Key Takeaways

-

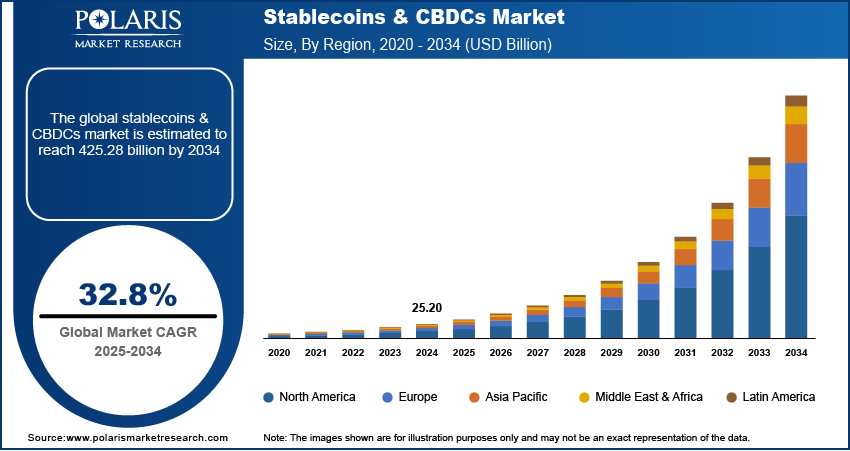

The global stablecoins and CBDCs market sits at USD 25.20 billion in 2024, growing at 32.8% CAGR through 2034, with Stripe and Mastercard already betting on stablecoin rails. The infrastructure window for early movers is narrowing fast

-

A stablecoin banking system is an operational financial infrastructure. It automates treasury, embeds compliance, and integrates with ERP and payroll systems, while a crypto wallet does none of that

-

Blockchain model selection, stablecoin type, and public versus permissioned architecture are not technical decisions. They directly set your compliance exposure, cost structure, and scalability ceiling

-

Most stablecoin banking projects fail due to weak regulatory planning, poor cross-system reconciliation, and prioritizing UI over infrastructure. All decisions are made in the first 90 days of the build

-

A correctly architected platform delivers compounding returns: Intellivon’s client recorded a 38% drop in transaction costs, 90% reduction in accounting overhead, and zero compliance violations post-deployment

Global commerce has quietly outpaced the systems that were built to support it. Somewhere between approving an international vendor payment and that payment actually arriving, three correspondent banks, a currency conversion, and a two-day settlement window get involved, which makes the process slower than anticipated.

Stablecoins change that equation in a way that’s hard to ignore once you see it clearly. This is where value moves across borders in seconds and settles with finality. At the same time, it does so without the friction, opacity, or geography-dependence that traditional rails carry by default. This change happens when programmable money meets enterprise-grade financial architecture. The businesses building at that intersection right now are getting ahead of a fundamental shift in how capital moves.

While the business implications behind a stablecoin-enabled banking system are viable, the question serious decision-makers are sitting with is whether their organization can build it with the depth and precision that enterprise scale actually demands.

That’s where Intellivon comes in. Our experts specialize in building enterprise-grade financial platforms where compliance architecture and engineering rigor are the foundation on which everything else is built. This blog draws from our experience and explains how a stablecoin-enabled banking system is built from scratch.

Why Stablecoin Banking Is Replacing Legacy Rails

Stablecoin banking is earning its place in enterprise strategy because it solves the two things financial decision-makers actually lose sleep over: settlement speed with real finality, and operational friction that quietly bleeds cost at scale.

The market signal has moved well past early adoption. The numbers reinforce what the market is already signaling. The global stablecoins and CBDCs market was valued at USD 25.20 billion in 2024 and is projected to grow at a CAGR of 32.8% through 2034.

This market growth is being driven by expanding adoption across decentralized financial applications, DeFi infrastructure, and an increasing number of government-backed digital currency initiatives that are bringing institutional credibility to the space.

Stripe and Mastercard have already placed significant bets on stablecoin rails, and when incumbents of that size move, the direction of travel becomes clear. Here is why:

1. Faster Settlement, Lower Friction

Legacy payment rails move money on their own schedule, not yours. This is because batch processing, correspondent bank dependencies, and delayed reconciliation cycles create a kind of structural lag that finance teams have simply learned to work around.

Stablecoin banking removes that workaround by settling payments in near real time, with finality, and without the intermediary chain that adds both cost and ambiguity.

The impact is most visible in cross-border transfers, treasury operations, and high-volume B2B payments. In those contexts, even small delays compound into liquidity pressure and manual overhead that quietly drains operational capacity.

2. Always-On Payment Infrastructure

Traditional banking infrastructure was built around banking hours, regional intermediaries, and settlement windows that made sense in a pre-digital economy. Global commerce no longer operates that way.

Stablecoin rails run continuously, which means payments clear on weekends, across time zones, and outside the operating hours of any single regional banking system.

For enterprises managing global teams, international vendors, or digital-first commerce, that kind of always-on availability is a structural advantage that legacy rails simply cannot replicate.

3. Better Treasury Efficiency

One of the more underappreciated advantages of stablecoin banking is what it does for working capital. Under traditional models, treasury teams often pre-fund multiple regional accounts and hold excess balances in various markets just to keep payment flows running smoothly. That trapped liquidity has a real cost.

Stablecoin rails allow treasury teams to move funds more dynamically, reduce idle cash sitting in fragmented accounts, and maintain tighter control over liquidity positions across markets. The result is a more responsive treasury function with less operational overhead.

4. Lower Cross-Border Costs

International payments passing through multiple correspondent banks accumulate fees, delays, and reconciliation complexity at each step. That cost structure makes frequent or smaller cross-border payments economically inefficient for many businesses.

Stablecoins simplify the transfer chain by enabling more direct value exchange between counterparties. For organizations operating across multiple markets, this opens up payment patterns that were previously too costly to run at scale, including high-frequency supplier payments, micro-settlements, and real-time marketplace payouts.

5. Built for Programmable Finance

What separates stablecoin banking from simply being a faster payment method is its capacity to integrate directly into software workflows. Payments can be triggered by API calls, governed by business logic, or tied to specific milestones in supply chain, payroll, or marketplace operations.

That programmability transforms stablecoins from a transaction tool into a financial infrastructure layer. Business rules can automate what previously required manual intervention, and payment logic can sit closer to the operational systems that generate it.

6. Stronger Visibility and Reconciliation

Finance teams managing high transaction volumes know the cost of reconciliation exceptions. Waiting on status updates across disconnected systems, manually matching transactions, and resolving discrepancies consume time and resources that scale poorly.

Stablecoin transactions offer clearer traceability and faster confirmation by design. That visibility reduces the reconciliation burden, shortens exception handling cycles, and gives finance operations a more accurate, real-time picture of where money is and where it has been.

Enterprises are increasingly treating stablecoin banking as a serious operational decision, one that addresses payment latency, tightens liquidity control, and simplifies the complexity of running financial operations across multiple markets, all without stepping outside the compliance and treasury frameworks they already operate within.

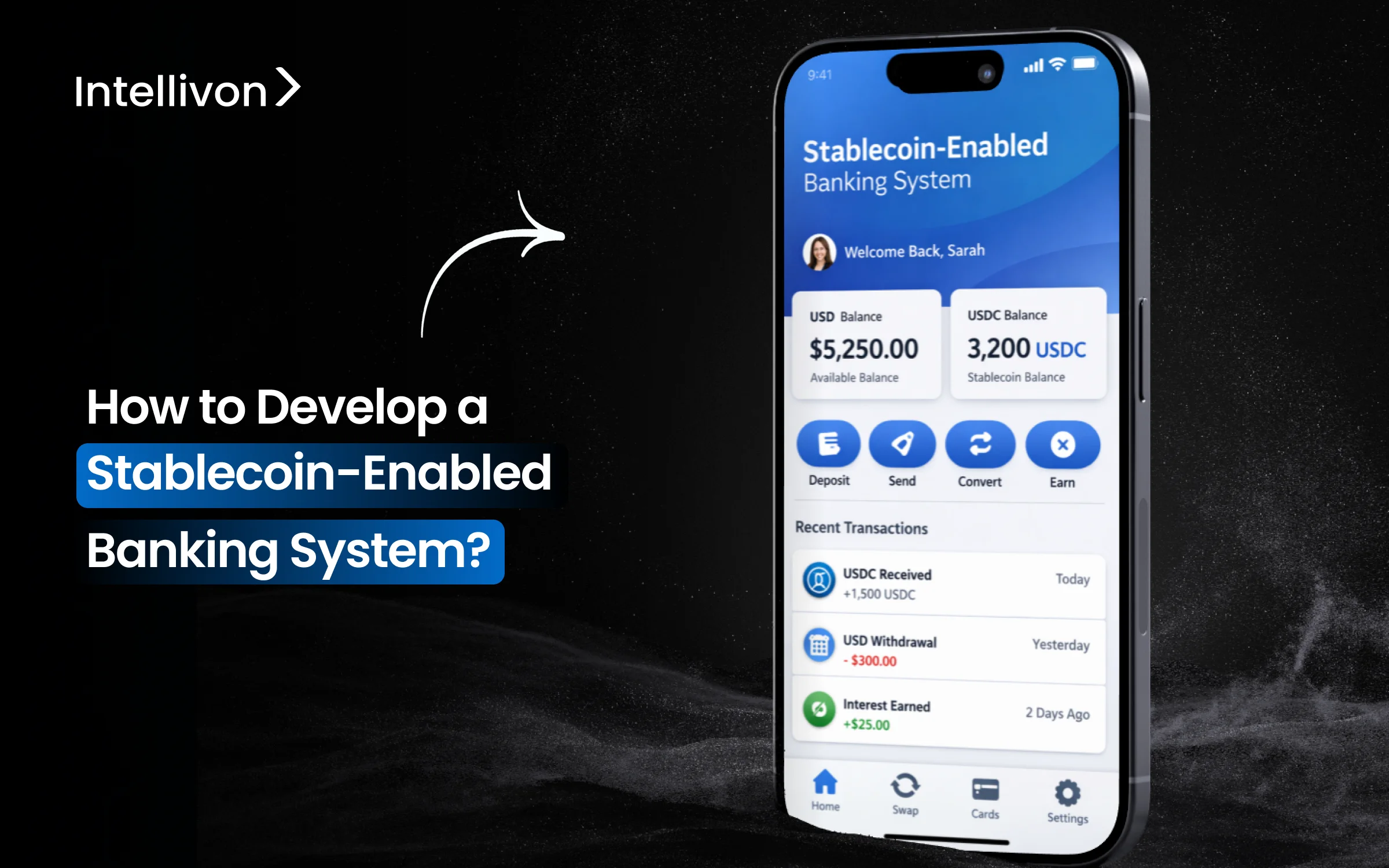

What is a Stablecoin-Enabled Banking System?

A stablecoin-enabled banking system is a financial platform that uses price-stable digital currencies, typically pegged to fiat like the US dollar, to power core banking functions. It handles payments, transfers, lending, and treasury operations on blockchain infrastructure rather than traditional rails.

The result is a banking layer that settles faster, operates continuously, and integrates directly with software workflows without depending on legacy intermediaries.

Why Is This More Than A Crypto Wallet

A crypto wallet is a storage tool. A stablecoin banking system, however, is an operational infrastructure.

The two serve fundamentally different purposes. Therefore, evaluating them on the same terms leads enterprises to significantly underestimate what this build can actually do.

1. Wallets Store. Banking Systems Execute

Wallets hold balances. Stablecoin banking systems, in contrast, run payment cycles, automate treasury movements, and settle vendor obligations. Each function operates within defined business rules. Consequently, the platform works continuously without manual triggers.

2. Automation Replaces Manual Intervention

Traditional payment workflows depend heavily on human steps. Stablecoin banking systems, however, embed approval logic, payment triggers, and settlement rules directly into the platform. As a result, entire payment cycles run without manual processing.

3. Compliance Runs as Core Infrastructure

Enterprise compliance cannot be an add-on. Therefore, a properly built stablecoin banking system integrates KYC, AML screening, and transaction monitoring natively. Regulatory reporting, in addition, runs automatically rather than reactively.

4. Platform Connects Across the Business

A stablecoin banking platform connects directly to ERP systems, treasury tools, and payroll engines. It doesn’t sit separately from operations. Instead, it becomes embedded in how the business manages money daily.

The difference between storing digital currency and building infrastructure around it is significant. Enterprises that understand this distinction early build systems with real, compounding operational value.

How Fiat and Blockchain Layers Work Together

The bridge between traditional currency and distributed ledgers is the most critical component of a stablecoin banking platform development project.

This integration ensures that value can move fluidly between the regulated world of commercial bank accounts and the borderless efficiency of a blockchain.

1. The Gateway: On-Ramp and Off-Ramp Integration

To function as a banking system, the platform must connect to the legacy financial grid via secure APIs. When a user deposits fiat, the system triggers a smart contract to mint an equivalent volume of stablecoins.

This process requires a robust payment gateway that executes KYC and AML checks in real time. Consequently, the digital balance reflected on the ledger remains a legally compliant representation of locked collateral.

2. The Core: Layer 1 and Layer 2 Efficiency

The blockchain serves as the immutable record where every transaction is settled with finality. While Layer 1 provides the underlying security, Layer 2 scaling solutions are typically deployed to handle high-frequency banking tasks.

For instance, utilizing a sidechain enables thousands of near-instant transactions at a fraction of the usual cost. Therefore, the enterprise benefits from the security of a global network without the performance bottlenecks of a public chain.

3. The Custody: Asset Backing and Reserve Management

Every unit of digital currency in circulation must be backed by liquid assets held in a secure, regulated environment. Smart contracts are programmed to provide “Proof of Reserve,” which allows for automated, real-time audits of the underlying collateral.

In addition, sophisticated treasury management tools ensure the peg remains stable even during periods of high market volatility. This transparency is what builds the institutional trust necessary for large-scale adoption and long-term liquidity.

By aligning these layers, organizations can move capital across borders with the speed of data and the reliability of a central bank.

Stablecoin Systems vs Traditional Banking Rails

The fundamental difference between these two systems lies in how they define “truth.” Traditional banking uses a ledger-to-ledger reconciliation process where multiple banks must agree on a balance over several days.

In contrast, a stablecoin system uses a single, shared ledger where the transaction is the settlement. This shift from “verify then move” to “move and verify simultaneously” changes the entire economic profile of a financial institution.

| Feature | Traditional Banking Rails (SWIFT/ACH) | Stablecoin-Enabled Systems |

| Settlement Speed | 2 to 5 business days (T+2/T+5) | Near-instant (Seconds to minutes) |

| Operational Hours | Monday–Friday, 9 AM – 5 PM (Banking days) | 24/7/365 (Including holidays) |

| Transaction Costs | High (Intermediary fees + FX spreads) | Minimal (Network “gas” fees only) |

| Transparency | Opaque; requires manual tracking | Publicly or privately auditable in real-time |

| Programmability | None; requires manual execution | High; supports automated Smart Contracts |

| Intermediaries | Multiple (Correspondent & Central banks) | Peer-to-peer (Direct ledger interaction) |

| Failure Points | High (Human error, bank holidays, mismatched data) | Low (Automated code validation) |

| Liquidity Efficiency | Low (Requires heavy pre-funding) | High (Just-in-time liquidity movement) |

Transitioning to a stablecoin-enabled system rests on moving from a reactive financial model to a proactive, automated one. By adopting these modern rails, enterprises can ensure their capital moves as fast as their ideas.

How Stablecoin Systems Integrate with Enterprise Infrastructure

The true differentiator of a modern stablecoin system is its ability to act as a universal translator. It must take the rigid data from a 30-year-old core banking system and turn it into a programmable asset on the blockchain.

When these integrations are handled correctly, the enterprise gains a massive performance boost without having to rip and replace its foundational technology.

1. Integration with core banking systems

The core banking system is the central nervous system of any financial institution. Integration here requires secure middleware that monitors traditional ledger entries and triggers corresponding actions on the blockchain.

- Event Listening: The system detects a fiat deposit in a commercial bank account via a secure webhook.

- Instruction Matching: It confirms the account details and initiates the minting of stablecoins.

- Legacy Sync: The legacy ledger is updated to show that the fiat is now locked or earmarked for digital use.

2. Integration with payment rails and gateways

To move money in and out of the system, the platform must talk to networks like SWIFT, ACH, or SEPA. This is achieved through API-driven payment gateways that bridge the gap between bank messages and smart contract calls.

- Payment Orchestration: The system automatically chooses the best rail based on the user’s location and urgency.

- Status Tracking: Real-time updates are pushed back to the user interface, so they see exactly when a wire moves from pending to settled.

- Global Access: By connecting to multiple local gateways, the platform can offer low-cost local transfers instead of expensive international wires.

3. Integration with KYC, AML, and compliance tools

Compliance cannot be an afterthought; it must be baked into the data flow. Integration with specialized identity and risk providers ensures that every transaction is screened before it is ever written to the blockchain.

- Automated Onboarding: User data is sent to identity providers for instant verification.

- On-Chain Monitoring: Every wallet address is screened against sanction lists and risk databases in real-time.

- Transaction Scoring: Payments that look suspicious are automatically routed to a human compliance officer for review.

4. Integration with ERP and treasury systems

For large corporations, the stablecoin platform must feed data directly into tools like SAP or Oracle. This ensures that the finance team has a unified view of the company’s cash position across both digital and traditional accounts.

- Automated Bookkeeping: Every blockchain transaction generates a corresponding journal entry in the ERP.

- Cash Positioning: Treasury managers can see their global liquidity in one dashboard, regardless of which currency or chain it lives on.

- Simplified Reconciliation: The system matches digital payments with open invoices, reducing the need for manual tracking.

5. Integration with custody and liquidity providers

A banking system needs a safe place to store assets and a way to swap them. This layer integrates with institutional custodians and market makers to ensure the platform is always secure and liquid.

- Secure Vaulting: Integration with hardware security modules ensures that private keys are never exposed.

- Liquidity Routing: When a user needs to swap USDC for EURC, the system fetches the best price from a connected liquidity provider.

- Instant Rebalancing: The platform automatically moves funds between hot and cold storage based on daily volume trends.

6. Real-time data flow and system synchronization

The biggest hurdle in enterprise builds is ensuring that all systems agree on the truth at the same time. This requires a robust synchronization layer that prevents data silos from forming.

- State Management: The system ensures that a balance change in the digital wallet is reflected in the reporting database instantly.

- Message Queuing: If one system goes offline, messages are queued and processed the moment it returns to ensure no data is lost.

- Audit Trails: A continuous log of every API call and system change is maintained for future regulatory reviews.

7. Common integration challenges in enterprise builds

Building at this level is rarely a straightforward path. Organizations often face hurdles related to data formatting and security protocols that vary between departments.

- Data Mapping: Traditional banks use different messaging standards than blockchain networks, requiring complex transformation layers.

- Latency Mismatches: Blockchains operate on a block-time schedule, while internal databases operate in milliseconds.

- Security Silos: Different departments may have conflicting firewall rules that prevent smooth API communication between the new and old stacks.

The goal is to create a seamless loop where money flows into the system as fiat, moves through the organization as a stablecoin, and exits back into the banking grid whenever it is needed.

Choosing the Right Stablecoin Model

Selecting a model for stablecoin banking platform development is not a one-size-fits-all process. Decision-makers must evaluate whether they want to lean into the massive existing liquidity of public tokens or maintain the tight, walled-garden control of a bank-issued asset.

This choice impacts everything from your licensing requirements to the speed at which you can scale across borders.

1. Single vs multi-stablecoin support

A platform can either focus on one dominant asset or offer a basket of options. While a single-asset approach is easier to manage, a multi-stablecoin model provides the flexibility that global enterprises demand for diverse treasury needs.

| Strategy | Advantages | Trade-offs |

| Single-Asset | Simplified accounting; lower technical overhead; focused liquidity. | Concentration risk, limited to one currency zone, dependent on one issuer. |

| Multi-Asset | Natural FX hedging; broader market appeal; redundant liquidity paths. | Complex reconciliation, higher integration costs, and diverse regulatory risk. |

2. Bank-issued vs third-party stablecoins

The source of the stablecoin determines who holds the risk. Using a third-party token like USDC allows you to tap into a ready-made ecosystem, whereas issuing your own token gives you complete control over the reserve and the revenue generated from those deposits.

- Third-Party Tokens: These are managed by external entities. They offer high trust and immediate utility but leave you at the mercy of the issuer’s policies and fees.

- Bank-Issued Tokens: You mint these against your own reserves. This allows for customized compliance rules and keeps the interest income within your organization, though it requires a heavy regulatory lift.

3. Public vs permissioned blockchain models

The choice of ledger determines who can see and interact with your transactions. Public chains offer the most connectivity, while permissioned (private) chains offer the most privacy.

| Feature | Public Blockchains (e.g., Ethereum, Polygon) | Permissioned Blockchains (e.g., Hyperledger, Corda) |

| Access | Open to anyone; global reach. | Restricted to authorized participants only. |

| Privacy | Transparent; requires advanced shielding for privacy. | Inherently private; data shared only with relevant parties. |

| Speed | Subject to network congestion. | High-speed; optimized for specific enterprise use cases. |

| Cost | Variable gas fees based on market demand. | Predictable, low-cost internal maintenance. |

4. Liquidity, redemption, and reserve factors

A stablecoin is only as good as the promise that it can be turned back into cash. For investors and users, the mechanics of the reserve are the most important factor in the entire system.

- Redemption Windows: How quickly can a user get their fiat back? Real-time systems require a high percentage of cash equivalents in the reserve.

- Reserve Audits: Regular, third-party attestations are required to maintain market confidence and prevent bank-run scenarios.

- Yield Management: Organizations must decide if the interest earned on the fiat reserves will be kept as profit or shared with users to incentivize adoption.

5. Regional availability and compliance impact

Stablecoins are treated differently in every jurisdiction. A model that works in the EU under MiCA regulations might be non-compliant in the US or Asia without significant modifications.

- Legal Mapping: Ensuring that the chosen stablecoin is recognized as a legal digital representation of value in your target markets.

- Sanction Filtering: Implementing geographic blocks (geo-fencing) to ensure your system does not inadvertently serve prohibited regions.

- Tax Reporting: Automated systems must track the cost-basis of transactions to simplify tax filings for both the platform and its users.

By carefully selecting these parameters, you ensure that your banking platform is built on a foundation that can survive both market volatility and shifting global regulations.

Choosing the Right Blockchain Model for Your System

In 2026, the conversation has shifted from experimental pilots to production-grade performance. Enterprise leaders must decide between the massive, open liquidity of public networks and the controlled, high-speed environments of permissioned ledgers.

This choice is the primary driver of your long-term scalability and determines how easily you can plug into the global digital economy.

1. Throughput, fees, and confirmation times

A banking system is only as good as its ability to handle peak volume without slowing down or becoming too expensive.

While traditional systems are limited by banking hours, blockchain performance is measured by how many transactions can be finalized per second.

| Network Category | Average Real-Time TPS | Finality Time | Cost Profile |

| High-Performance L1 (e.g., Solana, ICP) | 700 to 1,000+ | Sub-second to 12 seconds | Ultra-low (Fractions of a cent) |

| Ethereum Layer 2 (e.g., Base, Arbitrum) | 90 to 130 | 2 seconds to 13 minutes | Low (Cents to dollars) |

| Enterprise/Private (e.g., Hyperledger) | 2,000+ | Immediate | Predictable (Fixed infrastructure cost) |

| Legacy Rails (for comparison) | 65,000 (Visa) | 2 to 5 days (Settlement) | High (Percentage-based fees) |

2. Ecosystem maturity and tooling support

You do not want to build every tool from scratch. A mature ecosystem provides pre-built infrastructure for custody, analytics, and wallet management. Networks like Ethereum and Solana have thousands of developers and battle-tested libraries, while newer or private chains might require more custom engineering.

Therefore, choosing a widely adopted network reduces your time-to-market and ensures you can easily find technical talent to maintain the system.

3. Compliance visibility and monitoring tools

For an enterprise, the ability to see and stop a transaction is a non-negotiable requirement. Modern blockchains now support sophisticated RegTech integrations that allow for real-time monitoring.

- On-Chain Analytics: Integration with tools like Chainalysis or Elliptic to score the risk of every incoming wallet address.

- Programmable Filters: The ability to use smart contracts that automatically reject transfers from sanctioned regions.

- Auditable Trails: Providing regulators with a read-only view of the ledger for effortless, real-time reporting.

4. Interoperability with financial systems

Your blockchain should not be an island. It must be able to talk to other chains and traditional financial messaging standards like ISO 20022.

In addition, the arrival of tokenized real-world assets (RWAs) means your banking system might soon need to handle not just stablecoins, but tokenized treasury bills or commercial paper.

Choosing a chain with strong cross-chain bridges and institutional gateways ensures your platform remains relevant as the broader market moves on-chain.

How the blockchain choice impacts scalability

As your user base grows, the limitations of your chosen network will become visible. If you choose a chain with low throughput, your transaction fees will spike during busy periods, eating into your margins.

- Layer 2 Strategy: Using a secondary layer for small, frequent payments while settling large amounts on a more secure Layer 1.

- State Sharding: Selecting a network that can split its workload across parallel chains to prevent bottlenecks.

- Vertical Integration: Building custom “app-chains” that are dedicated solely to your banking traffic to ensure guaranteed performance.

By aligning your blockchain choice with your specific business volume and regulatory needs, you create a system that is built to last through the next decade of financial evolution.

Key Features in an Enterprise Stablecoin Banking Build

When embarking on stablecoin banking platform development, the focus must be on creating a tool that solves the daily friction points of a finance department.

This means moving beyond simple send and receive buttons to a system that understands the complexities of corporate hierarchy, regional compliance, and liquidity management.

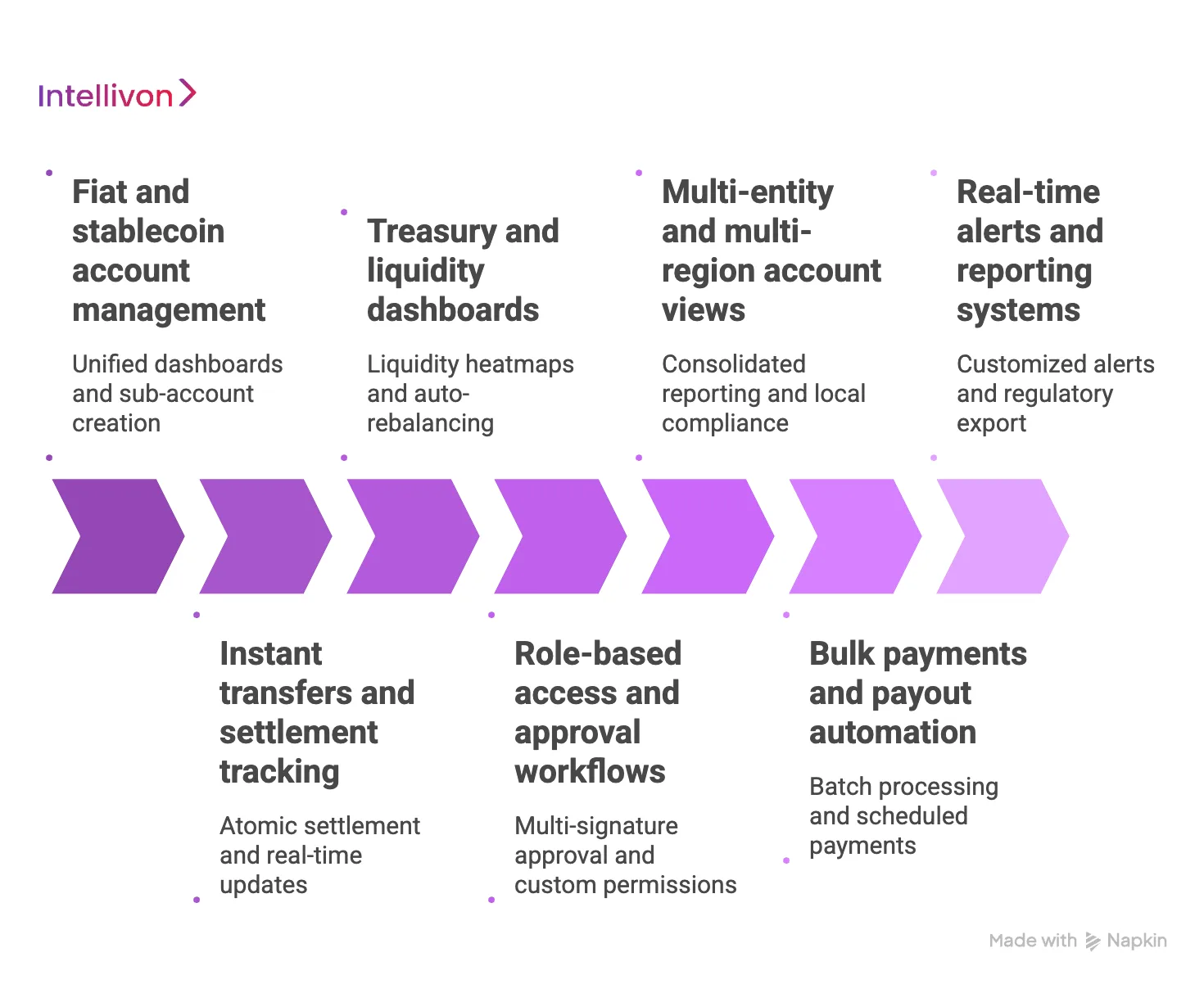

1. Fiat and stablecoin account management

A professional system must present a unified view of both digital and traditional balances. Users should not have to toggle between multiple apps to see their total net worth or current cash position.

- Unified Dashboards: Display USD, EUR, and GBP alongside their stablecoin equivalents like USDC or EURC.

- Sub-Account Creation: Allow departments to create dedicated accounts for specific projects or subsidiaries instantly.

- Transaction History: Provide a deep-searchable ledger that includes both blockchain hashes and traditional bank reference numbers.

2. Instant transfers and settlement tracking

The primary appeal of a stablecoin system is speed. However, for an enterprise, speed is useless without visibility. The system must provide real-time updates on every stage of a transfer.

- Atomic Settlement: Ensure that funds are only moved when both parties satisfy the predefined conditions.

- Status Updates: Provide granular tracking such as Initiated, Compliance Cleared, On-Chain Confirmed, and Finalized.

- Low-Latency Alerts: Notify the relevant teams the moment a large payment is received or sent.

3. Treasury and liquidity dashboards

CFOs and treasurers need to know where their money is and how hard it is working. A robust system provides a high-level view of liquidity across all connected chains and bank partners.

- Liquidity Heatmaps: Visualize where capital is concentrated and identify underutilized funds.

- Auto-Rebalancing: Set rules to move funds automatically if a specific account falls below a certain threshold.

- Yield Monitoring: If the platform is earning interest on reserves, this should be tracked in real-time to optimize income.

4. Role-based access and approval workflows

In an enterprise, no single person should be able to move millions of dollars with a single click. The system must support complex governance structures that mirror the organization’s actual hierarchy.

- Multi-Signature Approval: Require 2 out of 3 or 3 out of 5 executives to authorize high-value transactions.

- Custom Permissions: Allow view-only access for auditors while giving full operational control to the treasury team.

- Policy Enforcement: Set daily or per-transaction limits that cannot be bypassed without higher-level authorization.

5. Multi-entity and multi-region account views

Large organizations operate across dozens of countries and legal entities. The architecture must support a parent-child relationship where the head office can oversee global operations while local offices manage their own daily flows.

- Consolidated Reporting: Roll up the data from all international subsidiaries into a single currency view for the board.

- Local Compliance Toggles: Apply different KYC or tax rules based on the region where the entity is registered.

- Intercompany Clearing: Simplify the process of moving funds between internal entities without external bank interference.

6. Bulk payments and payout automation

For businesses that handle payroll or marketplace payouts, manual entry is not an option. The system must be able to handle thousands of payments simultaneously via API or file upload.

- Batch Processing: Group thousands of individual stablecoin transfers into a single execution to save on administrative time and fees.

- Scheduled Payments: Automate recurring transfers such as monthly salaries or vendor retainers.

- Error Handling: Automatically flag and hold payments with incorrect wallet addresses before they are sent.

7. Real-time alerts and reporting systems

Transparency is the backbone of trust in a digital banking system. The platform must offer a constant stream of data that satisfies both internal stakeholders and external regulators.

- Customized Alerts: Set triggers for unusual activity, such as a transfer to a new wallet or a sudden large withdrawal.

- Regulatory Export: One-click generation of reports formatted for tax authorities or central bank auditors.

- System Health Monitoring: Provide real-time data on the status of blockchain nodes and API gateways to ensure 100% uptime.

Integrating these features ensures that the platform is not just a digital wallet, but a scalable piece of infrastructure that can grow alongside the business.

How Intellivon Builds A Stablecoin-Enabled Banking System

Building a platform that functions as a 24/7 global bank requires an architectural overhaul of traditional financial logic. We treat your infrastructure as mission-critical hardware that must remain resilient under extreme load, market volatility, and relentless regulatory scrutiny.

Our process eliminates the latency of legacy systems, replacing them with a bespoke technical stack designed for the speed of the modern internet.

Step 1: Strategic Value Engineering and Asset Mapping

We begin by identifying the specific financial workflows that will serve as the engine of your business model. While standard banking features are a baseline, we focus on high-value differentiators that attract institutional capital and ensure long-term market dominance.

- Liquidity Orchestration: We map real-time visibility across global sub-accounts and diverse currency pairs.

- Smart Treasury Logic: Our team designs automated cash-sweeping protocols and yield-optimization strategies for your reserves.

- Feature Moats: We identify unique functionalities, such as atomic settlement rails, that make your platform indispensable to your target users.

Step 2: Architecting the High-Concurrency Tech Stack

A 24/7 banking platform requires a modular stack that supports horizontal scaling and zero-downtime updates. We utilize a distributed approach to ensure the frontend remains responsive while the backend handles heavy, asynchronous transaction processing.

| Layer | Strategic Technology Focus | Enterprise Benefit |

| Frontend | Micro-frontend Architecture | Deploy updates to specific modules without site-wide downtime. |

| Backend | High-Performance Go / Rust | Type-safe, low-latency processing capable of thousands of TPS. |

| Data Stream | Distributed Event Streaming | Ensures 100% data consistency across global nodes in real-time. |

| Database | Distributed SQL (ACID Compliant) | Native multi-region resilience and rapid recovery from hardware failure. |

Step 3: Engineering the Blockchain and Ledger Layer

We select and configure the ledger technology that best aligns with your throughput needs and privacy requirements. This layer is the source of truth for every digital dollar in your system.

- Network Selection: We help you choose between high-performance public layers for liquidity or permissioned environments for maximum privacy.

- Smart Contract Hardening: Our developers write and audit the contracts that govern minting, burning, and automated transfers.

- Hybrid Ledgering: We build a high-speed internal engine that mirrors the blockchain, ensuring your users see balance updates in milliseconds.

Step 4: Navigating Global Regulatory Guardrails

Compliance is a structural requirement for banking. We design the system to meet the specific licensing needs of your target markets, ensuring your platform is ready for institutional oversight from day one.

- Jurisdictional Adapters: We build logic specifically for UAE, Singapore, or EU-specific financial mandates.

- Immutable Audit Chains: Every system change and transaction is recorded in a tamper-proof log to satisfy central bank requirements.

- Automated Reporting: We integrate tools that generate regulatory-ready filings at the touch of a button.

Step 5: Implementing Zero-Trust Security Infrastructure

We protect your assets by assuming every request is a potential threat until proven otherwise. Our security layer is integrated directly into the transaction flow rather than sitting on top of it as an afterthought.

- MPC Custody: We implement Multi-Party Computation to ensure that no single employee or attacker can access the full keys to your funds.

- Adaptive Biometrics: Multi-factor authentication tailored for high-value corporate transfers and sensitive administrative actions.

- AI-Enhanced Monitoring: Real-time identity verification and transaction scoring to prevent money laundering and fraud before they occur.

Step 6: Open Banking and Ecosystem Orchestration

Your platform should not exist in a vacuum. We use an API-first strategy to integrate your system with the broader financial world, including ERPs, payroll providers, and global payment gateways.

- Seamless Integrations: Connect your ledger directly to software like SAP, Oracle, or Microsoft Dynamics.

- External Rail Access: We plug your platform into the global banking grid via secure fiat gateways and on-ramp providers.

- Developer SDKs: We provide the tools for your partners to build their own apps on top of your banking infrastructure.

Step 7: Chaos Engineering and Resilience Validation

Before going live, we subject the platform to rigorous stress tests that simulate the worst-case scenarios of the global market.

- Load Simulation: We test the system under massive traffic spikes to ensure transaction finality remains constant.

- Outage Drills: We simulate regional cloud outages to verify that your multi-region failover protocols trigger instantly.

- Security Red-Teaming: We coordinate mock security attacks to validate that your zero-trust layers are impenetrable.

Step 8: Continuous Optimization and Scale Support

The financial landscape shifts daily, and your platform must adapt. We provide ongoing maintenance that focuses on optimizing transaction speeds and lowering your operational costs as you grow.

- Gas Fee Optimization: We refine transaction batching to lower the cost of every move on the blockchain.

- Emerging Tech Integration: We help you integrate new features like predictive treasury analytics and tokenized real-world assets.

- Global Scaling: As you enter new markets, we update your jurisdictional adapters to maintain compliance without needing a rebuild.

In conclusion, partnering with Intellivon means moving from a vision to a high-performance reality. We provide the technical depth and strategic foresight needed to lead the next generation of finance. Your infrastructure should be a growth engine, not a liability.

Security Design for Stablecoin Banking-Grade Systems

In the world of stablecoin banking platform development, security is the primary product. Investors and decision-makers must be confident that the system can withstand both external cyber-attacks and internal collusion.

By implementing a zero-trust architecture, the system assumes that every part of the network is potentially compromised, requiring constant, multi-layered verification for every movement of value.

1. Wallet security and key management

The private keys that authorize transactions are the ultimate prize for any attacker. Protecting these keys is the most critical technical challenge in the entire build.

- MPC Architecture: We utilize Multi-Party Computation to split a single private key into multiple shards distributed across different servers.

- Hardware Isolation: Keys are never stored in a single location or in plain text; they are generated and used within specialized hardware security modules.

- Cold Storage logic: High-value reserves are kept in offline environments, ensuring they are physically unreachable by remote hackers.

2. Transaction authorization controls

Speed must not come at the expense of oversight. A banking-grade system ensures that no single individual can unilaterally move significant sums of capital.

- Multi-Signature Requirements: Large transfers require approval from multiple stakeholders, such as a Treasurer and a CFO, before execution.

- Time-Locking: Sensitive transactions can be programmed with a delay, allowing the security team to intervene if an unauthorized move is detected.

- Spending Limits: Granular caps are placed on specific accounts or departments to contain the impact of a potential account takeover.

3. Smart contract and protocol risks

Because the logic of your bank lives in code, that code must be flawless. Any bug in a smart contract can be exploited to drain the platform’s liquidity in seconds.

- Rigorous Auditing: Every line of code is reviewed by multiple independent security firms before being deployed to a live environment.

- Formal Verification: Using mathematical proofs to ensure the code behaves exactly as intended under every possible scenario.

- Upgradeability Governance: Changes to the underlying protocol require a transparent voting process or a long lead time to prevent malicious updates.

4. Fraud detection and monitoring systems

Traditional banking fraud is often caught days later; in stablecoin systems, it must be caught before the block is confirmed.

- AI-Powered Analysis: Machine learning models scan for unusual transaction patterns, such as a sudden surge in high-value transfers to new addresses.

- Velocity Checks: The system automatically freezes accounts that exceed a predefined frequency of transactions within a short window.

- Blacklist Integration: Real-time synchronization with global databases ensures funds never flow to known high-risk or criminal wallets.

5. Infrastructure security and resilience

The servers and databases that support your ledger are just as vital as the blockchain itself. A banking system must remain operational even during a massive DDoS attack or a regional cloud outage.

- Distributed Denial of Service Protection: Advanced scrubbing layers to filter out malicious traffic before it reaches your core API.

- Multi-Cloud Redundancy: Running identical system nodes across different cloud providers like AWS and Azure to ensure 100% uptime.

- End-to-End Encryption: Using mTLS (Mutual TLS) to ensure that every internal microservice verifies the identity of the service it is talking to.

6. Access control across internal teams

The threat often comes from the inside. Managing who can see and do what within your organization is essential for preventing administrative abuse.

- Least Privilege Principle: Employees are only given the specific permissions required for their daily tasks and nothing more.

- Audit Logging: Every action taken by an administrator, from changing a limit to viewing a user’s history, is logged in a tamper-proof ledger.

- Just-In-Time Access: Sensitive permissions are granted temporarily and revoked automatically after the task is completed.

A robust security design transforms your platform from a vulnerable target into a fortress, providing the legal and financial certainty that institutional investors demand.

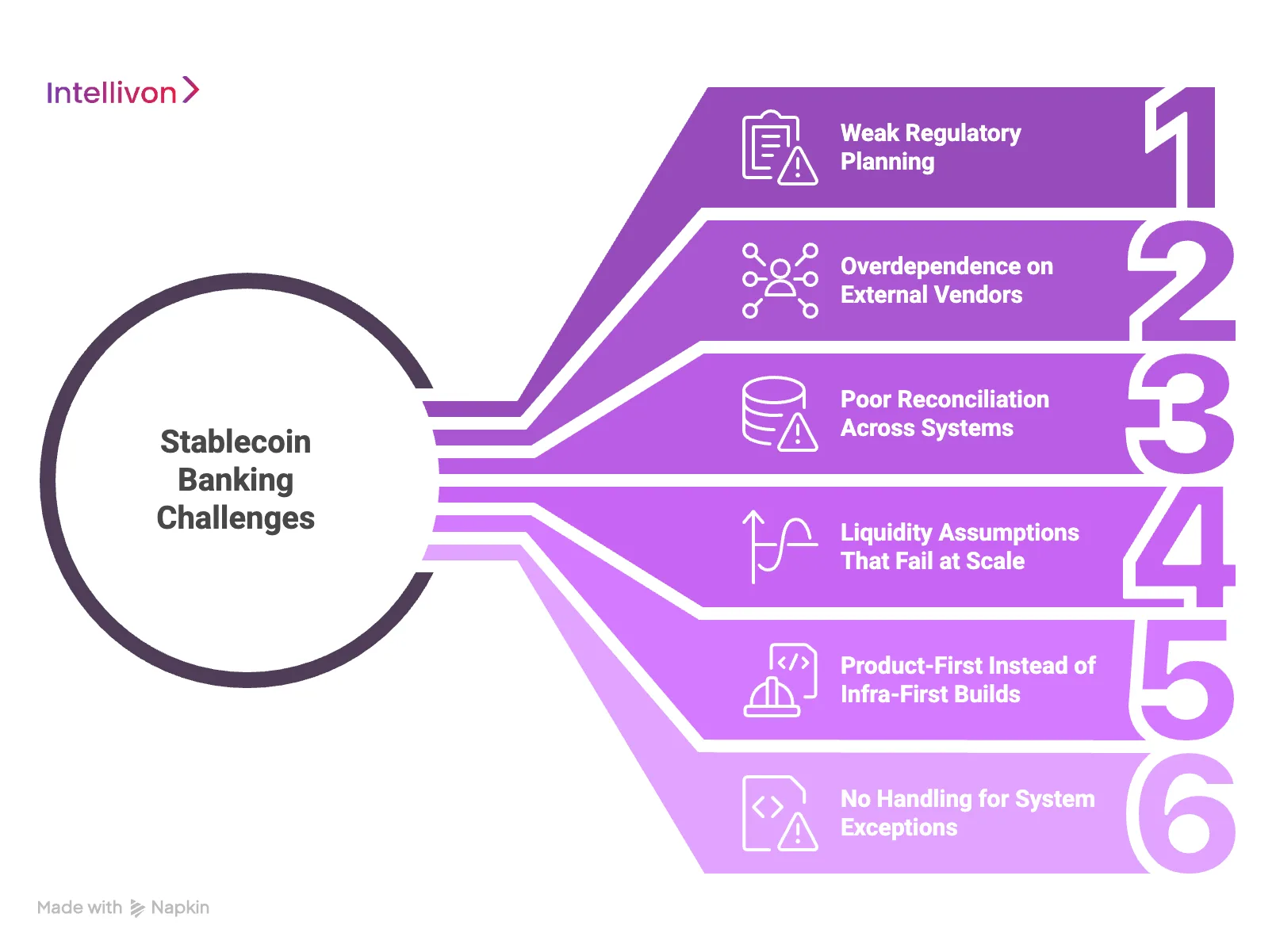

Where Stablecoin Banking Projects Fail (And How We Solve Them)

Transitioning to a decentralized financial model introduces technical and operational hurdles that legacy institutions rarely face. You must manage complex data synchronization while ensuring the system remains impenetrable to evolving cyber threats.

Therefore, understanding these obstacles is the first step toward building a resilient financial infrastructure. These challenges require a shift from traditional maintenance mindsets to a culture of continuous engineering and proactive monitoring.

1. Weak regulatory planning from the start

Many projects fail because they build the technology first and consider the law later. This leads to expensive pivots or complete shutdowns when a regulator determines the platform is operating outside of legal boundaries.

- The Failure: Launching a token or a ledger without a clear jurisdictional strategy, leading to immediate cease-and-desist orders.

- The Solution: We implement automated compliance engines that act as jurisdictional adapters. These tools update internal logic instantly based on the latest central bank directives. Consequently, your enterprise remains audit-ready in every market without manual intervention.

2. Overdependence on external vendors

Relying too heavily on a single provider for critical services like custody, KYC, or cloud hosting creates a massive single point of failure. If that partner goes offline or changes their terms, your entire business is at risk.

- The Failure: A platform going dark because its sole cloud provider experienced a regional outage.

- The Solution: We implement circuit-breaker patterns and multi-vendor redundancy. If one provider fails, the system automatically reroutes traffic to a backup partner. Therefore, your platform remains operational regardless of external failures.

3. Poor reconciliation across systems

A frequent cause of failure is a mismatch between the blockchain ledger and the internal database. This can lead to double-spending, incorrect balances, and a total loss of user trust.

- The Failure: A user sees a balance in their dashboard that does not actually exist on the blockchain, leading to withdrawal failures.

- The Solution: Our architecture utilizes distributed consensus protocols and atomic ledger updates. This ensures that every node in the network agrees on the account state before the transaction finalizes. You maintain 100% data integrity even during peak global traffic.

4. Liquidity assumptions that fail at scale

Systems often work well with a few dozen users but break during market volatility when everyone tries to redeem their stablecoins at once. Without a robust liquidity engine, the platform can face a digital bank run.

- The Failure: Not having enough fiat in the reserve to cover a sudden spike in redemption requests.

- The Solution: By using cloud-native microservices, the platform scales elastically in response to real-time load.

| Component | Scaling Strategy | Benefit |

| Transaction Engine | Horizontal Pod Autoscaling | Handles unlimited concurrent payments without lag. |

| Data Stream | Partitioned Messaging Queues | Prevents bottlenecks during high-volume spikes. |

| API Gateway | Global Edge Distribution | Reduces latency for international users by processing data locally. |

5. Product-first instead of infra-first builds

Teams often focus on the flashy user interface while neglecting the “plumbing” of the system. In banking, the infrastructure, the security, the ledger, and the compliance are the actual product.

- The Failure: A beautiful app that suffers from frequent downtime, slow transaction times, and security vulnerabilities.

- The Solution: We focus on the core infrastructure first, ensuring the foundation is mission-critical grade. Therefore, the final interface reduces cognitive load for your clients while maintaining a premium, enterprise-grade aesthetic.

6. No handling for system exceptions

Blockchains can experience forks, high gas fees, or network congestion. Systems that are not programmed to handle these exceptions will simply stop working or lose funds in transit.

- The Failure: A transaction got stuck in a mempool for days because the system did not account for a sudden spike in network fees.

- The Solution: We build sophisticated middleware and API abstraction layers to bridge the gap between different technologies. This allows for automated rerouting and fee management, ensuring that transactions always reach their destination regardless of network conditions.

In summary, these challenges are the barrier to entry that protects your market position once overcome. By solving these complex problems, you build a technical moat that competitors cannot easily replicate.

Enterprise Use Cases Driving Stablecoin System Adoption

Enterprises are no longer treating blockchain as an experiment but as a mission-critical utility for moving value. By shifting to a stablecoin-enabled model, organizations can bypass the friction of multiple time zones, fluctuating exchange rates, and banking holidays.

This transition transforms the finance department from a bottleneck into a real-time service provider for the entire global operation.

1. Cross-border B2B payments

Traditional international business payments often lose 2% to 5% of their value to intermediary fees and currency spreads. Stablecoins allow companies to send the exact value required without these hidden drains.

- The Workflow: A manufacturer in Germany receives stablecoins from a buyer in Brazil instantly, bypassing the three-day SWIFT waiting period.

- Enterprise Example: SAP has explored using stablecoins like USDC to settle cross-border payments, allowing its enterprise clients to manage accounts payable with far greater speed and lower overhead.

2. Global payroll and contractor payouts

Managing a remote, global workforce is a logistical challenge when using traditional bank wires. Stablecoin systems allow for instant, low-cost salary disbursements to any employee with a digital wallet.

- The Workflow: A tech firm sends a single batch payment that reaches developers in India, Argentina, and Nigeria simultaneously at 3:00 AM on a Sunday.

- Enterprise Example: Deel, a global HR and payroll platform, integrates stablecoin payouts to allow contractors to receive their earnings in USDC, ensuring they aren’t trapped by local banking delays or currency devaluation.

3. Merchant settlement and acquiring flows

E-commerce platforms often hold onto merchant funds for days to manage risk and settlement delays. Stablecoin rails allow these platforms to offer instant payouts, significantly improving merchant satisfaction.

- The Workflow: A marketplace settles vendor sales in real-time, allowing small businesses to reinvest that capital into inventory immediately.

- Enterprise Example: Stripe has reintroduced crypto-payout capabilities, allowing businesses to accept payments and settle them in stablecoins, effectively narrowing the gap between a customer’s click and the merchant’s access to cash.

4. Corporate treasury movement

Large corporations often have millions of dollars sitting idle in regional bank accounts just to cover local expenses. Stablecoin systems allow for just-in-time liquidity management across the entire globe.

- The Workflow: The central treasury office pulls excess liquidity from a Singapore branch and moves it to a London branch in seconds to cover a high-interest debt payment.

- Enterprise Example: Circle works with various institutional treasuries to help them hold cash in digital format, allowing for 24/7 rebalancing without the constraints of commercial bank opening hours.

5. Embedded finance for global platforms

Software-as-a-Service (SaaS) companies are increasingly adding banking features to their own platforms. Stablecoin infrastructure allows them to offer these services without the massive overhead of a traditional banking license in every country.

- The Workflow: A logistics software company allows its trucking partners to hold and spend digital dollars directly within the app.

- Enterprise Example: Grab, the super-app, has integrated digital asset features into its wallet infrastructure, allowing users to interact with stablecoin-based value for everyday services.

6. Internal liquidity optimization

In multi-entity corporations, moving money between a parent company and its subsidiaries is often treated as an external transaction by banks. An internal stablecoin ledger turns these moves into simple database entries.

- The Workflow: A US parent company sends capital to its Mexican subsidiary via an internal stablecoin, avoiding the expensive FX spreads typically charged for USD-to-MXN transfers.

- Enterprise Example: J.P. Morgan utilizes JPM Coin, its own internal stablecoin-like system, to allow its large institutional clients to move liquidity between different branches of the bank instantly and at a massive scale.

By focusing on these high-impact use cases, organizations can achieve an immediate return on investment while building the foundation for a fully digital financial future.

Case Study: Building an AI-Powered Enterprise Stablecoin Banking Platform

Our client, a major fintech provider, was already utilizing stablecoins to bypass the latency of traditional bank transfers. However, their initial infrastructure was not designed for the complexities of institutional scale.

As their transaction volume doubled, they faced mounting manual risks, unpredictable network costs, and a total lack of automated reconciliation. They partnered with us to transform this fragmented setup into a resilient, AI-driven financial powerhouse.

The Strategic Challenges

Before our intervention, the client operated in a state of reactive management. They were forced to overpay on network fees to ensure payments cleared, and their finance team spent weeks manually matching cryptographic hashes to corporate invoices.

- Unpredictable Operational Costs: Volatile blockchain network fees made monthly budgeting impossible.

- Asset De-pegging Risks: The system lacked the intelligence to monitor the health of the stablecoins in their reserve.

- Accounting Gridlock: A lack of automated ledger matching resulted in constant errors and delayed financial reporting.

- Compliance Bottlenecks: Manual reviews of every destination wallet slowed down global fund movements.

- Liquidity Fragmentation: Inefficient routing meant they were paying significantly above market rates for large-scale transfers.

The Intellivon Solution: A Modern Tech Stack

We replaced their manual workflows with a sophisticated, modular architecture. By combining high-performance backend languages with predictive AI models, we built a system that manages the heavy lifting of global finance automatically.

| Category | Strategic Technology Focus |

| Intelligence Layer | XGBoost, Scikit-Learn, AWS SageMaker |

| Backend & Messaging | FastAPI, gRPC, REST |

| Data & Storage | PostgreSQL, Redis, Apache Airflow |

| Security & Ops | Vault, Docker, Kubernetes, Terraform |

The Implementation Roadmap

Our team focused on five core AI-driven pillars to stabilize and scale the client’s operations.

1. Predictive Fee Forecasting

We integrated an AI tool that analyzes network traffic patterns to predict when fees will drop. The platform now identifies the most cost-effective windows to execute non-urgent batch payments, effectively lowering the cost of every transaction.

2. Stablecoin Health Monitoring

We built machine-learning models that constantly monitor market depth and peg stability. If a specific stablecoin shows signs of volatility, the system triggers real-time alerts or automatically moves reserves to a more secure asset to protect company savings.

3. Automated Ledger Matching

Our system uses intelligent matching logic to connect complex blockchain transaction codes directly to the company’s internal invoices. This transition from manual entry to automated reconciliation ensures the finance team maintains a perfect, real-time view of the balance sheet.

4. Predictive Risk Scoring for Compliance

Instead of slow, manual reviews, we implemented an instant wallet screening layer. Every destination address is scanned for links to high-risk or sanctioned entities before the payment is broadcast, ensuring total adherence to international financial laws.

5. Smart Liquidity Routing

The platform now utilizes AI to scan multiple digital markets simultaneously to find the best exchange rates. By automatically selecting the most efficient path for large transfers, we eliminated the hidden fees that previously eroded their margins.

Tangible Business Results

The deployment of this platform provided the client with a technical moat that transformed their operational efficiency.

- 38% Reduction in Transaction Costs: Achieved through automated fee-window optimization.

- 90% Decrease in Accounting Time: Paperwork that previously took weeks is now completed in hours.

- Zero Regulatory Violations: Real-time safety checks replaced human error in the compliance process.

- Eliminated Hidden Fees: Smarter routing ensured they always accessed the most competitive market rates.

- Protected Reserves: Constant market monitoring ensured their capital remained safe during periods of volatility.

By partnering with Intellivon, this client moved from a risky, manual process to a high-trust, automated banking system that is built to scale alongside their global ambitions.

Conclusion

The transition toward stablecoin-enabled banking is a strategic shift from static finance to programmable growth. By eliminating settlement delays and reducing operational friction, organizations can finally align their capital movement with the speed of global trade.

Adopting this resilient infrastructure ensures your enterprise remains competitive, compliant, and ready for the future of digital value. Now is the time to secure your position in the next era of institutional finance.

Why Choose Intellivon To Build a Stablecoin Banking System

Engineering a stablecoin-enabled banking system is a specialized discipline that sits at the intersection of high-frequency distributed systems and rigorous financial regulation.

At Intellivon, we architect the high-trust digital rails that allow global enterprises to move capital at the speed of the internet. Our approach is designed to turn the complexities of blockchain and AI into a seamless, competitive advantage for your organization.

A. Bridging the Gap Between Legacy Finance and Programmable Value

We specialize in the “missing link” of digital banking: the seamless integration of traditional fiat systems with modern blockchain ledgers. By building sophisticated middleware, we ensure your new platform talks to existing banking grids while enjoying the sub-second finality of a stablecoin core.

This allows for a gradual, risk-managed modernization of your financial infrastructure without disrupting current operations.

B. Embedding Predictive Intelligence into the Transaction Layer

As demonstrated in our case study, we believe a modern bank must be “smart” by default.

We embed machine learning models directly into your payment orchestration engine to handle the variables that usually eat into margins.

- Proactive Fee Management: Our AI predicts network congestion to execute transfers when costs are lowest.

- Real-Time Peg Stability Monitoring: We build automated safety nets that monitor stablecoin health to protect your treasury from volatility.

- Automated Reconciliation Engines: We eliminate the “manual matching” nightmare by using AI to sync on-chain hashes with internal corporate invoices instantly.

C. Architecture Designed for Regulatory Permanence

We recognize that the greatest threat to a stablecoin project is not technical failure, but regulatory shift. Therefore, we build compliance into the “source code” of your platform.

From automated Travel Rule messaging to jurisdictional adapters that update logic based on regional law, we ensure your platform remains a “safe harbor” for institutional capital in any market.

D. Resilience Engineered for Global Concurrency

Financial markets never sleep, and neither should your infrastructure.

We utilize a high-concurrency tech stack (Rust, Go, and Distributed SQL) to ensure your system handles massive batch payouts or market spikes without a single millisecond of lag.

| System Milestone | Intellivon’s Engineering Priority | Long-Term Business Value |

| Launch Phase | Rapid MVP of core settlement rails. | Early capture of global liquidity and user trust. |

| Growth Phase | Horizontal scaling of microservices. | Zero performance degradation as transaction volume doubles. |

| Mature Phase | Continuous AI-driven cost optimization. | Maximized margins through reduced overhead and wasted fees. |

By partnering with Intellivon, you are securing a technical moat that protects your capital and scales your global influence.

Are you ready to lead the next generation of global finance?

Contact Intellivon today to begin architecting a 24/7 banking system that is as ambitious as your business goals. Let’s transform your vision into a production-ready reality.

FAQs

Q1: What is a stablecoin-enabled banking system?

A1. A stablecoin-enabled banking system is a financial platform that combines traditional banking rails with blockchain infrastructure to enable real-time, low-cost transactions using stablecoins. It includes wallets, fiat on/off-ramps, compliance layers, and internal ledgers, allowing businesses to manage both fiat and digital assets seamlessly.

Q2: How is a stablecoin banking system different from a crypto wallet?

A2. A crypto wallet only stores and transfers digital assets, while a stablecoin banking system is a full financial infrastructure. It integrates fiat banking, compliance systems, payment rails, and reconciliation layers, enabling enterprises to process transactions, manage liquidity, and operate at scale with regulatory controls.

Q3: What integrations are required to build a stablecoin banking system?

A3. Building a stablecoin banking system requires integration with core banking systems, payment rails (ACH, SEPA, SWIFT), KYC/AML tools, custody providers, and ERP or treasury systems. These integrations ensure seamless movement of funds, compliance monitoring, and accurate reconciliation across fiat and blockchain layers.

Q4: How long does it take to develop a stablecoin banking system?

A4. Development timelines typically range from 3 to 6 months for an MVP and 6 to 12 months for a full enterprise system. The timeline depends on integration complexity, compliance requirements, and the number of features such as multi-currency support, treasury management, and reporting systems.

Q5: How much does it cost to build a stablecoin-enabled banking system?

A5. The cost to build a stablecoin banking system ranges from $50,000 to $150,000+, depending on architecture complexity, compliance layers, integrations, and scalability requirements. Enterprise builds with advanced security, multi-region support, and deep integrations tend to be at the higher end of the range.