Key Takeaways:

-

CSRD compliance platforms map ESRS data points and automate double materiality assessment workflows.

-

ERP, HRIS, EHS, procurement, supplier, and finance integrations feed value chain disclosure data automatically.

-

ESEF/iXBRL tagging, EU Taxonomy alignment, and limited assurance readiness ensure regulator-ready compliance evidence.

-

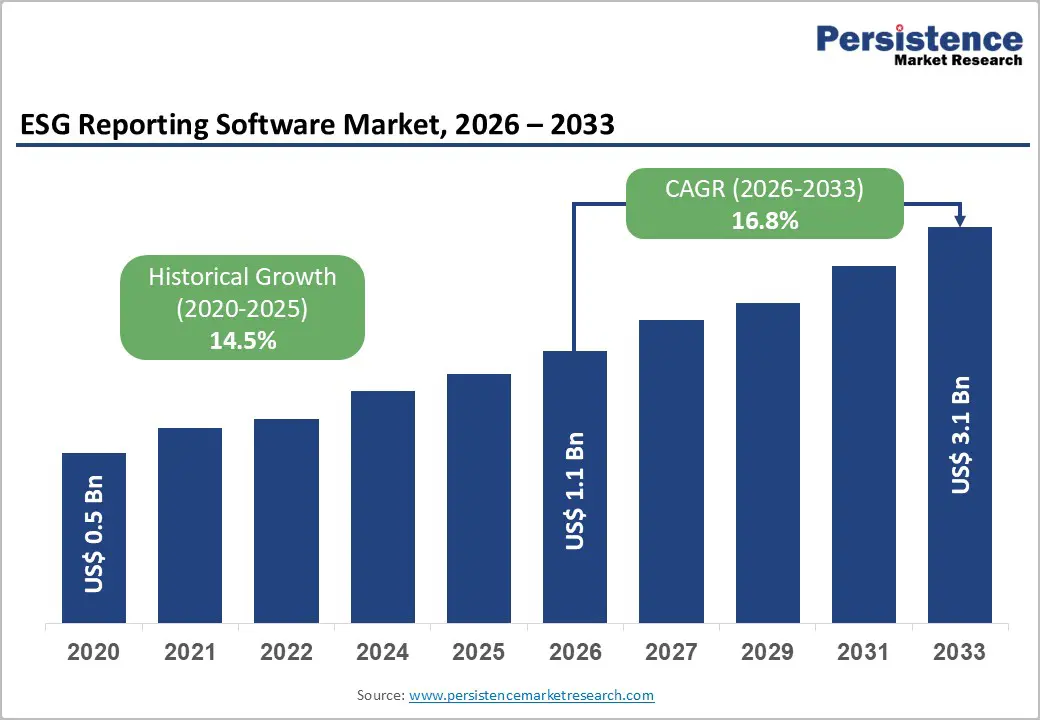

Focused MVPs cost $70,000 to $120,000 while multi-entity AI-powered platforms reach $180,000 to $300,000.

-

How Intellivon builds CSRD platforms as compliance infrastructure.

Building CSRD and ESG disclosure management software starts with the double materiality assessment engine, because that single module determines which of the more than 1,100 ESRS data points actually apply to the organization. Once that assessment logic is built, the platform maps the resulting material topics to ESRS data points, builds the XBRL digital tagging layer for ESEF submission, and layers in AI to draft narrative disclosures from the underlying data.

Building the data point mapping layer before the materiality engine is where most CSRD platforms get the sequence backward, since teams often try to build reporting templates for all twelve ESRS standards up front and then narrow them down later. The full ESRS data point list runs past 1,100 individual disclosure items, and mapping a platform to every one of them before materiality has been assessed means building reporting infrastructure for data the organization will never actually need to disclose.

Intellivon builds CSRD disclosure platforms by locking the materiality assessment architecture first, letting it determine scope before a single ESRS template gets built. This blog walks through double materiality automation, ESRS data point mapping, XBRL tagging, AI-assisted narrative drafting, audit readiness, and cost from $70,000 to $300,000, closing with a clear build-versus-buy framework.

What is CSRD Software?

Corporate Sustainability Reporting Directive (CSRD) software collects ESG data, maps it to European Sustainability Reporting Standards (ESRS) requirements, supports double materiality decisions, generates assurance-ready evidence, and prepares digitally tagged reports.

Consequently, the platform does not function as a simple dashboard. It operates as a governed disclosure system connecting sustainability, finance, legal, operations, suppliers, and external auditors.

Core Modules: The Platform Must Contain

To achieve complete compliance, your software requires dedicated infrastructure modules that process data through a strict verification pipeline. Specifically, the system must include the following functional blocks:

- ESRS Data Point Mapping Engine: Links enterprise data directly to specific regulatory requirements.

- Double Materiality Assessment Workflow: Automates stakeholder impact scoring and financial materiality matrix creation.

- Multi-Source Data Ingestion Engine: Connects to ERP, HR, and utility systems via secure API nodes.

- Supplier Value Chain Portal: Gathers external Scope 3 and social metrics securely from vendor networks.

- Audit Trail & Data Lineage Ledger: Logs every data change, formula change, and approval step automatically.

- ESEF XBRL Tagging Automation: Embeds machine-readable digital tags into final reports for regulatory submission.

Why Manual Spreadsheets Break at the ESRS Scale

Large organizations consistently struggle with fragmented ESG tools, manual data tracking, poor automation, and low user satisfaction. Because the ESRS framework demands hundreds of detailed data points, spreadsheet version control breaks down rapidly across multi-entity operations.

Furthermore, manual data entry lacks a verifiable audit trail, which exposes the firm to severe compliance penalties during limited assurance reviews.

Enterprise CSRD software is not just an ESG reporting tool. It is a controlled disclosure infrastructure designed to withstand financial-grade audits.

Why Enterprises Need A Custom CSRD Platform

Enterprises need a custom CSRD platform because CSRD reporting requires double materiality, value-chain data, assurance-ready evidence, and consistent ESRS-aligned disclosures across complex organizations.

1. Where Off-The-Shelf CSRD Tools Fall Short

Standard vendor software imposes rigid limitations that restrict multinational operations. Specifically, these packaged tools fail at the following:

- Rigid Approval Chains: They lack customizable, multi-tier legal and financial sign-off workflows.

- Weak System Integration: Packaged software cannot easily bridge custom ERPs and non-standard data silos.

- Opaque AI Governance: Standard tools use black-box language models that compromise data privacy.

Why Custom Build Makes Sense For Multi-Entity Firms

A custom engineering path allows complex organizations to build an ESG disclosure management system for enterprises that matches their exact footprints. Key operational advantages include:

- Subsidiary Rollups: Automate multi-tiered entity consolidation while preserving local data lineage.

- Multilingual Workflows: Enable localized evidence gathering from global facility managers effortlessly.

- Finance Integration: Aligns sustainability data capture with fast-closing financial reporting cycles.

ROI Comes From Audit Time And Data Reuse

Engineering a dedicated platform pays dividends by eliminating redundant operational work. Consider these core financial drivers:

- Fewer Rework Cycles: Automated verification routines catch missing utility data points early.

- Data Multiplicity: Allows cross-mapping of single data points across GRI, TCFD, and SEC frameworks.

Build vs Buy Decision Rule

Our custom CSRD reporting software development guide uses a simple binary framework to guide your technology choices:

- Buy: If your enterprise has a single entity, simple supply chains, and low regulatory complexity.

- Build: If you navigate multi-framework requirements, complex data structures, and strict audit demands.

Custom development becomes necessary when reporting complexity creates recurring manual work.

Why CSRD Reporting Is Now A Data Control Problem

CSRD reporting is now a data control problem because sustainability disclosures must meet financial-grade expectations for evidence, consistency, and assurance. Companies must report under ESRS, connecting ESG, finance, legal, operations, and auditors. Therefore, isolated data silos are no longer acceptable.

1. CSRD Turns ESG Reporting Into Regulated Disclosure

This framework moves ESG metrics into the official corporate management report. Consequently, this changes ownership from the ESG team to finance, compliance, legal, and operations.

- Mandatory Framework: Establishes legally binding disclosure obligations for enterprise companies.

- ESRS Standards define the exact data points companies must report.

- Management Report: Integrates sustainability metrics directly into the core corporate filing.

CSRD does not ask companies to publish a prettier sustainability report. It asks them to prove sustainability claims through controlled disclosure.

2. Finance Teams Now Need Audit-Ready ESG Evidence

CFOs now care because ESG metrics enter reporting cycles that regulators review thoroughly. For instance, the European Securities and Markets Authority (ESMA) enforces sustainability guidelines alongside financial reporting rules.

- Evidence Tracking: Ties verifiable source documents to every single disclosure.

- Review Workflows: Enforce multi-tier legal and financial sign-off chains.

- Finance-Grade Controls: Aligns sustainability data capture with fast-closing financial timelines.

3. Sustainability Data Must Match Annual Report Standards

Sustainability data cannot remain in loose spreadsheets, PDFs, and unstructured supplier email threads. Because auditors require clear verification, the data must become structured enough to support digital reporting and limited assurance.

- Period Consistency: Assures tracking methods remain uniform across multiple fiscal years.

- Data Lineage: Tracks the historical path of every metric from origin to report.

- Calculation Methodology: Records the specific mathematical calculation models used for emission factors.

The hard part is not writing the CSRD report. Instead, the hard part is proving that every number and statement came from an approved source.

4. Manual ESG Workflows Create Filing And Assurance Risk

Practitioners report that CSRD work has shifted rapidly into gritty Scope 1–3 inventories, supplier engagement, and audit-ready documentation. Reliance on manual processes introduces version chaos, missing evidence, and late reviewer comments that delay filing deadlines.

- Version Chaos: Disconnected files lead to conflicting metrics across global subsidiaries.

- Supplier Delays: Manual email follow-ups stall the collection of value chain data.

- Audit Sampling: Broken tracking prevents external auditors from verifying source documents quickly.

Turning ESG data into controlled disclosure infrastructure eliminates manual version chaos and filing risks.

For a deeper breakdown of system safety, see how we build Healthcare AI systems. This controlled data transition sets up the core platform capabilities your engineering team must build next.

CSRD Requirements Your Platform Must Support

A CSRD platform must support ESRS data point mapping, double materiality, value chain data collection, Scope 3 inputs, EU Taxonomy alignment, ESEF/iXBRL digital tagging, audit trails, and limited assurance readiness.

Therefore, these features are not optional because they define whether the disclosure process can survive a regulatory review.

Core Regulatory Architecture

| Core Module | Technical Requirement | Regulatory / Source Basis |

| ESRS Data Point Mapping | Maps requirement IDs, entity applicability, and metric types directly to active data source endpoints. | EFRAG IG3 (Detailed ESRS Datapoints List). |

| Double Materiality Assessment | Automates stakeholder impact scoring, financial impact thresholds, and material IRO logging. | PwC & Deloitte compliance guidance frameworks. |

| Value Chain Data Collection | Track upstream and downstream Scope 3 data with integrated vendor data quality scores. | EFRAG IG2 (Value Chain Implementation Guidance). |

| ESEF & iXBRL Digital Tagging | Converts narrative and table blocks into XHTML format with embedded machine-readable iXBRL tags. | ESMA ESEF Regulatory Technical Standards (RTS). |

| Limited Assurance Readiness | Records complete historical data lineage, comment histories, and access control sign-offs. | Third-party independent audit protocols. |

Limited assurance does not mean light evidence. Specifically, it means the software must prove enough structural lineage for external auditors to test the entire operational process seamlessly.

For a deeper breakdown of building scalable corporate data engines, see our guide on enterprise microservices architecture. Establishing these mandatory architectural pillars allows your engineering team to construct the core data ingestion engine safely.

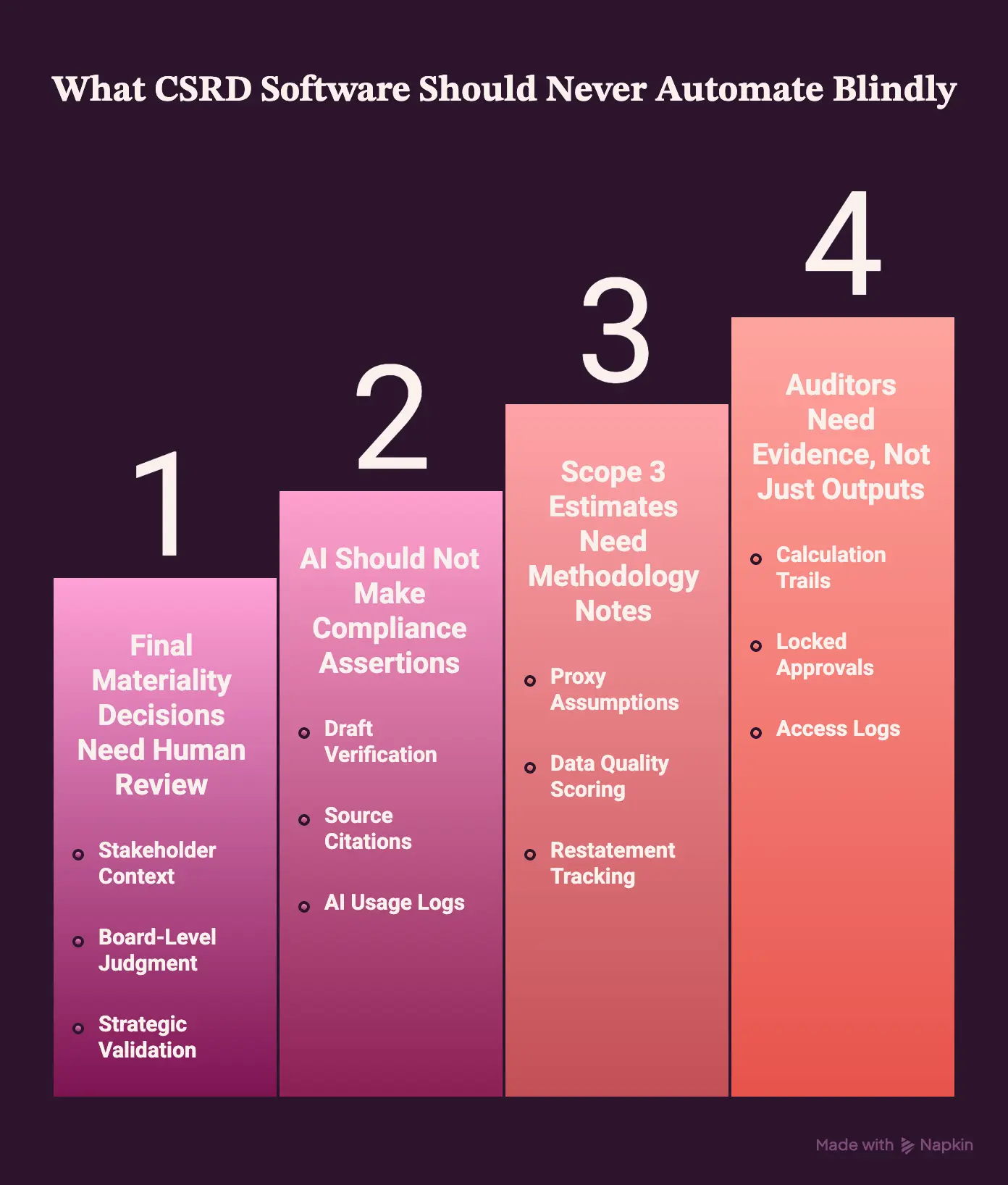

What CSRD Software Should Never Automate Blindly

CSRD software should never blindly automate final materiality decisions, compliance assertions, Scope 3 estimates, supplier claims, or assurance conclusions. Although workflow automation can speed evidence handling, humans must approve judgments that affect legal, financial, and sustainability disclosures.

Therefore, software must protect decision-makers rather than replace them.

1. Final Materiality Decisions Need Human Review

Double materiality assessment operates as a structured business judgment process rather than a mere data aggregation exercise. Consequently, software cannot independently evaluate strategic risk or determine final significance thresholds without human oversight.

- Stakeholder Context: Translates nuanced qualitative inputs into clear governance priorities.

- Board-Level Judgment: Secures formal executive agreement on long-term sustainability impacts.

- Strategic Validation: Protects the enterprise by ensuring compliance data matches broader corporate strategy.

2. AI Should Not Make Compliance Assertions

Large organizations require a strict human-in-the-loop framework because automated language models can introduce compliance vulnerabilities. For instance, data errors, proxy assumptions, and outdated tracking can create legal exposure if reports are published without review.

- Draft Verification: Marks all AI-generated text clearly as unverified draft material.

- Source Citations: Links narrative claims directly back to raw evidence files.

- AI Usage Logs: Records machine actions to provide transparent system histories for auditors.

3. Scope 3 Estimates Need Methodology Notes

Enterprises regularly struggle to collect ESG data from thousands of diverse global suppliers. Because value chain visibility remains uneven, platforms must document calculation methods rather than hiding data gaps behind smooth averages.

- Proxy Assumptions: Notes where spend-based estimates substitute for direct operational metrics.

- Data Quality Scoring: Ranks supplier inputs based on actual primary source availability.

- Restatement Tracking: Flags historical baselines that require adjustment when better data arrives.

4. Auditors Need Evidence, Not Just Outputs

External verification teams do not test high-level dashboard metrics alone. Specifically, they inspect the underlying control environments, version trails, and approval chains that generated those metrics.

- Calculation Trails: Expose the raw mathematical formulas used to convert energy usage into carbon equivalents.

- Locked Approvals: Prevents historical data modification once a reporting period closes.

- Access Logs: Record individual user modifications to ensure complete internal accountability.

Key Takeaway: Automation must reduce repetitive operational work rather than hiding critical human judgments.

For a deeper breakdown of structured software deployment, see our guide on enterprise DevOps consultancy. Protecting these boundary limits prepares your team to architect a highly secure platform layout.

Where AI Helps In CSRD Disclosure Workflows

AI helps CSRD workflows by extracting evidence from internal documents, drafting source-linked disclosure narratives, detecting missing data, comparing drafts against ESRS requirements, and summarizing reviewer comments.

The safest use case is AI-assisted preparation with human approval, not autonomous compliance reporting. Therefore, automated engines must act strictly as structured operational tools.

1. Extract ESRS Evidence From Internal Documents

Large organizations often struggle to manually locate sustainability data buried across disparate corporate assets. Specifically, natural language processing models can parse unstructured files rapidly to isolate critical metrics.

- Policy Processing: Scans HR guidelines, health and safety logs, and procurement records automatically.

- Targeted Tagging: Matches text blocks directly to corresponding environmental or social disclosure pillars.

- Context Retrieval: Identifies relevant historical evidence files across global operating subsidiaries efficiently.

2. Draft Disclosure Narratives With Source Links

Retrieval-Augmented Generation (RAG) workflows allow engineering teams to deploy language models safely without risking hallucinated outputs. Consequently, text generation remains anchored to verified data.

- Source Citation: Appends precise audit trails to every drafted paragraph automatically.

- Tone Alignment: Standardizes style syntax to match professional financial reporting expectations.

- Reviewer Efficiency: Speeds up drafting by providing compliant baselines for human sign-off.

3. Flag Missing Data And Weak Claims

Machine learning tools evaluate qualitative assertions to identify vulnerabilities before third-party assurance audits occur. This provides early visibility into reporting gaps.

- Anomaly Detection: Highlights statistical outliers or incomplete facility-level utility logs instantly.

- Methodology Verification: Flags calculations that lack clear emissions factor references.

- Stale Metrics: Alerts internal owners when vendor Scope 3 inputs require updates.

4. Compare Drafts Against ESRS Requirements

Automated semantic analysis checks the final report text against regulatory disclosure checklists to guarantee structural coverage.

- Gap Mitigation: Verifies that every material impact, risk, and opportunity contains its mandated narrative.

- Tagging Inspection: Confirms that data formatting matches required digital taxonomy frameworks.

- Compliance Scorecards: Generate real-time readiness assessments ahead of the final corporate submission.

AI must be used to find, draft, and cross-check evidence, but final compliance accountability remains a human preserve.

How To Build CSRD Software In 8 Clear Steps

Build CSRD software by turning regulatory requirements into a controlled disclosure system, then layering materiality, supplier data, integrations, sector workflows, AI, digital tagging, and framework reuse. The right sequence matters because AI, dashboards, and XBRL outputs only work when ESRS mapping, evidence ownership, and data controls are already stable.

Therefore, trying to build user interfaces before establishing data governance will derail the engineering lifecycle.

![]()

Step 1: Turn ESRS Data Points Into A Schema

The first step is converting ESRS disclosure requirements into structured software fields, owners, evidence rules, source systems, and validation logic.

This gives the platform a regulatory backbone before dashboards, AI, or reporting workflows are added. Specifically, the data model requires the following elements:

- Controlled Fields: Assign distinct disclosure IDs, units, and verification rules to every qualitative metric.

- Schema Segregation: Separates quantitative calculations cleanly from descriptive narrative blocks to simplify storage.

- Multi-Tier Scope: Traces whether each data point applies at the subsidiary, facility, or vendor level.

Intellivon treats ESRS mapping as the core platform layer, not a checklist screen. The team structures the schema so every data point can connect to evidence, workflows, AI review, and future XBRL tagging.

Once the ESRS schema exists, the platform can decide which disclosures matter through double materiality.

Step 2: Build Double Materiality Workflows

The second step is building double materiality workflows that capture stakeholder input, score impact materiality, score financial materiality, generate a defensible matrix, and preserve every review decision. This makes the materiality process traceable instead of spreadsheet-driven.

As a result, third-party reviewers can verify your scoring paths easily through these automated system tracks:

- Traceable Assessments: Captures stakeholder survey inputs and interview notes directly inside the database ledger.

- Dual-Score Matrices: Process impact and financial significance scores against customizable regulatory thresholds.

- Change Log Auditing: Preserves historical scoring updates along with full reviewer comments for future validation.

Intellivon designs this as a governance workflow with human approval at the center. AI can summarize stakeholder feedback or cluster topics, but final materiality decisions stay with sustainability, finance, legal, and leadership teams.

After material topics are confirmed, the platform needs reliable value chain and Scope 3 data to support those disclosures.

Step 3: Collect Value Chain And Scope 3 Data

The third step is creating structured workflows for supplier, value chain, and Scope 3 data collection. This replaces email-based requests with portals, questionnaires, reminders, evidence uploads, data quality scores, and estimate logic.

Thus, it eliminates the operational friction of chasing down manual supplier responses via these built-in systems:

- Vendor Portals: Hosts secure questionnaires where upstream partners can upload raw environmental evidence directly.

- Escalation Engines: Triggers automated reminders and notification rules when collection deadlines run close.

- Methodology Notes: Ranks data quality while attaching clear confidence scores to spend-based estimation proxies.

Intellivon builds supplier workflows so procurement, sustainability, and finance teams can reuse supplier evidence across reporting cycles. The goal is not to ask suppliers more questions. The goal is to ask once in a controlled format.

Once external data collection is structured, the platform must connect internal enterprise systems.

Step 4: Connect ERP, HRIS, Procurement, And EHS

The fourth step is connecting CSRD workflows to the enterprise systems where ESG evidence already lives. ERP, HRIS, procurement, EHS, finance, carbon tools, and document systems should feed the platform instead of forcing teams to re-enter data manually.

Consequently, this creates an unalterable bridge for source data pipelines using the following integrations:

- ERP Gateways: Extract financial CapEx, OpEx, and procurement spend data automatically for environmental calculations.

- HRIS Connectors: Gather employee safety records, training logs, and diversity metrics for social disclosures.

- EHS Pipelines: Streams real-time facility-level utility, water, waste, and direct carbon emission values safely.

Intellivon uses API-first architecture where possible and controlled data imports where legacy systems limit access. The team prioritizes traceability, so every imported metric shows its source, refresh cycle, owner, and validation status.

Once core enterprise systems are connected, the platform should adapt to sector-specific reporting realities.

Step 5: Add Healthcare And Fintech Workflows

The fifth step is adding sector-specific workflows for healthcare and fintech users. CSRD software should not treat a hospital, pharma company, medical device firm, bank, insurer, and asset manager as if they collect the same ESG evidence.

Therefore, custom validation rules must be applied based on these specialized market realities:

- Healthcare Controls: Enforce HIPAA-aware access permissions while tracking clinical waste and medical gas pipelines.

- Fintech Compliance: Integrates financed emissions calculations using precise PCAF data quality scoring rules.

- Framework Alignment: Bridges core data repositories directly into SFDR and EU Taxonomy scoring models.

Intellivon configures sector workflows around the systems and evidence each industry actually uses. For healthcare, that means facility- and procurement-heavy reporting. For fintech, that means portfolio, product, risk, and framework-mapping logic.

Once the platform understands the industry workflow, AI can be added safely to reduce review workload.

Step 6: Build AI Assistance Without Audit Risk

The sixth step is adding AI assistance for evidence extraction, disclosure drafting, gap detection, and ESRS comparison without allowing AI to make final compliance judgments. AI should accelerate review, not replace accountability.

Because errors create regulatory risks, the system implements text safety through these specific guardrails:

- Anchored Pipelines: Deploy RAG-based systems that link every drafted line directly to verified source files.

- Vulnerability Detection: Identifies unbacked claims, missing owner fields, or anomalous facility utility data points early.

- Immutable Tracking: Records every single user edit, model prompt, and narrative modification for auditors.

Intellivon keeps AI inside a controlled compliance workflow. The model can draft, summarize, compare, and flag risk, but sustainability, finance, legal, and audit teams approve final disclosures.

After disclosures are approved, the platform must prepare them for digital reporting and XBRL workflows.

Step 7: Prepare Reports For ESEF And XBRL Tagging

The seventh step is preparing approved CSRD disclosures for ESEF and XBRL tagging. The platform should support report exports, taxonomy mapping, XHTML preparation, iXBRL tagging workflows, validation checks, and reviewer approval before filing.

Consequently, this step prepares your data for direct electronic distribution using these tools:

- Taxonomy Mappers: Connect validated narrative blocks to their precise legal European regulatory reference codes.

- XHTML Generators: Convert raw documents into the universal web formats required by European authorities.

- Tagging Bridges: Integrates with specialist digital stamping software while keeping your raw evidence trails locked.

Intellivon separates disclosure control from tagging execution. That prevents the platform from becoming too rigid while still giving the enterprise traceability from the initial data point to the final digital report.

Once the report output works, the final step is making CSRD data reusable beyond one filing cycle.

Step 8: Make CSRD Data Reusable Across Frameworks

The eighth step is building a framework reuse layer so approved CSRD data can support ESRS, GRI, TCFD, CDP, SFDR, EU Taxonomy, SEC readiness, board reports, and internal ESG dashboards. This is where the platform creates long-term ROI.

Specifically, this cross-mapping engine handles data management through these methods:

- Single-Source Ingestion: Maps an individual validated workforce or carbon metric across multiple different framework outputs.

- Historical Repositories: Store approved corporate narratives and methodology notes securely for future annual cycles.

- Scalable Architecture: Prepares the system foundation to absorb future regulatory updates without expensive code rewrites.

Intellivon designs this layer so CSRD software becomes an ESG disclosure infrastructure, not a one-year compliance tool. The system supports future frameworks, regulatory changes, new entities, and expanded AI workflows without rebuilding the foundation.

This reusable layout brings us directly to the cost conversation, as framework breadth directly impacts engineering timelines.

CSRD Compliance SaaS Platform Development Cost

CSRD compliance SaaS platform development usually costs $70,000 to $300,000, depending on entity count, ESRS mapping depth, integrations, double materiality workflow complexity, AI modules, supplier portals, XBRL tagging scope, assurance controls, and multi-framework reporting needs.

A focused MVP should stay near $70,000 to $120,000, while enterprise builds reach $180,000 to $300,000. Therefore, setting your architectural scope early prevents unexpected budget inflation.

Phase-by-Phase Cost Breakdown

| Development Phase | What It Includes | Estimated Cost |

| CSRD Scope and Discovery | Entity mapping, reporting scope, stakeholder map, workflow audit | $8,000–$18,000 |

| ESRS Data Model | ESRS data point mapping, schema, owners, evidence rules | $12,000–$30,000 |

| Double Materiality Workflows | Stakeholder inputs, scoring, matrix, approvals, audit evidence | $10,000–$28,000 |

| Core Platform Build | Dashboards, forms, workflow engine, role access, notifications | $18,000–$50,000 |

| Enterprise Integrations | ERP, HRIS, EHS, procurement, supplier, finance, carbon systems | $20,000–$65,000 |

| Supplier and Value Chain Portal | Supplier requests, evidence upload, Scope 3 inputs, reminders | $12,000–$35,000 |

| AI Disclosure Assistance | NLP extraction, RAG drafting, missing data flags, review controls | $15,000–$45,000 |

| Audit and Assurance Controls | Data lineage, versioning, approvals, evidence packs, auditor access | $12,000–$32,000 |

| ESEF/iXBRL Workflows | Tagging tool integration, validation, export, taxonomy updates | $10,000–$30,000 |

| Testing and Rollout | QA, UAT, security testing, training, production deployment | $8,000–$22,000 |

- Total Build Range: $70,000–$300,000

- Ongoing Maintenance: 15%–25% of the initial build cost per year

- Typical Timeline: 10–16 weeks for an MVP; 5–9 months for a full enterprise rollout

The right financial model separates baseline compliance must-haves from advanced automated workflows. Consequently, this prevents overspending on high-fidelity user dashboards before your underlying core data validation engine functions correctly.

Because budget constraints depend heavily on organizational layout, understanding when to avoid a custom project helps clarify the financial commitment.

Why Hire Intellivon For CSRD Software Development

Hire Intellivon when your CSRD platform needs assurance-ready controls, safe AI, and sector-specific depth beyond generic ESG tools.

- Built for audit readiness: Get ESRS data lineage, evidence logs, approval trails, version history, and auditor-ready exports.

- AI without compliance risk: Use RAG-based disclosure drafting, ESRS evidence extraction, missing data alerts, and human review workflows.

- Healthcare and fintech expertise: Support hospital, pharma, medical device, banking, insurance, SFDR, EU Taxonomy, and PCAF workflows.

- Enterprise-grade engineering: Work with ex-MAANG engineers and teams backed by 500K+ engineering hours across complex AI builds.

- Cost clarity upfront: Plan MVP, enterprise, AI, integration, and maintenance budgets within the $70,000–$300,000 range.

Talk to Intellivon’s CSRD software experts to scope your disclosure platform, estimate your build cost, and decide whether custom development is the right move.

Conclusion

CSRD compliance software development is not about adding another ESG dashboard. Instead, it builds disclosure infrastructure that connects ESRS data, double materiality, supplier evidence, AI-assisted review, audit trails, and digital reporting.

As a result, complex healthcare and fintech enterprises can reduce manual work, improve assurance readiness, and reuse ESG data across frameworks. Therefore, a focused $70,000–$300,000 build gives teams control before CSRD reporting becomes harder across reporting cycles and audits.

FAQs

Q1. How much does CSRD compliance software cost?

A1. CSRD compliance software usually costs $70,000–$300,000. A focused MVP with ESRS mapping, data collection, evidence uploads, and dashboards costs $70,000–$120,000. However, a multi-entity platform with integrations, supplier workflows, AI assistance, assurance controls, and XBRL support usually costs $180,000–$300,000.

Q2. How long does it take to build CSRD software?

A2. A CSRD software MVP usually takes 10–16 weeks. However, a production-grade enterprise platform usually takes 5–9 months. Timelines increase when the build includes deep ESRS mapping, double materiality workflows, ERP integrations, supplier portals, AI modules, assurance testing, and XBRL reporting support.

Q3. Can AI write a CSRD report by itself?

A3. AI can support CSRD reporting, but it should not write and finalize the report by itself. Instead, it should extract evidence, summarize policies, draft ESRS narratives, flag missing data, and check consistency. However, sustainability, finance, legal, and audit teams must approve every final disclosure.

Q4. Should we build or buy CSRD software?

A4. Buy CSRD software when your reporting scope is simple, your workflows match vendor templates, and your deadline is close. However, build custom software when you have complex subsidiaries, regulated data, sector-specific workflows, non-standard approvals, multi-framework reuse, or integrations that create recurring manual work every reporting cycle.

Q5. What makes CSRD software audit-ready?

A5. CSRD software becomes audit-ready when every disclosure links to source data, evidence, owner, reviewer, methodology, timestamp, approval trail, and version history. Additionally, the platform should support limited assurance, controlled auditor access, evidence pack exports, role-based permissions, and stronger assurance requirements as reporting expectations mature.

To Sum It Up

- CSRD software fails when teams build report screens before they map ESRS data ownership, evidence rules, and assurance controls.

- The real ROI of CSRD software comes from reusable data, fewer audit rework cycles, and less manual supplier follow-up.

- AI can draft CSRD narratives, but it cannot replace materiality judgment, Scope 3 methodology, or auditor-ready evidence.

- A $70,000 MVP can prove the workflow, but multi-entity CSRD disclosure platforms usually need $180,000–$300,000 to handle integrations and assurance properly.

- The strongest CSRD platforms reuse one validated ESG metric across ESRS, GRI, TCFD, CDP, SFDR, SEC readiness, and board reporting.