In the United States, access to financial data is becoming more organized and regulated. Clearer rules now guide how consumers give permission for their data to be used, and banks, lenders, and wealth platforms all need reliable access to that information. Choosing whether to build or use an account aggregation platform has become a key strategy, and not just a technical decision. While moving quickly is important, having long-term control over data, compliance, and costs matters even more.

Building an account aggregation platform in the US goes far beyond connecting APIs. It means managing user consent, using secure cloud systems, staying ready for audits, and following all regulations. Costs of building such a platform can range from about $70,000 for a basic setup to over $500,000 for a solution that meets full compliance standards. These differences depend on how deeply the platform is designed and the level of risk a business is willing to take.

At Intellivon, data platforms are built to serve as secure, scalable infrastructure for financial organizations. In this blog, we look at what really drives the costs of building an account aggregation platform in the US, and how we build it from scratch.

Key Takeaways Of An Account Aggregation Platform

An account aggregation platform brings financial data from multiple accounts into one secure, unified interface. It pulls information from banks, credit cards, investment accounts, and other financial sources.

As a result, users gain a complete financial picture instead of fragmented snapshots. This consolidated view supports stronger insights for consumers, lenders, and enterprise platforms that rely on accurate, real-time data.

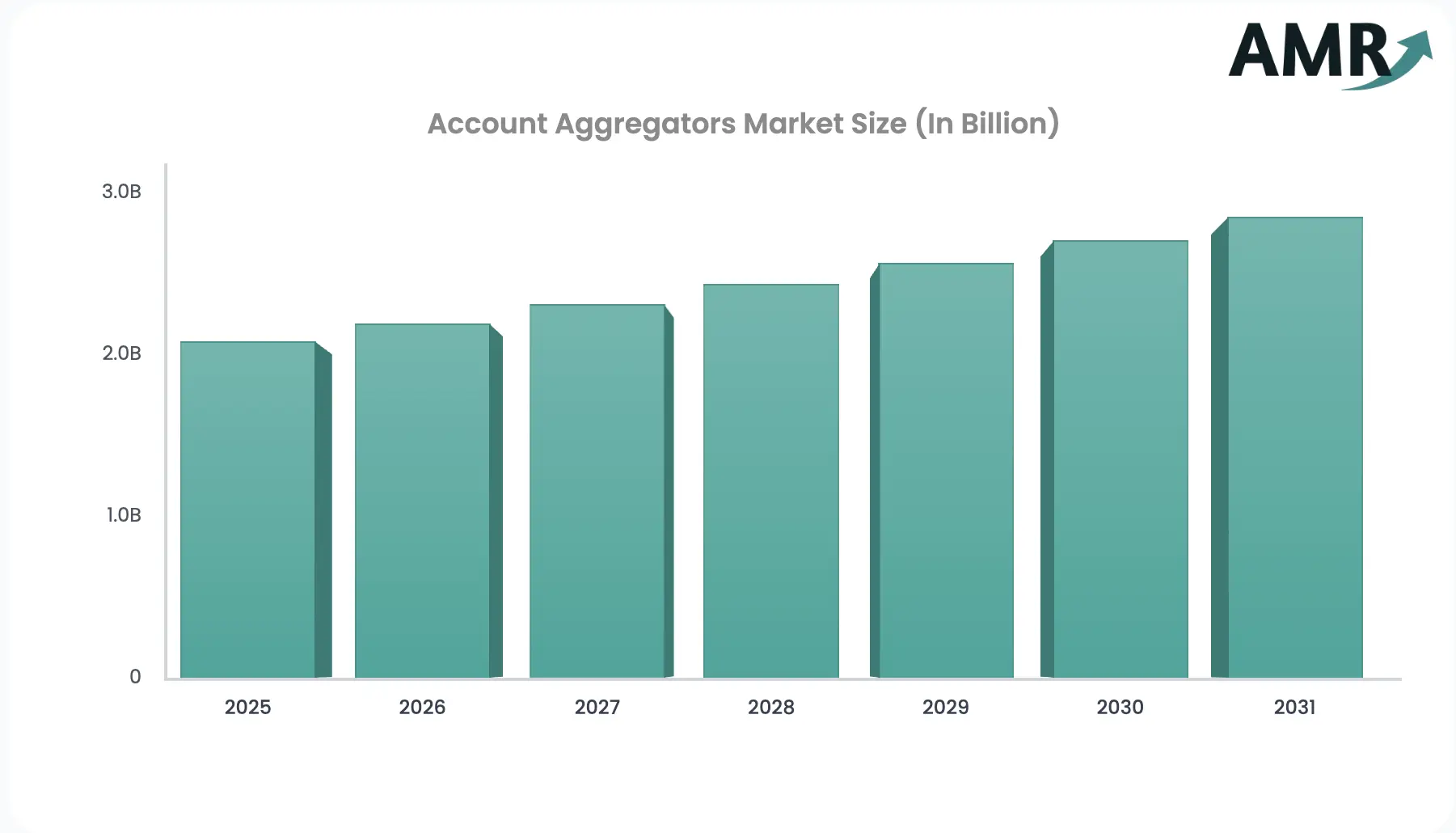

The account aggregator market will reach approximately $2.08 billion in 2025. In addition, analysts expect a compound annual growth rate of 5.4% between 2025 and 2033. This steady expansion reflects increasing enterprise adoption rather than short-term hype.

Therefore, organizations evaluating investment in this space are entering a market with sustained, long-term demand.

Market Insights:

- Regulatory support is driving growth. Open banking frameworks and US data access rules are formalizing secure, API-based financial data sharing.

- Cloud deployment leads adoption. Scalable, real-time cloud infrastructure continues to outpace on-premises systems across fintech ecosystems.

- PFM apps fuel demand. Personal finance management platforms hold about 35% market share, driven by budgeting and analytics features.

What Is an Account Aggregation Platform?

An account aggregation platform collects financial data from multiple accounts and presents it in one unified view. It connects securely to banks, credit cards, investment platforms, and other financial sources through APIs. As a result, users can access complete financial information without logging into separate systems.

Enterprises use this consolidated data to improve decision-making across lending, onboarding, and risk assessment. In addition, it helps power personal finance tools, wealth dashboards, and corporate financial analytics. Instead of relying on fragmented data, organizations gain a real-time financial snapshot. This improves accuracy and operational efficiency.

Simply put, an account aggregation platform acts as a secure bridge between financial institutions and applications. It enables controlled, permission-based data sharing while maintaining privacy and compliance standards.

Account Aggregation Platform Use Cases

Account aggregation platforms create value across multiple enterprise functions. By bringing financial data into one unified layer, they support faster decisions and stronger operational visibility.

1. Digital Banking Applications

Banks use aggregated data to offer customers a consolidated financial view. This improves user experience while enabling smarter product recommendations and engagement.

2. Lending Underwriting Platforms

Lenders rely on verified financial data to assess creditworthiness. Aggregation improves risk evaluation and speeds up loan approval workflows.

3. Wealth Management Dashboards

Advisors gain a complete picture of client assets and liabilities. As a result, portfolio planning becomes more accurate and personalized.

4. Personal Finance Management Tools

These platforms use aggregated data to deliver budgeting insights and spending analytics. This strengthens customer retention and engagement.

5. Corporate Treasury Intelligence

Enterprises use aggregation to track liquidity across institutions. This enhances cash flow planning and financial risk monitoring.

In summary, aggregation platforms turn fragmented financial data into actionable intelligence across enterprise workflows.

Cost Range Of Account Aggregation Platforms in the USA (2026 Estimates)

The cost of building an account aggregation platform depends on how deeply it integrates into enterprise systems. A simple implementation may focus only on data connectivity.

However, a full-scale platform must support compliance, security, and operational resilience. Therefore, investment levels vary based on scope and regulatory readiness.

| Platform Scope | Estimated Cost Range |

| Basic Integration Layer | $70,000 – $120,000 |

| Mid-Level Enterprise Platform | $120,000 – $300,000 |

| Enterprise-Grade Infrastructure | $300,000 – $500,000+ |

Basic solutions connect financial data sources into a unified view. In contrast, mid-level platforms add governance, analytics, and secure orchestration.

Enterprise-grade infrastructure introduces audit readiness, advanced security layers, and scalable cloud architecture.

In summary, cost reflects architectural depth rather than feature count. Organizations that invest in compliance-ready systems often gain stronger long-term control and scalability.

Core Cost Components of Building an Account Aggregation Platform

Cost planning becomes easier when the platform is broken into real build layers. Each layer solves a specific enterprise problem. Some handle connectivity. Others protect data, enforce consent, and keep operations stable.

Therefore, cost depends on how “production-ready” the platform must be. A lightly governed build looks cheaper upfront. However, it often creates higher operational risk later.

Cost Breakdown by Component

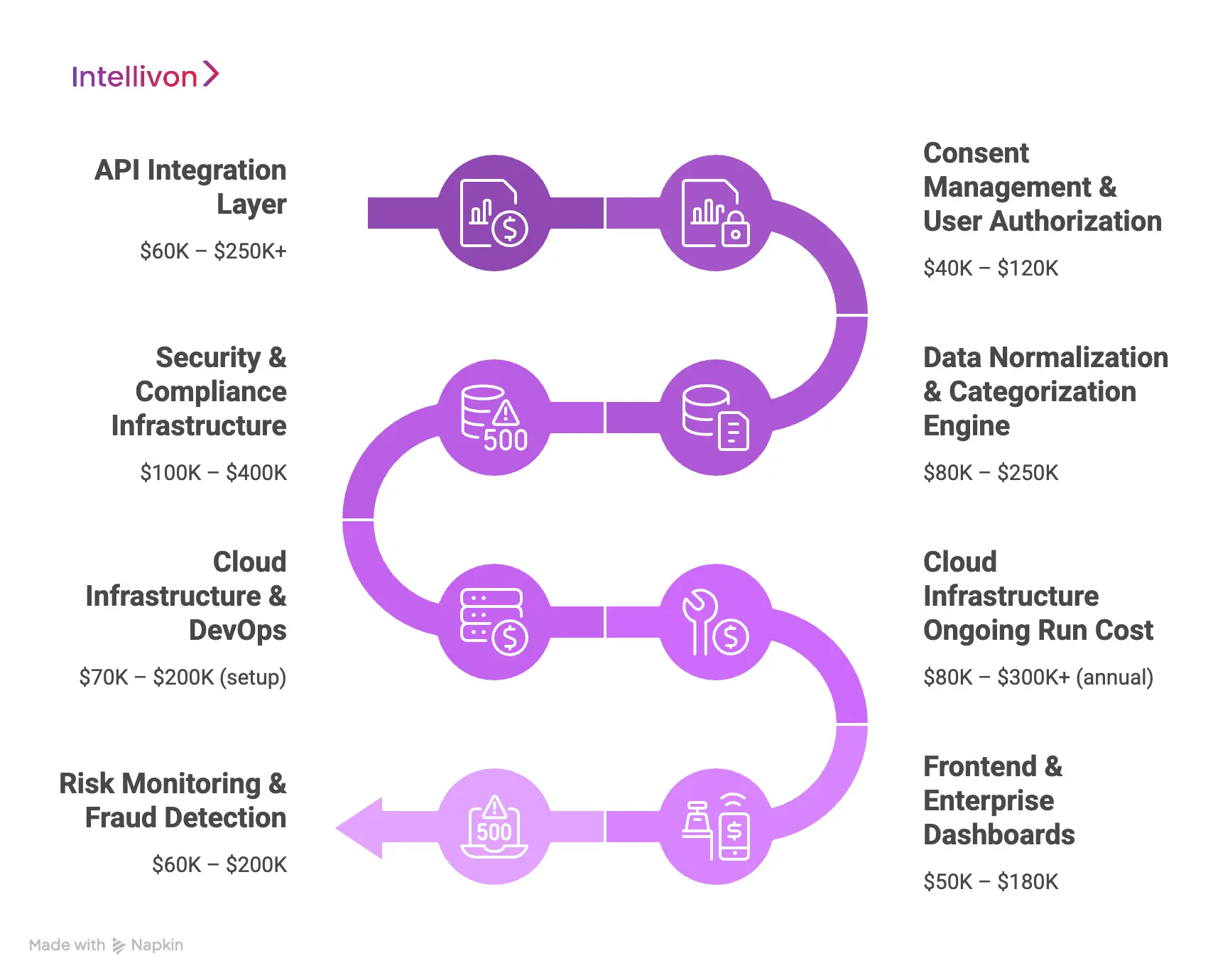

| Component | Estimated Cost |

| API Integration Layer | $60K – $250K+ |

| Consent Management & User Authorization | $40K – $120K |

| Data Normalization & Categorization Engine | $80K – $250K |

| Security & Compliance Infrastructure | $100K – $400K |

| Cloud Infrastructure & DevOps | $70K – $200K (setup) |

| Cloud Infrastructure Ongoing Run Cost | $80K – $300K+ (annual) |

| Frontend & Enterprise Dashboards | $50K – $180K |

| Risk Monitoring & Fraud Detection | $60K – $200K |

In addition, these ranges shift based on integration count, data refresh frequency, and compliance requirements.

1. API Integration Layer

This layer connects to banks and financial data sources. It also manages uptime, retries, and change handling. Therefore, it often becomes one of the biggest cost drivers.

What drives effort:

- Direct bank API integrations and partner onboarding

- Support for aggregator providers and alternatives

- FDX-aligned data access patterns where applicable

- OAuth flows, refresh tokens, and session controls

- Rate limiting, throttling, and API gateway rules

- Versioning to handle bank API changes safely

2. Consent Management & User Authorization

Consent is not a checkbox in the US. It is a governance system. This layer controls who can access data, for what purpose, and for how long.

Key capabilities:

- CFPB Section 1033 readiness and audit-friendly consent records

- OAuth 2.0 authorization with clear permission scopes

- Consent revocation logic that propagates across systems

- User permission dashboards with plain-language controls

- Data minimization to avoid collecting unnecessary fields

3. Data Normalization & Categorization Engine

Raw data arrives in different formats. Normalization turns it into consistent, usable signals. As a result, downstream teams trust dashboards and models.

Core components:

- Transaction parsing and field validation

- Merchant identification and naming cleanup

- Categorization using rules plus ML was useful

- Standardized schemas across institutions and products

- Enrichment for better analytics and decisioning

4. Security & Compliance Infrastructure

This layer protects the platform under real scrutiny. It also reduces vendor risk for enterprise clients. Therefore, it deserves detailed planning from day one.

Security and compliance scope:

- SOC 2 control design and evidence collection readiness

- PCI-DSS alignment when card data enters the environment

- Encryption in transit and at rest with key management

- Zero-trust access controls and network segmentation

- MFA and identity orchestration for users and admins

- Audit logging with tamper-resistant storage

- Data residency controls and retention policies

- Vendor risk management and third-party access governance

5. Cloud Infrastructure & DevOps

This is the reliability layer. It keeps the platform stable under load. It also enables faster releases with fewer incidents.

Setup typically includes:

- AWS, Azure, or GCP architecture and provisioning

- Multi-region deployment strategy where needed

- High availability patterns and failover planning

- Containerization with Kubernetes or managed services

- CI/CD pipelines with approvals and rollback controls

- Infrastructure as Code for repeatable environments

- Monitoring and observability for latency and errors

Ongoing annual run cost depends on usage. It also depends on refresh frequency and data volume.

6. Frontend & Enterprise Dashboards

Enterprises need more than a user UI. They need operating control. Dashboards give teams visibility into data health and access behavior.

Common dashboard views:

- Admin control panels for integrations and settings

- Data quality and refresh analytics

- Treasury and cash visibility views when relevant

- Risk and security monitoring screens

- Role-based access control for different teams

7. Risk Monitoring & Fraud Detection

Aggregation creates a new attack surface. This layer watches behavior and flags misuse. It also protects trust with partners.

Typical detection coverage:

- Behavioral anomaly detection for unusual access patterns

- API misuse detection and token abuse alerts

- Suspicious data access monitoring by role and scope

- AI-driven monitoring to reduce alert fatigue over time

An account aggregation platform budget is rarely driven by UI features. It is shaped by governance, security, and operational reliability. Therefore, the smartest cost planning starts with risk posture and compliance scope.

When these layers are designed correctly, the platform becomes a scalable infrastructure. It also becomes a long-term growth enabler.

Regulatory Costs Specific to the United States

Regulation is one of the strongest cost drivers when building an account aggregation platform in the US. It does not sit outside the architecture. Instead, it shapes how data is accessed, stored, and governed from day one. Therefore, compliance planning must begin early in the design phase rather than after launch.

Compliance Cost Breakdown

| Regulatory Area | Estimated Cost |

| CFPB Section 1033 Readiness | $25K – $100K |

| State-Level Privacy Compliance | $20K – $80K |

| SOC 2 & Third-Party Audits | $30K – $120K |

| Total Estimated Compliance Cost | $75K – $250K+ |

These costs vary depending on data sensitivity, integration scale, and audit scope.

1. CFPB Section 1033 Compliance

This framework focuses on consumer control over financial data. Platforms must provide clear mechanisms for users to grant and revoke access. In addition, systems must track how data is used and shared across applications.

Secure data transfer also becomes mandatory, which means encryption and access logging must be embedded. As a result, the platform must support transparency without slowing down operations.

2. State-Level Data Privacy Laws

US privacy requirements differ by state. For example, CCPA requires clear disclosure of how user data is collected and used. Meanwhile, NYDFS cybersecurity rules demand strong protection measures and incident response planning.

Therefore, platforms must support flexible privacy controls that work across jurisdictions. This often increases engineering and legal alignment costs.

3. SOC 2 & Third-Party Audits

Enterprise platforms must prove their reliability. SOC 2 helps establish trust through formal security reviews. Preparation includes documenting policies and implementing technical safeguards.

In addition, annual audits ensure ongoing accountability. These processes create recurring operational expenses.

In conclusion, regulation is not optional. It directly defines platform architecture, operating processes, and long-term risk posture.

Hidden Costs Enterprises Often Miss

Initial budgets often focus on development and compliance. However, long-term ownership of an account aggregation platform introduces additional expenses that rarely appear in early forecasts.

These costs emerge as usage grows, partnerships expand, and regulatory expectations evolve. Therefore, leadership teams should evaluate the total cost of ownership, not just the launch investment.

Estimated Hidden Cost Impact (Annual)

| Hidden Cost Area | Estimated Annual Cost |

| Bank API Change Management | $20K – $80K |

| Data Refresh Optimization | $25K – $100K |

| Legal Review & Contract Negotiation | $15K – $60K |

| Cyber Liability Insurance | $20K – $75K |

| Vendor Certification Fees | $10K – $50K |

| Customer Support & Dispute Handling | $30K – $120K |

| Peak Load Scalability | $40K – $150K+ |

1. Bank API Change Management

Financial institutions update APIs frequently. Changes may affect authentication flows, rate limits, or data structures. As a result, integrations can fail or produce incomplete records.

Engineering teams must monitor documentation updates and test integrations regularly. In addition, sandbox validation and regression testing require time and resources. Over a year, these adjustments create steady maintenance costs that are often underestimated.

2. Data Refresh Optimization Costs

More frequent refresh cycles improve underwriting accuracy and analytics precision. However, each refresh consumes API calls and cloud processing power. Therefore, enterprises must design intelligent refresh logic that balances performance with cost.

This includes prioritizing active accounts and limiting unnecessary background calls. Optimization work continues as user volume grows.

3. Legal Review & Contract Negotiation

Data-sharing agreements define responsibility for breaches, data misuse, and operational failure. These contracts require careful drafting and periodic review. In addition, new regulations or expanded product lines may trigger renegotiation.

Legal teams must assess liability exposure and update language accordingly. Over time, this creates recurring advisory and review expenses.

4. Insurance (Cyber Liability)

Cyber insurance provides financial protection against breaches and service interruptions. Premiums depend on transaction volume and data sensitivity.

As the platform scales, insurers often reassess coverage requirements. Therefore, insurance costs typically increase alongside platform growth.

5. Vendor Certification Fees

Some financial partners require formal certification before enabling integration. These reviews validate security controls and operational readiness.

Certification may also require renewal after system changes. Consequently, onboarding additional institutions introduces repeated compliance-related expenses.

6. Customer Support & Dispute Handling

Users may question transaction categorization or connection errors. Addressing these concerns requires trained support staff and structured escalation paths.

Enterprise clients may demand faster service levels, which increases staffing needs. Therefore, support becomes a growing operational line item.

7. Scalability Costs Under Peak Loads

Transaction volumes rise during tax periods, reporting cycles, or promotional campaigns. Infrastructure must scale to maintain response times and uptime.

This expansion increases compute, storage, and monitoring costs. Once demand stabilizes, usage declines, yet peak readiness must remain available.

Hidden costs do not appear dramatic at first. However, over time, they shape profitability and operational stability. Enterprises that anticipate these expenses can build more predictable financial models. Planning for them early strengthens resilience and protects long-term ROI.

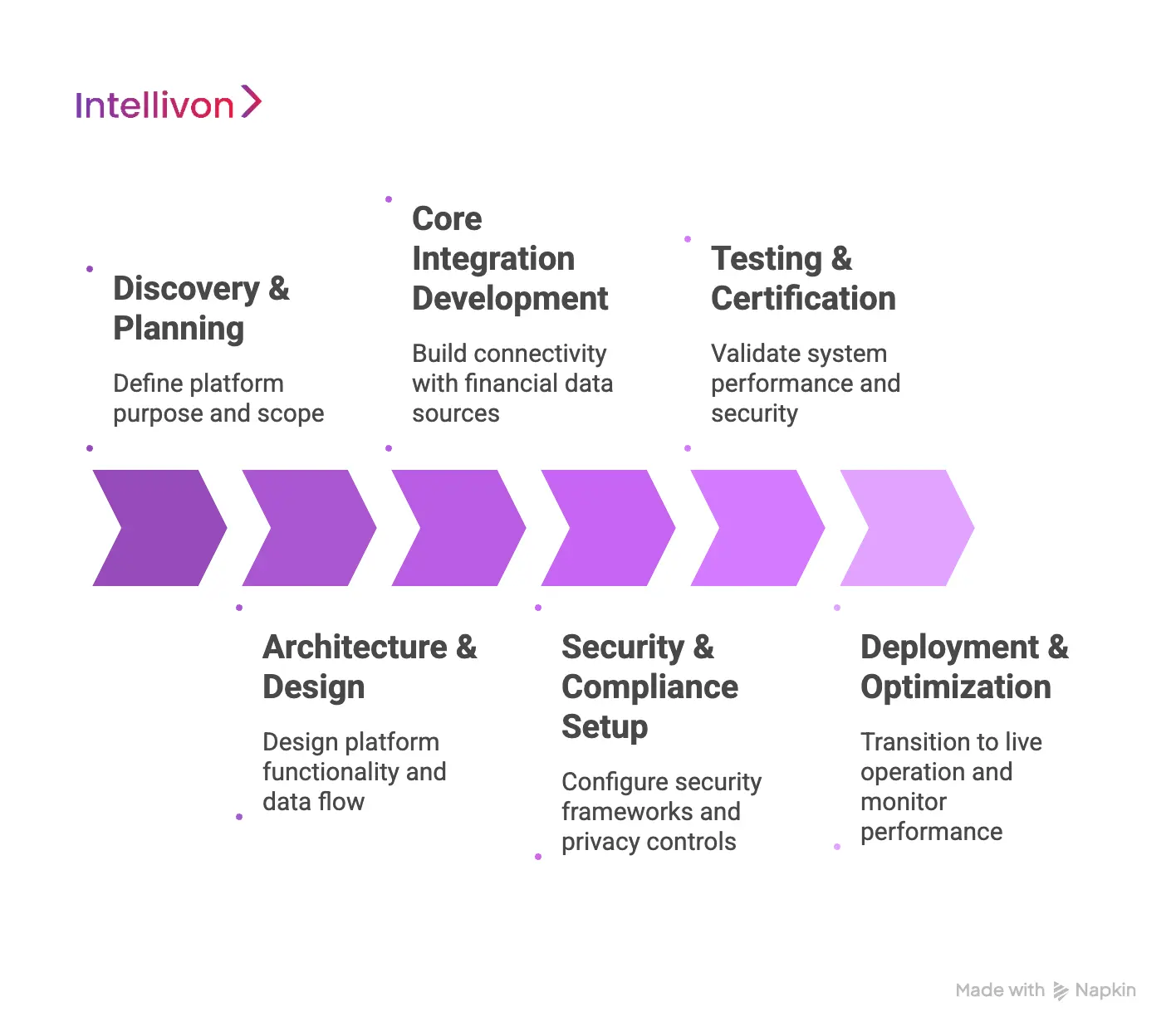

Phase-Wise Costs To Build An Account Aggregation Platform

Building an account aggregation platform happens in stages. Each phase introduces new technical and operational requirements. Therefore, investment spreads across planning, development, security, and deployment activities.

Understanding these phases helps enterprises forecast cost and avoid downstream rework.

Estimated Cost by Phase

| Development Phase | Estimated Cost |

| Discovery & Planning | $15K – $50K |

| Architecture & Design | $25K – $80K |

| Core Integration Development | $40K – $150K |

| Security & Compliance Setup | $50K – $150K |

| Testing & Certification | $20K – $70K |

| Deployment & Optimization | $20K – $60K |

1. Discovery & Planning

This phase defines the platform’s purpose and operating scope. Teams decide which institutions to connect and how data will be used internally. In addition, governance expectations and access policies are outlined.

Stakeholders align on risk tolerance and performance targets. Early clarity reduces integration conflicts later. As a result, downstream redesign costs remain limited.

2. Architecture & Design

Engineers design how the platform will function at scale. This includes defining data flow between institutions and internal systems. In addition, access rules and identity controls are mapped.

Performance stability and failover needs are also considered. These decisions shape long-term resilience. Therefore, thoughtful design prevents scalability issues later.

3. Core Integration Development

This phase builds real connectivity with financial data sources. Authentication logic and token handling are implemented. In addition, error handling ensures consistent data delivery.

Teams also manage API limits and refresh timing. Integration accuracy becomes critical for downstream analytics. As a result, this stage often requires sustained engineering effort.

4. Security & Compliance Setup

Security frameworks are configured to protect sensitive financial information. Privacy controls ensure that only necessary data is accessed. In addition, monitoring systems track usage and anomalies.

Audit readiness is prepared during this stage. These measures support regulatory alignment. Consequently, operational risk is reduced before launch.

5. Testing & Certification

Functional testing validates system performance. Security testing ensures safe data exchange. In addition, certification may be required for partner integrations. Teams simulate real usage scenarios.

This helps identify stability issues early. Therefore, launch readiness improves significantly.

6. Deployment & Optimization

The platform transitions into live operation. Monitoring tools track performance and usage patterns. In addition, teams adjust refresh cycles and workflows. Feedback loops guide system improvements.

This phase stabilizes performance over time. As a result, user experience and reliability improve.

Phase-wise planning improves cost visibility. At the same time, it also supports smoother implementation and sustained performance.

Ongoing Operational Costs After Launch

Launching an account aggregation platform marks the beginning of a continuous operating phase. Once live, the platform requires ongoing infrastructure support, governance oversight, and performance monitoring.

In addition, growing user adoption increases the need for data refresh cycles and processing capacity. Therefore, enterprises must plan for recurring operational costs from the outset. These expenses expand as integrations, usage levels, and regulatory expectations grow.

Estimated Annual Operational Costs

| Operational Area | Estimated Annual Cost |

| Cloud Hosting | $40K – $150K |

| API Usage Fees | $30K – $120K |

| Compliance & Audit Renewals | $20K – $80K |

| Security Monitoring Teams | $25K – $100K |

| SRE & DevOps | $20K – $70K |

| Data Infrastructure Scaling | $15K – $80K |

| Total Estimated Annual Cost | $150K – $500K+ |

Cloud Hosting

Cloud hosting ensures that the platform remains accessible and responsive at all times. As more users connect financial accounts, the system must process larger volumes of data continuously.

In addition, real-time updates require persistent compute resources. Multi-region deployments may also be necessary to maintain uptime. These factors steadily increase infrastructure usage. Over time, cloud hosting has become one of the most significant operational expenses.

1. API Usage Fees

Financial data providers typically charge based on usage levels. Each data refresh, or account update, generates API requests. When users connect multiple accounts, the total request volume rises quickly.

In addition, frequent refresh cycles further increase consumption. As platform adoption grows, these usage-based costs scale accordingly. Monitoring and optimization are therefore essential to control spending.

2. Compliance & Audit Renewals

Maintaining regulatory alignment requires regular validation of privacy and security controls. Annual audits confirm that the platform continues to meet industry standards. In addition, evolving regulations may require updates to policies or system configurations.

Documentation must remain accurate and current at all times. These recurring activities create ongoing compliance expenses. As a result, governance becomes a permanent operational responsibility.

3. Security Monitoring Teams

Security teams play a critical role in maintaining trust and stability. They monitor platform activity to detect unusual behavior and potential threats.

In addition, they manage access permissions and review security events. Incident response readiness must also remain active. Continuous oversight helps prevent breaches and misuse. Therefore, skilled monitoring remains a long-term necessity.

4. SRE & DevOps

Reliability teams ensure that the platform operates smoothly under varying conditions. They manage deployments, performance tuning, and system updates. In addition, they respond to operational incidents that may affect uptime.

Continuous maintenance keeps the system stable. These responsibilities require dedicated expertise. As a result, DevOps support remains an ongoing investment.

5. Data Infrastructure Scaling

As user adoption increases, the volume of stored financial data grows significantly. Analytics workloads also expand over time. In addition, storage and processing requirements rise steadily.

Infrastructure must scale to maintain performance. Peak activity periods may increase demand further. Therefore, scaling introduces variable operational costs.

Operational costs continue long after the platform launches. Planning for them supports stability, scalability, and long-term value.

Conclusion

Building an account aggregation platform is not just a technical investment. Instead, it shapes how financial data moves across the organization. In addition, it improves risk visibility and customer understanding. While upfront costs may vary, long-term value depends on scalability and compliance readiness. Therefore, enterprises should prioritize sustainable architecture over short-term savings.

Over time, a well-designed platform improves decision-making and supports new financial products. As a result, organizations gain stronger control over data-driven growth. With the right approach, this investment becomes more than a cost. It becomes a foundation for future innovation and competitive advantage.

Build an Account Aggregation Platform With Intellivon

At Intellivon, account aggregation platforms are designed as governed financial infrastructure rather than simple data connectors. Every architectural decision focuses on secure data access, regulatory alignment, and operational resilience across complex enterprise environments.

Each platform integrates seamlessly with existing banking systems, lending workflows, and analytics tools. In addition, modular architecture allows enterprises to expand capabilities without disrupting core operations. This ensures the platform continues to support evolving business needs while maintaining long-term reliability.

Why Partner With Intellivon?

- Enterprise-grade architecture built for regulated financial ecosystems

- Compliance-by-design approach with embedded governance controls

- Secure, scalable infrastructure supporting multi-institution integrations

- AI-driven monitoring for risk visibility and operational intelligence

- Modular deployment aligned with long-term growth strategies

- API-first framework that simplifies integration with legacy systems

- Built-in data governance to support evolving regulatory requirements

- Future-ready architecture that adapts to emerging open banking standards

Connect with Intellivon to explore how your organization can build and scale an account aggregation platform with confidence and control.

FAQs

Q1. What is the cost to build an account aggregation platform in the USA?

A1. The cost usually ranges from $70,000 to $500,000 or more. The final investment depends on platform scope and compliance needs. In addition, integration complexity also affects pricing. Enterprise-grade platforms require stronger security and governance. Therefore, costs rise with scalability and regulatory readiness.

Q2. What factors influence account aggregation platform development cost?

A2. Several elements shape the total cost. These include integration depth, security requirements, and compliance standards. In addition, real-time data refresh increases infrastructure usage. Platform scalability also affects long-term investment. Therefore, architecture decisions play a major role.

Q3. How long does it take to build an account aggregation platform?

A3. Development timelines usually range from 4 to 9 months. The duration depends on platform complexity and regulatory readiness. In addition, integration with multiple institutions can extend timelines. Testing and certification also require time. Therefore, enterprise deployments may take longer.

Q4. Is regulatory compliance mandatory for account aggregation platforms?

A4. Yes, compliance is essential in the United States. Platforms must support secure data sharing and consumer transparency. In addition, privacy regulations require strong governance controls. Annual audits may also be needed. Therefore, compliance must be built into the system from the start.

Q5. Should enterprises build or partner for account aggregation?

A5. Both options offer benefits. Building provides greater control and flexibility. However, partnering may accelerate deployment. In addition, hybrid approaches balance speed and ownership. Therefore, the choice depends on long-term strategy and risk tolerance.