Not long ago, virtual cards were mainly simple replacements for physical cards. Now, they play a much larger role in business finance by driving spend management, allowing embedded finance, and giving finance teams real-time control over complex operations. The finance leaders we partner with want to reduce spending loss, strengthen policy enforcement, and gain immediate visibility into spending across teams and regions.

As these demands increase, many organizations are asking if their current virtual card platforms can truly expand and provide the necessary oversight. In our experience, checking off features isn’t enough. Instead, businesses need to quickly identify the shortcomings of basic solutions, including issues with bank support, scheme regulations, multi-entity oversight, and changing regulatory demands.

At Intellivon, we view virtual card management as essential financial infrastructure. Our projects focus on creating programmable controls, strong compliance, and smart risk monitoring. This approach helps clients maintain discipline without losing flexibility. In this blog, we will highlight the key features and design choices that make scalable platforms stand out.

Why Enterprises Are Rapidly Adopting Virtual Card Infrastructure

Enterprises are rapidly adopting virtual card infrastructure for enhanced spend control, security, and operational efficiency in B2B payments. Virtual card management market insights build on the rapid enterprise adoption trends discussed earlier, with B2B segments leading growth through enhanced controls and digital disbursements.

The virtual cards market reached $6.43 trillion in 2026 and is expected to grow to $15.14 trillion by 2031. This reflects a strong 18.67% compound annual growth rate (CAGR) over the forecast period.

Market Insights:

- Rising e-commerce activity, digital payment growth, and stronger security requirements continue to accelerate virtual card adoption. This trend is especially visible across BFSI, retail, and procurement, where NFC and mobile integrations improve usability and control.

- Enterprises increasingly prefer virtual cards because they support granular spend limits, seamless ERP integration, and stronger fraud prevention through tokenization and AI-driven risk detection.

- Cross-border payment needs and expanding supplier ecosystems continue to sustain demand, even as instant payment rails gain wider adoption.

Enterprises are placing greater focus on chargeback automation, embedded compliance, and payment gateway API optimization to strengthen control across virtual card programs.

At the same time, hybrid models that combine card rails with alternative payment networks are emerging to support global orchestration. Industry leaders continue to invest heavily in developer tooling and payment orchestration capabilities, creating a clear strategic opportunity for enterprises building modern virtual card management platforms.

What Is An Enterprise-Grade Virtual Card Platform?

An enterprise-grade virtual card platform is a governed financial infrastructure that enables organizations to issue, control, and monitor virtual payment credentials at scale. Unlike basic expense tools, these platforms embed real-time policy enforcement, multi-entity controls, and compliance safeguards directly into the card lifecycle.

At the enterprise level, the platform must support programmable spend limits, merchant restrictions, audit-ready reporting, and seamless integration with ERP and finance systems. It should also align with sponsor bank requirements, card network rules, and regional regulatory obligations without creating operational friction.

Most importantly, an enterprise-grade system is designed for continuous oversight. Finance, risk, and compliance teams can enforce controls proactively rather than reviewing transactions after the fact.

This architecture helps large organizations maintain financial discipline, reduce fraud exposure, and scale virtual card programs confidently across regions, business units, and partner ecosystems.

SMB Card Tools vs Enterprise Card Infrastructure

At first glance, many virtual card solutions appear similar. Both can issue cards, set limits, and track expenses. However, the underlying architecture and control depth differ significantly.

SMB card tools are typically designed for speed and simplicity. In contrast, enterprise card infrastructure is built for governance, scale, and regulatory resilience. Decision-makers evaluating platforms must look beyond surface features and assess whether the system can support multi-entity operations, continuous compliance, and high transaction volumes.

Key Differences at a Glance

| Area | SMB Card Tools | Enterprise Card Infrastructure |

| Primary focus | Expense convenience | Financial governance and control |

| Scale support | Small teams and single entities | Multi-entity, global programs |

| Spend controls | Basic limits and categories | Programmable, policy-driven controls |

| Compliance readiness | Minimal or add-on | Embedded, audit-ready by design |

| Integrations | Limited accounting sync | Deep ERP and finance ecosystem integration |

| Risk monitoring | Reactive alerts | Real-time, AI-assisted risk intelligence |

| Operating model | SaaS expense platform | Issuer-processor aligned infrastructure |

| Customization | Low configuration depth | Highly configurable and extensible |

In practice, SMB tools work well for early-stage or single-entity organizations. However, enterprises require infrastructure that can consistently enforce policy, meet regulatory requirements, and scale across complex operating environments. Evaluating platforms through this governance lens helps decision-makers avoid costly rebuilds later.

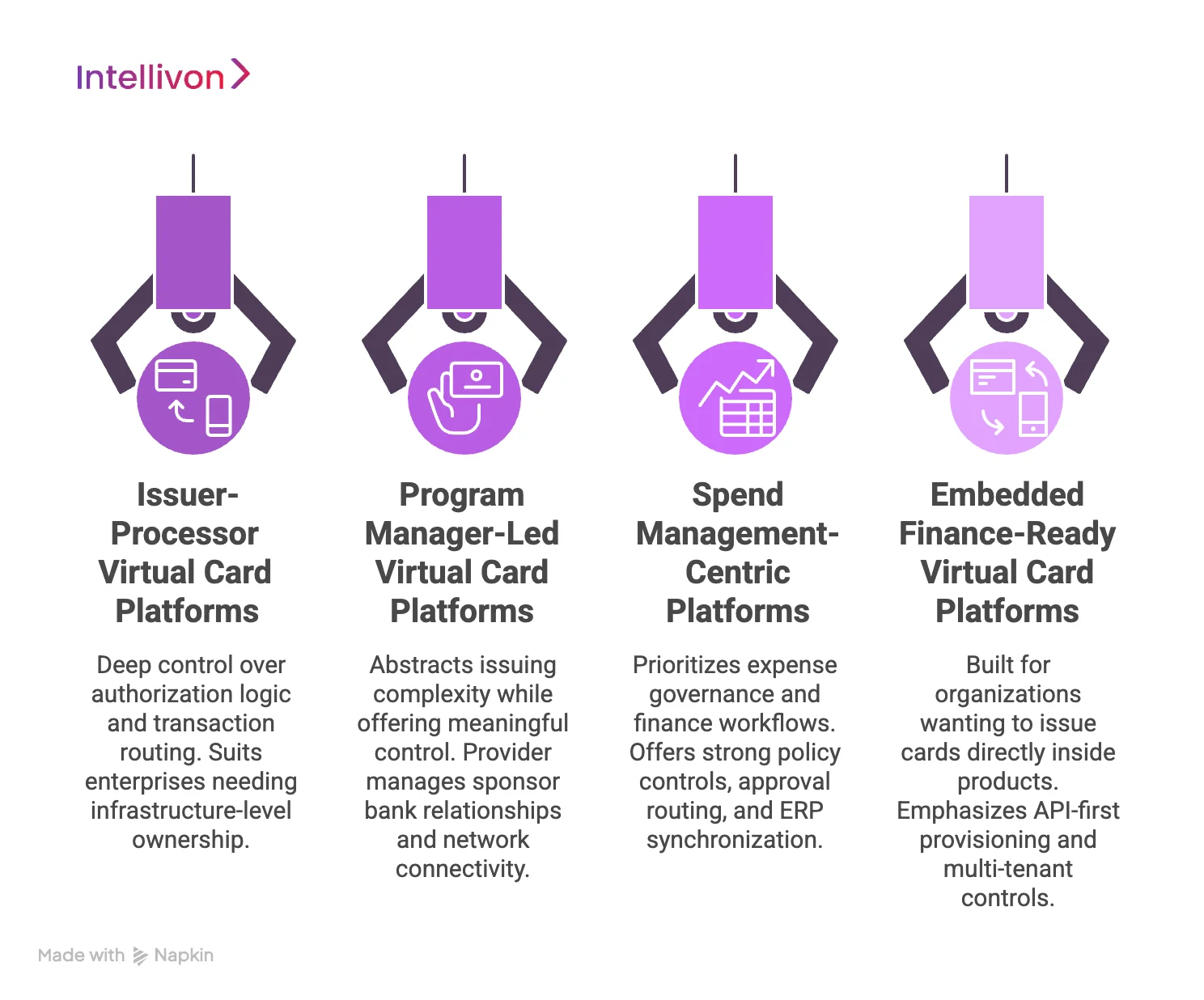

Types of Enterprise Virtual Card Management Platforms

Enterprise virtual card platforms typically fall into four categories based on issuing ownership, control depth, and integration complexity. Selecting the right model depends on scale, compliance exposure, and embedded finance goals.

Not every virtual card platform serves the same enterprise need. Some focus on expense convenience, while others deliver full issuing control. Therefore, understanding the structural differences helps organizations avoid costly platform misalignment later.

From a strategy perspective, the right choice depends on how much control the enterprise wants over the card lifecycle, risk management, and partner dependencies. The sections below outline the primary platform models used across large organizations today.

1. Issuer-Processor Virtual Card Platforms

Issuer-processor platforms sit closest to the card networks and sponsor banks. They provide deep control over authorization logic, card lifecycle events, and transaction routing. As a result, they suit enterprises that need infrastructure-level ownership.

These environments typically support high transaction volumes and complex regulatory requirements. However, they also demand stronger compliance maturity and closer bank alignment. Organizations pursuing embedded finance at scale often evaluate this model first.

2. Program Manager-Led Virtual Card Platforms

Program manager platforms abstract much of the issuing complexity while still offering meaningful control. The provider manages sponsor bank relationships, network connectivity, and parts of compliance oversight. Therefore, enterprises can launch faster without building the full issuing stack internally.

This model works well for companies that want flexibility but prefer shared operational responsibility. Many B2B payment platforms and mid-to-large enterprises start here before moving deeper into issuing ownership.

3. Spend Management-Centric Platforms

Spend management platforms prioritize expense governance and finance workflows over deep issuing infrastructure. They typically offer strong policy controls, approval routing, and ERP synchronization. Consequently, finance teams gain immediate visibility into distributed spending.

However, these systems may limit customization at the network or authorization layer. Enterprises with straightforward procurement or employee spend programs often find this model sufficient. More complex embedded finance strategies usually require a deeper infrastructure approach.

4. Embedded Finance-Ready Virtual Card Platforms

Embedded finance platforms are built for organizations that want to issue cards directly inside their products. These environments emphasize API-first provisioning, multi-tenant controls, and partner ecosystem support. In addition, they enable businesses to monetize payment flows within their own platforms.

This model is gaining traction across marketplaces, SaaS providers, and digital ecosystems. It allows enterprises to transform payments from a back-office function into a revenue and engagement lever.

In practice, platform selection should align with long-term control requirements, not just immediate launch speed. Enterprises that evaluate these models early position themselves to scale virtual card programs without major architectural rework later.

What Data Is Managed In A Virtual Card Platform?

A virtual card platform manages sensitive financial, identity, and transaction data in real time. This includes card credentials, spend policies, user permissions, and audit trails required for enterprise governance.

A modern virtual card platform operates as a controlled data environment, not just a payment utility. Every transaction, limit change, and authorization request generates data that must be governed carefully. Therefore, enterprises evaluating these systems should understand the full data footprint before scaling programs.

At a high level, the platform manages several critical data domains that support security, compliance, and financial visibility. Each domain plays a direct role in maintaining operational control.

1. Card and Credential Data

This layer includes virtual card numbers, tokenized credentials, expiration details, and network identifiers. The platform must protect this information using tokenization, encryption, and secure vaulting.

In addition, lifecycle events such as card creation, suspension, and expiration are tracked continuously. Strong credential governance reduces exposure to fraud and unauthorized usage.

2. Transaction and Authorization Data

Every swipe or API-based payment generates authorization data. This includes merchant details, timestamps, MCC codes, currency values, and approval outcomes.

Enterprises rely on this stream to monitor spend behavior in real time. It also feeds fraud detection engines and reconciliation workflows. Therefore, the platform must process and store this data with low latency and high integrity.

3. Spend Policy and Control Data

Policy data defines how cards can be used across the organization. It includes spend limits, merchant restrictions, velocity rules, and budget allocations.

When structured properly, these controls allow finance teams to enforce guardrails proactively. As a result, policy data becomes one of the most valuable assets inside the virtual card environment.

4. Identity and Access Data

Virtual card platforms must track who can create, approve, fund, or monitor cards. This includes user roles, permissions, authentication logs, and session activity.

Enterprises typically integrate this layer with identity providers and RBAC frameworks. Tight access governance helps reduce insider risk and strengthens audit readiness.

5. Reconciliation and Financial Reporting Data

This domain supports finance operations and audit workflows. It includes settlement files, ledger mappings, invoice links, and ERP synchronization records.

Accurate reconciliation data helps organizations close books faster and maintain financial transparency. In addition, it supports dispute handling and chargeback investigations.

6. Compliance and Audit Trail Data

Every enterprise-grade system must maintain detailed audit logs. These records capture policy changes, user actions, approval flows, and exception handling.

Regulators and internal auditors rely on this visibility to validate controls. Therefore, the platform must ensure logs are immutable, searchable, and retained according to regulatory requirements.

What APIs Are Used To Manage This Data

Modern virtual card platforms depend on APIs to manage sensitive financial and operational data at scale. Instead of relying on manual workflows, enterprises use these interfaces to automate card issuance, enforce policies, and maintain real-time visibility across systems.

Therefore, API depth often determines whether a virtual card platform can support enterprise complexity. Below are the core API categories that typically power enterprise-grade environments.

1. Card Issuance and Lifecycle APIs

These APIs manage the full lifecycle of a virtual card. They allow systems to create, activate, freeze, or terminate cards programmatically.

Common capabilities include:

- Instant virtual card generation

- Bulk card provisioning

- Card status updates and controls

- Expiry and renewal management

Because these actions occur through APIs, enterprises can scale card programs without operational bottlenecks.

2. Authorization and Transaction APIs

Authorization APIs evaluate payment requests in real time. They inspect merchant details, spend rules, and risk signals before approving or declining a transaction.

Key functions typically include:

- Real-time authorization decisioning

- Merchant category validation

- Currency and amount checks

- Transaction metadata capture

As a result, finance and risk teams gain immediate visibility into spend behavior.

3. Spend Control and Policy APIs

Policy APIs enforce how virtual cards can be used across the organization. They allow teams to apply dynamic controls without rebuilding the issuing logic.

These APIs commonly manage:

- Spend limits by user or department

- MCC and merchant restrictions

- Velocity and frequency rules

- Budget-linked card controls

When structured correctly, this layer becomes the backbone of proactive spend governance.

4. Identity and Access Management APIs

Identity APIs regulate who can create, fund, approve, or monitor cards. They typically integrate with enterprise identity providers and RBAC systems.

They support:

- Role and permission management

- Multi-factor authentication triggers

- Session and access logging

- User provisioning and deprovisioning

Tight identity orchestration reduces insider risk and strengthens audit readiness.

5. Reconciliation and Reporting APIs

These APIs connect the virtual card platform with finance and accounting systems. They ensure transaction data flows cleanly into ERP and ledger environments.

Typical use cases include:

- ERP synchronization

- Ledger mapping

- Settlement file ingestion

- Financial reporting automation

Therefore, organizations can accelerate close cycles and reduce manual reconciliation efforts.

6. Webhooks and Event Streaming APIs

Event-driven APIs push real-time updates when key actions occur. This includes transaction approvals, policy violations, and lifecycle changes.

Enterprises use this layer to:

- Trigger fraud monitoring workflows

- Update downstream systems instantly

- Power AI-driven risk models

- Enable real-time alerts and notifications

Because the architecture is event-driven, the platform can support continuous oversight rather than batch-based monitoring.

In combination, these APIs turn the virtual card platform into a programmable control layer for enterprise payments. Organizations that invest in strong API architecture typically achieve faster automation, tighter governance, and more resilient global scaling.

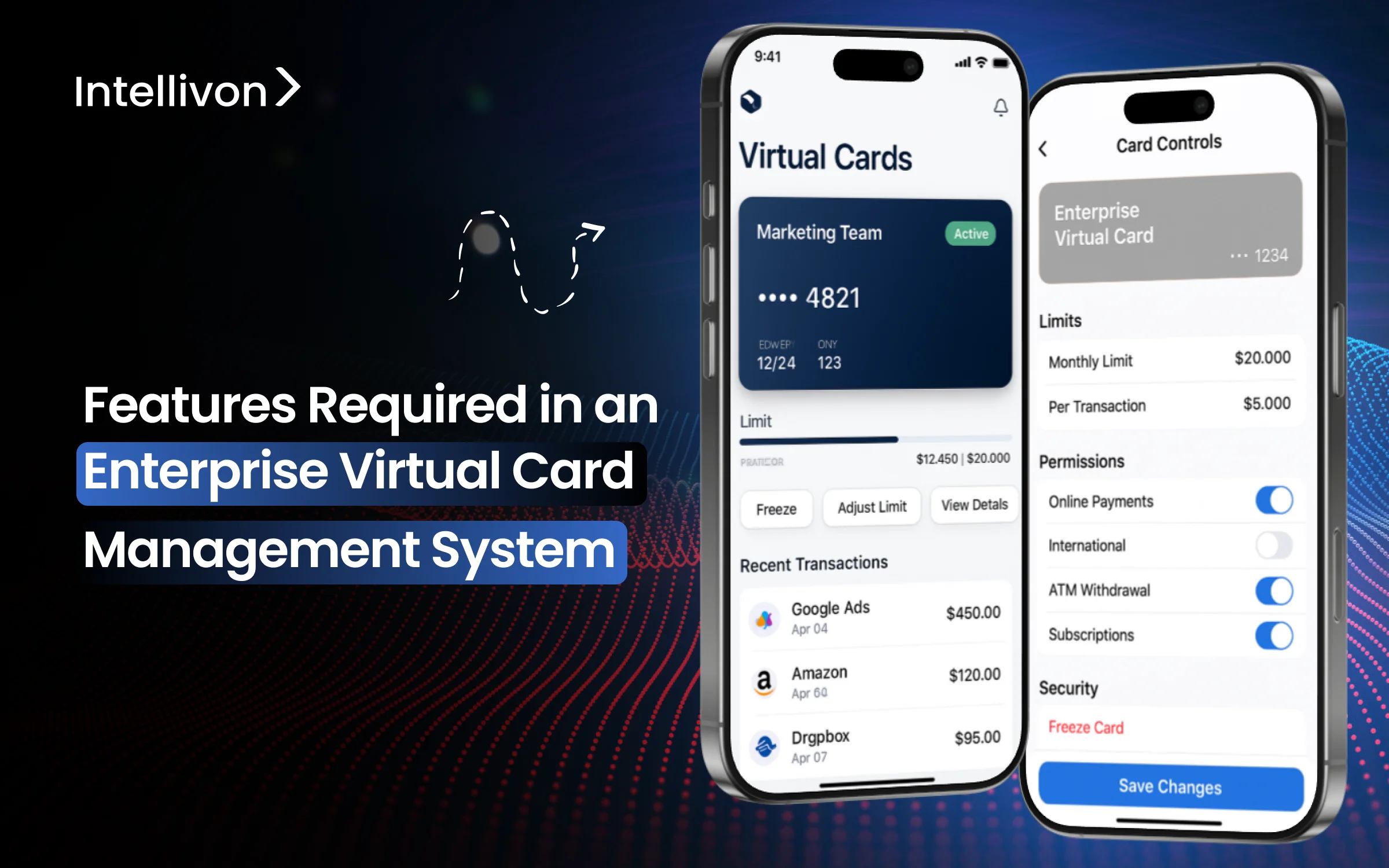

Features Of An Enterprise Virtual Card Management System

An enterprise virtual card platform must combine issuing controls, spend governance, security safeguards, compliance readiness, and deep integrations to support large-scale financial operations.

At a strategic level, the most capable platforms bring together five capability layers. Each layer supports a different aspect of financial control, risk management, and operational efficiency. The table below outlines how these feature groups map to enterprise priorities.

Enterprise Virtual Card Platform Feature Framework

| Capability Layer | What It Enables | Why It Matters For Enterprises |

| Issuing and lifecycle controls | On-demand card creation and management | Supports scalable program growth |

| Spend policy enforcement | Real-time limits and merchant controls | Prevents leakage and budget overruns |

| Security and fraud management | Continuous risk monitoring | Reduces fraud exposure |

| Compliance readiness | Audit and regulatory alignment | Maintains regulatory confidence |

| Program and workflow management | Multi-entity and approval controls | Enables operational governance |

| Developer and integration tooling | APIs and event-driven connectivity | Supports automation and ecosystem scale |

When these capabilities operate together, the virtual card platform becomes a governed financial control layer rather than a simple payment utility.

Enterprises that evaluate features through this structured lens are better positioned to scale programs confidently, maintain compliance, and support future embedded finance initiatives.

Let us dive into each of the categories of the features to get a better understanding of such a platform.

Core Issuing and Card Lifecycle Features

Core issuing features enable enterprises to create, control, secure, and manage virtual cards at scale while maintaining network and regulatory alignment.

The issuing layer forms the foundation of any enterprise virtual card platform. Without strong lifecycle controls, even advanced spend policies and fraud tools lose effectiveness. Therefore, decision-makers should evaluate whether the platform can support real-time provisioning, secure credential handling, and flexible network routing.

The following capabilities define a mature issuing and lifecycle framework.

1. Instant Virtual Card Creation

Enterprises need the ability to generate virtual cards on demand through APIs or admin workflows. This supports vendor payments, employee spend, and embedded finance use cases without delay.

Fast provisioning reduces manual intervention and improves operational responsiveness across distributed teams.

2. Dynamic Card Controls

Dynamic controls allow organizations to adjust card parameters in real time. Teams can modify limits, merchant rules, or usage windows without reissuing the card.

As a result, finance leaders maintain tighter control while preserving flexibility for business units.

3. Tokenization and Secure Provisioning

Tokenization replaces sensitive card data with secure digital tokens. This approach reduces exposure to credential theft and supports safer digital transactions.

Secure provisioning also ensures cards can be deployed into wallets and applications without exposing raw PAN data.

4. Card Lifecycle Management

Lifecycle management tracks every stage of the card journey, from creation to suspension and expiration. Enterprises rely on this visibility to maintain policy consistency and audit readiness.

Strong lifecycle orchestration also supports bulk updates and automated status changes.

5. Multi-network Support

Multi-network capability allows the platform to operate across major card schemes and regional rails. This flexibility supports global expansion and localized payment optimization.

Enterprises benefit from improved acceptance rates and reduced dependency on a single network.

Together, these issuing and lifecycle features create the operational backbone of a scalable virtual card program. Platforms that get this layer right are better prepared to support advanced controls, compliance requirements, and global growth.

Spend Controls and Policy Enforcement Features

Enterprise virtual card platforms must enforce real-time spend controls, merchant restrictions, and dynamic funding rules to prevent leakage and maintain financial discipline.

For most large organizations, spend governance is the primary reason to deploy a virtual card platform. Issuing cards is relatively straightforward. However, enforcing how money moves across teams, vendors, and regions is far more complex.

Therefore, decision-makers should prioritize platforms that apply policy controls at the authorization stage, not after transactions settle. The capabilities below form the core of enterprise-grade spend enforcement.

1. Real-time Spend Limits

Real-time limits allow finance teams to define how much can be spent per transaction, per day, or per budget cycle. These thresholds are enforced instantly during authorization.

This control helps prevent overspending before it occurs. It also reduces the need for manual expense corrections later.

2. MCC and Merchant Controls

Merchant Category Code controls restrict where a virtual card can be used. Enterprises can allow or block specific merchant types based on policy.

In addition, merchant-level rules can limit spend to approved vendors only. This approach strengthens procurement discipline and reduces misuse.

3. Velocity and Frequency Controls

Velocity rules govern how often a card can be used within a defined time window. Frequency controls limit repeated transactions that may indicate abuse or automation risk.

Together, these safeguards help detect abnormal usage patterns early. They also protect programs from rapid-fire fraud attempts.

4. Budget and Department Allocation

Budget-linked controls connect virtual cards directly to cost centers, departments, or project budgets. Every transaction is mapped to the appropriate financial bucket.

As a result, finance teams gain clearer spend visibility and faster reconciliation. Business units also operate within predefined financial guardrails.

5. Just-in-time (JIT) Funding

JIT funding provisions card balances only at the moment of authorization. Instead of preloading funds, the platform releases money dynamically when policy conditions are met.

This model reduces idle capital exposure and tightens cash control. It is particularly valuable for high-volume or vendor-specific programs.

When these controls operate together, the virtual card platform shifts from passive tracking to active financial enforcement. Enterprises that implement strong policy frameworks typically see lower leakage, faster audits, and more predictable spend behavior.

Security, Fraud, and Risk Management Capabilities

Enterprise virtual card platforms must combine real-time monitoring, AI-driven fraud detection, strong credential protection, and structured dispute workflows to reduce payment risk at scale.

As virtual card usage grows, risk exposure expands alongside it. Static controls are no longer sufficient for enterprise environments handling high transaction volumes.

Therefore, the platform must detect, evaluate, and respond to threats continuously across the payment lifecycle. The following capabilities define a resilient fraud and risk framework.

1. Real-time Transaction Monitoring

Real-time monitoring evaluates every authorization request as it happens. The system reviews merchant data, location signals, spend patterns, and policy rules before approving a transaction.

This immediate visibility helps teams identify anomalies early. It also enables faster intervention when suspicious activity appears.

2. AI-driven Fraud Detection

AI models within the virtual card management platform analyze behavioral patterns across users, vendors, and transactions. Over time, the system learns what normal activity looks like and flags deviations automatically.

This approach improves detection accuracy and reduces false positives. As a result, risk teams can focus on genuinely high-risk events.

3. Token and PAN Protection

Strong platforms never expose raw card credentials unnecessarily. Tokenization and secure vaulting protect the Primary Account Number throughout the transaction flow.

This layer reduces the attack surface for data theft. It also supports safer wallet provisioning and digital payments.

4. 3D Secure and Step-up Authentication

Step-up authentication adds an extra verification layer for high-risk transactions. 3D Secure flows, biometric checks, or one-time passcodes can be triggered dynamically.

Enterprises use this capability to balance security with user experience. Higher-risk payments receive stronger verification without slowing routine spend.

5. Dispute and Chargeback Workflows

Dispute management tools track contested transactions from initiation through resolution. They capture evidence, manage case status, and integrate with network processes.

Structured workflows help finance and operations teams recover funds faster. They also improve audit visibility across the dispute lifecycle.

When these protections operate together, the virtual card platform becomes a proactive risk control environment. Organizations that invest in this layer typically reduce fraud losses, improve approval confidence, and maintain stronger trust across their payment ecosystem.

Compliance and Regulatory Readiness Requirements

A virtual card platform must embed PCI alignment, identity verification, AML monitoring, and audit traceability to meet enterprise regulatory expectations.

In enterprise environments, compliance cannot sit outside the virtual card platform. It must be built directly into the transaction and data flow. As programs expand across regions and partners, regulatory exposure increases quickly.

Therefore, decision-makers should evaluate whether compliance controls operate continuously rather than through manual reviews. The capabilities below define a compliance-ready virtual card management system.

1. PCI-DSS Alignment

The platform must support PCI-DSS requirements across card storage, processing, and transmission. This includes encryption, tokenization, and secure key management.

Strong PCI alignment reduces the risk of data exposure. It also simplifies audits and partner due diligence.

2. KYC and KYB Integration

Enterprise virtual card programs often require identity verification for individuals and businesses. The platform should integrate with KYC and KYB providers to validate users, vendors, and partners.

Automated verification helps reduce onboarding risk. It also ensures regulatory obligations are met before cards are issued.

3. AML Monitoring Hooks

AML monitoring capabilities allow the platform to flag suspicious payment behavior. Transaction data should flow into risk engines that support screening, pattern detection, and escalation workflows.

This integration strengthens financial crime controls. It also supports ongoing regulatory reporting.

4. Audit Logging and Traceability

Every critical action inside the virtual card platform must be logged. This includes card creation, policy changes, approvals, and access events.

Immutable audit trails help internal teams and regulators verify control effectiveness. They also improve incident investigation speed.

5. Data Residency and Privacy Controls

Global enterprises must manage where payment and identity data is stored. The platform should support regional data residency rules and privacy frameworks.

This capability becomes essential when operating across multiple jurisdictions. It helps organizations remain compliant without fragmenting their infrastructure.

When compliance is embedded at the platform level, virtual card programs scale with far less regulatory friction. Enterprises that prioritize this layer typically experience smoother audits, stronger partner confidence, and more sustainable global expansion.

Enterprise Program Management and Workflow Features

An enterprise virtual card platform must support multi-entity governance, RBAC, approval workflows, ERP connectivity, and real-time reporting to maintain operational control at scale.

As virtual card programs expand, operational complexity rises quickly. Issuing cards is only one part of the equation. Enterprises also need structured workflows that keep finance, risk, and operations aligned. Therefore, program management capabilities must be embedded directly into the virtual card platform.

The features below help organizations maintain governance while supporting distributed teams and global operations.

1. Multi-entity Program Management

Large organizations often operate across multiple subsidiaries, regions, and business units. The platform should allow each entity to run its own card program while maintaining centralized oversight.

This structure supports local flexibility without losing enterprise control. It also simplifies reporting across complex corporate hierarchies.

2. Role-based Access Control (RBAC)

RBAC ensures users can only perform actions aligned with their responsibilities. Permissions typically cover card creation, funding, approvals, and reporting access.

Strong access governance reduces insider risk. It also supports audit readiness and policy enforcement.

3. Approval Workflows

Approval engines route card requests, limit changes, and funding actions through predefined workflows. These workflows can be configured by department, spend threshold, or risk level.

As a result, organizations maintain financial discipline without slowing business operations. Automated approvals also reduce manual review overhead.

4. Finance and ERP Integrations

Enterprise virtual card platforms must integrate cleanly with ERP, accounting, and treasury systems. Transaction data, ledger mappings, and settlement records should flow automatically.

This connectivity improves financial visibility and accelerates close cycles. It also reduces reconciliation effort for finance teams.

5. Reporting and Reconciliation

Real-time dashboards and structured reports give stakeholders continuous visibility into spend behavior. The platform should support custom reporting across entities, vendors, and cost centers.

Strong reconciliation tooling helps finance teams match transactions quickly. It also improves audit confidence and financial accuracy.

When program management and workflow features are well designed, the virtual card platform becomes easier to govern and scale. Enterprises that prioritize this layer typically achieve cleaner operations, faster approvals, and stronger financial oversight.

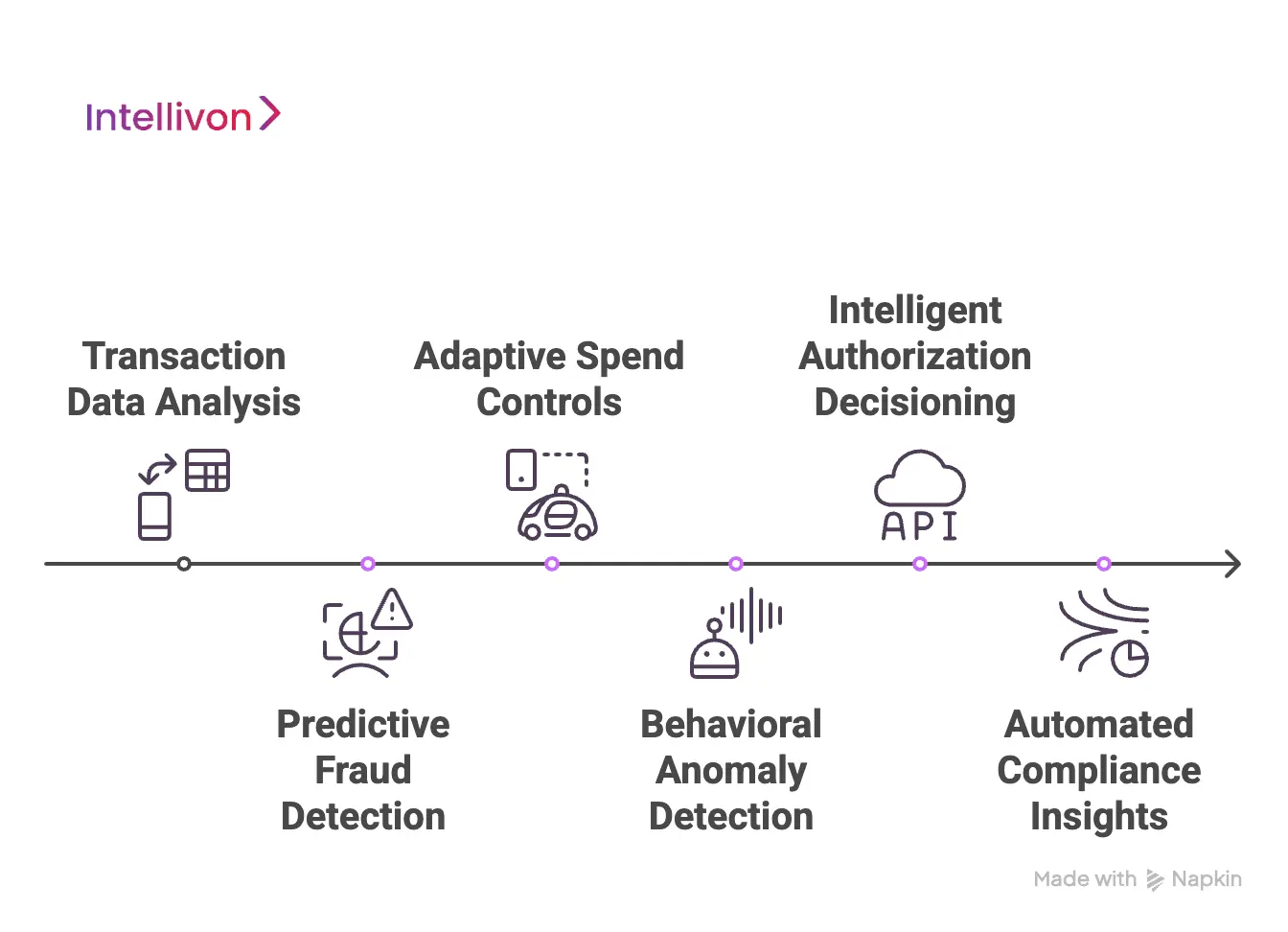

Advanced AI-Powered Features Of A Virtual Card Management Platform

AI enhances a virtual card platform by enabling predictive fraud detection, adaptive spend controls, intelligent anomaly detection, and automated financial decision support at scale.

As transaction volumes grow, rule-based controls alone struggle to keep pace with modern risk patterns. Enterprises are therefore embedding AI directly into their virtual card platform to improve decision speed and accuracy. When deployed correctly, AI shifts the platform from reactive monitoring to continuous financial intelligence.

The following capabilities represent the most impactful AI-driven enhancements.

1. Predictive Fraud and Risk Scoring

AI models analyze historical and real-time transaction behavior to predict risk before authorization completes. Instead of relying only on static rules, the system learns evolving fraud patterns across users and merchants.

Key benefits include:

- Earlier detection of abnormal spending behavior

- Reduced false positives during authorization

- Stronger protection against coordinated fraud attempts

As a result, enterprises improve approval confidence without increasing manual reviews.

2. Adaptive Spend Intelligence

Adaptive models adjust spend thresholds based on user behavior, department patterns, and vendor history. The platform can dynamically tighten or relax controls as risk signals change.

This approach helps finance teams maintain guardrails without slowing legitimate business activity. It also supports more flexible global card programs.

3. Behavioral Anomaly Detection

AI continuously profiles normal usage patterns across employees, vendors, and business units. When activity deviates from expected behavior, the platform triggers alerts or step-up verification.

Typical detection scenarios include:

- Unusual merchant patterns

- Sudden spend spikes

- Geographic anomalies

- Rapid transaction bursts

Because monitoring runs continuously, enterprises gain earlier visibility into emerging risks.

4. Intelligent Authorization Decisioning

Advanced platforms embed AI directly into the authorization flow. The model evaluates contextual signals such as device data, spend history, and merchant risk before returning a decision.

This capability enables more precise approvals and declines. It also supports risk-based authentication strategies that balance security and user experience.

5. Automated Compliance and Audit Insights

AI can scan transaction and policy data to surface compliance gaps or unusual control activity. Instead of waiting for periodic audits, teams receive continuous insight into potential exposure areas.

Over time, this reduces audit friction and strengthens governance posture. It also helps large organizations manage regulatory complexity more efficiently.

When AI is embedded thoughtfully, the virtual card platform evolves into an intelligent financial control system. Enterprises that invest in these capabilities typically achieve stronger fraud resilience, cleaner oversight, and more adaptive global spend programs.

Integration Capabilities Of Virtual Card Platforms

A virtual card platform must provide robust APIs, event-driven connectivity, sandbox environments, and ecosystem support to enable secure enterprise integrations.

For many enterprises, integration depth determines whether a virtual card platform will succeed long term. Even strong issuing and control features lose value if the system cannot connect cleanly with existing infrastructure.

Therefore, decision-makers should evaluate how easily the platform fits into payment flows, finance systems, and digital products. The capabilities below signal true enterprise integration maturity.

1. Issuing APIs and SDKs

Issuing APIs allow enterprises to create, fund, and manage virtual cards programmatically. SDKs further simplify implementation across web and mobile environments.

Strong API coverage reduces manual overhead and accelerates deployment timelines. It also gives engineering teams the flexibility to embed card functionality where needed.

2. Webhooks and Event Streaming

Event-driven architecture ensures systems receive updates the moment something changes. Webhooks push notifications for transactions, policy violations, and lifecycle events.

This real-time flow supports faster decision-making and automated workflows. It also enables downstream risk monitoring and analytics.

3. Sandbox and Testing Environment

A mature virtual card platform provides a dedicated sandbox for safe testing. Teams can simulate transactions, validate controls, and test integrations without affecting production data.

This environment reduces deployment risk and shortens development cycles. It also helps enterprises validate edge cases before scaling programs.

4. Embedded Finance Readiness

Enterprises increasingly want to embed payment capabilities directly into their products. The platform should support multi-tenant controls, white-label configurations, and flexible program structures.

This readiness allows organizations to turn payments into a product feature. It also supports new revenue and engagement models.

5. Partner Ecosystem Support

No enterprise platform operates in isolation. Strong solutions integrate with sponsor banks, processors, identity providers, fraud engines, and ERP systems.

Broad ecosystem support reduces implementation friction. It also ensures the virtual card platform can evolve as the enterprise technology stack grows.

When integration capabilities are well designed, the virtual card platform becomes a natural extension of the enterprise architecture. Organizations that prioritize this layer typically achieve faster deployment, cleaner data flow, and more scalable embedded finance initiatives.

Leading Virtual Card Management Platforms in the Market

Leading virtual card platforms differ in how they handle issuing control, spend governance, and monetization. Evaluating their models helps enterprises benchmark build decisions.

Enterprises rarely evaluate virtual card infrastructure in isolation. Most teams begin by studying existing platforms to understand how modern controls, workflows, and revenue models operate in production. Therefore, reviewing market leaders helps decision-makers benchmark both capability depth and operating strategy.

While requirements vary by scale and regulatory exposure, the platforms below illustrate widely adopted approaches to virtual card management. Each reflects a different balance between automation, control, and infrastructure ownership.

1. Ramp

Ramp is a finance-led virtual card and spend management platform designed to improve cost visibility and control. The platform enables organizations to generate virtual cards instantly, apply policy rules, and monitor transactions in real time.

How Ramp generates revenue:

- Interchange share from card transactions

- Subscription fees for advanced platform features

- Value-added financial automation services

Finance teams typically use Ramp to issue vendor-specific cards and automate approvals. As a result, organizations reduce manual expense reviews and improve policy compliance.

Best known for: strong automation and real-time spend controls.

2. Brex

Brex provides a unified corporate card and spend management environment built for scaling and globally distributed teams. The platform supports issuing multiple virtual cards per user with configurable controls.

How Brex generates revenue:

- Interchange revenue from card usage

- Premium subscription tiers

- Financial services and treasury products

Organizations adopt Brex to combine card issuance, expense tracking, and financial workflows within one system. Consequently, it appeals strongly to high-growth companies seeking operational simplicity.

Best known for: an integrated financial stack for fast-scaling businesses.

3. Airbase

Airbase focuses on finance workflow automation combined with virtual card capabilities. The platform emphasizes real-time budgets, automated approvals, and centralized reporting across procurement and expenses.

How Airbase generates revenue:

- SaaS subscription pricing

- Interchange participation

- Premium workflow and automation features

Enterprises often deploy Airbase to improve spend visibility across distributed teams. In addition, its unified finance layer helps reduce reconciliation complexity.

Best known for: finance workflow orchestration with embedded card controls.

4. Payhawk

Payhawk delivers enterprise expense management supported by tightly controlled virtual cards. The system allows organizations to issue purpose-specific cards for travel, subscriptions, vendors, and project spend.

How Payhawk generates revenue:

- Interchange share

- Platform subscription fees

- Foreign exchange and cross-border fees

Finance teams use Payhawk to enforce granular limits and automate card expiration rules. Therefore, organizations maintain stronger budget discipline and reduce uncontrolled recurring spend.

Best known for: granular, use-case-driven virtual card controls.

5. Highnote

Highnote takes an infrastructure-first approach, offering embedded finance and card issuing capabilities for platforms and enterprises. It focuses heavily on real-time ledgering and modern program management.

How Highnote generates revenue:

- Platform and program management fees

- Interchange participation

- Processing and infrastructure services

Organizations exploring deeper issuing ownership often evaluate Highnote as an alternative to traditional processor models. Its architecture supports advanced control and flexible payment flows.

Best known for: embedded finance and issuing infrastructure.

While these platforms show how virtual card management has matured, enterprise programs still demand carefully designed controls, compliance guardrails, and scalable architecture. The next section examines the core features every enterprise-grade virtual card platform must support.

Conclusion

Enterprise virtual card platforms have become a strategic control layer, not just a payment tool. Organizations that evaluate features through a governance and scalability lens position themselves for cleaner operations and stronger risk oversight.

However, building the right architecture requires deep domain expertise. Intellivon helps enterprises design and deploy secure, AI-enabled virtual card infrastructure that supports growth, compliance, and long-term financial control with confidence.

Build An Enterprise-Ready Virtual Card Platform With Intellivon

At Intellivon, enterprise virtual card platforms are engineered as governed financial infrastructure, not as lightweight payment features. Our delivery approach combines AI-driven risk intelligence, compliance-first architecture, and scale-ready engineering to support high-volume card programs across complex enterprise environments.

Each virtual card platform is designed to integrate cleanly into existing finance and payment ecosystems. We connect sponsor banks, processors, ERP systems, identity providers, and risk engines into a unified control layer that supports secure, real-time spend governance. The result is a virtual card platform built for operational clarity, regulatory confidence, and measurable financial impact across global programs.

Why Partner With Intellivon?

- Compliance-first delivery aligned with PCI-DSS, global privacy frameworks, and card network requirements

- AI-enabled fraud monitoring and spend intelligence to strengthen real-time risk controls

- Deep integration with ERP, treasury, and enterprise finance systems through secure APIs

- Cloud-native architecture built for high-volume processing and global scalability

- Zero-trust security model with human-in-the-loop oversight for continuous governance

Book a strategy call to explore how a custom enterprise virtual card platform can strengthen financial control, support embedded finance initiatives, and enable long-term growth across your organization.

FAQs

Q1. What is an enterprise virtual card platform?

A1. An enterprise virtual card platform is a controlled payment infrastructure that allows organizations to issue and manage virtual cards at scale. It embeds real-time spend controls, compliance safeguards, and integration capabilities. As a result, enterprises gain stronger financial oversight and operational flexibility across departments and regions.

Q2. How do enterprises control spending with virtual cards?

A2. Enterprises control spending by applying real-time limits, merchant restrictions, and budget-linked policies directly at the authorization stage. These controls prevent unauthorized or excessive spending before it occurs. In addition, finance teams gain continuous visibility into transactions, which improves forecasting and audit readiness.

Q3. What compliance requirements apply to virtual card platforms?

A3. Enterprise virtual card platforms must align with PCI-DSS, data privacy regulations, and card network rules. Many programs also require KYC, KYB, and AML monitoring integrations. Therefore, compliance capabilities should be embedded into the platform rather than handled through manual processes.

Q4. When should an organization build its own virtual card platform?

A4. Organizations typically consider building a platform when transaction volumes rise, embedded finance becomes strategic, or existing tools limit control. However, the decision depends on regulatory complexity, integration needs, and long-term ownership goals. Enterprises often evaluate this move during large-scale payment modernization initiatives.

Q5. How long does it take to deploy an enterprise virtual card platform?

A5. Deployment timelines vary based on sponsor bank alignment, network certification, and integration scope. A focused implementation can take a few months, while complex global programs may take longer. Therefore, enterprises should plan for a phased rollout and strong architectural preparation.