In 2026, AI will be integrated into the most sensitive parts of fintech platforms. It will affect transaction approvals, credit decisions, fraud controls, and compliance actions in real time. This change has led industry analysis to view AI in fintech as essential infrastructure instead of an experimental tool, highlighting how significantly these systems impact financial risk and trust.

What has changed is not access to AI but expectations about control. A clear trend is the shift from using AI in isolated cases to governance of decisions across the enterprise. Explainability, auditability, and ongoing oversight are now essential. Leading fintech perspectives for 2026 see this shift as a key marker of growth for regulated platforms.

At Intellivon, we are well aware of this reality. We create fintech platforms where AI functions under real regulatory and operational pressure. Our experience shows that lasting success with AI relies on structure, governance, and ownership of decisions, rather than just new models. In this blog, we look at the AI use cases shaping fintech apps in 2026. We reference real platforms that are using them and explain how enterprises can embrace these capabilities responsibly while preparing for large-scale use and scrutiny.

How Is AI Changing The 2026 Fintech Landscape

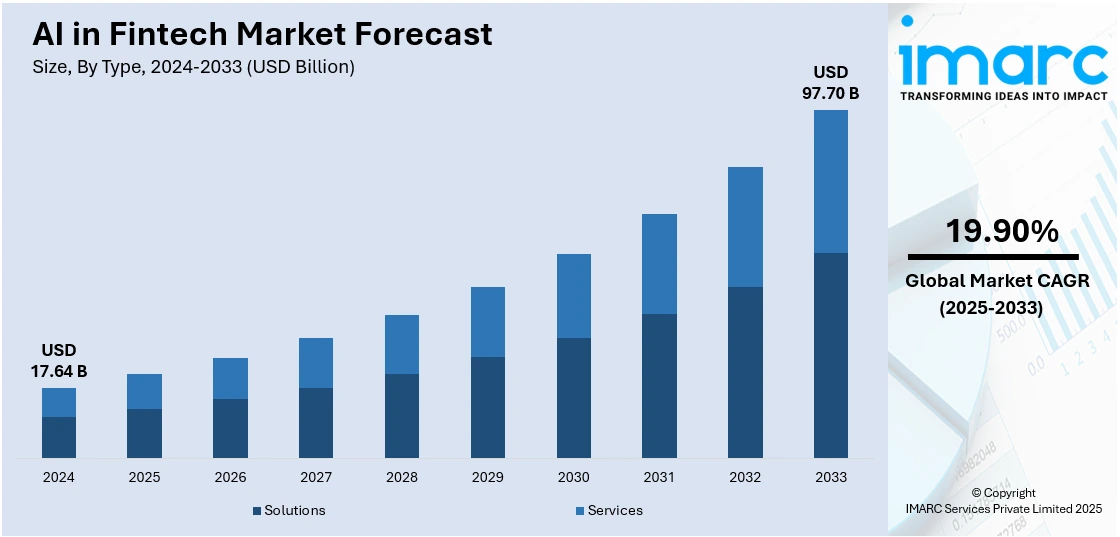

The global AI in fintech market reached a value of USD 17.64 billion in 2025. Growth is accelerating as financial institutions embed AI deeper into core operations. According to IMARC Group, the market is projected to reach USD 97.70 billion by 2034. This reflects a strong compound annual growth rate of 19.90% between 2026 and 2034.

At present, North America leads this expansion. The region accounted for more than 36.8% of the global market share in 2024.

This dominance is driven by early AI adoption, mature financial infrastructure, and sustained enterprise investment. As a result, many large-scale fintech AI deployments are being shaped and validated in this region first.

Key Applications of AI in Fintech

- Fraud Detection: Autonomous AI agents flag transaction anomalies within milliseconds, helping platforms counter increasingly sophisticated, AI-driven fraud attacks.

- Credit and Lending: AI manages risk scoring, income verification, and approvals, now powering nearly 60% of digital lending workflows globally.

- Customer Service: Intelligent agents resolve up to 78% of customer queries independently, using natural language processing to deliver contextual and personalized support.

- Payments and Compliance: AI enables real-time verification and dynamic regulatory checks by leveraging open finance and transaction-level data.

Major Players Shaping This Landscape

Large technology providers and financial networks are leading AI adoption in fintech. Cloud and infrastructure players like Intel, AWS, IBM, Microsoft, and NVIDIA enable AI at scale, while firms such as ComplyAdvantage focus on risk and compliance intelligence.

Payment networks, including Visa and Mastercard, are embedding AI into transaction flows through agentic commerce. At the same time, newer startups are advancing AI-driven underwriting and credit decisioning, accelerating the shift from experimentation to production.

Challenges Enterprises Must Prepare For

As AI scales, new risks emerge:

- Autonomous AI-driven attacks increase pressure on identity, authentication, and blockchain systems.

- Regulatory frameworks like ISO 20022 and stricter data governance now require trust-by-design architectures, especially for cross-border use.

Meanwhile, as AI models converge, differentiation becomes harder. This pushes enterprises to prioritize measurable ROI over experimentation.

Top AI Technologies Powering FinTech Apps in 2026

AI adoption in fintech is entering a new phase. The focus is shifting from isolated machine learning models to technologies that support scale, governance, and continuous decision-making.

In 2026, the most impactful AI technologies are those that can operate reliably inside regulated financial systems. These technologies are already influencing how modern fintech platforms are being designed.

1. Agentic AI for Autonomous Financial Workflows

Agentic AI systems can execute multi-step tasks without constant human input. In fintech, this means handling workflows such as loan processing, dispute resolution, and transaction monitoring. Each step is coordinated through policy rules and oversight controls.

As a result, operational teams reduce manual effort while retaining accountability. These systems matter because fintech platforms must scale decisions without scaling headcount. In 2026, agentic AI is becoming viable due to better governance layers and real-time monitoring.

2. Generative AI for Decision Explanation

Generative AI is moving beyond chat interfaces. In fintech apps, it is increasingly used to explain decisions made by risk, credit, or compliance systems. This includes natural-language summaries of why a transaction was flagged or why a loan was approved.

Therefore, decision transparency improves for both internal teams and regulators. This technology matters because explainability is now a requirement, not a bonus. In 2026, generative AI plays a key role in audit readiness.

3. Multi-Modal AI for Identity and Onboarding

Multi-modal AI processes text, documents, images, voice, and behavioral signals together. In fintech, this technology simplifies onboarding, identity verification, and customer support. Instead of fragmented checks, platforms gain a unified view of user intent and risk.

As a result, friction drops while security improves. This approach is gaining traction because digital onboarding remains a major failure point. In 2026, multi-modal AI helps fintech apps balance speed with trust.

4. Privacy-Preserving AI for Regulated Data Use

Privacy-preserving AI allows models to learn without exposing raw financial data. Techniques such as federated learning and secure data isolation are increasingly relevant. They enable collaboration across entities while respecting data boundaries.

Consequently, fintech platforms can unlock intelligence without violating privacy rules. This technology matters most in cross-border and multi-partner ecosystems. In 2026, it supports compliance without limiting innovation.

5. AI Orchestration Layers

AI orchestration layers coordinate multiple models across products and channels. Instead of isolated outputs, decisions are aligned through a central control layer. Policies, thresholds, and overrides are applied consistently.

This reduces fragmentation across teams and systems. In addition, it makes AI behavior predictable and governable at scale. In 2026, orchestration layers are critical for enterprise-grade fintech platforms.

6. Continuous Learning Models with Drift Detection

Static AI models degrade over time. Continuous learning models address this by adapting to new data patterns. Drift detection ensures changes are monitored and approved before deployment.

As a result, fintech platforms stay resilient in dynamic environments. This technology matters because fraud patterns and user behavior evolve constantly. In 2026, controlled adaptability becomes a baseline expectation.

Together, these technologies signal that fintech AI is now defined by governance, adaptability, and operational trust. Enterprises that invest in these foundations are better prepared for regulatory scrutiny and long-term growth.

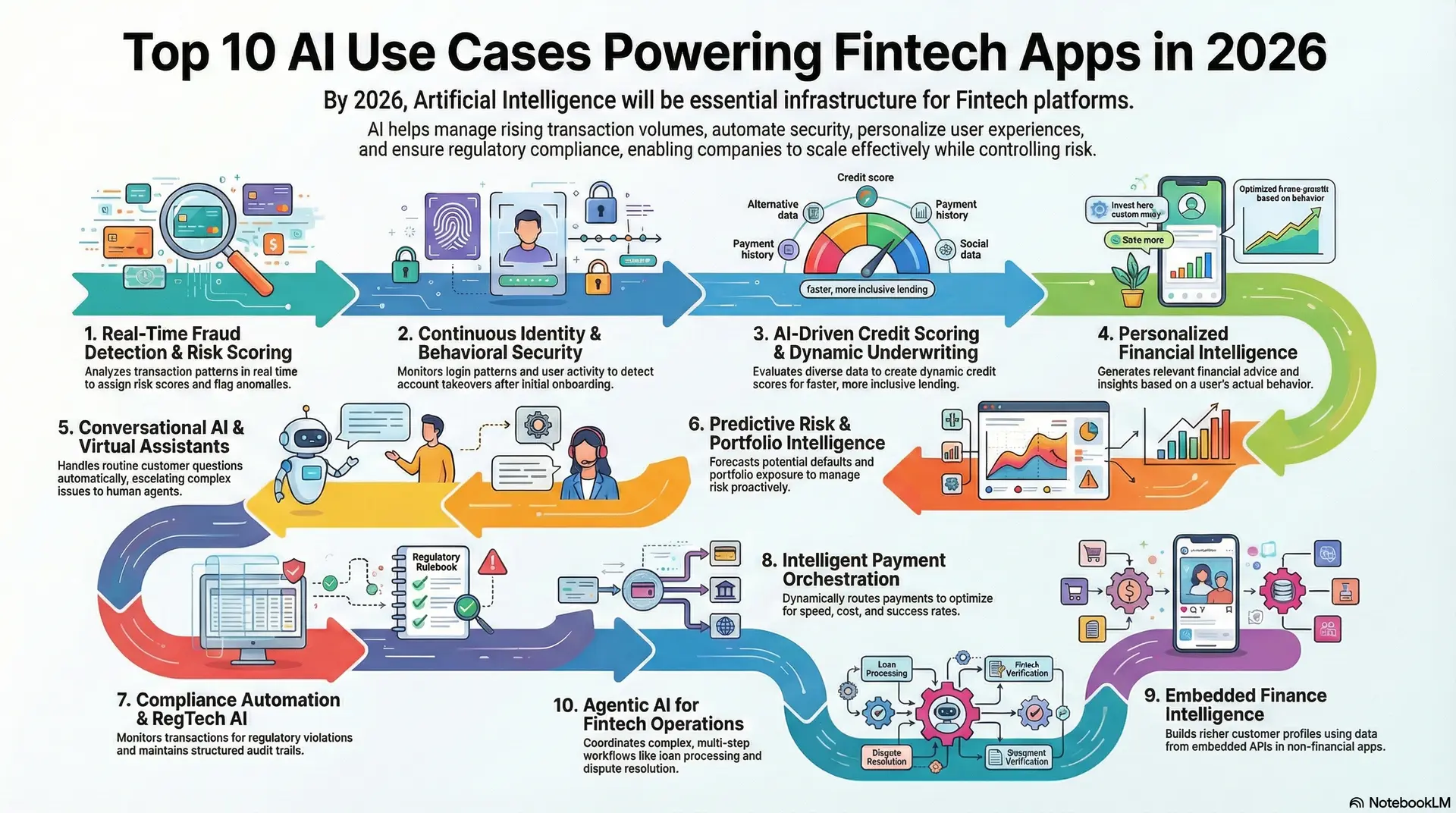

Top 10 AI Use Cases Powering Fintech Apps in 2026

By 2026, AI use cases in fintech are embedded into core workflows that influence payments, credit, risk, and compliance. The focus has moved from experimentation to controlled deployment, where AI delivers measurable value without increasing exposure.

However, not every use case scales safely. Some strengthen platforms, while others introduce operational or regulatory risk when applied without governance. The difference lies in how AI is integrated into decision workflows and oversight structures.

The following use cases reflect where AI is actively operating inside fintech platforms today and where adoption is accelerating. Each example highlights practical value, real constraints, and the role of governance in long-term scalability.

1. Real-Time Fraud Detection & Risk Scoring

Fintech platforms face rising transaction volumes and increasingly automated fraud. Rule-based systems struggle to adapt, leading to missed threats and unnecessary customer friction.

How AI fits in the workflow

AI analyzes transaction patterns, behavioral signals, and device context in real time. It assigns risk scores and flags anomalies within payment flows. These alerts support fraud teams and trigger additional checks when needed. AI surfaces risk but does not enforce decisions.

Why this is real by 2026

As digital payments scale, AI-driven fraud scoring is becoming standard. Enterprises adopt it to improve accuracy, reduce losses, and meet proactive risk expectations at scale.

2. Continuous Identity & Behavioral Security

Identity risk does not end after onboarding. Account takeovers, credential stuffing, and session hijacking often occur during routine usage. Traditional KYC checks provide a one-time snapshot, which leaves gaps as user behavior changes over time. As fintech platforms grow, these gaps increase fraud losses and operational strain.

How AI fits in the workflow

AI continuously analyzes login patterns, device fingerprints, location changes, and interaction behavior across sessions. When activity deviates from a trusted baseline, the system raises a risk score or triggers additional verification. AI supports detection and prioritization, while enforcement actions remain policy-led.

Why this is real by 2026

As identity attacks become automated, continuous AI-based monitoring is becoming a standard security layer for active fintech accounts.

3. AI-Driven Credit Scoring & Dynamic Underwriting

Traditional credit scoring relies on static data and manual review cycles. This slows approvals and excludes borrowers with limited credit history. As lending volumes rise, these models struggle to balance growth with risk control.

How AI fits in the workflow

AI evaluates income signals, spending behavior, repayment trends, and alternative data sources in near real time. Credit scores update dynamically as new information becomes available. Underwriting teams use these insights to approve, adjust, or escalate applications without delaying decisions.

Why this is real by 2026

Digital lending continues to expand globally. AI-driven underwriting enables faster decisions, broader inclusion, and more consistent risk management at scale.

4. Personalized Financial Intelligence

Generic financial insights often fail to reflect real user behavior. Customers receive alerts and advice that feel irrelevant, which reduces engagement and trust over time.

How AI fits in the workflow

AI analyzes transaction history, savings patterns, financial goals, and usage trends to generate contextual insights. These appear within budgeting, planning, or investment flows, supporting timely and relevant actions based on actual behavior.

Why this is real by 2026

Customer expectations now center on relevance and clarity. Fintech platforms increasingly rely on AI-driven personalization to improve engagement, retention, and long-term customer value.

5. Conversational AI & Virtual Assistants

Customer support costs rise as user bases grow. Human-only support models struggle to maintain speed, consistency, and availability at scale.

How AI fits in the workflow

Natural language systems handle routine questions, guide users through workflows, and retrieve account information. When queries become complex or sensitive, conversations escalate to human agents with full context preserved.

Why this is real by 2026

Conversational AI has matured significantly. By 2026, it will play a central role in reducing support load while maintaining service quality across fintech platforms.

6. Predictive Risk & Portfolio Intelligence

Risk teams often rely on backward-looking reports. These approaches identify problems after exposure has already increased, limiting prevention options.

How AI fits in the workflow

AI models analyze historical trends alongside live transactions and market data. They forecast defaults, liquidity stress, and portfolio exposure. Teams use these predictions to adjust limits, pricing, and interventions early.

Why this is real by 2026

As financial volatility increases, predictive insight becomes essential. AI enables proactive risk management instead of reactive loss control.

7. Compliance Automation & RegTech AI

Compliance requirements grow more complex each year. Manual monitoring is slow, expensive, and difficult to scale across regions.

How AI fits in the workflow

AI continuously monitors transactions and user behavior against regulatory thresholds. It flags potential violations and maintains structured audit trails. Compliance teams focus on reviewing alerts rather than scanning entire datasets.

Why this is real by 2026

Regulatory scrutiny continues to intensify. AI-supported compliance is becoming essential for audit readiness and operational efficiency.

8. Intelligent Payment Orchestration

Payment systems must balance speed, success rates, cost, and fraud risk. Static routing logic cannot adapt to changing conditions in real time.

How AI fits in the workflow

AI evaluates transaction context, network performance, and risk signals instantly. It dynamically routes payments and adjusts authorization logic to optimize outcomes across channels.

Why this is real by 2026

As real-time payments expand globally, intelligent orchestration becomes critical for reliable and scalable transaction processing.

9. Embedded Finance Intelligence

Financial data often remains fragmented across platforms. This limits insight into affordability, risk, and customer behavior.

How AI fits in the workflow

AI interprets data from open finance and embedded APIs to build richer profiles. These insights support credit decisions, pricing strategies, and personalized offers within non-financial platforms.

Why this is real by 2026

As embedded finance grows, AI becomes essential for turning shared data into actionable intelligence.

10. Agentic AI for Fintech Operations

Operational workflows involve multiple handoffs, reviews, and delays. Manual coordination increases cost, errors, and processing time.

How AI fits in the workflow

Agentic AI coordinates multi-step processes such as loan processing, dispute resolution, and compliance triage. At the same time, humans remain responsible at defined checkpoints, ensuring accountability.

Why this is real by 2026

As fintech platforms scale, agent-based systems help manage operational complexity without sacrificing control.

Together, these use cases show how AI is reshaping fintech platforms in practical ways. The impact is not limited to efficiency gains. It extends to risk control, compliance readiness, and long-term scalability. Each use case addresses a specific operational gap that traditional systems can no longer manage alone.

However, success depends on how these capabilities are implemented. AI delivers value only when it operates within governed workflows and clear accountability structures. By 2026, fintech platforms that treat AI as regulated infrastructure rather than standalone features will be better positioned to scale with confidence.

Real Fintech Apps Where These AI Use Cases Are Live

AI use cases in fintech are no longer theoretical. Many large-scale platforms already rely on these capabilities to manage risk, improve efficiency, and support growth. What matters is not experimentation, but sustained operation under real volume, regulation, and customer expectations.

Below are examples of fintech platforms where these AI use cases are actively deployed in production environments.

1. Payments and Fraud Prevention Platforms

Global payment platforms such as Stripe and PayPal use machine learning models to detect fraud in real time. These systems analyze transaction patterns, device signals, and behavioral data to flag anomalies before settlement.

As payment volumes scale, AI supports faster risk decisions without increasing customer friction. This approach allows fraud teams to focus on high-risk cases rather than manual reviews.

2. Digital Banks and Neobanks

Neobanks like Revolut and Monzo rely on AI to support fraud monitoring, spending insights, and customer support. Behavioral models help identify unusual activity, while personalization engines deliver contextual financial guidance.

At the same time, conversational AI handles a large share of routine customer queries. These systems operate continuously, supporting day-to-day banking at scale.

3. Lending and Credit Platforms

Lending platforms such as Upstart and SoFi apply AI to credit scoring and underwriting. Their models incorporate alternative data and real-time signals to assess risk more accurately.

This allows faster loan decisions while maintaining credit discipline. Human reviewers remain involved for edge cases, ensuring accountability within automated workflows.

4. Wealth and Financial Management Apps

Platforms like Wealthfront and Betterment use AI to support portfolio analysis, risk profiling, and personalized recommendations.

Predictive models help anticipate market shifts and align investment strategies with user goals. These insights assist advisors and users rather than replacing human judgment.

5. Compliance and Risk Intelligence Providers

Firms such as ComplyAdvantage apply AI to transaction monitoring and risk assessment. Their systems scan large volumes of data to surface potential compliance issues early.

As regulatory requirements grow more complex, AI helps compliance teams prioritize reviews and maintain audit readiness.

6. Embedded Finance and Infrastructure Providers

Infrastructure platforms like Adyen and Plaid use AI to support payment routing, data interpretation, and risk controls across partner ecosystems. These capabilities enable embedded finance use cases while maintaining consistency and security across integrations.

These platforms demonstrate that AI use cases discussed earlier are already operating at scale. They also show that AI supports decisions, but governance and human oversight remain central. This balance is what allows fintech platforms to grow without increasing operational or regulatory risk.

How AI Systems Are Architected in Fintech Apps

Successful AI adoption in fintech depends less on individual models and more on system design. Platforms that scale reliably treat AI as a layered decision system, not a collection of disconnected tools.

This approach reduces risk, improves explainability, and supports long-term governance. In contrast, poorly designed architectures often fail during audits, scale events, or regulatory reviews.

Below is the practical architecture pattern increasingly used in production fintech apps.

1. Data Layer: Quality, Lineage, and Real-World Signals

The data layer forms the foundation of every AI decision. It aggregates transaction data, user behavior, device signals, and external inputs. Quality checks ensure accuracy and consistency across sources.

In addition, lineage and versioning track where the data comes from and how it changes. This matters because fintech decisions must be explainable long after they occur. Without strong data foundations, even accurate models become unreliable.

2. Feature Engineering Layer

Raw data rarely reflects financial reality on its own. The feature layer transforms inputs into meaningful signals such as spending velocity, income stability, or risk indicators.

These transformations encode domain knowledge into the system. As a result, models receive consistent, interpretable inputs. This layer also improves reuse across products, which reduces duplication and operational complexity.

3. Model Layer: Specialized Intelligence

Fintech apps use different models for fraud detection, credit risk, forecasting, and language understanding.

Each model serves a defined purpose and operates within known limits. This separation improves performance and simplifies validation. It also allows teams to update models independently without destabilizing the entire system.

4. Decision Engine: Intelligence with Policy Control

The decision engine combines model outputs with business rules and regulatory policies. It determines what action is allowed, what requires review, and what must be blocked.

This layer ensures AI supports decisions rather than making uncontrolled ones. It also provides a clear point for human oversight and accountability, which is essential in regulated environments.

5. Monitoring and Governance: Continuous Control

AI systems must be monitored after deployment. Drift detection tracks changes in data or model behavior over time. At the same time, bias monitoring identifies unintended patterns.

Audit logs record every decision and input. Together, these controls ensure systems remain compliant, explainable, and trustworthy as conditions evolve.

This layered approach separates successful fintech AI apps from fragile ones. It enables scale without sacrificing control. More importantly, it allows enterprises to adapt AI systems over time while meeting regulatory and operational expectations.

How We Build Fintech Apps Ready for AI in 2026

Building AI-powered fintech platforms in 2026 requires more than technical capability. It requires discipline, foresight, and control. AI decisions now affect money movement, credit access, and regulatory exposure.

At Intellivon, our build approach reflects how AI operates in real financial environments, not controlled labs. Every step is designed to balance innovation with accountability. This ensures platforms scale without introducing hidden risk.

1. Assess Business and AI Impact Areas

We begin by understanding the business decisions that matter most. These often sit across fraud, credit, payments, and compliance workflows. Each decision is evaluated for financial impact, risk exposure, and operational readiness.

We avoid applying AI where it adds complexity without value. Instead, we focus on areas where AI improves speed, accuracy, or control. This step ensures AI aligns with business outcomes from day one.

2. Design Regulation-Aware AI Architecture

Next, we design AI as part of a governed system. Models never operate in isolation. They sit behind decision layers that apply policies, thresholds, and approval logic.

This structure ensures every AI output can be explained and reviewed. It also supports audit and regulatory expectations. As a result, platforms remain stable as volume and scrutiny increase.

3. Build Secure Data and Feature Pipelines

AI depends on reliable data foundations. We design data pipelines with quality checks, lineage tracking, and strict access controls. Feature layers transform raw data into meaningful financial signals.

Training and production environments remain clearly separated. This reduces leakage and operational risk. Over time, this structure supports consistency across products and regions.

4. Integrate Human-in-the-Loop

Not every decision should be automated. For high-risk actions, human oversight remains essential. We define clear escalation paths and review checkpoints. AI supports prioritization and insight, not final authority.

This approach protects accountability while still improving efficiency. It also aligns with regulatory expectations around responsible automation.

5. Govern Models Through Their Lifecycle

AI systems change over time. We monitor models continuously for performance drift and unintended bias. At the same time, audit logs capture inputs, outputs, and decisions. Governance processes define when retraining is allowed and how updates are approved.

This ensures AI behavior remains predictable. As regulations evolve, governance adapts without disrupting operations.

6. Incrementally Adopt Emerging AI Capabilities

New AI technologies bring opportunity and risk. We introduce them through controlled pilots, not full deployments. Each capability is evaluated against governance and compliance criteria.

Expansion happens only after stability is proven. This prevents innovation from outpacing control. It also allows teams to learn without exposing the platform.

7. Test, Validate, and Iterate With Real Data

Finally, systems are tested under real operating conditions. We observe how AI behaves at scale, not just in simulations. Feedback loops inform ongoing improvement. Models, features, and controls evolve together.

This ensures the platform stays resilient as business needs change. Over time, AI becomes a stable part of the operating model.

This approach prepares fintech platforms for long-term AI adoption. It supports growth without sacrificing trust or compliance. Most importantly, it reflects how AI must function inside regulated financial systems in 2026.

AI Compliance and Regulatory Requirements for FinTech Apps

As AI becomes embedded in core fintech workflows, compliance is no longer a separate checklist. It shapes how systems are designed, deployed, and governed. By 2026, regulators expect AI-driven decisions to be explainable, auditable, and accountable. This section outlines the regulatory landscape and the practical requirements enterprises must address.

Key AI and FinTech Regulations to Consider

| Regulation / Standard | Region | What It Governs |

| GDPR | EU | Data privacy, consent, automated decision rights |

| EU AI Act | EU | Risk classification, transparency, human oversight |

| ISO 20022 | Global | Financial messaging and data standardization |

| SOC 2 | Global | Security, availability, and data handling controls |

| PCI DSS | Global | Payment data security |

| AML / KYC Regulations | Global | Identity verification and transaction monitoring |

| Fair Lending Laws | US / Global | Bias prevention in credit decisions |

1. Explainability and Transparent Decision-Making

AI systems must be able to explain why a decision was made. This includes credit approvals, fraud flags, and account restrictions. Black-box outputs are increasingly unacceptable.

Platforms must provide human-readable explanations for regulators and internal teams. This improves trust and reduces regulatory friction. By 2026, explainability is expected, not optional.

2. Human Oversight and Accountability

Regulators do not allow AI to operate without responsibility. High-impact decisions must include human review paths. Clear ownership is required for overrides and exceptions.

AI supports decisions but does not replace accountability. This structure ensures errors can be corrected quickly. It also aligns with global expectations around responsible automation.

3. Bias Detection and Fairness Controls

AI models can inherit bias from historical data. In fintech, this creates legal and ethical risk. Platforms must monitor outcomes across demographics. Regular bias testing helps detect unintended discrimination.

When issues appear, teams must adjust models or features. Fairness controls protect both customers and the business.

4. Audit Trails and Record Keeping

Every AI-assisted decision must be traceable. Audit logs should capture inputs, outputs, model versions, and decision paths. These records support regulatory reviews and internal investigations.

Without strong logging, compliance teams operate blind. By 2026, audit readiness is a baseline requirement.

5. Data Privacy, Consent, and Residency

AI systems rely on sensitive financial data. Regulations require clear consent management and strict access controls. Data residency rules may limit where information can be processed.

Training and inference environments must remain separated. Strong privacy design reduces regulatory exposure and customer risk.

6. Model Governance and Change Management

AI models evolve over time. Regulators expect controlled updates, not silent changes. Governance frameworks define when retraining is allowed and how changes are approved. Performance drift must be monitored continuously.

This prevents unexpected behavior in production systems. Stable governance supports long-term trust.

Compliance defines how AI operates in fintech, not just where it is applied. Platforms that embed regulatory requirements into architecture and workflows scale more confidently.

What Most Fintech Teams Get Wrong About AI Adoption

Many fintech organizations invest in AI with the right intent. However, execution often breaks down after early pilots. The gap between experimentation and production is where most failures occur.

These missteps usually stem from how AI is positioned within the organization, not from the technology itself. Understanding these mistakes helps enterprises avoid costly rework.

1. Treating AI as a Feature Instead of Infrastructure

Teams often deploy AI as a standalone capability. This approach ignores how decisions flow across systems. As a result, models operate without proper context or control. Over time, this creates fragmentation and risk.

AI must be designed as part of the core platform. Without that foundation, scale becomes fragile.

2. Scaling Models Before Governance Is Ready

Many teams focus on accuracy before control. Models are pushed into production without clear oversight. Audit trails, explainability, and approval paths come later. This creates exposure during regulatory reviews.

In this case, governance must exist before scale. Otherwise, growth increases risk instead of value.

3. Underestimating Data Quality and Lineage

AI is only as reliable as the data behind it. Teams often overlook data gaps, inconsistencies, and ownership. When issues surface, root causes are hard to trace. This slows response and erodes trust.

Strong data foundations should always come first. Everything else depends on them.

4. Removing Humans Too Early from Critical Decisions

Automation promises efficiency, but full autonomy introduces risk. Some teams eliminate human review for high-impact actions. When errors occur, accountability becomes unclear.

AI should support decisions, not replace responsibility. Human oversight protects both customers and the business.

5. Chasing New AI Capabilities Without Clear Use Cases

Emerging AI technologies attract attention quickly. Teams experiment without linking them to business outcomes. This leads to scattered pilots and unclear ROI.

Innovation should be intentional, and clear use cases prevent wasted effort.

Avoiding these pitfalls requires more than technical skill. It requires experience building AI inside regulated financial systems. At Intellivon, we help fintech teams move from experimentation to production with confidence. Our approach embeds governance, accountability, and scalability from the start.

This allows enterprises to adopt AI responsibly while focusing on growth, not remediation.

Conclusion

AI in fintech has moved beyond experimentation. It now shapes decisions that affect risk, compliance, and growth at scale. The use cases discussed in this blog reflect how leading platforms are applying AI responsibly, not aggressively. Success depends on architecture, governance, and disciplined execution, not model novelty. By 2026, fintech teams that treat AI as regulated infrastructure will outperform those chasing isolated wins.

At Intellivon, we help enterprises build AI-powered fintech platforms that scale with confidence. Our approach balances innovation with control, ensuring systems remain explainable, auditable, and resilient. For organizations planning their next phase of growth, responsible AI adoption is no longer optional. It is a strategic advantage when built correctly.

Build 2026-Ready AI-Powered Fintech Apps With Intellivon

At Intellivon, AI-powered fintech apps are built as regulated financial systems, not as intelligence layers added onto legacy platforms. Every architectural and delivery decision prioritizes risk control, regulatory alignment, and long-term scalability. This ensures fintech platforms operate reliably across payments, lending, compliance, and embedded finance use cases, not just during early adoption.

As fintech programs expand across markets, volumes, and regulatory environments, stability becomes critical. Governance, explainability, and performance remain consistent as AI-driven decisions scale. Organizations retain control over data, models, and decision outcomes without introducing compliance gaps, operational fragility, or hidden risk.

Why Partner With Intellivon?

- Enterprise-grade fintech architecture designed for regulated, high-volume financial ecosystems

- Proven delivery across payments, lending, risk, compliance, and embedded finance platforms

- Compliance-by-design approach with audit readiness, explainability, and policy enforcement

- Secure, modular infrastructure supporting cloud, hybrid, and multi-region deployments

- Governed AI enablement for fraud detection, risk intelligence, automation, and decision support

Book a strategy call to explore how Intellivon can help you build and scale an AI-powered fintech app with confidence, control, and long-term enterprise value.

FAQs

Q1. How is AI used in fintech apps in 2026?

A1. In 2026, AI is embedded into core fintech workflows such as fraud detection, credit scoring, compliance monitoring, and payment orchestration. It supports real-time decision-making while operating within governed systems.

AI does not act independently. Instead, it works alongside policy rules and human oversight to ensure accuracy, compliance, and scalability across regulated financial environments.

Q2. Are AI-powered fintech apps compliant with financial regulations?

A2. AI-powered fintech apps can be compliant when designed correctly. Compliance depends on explainability, audit trails, data privacy controls, and human-in-the-loop decision paths.

Regulations such as GDPR, the EU AI Act, and fair lending laws require AI systems to be transparent and accountable. Platforms built with compliance-by-design can meet these requirements at scale.

Q3. What are the biggest risks of using AI in fintech?

A3. The main risks include biased decision outcomes, lack of explainability, data quality issues, and uncontrolled automation. These risks increase when AI is deployed without governance frameworks.

Fintech platforms reduce exposure by monitoring models continuously, maintaining audit logs, and ensuring humans remain accountable for high-impact decisions.

Q4. How long does it take to build an AI-powered fintech app?

A4. Timelines vary based on scope, regulatory complexity, and data readiness. Most enterprise-grade AI fintech platforms are built in phases.

Initial foundations may take several months, followed by controlled AI rollout and validation. Incremental delivery helps teams manage risk while accelerating time to value.

Q5. Why should enterprises partner with a specialist to build AI fintech apps?

A5. Building AI for fintech requires more than model development. It demands experience with regulated systems, governance, and scale.

Specialist partners help enterprises avoid costly rework by embedding compliance, security, and accountability from the start. This approach supports faster adoption and long-term platform stability.