Financial services right now are moving beyond just digital banking and into a new era of open banking. In the past, banks focused on making their own systems and customer channels digital. Now, they need to safely share financial data and payment options through regulated APIs. This shift changes how control works. Fintech companies are now part of bigger networks where data moves between banks, platforms, and third-party providers, all under strict rules and customer consent.

But open access does not mean open risk. For open banking to work, secure API connections are essential. Things like authentication, managing consent, keeping tokens secure, system reliability, and meeting regulatory standards all have to fit together.

Laws and rules such as PSD2, new PSD3 requirements, and local open banking standards set the guidelines for how data is shared and checked. The way a platform is built directly affects its risk of fraud, ability to handle problems, and how well it can grow over time.

At Intellivon, open banking platforms are designed for regulated environments and built to enterprise standards. In this blog, we will look at key architecture models, compliance rules, API security, ways to manage risks, and the main benefits open banking brings to growing businesses.

Why Enterprises Are Adopting Open Banking Platforms Now

Enterprises are accelerating open banking platform adoption due to regulatory mandates, rapid fintech growth, and rising demand for secure data exchange. In addition, customers expect faster payments and personalized financial experiences.

Therefore, organizations view open banking as a strategic move to drive innovation and remain competitive within evolving financial ecosystems.

The global open banking market was valued at USD 31.61 billion in 2024 and is expected to reach USD 135.17 billion by 2030. This growth reflects a projected CAGR of 27.6% between 2025 and 2030, highlighting the rapid expansion of open financial ecosystems worldwide.

Market Insights:

- Regulatory frameworks such as Europe’s PSD2 and the UK’s Open Banking standards require secure data sharing. As a result, transparency improves and competition increases across financial ecosystems.

- Meanwhile, rising smartphone adoption, digital banking maturity, and AI integration enable more personalized services. In addition, secure APIs support stronger authentication and real-time risk analytics.

- Consequently, enterprises gain operational agility. They process transactions faster, improve cash flow visibility, and make data-driven decisions beyond traditional bank statements.

2026 Trends Driving Open Banking Growth

In 2026, open banking continues to gain momentum, particularly through the rapid rise of account-to-account payments. At the same time, frameworks such as eIDAS 2.0 are strengthening digital identity verification across Europe.

Moreover, account information services now support KYC, underwriting, and embedded finance use cases, including EV charging and subscription models.

As a result, open banking is moving beyond infrastructure and delivering real impact through instant payments and seamless onboarding.

What Is an Open Banking Platform?

An open banking platform is a secure system that allows banks and approved third parties to share financial data through standardized APIs. This sharing only happens with customer consent. Therefore, every data request is authorized, recorded, and traceable.

The platform manages user authentication, consent approvals, and secure API connections. It ensures that only the right data is accessed, for the right purpose, at the right time. In addition, it connects with multiple banks and presents data in a consistent format.

For enterprises, this platform becomes a central control layer. It supports real-time account access, direct bank payments, and data-based decision making. As a result, organizations can innovate faster while maintaining security, compliance, and operational stability.

Core Components of a Secure Open Banking Platform

A secure open banking platform is not a single tool. It is a structured system made up of tightly integrated layers.

Each component plays a clear role in managing access, protecting data, and ensuring regulatory alignment. When these layers work together, enterprises gain both control and scalability.

1. API Management and Security Layer

This layer governs how external applications connect to the platform. It enforces authentication, rate limits, and traffic controls. In addition, it protects against abuse, injection attacks, and abnormal traffic patterns.

Strong API management ensures availability without compromising security.

2. Identity and Authentication Framework

Identity orchestration controls how users and third parties are verified. It manages OAuth flows, token issuance, and secure session handling.

When risk levels rise, step-up authentication can be triggered. Therefore, access remains controlled at every stage.

3. Consent Management Engine

Consent is the backbone of open banking. This component captures user approvals, defines access scope, and manages renewals or revocations.

It also stores detailed audit logs. As a result, enterprises can demonstrate compliance at any time.

4. Bank Integration and Data Normalization Layer

This layer connects with multiple financial institutions using standardized APIs. However, banks may structure data differently.

Therefore, the platform translates and normalizes information into a consistent internal format. This enables accurate reporting and decision-making.

5. Risk Monitoring and Fraud Controls

Continuous monitoring detects unusual patterns across transactions and API calls. Real-time analytics flag anomalies before damage escalates.

In addition, system health metrics track uptime and latency across bank connectors.

6. Compliance and Audit Infrastructure

Every action within the platform must be traceable. This component maintains immutable logs, access records, and policy enforcement data.

Consequently, regulatory reviews become manageable rather than disruptive.

Together, these components transform API connectivity into governed financial infrastructure.

The Current Regulatory Reality for Open Banking APIs

Open banking regulations now influence how APIs are designed, secured, and operated. As a result, compliance directly shapes platform architecture and long-term scalability.

Open banking has evolved from an innovation-led concept into a regulated operating model. Today, regulations determine how financial data must be accessed, shared, and protected. They also define how consent should be captured and how third parties must be verified before access is granted. Therefore, enterprises cannot treat APIs as simple integration tools. Instead, they must build them as controlled and traceable access layers.

In addition, regulatory expectations now extend beyond data sharing. They influence authentication flows, uptime requirements, and monitoring practices. This means API design decisions impact both compliance readiness and operational resilience.

1. EU: PSD2 Today and PSD3 Direction

European regulation continues to shape how open banking platforms should function. These rules influence how APIs are designed, how access is granted, and how consent is managed. As PSD3 evolves from PSD2, the focus is shifting from access enablement to access control and operational clarity.

A. APIs as the Primary Access Channel

APIs must now serve as the main route for accessing financial data.

- Direct integrations through customer-facing channels are being phased out.

- Screen scraping is no longer considered reliable or compliant.

- Secure, standardized APIs are expected for AIS and PIS access.

This means enterprises must design platforms where APIs are the default gateway for financial data exchange.

B. Strong Authentication and Evolving Access Controls

Strong Customer Authentication remains a core requirement.

- Authentication must protect data access and payment initiation.

- Exemption rules are evolving across regions.

- Re-authentication timelines may change based on risk and usage patterns.

Therefore, platforms must support step-up authentication when risk levels increase.

C. Consent as a Regulated Asset

Consent is no longer a one-time action.

It must be managed across its lifecycle:

- Creation

- Approval

- Renewal

- Revocation

Consent records must also be auditable. This ensures enterprises can demonstrate compliance when required.

D. Operational Expectations for API Performance

Reliable APIs are now part of regulatory readiness.

Platforms must:

- Monitor API uptime

- Track latency

- Detect failures early

This ensures financial services remain accessible without disruption.

PSD3 is pushing open banking from access enablement toward controlled, secure operations. Enterprises must build platforms that manage identity, consent, and API reliability together.

2. UK: Governance and Reliability Expectations

The UK ecosystem reflects how open banking is maturing beyond initial rollout. The focus is shifting toward long-term governance and consistent performance across providers.

A. Strengthening Governance Models

The UK is working toward structured governance for open banking operations.

- Ecosystem standards are becoming more centralized.

- Long-term oversight is gaining importance.

As a result, enterprises must prepare for more defined operational expectations.

B. Performance as a Strategic Requirement

API availability is now critical.

Platforms must ensure:

- Consistent uptime

- Stable connections with banks

- Reliable transaction processing

Availability is no longer optional. It directly impacts ecosystem trust.

C. Standardized Data and Payment Access

The UK Read and Write API framework supports:

- Account information access

- Payment initiation

These standards reduce integration complexity and improve interoperability.

D. Operational Readiness

Enterprises must support:

- Continuous uptime monitoring

- Incident response processes

- Transparent performance reporting

This ensures resilience across financial partnerships.

UK developments highlight a shift toward performance-driven open banking. Enterprises must treat reliability as a core capability, not a secondary feature.

3. Security Standards That Support Compliance

Beyond regulation, enterprises are expected to follow recognized security practices. These standards help protect data and reduce operational risk.

A. Financial-Grade API Security

Financial-grade API profiles strengthen authentication.

They help:

- Protect sensitive data

- Secure token exchanges

- Prevent unauthorized access

This is especially important for payment-related APIs.

B. OWASP API Security Guidelines

OWASP provides guidance on preventing common API risks.

These include:

- Unauthorized data access

- Broken authentication

- Data exposure

Aligning with these practices improves platform resilience.

Security standards complement regulation. Together, they ensure APIs remain protected, auditable, and reliable within open banking ecosystems.

How an Open Banking Platform Works (End-to-End With APIs)

An open banking platform connects banks, applications, and enterprises through secure APIs. It manages access, consent, and monitoring across every interaction.

An open banking platform operates as a coordinated system rather than a single application. It connects financial institutions, enterprise tools, and third-party providers through secure APIs.

Therefore, the platform ensures that access remains secure and compliant at every stage. These moving parts work together to support real-time financial services without compromising reliability.

1. Core Services Inside the Platform

These core services ensure that every API interaction remains secure and traceable. Together, they help maintain compliance, reliability, and operational control.

A. API Gateway and Web Application Firewall

The API gateway manages how requests enter the platform. It controls traffic flow, applies access rules, and prevents overload through throttling. In addition, the web application firewall protects against threats such as malicious requests and injection attacks.

Together, these tools ensure that only valid and safe traffic reaches internal systems. This helps maintain both security and performance across connected services.

B. Identity and Token Service

This service verifies users and third-party applications before access is granted. It manages authentication through OAuth or similar protocols. Tokens are issued to confirm identity and define access rights.

These tokens also include limits to control what actions can be performed. As a result, only authorized entities can interact with financial data or payment services.

C. Consent Management Service

Consent defines what data can be shared and for what purpose. This service captures approvals, sets access scope, and manages expiration timelines. It also supports consent renewal and revocation when needed.

In addition, it stores records for compliance checks. This ensures that every data exchange remains transparent and authorized.

D. Bank Connector Layer

This layer connects the platform with multiple banks. Each institution may structure data differently. Therefore, connectors adapt to individual banking APIs and map their formats into a common structure.

Retry mechanisms handle temporary failures. This helps maintain continuity even when external systems experience delays.

E. Data Normalization Layer

Financial data arrives in varied formats. This layer standardizes account details and transaction information. It converts inputs into a consistent internal model.

As a result, enterprise applications receive uniform data regardless of source. This improves reporting accuracy and supports better decision-making.

F. Audit and Compliance Log Store

Every action within the platform must be recorded. This component stores logs that cannot be altered. It also tracks request paths using correlation identifiers.

These records help demonstrate regulatory compliance. In addition, they support investigations and internal reviews.

G. Observability and Monitoring

Observability tools monitor system performance and reliability. They track uptime, response times, and error rates. Incident playbooks guide teams during disruptions.

Service level objectives help measure performance goals. Together, these controls ensure stable operations across financial ecosystems.

2. The “Consent to Data/Payment” Flow

This flow explains how secure access to financial data or payments actually happens. Each step ensures that user approval is respected and every action remains traceable.

A. Consent Request Initiation

The process begins when a third-party provider requests access. Your platform creates a consent intent based on the requested scope. This defines what data or payment action is needed.

It also ensures that access is purpose-specific. As a result, no unnecessary permissions are granted.

B. User Authentication at the Bank

The user is redirected to their bank to approve the request. Strong Customer Authentication verifies identity before any access is allowed.

This step confirms that the request is genuine. It also ensures that the user remains in control of their financial data.

C. Token Issuance

Once authentication is complete, the bank issues a secure authorization token. This token defines what actions can be performed.

It also limits access to approved data or payment instructions. Therefore, only permitted operations can proceed.

D. Data Access or Payment Initiation

Your platform then uses the token to connect with the bank’s APIs. It either retrieves financial data or initiates the requested payment.

Access remains restricted to the approved scope. This prevents misuse or overreach.

E. Response and Audit Logging

Finally, the platform standardizes the response for enterprise use. It also records each step in secure logs.

These records support compliance checks and internal monitoring.

This structured flow ensures that every data request or payment remains secure, authorized, and traceable.

Secure API Integration Blueprint For Open Banking Platforms

A Secure API integration combines identity protocols, encryption, consent enforcement, and monitoring frameworks to protect financial data and payment flows.

Secure APIs form the foundation of any open banking platform. They allow banks, enterprises, and trusted partners to exchange financial data and initiate payments safely. However, security does not depend on a single control.

Instead, it requires multiple frameworks working together across identity, communication, and monitoring layers. Therefore, a structured integration blueprint helps ensure safe operations without slowing innovation.

1. Identity and Access Controls Using OAuth and OpenID

Identity and access management ensure that only approved users and applications can interact with financial services. Protocols such as OAuth 2.0 and OpenID Connect help verify identity before granting access. In addition, these frameworks issue tokens that define permissions and usage limits. This ensures that access remains restricted to approved actions.

These controls help:

- Verify user identity before access is granted

- Issue tokens with defined permissions

- Limit third-party actions

- Prevent unauthorized interactions

Financial-grade API (FAPI) profiles further strengthen these protections. As a result, token misuse and unauthorized access risks are reduced.

2. Secure API Communication Through Encryption and mTLS

APIs must exchange financial data securely at all times. Encryption protects sensitive information while it moves between systems. Meanwhile, mutual TLS verifies both parties involved in the communication. This ensures that only trusted entities exchange data.

Secure communication relies on:

- Transport Layer Security for data protection

- Mutual TLS for dual verification

- Certificate-based authentication

Therefore, financial information remains protected during every interaction.

3. Consent Enforcement Through API Scope Controls

Consent defines what data can be shared and why. APIs must enforce these limits consistently. Platforms should ensure that access remains aligned with user approvals.

Key practices include:

- Restricting access to approved data scopes

- Applying expiration timelines

- Allowing users to revoke permissions

- Maintaining consent records

As a result, data sharing remains transparent and controlled.

4. Threat Protection Using OWASP API Guidelines

API endpoints are exposed to potential risks. OWASP guidelines provide practical methods to reduce these threats. They help strengthen platform defenses against misuse.

These protections address:

- Unauthorized access attempts

- Broken authentication

- Excessive data exposure

- Injection-based attacks

Therefore, platforms remain resilient against common vulnerabilities.

5. Monitoring and Anomaly Detection

Continuous monitoring improves visibility across API activity. It helps detect unusual behavior early. This allows teams to respond before issues escalate.

Platforms should monitor:

- Request spikes

- Access anomalies

- Authentication failures

- Data retrieval patterns

In addition, monitoring tools support proactive risk management.

6. Performance and Reliability Safeguards

Secure APIs must also deliver consistent performance. Reliability controls help maintain uninterrupted services. Meanwhile, performance monitoring ensures stability across integrations.

These safeguards include:

- Tracking uptime and latency

- Applying retry mechanisms

- Defining service-level objectives

- Preparing incident response plans

Therefore, financial services remain accessible and dependable.

Secure API integration depends on both technical frameworks and operational discipline. By combining identity protocols, encryption, consent controls, and monitoring, open banking platforms can protect financial data while enabling trusted collaboration.

Risks in Open Banking API Adoption and How to Mitigate Them

Open banking APIs introduce risks across consent, identity, uptime, and compliance. However, structured safeguards help enterprises reduce exposure and operate securely.

Adopting open banking APIs unlocks faster data access and ecosystem partnerships. However, it also introduces operational and security risks. These risks often emerge from weak access control, system dependencies, or compliance gaps.

Therefore, enterprises must identify potential exposure early and apply structured safeguards. A proactive risk management approach strengthens resilience and builds long-term trust.

1. Consent Abuse and Over-Permissioning

Users may approve broader access than required. As a result, more financial data becomes available than is necessary. This weakens data governance and increases the likelihood of misuse.

To address this, platforms should apply granular access scopes tied to clear purposes. In addition, permissions should expire by default and require renewal where needed.

Re-consent workflows help maintain relevance over time. Meanwhile, user dashboards improve transparency and control. Maintaining full consent audit trails further ensures that enterprises can demonstrate compliance when required.

2. Broken Object-Level Authorization (BOLA)

Authorization failures at the data level can expose sensitive customer information. For example, a user may gain access to another account due to weak object-level checks. Consequently, this creates privacy risks and potential regulatory issues.

Enterprises can mitigate this by enforcing object-level access controls across all resources. A centralized policy engine should validate permissions consistently.

In addition, regular testing for IDOR and BOLA vulnerabilities helps prevent unintended exposure. Aligning with OWASP API security guidance strengthens these defenses further.

3. Token Theft and Replay

Attackers may attempt to reuse stolen tokens to retrieve financial data. If successful, unauthorized transactions or data access can occur.

To reduce this risk, platforms should use sender-constrained tokens and short token lifetimes. Device binding patterns can also restrict token reuse.

Meanwhile, anomaly detection tools help identify suspicious behavior early. Aligning with financial-grade API security practices strengthens protection against token misuse.

4. Availability Failures and Ecosystem-Scale Outages

Bank API downtime can disrupt enterprise services. When one integration fails, the impact may extend across operations. As a result, customer experience and trust may suffer.

Enterprises should build resilience into their integration layer. Per-bank connectors with circuit breakers can isolate failures. Backoff strategies and idempotency support safe retries.

In addition, graceful degradation ensures partial service continuity. Monitoring uptime and preparing incident playbooks further strengthen reliability.

5. Data Integrity and Reconciliation Gaps

Financial data may vary across institutions. Inconsistent balances or transaction records can disrupt reporting and decision-making.

To maintain accuracy, platforms should adopt a canonical data model. Bank-specific mapping rules help standardize inputs.

Meanwhile, reconciliation processes verify consistency across sources. Lineage tracking clarifies data origin. Assigning a source-of-truth tag further improves reliability.

6. Regulatory Non-Compliance and Audit Failure

Insufficient logging or governance may prevent enterprises from providing authorized access. Consequently, this increases audit risk and regulatory exposure.

Mitigation requires immutable audit logs and correlation identifiers for traceability. Access governance should be clearly defined. In addition, retaining consent evidence supports accountability. Periodic control testing helps maintain readiness for reviews.

Open banking APIs introduce both opportunity and responsibility. Enterprises that actively manage consent, access, reliability, and compliance risks can adopt these platforms with greater confidence. This not only reduces operational exposure but also strengthens ecosystem trust and long-term scalability.

Use Cases With Workflows and APIs Used

Open banking platforms support enterprise use cases such as cash visibility, lending insights, payments, and fraud monitoring through structured API workflows.

Open banking platforms enable enterprises to unlock new financial capabilities through secure data access and payment initiation. These use cases move beyond simple data sharing.

They support decision-making, risk management, and operational efficiency. Below are key enterprise-focused applications along with how they function and which APIs support them.

1. Account Aggregation for Corporate Cash Visibility

This use case helps enterprises gain a unified view of financial positions across multiple banks. It supports treasury teams by improving visibility and enabling real-time monitoring of cash flow.

Workflow

The process begins when the enterprise creates consent for accessing account and transaction data. The user then authenticates through the bank using strong verification methods.

Once approved, the platform retrieves account details, balances, and transaction history. This information is then normalized and categorized. Finally, the structured data is presented within treasury dashboards for analysis.

APIs Used

- Consent and authorization APIs manage access approvals.

- Account, balance, and transaction APIs retrieve financial data.

2. Affordability and Underwriting for SME Lending

This use case supports credit evaluation by analyzing financial behavior rather than relying solely on static documents.

Workflow

The borrower first grants consent for data access. The platform then retrieves transaction data from the past several months.

This information is enriched to identify income patterns, spending volatility, and existing obligations. Based on this analysis, the system generates a risk profile along with a decision trail.

APIs Used

- Transaction APIs provide financial history.

- Account detail APIs offer contextual insights.

- Optional identity attributes may support verification.

3. Payment Initiation for Supplier Payouts

Enterprises can initiate payments directly from bank accounts, reducing reliance on card networks.

Workflow

The process begins by creating a payment consent intent. The user authenticates with their bank to authorize the transaction. The platform then submits the payment order. Afterward, payment status is tracked, and settlements are reconciled.

APIs Used

- Payment consent APIs initiate authorization.

- Payment initiation APIs execute transfers.

- Status APIs monitor progress.

4. Funds Confirmation for Risk Controls

This use case helps verify whether sufficient funds are available before initiating payments.

Workflow

The platform first creates a payment intent. It then checks available balances using bank-supported verification services. Based on the response, the payment proceeds or is halted.

APIs Used

- Funds confirmation APIs verify account balances.

5. Fraud and Risk Enrichment for Enterprise Payments

Open banking data can strengthen fraud detection and risk analysis.

Workflow

The platform retrieves transaction context through approved access. This data is analyzed to detect anomalies and assess beneficiary risk. Based on findings, the system may trigger additional verification, block the transaction, or escalate for manual review.

APIs Used

- Transaction APIs provide behavioral insights.

- Balance APIs offer financial context.

- Beneficiary data APIs may support risk evaluation.

These use cases demonstrate how open banking APIs support enterprise decision-making and operational efficiency. By combining secure access with structured workflows, organizations can enhance visibility, improve risk assessment, and streamline financial operations.

How Intellivon Builds Open Banking Platforms With APIs

Intellivon builds open banking platforms by defining governance first, then designing secure API flows, consent controls, bank connectors, and reliability monitoring for regulated enterprise scale.

Building an open banking platform requires more than connecting to bank APIs. Enterprises need secure access, clear governance, and stable operations across partners. Therefore,

Intellivon follows a step-by-step delivery process that reduces risk while accelerating adoption. Each step is designed to protect data, support compliance, and maintain reliability at scale.

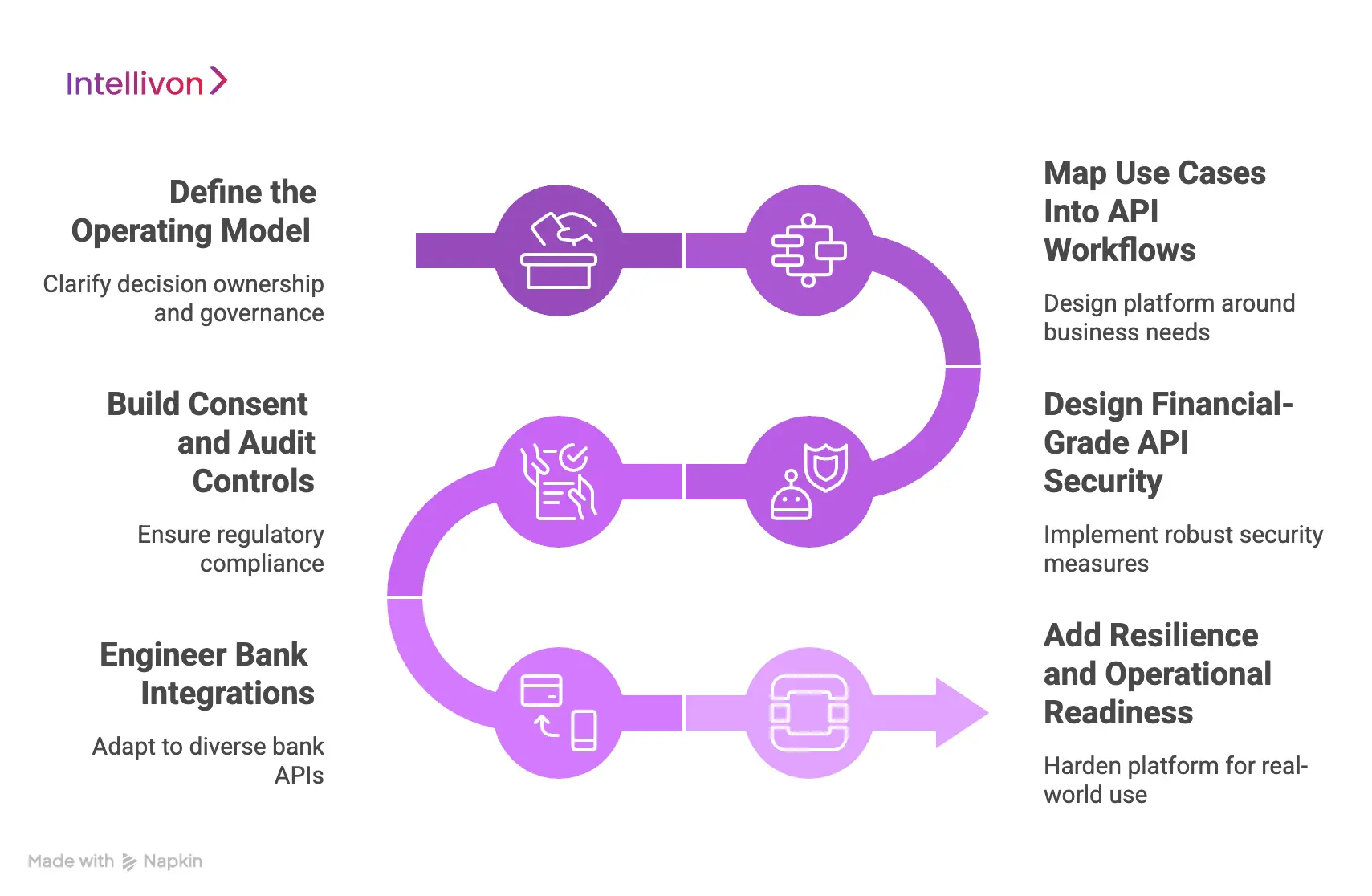

Step 1: Define the Operating Model

The work starts by clarifying who owns key decisions across the platform. This includes consent policies, risk controls, onboarding rules, and audit requirements. In addition, approval workflows are defined for changes to scopes, access rules, and integrations.

This ensures platform decisions remain controlled and traceable. As a result, governance stays strong even as usage grows across teams, regions, and partners.

Step 2: Map Use Cases Into API Workflows

Next, the platform is designed around real enterprise workflows. Intellivon breaks down each use case into a clear sequence, such as consent creation, bank authentication, token exchange, data retrieval, and audit logging.

This approach ensures that the platform supports business outcomes, not generic integrations. In addition, each workflow is linked to the required API families and success criteria. Therefore, implementation stays aligned with operational needs from day one.

Step 3: Design Financial-Grade API Security

Security architecture is built early because it shapes every other layer. Intellivon implements strong authentication, token controls, and least-privilege access. Consent scopes remain granular and purpose-bound.

In addition, sensitive API traffic is protected through encryption and verified connections. This reduces risks such as token replay, over-permissioning, and unauthorized data access. As a result, API security becomes an enforceable platform standard, not a policy document.

Step 4: Build Consent and Audit Controls

Consent and identity controls are treated as regulated records. Intellivon builds consent lifecycle handling for creation, renewal, expiry, and revocation. Identity services support secure authentication and step-up triggers when risk increases.

In addition, every request is logged with traceable identifiers. This makes audits easier and reduces compliance pressure later. Therefore, enterprises can prove what was accessed, when, and under what permission.

Step 5: Engineer Bank Integrations

Bank APIs often vary even when standards exist. Intellivon builds a connector layer that adapts to each institution’s patterns and error behaviors. Data is then normalized into a consistent internal format for accounts, balances, and transactions.

In addition, retry logic and idempotency controls reduce operational failures. This ensures enterprise systems receive consistent outputs across banks. As a result, reporting and decision-making remain reliable.

Step 6: Add Resilience and Operational Readiness

Finally, the platform is hardened for real-world operations. Intellivon defines service level targets for uptime, latency, and error rates. Monitoring tracks API health per bank connector and flags failures early. Incident playbooks support quick recovery.

In addition, performance reporting builds transparency for internal teams and ecosystem partners. Therefore, the platform remains stable even when external bank services degrade.

Our experts build open banking platforms as governed financial infrastructure. This step-by-step approach reduces compliance risk, strengthens API security, and improves operational stability. As a result, enterprises can launch faster while maintaining long-term control, trust, and scalability.

Reliability Engineering for Open Banking APIs

Reliable open banking APIs depend on uptime planning, safe payment handling, smart retries, and strong incident response processes.

Open banking APIs support critical financial activities such as payments and data access. Therefore, they must work consistently without unexpected disruptions. Reliability ensures that services remain available even when external systems experience delays or outages.

For enterprises, this directly affects customer experience and operational stability. A strong reliability approach helps maintain trust while supporting uninterrupted financial workflows.

1. Clear Performance Targets

Reliable platforms begin with clearly defined performance goals. These targets set expectations for how often services should remain available and how quickly they should respond.

In addition, teams monitor these goals regularly to identify any performance drops early. This allows issues to be addressed before they affect users. As a result, enterprises can depend on stable access to financial data and payment services.

2. Safe Payment Processing

Payments must always be handled with precision. Systems should recognize duplicate requests and prevent the same payment from being processed twice. This is especially important when retries are needed due to temporary failures.

In addition, safeguards ensure that financial instructions remain accurate even during disruptions. Therefore, enterprises can avoid reconciliation errors and maintain transaction integrity.

3. Retry and Fallback Mechanisms

Temporary interruptions may occur when connecting with banks. Platforms should retry requests in a controlled manner when these issues arise. If retries fail, fallback processes can maintain continuity by using alternative pathways or delaying execution safely.

Meanwhile, timeout behavior ensures that requests do not remain unresolved indefinitely. This helps prevent cascading delays across financial operations.

4. System Resilience

Failures in one connection should not affect the entire platform. Reliability patterns help isolate problems when they occur. For example, circuit breaker mechanisms limit the impact of failing integrations.

Regional failover strategies ensure that services remain accessible even if one location experiences downtime. As a result, disruptions remain contained, and operations continue smoothly.

5. Incident Readiness

Despite preventive measures, issues may still arise. Therefore, platforms must be prepared to respond quickly.

Runbooks provide step-by-step guidance for handling disruptions. In addition, post-incident reviews help identify root causes and improve future readiness. This ensures that reliability strengthens over time rather than remaining static.

Reliable APIs enable continuous financial operations. By setting clear targets, ensuring safe payment handling, preparing fallback strategies, and strengthening incident response, enterprises can maintain stability across open banking services.

Monetization Of Open Banking Platforms

Open banking platforms create new revenue opportunities through premium APIs, data insights, payment capabilities, and ecosystem partnerships.

Open banking platforms are not just compliance tools. They can also become growth engines for enterprises. By enabling secure financial data access and payment capabilities, these platforms support new service models.

However, monetization must remain aligned with trust and regulatory expectations. Therefore, enterprises should focus on value-driven offerings rather than simple access fees.

1. Premium API Access

Enterprises can offer enhanced API capabilities beyond standard data sharing. These may include faster processing, enriched insights, or advanced payment features. Partners may subscribe to these premium services to improve their own offerings.

In addition, tiered access models allow enterprises to differentiate between basic and advanced usage. This approach creates steady revenue while maintaining accessibility for ecosystem participants.

2. Data-Driven Services

Open banking data can support value-added analytics services. For example, enterprises can provide insights into cash flow trends or financial risk indicators.

These services help partners make informed decisions. In addition, subscription-based analytics can generate recurring income. Therefore, data becomes a strategic asset rather than just an operational resource.

3. Payment Enablement

Payment initiation features allow enterprises to offer direct bank-to-bank transfers. This reduces reliance on traditional card networks. In addition, enterprises can provide services such as automated payouts or payment tracking.

These offerings improve transaction efficiency for partners. As a result, enterprises can monetize payment services while enhancing operational convenience.

4. Ecosystem Partnerships

Open banking platforms encourage collaboration between financial institutions and technology providers. Enterprises can offer onboarding support, integration services, or shared revenue models.

Meanwhile, partnerships may extend into new sectors such as embedded finance. This helps create long-term value across the ecosystem.

Monetization enables enterprises to transform open banking capabilities into sustainable growth opportunities. By combining premium APIs, analytics services, payment solutions, and partnerships, organizations can generate revenue while strengthening their financial ecosystems.

Conclusion

Open banking platforms are shaping the future of financial services. When built with secure APIs, strong governance, and reliable operations, they move beyond compliance into real business value. Enterprises gain faster decision-making, better collaboration, and new revenue opportunities.

However, success depends on the right architecture and safeguards. With the right partner, organizations can turn open banking into a growth engine that strengthens trust, resilience, and long-term competitiveness.

Build An Open Banking Platform With Secure API With Intellivon

At Intellivon, open banking platforms are built as secure financial infrastructure, not just API integrations. Every design decision focuses on protecting data, managing consent, and ensuring reliable performance across enterprise environments.

As financial ecosystems grow, stability becomes critical. Therefore, security, governance, and uptime remain consistent even as integrations expand. This helps organizations innovate faster without increasing operational risk.

Why Partner With Intellivon?

- Enterprise-grade API architecture designed for regulated environments

- Secure consent and identity management are built into every workflow

- Reliable integrations with banks and financial partners

- Compliance-focused monitoring and audit readiness

- Scalable infrastructure that supports growth

Book a strategy call to explore how Intellivon can help you build a secure open banking platform that supports innovation, resilience, and long-term growth.

FAQs

Q1. What is an open banking platform, and how does it help enterprises?

A1. An open banking platform allows enterprises to securely access financial data and initiate payments through APIs. This helps organizations gain better visibility into cash flow and customer behavior. In addition, it supports faster decision-making and new financial services. As a result, enterprises can improve efficiency and collaboration across their ecosystem.

Q2. Why is secure API integration important in open banking?

A2. Secure APIs protect financial data during exchange between systems. They verify identity, enforce consent, and prevent unauthorized access. Therefore, secure integration reduces fraud risks and strengthens compliance. It also ensures that financial services remain reliable and trustworthy.

Q3. What are the main risks of open banking API adoption?

A3. Open banking APIs may introduce risks such as data misuse, unauthorized access, or service disruptions. However, these risks can be managed through strong authentication, consent controls, and monitoring systems. In addition, regular testing helps identify vulnerabilities early.

Q4. How can open banking platforms support enterprise growth?

A4. Open banking platforms enable faster payments, improved data insights, and new partnership opportunities. They help enterprises offer personalized services and streamline operations. As a result, organizations can unlock new revenue streams and enhance customer experiences.

Q5. How does Intellivon help build secure open banking platforms?

A5. Intellivon designs platforms that combine secure APIs, consent management, and reliable integrations. In addition, it focuses on governance and monitoring to maintain compliance. This approach helps enterprises adopt open banking safely while supporting long-term scalability.