The way companies provide credit to customers and partners has changed significantly. What used to take weeks of underwriting and manual checks can now happen in real time, done intelligently, within the rules, and on a large scale. Buy Now, Pay Later is no longer just a trend for consumers. At the enterprise level, it has become an important financial tool. Companies in manufacturing, B2B commerce, healthcare, and logistics are integrating flexible payment options directly into their purchasing and sales processes.

Most old payment systems were not made for this. This is because they manage transactions but struggle with changing credit processes, agreements with multiple parties, immediate risk assessments, or varying regulations across different areas.

At Intellivon, we create enterprise BNPL infrastructure that organizations can use confidently on a large scale. This blog outlines the platform features that distinguish a ready-to-use BNPL infrastructure from a collection of payment tools that fail to meet the demands of large companies.

Why BNPL Is Becoming Core Payment Infrastructure

Modern financial ecosystems face an unprecedented regulatory burden that traditional systems simply cannot shoulder. Consequently, leading fintech enterprises are prioritizing RegTech integration to transform compliance from a bottleneck into a competitive strategic advantage.

The global BNPL market is projected to reach $509.2 billion in 2026, growing at an annual rate of 18.9%. After a 25.3% CAGR between 2022 and 2025, it is expected to expand to $1 trillion by 2031.

Modern commerce now treats credit as a fluid feature rather than a standalone banking product. Therefore, integrating BNPL directly into the core payment stack allows enterprises to capture higher conversion rates and larger average order values.

1. Growth of Embedded Credit in Digital Commerce

Embedding credit options directly into the checkout flow removes the psychological friction of high-cost purchases. Consequently, consumers view these installments as a budgeting tool rather than a traditional debt obligation.

This shift creates a seamless bridge between a customer’s immediate needs and their long-term purchasing power.

2. Enterprises Prefer Infrastructure Over Plug-Ins

Standard plug-ins often lead to fragmented data and a disjointed user experience that alienates high-value customers. However, custom infrastructure provides complete control over the branding, data ownership, and underwriting logic.

This level of technical autonomy ensures the payment experience aligns perfectly with your existing enterprise ecosystem.

3. Limits of Consumer-Focused BNPL Tools

Basic consumer apps frequently prioritize their own brand recognition over the merchant’s long-term relationship with the buyer. These tools also lack the sophisticated API flexibility required to handle complex B2B transactions or multi-entity accounting.

Furthermore, relying on third-party apps often results in losing critical customer insights to a potential competitor.

4. BNPL as a Strategic Financial Product Layer

Positioning credit as a strategic layer allows your organization to experiment with dynamic pricing and loyalty incentives. This infrastructure supports various lending models, ranging from interest-free short-term cycles to longer-term interest-bearing loans.

Consequently, the platform becomes a versatile engine for revenue growth rather than just a simple checkout alternative.

Integrating BNPL at the infrastructure level transforms how your business interacts with capital and customer trust. It is the definitive move for leaders who want to own their financial future.

What Is An Enterprise BNPL Infrastructure Platform?

An enterprise BNPL infrastructure platform provides the technical foundation for large organizations to offer embedded financing. This ecosystem integrates directly into existing checkout or procurement workflows. It manages the entire credit lifecycle through automated APIs.

These systems handle real-time risk assessment, loan servicing, and merchant settlements at high volumes. Large companies use this infrastructure to launch white-labeled lending solutions without rebuilding their core banking software.

Consequently, it bridges the gap between traditional enterprise resource planning and modern financial services.

BNPL Infrastructure vs BNPL Consumer Apps

BNPL is often associated with consumer-facing apps. However, large fintech companies and payment providers operate at a different layer. Instead of building only consumer apps, they develop BNPL infrastructure platforms that enable merchants, fintech products, and marketplaces to offer installment financing.

Understanding this distinction is important. A consumer BNPL app focuses on the user experience, while BNPL infrastructure focuses on credit decisioning, payment orchestration, and financial governance at scale.

Key Differences Between BNPL Infrastructure and Consumer Apps

| Feature | BNPL Infrastructure Platform | BNPL Consumer App |

| Primary Purpose | Provides lending and payment infrastructure for fintechs and merchants | Allows consumers to access installment payments during purchases |

| Target Users | Fintech platforms, lenders, payment providers, and marketplaces | Individual shoppers making purchases |

| Core Function | Credit decisioning, loan servicing, risk management, and merchant integrations | Consumer checkout financing and repayment management |

| Integration | API-based integrations with merchant systems and fintech platforms | Mobile or web application used directly by customers |

| Scalability | Built to support large transaction volumes across multiple merchants | Designed mainly for individual consumer usage |

| Compliance | Includes regulatory controls, audit trails, and governance frameworks | Focuses primarily on consumer payment convenience |

| Data Capabilities | Advanced analytics for credit risk, portfolio monitoring, and fraud detection | Limited analytics mainly for user transactions |

In simple terms, BNPL consumer apps deliver the experience, while BNPL infrastructure platforms power the financial system behind that experience. Enterprises building fintech products typically focus on infrastructure because it supports credit decisioning, merchant integrations, and regulatory compliance at scale.

BNPL as a Credit Orchestration Layer

In enterprise fintech systems, BNPL operates as a credit orchestration layer that coordinates lending decisions, payment processing, and repayment management during a transaction.

Instead of functioning as a simple checkout feature, the platform connects credit risk engines, identity verification systems, payment networks, and merchant integrations in real time.

As a result, fintech apps and payment platforms can offer installment financing while maintaining control over underwriting rules, risk exposure, and regulatory compliance.

How BNPL Infrastructure Connects Payments and Lending

BNPL infrastructure bridges the gap between payment processing and short-term lending within a single transaction flow. When a customer selects BNPL at checkout, the platform evaluates credit risk, approves the installment plan, pays the merchant upfront, and manages the repayment schedule.

As a result, fintech platforms can embed lending directly into payment experiences while maintaining control over credit decisioning, settlement processes, and repayment tracking.

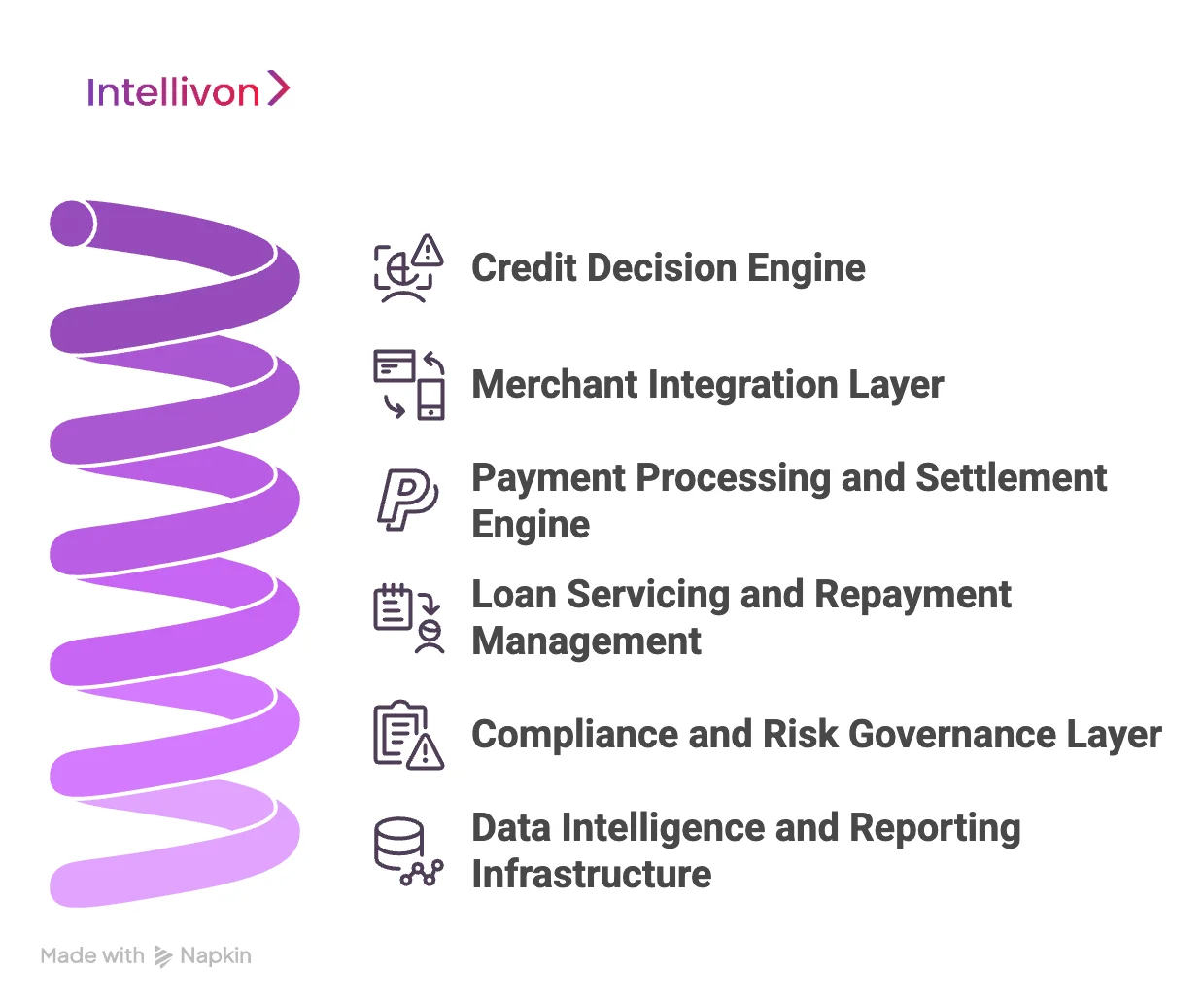

Core Architecture of a BNPL Infrastructure Platform

A robust BNPL architecture must act as a high-performance bridge between consumer demand and institutional capital. Therefore, the system relies on a modular framework that balances rapid transaction speeds with rigorous financial oversight.

1. Credit Decision Engine

The heart of the platform evaluates borrower risk using real-time data and proprietary scoring models. Consequently, it moves beyond traditional credit scores by analyzing alternative data points like purchase history or behavioral patterns.

This high-speed assessment ensures that credit approvals happen in milliseconds without compromising the quality of the loan book.

2. Merchant Integration Layer

Enterprises require a flexible interface that connects diverse storefronts to the central lending engine. This layer provides standardized APIs and SDKs that allow developers to deploy installment options across web, mobile, and physical terminals.

However, it remains light enough to prevent any negative impact on the merchant’s page load speeds or checkout performance.

3. Payment Processing and Settlement Engine

Managing the actual movement of funds requires a reliable engine capable of handling split payments and merchant payouts. The system must coordinate between bank rails, card networks, and internal ledgers to ensure every cent is accounted for.

Furthermore, automated reconciliation reduces the administrative burden on your finance team by matching every transaction to its specific repayment schedule.

4. Loan Servicing and Repayment Management

Once a purchase is finalized, the platform transitions into an active loan management phase. It handles automated recurring billing, sends proactive payment reminders, and manages the logic for late fees or interest accrual.

This proactive approach minimizes delinquency rates while maintaining a positive relationship with the consumer through transparent communication.

5. Compliance and Risk Governance Layer

Every installment loan must adhere to strict regional lending laws and consumer protection acts. Therefore, this layer embeds KYC (Know Your Customer) and AML (Anti-Money Laundering) checks directly into the user onboarding flow.

It ensures that your enterprise remains fully compliant with evolving financial regulations across multiple international jurisdictions simultaneously.

6. Data Intelligence and Reporting Infrastructure

High-level decision-makers rely on granular visibility to optimize their lending strategies and capital allocation. This infrastructure aggregates transaction data into actionable dashboards that track portfolio health, conversion metrics, and default risks.

Consequently, it transforms raw financial data into a strategic asset that informs future product development and market expansion.

Building a BNPL platform on these core pillars ensures that your financial ecosystem is both resilient and infinitely scalable. It is the architectural blueprint for a modern, credit-enabled enterprise.

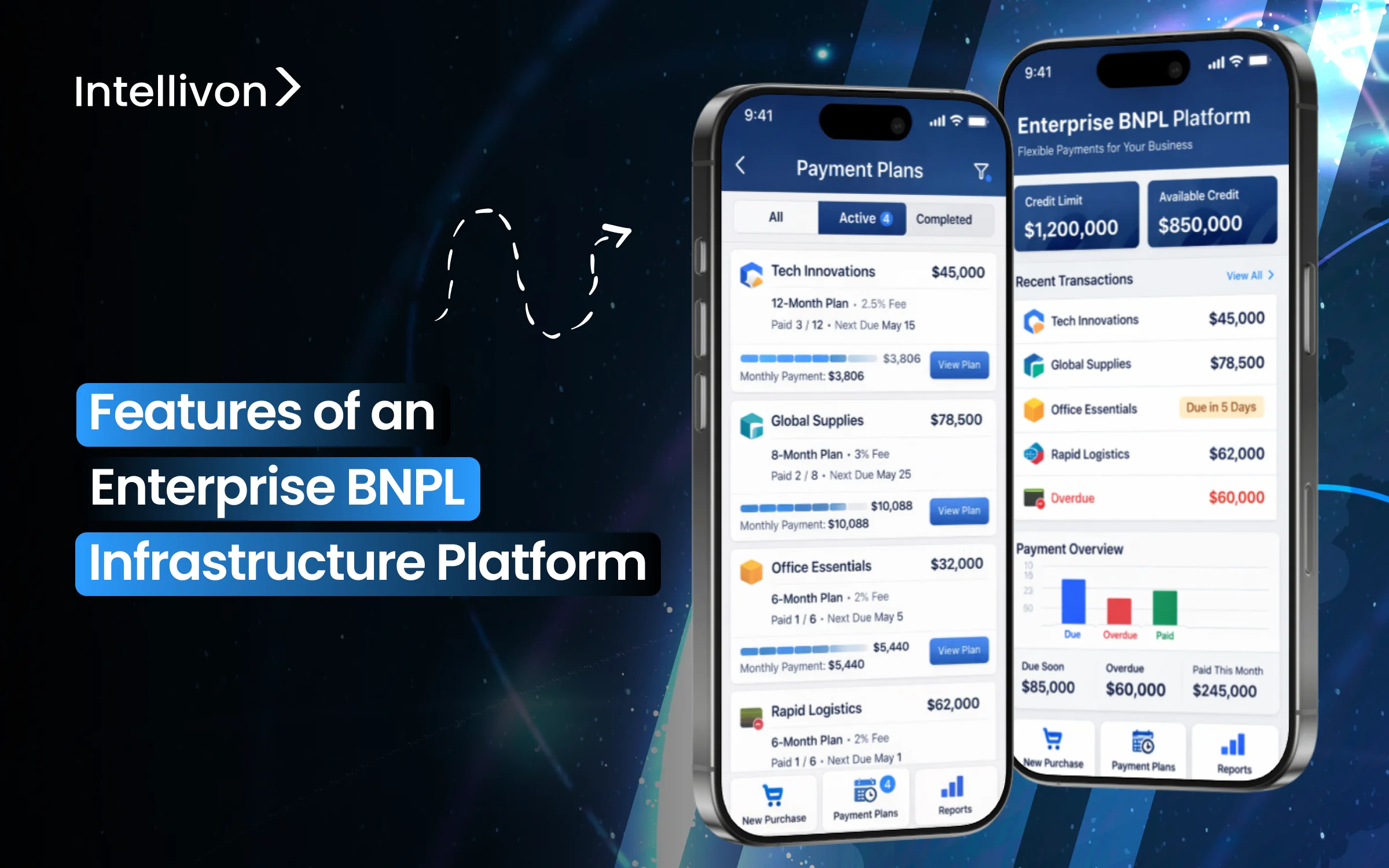

Essential Features of an Enterprise BNPL Platform

An enterprise-grade platform distinguishes itself through deep customization and the ability to handle extreme transaction loads.

Consequently, the following features represent the non-negotiable building blocks for any organization aiming to own its credit ecosystem.

1. Real-Time Credit Risk Decisioning

Precision in lending depends on the ability to analyze a borrower’s profile within seconds of a request. Therefore, the platform utilizes machine learning to evaluate traditional credit data alongside alternative behavioral signals.

This results in highly accurate approvals that protect your margins while maximizing the volume of successful checkouts.

2. Configurable Installment Plan Engine

Different products and customer segments require varied financial terms to remain attractive. This engine allows you to toggle between interest-free “Pay in 4” models and longer-term monthly financing options.

However, the system remains flexible enough to update these parameters instantly across your entire network without requiring a code deployment.

3. Merchant Onboarding and Partner APIs

Scaling a BNPL network requires a frictionless way for new partners to join your ecosystem. Specialized APIs automate the vetting process for new merchants, allowing them to integrate your payment options in hours rather than weeks.

This speed to market is essential for capturing market share in competitive retail environments.

4. Multi-Currency Payment Processing

Global enterprises must support the local currencies of their international customer base to avoid conversion friction. The platform handles real-time exchange rates and cross-border settlement logic automatically.

Furthermore, this feature ensures that your financial reporting remains consolidated regardless of where the individual transaction originated.

5. Automated Repayment Scheduling

Consistency in collections is the primary driver of a sustainable lending portfolio. The system sets up automated billing cycles at the moment of purchase, linking directly to the consumer’s preferred payment method.

Consequently, this reduces the likelihood of missed payments and ensures a predictable cash flow for your treasury department.

6. AI-Driven Fraud and Identity Checks

Security must be invisible yet impenetrable to maintain a smooth user experience. AI-driven modules verify identities in real-time by checking for synthetic ID patterns and device fingerprinting.

This proactive layer blocks fraudulent attempts before they can impact your bottom line, preserving the integrity of the platform.

7. Delinquency and Collections Management

Managing late payments requires a delicate balance between financial recovery and brand reputation. Automated workflows trigger gentle reminders via SMS or email when a payment is overdue.

If a debt remains unpaid, the system can escalate to more formal collections protocols based on pre-defined business rules.

8. Merchant Settlement and Reconciliation

Accurate payouts are vital for maintaining strong relationships with your retail partners. This feature automates the calculation of merchant fees and the distribution of funds after a successful transaction.

In addition, it provides a transparent ledger that allows merchants to reconcile their accounts without manual intervention.

9. BNPL Product Configuration Controls

Administrators need a centralized dashboard to manage the high-level logic of the credit product. You can set minimum purchase thresholds, define maximum credit limits, or adjust interest rates based on market conditions.

This control ensures that your BNPL offering remains a dynamic tool that responds to your enterprise’s evolving strategic goals.

By integrating these essential features, your organization moves beyond basic lending into a sophisticated, data-driven financial powerhouse. These tools provide the necessary control to scale safely in a volatile market.

Risk and Compliance Features Enterprises Require

Operating a lending platform demands a rigorous approach to global financial regulations and consumer safety.

Consequently, enterprise-grade BNPL infrastructure must embed compliance directly into its code to prevent legal exposure and financial loss.

1. KYC and Identity Verification Infrastructure

Verifying the identity of a borrower is the first line of defense against systemic fraud. Therefore, the platform integrates with global databases to perform instant document verification and biometric checks.

This seamless process ensures that your organization meets “Know Your Customer” standards without adding unnecessary friction to the user experience.

2. Responsible Lending Compliance Controls

Enterprises must ensure that their credit products do not lead consumers into unsustainable debt cycles. These controls include automated affordability assessments that evaluate a user’s current financial health before approving new installments.

Furthermore, this proactive stance builds long-term brand trust and ensures compliance with evolving consumer protection regulations.

3. AML Monitoring for BNPL Transactions

Lending platforms can often become targets for sophisticated money laundering schemes if left unmonitored. Robust Anti-Money Laundering (AML) modules analyze transaction velocity and funding sources to flag suspicious activities in real-time.

Consequently, your enterprise can maintain a secure ecosystem that satisfies the stringent requirements of banking partners and regulators.

4. Audit Trails for Regulatory Reporting

Transparency is a core requirement for any financial entity facing periodic regulatory audits. The infrastructure maintains an immutable log of every credit decision, payment transaction, and customer communication.

Therefore, generating comprehensive reports for state or federal authorities becomes a simple, automated task rather than a manual administrative burden.

5. Data Privacy and Consumer Protection Controls

Handling sensitive financial data requires the highest level of encryption and strict access management protocols. The platform must adhere to regional standards such as GDPR or CCPA to ensure that consumer rights are always protected.

In addition, these controls provide users with clear disclosures regarding their loan terms, interest rates, and data usage rights.

By prioritizing these compliance features, your organization creates a resilient foundation for sustainable financial innovation. This focus on risk management ensures that your growth is both rapid and legally secure.

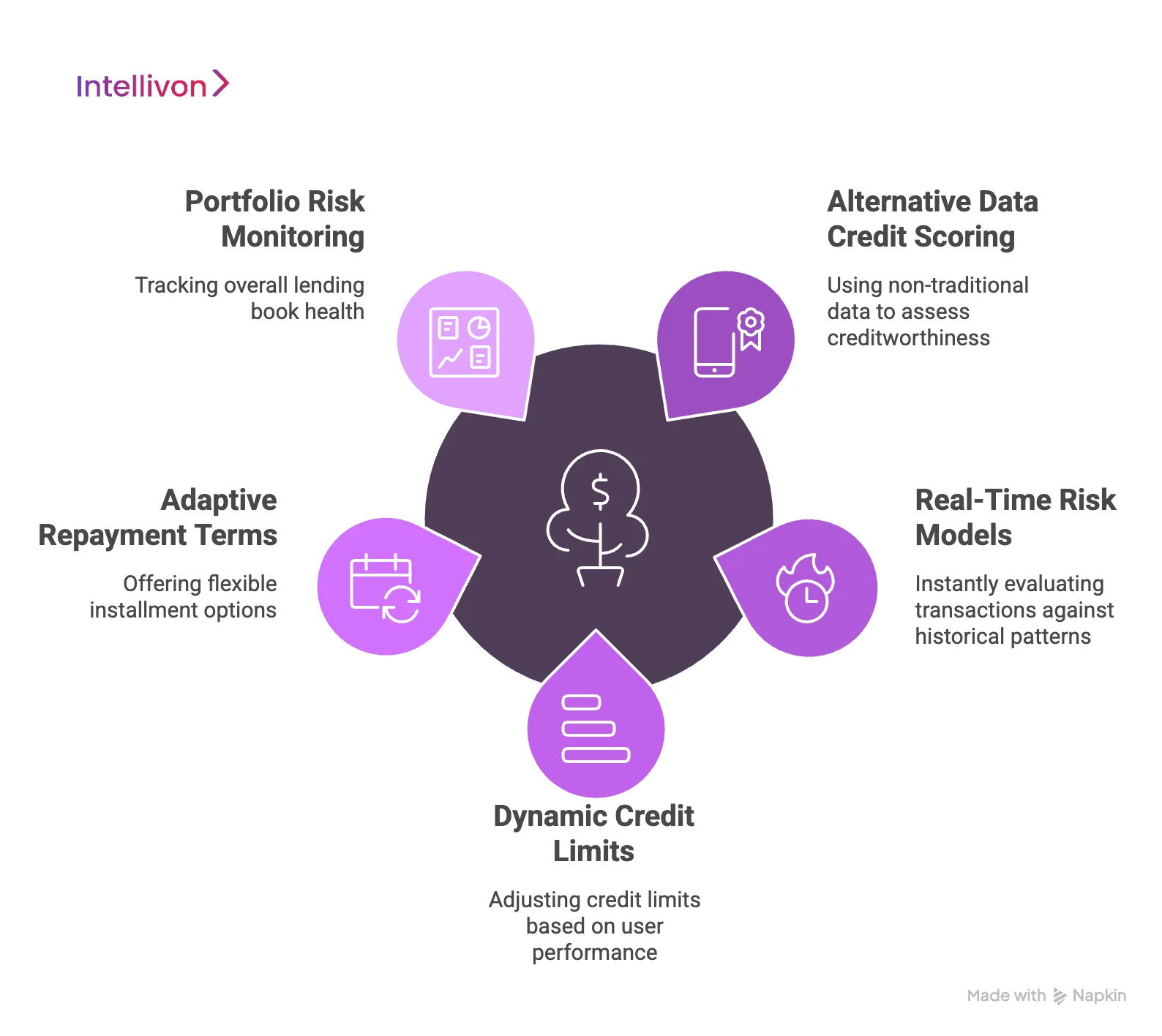

Credit and Underwriting Capabilities Inside BNPL

Modern credit evaluation moves beyond static scores to provide a holistic view of borrower reliability.

Consequently, enterprise BNPL infrastructure utilizes sophisticated modeling to approve more customers while strictly controlling for default risks.

1. Alternative Data Credit Scoring

Traditional credit bureaus often fail to capture the nuances of a modern consumer’s financial behavior. Therefore, this platform ingests alternative data points such as utility payments, digital footprint, and recurring subscription history.

This wider lens allows your enterprise to safely extend credit to “thin-file” customers who are often overlooked by legacy banks.

2. Real-Time Risk Models

Static risk assessments are unable to react to the rapid shifts of a digital commerce environment. Instead, these models utilize streaming data to evaluate every transaction against thousands of historical patterns instantly.

Furthermore, this high-speed analysis ensures that credit decisions are made in milliseconds, preserving the “buy now” impulse of the shopper.

3. Dynamic Credit Limits

Fixed credit ceilings can often frustrate high-value customers or overextend those with lower financial stability. Consequently, the system adjusts credit limits in real-time based on the user’s repayment performance and current shopping context.

This tailored approach minimizes the risk of default while encouraging responsible spending growth among your most loyal users.

4. Adaptive Repayment Terms

Flexibility in repayment is a key driver of long-term customer satisfaction and brand loyalty. The platform can automatically suggest different installment lengths based on the total cart value or the borrower’s risk profile.

However, it maintains strict guardrails to ensure that these terms always align with your internal capital requirements and risk appetite.

5. Portfolio Risk Monitoring

Executive leaders require a bird’s-eye view of the entire lending book to maintain financial health. This capability provides real-time dashboards that track delinquency trends, loss ratios, and capital utilization across different merchant categories.

Therefore, you can make data-driven adjustments to your underwriting criteria before small trends turn into significant institutional risks.

By embedding these advanced underwriting capabilities, your organization transforms credit from a binary “yes/no” into a precise strategic tool. This level of sophistication ensures that every loan issued contributes to sustainable, long-term profitability.

Consumer Experience Features of Modern BNPL Systems

The success of any financial product depends entirely on the quality of its user interface. Consequently, enterprise BNPL systems prioritize a frictionless journey that turns a complex credit transaction into a simple checkout step.

1. Instant Checkout Financing

Speed is the ultimate currency in digital commerce and determines the final conversion rate. Therefore, the platform completes identity checks and credit scoring within the existing checkout flow.

This seamless integration ensures that customers can finalize their purchase in seconds without ever leaving your branded environment.

2. Transparent Installment Schedules

Clarity regarding future financial obligations builds deep trust between the consumer and the brand. Every loan includes a clear breakdown of payment dates, amounts, and any applicable interest or fees.

Furthermore, this transparency eliminates the “hidden fee” anxiety that often leads to cart abandonment and negative reviews.

3. Flexible Repayment Management

Life events often require a degree of flexibility in how a consumer manages their debt. The system allows users to change their payment dates or pay off their balance early.

However, these adjustments occur within pre-defined risk guardrails to ensure your enterprise maintains a predictable and healthy cash flow.

4. Customer Self-Service Portals

Empowering users to manage their own accounts reduces the strain on your internal support teams. These portals provide a centralized view of all active loans, historical payments, and available credit limits.

Consequently, customers feel more in control of their financial journey, which directly correlates to higher long-term loyalty.

5. Real-Time Payment Notifications

Proactive communication prevents missed payments and keeps the consumer engaged with the platform. Automated alerts via SMS or push notifications remind users of upcoming installments several days in advance.

In addition, instant confirmation of successful payments provides immediate peace of mind and reinforces a positive repayment habit.

By focusing on these consumer-centric features, your organization creates a premium financial experience that drives repeat business. It is the definitive way to bridge the gap between utility and delight.

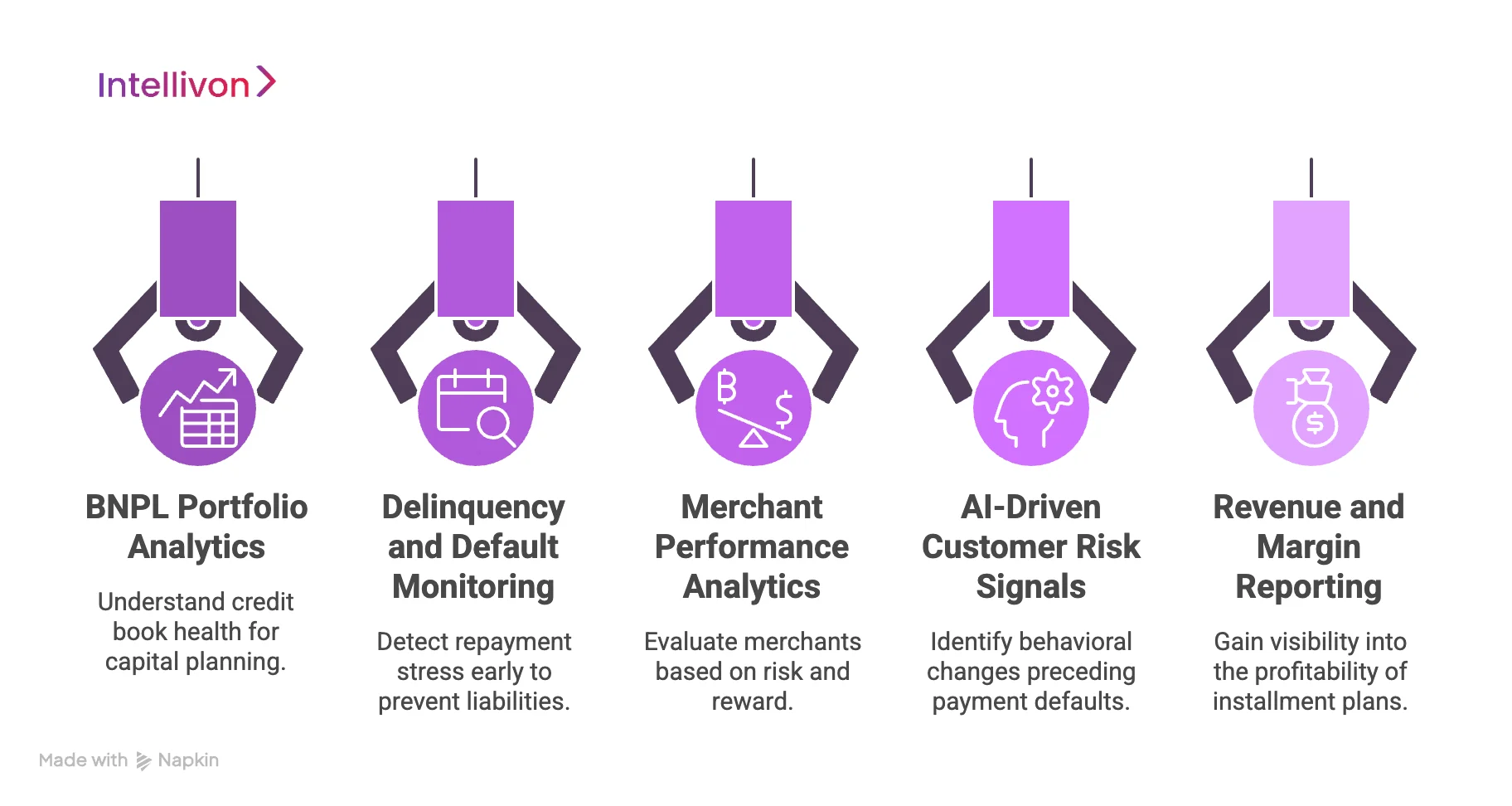

Data Intelligence Features in BNPL Platforms

Decision-makers require granular visibility to balance aggressive growth with institutional stability. Therefore, the data intelligence layer transforms millions of raw data points into a strategic compass for your entire lending operation.

1. BNPL Portfolio Analytics

Understanding the overall health of your credit book is essential for long-term capital planning. This feature provides a high-level view of total originations, active balances, and weighted average interest rates.

Consequently, your treasury team can make informed decisions about credit expansion or contraction based on real-time market performance.

2. Delinquency and Default Monitoring

Early detection of repayment stress prevents minor trends from becoming significant balance sheet liabilities. The system tracks “Days Past Due” (DPD) across various demographic and geographic cohorts.

Furthermore, these insights allow you to adjust underwriting models instantly when specific segments show signs of increased financial volatility.

3. Merchant Performance Analytics

Not all retail partners bring the same level of risk or reward to your platform. This analytics module evaluates each merchant based on their average order value, return rates, and customer repayment history.

Therefore, you can identify high-performing partners and optimize your commission structures to favor the most profitable relationships.

4. AI-Driven Customer Risk Signals

Machine learning models identify subtle behavioral changes that often precede a payment default. These signals might include shifts in shopping frequency, payment method updates, or changes in average transaction amounts.

Consequently, the platform can proactively adjust credit limits or offer tailored repayment plans to mitigate risk before it crystallizes.

5. Revenue and Margin Reporting

Direct visibility into the profitability of every installment plan is vital for your CFO’s office. This reporting engine calculates the net margin by accounting for merchant fees, cost of capital, and expected credit losses.

In addition, it provides a transparent view of how different product configurations impact your bottom line over time.

By leveraging these intelligence features, your organization moves from reactive management to proactive financial leadership. This data-first approach is the hallmark of a truly sophisticated enterprise credit ecosystem.

Infrastructure Capabilities Required at Scale

Enterprise-grade credit systems must maintain perfect reliability even during massive seasonal spikes in transaction volume. Therefore, your underlying architecture requires a resilient, distributed foundation that prioritizes both high throughput and sub-second execution speeds.

1. High-Volume Transaction Processing

Peak shopping events like Black Friday can stress test even the most robust legacy payment systems. Therefore, the platform utilizes elastic scaling to handle sudden surges in concurrent loan applications without slowing down.

This capability ensures that every customer receives a response in real-time, regardless of the global traffic load.

2. API-First BNPL Infrastructure

Modern enterprises rely on a web of interconnected services to deliver a unified customer experience. An API-first approach allows for seamless data exchange between your lending engine, ERP, and CRM systems.

Consequently, developers can build custom front-end experiences while the core credit logic remains centralized and secure.

3. Multi-Region Deployment Architecture

Global operations require data residency compliance and low-latency access for users in different geographic zones. By deploying across multiple cloud regions, the platform ensures that sensitive financial data stays within local legal boundaries.

Furthermore, this distributed footprint provides a natural defense against regional outages or localized network failures.

4. Real-Time Decision Latency Requirements

In the world of digital commerce, a three-second delay can lead to a complete loss of the sale. The credit engine must ingest data, run risk models, and return an approval in under 500 milliseconds.

This near-instant execution keeps the checkout momentum high and prevents the customer from reconsidering their purchase.

5. Fault-Tolerant Payment Systems

Financial transactions cannot afford a single point of failure in their processing logic. The system incorporates automated failover protocols and idempotent API designs to prevent duplicate charges or lost records.

In addition, persistent event logging ensures that every transaction can be fully recovered and reconciled in the event of a crash.

By investing in these high-scale infrastructure capabilities, your organization builds a future-proof engine for global commerce. This technical excellence is what separates market leaders from those struggling with legacy limitations.

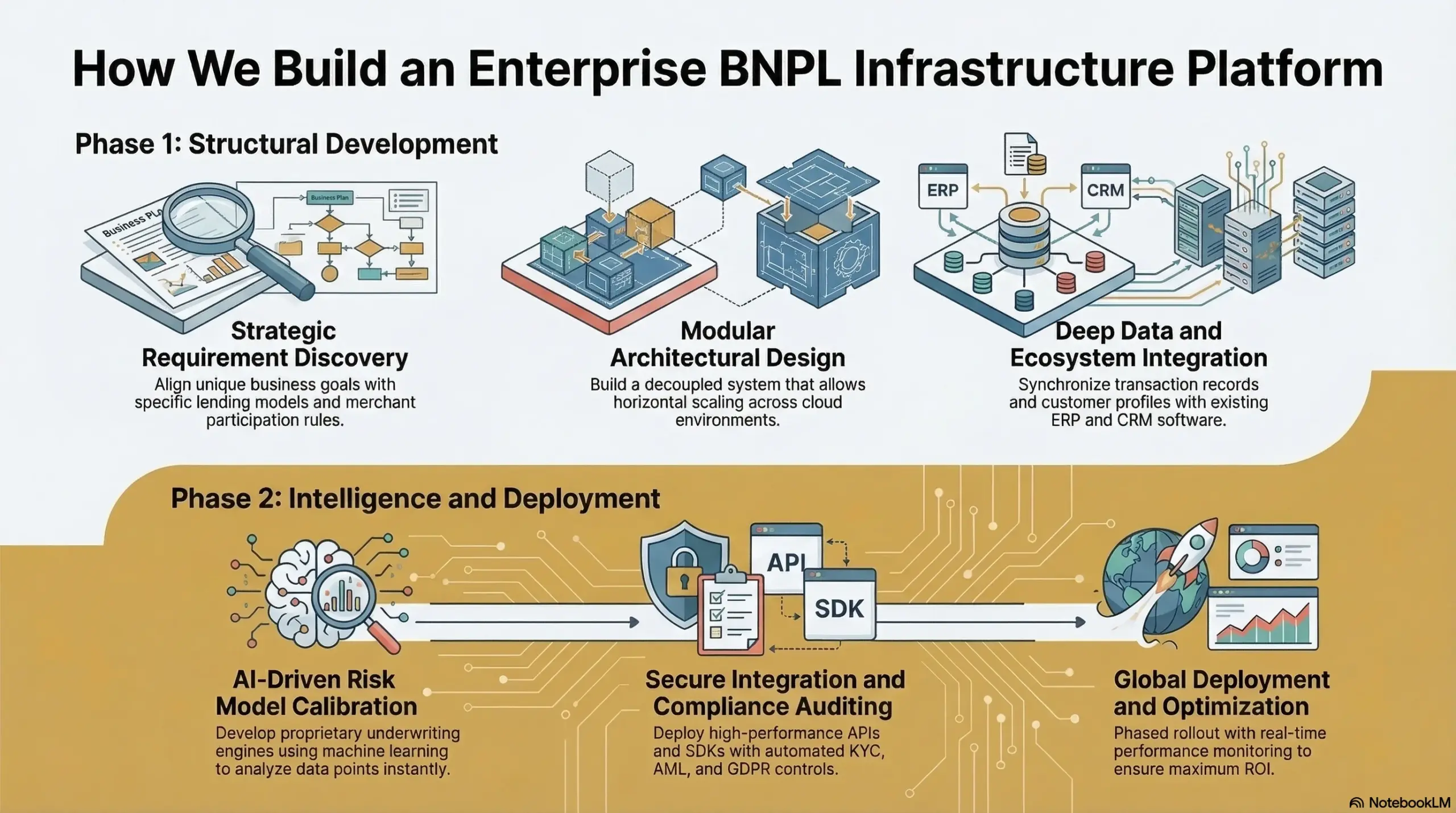

How We Build an Enterprise BNPL Infrastructure Platform

Transforming a traditional payment stack into a credit-enabled powerhouse requires a meticulous, phased architectural approach.

Consequently, Intellivon leverages deep expertise in AI and fintech to deliver a custom, high-performance BNPL ecosystem.

Step 1: Strategic Requirement Discovery

We begin by aligning your unique business goals with the specific needs of your customer segments. Therefore, our team identifies the ideal lending models, interest structures, and merchant participation rules for your organization.

This foundational phase ensures the final product drives measurable growth while fitting your risk appetite.

Step 2: Modular Architectural Design

Our engineers design a decoupled system that separates core ledger functions from the user-facing checkout layers. This modularity allows your enterprise to update individual components without disrupting the entire payment flow.

Furthermore, it provides the necessary flexibility to scale horizontally across different cloud environments as your volume grows.

Step 3: Deep Data and Ecosystem Integration

A successful BNPL platform must communicate fluently with your existing ERP, CRM, and accounting software. Consequently, we build robust data pipelines that synchronize transaction records and customer profiles in real-time.

This integration ensures that your financial reporting remains accurate and your marketing teams stay informed.

Step 4: AI-Driven Risk Model Calibration

We develop proprietary underwriting engines that utilize machine learning to analyze thousands of data points instantly. Therefore, your platform can approve more users with higher precision than traditional credit scoring methods.

These models are continuously refined to adapt to changing market conditions and consumer behavior patterns.

Step 5: Secure API and SDK Development

Our developers create a suite of high-performance APIs and mobile SDKs for seamless merchant adoption. These tools allow your partners to integrate your BNPL options into their websites or apps with minimal technical effort.

However, we maintain strict security protocols to protect every data packet during the transmission process.

Step 6: Rigorous Compliance and Security Auditing

Before going live, the platform undergoes exhaustive testing for regulatory adherence and data privacy standards. We embed automated KYC, AML, and GDPR controls directly into the core logic of the system.

In addition, third-party security audits ensure that your infrastructure is resilient against modern cyber threats.

Step 7: Global Deployment and Optimization

The final stage involves a phased rollout across your target markets with real-time performance monitoring. We use automated dashboards to track conversion rates, repayment health, and system latency during the initial launch.

Consequently, Intellivon provides continuous optimization to ensure your BNPL platform delivers maximum ROI from day one.

By following this rigorous process, we turn complex financial goals into a high-utility reality for your enterprise. It is the most reliable path to owning a world-class credit infrastructure.

Real-World Examples of BNPL Infrastructure Platforms

Examining established market leaders provides critical insights into how high-scale credit systems operate in the wild. Consequently, these case studies highlight the diverse architectural choices that allow global firms to balance rapid consumer approval with long-term financial stability.

1. How Affirm Built Its BNPL Credit Platform

Affirm distinguishes itself by using a vertically integrated model that handles every aspect of the loan lifecycle in-house. Therefore, they do not outsource critical functions like underwriting or capital market activities to third-party providers.

This level of control allows them to offer highly transparent, fixed-rate installment plans without any hidden late fees for the consumer.

2. Klarna’s Merchant and Consumer Infrastructure

Klarna has evolved into a comprehensive commerce network that connects distribution and capital within a single unified flow. Consequently, their infrastructure actively generates consumer demand through a high-traffic shopping app.

This “checkout as a moat” strategy ensures they remain a dominant player in both the merchant and consumer financial ecosystems.

3. Afterpay’s Installment Payment Network

Afterpay pioneered a simplified “Pay in 4” model that focuses on short-term, interest-free credit for high-frequency retail purchases. Their infrastructure utilizes a robust affiliate marketing model, earning the majority of its revenue from merchant commissions rather than borrower interest.

Furthermore, their automated repayment system ensures that the first installment is collected at the moment of purchase, significantly reducing their initial credit exposure.

4. PayPal Pay Later Infrastructure Model

PayPal leverages its massive existing network of 400 million active accounts to provide instant credit without requiring new user sign-ups. Therefore, their “Pay Later” infrastructure benefits from decades of historical transaction data to inform its real-time risk modeling.

This deep data advantage allows them to offer a highly frictionless experience that integrates perfectly with their world-class fraud detection systems.

In summary, these industry leaders demonstrate that successful BNPL deployment requires a perfect harmony between technical speed and financial oversight. By studying their models, your enterprise can adopt the best practices needed to build a resilient and profitable credit ecosystem.

Conclusion

The shift toward embedded credit is no longer a trend; it is a fundamental requirement for the modern digital economy. Therefore, investing in a robust BNPL infrastructure platform allows your organization to capture new revenue streams, increase customer loyalty, and own the entire financial journey. By prioritizing real-time intelligence, modular architecture, and rigorous compliance, you position your brand at the forefront of the fintech revolution.

At Intellivon, we specialize in building cutting-edge, enterprise-grade AI solutions that power tomorrow’s financial leaders. Our team of strategists and engineers is ready to help you design, deploy, and scale a custom BNPL ecosystem that meets your exact business requirements.

Build an Enterprise BNPL Platform With Intellivon

At Intellivon, BNPL platforms are engineered as enterprise credit infrastructure, not as checkout plugins layered onto existing payment systems. Each platform is designed to coordinate credit decisioning, merchant integrations, installment management, and repayment orchestration across complex fintech environments.

Every solution is built for regulated financial ecosystems. BNPL platforms must process high transaction volumes, evaluate credit risk in real time, integrate with payment networks, and maintain governance across lending operations through compliant, scalable infrastructure.

Why Partner With Intellivon?

- Governance-First BNPL Architecture: BNPL platforms are designed with embedded policy controls, underwriting governance, and role-based access frameworks to maintain accountability across credit and repayment operations.

- AI-Driven Credit Decision Engines: Our systems include real-time credit evaluation models, behavioral risk analysis, and adaptive underwriting logic to approve installment financing while managing portfolio risk.

- Integrated Payment and Lending Infrastructure: BNPL platforms connect payment gateways, merchant checkout systems, and lending workflows, ensuring seamless installment approvals and merchant settlements during transactions.

- Configurable Installment and Repayment Engines: Enterprises can define repayment schedules, installment structures, and credit limits through configurable rule frameworks aligned with lending policies and risk tolerance.

- Provider-Agnostic Merchant and Data Integrations: BNPL platforms integrate with payment processors, identity verification providers, credit bureaus, and financial data sources to support accurate credit decisioning.

- Scalable Infrastructure for BNPL Networks: Architecture supports expanding merchant ecosystems, increasing transaction volumes, and growing lending portfolios without compromising system reliability or decision latency.

Organizations exploring enterprise BNPL platform development can work with Intellivon’s fintech experts to design and deploy a secure, scalable, and credit-ready infrastructure built for modern digital commerce ecosystems.

FAQs

Q1. What technologies are behind the buy now, pay later options?

A1. BNPL platforms rely on several technologies that enable instant credit approvals and installment payments. These systems include credit decision engines, payment processing infrastructure, identity verification tools, and risk monitoring systems.

Q2. What are the benefits of BNPL?

A2. BNPL allows customers to split purchases into smaller payments instead of paying the full amount upfront. As a result, merchants often see higher conversion rates and larger order values. At the same time, fintech platforms can introduce new revenue streams through merchant fees and financing charges.

Q3. What is the business model of BNPL?

A3. Most BNPL providers generate revenue through merchant discount fees, consumer interest charges, and late payment fees. Merchants pay a fee because BNPL often increases sales and checkout completion rates. In some cases, providers also earn revenue from financial partnerships, lending spreads, and data-driven credit services.

Q4. Is the BNPL service suitable for businesses?

A4. Yes, BNPL services can benefit many businesses, especially those operating in e-commerce, marketplaces, fintech apps, and digital payment platforms. By offering installment payments, businesses can make higher-value products more accessible to customers. In addition, BNPL can increase sales conversion while allowing merchants to receive full payment upfront from the financing provider.