services integrated into the platform, the higher the engineering complexity and infrastructure requirements.

Q3. How long does it take to build a fintech super app?

A3. Building a fintech super app typically takes 4 to 10 months, depending on the platform’s scope and complexity. An MVP version with core services can launch faster, while a full financial ecosystem requires longer development due to integrations, compliance checks, and scalability testing.

Q4. Can enterprises launch fintech super apps using white-label platforms?

A4. Yes, enterprises can launch fintech super apps using white-label platforms. In this model, the underlying fintech infrastructure is built by a technology provider, while the enterprise customizes the platform with its own brand and services. This approach allows companies to launch financial ecosystems faster without building the entire platform from scratch.