Key Takeaways:

-

Custom AI banking agents should start with one bounded workflow, and not a general-purpose autonomous banking system.

-

7 layers, including model routing, RAG knowledge base, core banking APIs, and human approval gates, are required.

-

Credit decisions, SAR filing, and funds movement must remain under bank-defined authorization controls throughout.

-

Controlled pilots cost $70,000 to $110,000 while multi-agent production platforms reach $210,000 to $300,000.

-

How Intellivon builds AI banking agent systems where agents retrieve evidence and execute only bank-approved actions.

The core banking system a regional bank runs on determines what each custom AI agent can do. Building custom AI agents for banking starts with mapping the core integration layer of that specific system. Instead, each agent reads and writes banking data through that specific system’s API. From there, agents deploy across loan origination, compliance monitoring, fraud detection, and relationship banking.

Regional banks need SR 11-7-compliant AI agents without dedicated model risk teams. Without pre-built model documentation in the agent architecture, OCC and FDIC examination findings follow. CSI’s 2026 survey found 63% of financial institutions have no AI governance policies in place. Therefore, building governance into the agent architecture before deployment is what prevents those findings.

Intellivon builds custom AI agents for regional banks where core integration and SR 11-7 are non-negotiable. The approach always starts with core integration mapping before agent workflows or the RAG knowledge base. Accordingly, this blog covers agent architecture, SR 11-7 governance design, and banking compliance automation.

What Custom AI Agents Banking Systems Actually Do

Custom banking AI agents are controlled software workers that retrieve information, reason over bank policies, call approved systems, and advance multi-step workflows. Unlike chatbots, they maintain task state and initiate permitted actions.

However, the bank must define its goals, data access, tools, spending limits, escalation rules, and prohibited actions before deployment.

1. Banking Chatbots, Copilots, Automation, And Agents Are Different

Autonomy is an action-by-action permission model designed to mitigate operational risk. At the same time, regional banks must distinguish between these systems to deploy them safely.

| System | What It Does | Example | Level Of Authority |

| Chatbot | Answers a request | Explains CD rates | None |

| RPA bot | Executes fixed steps | Copies data between systems | Deterministic |

| Copilot | Drafts or recommends | Prepares a credit memo | Human acts |

| AI agent | Plans and uses tools | Collects missing loan documents | Bounded |

| Multi-agent system | Coordinates specialists | Runs onboarding evidence collection | Bounded and distributed |

2. Goal-Oriented Agents Need More Than An LLM

An isolated LLM cannot run enterprise operations. At the same time, a complete custom AI agents banking system requires an integrated operational framework to ensure predictability:

- Workflow state: Tracks the progress, data inputs, and current status of multi-step financial transactions.

- Planning and task decomposition: Break broad goals down into a sequential checklist of micro-tasks.

- Tool registration: Connects the system safely to verified banking APIs, calculators, and database environments.

- Policy retrieval: Pulls internal underwriting guidelines using an RAG-powered banking knowledge base.

- Short-term memory: Maintains transaction context across long customer interactions.

- Identity and permissions: Enforce zero-trust role-based access tokens for every system request.

- Validation: Screens all outputs to ensure absolute compliance with internal credit and operational metrics.

- Escalation: Routes complex cases directly to human operators when boundary errors.

- Audit evidence: Generates cryptographic, immutable logs of all agent reasoning paths.

3. The Agent Authority Matrix Comes Before Architecture

Before building a system, banks must implement an Agent Authority Matrix to govern behavior across five distinct operational tiers:

- Retrieve: Reads approved information from connected systems without altering data.

- Draft: Prepares internal content or messages without transmitting or submitting them.

- Recommend: Analyzes data to suggest explicit actions backed by clear policy evidence.

- Execute after approval: Performs a transaction only after a named human reviewer explicitly clicks approve.

- Bounded execution: Completes low-risk, fully reversible actions within predefined spending or balance limits.

4. Actions A Regional Bank Should Not Fully Delegate

Certain sensitive workflows present extreme regulatory risks and must never be left to fully autonomous systems.

| Prohibited Action | Risk Mitigation Strategy |

| Final adverse-action decisions | Requires a human credit officer to issue official loan denials. |

| Filing SARs without a qualified review | Requires compliance officers to audit and sign off on all filings. |

| Sanctions overrides | Mandates human validation for potential OFAC or sanctions list hits. |

| Unsupervised wire or ACH release | Locks high-value funds routing behind strict multi-factor human authorization. |

| Account closure or restriction | Restricts systemic asset locks to authorized retail and operations managers. |

| Pricing exceptions | Escalates custom interest rate quotes to treasury management teams. |

| Credit-policy overrides | Rejects automated deviations from core underwriting parameters. |

| Customer identity overrides | Flags structural KYC onboarding failures for manual review. |

| Destructive changes to core records | Blocks automated deletion or un-audited manipulation of core customer profiles. |

The intelligence of a custom agent matters far less than the authority attached to its active tools. Once the bank defines those clear boundaries, it can identify specific workflows where agentic automation creates maximum value without transferring institutional accountability.

Why Are Regional Banks Adopting Agents For Their Functions

Mid-size financial institutions face critical resource constraints compared to national tier-one banks. Consequently, they are deploying custom AI-based banking software to protect margins, scale operations, and compress their time-to-revenue without increasing headcount.

At the same time, mid-size institutions are shifting away from traditional copilots toward hybrid, small language models to systematically embed explainable, autonomous execution within risk-sensitive workflows.

1. The Cost and Headcount Squeeze

Regional banks cannot simply hire their way out of heavy operational backlogs due to rising labor costs. Therefore, they rely on autonomous agents to absorb skyrocketing transaction volumes.

- Straight-Through Processing Expansion: Agents handle clean operational cases automatically, leaving only complex anomalies for human staff.

- Operational Expense Control: Multi-agent architectures reduce manual intervention in critical workflows by up to 80%, immediately cutting overhead costs.

- Talent Reallocation: Employees shift away from boring data entry to focus entirely on high-value client advisory roles.

2. The Failure of Legacy Automation

Traditional Robotic Process Automation (RPA) breaks down whenever layout designs change or document formats shift. On the other hand, goal-oriented agents adapt to dynamic banking scenarios seamlessly.

- Contextual Policy Reasoning: Agents use advanced reasoning engines to interpret complex guidelines rather than following rigid, easily broken rules.

- Unstructured Data Processing: Systems ingest variable financial formats—like tax returns or legal contracts—without requiring manual reformatting.

- Dynamic Exception Handling: When a tool workflow stalls, the agent automatically attempts alternative paths before requesting human intervention.

3. Core System Integration Openings

Modern middleware and composable core extensions make it easier than ever to deploy agents safely. As a result, banks can implement autonomous workflows without executing high-risk, expensive core replacements.

- API-Driven Execution Layers: Thin, feature-rich banking cores allow custom software workers to read and write ledger data safely.

- Bidirectional Core Synchronization: Platforms keep agents updated with real-time customer states, preventing conflicting data writes.

- Reduced Integration Costs: Standardized connection tools allow quick deployment across platforms like Fiserv or Jack Henry.

Regional banks use agentic infrastructure to bridge the technology gap with major national competitors at a fraction of the cost. By automating complex processes like loan triage and AML reviews, they secure structural efficiencies that traditional software cannot match.

Design The Regional Bank AI Agent Control Architecture

A regional bank agent platform needs a shared control architecture rather than separate chatbots attached to individual departments. The platform should centralize identity, model access, RAG, tool permissions, workflow state, approval rules, and audit evidence.

At the same time, individual agents may specialize by function, but they should operate through the same governed infrastructure.

The Seven-Layer Governance Blueprint

To prevent architectural fragmentation, mid-size financial institutions must implement a centralized, multi-tier system topology. Furthermore, this approach isolates risk while maintaining operational continuity across business units.

| Architectural Layer | Core Technical Focus | Primary System Components & Protocols |

| Layer 1: Identity & Channels | Maps secure access across user touchpoints | Integrates SAML/OIDC SSO, CRM panels, mobile endpoints, and active role mapping. |

| Layer 2: Orchestration & State | Controls sequential workflow execution | Deploys deterministic state machines (e.g., LangGraph), task queues, and dead-letter queues. |

| Layer 3: Model Routing | Matches incoming tasks to optimal compute | Pair large language models for policy parsing with small models for fast extraction. |

| Layer 4: RAG & Knowledge | Supplies verified domain context | Uses vector databases (Pinecone) with effective dates and strict version handling. |

| Layer 5: Policy & Authorization | Governs transactional safety guardrails | Evaluates runtime tool permissions, strict value limits, and role-based approval triggers. |

| Layer 6: Tool Gateway | Connects external infrastructure | Hosts secure adapters for cores (Fiserv DNA, Jack Henry), credit bureaus, and payment rails. |

| Layer 7: Observability & Audit | Generates immutable compliance logs | Tracks versions, applied rules, and user identities within an explicit, structured decision trace. |

Specifically, engineering teams should build these layers using stateful orchestration frameworks like LangGraph rather than letting free-form agent loops manage regulated processes. In practice, this ensures predictable execution boundaries.

For a deeper breakdown of compliant framework mechanics, see our technical guide on How to Build AI Agents for Banking Compliance & AML. Intellivon’s framework natively separates predictive risk evaluation from automated evidence assembly pipelines.

Centralizing agent coordination within a single, audited framework prevents isolated security gaps across banking channels. Consequently, regional operations leaders can scale functional capabilities safely while preserving an untampered, end-to-end regulatory compliance trail.

Build Banking RAG, Models, And Memory Around Policy

Regional-bank agents should combine RAG, deterministic rules, traditional models, and task-specific LLMs. RAG supplies current policies and evidence. Rules enforce non-negotiable controls. Predictive models produce risk or anomaly scores. LLMs interpret documents, coordinate steps, and explain evidence without becoming the final authority for every banking decision.

Deploy a Hybrid Technology and Routing Topology

To operate effectively under regulatory scrutiny, a custom AI agent’s banking ecosystem requires a modular, task-specific architecture rather than a single massive language model.

Consequently, routing logic must align execution with the exact operational layer needed for the task.

| Task | Recommended Technology | Operational Functionality |

| Policy Q&A | RAG-grounded LLM | Searches versioned internal product manuals and deposit guidelines. |

| Document Classification | Small Language Model (SLM) | Parses unstructured loan uploads and income files quickly. |

| Transaction Anomaly Scoring | Traditional ML / Graph Model | Identifies behavioral fraud markers and velocity spikes. |

| Credit-Risk Score | Validated Statistical Model | Generates mathematical probabilities of default deterministically. |

| Eligibility Threshold | Deterministic Rules Engine | Enforces hard limits like credit score minimums or geographic bounds. |

| Credit Memo Drafting | LLM with Structured Evidence | Compiles verified asset data into pre-configured banking formats. |

| Reason-Code Selection | Controlled Mapping Logic | Selects specific adverse-action justifications without text drift. |

| Tool Authorization | Policy Engine | Assesses runtime execution bounds and human approval queues. |

| SAR Narrative Prep | RAG-grounded LLM | Builds comprehensive alert summaries for compliance sign-off. |

Furthermore, this multi-tiered architecture ensures that sensitive bank documentation, such as credit policies, BSA/AML operations procedures, and examination responses, remains compartmentalized.

As a result, individual agents pull real-time policy data using metadata-filtered retrieval sequences while isolating conversation memory from permanent customer records to prevent data leakage.

For more context on automating these financial processes securely, you can check out this technical overview on How to Build an AI Underwriting Engine for Lenders, which details the operational timelines and data integrations necessary for banking deployments.

Map Banking Compliance To Every Agent Action

Compliance should be mapped at the workflow-action level. A single banking agent may touch consumer protection, privacy, BSA, sanctions, lending, recordkeeping, and third-party risk obligations during one task.

At the same time, the control register must therefore connect every tool, data element, generated output, and approval step to the applicable policy owner and evidence requirement.

1. Apply The Revised Model Risk Framework Correctly

The regulatory environment for model risk has undergone direct structural shifts. Notably, the newly issued SR 26-2 guidance officially supersedes the long-standing SR 11-7 standard. Consequently, this updated guidance alters how financial institutions approach system validation.

- Asset Boundaries: The revised framework is expected to be most relevant for large banking organizations operating above a $30 billion asset threshold.

- Small Institution Scope: Smaller community institutions may still find the framework highly relevant when their specific model exposure or architectural risk is significant.

- Generative AI Exclusions: Generative software applications and autonomous agentic workflows currently sit entirely outside the stated formal scope of SR 26-2.

Therefore, rather than declaring that an agentic platform is SR 11-7 compliant, the bank applies risk-based governance informed by SR 26-2, internal AI policy, operational-risk standards, information-security requirements, consumer-protection obligations, and the materiality of each use case. Traditional quantitative statistical infrastructure and non-generative risk scoring models remain actively covered under standard compliance validations.

2. BSA, AML, OFAC, And SAR Workflows

Anti-money laundering operations demand explicit structural separation between model suggestions and financial reporting execution. Accordingly, automated pipelines organize compliance data without bypassing human oversight:

- Rule Isolation: Deterministic transaction monitoring systems remain completely separate from generative parsing layers.

- Evidence Collection: Custom agents systematically enrich case files, gather core ledger histories, and build linked graph models to isolate related entities.

- Disposition and Review: Natural language engines summarize alert details, but qualified compliance staff exclusively determine final case dispositions.

Furthermore, generated Suspicious Activity Report (SAR) text narratives require mandatory manual review. Thus, critical regulatory filing credentials remain strictly restricted to certified human officers, ensuring all underlying evidence and reviewer modifications are permanently recorded in the audit trail.

For a deeper breakdown of compliance-agent architecture, see our guide on How to Build AI Agents for Banking Compliance & AML.

3. ECOA, FCRA, Fair Lending, And Adverse Action

Automated lending assistance must never become an opaque credit evaluation black box. Instead, platforms implement continuous monitoring protocols to safeguard fair lending integrity:

- Variable Registers: The system restricts inputs to a board-approved variable register, entirely eliminating prohibited-basis fields.

- Fidelity & Testing: Engineers deploy counterfactual tests and segment performance audits to confirm strict reason-code fidelity across demographic groups.

- Exception Tracking: Operational managers monitor credit overrides continuously, reconciling adverse-action outputs against underwritten metrics.

Specifically, CFPB guidance explicitly states that structural model complexity does not remove a creditor’s strict obligation to provide specific, accurate reasons for adverse action. As a result, any policy exception flags immediately halt processing, routing the credit file straight to an expert underwriting panel for manual validation.

4. GLBA, Privacy, Retention, And Customer Consent

Protecting consumer data requires granular field privacy rather than generic perimeter firewalls. Therefore, agent environments enforce zero-trust data protection policies natively:

- Minimization Frameworks: System workflows enforce strict data minimization and purpose limitation across every automated task.

- Field Masking: API components execute field-level masking, removing sensitive account identifiers and PII strings before payloads hit external LLMs.

- Retention Enforcement: Database routines coordinate strict retention schedules, driving deletion workflows that instantly fulfill data-subject removal requests.

In practice, customer-consent status is checked programmatically before an agent triggers a workflow. Furthermore, vendor data-processing terms must legally block banking payloads from being used for generic model training, ensuring total information isolation.

The compliance layer should not consist of static policy documents stored beside the platform. Instead, it must function as an active, hard-coded software gatekeeper that determines exactly what data the agent may access, which output format it must use, and whether the next workflow step is legally permitted.

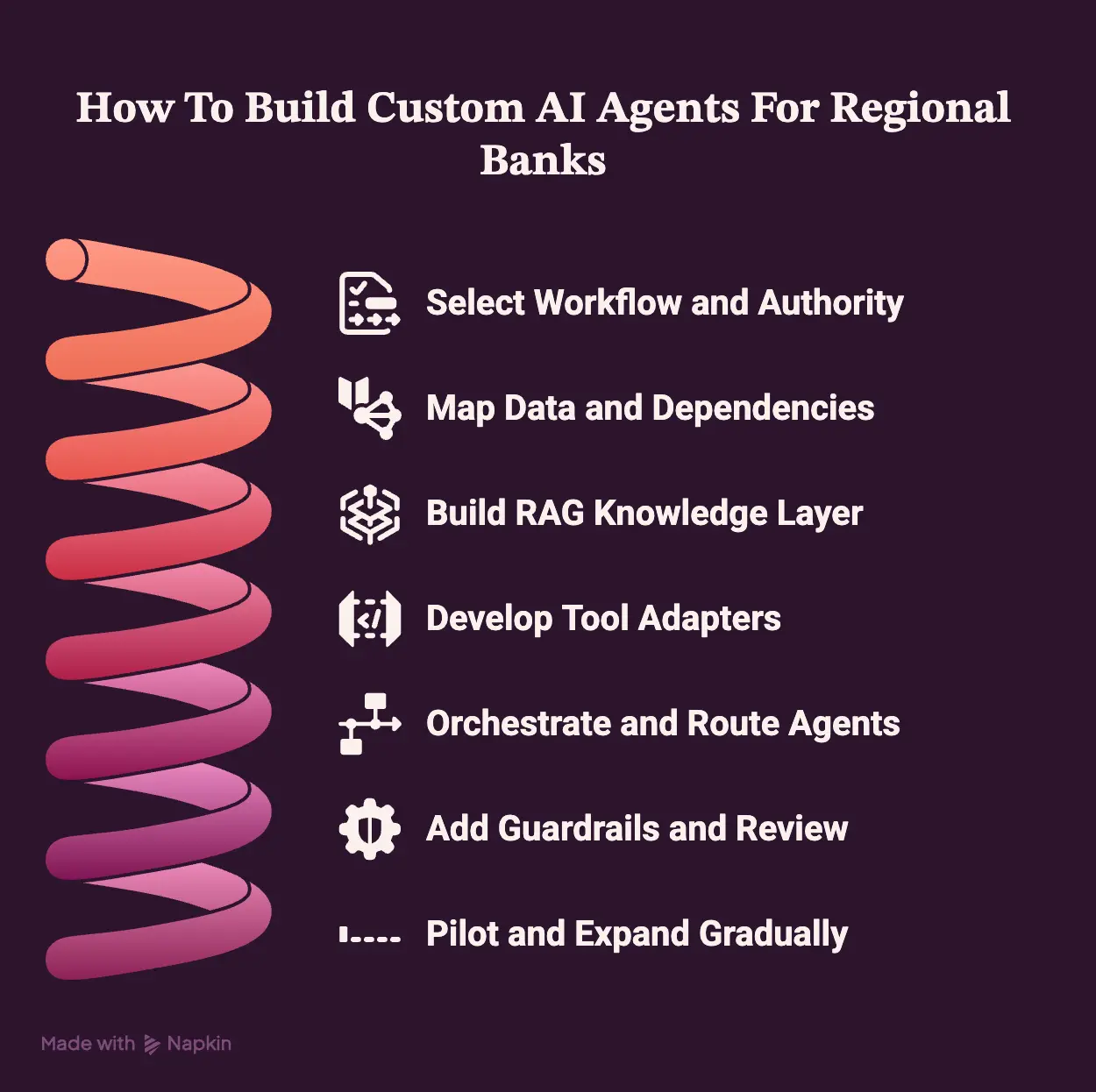

How To Build Custom AI Agents For Regional Banks

Building custom AI agents for banking frameworks requires shifting away from open-ended chat scripts toward deterministic software engineering. The implementation process must be executed across seven distinct development phases to ensure absolute predictability and compliance.

Phase 1 — Select One Workflow And Define Agent Authority

Start by selecting one workflow with clear ownership, measurable volume, stable procedures, and a manageable consequence level. This authority map becomes the product scope, security model, testing plan, and governance record.

- Engineering Framework: Map current workflows, establish performance baselines, catalogue potential errors, and deploy explicit prohibited-action registers alongside strict data classification boundaries.

- The Intellivon Approach: We begin with workflow decomposition rather than model selection. The engineering team turns each manual action into a controlled state, then explicitly assigns the necessary evidence metrics, system permissions, approving human roles, and audit trail requirements.

Once authority boundaries are fixed, the bank can confidently map the exact data models and policies needed for each operational state.

Phase 2 — Map Data, Policies, And System Dependencies

Create a dependency map showing where the agent obtains customer data, account history, policies, documents, scores, and approvals. This prevents the agent from treating stale CRM data, retrieved documents, or generated summaries as authoritative banking records.

- Engineering Framework: Conduct thorough source-system inventories, enforce strict customer identity matching, evaluate live API boundaries, and outline robust test-data strategies.

- The Intellivon Approach: The engineering team constructs a normalized canonical banking data model before connecting any live agent tools. This structural separation drastically reduces vendor-specific runtime assumptions embedded inside prompts and workflow execution logic.

The approved data and policy inventory then becomes the stable foundation for all downstream retrieval and memory layers.

Phase 3 — Build The RAG And Banking Knowledge Layer

Build a versioned RAG layer that retrieves only policies applicable to the product, customer, jurisdiction, and effective date. The agent should quote or cite the controlling source, detect conflicting procedures, and stop when evidence is missing.

- Engineering Framework: Implement structured OCR pipelines, establish clear metadata schemas, and deploy hybrid keyword-semantic search algorithms coupled with automated source verification.

- The Intellivon Approach: Intellivon combines metadata-driven database filters directly with semantic vector retrieval. This architectural design completely prevents an autonomous agent from accidentally using an expired lending policy or a retail procedure written for a different state or financial product.

The versioned knowledge layer can now safely support agent reasoning, but it still requires secure access to active core banking environments.

Phase 4 — Develop Core And Fintech Tool Adapters

Convert broad system access into narrow, typed tools. Instead of giving an agent unrestricted core credentials, expose functions such as get_account_status, retrieve_loan_documents, or create_review_task. Validate every input and separate read, draft, approval, and write permissions.

- Engineering Framework: Build narrow API gateway adapter services, enforce OAuth 2.0 service identities, validate payloads, and script automated rate-limiting and data tokenization routines.

- The Intellivon Approach: The development team places every core and fintech adapter behind a strict policy-enforcement layer. Therefore, the language model never decides on its own whether it has programmatic permission to modify an active ledger record.

With verified data paths and structured tools available, the targeted workflow can be successfully implemented as a controlled agent system.

Phase 5 — Build Agents, Orchestration, And Model Routing

Implement the workflow as a deterministic state graph with AI used inside defined states. Create specialist agents only when they need separate prompts, permissions, models, or evaluation criteria. A single controlled agent is preferable when multiple agents would add coordination risk without improving the outcome.

- Engineering Framework: Code supervisor routing logic, define rigid task state structures, enforce JSON schema outputs, and manage context window limits using programmatic timeout rules.

- The Intellivon Approach: Intellivon explicitly separates probabilistic reasoning from deterministic workflow control. The LLM may interpret unstructured evidence or draft an account response, but the underlying orchestration engine strictly controls which state and tool may run next.

The functional agent must now be aggressively tested against system misuse, missing evidence inputs, and real-world banking exceptions.

Phase 6 — Add Guardrails, Evaluation, And Independent Review

Test the agent as a workflow system, not only as a language model. Evaluation must measure whether it retrieves the correct evidence, follows the permitted path, selects the right tool, requests approval, and avoids action when confidence or authorization is insufficient.

- Engineering Framework: Establish golden test case suites, simulate malicious prompt-injections, validate reason-code fidelity, and conduct blind independent challenges before compliance sign-off.

- The Intellivon Approach: Intellivon creates a highly reproducible, automated evaluation suite for every individual software release. A platform deployment cannot progress to production merely because a small sample of testing conversations appears convincing.

Once the agent successfully passes controlled automated testing, it enters live shadow mode before gaining any production transaction authority.

Phase 7 — Pilot In Shadow Mode And Expand Gradually

Run the agent beside the existing process before allowing production actions. Compare its evidence, recommendations, escalations, and processing time against human outcomes. At the same time, grant additional permissions only after the bank meets predefined quality, risk, and operational thresholds across a representative sample.

- Engineering Framework: Deploy in read-only shadow configurations, execute structured user acceptance testing (UAT), analyze system overrides, and build reliable fallback protocols.

- The Intellivon Approach: Intellivon moves custom banking agents from read-only access to automated drafting, recommendation, human approval, and bounded execution across separate, monitored releases. Every single increase in systemic authority mandates a new round of independent risk testing and formal control validation.

Developing an enterprise-grade banking agent is a systematic engineering process and not a prompt engineering experiment.

Custom Banking AI Agent System Development Cost

Custom banking AI agent system development usually costs $70,000–$300,000, depending on workflow count, agent authority, core-banking integrations, RAG complexity, compliance controls, model deployment, and whether the system supports one bank or a white-label SaaS product.

Consequently, financial institutions must evaluate total costs based on the engineering tier required to meet their operational parameters.

1. Project Cost Tiers

Mid-size banks can adjust their financial allocation by choosing a predefined implementation scope matching their functional target.

| Build Tier | Included Scope | Timeline | Cost |

| Controlled pilot | One workflow, one agent, read or draft authority, one major integration, RAG, approval queue, basic monitoring | 12–16 weeks | $70,000–$110,000 |

| Production departmental platform | Two to four agents, two to four integrations, HITL workflows, role-based access, complete evaluation, MLOps | 18–26 weeks | $120,000–$200,000 |

| Multi-agent regional bank platform | Four to eight agents, four to seven integrations, reusable control plane, advanced observability, multiple business lines | 24–36 weeks | $210,000–$300,000 |

2. Development Phase Breakdown

The aggregate financial budget scales cleanly across specialized engineering milestones.

- Workflow discovery and authority design: $6,000–$12,000

- Architecture, security, and compliance blueprint: $8,000–$18,000

- RAG, knowledge base, and banking data layer: $10,000–$28,000

- Core, LOS, CRM, AML, and vendor integrations: $14,000–$70,000

- Agent development and orchestration: $16,000–$55,000

- Evaluation, red teaming, compliance testing, and UAT: $8,000–$35,000

- Deployment, observability, and MLOps: $8,000–$25,000

Importantly, phase maximums should not be added mechanically. In practice, the selected project tier strictly constrains the total number of live core integrations, active agents, testing environments, and automated workflows.

3. What Pushes The Cost Toward $300,000

Furthermore, certain advanced structural capabilities will naturally drive infrastructure costs toward the top of the estimation bracket:

- Legacy Overheads: Synchronizing multiple legacy cores or connecting disparate acquired-bank accounting systems.

- Write Access Permissions: Activating high-risk write access rails or deploying real-time domestic payment tools.

- Identity Complexity: Structuring complex customer-identity resolution frameworks across several loan products.

- Processing Requirements: Ingesting high-volume document processing pipelines under private-cloud deployment parameters.

- Advanced Data Mapping: Utilizing advanced graph models alongside multi-state policy retrieval networks.

- Tenancy Extensions: Deploying multilingual customer channels, establishing white-label tenancy boundaries, and securing independent model reviews.

Ongoing Maintenance Costs

Ultimately, financial institutions must budget 15%–25% of the initial system build cost per year for ongoing operational upkeep. This recurring baseline cover ensures reliable long-term functionality:

Custom banking AI agent development investment scales directly with the depth of active ledger write permissions and core systems complexity. By starting with focused, read-and-draft workflows, regional banks can establish clear operational ROI before expanding automation budgets.

5 Agentic AI Banking Platforms Regional Banks Can Study

Regional banks can study existing banking AI platforms to understand which capabilities are already commercially available and which requirements still need custom development.

The strongest examples combine banking-specific knowledge, customer and employee agents, human handoffs, core-system integrations, and controlled workflow execution.

However, their scope, customization depth, and operational focus vary significantly.

| Platform | Primary Focus | Best Suited For | Main Limitation For A Custom Build |

| Interface.ai BankGPT | Customer service, collections, employee assistance | Community banks and credit unions | Primarily centered on predefined banking agents |

| Posh AI | Voice, digital service, knowledge, and outreach | Community and regional financial institutions | Strongest in customer and employee interaction workflows |

| Glia Banking AI Workforce | Voice, digital service, staff copilots, analytics | Regional banks and credit unions | Focuses mainly on frontline interactions |

| Kasisto KAI | Conversational banking and personalized engagement | Retail banks, community banks, and credit unions | Less focused on back-office agent orchestration |

| Backbase AI-Native Banking OS | Frontline journey orchestration across bank systems | Mid-size and large retail banks | Broader implementation scope and platform dependency |

Therefore, regional banks should not ask which platform has the longest feature list. They should compare where each platform stores workflow state, how it controls agent actions, which core systems it can access, whether approval logic can be customized, and who owns the resulting data, policies, integrations, and audit records.

Build Custom AI Agents For Regional Banks With Intellivon

Build custom AI agents with Intellivon when your regional bank needs controlled automation across legacy cores, lending systems, compliance platforms, customer channels, and internal operations.

Intellivon designs the shared agent infrastructure first, then adds narrowly scoped agents that follow bank-defined policies, permissions, approval requirements, and audit standards.

Elite Engineering Capabilities For Regulated Environments

With over 11 years of deep industry expertise, 500+ successfully delivered enterprise AI installations, and an elite squad of 200+ specialized engineering practitioners, Intellivon bridges the gap between complex legacy banking limitations and modern, autonomous infrastructure.

- Workflow & Authority Design: We meticulously map permitted, approval-gated, and prohibited actions, establishing rigid boundaries for every software assistant.

- Regional Bank Architecture: Our teams build specialized RAG pipelines, model routers, orchestration matrices, policy engines, and immutable audit controls natively.

- Core Connectivity: We engineer secure API adapters to seamlessly integrate platforms with Jack Henry, Fiserv, FIS, Temenos, Finastra, CRM panels, and payment rails.

- Governed AI Guardrails: Our system architecture purposefully separates deterministic banking compliance rules from probabilistic language model outputs.

- Production Evaluation: Every deployment runs through intense validation suites, stress-testing retrieval accuracy, tool payloads, role permissions, and error exceptions.

- Deployment Support: We deploy mature MLOps automation, real-time observability dashboards, structural kill switches, and structured authority expansion roadmaps.

Ultimately, by leveraging hundreds of thousands of accumulated engineering hours alongside seasoned ex-MAANG technical specialists, we provide financial institutions with a robust, production-ready environment built to withstand rigorous regulatory audits while significantly compressing operational timelines.

Plan a regional bank AI agent built around your workflow, core environment, compliance responsibilities, and authority model.

Conclusion

Deploying custom AI agents in banking architectures allows mid-size financial institutions to secure enterprise-grade automation without sacrificing regulatory safety. Isolating generative execution layers inside structured state machines isolates operational risk while keeping compliance officers securely in the loop.

Ultimately, building a centralized, audited control plane yields definitive efficiencies across legacy core systems, positioning regional banking networks to confidently outpace legacy operational limitations.

FAQs

Q1. How Many Agents Should A Regional Bank Build First?

A1. Start with one to three agents inside a single workflow, rather than an enterprise-wide collection of autonomous workers. Furthermore, add a second agent only when it requires entirely different tools, permissions, prompts, models, or evaluation rules. Otherwise, a single agent with deterministic workflow states remains much easier to validate, monitor, and operate safely.

Q2. Can Regional Bank Agents Integrate With Jack Henry, Fiserv, And FIS?

A2. Yes, you can integrate them through official APIs, approved middleware, event interfaces, batch integrations, or vendor-specific connectors. However, the available operations depend heavily on the bank’s core edition, licensing, environment, and vendor approvals. Consequently, begin with read-only access, then expose narrow write tools after validating authorization, rollback, and idempotency.

Q3. Where Does A Banking AI Agent Store Its Memory?

A3. Store active task states inside a bank-controlled workflow database. Meanwhile, retrieve customer context directly from primary systems of record when required. Keep policy knowledge in a versioned RAG repository, and never store unrestricted customer records inside conversational memory. Ultimately, apply encryption, retention, and deletion rules across every category.

Q4. Does AI Agent Development For Community Banks And Credit Unions Require A Private LLM?

A4. Not necessarily. Use a private or self-hosted model only when data residency, contractual restrictions, latency, or transaction volumes strictly justify it. Alternatively, many institutions can leverage a hosted model through private networking and zero-data-training terms. Consequently, keep sensitive fields outside prompts to easily shift providers if needed.

Q5. Does SR 11-7 Apply To Custom Agentic AI Banking Assistants?

A5. Banks should not frame these systems around legacy “SR 11-7 compliance.” Notably, SR 26-2 superseded SR 11-7 in April 2026, explicitly stating that generative and agentic AI are outside its current formal scope. Nevertheless, institutions must still apply risk-appropriate governance, effective challenge, validation, and consumer-protection controls based on materiality.

Q6. What Is The Biggest Integration Risk In A Regional Bank AI Automation Build?

A6. The largest risk is assuming that every connected legacy system contains consistent, real-time customer data. Because regional banks operate several vendor platforms with different identifiers and business-day behaviors, inconsistencies are common. Thus, you must build a canonical data model and test stale data, duplicate events, and partial writes before production.

To Sum It Up:

- A banking agent should never receive more system authority than the employee role responsible for reviewing its work.

- Regional banks should start with evidence preparation and exception handling before autonomous credit or payment execution.

- RAG retrieves policy, but a deterministic policy engine still decides whether the next action is permitted.

- The most expensive part of a banking agent build is often core integration and control design, not the LLM.

- Banks that build a reusable control plane can add later agents without rebuilding security, approvals, and audit infrastructure.