In the past, corporate card programs mainly issued physical cards and handled expenses later. Today, that approach does not fit what modern businesses need. Finance leaders now want real-time spending visibility, flexible controls, built-in compliance, and systems that can grow with their company without making operations more complicated.

Platforms such as Marqeta have changed expectations for corporate card issuing. But matching their control, reliability, and regulatory standards takes more than just setting up card APIs. Companies need to plan for sponsor bank relationships, certification, fraud detection, managing multiple business units, and ongoing compliance from the start.

At Intellivon, corporate card issuing is a core part of our financial infrastructure, not just an extra feature. Our teams partner with enterprise clients to design integrations, set up policy-based spending controls, leverage AI for fraud monitoring, and embed compliance at every step. In this blog, we will explain how we built a secure, scalable corporate card platform similar to Marqeta.

Key Market Takeaways for Corporate Card Issuing Platforms

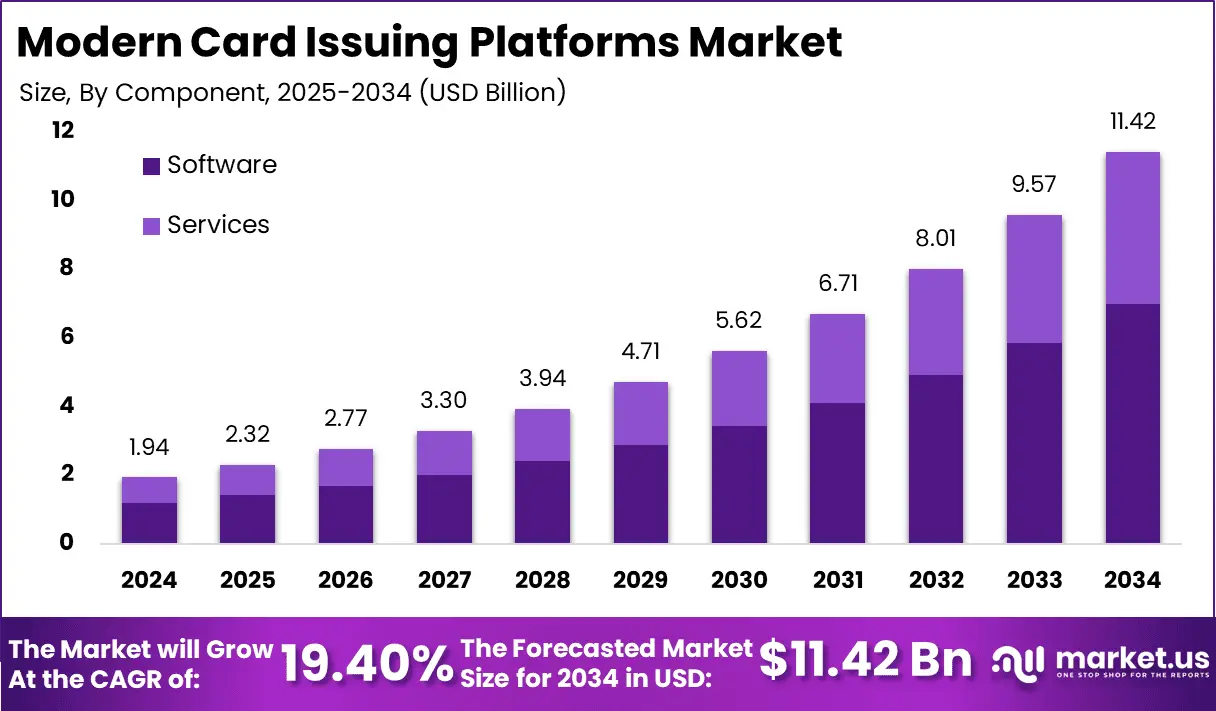

Corporate card issuing platforms are expanding quickly as organizations modernize finance operations and demand tighter spend control. These systems allow businesses to issue both virtual and physical cards with real-time governance.

As a result, many enterprises are moving away from rigid legacy setups toward API-driven issuing environments that offer greater flexibility and oversight.

The modern card issuing platform market is projected to reach USD 11.42 billion by 2034, expanding at a 19.4% CAGR. This growth is largely driven by cloud native infrastructure and the rising adoption of virtual cards across enterprise payment programs.

Key Market Insights:

- Digital transformation continues to accelerate adoption as organizations seek simpler expense workflows, stronger AI-driven insights, and built-in regulatory alignment.

- At the same time, embedded finance and real-time payments are creating new opportunities across e-commerce, subscription models, and enterprise spend programs. More than 60% of enterprises now prioritize payments modernization.

- Small and mid-sized businesses are also shifting toward cloud-based issuing platforms for payouts and vendor cards. This move helps reduce infrastructure overhead while improving operational flexibility.

Marqeta has played a pivotal role in reshaping corporate card issuing by pushing the market toward real-time, API-first infrastructure. The company reported roughly 33% growth in total processing volume, reflecting strong demand for programmable card controls and embedded finance use cases.

In addition, strategic moves such as the TransactPay acquisition signal a clear focus on expanding European issuing capabilities and regulatory reach.

As a result, Marqeta has helped shift industry expectations from basic card enablement to highly configurable, developer-friendly issuing environments that can scale across modern enterprise workflows.

What Is The Corporate Card Issuing Platform Marqeta?

A corporate card issuing platform like Marqeta is a modern payments infrastructure that allows organizations to create, manage, and control payment cards through software. Instead of relying on rigid banking systems, enterprises can program card behavior in real time using APIs and policy rules.

These platforms support the full card lifecycle, including virtual and physical card creation, authorization controls, transaction monitoring, and settlement visibility. As a result, finance and product teams gain tighter control over business spend without slowing operations.

In addition, Marqeta-style platforms connect sponsor banks, card networks, and enterprise systems into a single programmable environment. This makes it easier to launch embedded finance products, manage corporate expense programs, and scale card operations across regions.

For growing enterprises, the platform becomes a core layer of financial control rather than just a payment feature.

Why Fintech Enterprises Need Corporate Card Issuing Platforms

Corporate card issuing platforms help transform static card programs into programmable financial systems. Instead of relying on manual reviews or delayed reports, teams can enforce policies automatically and monitor transactions as they happen.

This shift supports faster innovation while keeping financial risk tightly governed.

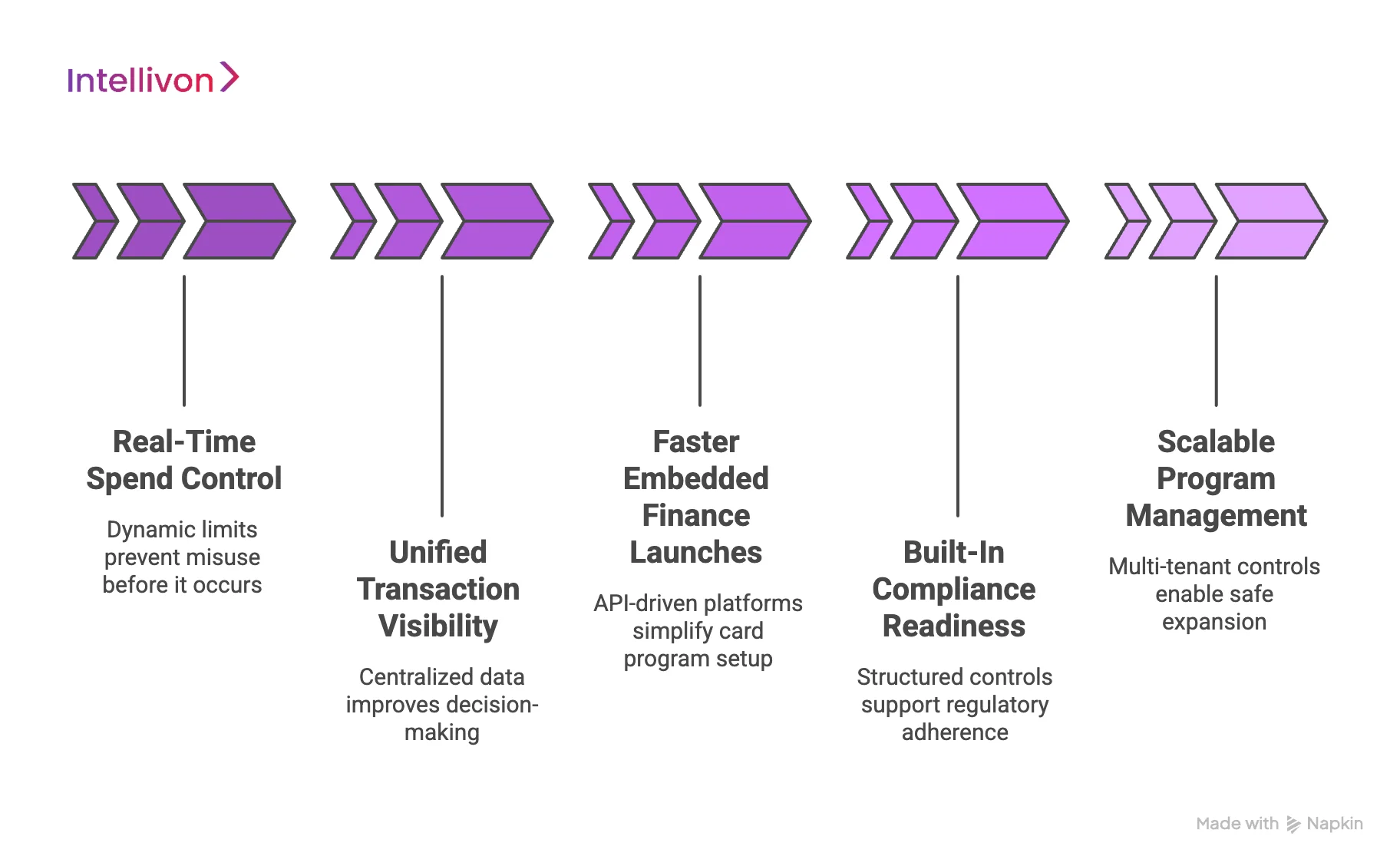

1. Real-Time Spend Control

Modern fintech products require precise control over how funds are used. Issuing platforms allow teams to set dynamic limits based on merchant category, geography, time window, or user role.

As a result, finance and risk teams can prevent misuse before it occurs rather than correcting it later. This proactive control becomes especially valuable as transaction volume increases.

2. Unified Transaction Visibility

Fragmented reporting often slows decision-making. A dedicated issuing layer provides real-time transaction data, event notifications, and consistent audit trails in one place.

Because of this, finance, product, and risk teams work from the same source of truth. The organization gains faster insight into spend behavior and emerging risk patterns.

3. Faster Embedded Finance Launches

Fintech companies increasingly embed cards into broader product experiences. However, building an issuing infrastructure from scratch can delay time to market.

API-driven issuing platforms simplify this process. Teams can configure new card programs, virtual cards, and customer segments without rebuilding core payment rails each time.

4. Built-In Compliance Readiness

Regulatory scrutiny continues to increase across payment ecosystems. Corporate card issuing platforms help address this pressure through structured controls and traceable workflows.

Features such as role-based access, detailed audit logs, and policy enforcement support ongoing compliance efforts. Therefore, organizations reduce the risk of costly retrofits later.

5. Scalable Program Management

What works for a pilot often breaks at scale. As fintech platforms expand across regions and customer segments, operational complexity rises quickly.

Issuing platforms provide the multi-tenant controls and program isolation needed to grow safely. This foundation allows teams to onboard new programs without destabilizing existing operations.

For fintech enterprises, corporate card issuing platforms have become a core layer of financial infrastructure. They provide the control, visibility, and scalability required to support modern payment products.

What Makes Marqeta-Style Platforms Different From Basic Issuing Tools

Marqeta-style corporate card issuing platforms differ from basic card APIs by enabling real-time controls, deeper reconciliation, and scalable multi-program governance.

Marqeta-style platforms were built for programmable finance at scale. They combine real-time authorization logic, multi-program management, and operational tooling into a unified issuing environment. Therefore, enterprises gain tighter financial control and stronger reliability across complex payment workflows.

Below is a practical comparison that highlights where the differences become material.

Table: Marqeta-Style Issuing vs Basic Card APIs

| Area | Marqeta-Style Issuing | Basic Card APIs |

| Core purpose | Programmable issuing infrastructure for enterprise-scale card programs | Simple card enablement and transaction processing |

| Authorization intelligence | Real-time, rule-based decision engine with granular controls | Basic approve or decline logic with limited configurability |

| Program configurability | Multi-program, multi-tenant support with dynamic controls | Single-program focus with minimal flexibility |

| Tokenization readiness | Native support for virtual cards and wallet provisioning | Often requires external tooling or custom work |

| Ledger and reconciliation depth | Built for transaction matching, settlement visibility, and finance workflows | Limited reconciliation support, often manual |

| Risk and fraud tooling | Integrated risk signals and extensible fraud controls | Basic monitoring with heavy reliance on third parties |

| Disputes and chargeback readiness | Structured workflows and evidence tracking | Minimal or external dispute handling |

| Auditability | Detailed event logs and role-based traceability | Partial logging with limited audit depth |

| Scalability | Designed for high-volume, multi-entity growth | Works for pilots but strains at enterprise scale |

Why Architecture Matters at Scale

High customer concentration in corporate card issuing can expose platforms to revenue volatility, pricing pressure, and operational dependency as programs grow. Because of this, architectural decisions made early tend to surface later in the form of performance limits, reconciliation gaps, or governance challenges.

Enterprises that adopt issuing infrastructure designed for real-time control and multi-program scale are better positioned to absorb growth without disruption. In contrast, teams that rely on lightweight card APIs often face costly rework once transaction complexity increases.

Business and Revenue Models Of Marqeta

Marqeta operates a modern issuing and processing platform that monetizes card volume through interchange, processing fees, and program services while sharing incentives with customers.

Marqeta’s model focuses on helping fintechs and large platforms launch and scale card programs efficiently. Instead of offering a single packaged product, the company provides programmable issuing infrastructure combined with transaction processing and operational support. As a result, Marqeta grows when customers expand card usage, introduce new programs, and increase payment volume.

From a financial reporting perspective, Marqeta groups revenue into platform services revenue and other services revenue. Platform services revenue includes interchange earned on processed transactions, net of customer incentives, along with processing and related fees. Other services revenue primarily comes from card fulfillment activities.

Business Models of Marqeta

Marqeta supports multiple adoption paths depending on how much control and operational ownership a customer wants to retain. Each model influences implementation speed, internal workload, and long-term platform dependency.

1. API-First Issuing Platform

Marqeta primarily operates as an API-driven issuing and processing layer that customers embed directly into their products. Teams use the platform to create cards, configure controls, and manage lifecycle events while keeping the user experience within their own applications.

Because of this flexibility, the model works well for fintech companies, digital banks, and embedded finance providers that need rapid iteration.

2. Program Management Expansion

As customers scale, many require deeper operational consistency across controls, reporting, and partner coordination. Marqeta supports program-level capabilities that help standardize issuing operations as transaction complexity grows.

Over time, this often increases platform reliance, especially for customers running high-volume card programs across multiple segments.

3. Managed Services Support

Marqeta also offers operational services designed to reduce customer workload. These services include areas such as dispute management, fraud scoring support, and cardholder assistance.

Consequently, organizations can scale card programs without building large in-house operations teams. This model is particularly useful for fast-growing fintech platforms.

4. Regional Program Enablement

Marqeta has expanded its geographic coverage to support customers operating outside North America. For example, the TransactPay acquisition strengthened its ability to provide BIN sponsorship and issuing capabilities across the United Kingdom and European markets.

This expansion matters because cross-border issuing typically increases regulatory and partner complexity. Therefore, platforms that simplify regional rollout can accelerate global program launches.

Marqeta’s business approach typically begins with flexible issuing infrastructure and gradually deepens into broader program operations. This progression increases platform stickiness and supports long-term customer expansion.

Revenue Models Of Marqeta

Marqeta generates revenue primarily from card transaction activity and the services that support those transactions. Its filings provide useful visibility into how unit economics evolve as customer volume increases.

1. Interchange Fees Net of Revenue Share

A significant portion of Marqeta’s revenue comes from interchange fees earned on processed card transactions. These fees are calculated as a percentage of transaction value plus a fixed component and are recognized when transactions settle.

However, Marqeta also pays revenue share incentives to certain customers to encourage growth. These incentives are typically calculated as a percentage of interchange or processing volume and are recorded as a reduction to net revenue.

As programs scale, this dynamic can materially influence margins. Therefore, enterprises evaluating issuing economics must model revenue share carefully.

2. Processing and Transaction Fees

Marqeta also earns processing and related platform fees. These charges may be structured as per-transaction pricing, volume-based fees, or minimum commitments when activity falls below agreed thresholds.

This revenue stream provides additional stability because it is not fully dependent on interchange performance.

3. Card Fulfillment Revenue

The company generates additional income through card fulfillment services, including the production and shipment of physical cards. Revenue is typically recognized when customers order card inventory and the cards are delivered.

While smaller than transaction revenue, fulfillment services support full program rollout and customer onboarding.

Marqeta’s revenue engine scales primarily with customer transaction volume, while revenue share structures shape net economics as programs mature. Processing fees and fulfillment services provide supplemental income streams that support the broader issuing lifecycle.

Marqeta’s business and revenue structure reflects how modern corporate card issuing platforms expand in practice. Growth is closely tied to customer volume, program diversification, and geographic reach. At the same time, revenue share mechanics and processing mix directly influence long-term profitability.

How Corporate Card Issuing Faces 44–47% Revenue Risk

Customer concentration rarely appears in early program discussions. However, it quickly becomes visible as issuing volume grows. In several public filings across the issuer-processor ecosystem, a single client has contributed roughly 44 to 47% of net revenue. That level of dependency creates structural exposure that finance, risk, and product teams must plan for early.

For organizations building corporate card issuing capabilities, the issue is not theoretical. Revenue concentration affects negotiating leverage, program stability, and long-term platform resilience. Therefore, leaders evaluating infrastructure should treat concentration risk as a design consideration, not just a commercial metric.

1. Revenue Volatility Increases with Client Concentration

When one customer drives a large share of processing volume, revenue stability becomes sensitive to that relationship. Even a modest shift in client activity can materially affect top-line performance.

In corporate card issuing environments, this risk compounds because transaction volume often fluctuates with the customer’s own business cycles. As a result, forecasting becomes less predictable and financial planning requires wider buffers.

For enterprise platforms, a diversified program mix reduces this exposure and creates more consistent revenue behavior.

2. Negotiation Leverage Shifts Toward Large Programs

High concentration often changes the commercial balance between the platform and the client. Large programs typically negotiate more aggressively on interchange sharing, pricing tiers, and service commitments.

Over time, this dynamic can compress margins, especially when revenue share agreements scale with volume. Therefore, issuing platforms must model long-term unit economics carefully rather than relying on early growth assumptions.

Strong governance around pricing and contract structure helps maintain sustainable economics as programs mature.

3. Operational Dependency Creates Hidden Risk

Customer concentration is not only a financial concern. It also creates operational dependency across support, risk monitoring, and program management teams.

Large enterprise programs usually demand:

- dedicated support coverage

- custom authorization rules

- tailored reporting pipelines

- enhanced fraud monitoring

If too much infrastructure becomes specialized for one client, platform agility can decline. Consequently, onboarding new programs may require additional rework. Designing modular, multi-tenant issuing architecture helps prevent this form of lock-in.

4. Sponsor Bank and Network Exposure May Rise

In many issuing models, major clients drive a significant portion of sponsor bank throughput. When volume concentrates heavily, bank relationships and network certifications may also become indirectly dependent on that program.

This creates second-order risk. If the large client changes strategy, the platform may face:

- sudden volume drops

- renegotiation pressure from partners

- underutilized program capacity

Enterprises that plan multi-program growth early tend to avoid this fragility.

5. Diversification Requires Intentional Program Strategy

Reducing concentration is not simply a sales problem. It requires coordinated product, partnership, and market expansion decisions.

Effective platforms typically:

- support multiple card use cases

- enable rapid program configuration

- onboard varied customer segments

- maintain flexible pricing models

Because of this, diversification works best when built into the issuing roadmap from the beginning rather than added later.

Customer concentration is a quiet but material risk in corporate card issuing. While early growth often depends on a few large programs, sustained success requires a broader and more balanced portfolio.

Organizations that are architected for diversification, modular controls, and scalable program onboarding place themselves in a far stronger position as volume expands.

In the long run, disciplined issuing design protects both revenue stability and operational resilience, turning corporate card infrastructure into a dependable growth engine rather than a concentrated risk surface.

How Corporate Card Issuing Platforms Like Marqeta Work

Corporate card issuing platforms run as closed-loop systems that connect program design, real-time authorization, settlement, and compliance monitoring into one governed workflow.

Corporate card issuing is not a single transaction flow. It is an ongoing operational loop that connects product setup, payment decisions, financial settlement, and oversight controls. When any layer is weak, problems usually appear later as reconciliation gaps, risk exposure, or scaling friction.

Platforms like Marqeta perform well because they treat issuing as coordinated infrastructure. Each step feeds the next. Therefore, enterprises that design the full loop early tend to avoid costly rework. The following walkthrough explains how modern issuing environments typically function.

Step 1: Define the Card Program and Operating Model

Every successful program starts with clear design choices. Teams must decide who the cards serve, how money moves, and which controls apply from day one.

Common planning decisions include:

- corporate expense versus embedded finance use cases

- prefunded, debit, or credit funding models

- virtual, physical, or single-use card formats

- approval workflows and policy rules

This stage also clarifies responsibilities across the sponsor bank, network, and platform. When ownership is vague, implementation timelines often slip.

Step 2: Sponsor Bank and Network Readiness

Corporate card issuing cannot launch without bank and network alignment. These partners provide regulatory coverage and transaction routing across the payment ecosystem.

At this point, teams usually address:

- BIN sponsorship setup

- network certification requirements

- compliance ownership boundaries

- settlement and funding mechanics

Because these dependencies sit outside the product team, early coordination reduces surprises. Mature issuing platforms simplify this step through pre-integrated partner frameworks.

Step 3: Card Product Configuration

After program approval, teams configure the card products themselves. This is where issuing becomes truly programmable.

Typical configuration elements include:

- dynamic spend limits and velocity rules

- merchant category restrictions

- geographic and time controls

- tokenization and wallet provisioning

- user roles and permission structures

Flexible configuration matters because enterprise requirements rarely stay static. Platforms that support rapid policy changes help teams respond faster to risk and business needs.

Step 4: Card Lifecycle Management

Once cards are issued, the platform must manage the full lifecycle. This includes everything from activation to replacement.

Key lifecycle events usually include:

- card creation and provisioning

- activation and suspension

- freeze and unfreeze actions

- renewal and replacement

- termination and archival

Strong lifecycle orchestration improves customer experience and reduces manual workload for operations teams.

Step 5: Real-Time Authorization Decisioning

Real-time authorization is the core intelligence layer of corporate card issuing. Every transaction request triggers a decision in milliseconds.

During authorization, the platform evaluates:

- available balance or credit

- policy and spend rules

- merchant and location data

- risk and fraud signals

Based on these checks, the system approves or declines the transaction. Because this happens instantly, well-designed decisioning reduces both fraud exposure and false declines.

Step 6: Clearing, Settlement, and Reconciliation

Authorization is only the first half of the payment lifecycle. After approval, transactions move through clearing and settlement.

At this stage, the platform must:

- match authorization to clearing records

- calculate fees and interchange

- update balances and ledgers

- support finance reconciliation workflows

Many early-stage programs struggle here. Therefore, enterprise platforms invest heavily in reconciliation accuracy and reporting depth.

Step 7: Disputes and Chargeback Handling

Over time, some transactions will be disputed. A mature issuing environment includes structured workflows to manage these cases efficiently.

Typical capabilities include:

- dispute intake and case tracking

- evidence collection and submission

- network deadline management

- customer communication workflows

Without strong dispute tooling, support teams quickly become overloaded as volume grows.

Step 8: Reporting, Controls, and Continuous Monitoring

The final layer focuses on visibility and governance. Leadership teams need clear insight into program health, risk exposure, and financial performance.

Enterprise platforms typically provide:

- real-time transaction dashboards

- audit-ready event logs

- compliance reporting

- risk and performance alerts

- program level analytics

Continuous monitoring ensures the issuing environment remains stable as transaction volume expands.

Corporate card issuing platforms like Marqeta operate as closed-loop financial systems. Each stage, from program design to monitoring, reinforces the next. When enterprises build with this full lifecycle in mind, they gain stronger control, cleaner reconciliation, and more predictable scale.

In contrast, treating issues as a simple API layer often leads to operational strain later. A disciplined, end-to-end architecture is what ultimately turns corporate card programs into a reliable enterprise infrastructure.

Core Components of a Corporate Card Issuing Platform Like Marqeta

A Marqeta-style corporate card issuing platform depends on tightly integrated components such as KYC, authorization, ledger, reconciliation, and event orchestration working as one system.

Building a corporate card issuing platform like Marqeta requires more than card creation and payment routing. Enterprise reliability comes from how well the underlying components work together. Each layer supports a specific part of the issuing lifecycle, from onboarding to dispute resolution.

When these components are loosely connected, teams often face reconciliation errors, risk blind spots, or scaling friction. However, when designed as a coordinated stack, the platform can support high-volume programs with consistent control and visibility. The following components form the foundation of a modern issuing environment.

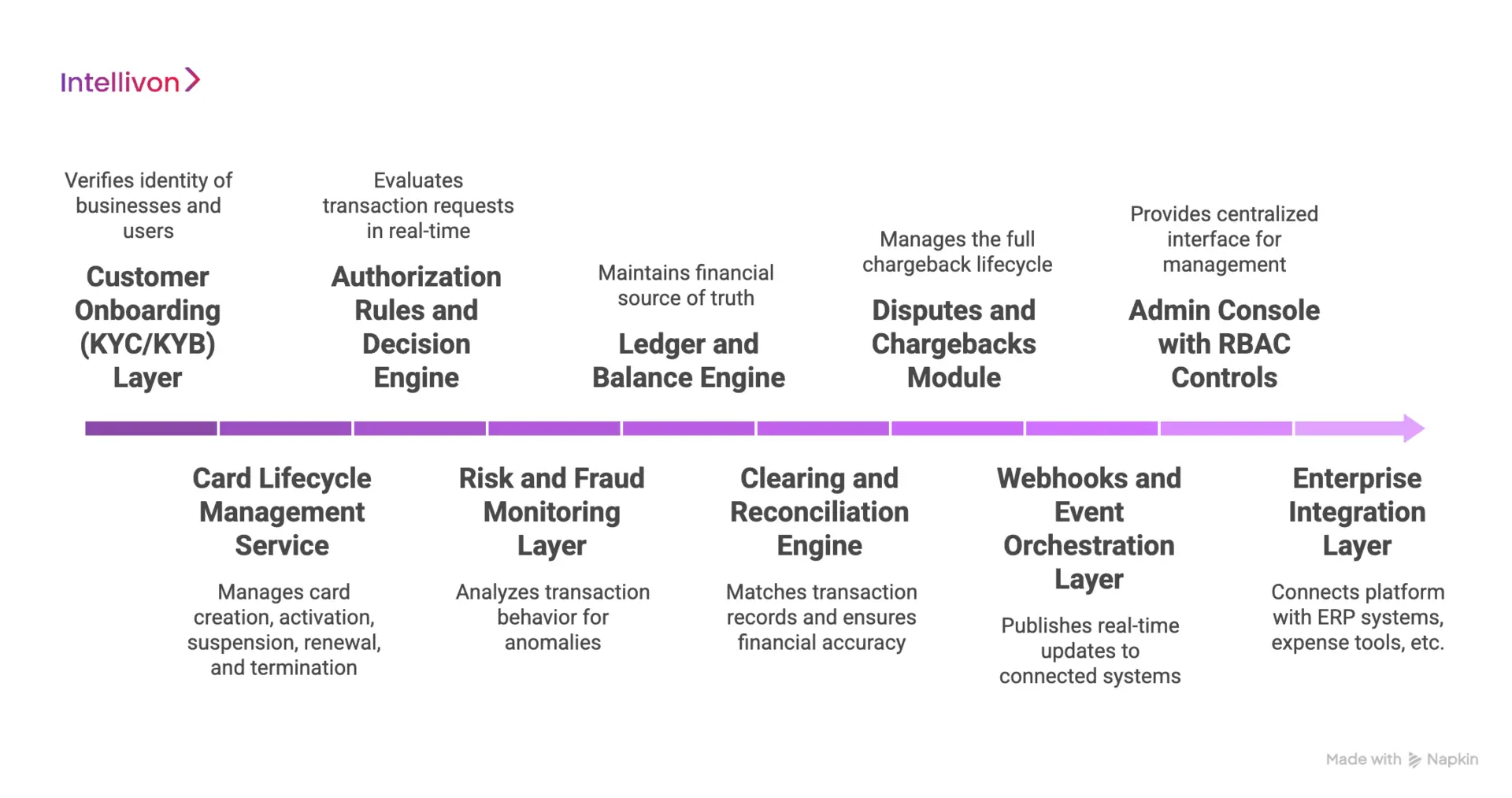

1. Customer Onboarding (KYC/KYB) Layer

The onboarding layer verifies the identity of businesses and users before cards are issued. It typically integrates Know Your Customer and Know Your Business checks into the application flow.

Strong onboarding helps prevent fraud and supports regulatory compliance from the start. In addition, automated verification reduces manual review time and speeds up program activation for legitimate customers.

2. Card Lifecycle Management Service

This service manages every stage of a card’s life. It handles card creation, activation, suspension, renewal, and termination.

A well-designed lifecycle layer ensures that operations teams can respond quickly to customer requests. It also improves user experience by enabling instant card actions across web and mobile environments.

3. Authorization Rules and Decision Engine

The authorization engine is the real-time brain of the issuing platform. It evaluates each transaction request against balances, policies, and risk signals.

Typical checks include spend limits, merchant restrictions, geographic rules, and velocity controls. Because decisions occur in milliseconds, this engine directly affects both fraud exposure and approval rates.

Flexible rule configuration becomes critical as enterprise programs grow more complex.

4. Risk and Fraud Monitoring Layer

Even strong authorization rules cannot catch every threat. The risk layer continuously analyzes transaction behavior to detect anomalies and emerging fraud patterns.

Modern platforms often combine rule-based controls with machine learning signals. As a result, risk teams can focus on high-priority alerts instead of reviewing every transaction manually.

This layer plays a major role in protecting both revenue and customer trust.

5. Ledger and Balance Engine

The ledger maintains the financial source of truth for the platform. It tracks balances, funding movements, and transaction states across accounts.

Accurate ledger design is essential for finance teams. Without it, reconciliation becomes manual and error-prone. Therefore, enterprise issuing platforms typically implement double-entry accounting principles within the ledger.

This component directly supports financial reporting and audit readiness.

6. Clearing and Reconciliation Engine

After authorization, transactions move through clearing and settlement. The reconciliation engine matches these records and ensures financial accuracy.

Key responsibilities include:

- authorization to clear matching

- fee and interchange calculations

- settlement tracking

- exception handling

Many platforms struggle at this stage. However, a strong reconciliation infrastructure reduces finance workload and improves confidence in reported numbers.

7. Disputes and Chargebacks Module

Disputes are unavoidable in card programs. This module manages the full chargeback lifecycle from intake to resolution.

Core capabilities typically include:

- case creation and tracking

- evidence collection workflows

- network deadline management

- customer communication support

Structured dispute handling prevents support backlogs and helps recover funds when appropriate.

8. Webhooks and Event Orchestration Layer

Modern issuing platforms are event-driven. The orchestration layer publishes real-time updates to connected systems whenever key events occur.

Examples include:

- authorization decisions

- card status changes

- settlement updates

- dispute events

Reliable event delivery ensures that downstream systems stay synchronized. As volume grows, this layer becomes essential for platform stability.

9. Admin Console with RBAC Controls

Enterprise teams need operational visibility and governance. The admin console provides a centralized interface to manage programs, users, and policies.

Role-based access control ensures that each team member sees only what they are permitted to access. This reduces internal risk and supports compliance requirements.

In addition, a strong console improves day-to-day operational efficiency.

10. Enterprise Integration Layer

Corporate card issuing platforms rarely operate in isolation. The integration layer connects the platform with ERP systems, expense tools, banking partners, and data pipelines.

Common integrations include:

- accounting and finance systems

- expense management platforms

- sponsor bank interfaces

- analytics and reporting tools

Flexible integrations allow enterprises to embed issuing into existing workflows rather than forcing teams to change processes.

Developing a corporate card issuing platform like Marqeta requires disciplined architecture across multiple coordinated components. Each layer, from onboarding to event orchestration, plays a distinct role in maintaining control, accuracy, and scalability.

How AI Is Used in Marqeta-Style Card Issuing Platforms

In corporate card issuing, AI improves fraud detection, authorization decisions, merchant visibility, and operational efficiency while keeping human oversight in place.

AI in modern issuing platforms is most valuable when it improves signal quality and reduces manual workload. Leading platforms do not use AI as a surface feature. Instead, they apply it to specific decision points across the transaction lifecycle.

For organizations building corporate card issuing infrastructure, the goal is practical impact. AI should help risk teams act faster, finance teams see clearer data, and operations teams handle scale without proportional headcount growth.

Below are the most common and proven use cases.

1. Fraud and Anomaly Detection

Fraud patterns often appear as subtle behavioral changes rather than obvious rule violations. AI models analyze transaction streams over time to detect unusual spending patterns, location shifts, or merchant anomalies.

Because of this continuous monitoring, platforms can flag high-risk activity earlier than static rule sets alone. Risk teams then review prioritized alerts instead of scanning large volumes of normal transactions.

This approach improves both fraud capture and operational efficiency.

2. Intelligent Authorization Risk Scoring

Real-time authorization decisions benefit from contextual risk scoring. AI models evaluate transaction attributes alongside historical behavior to assign a risk score during the approval window.

The platform can then combine this score with policy rules to make more informed decisions. As a result, legitimate transactions are less likely to be declined while suspicious activity receives closer scrutiny.

Over time, this balance helps improve approval rates without weakening controls.

3. Merchant Enrichment and Categorization

Raw merchant data is often inconsistent or difficult to interpret. AI helps normalize merchant names, assign accurate categories, and enrich transaction metadata.

This improved classification supports better spend analytics and cleaner reporting for finance teams. It also strengthens downstream controls that depend on merchant category data.

For enterprises managing large card portfolios, this enrichment reduces manual data cleanup.

4. Dispute Evidence Summarization

Dispute workflows generate large volumes of supporting data. AI can assist by summarizing transaction history, customer activity, and relevant context into structured case views.

Support and risk teams still make the final decision. However, summarized evidence reduces investigation time and helps teams meet network response deadlines more consistently.

As dispute volumes grow, this efficiency becomes increasingly valuable.

5. Compliance Monitoring and Alert Triage

Regulatory and policy monitoring often produces more alerts than teams can review manually. AI helps prioritize these alerts based on risk signals and historical patterns.

For example, models can surface accounts that show unusual behavior or potential policy breaches. Consequently, compliance teams focus attention where it matters most.

This improves coverage without overwhelming operations staff.

6. Support Automation and Case Routing

Customer support volumes rise quickly as card programs scale. AI can assist by classifying incoming cases, routing them to the correct queue, and suggesting next steps for agents.

This does not replace human support. Instead, it reduces triage time and ensures cases reach the right team faster.

The result is quicker resolution and more consistent customer experience.

Guardrails for Responsible AI Use

AI must operate within clear governance boundaries in corporate card issuing environments. Explainability is essential so teams understand why a transaction was flagged or declined. At the same time, black box decisions create both regulatory and operational risk.

Human review remains critical for high-impact actions such as fraud escalation or account restrictions. Consequently, most mature platforms use AI to prioritize and recommend, while trained teams make final decisions when necessary.

In addition, continuous model monitoring is required to detect drift, bias, or performance degradation. Regular evaluation ensures the system remains aligned with real-world transaction behavior as programs scale.

AI strengthens Marqeta-style issuing platforms when applied to focused operational problems. It improves fraud detection, sharpens authorization decisions, and reduces manual workload across support and compliance teams. However, sustainable value comes from disciplined deployment supported by strong governance and human oversight.

Ensuring Security and Compliance in Corporate Card Issuing Platforms

Enterprise card issuing platforms require PCI-aligned architecture, strong encryption, governed access, and continuous monitoring to maintain trust at scale.

Security and compliance are the foundation of any corporate card issuing platform like Marqeta. As transaction volume increases, so does regulatory exposure and fraud risk. Therefore, enterprises must design security into the architecture from the start rather than adding controls later.

Well-governed issuing environments protect cardholder data, maintain audit readiness, and support partner confidence across banks and networks. The areas below represent the controls that matter most in production environments.

1. PCI DSS Scope Strategy

PCI scope can expand quickly if not managed carefully. Mature platforms isolate cardholder data environments and minimize the number of systems that touch sensitive data.

Tokenization, network segmentation, and proxy patterns help reduce audit burden. As a result, organizations lower compliance overhead while maintaining strong protection.

A deliberate scope strategy often determines long-term operational cost.

2. Encryption and Tokenization

Card data must remain protected both in transit and at rest. Strong platforms enforce end-to-end encryption across APIs, storage layers, and internal services.

Tokenization adds another layer by replacing sensitive card data with non-sensitive tokens. This allows downstream systems to operate without exposing raw card numbers.

Together, encryption and tokenization significantly reduce breach impact.

3. Vault and Key Management

Secure key handling is critical in issuing environments. Platforms typically use hardened vault systems to store secrets, encryption keys, and credentials.

Best practice includes:

- centralized key lifecycle management

- automated rotation policies

- strict access controls

- hardware security module support when required

Disciplined key management prevents silent security drift over time.

4. RBAC and Least Privilege

Not every team member needs full system access. Role-based access control limits exposure by aligning permissions with job responsibilities.

Least privilege policies ensure users receive only the access required to perform their tasks. Consequently, insider risk and accidental data exposure are reduced.

This control becomes especially important as operations teams grow.

5. Audit Logging and Traceability

Enterprise issuing platforms must maintain detailed event visibility. Every critical action should generate a timestamped audit record.

Typical events include:

- authorization decisions

- card status changes

- administrative actions

- settlement updates

- dispute activity

Comprehensive logging supports regulatory reviews and internal investigations. It also strengthens operational accountability.

6. AML, KYC, and KYB Responsibility Model

Compliance ownership must be clearly defined across the ecosystem. Corporate card issuing often involves shared responsibility between the platform, sponsor bank, and program manager.

Strong programs document:

- Who performs identity verification

- Who monitors transactions

- Who files regulatory reports?

- How exceptions are escalated

Clear accountability reduces regulatory ambiguity and audit friction.

7. SOC 2 and Governance Controls

Many enterprise customers expect SOC 2 alignment as a baseline. Governance frameworks help demonstrate that security controls operate consistently over time.

Typical areas include:

- access governance

- change management

- incident handling

- vendor risk oversight

- control monitoring

SOC 2 readiness builds trust with enterprise buyers and banking partners.

8. Incident Response Posture

Even well-protected platforms must prepare for incidents. A mature response plan defines how teams detect, contain, investigate, and communicate security events.

Effective programs maintain:

- real-time monitoring coverage

- escalation playbooks

- cross-functional response teams

- post-incident review processes

Fast, coordinated response limits both financial and reputational damage.

9. Data Privacy and Residency

Data residency requirements continue to expand across regions. Corporate card issuing platforms must support jurisdiction-specific storage and processing rules.

Privacy controls typically include:

- regional data segregation

- consent and retention management

- cross-border transfer safeguards

- customer data access controls

Designing for privacy early prevents costly architectural changes later.

Security and compliance determine whether a corporate card issuing platform can operate confidently at enterprise scale. Organizations that invest in PCI scope discipline, strong encryption, governed access, and continuous monitoring build a foundation that withstands regulatory scrutiny and partner expectations.

How We Develop a Corporate Card Issuing Platform Like Marqeta

At Intellivon, corporate card issuing is treated as governed financial infrastructure. The focus stays on reliability, control, and long-term scalability rather than quick feature assembly. Because enterprise programs operate under regulatory and operational pressure, the development approach must reduce risk at every stage.

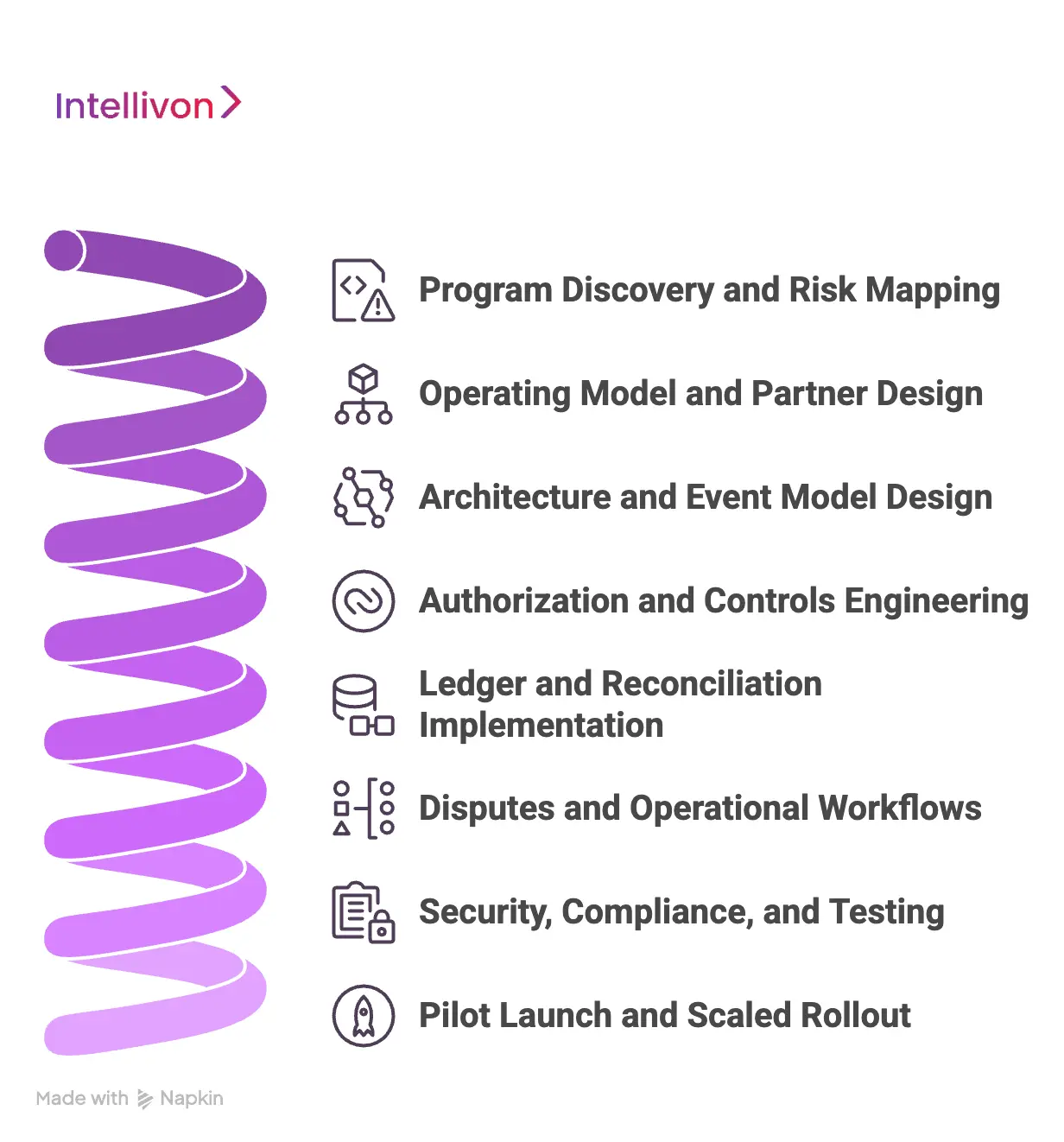

Our methodology follows a disciplined eight-step execution path. Each phase strengthens the next, so the platform can scale without hidden fragility.

Step 1: Program Discovery and Risk Mapping

Every engagement begins with deep program discovery. The team analyzes use cases, funding flows, customer segments, and expected transaction behavior.

Risk mapping happens early. This includes fraud exposure, regulatory obligations, and operational pressure points. As a result, the issuing design reflects real-world conditions rather than theoretical assumptions.

Step 2: Operating Model and Partner Design

Next, the operating structure is defined across sponsor banks, networks, processors, and internal teams. Clear ownership boundaries are established for compliance, settlement, and customer support.

This step reduces coordination friction later. It also ensures the platform aligns with partner expectations from the start.

Step 3: Architecture and Event Model Design

With the operating model in place, Intellivon designs the platform architecture and event flow. The goal is to support high volume, real-time processing without bottlenecks.

Key focus areas include:

- event-driven transaction flows

- service boundaries and isolation

- data consistency models

- integration patterns

Strong architecture at this stage prevents expensive refactoring later.

Step 4: Authorization and Controls Engineering

Authorization logic is engineered to enforce spend policies in real time. The platform evaluates balances, merchant data, velocity rules, and risk signals within milliseconds.

Controls are designed to remain flexible. Therefore, teams can adjust policies as business requirements evolve without rebuilding core systems.

This layer directly protects both revenue and customer experience.

Step 5: Ledger and Reconciliation Implementation

Financial accuracy depends on a robust ledger foundation. Intellivon implements double-entry accounting models that track balances and transaction states precisely.

The reconciliation layer then matches authorization, clearing, and settlement records. Because of this, finance teams gain clean visibility into program economics.

Strong financial infrastructure is often the difference between pilot success and enterprise scale.

Step 6: Disputes and Operational Workflows

Issuing programs generate ongoing operational workload. Intellivon builds structured workflows for disputes, chargebacks, support cases, and exception handling.

Automation is applied where appropriate. However, human review remains in place for sensitive actions.

This balance helps teams manage growth without losing control.

Step 7: Security, Compliance, and Testing

Before launch, the platform undergoes rigorous security and compliance validation. Controls are aligned with PCI expectations, access governance policies, and audit requirements.

Testing covers:

- authorization accuracy

- settlement integrity

- fraud scenarios

- failure recovery

Comprehensive validation reduces production risk and supports partner confidence.

Step 8: Pilot Launch and Scaled Rollout

The platform typically launches with a focused pilot program. This allows teams to observe real transaction behavior and fine-tune controls.

After validation, Intellivon supports structured scale across new customer segments, geographies, and card programs. Because the foundation was designed for growth, expansion happens with less operational strain.

Developing a corporate card issuing platform like Marqeta requires disciplined execution across architecture, controls, and compliance. Intellivon’s eight-step methodology helps enterprises move from concept to production-ready infrastructure with fewer surprises along the way.

By focusing on operating clarity, financial accuracy, and security from the beginning, organizations gain an issuing environment that supports both immediate launch goals and long-term platform growth.

Cost to Develop a Corporate Card Issuing Platform Like Marqeta

At Intellivon, corporate card issuing platforms are built as governed financial infrastructure, not as card features layered onto payment rails. The focus stays on creating issuing environments that operate reliably across sponsor banks, networks, regions, and evolving regulatory expectations. Every architectural decision considers authorization integrity, reconciliation accuracy, and long-term risk exposure from the start.

When budget constraints exist, scope is refined with intent. However, core elements such as real-time controls, ledger accuracy, compliance enforcement, and auditability are never reduced. Therefore, enterprises avoid remediation costs that often appear after launch. Predictability replaces rework, and long-term ROI remains protected.

Estimated Phase-Wise Cost Breakdown

| Phase | Description | Estimated Cost Range (USD) |

| Program Discovery & Regulatory Alignment | Card program design, sponsor bank scope, network requirements, compliance mapping | $10,000 – $18,000 |

| Issuing Architecture Design | Event-driven architecture, authorization flow design, scalability planning | $14,000 – $24,000 |

| Operating Model & Partner Integration | Sponsor bank integration, network readiness, and processor alignment | $12,000 – $22,000 |

| Authorization & Controls Engineering | Spend rules, velocity limits, merchant controls, and real-time decisioning | $15,000 – $28,000 |

| Ledger & Reconciliation Engine | Double-entry ledger, settlement matching, and financial reporting logic | $16,000 – $30,000 |

| Disputes & Operational Workflows | Chargeback handling, case management, support workflows | $10,000 – $18,000 |

| Security & Compliance Controls | PCI scope design, encryption, RBAC, audit logging | $12,000 – $22,000 |

| Testing & Network Validation | Functional testing, risk scenarios, certification readiness | $8,000 – $15,000 |

| Deployment & Scale Readiness | Cloud or hybrid rollout, monitoring, performance tuning | $10,000 – $18,000 |

Total initial investment: $107,000 – $195,000

Ongoing maintenance and optimization: 15–22% of the initial build per year

Hidden Costs Enterprises Should Plan For

Even well-scoped corporate card issuing programs can face pressure when indirect cost drivers are overlooked. Planning for these early protects both timelines and financial performance as transaction volume grows.

- Sponsor bank and network requirements often expand during scale phases

- Compliance overhead increases with audits and regulatory updates

- Fraud operations may require additional tooling and staffing

- Reconciliation complexity grows as transaction volume rises

- Multi-region expansion introduces licensing and data residency costs

- Support operations expand as cardholder volume increases

Because of this, mature cost planning always extends beyond the initial build.

Best Practices to Avoid Budget Overruns

Based on Intellivon’s experience delivering enterprise fintech infrastructure, several patterns consistently lead to more predictable outcomes.

- Start with a tightly defined issuing use case before broad expansion

- Embed real-time controls and ledger discipline into the core architecture

- Use modular services that support multi-program growth

- Plan sponsor, bank, and network alignment early

- Maintain strong observability across fraud, authorization, and settlement

- Design for regulatory change rather than one-time compliance

Enterprises that follow these principles typically avoid the expensive rework that slows many issuing initiatives.

Request a tailored proposal from Intellivon’s enterprise fintech specialists to receive a delivery roadmap aligned with your corporate card strategy, regulatory exposure, and long term growth plans.

Conclusion

Corporate card issuing has evolved into a core financial infrastructure for modern enterprises. Platforms like Marqeta demonstrate how programmable controls, real-time visibility, and disciplined architecture can transform traditional card programs into scalable operating systems. However, long-term success depends on more than APIs. It requires strong partner alignment, accurate ledger design, continuous risk monitoring, and compliance by design.

Organizations that approach issuing with this level of rigor position themselves to scale confidently across products and regions. More importantly, they avoid the operational strain that often surfaces later. With the right foundation in place, corporate card issuing becomes a growth lever that supports embedded finance expansion and sustained enterprise performance.

Build a Card Issuing Platform With Intellivon

At Intellivon, corporate card issuing platforms are engineered as governed financial infrastructure, not as payment features layered onto existing systems. Every architectural decision prioritizes authorization integrity, reconciliation accuracy, and regulatory readiness across complex enterprise environments.

As issuing programs expand across regions, partners, and customer segments, consistency becomes critical. Therefore, performance, compliance posture, and financial visibility remain stable even as transaction volume and operational complexity increase. This disciplined approach helps organizations launch faster while maintaining long-term control.

Why Partner With Intellivon?

- Enterprise-grade issuing architecture designed for regulated fintech ecosystems

- Proven delivery across embedded finance, digital banking, and corporate spend platforms

- Compliance by design with built-in audit readiness and policy enforcement

- Secure, modular infrastructure supporting cloud, hybrid, and multi-region deployments

- AI-enabled risk monitoring, authorization intelligence, and operational automation

Book a strategy call to explore how Intellivon can help you design and scale a corporate card issuing platform with confidence, control, and long-term enterprise value.

FAQs

Q1. What is a corporate card issuing platform?

A1. A corporate card issuing platform allows organizations to create, manage, and control payment cards through software. It connects sponsor banks, card networks, and enterprise systems into one programmable environment. As a result, finance and product teams gain real-time visibility and stronger spend governance.

Q2. How long does it take to build a platform like Marqeta?

A2. A focused corporate card issuing platform typically takes four to six months for an enterprise-ready launch. However, timelines vary based on sponsor bank readiness, network certification, compliance scope, and integration complexity. Starting with a narrow use case usually accelerates time to market.

Q3. What are the biggest challenges in corporate card issuing?

A3. The most common challenges include sponsor bank alignment, network certification, real-time authorization design, and reconciliation accuracy. In addition, many teams underestimate compliance ownership and dispute handling complexity. Addressing these areas early reduces costly rework later.

Q4. Do fintech companies need their own issuing infrastructure?

A4. Not always, but many growing fintech platforms benefit from owning more of the issuing stack. Greater control enables faster product innovation, tighter risk management, and better unit economics. However, the right approach depends on scale, regulatory exposure, and long-term product strategy.

Q5. How much does it cost to build a corporate card issuing platform?

A5. Enterprise-grade platforms typically require an initial investment between $100,000 and $200,000 for a focused first release. Costs increase with multi-region support, advanced fraud tooling, and deep integrations. Ongoing maintenance usually runs about 15 to 22 percent of the initial build annually.