In large organizations, major payment failures are rare. Instead, problems often show up as slow drops in revenue, approval rates that stop improving, or rising costs in certain regions. These small issues might not matter much at a smaller scale, but as companies grow and handle more payments in more places and with more methods, it becomes clear that basic payment systems don’t offer enough control or flexibility.

Many companies still rely on payment gateways built for simple sales. While these systems can process payments reliably, they usually use fixed routes and don’t have many ways to retry failed payments. This makes it harder to boost approval rates, manage costs, or keep payment providers reliable.

As payment operations get more complex, orchestration platforms are becoming important tools for businesses that want better control over their payments and finances. This makes the choice between a standard payment gateway and a payment orchestration platform a key decision.

At Intellivon, payment orchestration platforms are built for enterprise scale, with a focus on smart routing, strong reliability, and clear data visibility that helps improve financial results. In this blog, we explain how gateways and orchestration platforms work, compare their main features, and show when orchestration is the best choice for growing businesses.

Key Takeaways Of The Digital Payment Platform Market

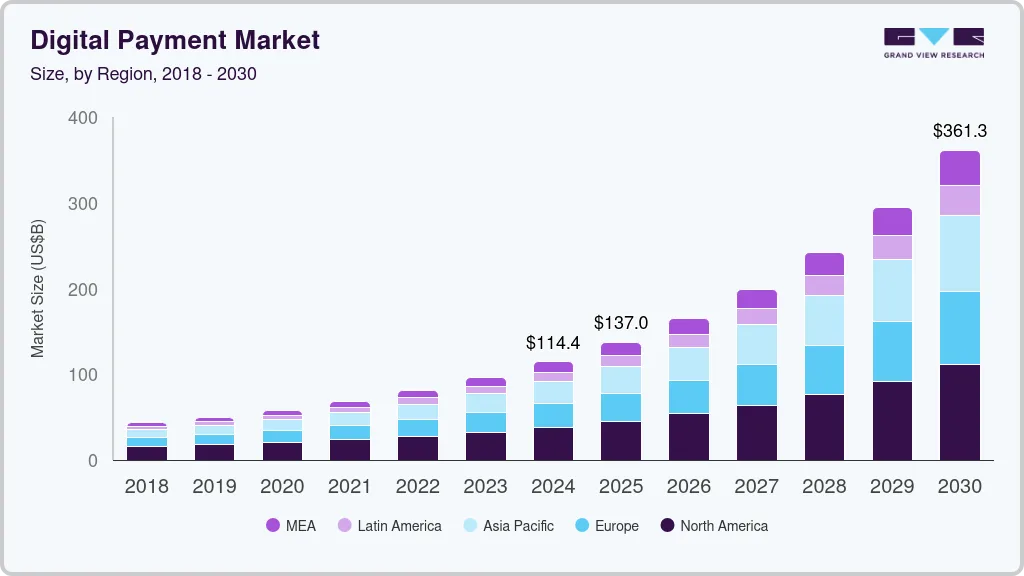

Digital payment platforms are growing rapidly as e-commerce expands, mobile wallet usage rises, and regulators continue to promote cashless economies.

According to the World Bank, by the end of 2021, more than two-thirds of adults worldwide were already sending or receiving digital payments. Consequently, this number is expected to rise further in the coming years.

Market Growth Drivers:

- E-commerce and m-commerce growth is increasing demand for fast and secure payment experiences.

- Embedded payments and open banking APIs are enabling quicker checkouts and more personalized journeys.

- Government digitization efforts and rising smartphone usage continue to accelerate digital payment adoption.

- Innovations such as real-time payments and biometrics are gaining strong traction, especially in retail, which is growing at about 18.77% CAGR.

- North America still leads due to mature infrastructure and major players like PayPal and Stripe.

As digital payment volumes accelerate globally, the pressure on enterprise payment infrastructure continues to rise. What once worked for moderate traffic often struggles under higher scale, cross-border complexity, and approval optimization demands.

Therefore, the decision between an enterprise payment gateway and a payment orchestration layer is no longer purely technical. It has become a strategic choice that directly affects cost control, resilience, and long-term scalability.

What Is A Payment Gateway?

A payment gateway is the technology layer that securely captures payment data, sends it for authorization, and returns the approval or decline to the merchant system.

A payment gateway is the system that moves payment information safely from the customer to the bank side of the network. In enterprise environments, its main job is to execute transactions securely and quickly. At the same time, it ensures payment details are encrypted, authorization requests are sent, and responses come back to the application in real time.

At a lower scale, a gateway often seems enough because it completes the payment flow reliably. However, most gateways follow a single-path model. Therefore, control over routing, retries, and provider selection is usually limited unless additional infrastructure is added.

What It Does

At a practical level, a payment gateway focuses on secure transaction handling and communication.

Core responsibilities include:

- Capturing and encrypting payment details at checkout

- Tokenizing sensitive data where supported

- Sending authorization requests to the processor or acquirer

- Receiving approval or decline responses from the issuing bank

- Supporting capture, void, and refund flows

- Returning transaction status to the merchant application

- Providing basic transaction reports and logs

In most enterprise stacks, the gateway acts as the execution bridge that allows payments to move safely through the system.

Where It Sits in the Enterprise Payment Stack

Inside an enterprise architecture, the payment gateway sits between the customer-facing application and the acquiring side of the network.

A simplified flow looks like this:

Customer → Merchant App → Payment Gateway → Processor/Acquirer → Card Network → Issuer

Because of this position, the gateway mainly handles secure data transfer and authorization. This is why it usually does not manage multi-provider routing, cross-PSP optimization, or unified payment intelligence across providers.

Core Components of a Payment Gateway

Most enterprise-grade gateways include these key building blocks:

- Payment capture interface to collect card or wallet data securely

- Encryption and tokenization module to protect sensitive information

- Authorization engine to communicate with processors and acquirers

- Transaction management layer for capture, voids, and refunds

- Fraud screening hooks or basic rule checks

- Response handler to standardize approvals and declines

- Reporting and reconciliation feeds for finance teams

Together, these components enable reliable payment execution. However, they are primarily built for processing, not for advanced routing or performance optimization at enterprise scale.

What Is A Payment Orchestration Layer?

A payment orchestration layer is the control platform that manages routing, retries, and multiple payment providers through a single unified integration.

A payment orchestration layer sits above gateways and processors and manages how payments flow across them. Instead of sending every transaction through one fixed path, it decides where and how each payment should be processed.

In enterprise environments, this layer provides the control, flexibility, and visibility that single-provider setups often lack.

As payment volumes grow and payment methods expand, this control becomes more valuable. Therefore, many large organizations use a payment orchestration layer to improve approval rates, reduce processing costs, and strengthen resilience across providers.

What It Does

At a practical level, a payment orchestration layer manages and optimizes the entire payment flow.

Core responsibilities include:

- Routing transactions to the most suitable gateway or acquirer

- Automatically retrying failed payments through alternate providers

- Managing multiple PSP and gateway integrations through one API

- Standardizing payment responses across providers

- Supporting unified token management, where implemented

- Providing centralized payment analytics and visibility

- Enabling rule-based control over payment flows

In enterprise stacks, this layer acts as the control center that governs how payments are executed rather than just passing data through one route.

Where It Sits in the Enterprise Payment Stack

In an enterprise architecture, the orchestration layer sits between the merchant application and the underlying payment providers.

A simplified flow looks like this:

Customer → Merchant App → Payment Orchestration Layer → Gateways/Processors → Card Network → Issuer

Because of this position, the orchestration layer can make real-time decisions about routing, retries, and provider selection. This is what enables better approval performance and operational flexibility at scale.

Core Components of a Payment Orchestration Layer

Enterprise-grade orchestration platforms typically include these key components:

- Routing engine to direct transactions based on rules and performance

- Cascading and retry logic to recover soft declines automatically

- Unified provider integration layer for multiple gateways and PSPs

- Token vault or token management layer, where supported

- Fraud and risk orchestration hooks for consistent screening

- Analytics and observability dashboard for performance monitoring

- Rules and configuration engine for business control

Together, these components give enterprises more control over payment performance, cost optimization, and provider flexibility as transaction complexity grows.

Gateway vs Orchestration: Functional and Performance Comparison

A payment gateway executes transactions through a single primary path, while a payment orchestration layer manages routing, retries, and multiple providers to optimize payment performance at scale.

At a glance, both payment gateways and orchestration platforms help move money. However, they serve different control levels inside the payment stack. A gateway focuses on secure transaction execution. In contrast, a payment orchestration layer focuses on managing and optimizing how those transactions are processed across providers.

Additionally, the comparison below highlights where each approach fits, how control differs, and what typically changes as enterprises scale payment operations.

Side-by-Side Comparison

| Category | Payment Gateway | Payment Orchestration Layer |

| What it does | Securely transmits payment data and processes authorizations through a primary provider. | Manages and optimizes payment flows across multiple gateways, PSPs, and acquirers. |

| Who uses it most | Small to mid-sized businesses or enterprises with simple payment flows. | High-volume or multi-region enterprises with complex payment ecosystems. |

| Role in transaction flow | Execution bridge between merchant and processor/acquirer. | Control layer that decides where and how payments are routed. |

| Key functions | Encryption, tokenization, authorization handling, and basic reporting. | Smart routing, cascading retries, multi-PSP management, unified analytics. |

| Performance levers | Limited control over approvals and retries. Mostly provider dependent. | Active control over approval rates, cost routing, failover, and latency. |

| Observability and reporting | Provider-level reports with limited cross-provider visibility. | Centralized dashboards across all providers and payment methods. |

| Tokenization model | Often, provider-tied tokensare with limited portability. | Unified token vault or portable token strategy, where implemented. |

| Routing and cascading | Typically, static routing with manual failover. | Dynamic routing and automated cascadingare built into the platform. |

| Compliance impact | Standard PCI scope based on the gateway integration model. | Broader PCI and governance considerations depending on the architecture. |

| Pros | Simple to implement, reliable for basic processing, and widely supported. | Higher flexibility, better approval optimization, stronger resilience. |

| Cons | Limited control, harder multi-provider management, and less optimization. | More complex to implement and govern at an enterprise scale. |

| Best-fit scenarios | Single-region commerce, moderate scale, limited payment complexity. | Cross-border, multi-PSP, high-volume, or performance-sensitive environments. |

What These Differences Mean in Practice

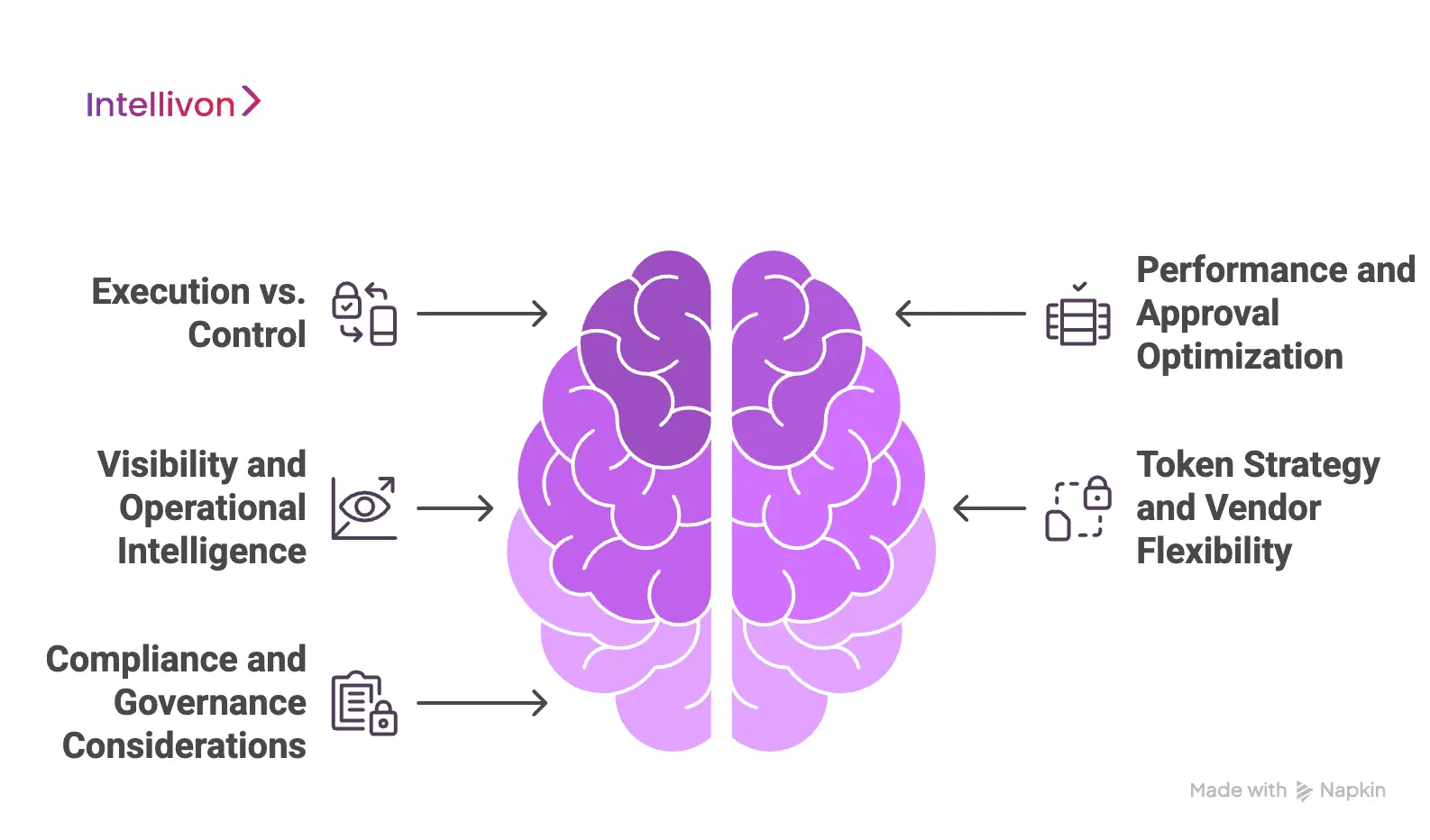

1. Execution vs Control

A payment gateway is primarily an execution component. It ensures payment data moves securely and authorization responses return quickly. At the same time, for many organizations, this is enough in the early stages.

A payment orchestration layer, however, introduces active control over payment behavior. Additionally, it decides which provider handles each transaction and how failures are recovered. Therefore, the conversation shifts from simply processing payments to managing payment performance.

2. Performance and Approval Optimization

With a gateway-only setup, approval outcomes depend heavily on the single configured provider. Here, if authorization rates drop in certain regions or issuers behave differently, the merchant has limited real-time options.

An orchestration layer changes this dynamic. Because transactions can be routed or retried intelligently, enterprises gain more influence over approval rates, latency management, and cost steering. Over time, this can materially affect revenue recovery and payment efficiency.

3. Visibility and Operational Intelligence

Gateways usually provide reporting tied to their own transaction stream. While useful, this view can become fragmented when multiple providers enter the ecosystem.

Orchestration platforms aggregate performance data across providers into one control surface. As a result, finance, payments, and operations teams can monitor trends, compare provider performance, and adjust routing rules based on real outcomes rather than assumptions.

4. Token Strategy and Vendor Flexibility

In many gateway-led environments, tokens are tied to the provider that issued them. However, this can create friction if the business later wants to add or change providers.

Orchestration platforms often introduce a more portable token approach, depending on the architecture. This improves flexibility and reduces dependency on any single provider. However, it also requires stronger governance and security discipline.

5. Compliance and Governance Considerations

Both models must address PCI and data protection requirements. That said, orchestration can expand the governance surface because it centralizes more control and data flows.

Enterprises typically need clearer ownership models, audit trails, and monitoring when adopting orchestration. Therefore, the architectural choice should be evaluated alongside the compliance strategy, not in isolation.

Payment gateways and payment orchestration layers solve different layers of the same problem. At the same time, gateways provide the secure execution foundation that every digital payment flow requires. Additionally, orchestration platforms add a management and optimization layer that becomes more valuable as scale, geographic reach, and provider diversity increase.

For many organizations, the decision rests on understanding when payment complexity, performance pressure, and growth plans justify introducing orchestration as a strategic control layer.

Which Structure Fits Which Enterprise Reality?

A gateway-first model works for simple, single-region payment needs. At the same time, a payment orchestration layer becomes valuable as scale, provider diversity, and performance pressure increase.

Not every enterprise needs orchestration at the beginning. Therefore, the right structure depends on payment complexity, geographic reach, and how much control the business needs. Here, many organizations start with a gateway-first setup. However, they often reassess the architecture as volume grows and payment operations become more demanding.

The scenarios below explain where each approach usually fits best.

When a Gateway-First Approach Is Enough

A gateway-led setup usually works well when payment operations are still simple and predictable.

- Single geography and stable payment mix

If most transactions come from one region and use a consistent set of payment methods, routing needs remain simple. In this situation, a single provider path can deliver stable performance.

- Lower complexity commerce environments

Businesses with straightforward checkout flows and minimal retry needs often see reliable results with a gateway-first model. Therefore, advanced routing logic may not yet provide significant value.

- Limited provider strategy

When the organization chooses to work with one main PSP or acquirer, the need for multi-provider control remains low. A gateway can securely execute transactions without adding extra layers.

- Early-stage embedded payments initiatives

During the early rollout of embedded payments, speed to market often matters more than optimization. Many teams begin with a gateway-first approach to validate demand before investing further.

When Orchestration Becomes the Better Enterprise Move

As payment environments grow more complex, orchestration often becomes a more effective structure.

- Cross-border expansion and local payment requirements

When businesses enter new regions, they must support local payment methods and different issuer behaviors. An orchestration layer helps manage this complexity more effectively.

- Multi-PSP strategy for resilience

Enterprises that want backup providers benefit from intelligent routing and automatic failover. This reduces the risk of relying on a single payment partner.

- High decline sensitivity

In high-volume environments, small improvements in approval rates can recover meaningful revenue. Orchestration enables smarter retries and better provider selection.

- Cost optimization across acquirers and processors

When processing fees vary by provider or region, routing decisions directly affect margins. An orchestration layer gives enterprises the control needed to manage costs more actively.

- Centralized governance and reporting needs

As payment data spreads across multiple providers, visibility becomes harder to maintain. Orchestration platforms bring reporting and monitoring into one unified view.

- Platform and marketplace business models

Marketplaces and multi-merchant platforms require flexible routing and consistent policy enforcement. These requirements usually align well with an orchestration-led architecture.

As payment complexity grows, the choice between a gateway and a payment orchestration layer becomes a strategic architecture decision, not just a technical one.

For many large enterprises, orchestration increasingly provides the control, resilience, and optimization needed to scale payments with confidence.

What Changes Operationally When You Add Orchestration

Adding a payment orchestration layer improves approval performance and visibility, but it also introduces new integration and governance responsibilities.

Adding a payment orchestration layer changes how payments are managed across the enterprise. The platform gives teams more control over routing, retries, and provider performance.

However, this added control also brings new operational responsibilities that require planning and ownership. Enterprises usually see the best results when they prepare for both the benefits and the added complexity.

What Orchestration Improves

When implemented correctly, orchestration strengthens payment performance in several important areas.

- Higher approval rates

Smart routing and automated retries help recover soft declines that would otherwise be lost. As a result, overall authorization performance often improves over time.

- Lower processing costs

Enterprises can route transactions to the most cost-efficient provider based on region, currency, or payment type. This creates more active control over payment margins.

- Faster geographic expansion

New markets usually require local payment methods and regional acquiring coverage. An orchestration layer makes it easier to add new providers without major platform changes.

- Unified visibility

Payment data from multiple providers flows into a single dashboard. Therefore, finance and operations teams gain a clearer and more consistent view of payment performance.

- Reduced lock-in risk

Because the orchestration layer sits above payment providers, switching or adding partners becomes easier. This improves long-term flexibility and negotiating leverage.

What Orchestration Adds

Alongside these benefits, orchestration also introduces new areas that require discipline and governance.

- Deeper integration effort upfront

The initial implementation is usually more involved than a single gateway setup. Teams must carefully design routing logic, provider connections, and data flows from the beginning.

- More moving parts to govern

Multiple providers, routing rules, and retry paths increase system complexity. Therefore, strong monitoring, ownership, and incident management practices become essential.

- Dependency on third parties and how to mitigate it

An orchestration layer still depends on external PSPs and acquirers to process payments. Enterprises typically reduce this risk by maintaining provider redundancy and tracking provider performance closely.

- Routing rule governance and change control

Routing decisions directly affect approval rates and costs. For this reason, rule changes should follow structured review, testing, and approval workflows.

In practice, orchestration transforms payments from a basic processing function into a managed performance system. Enterprises that plan for both the operational gains and the added responsibilities usually achieve the strongest long-term outcomes.

Architecture Models: How Gateways and Orchestration Are Implemented

Enterprises typically implement payment orchestration in two ways: as a separate middleware layer that connects multiple providers, or as an integrated platform that combines gateway and orchestration capabilities.

Once an organization decides to introduce orchestration, the next question is architectural. The implementation model directly affects flexibility, operational load, and long-term control. Most enterprise environments follow one of two patterns. Each approach can work well, but the tradeoffs are different.

Model 1: Separate Orchestration Layer (Middleware)

In this model, the orchestration platform sits as an independent control layer. The enterprise brings its own PSPs, acquirers, and gateway relationships into the system.

This approach offers maximum flexibility because the business can mix and match providers across regions and payment methods. It also gives payment teams strong control over routing strategy and provider selection.

However, this flexibility comes with added responsibility. The enterprise must manage multiple commercial contracts, settlement timelines, support channels, and reporting feeds. Over time, this can increase operational overhead if governance is not well structured.

This model usually fits organizations that want deep control and already have mature payment operations.

Model 2: Integrated Platform (Unified Gateway and Orchestration)

In the integrated model, a single provider delivers both gateway capabilities and orchestration intelligence in one platform. The enterprise connects once and accesses the provider’s network of payment partners.

This approach simplifies implementation and speeds up deployment. There is only one integration to maintain and one primary vendor relationship to manage. In addition, reconciliation and reporting are usually unified by default.

The tradeoff is reduced modular flexibility. Because the platform is more bundled, the enterprise may have fewer options to customize provider selection or swap components independently. Over time, this can increase dependency on the platform vendor.

This model often suits teams that prioritize speed, simplicity, and lower internal operational load.

Middleware vs Integrated Platform: Quick Comparison

| Area | Separate Orchestration Layer | Integrated Platform |

| Integration and operational complexity | Moderate build effort with higher ongoing operational ownership | Faster initial setup with lower internal operational burden |

| Vendor management | Enterprise manages multiple PSP and acquirer relationships | Single primary vendor relationship |

| Reconciliation | Often requires consolidation across providers | Typically unified out of the box |

| Data visibility | High flexibility, but may require aggregation work | Centralized visibility within the platform |

| Speed to market | Slower initial rollout in many cases | Generally faster deployment |

| Ideal user profile | Large enterprises seeking maximum control and provider flexibility | Organizations prioritizing simplicity and faster implementation |

In practice, the right model depends on how much control the enterprise wants to retain versus how much operational complexity it is prepared to manage.

What Changes When You Move to Orchestration?

When orchestration is added, payments shift from a single-path process to a managed performance system. Instead of relying on one fixed provider route, the enterprise gains the ability to actively steer transactions.

This change improves control, visibility, and resilience across the payment stack. Over time, teams move from reactive troubleshooting to proactive optimization. The sections below explain what typically changes in day-to-day operations.

1. Single Integration Point to Multiple Providers

The orchestration layer allows the enterprise to connect to multiple PSPs and acquirers through one unified API. This reduces the need to maintain separate integrations for every provider.

As a result, onboarding new payment partners becomes faster and less disruptive. Engineering teams also spend less time managing provider-specific changes. Over time, this simplifies the overall payment architecture and improves scalability.

2. Routing Optimization and Automatic Failover

With orchestration in place, transactions can be routed based on real-time rules such as geography, cost, or historical success rates. This means the system can choose the most effective provider for each payment.

If a transaction fails due to a soft decline or timeout, the platform can automatically retry through an alternate route. Therefore, fewer legitimate payments are lost due to temporary issues. Over time, this improves both approval performance and customer experience.

3. Unified Insights and Governance

An orchestration layer consolidates payment data from multiple providers into a single operational view. Finance, payments, and risk teams can monitor performance without switching between different provider dashboards.

This improves decision speed and reduces reporting gaps. In addition, standardized data makes it easier to compare provider performance objectively. As payment volume grows, this unified visibility becomes increasingly valuable for operational control.

4. Reduced Lock-In Over Time

Because the orchestration layer sits above individual providers, the enterprise is less tightly bound to any single PSP or acquirer. New providers can be added with minimal disruption to the customer experience.

Similarly, underperforming partners can be phased out more safely. This flexibility strengthens the enterprise’s negotiating position with payment partners. Over the long term, it helps maintain strategic control as the payment ecosystem evolves.

In practical terms, orchestration shifts payments from basic transaction handling to active performance management. Enterprises that adopt it thoughtfully gain stronger control, better resilience, and more room to scale without constant rework.

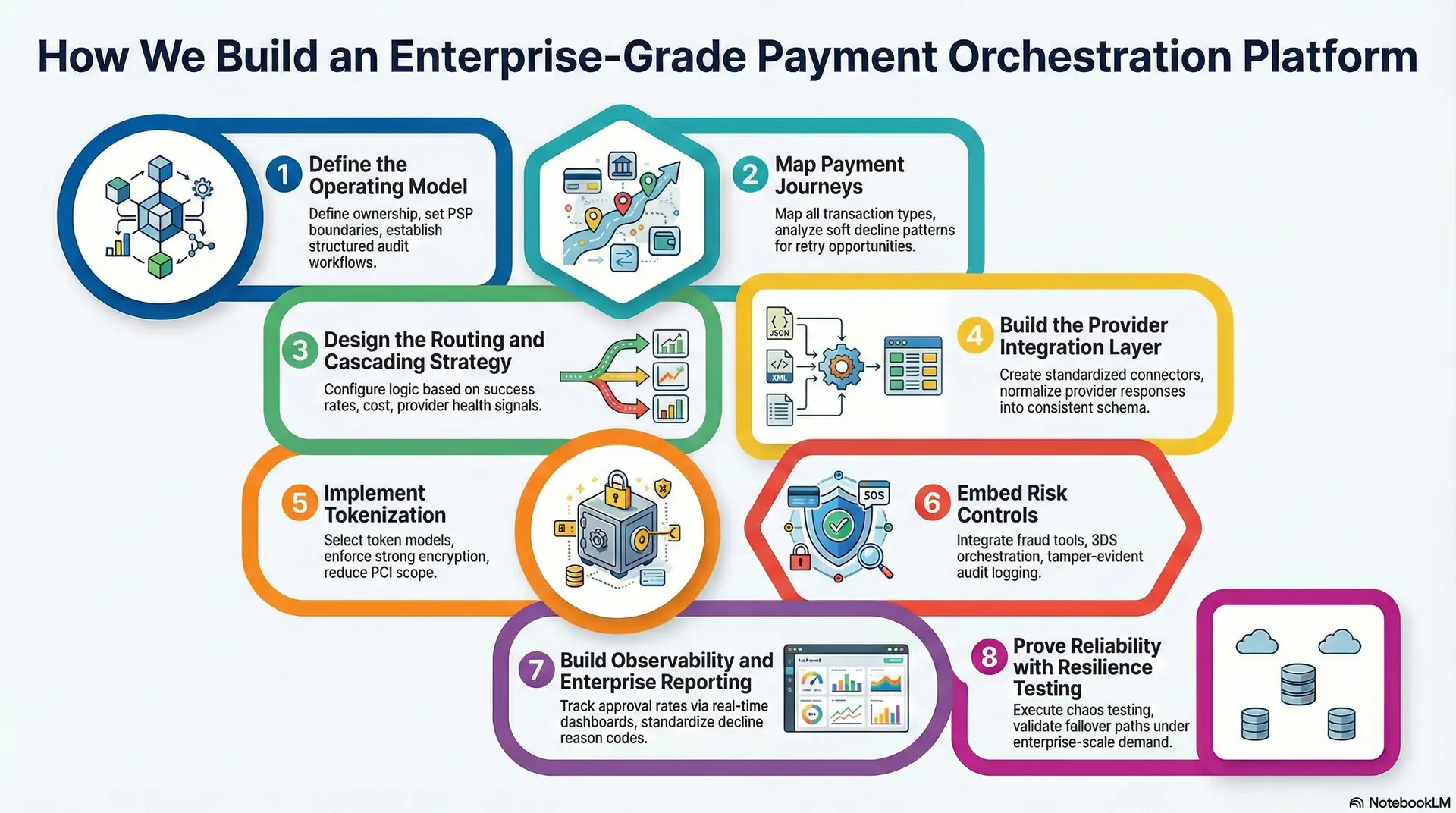

How We Build an Enterprise-Grade Payment Orchestration Platform

Intellivon builds enterprise payment orchestration platforms through a structured process that aligns operating models, routing intelligence, provider integrations, and resilience testing.

At Intellivon, orchestration is treated as core payment infrastructure, not an add-on feature. The delivery approach focuses on control, resilience, and measurable financial impact.

Each phase is designed to reduce operational risk while improving approval performance and cost efficiency. The steps below outline how enterprise orchestration platforms are typically implemented.

Step 1: Define the Operating Model

The process begins by establishing clear ownership across the payment ecosystem. This step prevents confusion once routing logic and provider strategies become more dynamic.

- Ownership of routing rules, risk policy, and provider onboarding is clearly defined.

- Boundaries are set between what PSPs handle and what the orchestration layer governs.

- Structured audit and approval workflows are created for routing and policy changes.

This foundation ensures the platform can scale without creating governance gaps later.

Step 2: Map Payment Journeys

Next comes a detailed review of how payments behave across the business. This phase often surfaces hidden failure patterns that affect revenue.

- All transaction types are mapped, including one-time payments, recurring billing, refunds, partial captures, and reversals.

- Soft decline patterns are analyzed to identify safe retry opportunities.

- Timeouts, fallback paths, and customer-visible behaviors are clearly defined.

This work creates the blueprint required for intelligent routing and controlled retries.

Step 3: Design the Routing and Cascading Strategy

With payment flows understood, the routing decision engine is designed to support performance at scale.

- Routing logic is configured using cost, region, currency, historical success rates, and provider health signals.

- Cascading behavior is defined by a decline category to separate soft failures from hard declines.

- Controlled A/B routing is introduced to validate performance improvements safely.

This step transforms payment processing from static execution to active optimization.

Step 4: Build the Provider Integration Layer

At this stage, the platform is connected to the broader payment ecosystem.

- Standardized connectors are created for PSPs, acquirers, wallets, APMs, and real-time payment rails.

- Provider responses are normalized into a consistent internal schema.

- Idempotency controls, replay protection, and safe retry mechanisms are implemented.

These measures ensure consistent behavior across multiple providers.

Step 5: Implement Tokenization

Token strategy is critical for both security and long-term flexibility.

- The appropriate model is selected, whether provider tokens, network tokens, or an orchestration vault.

- Strong encryption, key management, and access controls are enforced.

- PCI scope is reduced through isolation, segmentation, and compliant data flows.

This approach protects sensitive data while preserving future portability.

Step 6: Embed Risk Controls

Risk management is integrated directly into the orchestration layer to maintain consistency across providers.

- Fraud tools, velocity controls, 3DS orchestration, and anomaly detection are integrated.

- Policy enforcement is applied across markets, MCC categories, and defined risk thresholds.

- Audit logging is configured to remain complete and tamper-evident.

This ensures payment growth does not introduce unmanaged exposure.

Step 7: Build Observability and Enterprise Reporting

Operational visibility is treated as a core requirement rather than an afterthought.

- Real-time dashboards track approval rates, retries, latency, and provider health.

- Decline reason codes are standardized across all connected providers.

- Finance-ready exports support reconciliation and reporting workflows.

This unified view allows teams to monitor performance and act quickly when conditions change.

Step 8: Prove Reliability with Resilience Testing

Before full rollout, the platform is stress-tested under real-world conditions.

- Load testing, chaos testing, and provider outage simulations are executed.

- Failover paths and retry guardrails are validated end-to-end.

- Service level objectives, SLAs, and incident runbooks are formally defined.

This final step ensures the orchestration layer performs reliably under enterprise-scale demand.

Through this structured approach, Intellivon delivers payment orchestration platforms that are built for scale, governed for compliance, and optimized for measurable financial impact.

Conclusion

Payment infrastructure decisions shape more than transaction flow. They influence approval performance, cost control, resilience, and long-term flexibility. A gateway-first model can still work in contained environments. However, as payment ecosystems expand, many enterprises need the added control that a payment orchestration layer provides. The shift is not about adding complexity for its own sake. It is about building a payment foundation that can adapt, optimize, and scale with confidence.

Intellivon helps enterprises design and implement orchestration platforms that deliver measurable ROI without unnecessary risk. If your payment environment is starting to show signs of strain, now is the time to evaluate the next step. Connect with Intellivon to build a payment infrastructure ready for enterprise growth.

Build Enterprise Payment Orchestration With Intellivon

At Intellivon, payment orchestration platforms are engineered as governed enterprise infrastructure, not as routing logic layered onto existing gateways. Every architectural and delivery decision focuses on approval performance, cost control, and operational resilience across complex payment ecosystems.

As enterprise payment environments expand across regions, providers, and payment methods, consistency becomes critical. Governance, observability, and routing intelligence remain stable even as transaction volume and provider diversity increase. This disciplined approach helps organizations protect revenue while maintaining long-term control over their payment stack.

Why Partner With Intellivon?

- Enterprise-grade payment orchestration architecture built for high-volume environments

- Proven delivery across multi-provider, cross-border payment ecosystems

- Compliance-by-design approach with embedded audit visibility and controls

- Secure, modular infrastructure supporting cloud, hybrid, and on-prem deployments

- AI-enabled routing intelligence, performance monitoring, and cost optimization

Book a strategy call to explore how Intellivon can help you design and scale a payment orchestration layer with confidence, control, and measurable enterprise ROI.

FAQs

Q1. What is the difference between a payment gateway and a payment orchestration layer?

A1. A payment gateway securely captures payment data and sends it for authorization through a primary provider. A payment orchestration layer sits above gateways and manages how transactions are routed, retried, and monitored across multiple providers. In simple terms, the gateway executes payments, while orchestration optimizes and controls payment performance at scale.

Q2. When should an enterprise consider adding a payment orchestration layer?

A2. Enterprises typically consider orchestration when payment complexity increases. Common signals include cross-border expansion, rising soft declines, multi-PSP strategies, or growing pressure to optimize processing costs. If payment performance directly affects revenue and customer experience, orchestration usually becomes a strategic priority.

Q3. Does payment orchestration replace the payment gateway?

A3. No. In most enterprise architectures, orchestration does not replace the gateway. Instead, it governs multiple gateways or payment providers from a central control layer. The gateway still handles secure transaction execution, while orchestration manages routing, retries, and performance optimization across the ecosystem.

Q4. How does payment orchestration improve approval rates?

A4. Payment orchestration improves approval rates by using intelligent routing and automated retries. Furthermore, the platform can direct each transaction to the provider most likely to approve it. At the same time, if a payment fails due to a soft decline or timeout, the system can retry through an alternate path.

Q5. Is payment orchestration worth the added complexity for large enterprises?

A5. For many large enterprises, the benefits often outweigh the added complexity. Orchestration introduces stronger control over routing, costs, and provider resilience. Nevertheless, while the initial setup requires careful planning, organizations with high transaction volume or multi-region operations typically see meaningful gains in approval performance, visibility, and long-term flexibility.