Most traditional banking systems were not built for the way people use financial services today. Many banks are still tied to outdated, all-in-one platforms and locked-in vendors, which makes it hard for them to deliver the kind of experiences customers now expect. The gap between traditional banks and digital-first competitors keeps getting wider, and waiting to adapt is no longer a real option.

A neobank platform built on APIs changes the game. This is because it breaks banking into smaller parts, which include payments, lending, customer checks, compliance, and analytics, so each one can be launched, scaled, or replaced without overhauling the entire system. The result is a flexible, fast, and modern foundation that can grow as the market changes.

At Intellivon, we’ve worked with companies to build API-based financial platforms that reach real customers at scale. What we’ve learned from these projects shapes the advice in this guide. The next sections in the blog will cover the key design choices, building and connecting APIs, and meeting compliance needs while building a neobank platform that’s ready for today’s demands.

Why Neobanks Are Moving to API-First Architectures

Neobanks are moving toward API-first architectures to innovate faster and scale digital banking services. These systems enable seamless integrations, support embedded finance, and power real-time financial experiences.

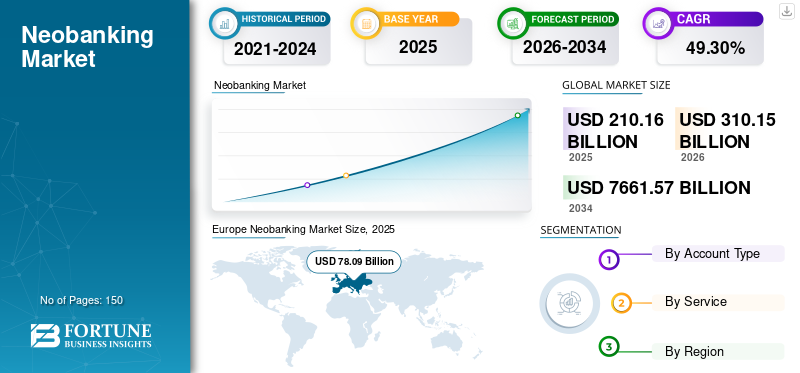

As a result, they align with the rapid growth expected in digital banking markets beyond 2026. The global neobanking market reached USD 210.16 billion in 2025. It is expected to grow to USD 310.15 billion in 2026 and reach USD 7,661.57 billion by 2034, expanding at a 49.30% CAGR during the forecast period.

By decoupling the front-end experience from back-end logic, firms can iterate without disrupting core operations. This architectural choice supports a modular model that is essential for scaling in a digital-first economy.

1. Limits of Legacy Banking Platforms

Legacy systems were originally designed for a branch-based world. These monolithic structures rely on batch processing, which creates significant delays in data updates. Therefore, real-time transaction monitoring and instant notifications become nearly impossible to implement effectively.

This financial drain prevents companies from investing in much-needed innovation. Decision makers often find that legacy codebases lack the flexibility required for modern security protocols.

2. Rise of Embedded Finance Ecosystems

Embedded finance is changing how non-financial brands interact with their customers. Companies in retail and logistics now offer integrated payment solutions directly within their apps. However, launching these features requires a robust neobank platform that handles high-volume API calls securely.

By embedding financial tools, businesses increase customer stickiness and unlock new revenue streams. This trend reflects a move toward “invisible banking,” where the financial transaction is a secondary part of a user journey. Organizations adopting this model early see a significant boost in lifetime customer value.

3. Fintech Platforms Require Modular Banking Services

A modular approach is vital for any neobank platform aiming for global reach. Fintechs need the ability to swap service providers for KYC or card issuance without rebuilding their stack.

Therefore, modularity provides a safety net against vendor lock-in and localized regulatory changes. This flexibility ensures that a platform remains compliant across different jurisdictions. In addition, modular services allow for hyper-personalization.

You can build specific workflows for gig workers or small businesses using the same underlying infrastructure. This capability transforms financial services into a dynamic growth engine.

How API-First Architecture Accelerates Fintech Platforms

Strategic partnerships thrive when technical friction is minimized. For this reason, API-first ecosystems create a standardized language that allows different platforms to communicate instantly.

This interoperability means that a neobank platform can onboard a new lending partner in weeks rather than months. As a result, the time-to-market for new features drops dramatically.

These ecosystems also foster a collaborative environment where data sharing is secure. By leveraging open banking standards, institutions can offer a more holistic view of financial health. This builds deeper trust and positions the enterprise as a central hub for users.

By solving the friction of legacy systems, these architectures empower brands to own the entire customer lifecycle. Moving to an API-first model is the critical first step in building a resilient, future-proof financial ecosystem.

What is an API-First Neobank Platform?

An API-first neobank platform is a modular financial infrastructure built using application programming interfaces as the primary foundation. Unlike traditional banks, it exposes core functions like ledgers and payments as programmable services.

Therefore, businesses can integrate banking features directly into their own applications. This architecture ensures high scalability, real-time data processing, and seamless interoperability for modern enterprise ecosystems.

API-First vs Traditional Banking Architecture

Traditional banking systems were built long before modern digital finance existed. As a result, many banks still rely on monolithic infrastructure and tightly coupled systems.

In contrast, API-first banking platforms expose services through programmable interfaces. This allows fintech products, partner platforms, and financial services to integrate easily and evolve faster.

Key Differences Between API-First and Traditional Banking

| Feature | API-First Banking Architecture | Traditional Banking Architecture |

| System design | Built around APIs from the start | Built as closed internal systems |

| Integration capability | Enables seamless third-party integrations | Integrations are complex and slow |

| Product development | New services can be launched quickly | Changes require major system updates |

| Platform flexibility | Modular services allow easier upgrades | Systems are tightly coupled |

| Embedded finance support | Designed to power partner ecosystems | Limited support for external platforms |

| Scalability | Scales easily with cloud infrastructure | Scaling requires infrastructure overhaul |

In short, API-first architecture turns banking capabilities into programmable services. This approach helps neobanks innovate faster, integrate with partners, and support modern financial ecosystems.

Role Of Microservices In Modern Neobanks

Microservices provide the granular agility necessary for a high-performance neobank platform.

This architecture breaks complex banking functions into independent, manageable units to ensure continuous availability.

1. Independent Service Scalability

Each microservice functions as a standalone entity within the broader ecosystem. Therefore, teams can scale specific features like payment processing without affecting the entire ledger system. This targeted scaling optimizes cloud resource consumption and lowers operational costs.

2. Fault Isolation and Resilience

System failures in one area do not cause a total platform outage. If a currency conversion service fails, the core deposit and withdrawal functions remain active. This isolation is critical for maintaining the high trust required in financial services.

3. Rapid Deployment Cycles

Developers can update individual services without a full system reboot. Consequently, new features or security patches reach the market much faster than monolithic alternatives. This speed allows enterprises to respond instantly to shifting regulatory requirements or customer demands.

By adopting a microservices framework, neobanks achieve the resilience and speed required for global operations. This structural choice transforms rigid financial systems into highly adaptable, enterprise-grade digital assets.

Core Components of an API-First Neobank Platform

A neobank platform is only as strong as the APIs connecting each functional layer. Every component must operate independently, scale without disruption, and integrate cleanly across the entire system.

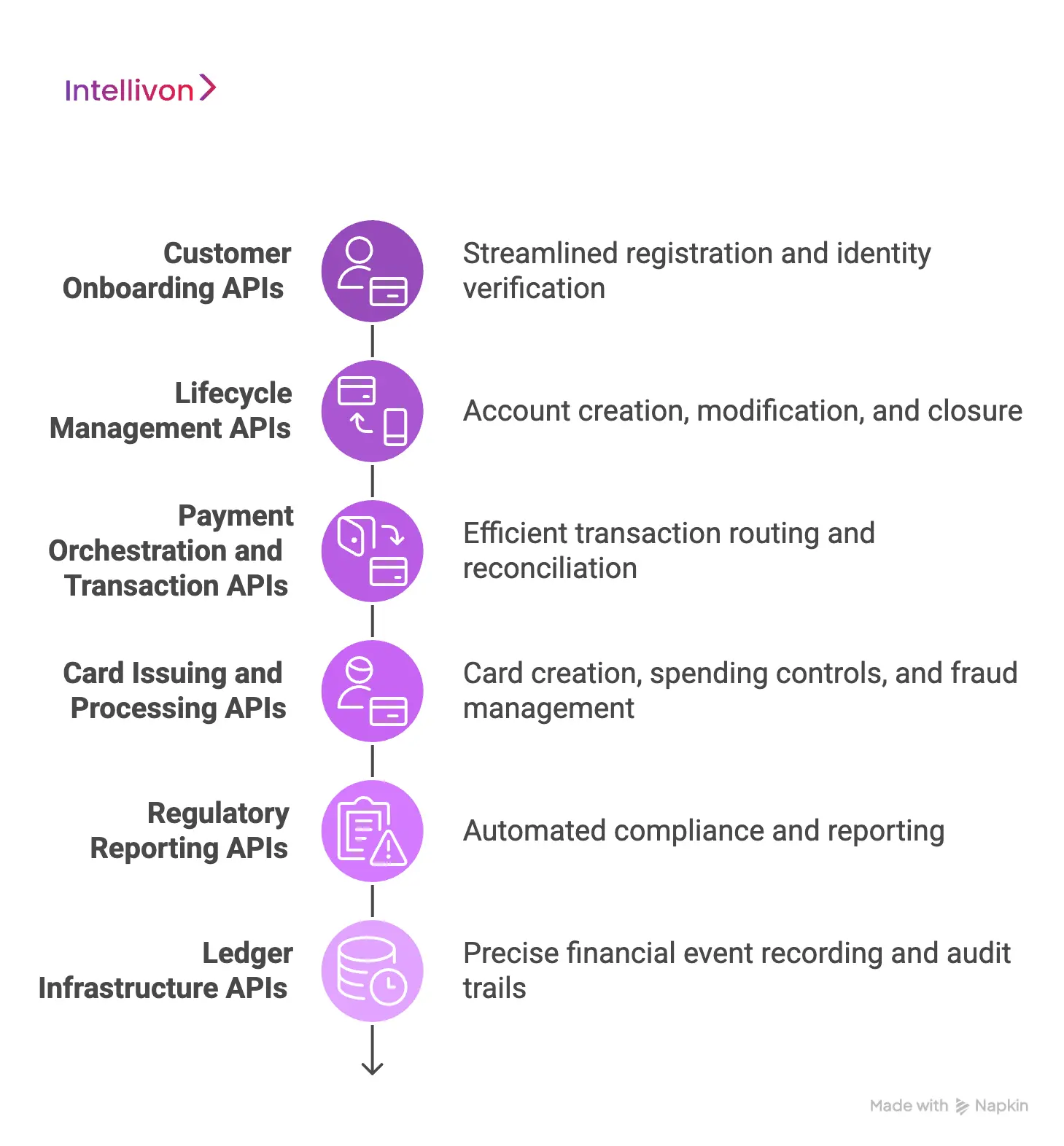

1. Customer Onboarding APIs

Onboarding speed determines whether customers complete registration or abandon it. Identity verification APIs run KYC, AML, biometric checks, and document validation simultaneously.

Configurable workflows adapt to different customer types, risk profiles, and jurisdictions without rebuilding underlying logic.

2. Lifecycle Management APIs

Account APIs handle creation, modification, suspension, and closure as discrete, auditable events.

They support multiple account types across individual and business customers. Therefore, product teams can launch new account structures without touching core banking logic.

3. Payment Orchestration and Transaction APIs

Payment APIs route transactions across SWIFT, SEPA, ACH, and real-time payment rails based on cost, speed, and availability.

They handle retries, reversals, and reconciliation automatically. In addition, they provide real-time transaction status visibility across every connected channel.

4. Card Issuing and Processing APIs

Card APIs connect directly to issuer processors and network schemes like Visa and Mastercard.

They manage virtual and physical card creation, spending controls, tokenization, and fraud triggers. Enterprises can configure card products independently per customer segment.

5. Regulatory Reporting APIs

These APIs automate transaction monitoring, sanctions screening, and regulatory report generation. They adapt reporting formats per jurisdiction, reducing manual compliance overhead significantly.

6. Ledger Infrastructure APIs

The ledger layer records every financial event with double-entry precision. It supports multi-currency balances, real-time reconciliation, and clean audit trails that satisfy both internal controls and external regulators.

These six API layers are the structural foundation every serious neobank platform is built upon. Get them right at the architecture stage, and every product decision that follows becomes faster, cleaner, and significantly easier to scale.

Security Architecture for API-First Neobank Platforms

Security in a neobank platform is not a feature added at the end. It is a design decision made at the very beginning.

Every API endpoint, every data exchange, and every third-party connection represents a potential vulnerability if not architected with deliberate controls from day one.

1. Identity and Access Management for Financial APIs

Every API call must be traceable to a verified identity. Role-based access controls ensure internal teams, partner integrations, and customer-facing services only access what they are explicitly permitted to.

OAuth 2.0 and OpenID Connect provide the industry-standard framework for managing these boundaries across complex, multi-tenant environments cleanly.

2. Encryption and Secure Transaction Protocols

Financial data in transit and at rest requires strong encryption without exception. TLS 1.3 protects data in motion, while AES-256 covers stored records. However, encryption alone is insufficient.

Certificate pinning, payload signing, and tokenization of sensitive values like card numbers add layers that make intercepted data functionally useless to any unauthorized party.

3. API Rate Limiting Mechanisms

Unconstrained API access is an open invitation to abuse. Rate limiting controls how frequently any single identity or IP address can call a given endpoint.

Combined with anomaly detection, velocity checks, and device fingerprinting, the platform builds a behavioral baseline and responds automatically when activity deviates from expected patterns.

4. Secure Authentication for Third-Party Integrations

Third-party integrations introduce risk that internal controls cannot manage alone. Mutual TLS authentication, scoped API keys, and webhook signature verification ensure only authorized external services communicate with the platform.

In addition, regular credential rotation reduces exposure windows significantly if any key is ever compromised.

5. Audit Trails and Compliance Monitoring Systems

Every API interaction should generate an immutable log entry. Audit trails capture who accessed what, when, and with what outcome.

These records support internal investigations, external regulatory audits, and real-time monitoring dashboards that surface policy violations before they escalate into serious incidents.

Security architecture built this way does not slow a platform down. It actually accelerates third-party partnerships because trust is already codified into the system design itself.

Regulatory Requirements for API-First Neobank Platforms

Navigating financial laws is the most critical hurdle for any emerging neobank platform. Success requires a proactive strategy that anticipates shifting global standards and protects institutional integrity.

Maintaining a secure environment is a non-negotiable prerequisite for enterprise-grade services. Therefore, leaders must prioritize an architecture that automates regulatory reporting and risk mitigation. This section outlines the essential frameworks required to secure a competitive market position.

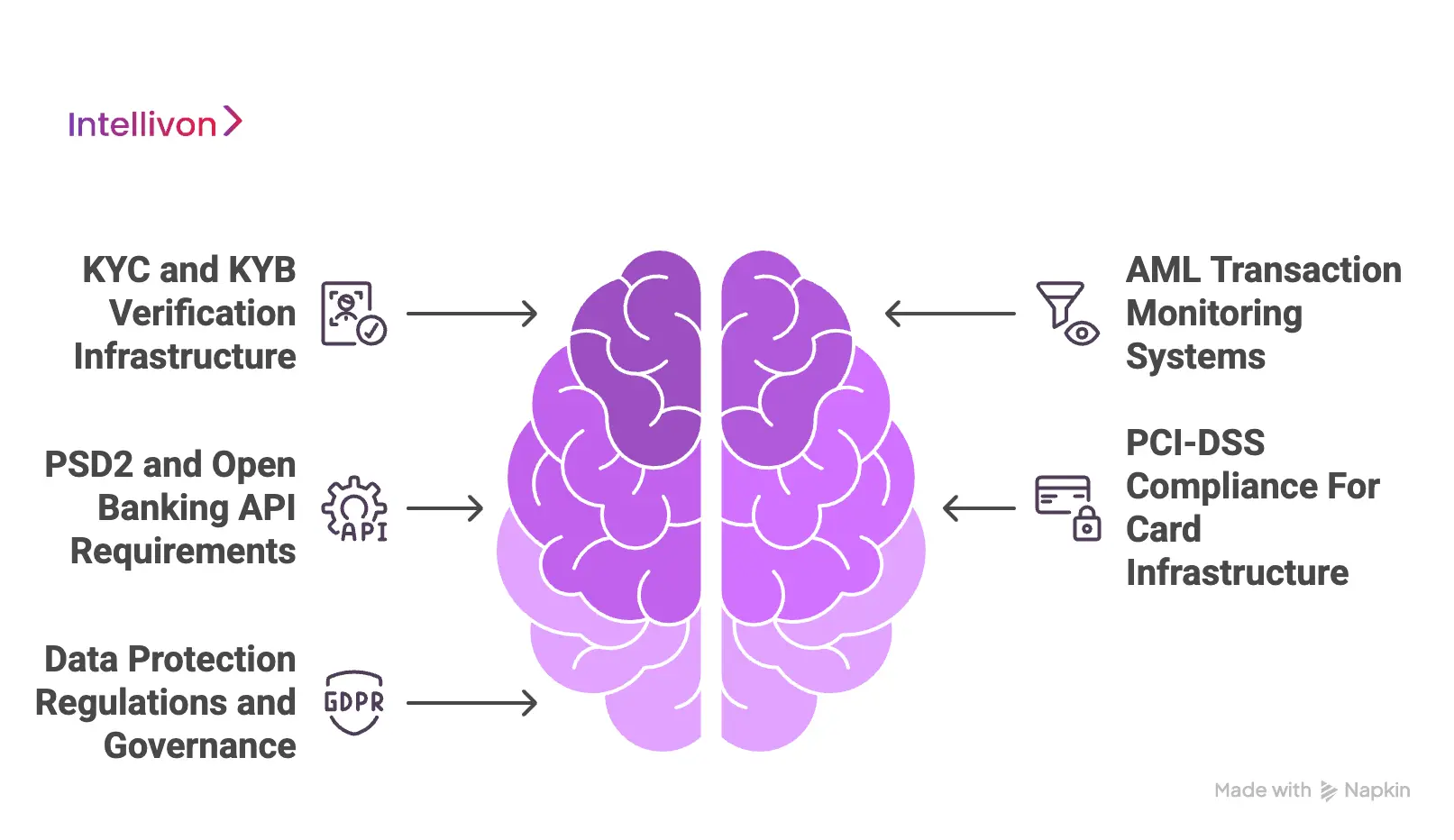

1. KYC and KYB verification infrastructure

Identity verification is the primary defense against financial fraud. A modern neobank platform must support both KYC for individuals and KYB for corporate entities. These systems now leverage “Perpetual KYC” to monitor risk changes in real-time.

Automated document verification and facial biometrics reduce onboarding friction while ensuring high accuracy. Furthermore, KYB processes must include the discovery of ultimate beneficial owners to uncover complex structures.

2. AML transaction monitoring systems

Anti-Money Laundering (AML) controls are vital for detecting suspicious patterns. Modern platforms move toward AI-driven behavioral analysis to identify emerging threats.

Therefore, implementing near-real-time monitoring ensures that high-risk transactions are flagged or blocked instantly. Effective systems also integrate with global sanctions lists and PEP databases.

This integration ensures that the enterprise remains compliant with international trade and financial restrictions.

3. PSD2 and open banking API requirements

The transition toward PSD3 reinforces the need for secure, high-performance APIs. Regulators now mandate Financial-grade API (FAPI) standards and OAuth 2.0 to protect sensitive data transfers.

Consequently, a neobank platform must provide transparent consent management tools. This ensures that third-party providers only access authorized data. Strong Customer Authentication (SCA) remains a cornerstone, requiring multi-factor verification for most online payments.

4. PCI-DSS compliance for card infrastructure

Any institution issuing cards must maintain strict PCI-DSS compliance. The latest 4.0.1 standards focus on continuous security rather than annual audits. Therefore, organizations should use tokenization to minimize the exposure of raw card data.

This reduces the compliance scope and simplifies the technical burden. In addition, robust encryption is required for all cardholder data environments. Regular penetration testing ensures that the infrastructure remains resilient.

5. Data protection regulations and governance

Data privacy laws like GDPR govern how institutions handle personal information. A neobank platform must implement “Privacy by Design” to ensure data minimization. For instance, encryption must be applied to data at rest and in transit.

Governance frameworks also require a designated individual to oversee information security. Furthermore, enterprises must be prepared to respond to breaches within 72 hours. This level of governance builds long-term trust.

A robust regulatory framework is more than a legal obligation; it is a strategic asset. By embedding these controls, enterprises can scale safely without compromising on speed or security.

Core Banking vs Banking-as-a-Service in Neobank Platforms

Choosing between a full banking stack and a managed service layer defines an organization’s long-term capital efficiency. This section evaluates how a neobank platform balances control with speed-to-market using modern infrastructure.

Selecting the right foundation is a critical pivot point for any financial entity. Therefore, decision-makers must weigh the benefits of ownership against the agility of partnership. This comparison provides the strategic clarity needed to align technical architecture with business goals.

Core Banking vs Banking-as-a-Service in Neobank Platforms

| Factor | Core Banking Infrastructure | Banking-as-a-Service (BaaS) |

| Ownership of banking systems | The neobank operates or licenses its own core banking system | The neobank uses infrastructure provided by a regulated BaaS provider |

| Regulatory responsibility | The organization manages licensing, compliance, and regulatory oversight | The BaaS provider handles most regulatory and compliance requirements |

| Infrastructure control | Full control over product features, ledger systems, and banking workflows | Platform capabilities depend on the provider’s API offerings |

| Time to launch | Building and integrating core banking systems takes significant time | Platforms can launch faster using existing banking infrastructure |

| Operational complexity | Requires managing banking operations, risk, and compliance internally | Operational burden is reduced because infrastructure is managed externally |

| Customization flexibility | Highly customizable architecture and financial product design | Customization may be limited by provider capabilities |

| Scalability approach | Scaling requires investment in internal banking infrastructure | Scalability depends on the BaaS provider’s platform capacity |

By selecting the appropriate integration path, leaders can optimize for both current agility and future scale. The right architectural choice ensures the platform remains competitive in an increasingly crowded financial landscape.

How API-First Neobanks Enable Embedded Finance

Embedded finance is transforming from a trend into a structural shift in global commerce. By integrating financial services into non-bank platforms, an API-first neobank platform allows brands to capture 2-5x higher customer lifetime value.

This section examines how modern APIs turn banking into a scalable utility for any enterprise.

1. Banking Capabilities Exposed Through APIs

The value of a modern neobank platform lies in its ability to unbundle services. Instead of a rigid app, the bank becomes a collection of endpoints. Therefore, a retail platform can trigger a credit line through a simple code command. This “atomic banking” approach ensures that features feel like a native part of the host application.

It removes the friction of redirecting users to external portals. This change significantly boosts conversion rates for digital businesses.

2. Partner Onboarding and Developer Portals

Successful embedded finance depends on the velocity of third-party partners. High-performance platforms provide robust developer portals equipped with sandboxes and documentation. These tools allow external teams to test integrations without risking live data.

In addition, automated onboarding workflows handle the necessary due diligence instantly. This self-service model is essential for scaling across different industries. It transforms the bank from a gatekeeper into an enabler of innovation.

3. Revenue Models for Embedded Banking

Moving to an embedded model opens diverse monetization paths beyond interest margins. Enterprises can earn recurring revenue through interchange fee sharing and subscription tiers. For instance, a logistics platform might charge for “Instant Pay” features.

Furthermore, contextual lending generates high-margin income with lower risk. These models turn financial services into a significant contributor to the bottom line. Therefore, companies can diversify their income streams while deepening user loyalty.

4. Platforms Turning Banking Into Infrastructure

The most advanced players move toward architectures that treat banking as pure infrastructure. These platforms handle the lifting of regulatory licenses and capital requirements.

As a result, companies can provide banking to merchants without becoming banks themselves. This shift mirrors the transition of computing to the cloud. Banking is now a programmable layer that is easily deployed.

Therefore, organizations can scale and optimize their financial offerings with minimal technical overhead.

By leveraging these API-driven capabilities, organizations can embed themselves deeper into daily user lives. This strategy drives immediate revenue and builds a competitive moat through data and loyalty.

Integration Challenges When Building Neobank Platforms

Engineering a high-performance neobank platform requires overcoming significant technical friction. This section addresses the structural hurdles of modernization and the strategic solutions that ensure operational excellence.

1. Connecting with legacy banking systems

Many established institutions still rely on COBOL-based systems and batch processing. These monolithic cores do not naturally support the real-time demands of a neobank platform.

Consequently, data synchronization often suffers from high latency and frequent consistency errors.

How We Solve It: We deploy an API abstraction layer that translates legacy formats into modern JSON structures. This middleware allows for real-time data polling and event-driven updates. Therefore, your digital interface reflects accurate balances without requiring a complete core replacement.

2. Payment network integrations

Connecting to networks like SWIFT, SEPA, or UPI involves navigating fragmented protocols. Each gateway has unique security requirements and messaging standards that complicate the engineering process. In addition, manual reconciliation of these transactions often leads to high operational overhead.

How We Solve It: Our platform utilizes a unified payment orchestrator to standardize outgoing and incoming requests. We automate the reconciliation process using distributed ledger technology for absolute transparency. This reduces settlement times and eliminates the risk of human error during high-volume periods.

3. Card network and issuing bank integrations

Launching a card program requires deep integration with Visa, Mastercard, and sponsor banks. These networks demand strict adherence to ISO 8583 standards and complex cryptographic signatures. Furthermore, managing card lifecycles and real-time authorization involves significant technical complexity.

How We Solve It: We provide a pre-certified card-issuing module that handles all network communication. Our system manages tokenization and 3D Secure protocols natively within the API. Therefore, you can launch physical or virtual cards without building the underlying security infrastructure from scratch.

4. Third-party fintech service integrations

A competitive neobank platform must integrate with external KYC, AML, and credit scoring providers. However, managing multiple third-party APIs often creates “vendor sprawl” and security vulnerabilities. Each new connection adds another potential point of failure to the ecosystem.

How We Solve It: We implement a “Service Mesh” architecture to manage all external dependencies centrally. This allows for rapid swapping of providers through a single configuration change. In addition, our platform enforces unified security policies across all third-party data flows to ensure total compliance.

5. Managing API performance at scale

High-growth platforms often struggle with “noisy neighbors” and database contention during peak hours. As the user base expands, the pressure on API endpoints can lead to slow response times. Therefore, maintaining a seamless user experience becomes increasingly difficult under heavy loads.

How We Solve It: We utilize horizontal auto-scaling and edge caching to distribute traffic effectively. Our platform implements “circuit breakers” to prevent localized failures from cascading into a total system outage. Consequently, your services remain responsive even during sudden surges in transaction volume.

Solving these integration hurdles is the foundation of a resilient financial ecosystem. By addressing technical debt early, enterprises can build a platform that is both stable and highly scalable.

How We Built an API-First Neobank Platform

Designing a resilient neobank platform requires a disciplined, step-by-step engineering strategy. At Intellivon, we utilize a proprietary framework that prioritizes security, scalability, and seamless user experiences.

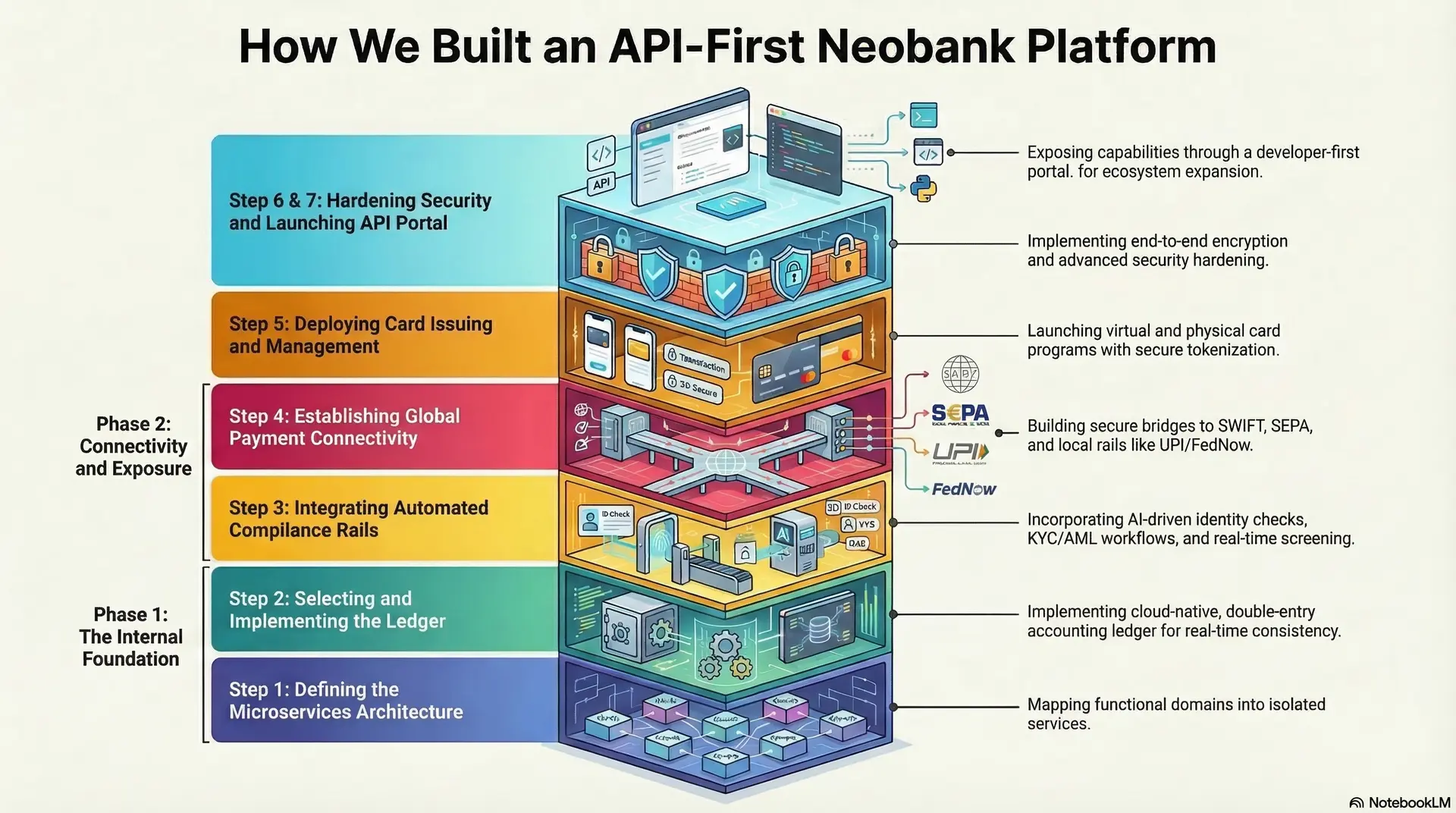

Step 1: Defining the Microservices Architecture

We begin by mapping out the functional domains of your neobank platform. Our team breaks down complex banking operations into isolated microservices for identity, accounts, and payments. This decoupling prevents system-wide failures and allows for independent scaling of high-traffic features.

Consequently, your platform maintains 99.99% uptime even during rapid user growth or maintenance cycles.

Step 2: Selecting and Implementing the Ledger

The ledger is the source of truth for every financial transaction. We implement a cloud-native, double-entry accounting ledger that ensures immutability and real-time consistency.

This system supports multi-currency accounts and complex interest-bearing structures natively. Therefore, your financial records remain audit-ready and mathematically perfect at all times.

Step 3: Integrating Automated Compliance Rails

Security starts with robust KYC and AML verification workflows. We integrate AI-driven identity checks that verify documents and biometrics in seconds. This step includes real-time screening against global sanctions and PEP lists to mitigate risk.

Furthermore, we automate suspicious activity reporting to ensure your platform meets every regulatory mandate without manual intervention.

Step 4: Establishing Global Payment Connectivity

Connecting to diverse payment networks is essential for a modern neobank platform. We build secure bridges to SWIFT, SEPA, and local real-time payment rails like UPI or FedNow.

Our orchestration layer standardizes these fragmented protocols into a single, easy-to-use API. As a result, users can move money across borders with minimal latency and lower transaction costs.

Step 5: Deploying Card Issuing and Management

We provide the technical infrastructure to launch virtual and physical card programs instantly. This includes managing sensitive cardholder data through secure tokenization and 3D Secure protocols.

Our system allows for granular control over card limits and merchant category blocking. Consequently, you can offer highly personalized spending tools to different customer segments.

Step 6: Hardening Security and Data Governance

Financial data requires the highest level of protection against cyber threats. We implement end-to-end encryption for all data at rest and in transit.

This step involves rigorous penetration testing and the setup of SOC 2-compliant monitoring systems. Therefore, your enterprise remains resilient against sophisticated attacks while maintaining strict privacy for every user.

Step 7: Launching the Developer-First API Portal

The final step is exposing your banking capabilities through a world-class developer portal. We provide comprehensive documentation, sandboxes, and SDKs to accelerate third-party integrations.

This empowers your partners to build on top of your neobank platform with ease. This ecosystem-led approach transforms your bank into a scalable platform for the wider fintech economy.

By following this structured methodology, we eliminate the traditional risks associated with digital banking transformation. Our process ensures that your platform is not just functional but also a powerful engine for long-term growth.

Real Case Studies of API-First Neobank Platforms

Examining market leaders reveals how an API-first neobank platform achieves global dominance. These case studies provide a blueprint for enterprises looking to scale financial infrastructure with technical precision.

1. Revolut

Revolut transitioned from a simple travel card to a global “super app” by leveraging a decentralized data model. Their neobank platform uses loosely coupled components that interact through open standards.

This modularity allowed them to deploy reusable services across different geographic regions with minimal friction.

Consequently, they can process millions of queries per week with 90% faster performance than traditional systems. Their open banking API serves as a gateway for third-party providers to integrate seamlessly into their ecosystem.

2. Chime

Chime achieved massive scale by building a serverless stream analytics platform on top of cloud infrastructure. Their architecture captures user events, like card swipes and logins, in real-time to update risk profiles instantly.

Therefore, Chime can detect and defeat fraud within milliseconds while supporting over 1 million events per second. The engineering team built an abstraction layer that hides lower-level complexities from developers. This approach has improved their model calculation speeds compared to legacy implementations.

3. N26

N26 focused on a fully decoupled microservices architecture to maintain a competitive edge in the European market. By moving away from a monolithic backend, they gained the ability to scale specific services like investing or reporting on the fly.

This structural flexibility allows them to launch updates without risking a total system outage. In addition, N26 utilizes a “lean” material flow for data to ensure high degrees of customer satisfaction. Their focus on simple, stable tools allows the team to prioritize speed and user-centric problem-solving.

4. Stripe Treasury

Stripe Treasury represents the pinnacle of “banking-as-infrastructure” for modern software platforms. It exposes regulated financial functions, such as balance management and wire transfers, through a unified API layer. Consequently, non-financial brands can provision FDIC-insured accounts for their users in a matter of weeks.

This removes the need for businesses to manage complex backend compliance and bank partnerships themselves. Stripe’s suite of products essentially turns banking into a programmable service that drives higher retention and lifetime value for its users.

These examples prove that an API-first approach is the most effective way to manage the complexity of modern finance. By following these established models, your enterprise can build a resilient platform that leads the market.

Conclusion

Developing an API-first neobank platform is a strategic necessity for modern growth. This architecture enables the agility, security, and scalability required to lead in a digital economy. Therefore, organizations must transition from legacy systems to modular frameworks to remain competitive.

Intellivon provides the cutting-edge AI and financial infrastructure needed to power this transformation. Contact us today to build your enterprise-grade banking solution and unlock new revenue streams.

Build an API-First Neobank Platform With Intellivon

At Intellivon, API-first neobank platforms are engineered as programmable banking infrastructure, not as simple digital banking apps. Each platform exposes core banking capabilities, such as accounts, payments, cards, and compliance, through secure APIs that allow fintech products, partner platforms, and financial services to integrate seamlessly.

Every solution is designed for enterprise-scale financial ecosystems. Neobank platforms must support high transaction volumes, integrate with multiple financial providers, and maintain governance across complex banking workflows. Our architecture ensures stability, regulatory readiness, and scalability for modern digital banking operations.

Why Partner With Intellivon?

- Governance-First Neobank Architecture: Platforms are built with embedded policy controls, access governance, and audit frameworks to ensure operational oversight across banking services and partner integrations.

- API-Driven Banking Infrastructure: Core financial capabilities, including accounts, payments, cards, and compliance, are exposed through secure APIs that enable rapid product innovation and seamless integrations.

- Multi-Provider Banking Integrations: Our platforms connect with core banking systems, payment networks, card issuers, identity verification providers, and financial data platforms without vendor lock-in.

- Scalable Cloud-Native Architecture: Infrastructure is designed to support growing user bases, increasing transaction volumes, and expanding fintech ecosystems while maintaining high system performance.

- Compliance-Ready Banking Systems: We integrate KYC, KYB, AML monitoring, and regulatory reporting systems to ensure neobank platforms operate within global financial compliance frameworks.

- Secure Infrastructure for Digital Banking: Platforms are built with strong encryption, secure authentication systems, and continuous monitoring to protect financial data and maintain platform resilience.

Organizations exploring API-first neobank platform development can work with Intellivon’s fintech specialists to design and deploy a secure, scalable, and integration-ready digital banking infrastructure built for the future of financial services.

FAQs

Q1. What is an API-first neobank platform?

A1. An API-first neobank platform is a digital banking system where all core services are exposed through APIs from the start. This includes accounts, payments, cards, and compliance systems. As a result, fintech platforms can integrate banking capabilities easily and launch new financial products faster.

Q2. How long does it take to build a neobank platform?

A2. Building a neobank platform typically takes 9 to 18 months, depending on complexity. Development timelines depend on core banking integrations, compliance systems, payment infrastructure, and regulatory requirements.

Q3. What technologies power neobank infrastructure?

A3. Neobank platforms usually rely on cloud-native infrastructure, microservices architecture, and API-driven systems. Technologies often include cloud platforms, secure APIs, event-driven messaging systems, and scalable financial databases.

Q4. What compliance systems must a neobank support?

A4. Neobanks must support KYC, KYB, AML monitoring, transaction reporting, and data protection frameworks. In addition, platforms must comply with regulations such as PCI-DSS and regional financial compliance standards.

Q5. Can enterprises launch white-label neobanks?

A5. Yes, enterprises can launch white-label neobank platforms using existing banking infrastructure and APIs. This approach allows organizations to offer digital banking services without building core banking systems from scratch.