Key Takeaways

-

AI-native infrastructure embeds machine learning as the core decisioning layer, while AI-added systems bolt models onto legacy rails.

-

Features defining a genuinely AI-native stack in 2026, including behavioral decisioning engines and ISO 20022 native data processing.

-

ISO 20022 structured data eliminates the gaps that trigger manual reviews, enabling zero-touch reconciliation.

-

Smart payment routing dynamically selects the lowest-cost, highest-approval path per transaction in real time.

-

How Intellivon builds AI-native payment infrastructure for banks using a modular transformation framework.

Payment infrastructures in fintech enterprises have a labeling problem in 2026. Platforms that run machine learning models on top of decade-old processing stacks are calling themselves AI-native. However, they are not, and the difference is not semantic.

AI-native infrastructure is built from the ground up for machine-speed decisions. The architecture underneath is event-driven, the fraud logic runs before execution, and the routing adapts in real time based on cost, risk, and counterparty signals. When AI is bolted onto legacy rails, none of that is possible, regardless of how many models sit on top.

This matters now because the operating environment has changed. Now, real-time settlement is standard across most major markets. Autonomous agents are beginning to initiate B2B transactions without human approval at each step. At the same time, ISO 20022 is generating richer transaction data than most stacks know what to do with. The infrastructure decisions made today will determine which platforms can participate in that environment and which ones cannot.

At Intellivon, we work with enterprises navigating exactly this gap. This post breaks down features that define a genuinely AI-native payment infrastructure and what it takes to build or assess one honestly.

Why “AI-Powered” Payments Break in Real-World Conditions

Success in 2026 payment infrastructure requires moving beyond basic automation to “Contextual Intelligence.” By integrating real-time data normalization with explainable AI (XAI), enterprises can reduce false positives by 40% and ensure regulatory compliance in noisy production environments.

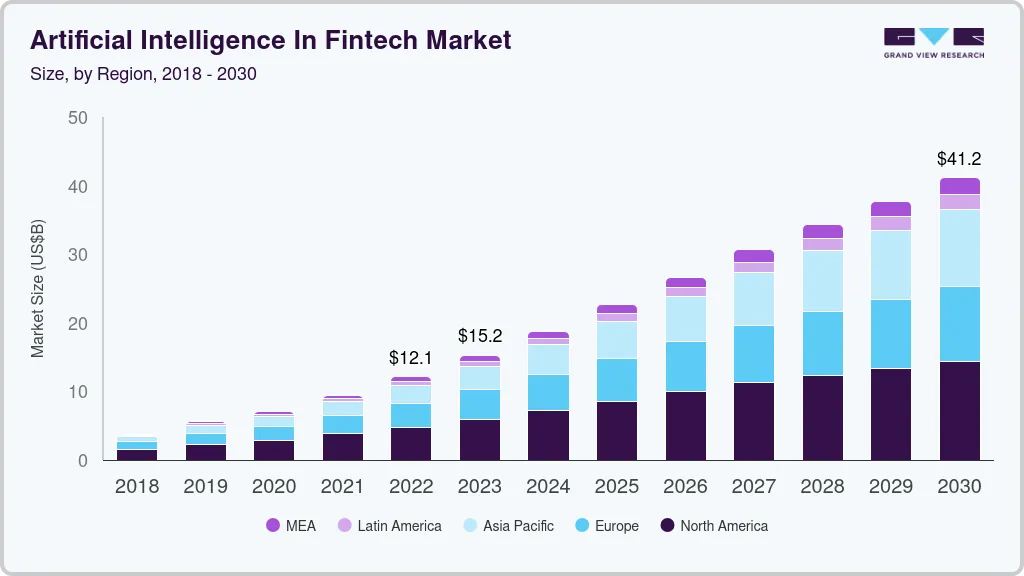

The fintech AI sector is rapidly expanding, with its market value projected to more than quadruple to $41.16 billion by 2030 as financial institutions integrate advanced automation to revolutionize banking and investment efficiency.

1. The Data Is Messier Than the Model

Payment systems do not run on clean training data. They deal with missing fields, duplicate records, and inconsistent merchant descriptors that rarely line up.

Therefore, AI can appear accurate in a test environment but misclassify legitimate payments once deployed. Robust systems prioritize data cleaning before the model ever touches the transaction.

2. Edge Cases Dominate Payments

Real operations are full of exceptions like high-value transfers and first-time beneficiaries. AI systems optimized for the average case often struggle with these scenarios.

Consequently, they can create friction without actually reducing risk. Smart infrastructure recognizes these outliers and applies specific business logic to ensure smooth execution.

3. Speed Creates Strategic Trade-offs

In real-time payments, AI must make decisions in milliseconds, often trading accuracy for low latency. This can result in overblocking customers or missing sophisticated fraud.

The market is shifting toward hybrid systems that combine machine decisioning with human escalation for high-risk events.

4. Fraudsters Are Using AI Too

Attackers now use generative AI to create deepfakes and synthetic identities. They adapt transaction behavior in real-time to evade detection thresholds.

This makes simple scoring models less effective as patterns evolve instantly. Protecting capital now requires proactive, behavioral analysis that anticipates these shifts.

5. Governance and Explainability Matter

AI fails when leaders cannot explain why a transaction was blocked. In regulated environments, black-box decisions create audit risk and slow down adoption.

Supervised automation provides the transparency needed to justify actions to finance teams and regulators.

Navigating these complexities requires an infrastructure built for the reality of 2026. Intellivon provides the cutting-edge enterprise AI solutions needed to turn these operational challenges into a secure growth engine.

What Is AI-Native Payment Infrastructure?

Traditional payment stacks were built on rigid rules and manual workflows, with AI added later as a simple fraud filter. In contrast, an AI-native payment infrastructure is designed with machine learning at the very foundation of the architecture.

It treats every transaction as a data point for real-time learning rather than a static entry in a ledger. Consequently, the system moves beyond simple “if-then” logic to understand the intent and context behind every movement of capital.

1. AI as a core decisioning layer, not an add-on

In an AI-native stack, the intelligence layer is involved in every step, from identity verification to final settlement. It optimizes routing for the lowest fees and highest approval rates in real-time.

This deep integration allows the system to make complex trade-offs that a human operator or a basic rule engine would likely miss.

2. Continuous intelligence vs batch processing systems

Legacy banking often relies on batch processing, where data is settled in chunks, leading to significant visibility gaps. AI-native systems utilize continuous intelligence, analyzing streams of data as they arrive to provide an instant view of liquidity and risk.

| Feature | Legacy Batch Processing | AI-Native Continuous Intelligence |

| Data Processing | Group transactions for end-of-day or scheduled intervals. | Processes data streams in real-time as events occur. |

| Visibility | Provides a historical snapshot (hours or days old). | Offers an instant, live view of liquidity and risk. |

| Fraud Response | Reactive; threats are often identified after the damage is done. | Proactive; flags or blocks anomalies in milliseconds. |

| Decision Speed | Limited by processing cycles and manual reporting. | Enables immediate action based on current market shifts. |

| Efficiency | High latency with significant operational gaps. | Zero-latency orchestration for optimized capital flow. |

Therefore, decision-makers can react to market shifts or fraud surges the moment they happen rather than hours after the fact.

3. Why cloud-native alone is not enough

Moving a legacy system to the cloud provides scalability, but it does not inherently provide intelligence. Cloud-native systems often still follow outdated, linear processes that cannot handle the speed of 2026’s digital economy.

An AI-native approach ensures that the underlying logic is as flexible as the infrastructure, allowing for rapid adaptation to new payment methods or regulatory changes.

4. Shift from workflows to autonomous systems

We are seeing a move away from manual “approval workflows” toward truly autonomous systems that manage themselves within set guardrails. Instead of a staff member reviewing every flagged payment, the AI handles standard exceptions and only escalates the most complex cases.

This shift allows your team to focus on high-level strategy and growth rather than getting bogged down in repetitive, manual oversight.

Deploying these advanced architectures requires a strategic vision for the future of finance.

AI-Native vs AI-Added Infrastructure Explained

The primary difference between high-performing payment stacks and those that struggle to scale lies in their foundational design. While many platforms “bolt on” AI as a supplementary feature to legacy systems, AI-native infrastructure treats intelligence as the primary operating system.

This distinction determines whether your AI initiatives result in a series of disconnected pilots or a cohesive, autonomous financial engine.

Comparison Table: Architectural Maturity in 2026

| Feature | AI-Added (Bolted-On) | AI-Native (Inherent) |

| Logic Integration | AI as an external service call or plugin. | AI as the core decisioning and routing layer. |

| Data Handling | Requires complex ETL and data cleaning. | Unified, real-time data streaming and normalization. |

| Operational Goal | Augments human workflows for efficiency. | Enables autonomous orchestration with human-by-exception. |

| Governance | Siloed controls for each AI feature. | Centralized, built-in policy enforcement and auditability. |

| Scaling Cost | Linear; costs increase with every new feature. | Sub-linear; shared intelligence reduces marginal costs. |

Understanding the Shift in Strategy

Choosing an AI-native approach is a move from performance-based tools to systemic delegation. AI-added systems often require constant manual intervention to bridge the gap between “smart” insights and actual execution.

In contrast, an AI-native stack allows you to define high-level policies that the system then executes across all payment corridors autonomously. Consequently, your enterprise gains the ability to move at machine speed without increasing your operational headcount.

How Does AI Work in Payment Infrastructure?

Understanding the engine of an AI-native system helps founders see beyond the marketing jargon. Instead of following a simple list of rules, the system acts like a highly trained digital analyst that reviews every transaction with superhuman speed.

It looks at thousands of data points simultaneously to decide if a payment is safe, efficient, and profitable for your business.

1. How AI scores transaction risk in milliseconds

When a customer clicks pay, the AI does not just check if they have enough money. It runs a predictive model that compares the current request against millions of historical transactions.

By using advanced mathematics, it calculates a risk score in the blink of an eye. If the score is low, the payment sails through. However, if it is high, the system can automatically ask for extra verification or block it entirely.

2. Behavioral, device, and transaction signal analysis

The system looks at three main categories to verify an identity.

- First, it analyzes behavior.

- Second, it inspects the device, checking for hidden software or unusual locations.

- Finally, it looks at the transaction itself, such as the amount and the merchant.

By combining these signals, the AI creates a unique digital fingerprint that is nearly impossible for fraudsters to forge.

3. How routing decisions are dynamically optimized

Not all payment paths are created equal; some are cheaper, while others are faster or more reliable. An AI-native system uses Dynamic Routing to choose the best path for every single payment. If one banking partner is experiencing a slowdown, the AI instantly redirects the transaction to a different route.

This ensures that your success rates stay high and your transaction costs stay as low as possible.

4. Feedback loops that improve accuracy over time

The most powerful feature of this technology is that it learns from its own mistakes. If a transaction was incorrectly flagged as fraud but later cleared by a human, the AI updates its logic to avoid that error in the future.

These feedback loops mean the system becomes smarter every day without you needing to write new code. Over time, this leads to fewer false alarms and a much smoother experience for your genuine customers.

5. Why real-time data pipelines are essential

For AI to work, it needs fresh information, not data that is hours or days old. Real-time data pipelines act like a nervous system, delivering information from the checkout page to the AI brain instantly.

Without this live connection, the AI would be making decisions based on old news, which is how fraud slips through the cracks. In 2026, the speed of your data determines the strength of your security.

Transitioning to an AI-native mechanism is the only way to stay competitive as payment volumes and fraud tactics evolve. By automating these complex decisions, you protect your margins and provide a frictionless experience for your users.

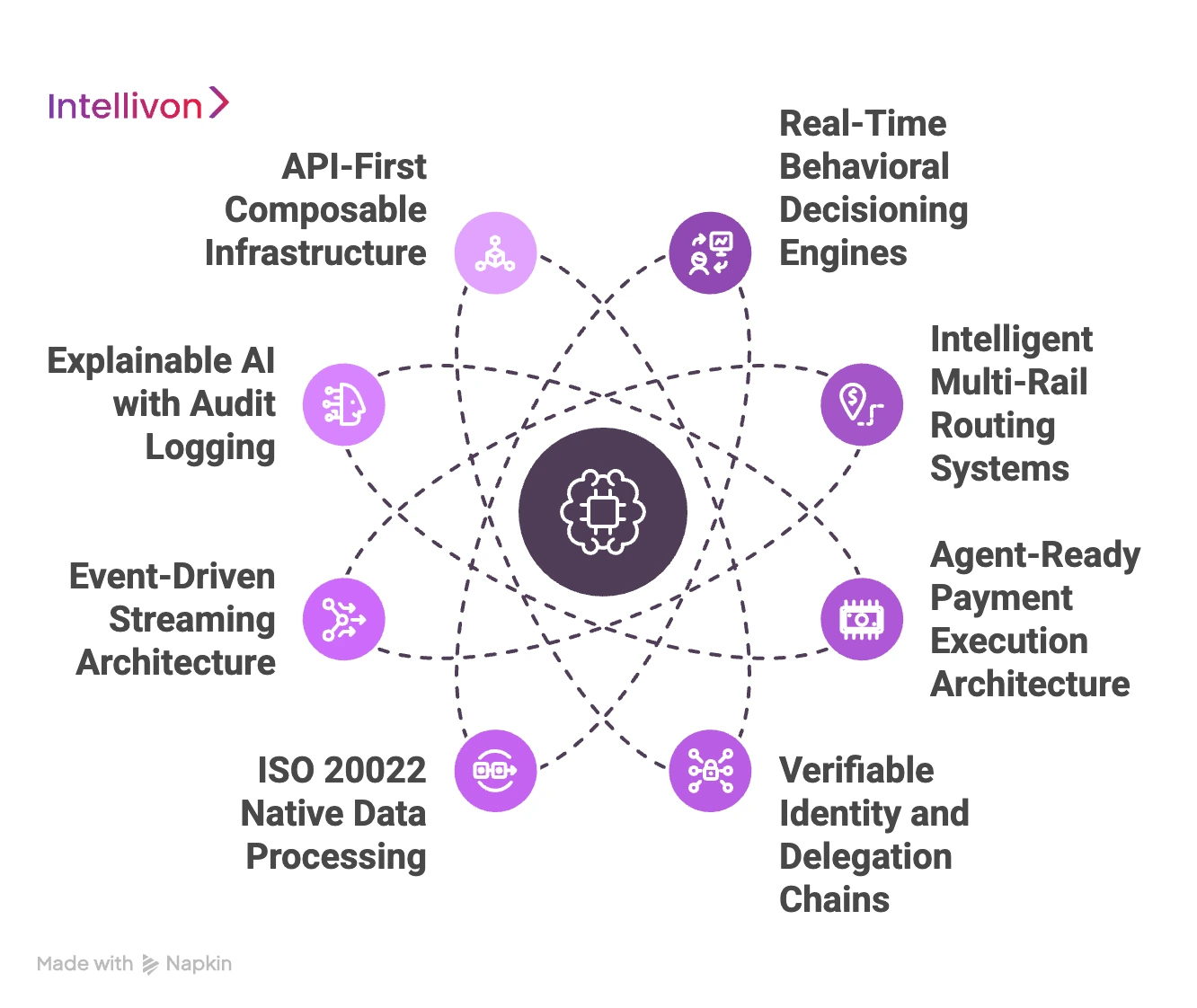

The 8 Features of AI-Native Payment Infrastructure

An AI-native stack is defined by its ability to move from passive processing to active decision-making. In 2026, these eight features will represent the gold standard for enterprises that need to manage high transaction volumes with surgical precision.

These components work together to ensure that every dollar moved is optimized for speed, safety, and cost.

1. Real-Time Behavioral Decisioning Engines

Rather than looking at static data, these engines analyze how a user interacts with the payment interface in real-time. This provides a much higher level of security than traditional passwords or pins alone.

- Biometric Nuance: Tracks typing speed, touch pressure, and scroll patterns to confirm identity.

- Anomaly Detection: Flags transactions that deviate from a user’s established financial profile.

- Adaptive Friction: Only triggers extra security steps when the risk score exceeds a specific threshold.

2. Intelligent Multi-Rail Routing Systems

This feature acts like a GPS for money, constantly evaluating the best path for a payment across various banking networks. It ensures that your platform is never dependent on a single point of failure.

- Cost Optimization: Automatically chooses the rails with the lowest interchange or processing fees.

- High Availability: Reroutes traffic instantly if a specific payment gateway goes offline.

- Speed Selection: Prioritizes instant payment rails for time-sensitive enterprise settlements.

3. Agent-Ready Payment Execution Architecture

As autonomous AI agents begin to handle procurement and subscriptions, the underlying infrastructure must be able to support them. This architecture allows machines to pay other machines within pre-defined business rules.

- Programmable Limits: Sets strict spending caps and frequency rules for AI-driven purchases.

- Contextual Permissions: Grants temporary authorization for specific tasks or vendor categories.

- Machine-to-Machine Protocols: Simplifies the handshake between autonomous buyers and sellers.

4. Verifiable Identity and Delegation Chains

Trust is the most important currency in finance. This feature uses advanced cryptography to ensure that every participant in a payment chain is exactly who they claim to be, even when multiple parties are involved.

- Proof of Authority: Validates that an individual or agent has the legal right to move funds.

- Immutable Logs: Records the entire delegation history to prevent unauthorized account takeovers.

- Zero-Knowledge Proofs: Verifies sensitive information without actually sharing the underlying private data.

5. ISO 20022 Native Data Processing

Modern payments require more than just a sender and a receiver; they need rich data to explain the purpose of the transfer. ISO 20022 is the global standard that makes this high-level communication possible.

- Structured Data: Replaces messy text fields with clear, categorized information for every transaction.

- Automated Reconciliation: Allows finance teams to match invoices to payments with 100% accuracy.

- Cross-Border Harmony: Ensures that international transfers meet the data requirements of every bank involved.

6. Event-Driven Streaming Architecture

Legacy systems wait for things to happen in batches, but AI-native systems react to events as they occur. This architecture ensures that your data is always moving and your intelligence is always fresh.

- Push Notifications: Triggers immediate actions, like balance updates or fraud alerts, the millisecond a transaction starts.

- Scalability: Handles massive spikes in traffic during peak shopping periods without slowing down.

- Decoupled Services: Allows different parts of the system to update independently without risking a total crash.

7. Explainable AI with Audit Logging

In a regulated industry, you cannot simply say the computer said no. This feature ensures that every automated decision comes with a clear, human-readable explanation that satisfies auditors and CFOs alike.

- Decision Transparency: Provides specific reasons why a payment was flagged or approved.

- Regulatory Compliance: Generates the documentation required for AML and KYC audits automatically.

- Bias Monitoring: Constantly checks the AI models to ensure they are making fair and consistent choices.

8. API-First Composable Infrastructure

An AI-native system should be like LEGO blocks, allowing you to swap out different components as your business grows. This flexibility prevents you from getting locked into an outdated technology stack.

- Microservices Design: Separates core functions like ledgering, risk, and routing for easier management.

- Developer Friendly: Offers robust documentation and tools that allow your team to build custom features fast.

- Future Proofing: Enables the easy integration of new technologies like blockchain or central bank digital currencies.

Building a platform with these eight features ensures that your business is not just participating in the digital economy but leading it.

What Does Smart Payment Routing Actually Mean?

In a traditional setup, moving money from point A to point B follows a fixed, pre-determined path. Smart payment routing replaces this rigid approach with a dynamic decision engine that selects the best possible journey for every individual transaction.

By treating the global payment network as a shifting landscape, the system ensures that your business always uses the most efficient route available at that exact microsecond.

1. Balancing cost, speed, and transaction risk

Every payment involves a trade-off between three main factors. Some routes are incredibly fast but come with high fees, while others are cheap but carry a higher risk of being declined. An AI-native system evaluates these variables instantly to find the sweet spot for your specific business goals.

For example, a low-value subscription might be sent through a slower, cheaper rail, while an urgent high-value settlement is routed through an instant, premium network.

2. Why static routing tables no longer work

Static tables are essentially a set of hard-coded rules that tell the system to always use Provider X for US transactions. However, provider performance changes constantly due to technical glitches, maintenance, or regional network congestion.

If Provider X goes down, a static system simply fails. In 2026, the complexity of global finance means a rule written yesterday is often obsolete by today, making static systems a significant liability for growing enterprises.

3. Real-time optimization across multiple rails

Modern payment infrastructure accesses multiple rails all at once. The AI acts as a traffic controller, monitoring the live health of each rail to avoid bottlenecks. If the system detects a spike in latency on one network, it automatically shifts traffic to a more stable alternative.

This real-time optimization ensures that your customers never experience a failed payment due to a backend issue they cannot see.

4. Failover and resilience in routing decisions

Resilience is about an invisible, automatic recovery. If a transaction attempt fails on the first route, the system can instantly “retry” through a different provider without the customer ever knowing there was a problem.

This failover capability protects your revenue and maintains a professional, seamless experience. Consequently, your platform remains operational and reliable even during major regional banking outages or network disruptions.

Smart routing transforms payments from a static cost center into a strategic advantage that protects your margins.

How Does AI Improve Fraud Prevention Systems?

Traditional fraud prevention relied on a library of known bad behaviors, which meant the system was always one step behind the latest scam. AI-native infrastructure flips this model by focusing on what is normal for your specific users and flagging anything that deviates from that baseline.

In 2026, this means moving away from rigid blocks toward a fluid, intelligent defense that adapts as quickly as the threats do.

1. Shifting from reactive rules to predictive modeling

Legacy systems wait for a fraud pattern to be reported before they can stop it, which often results in significant financial leakage. AI-native models analyze historical data to predict where the next attack will come from, blocking suspicious attempts in real-time.

This predictive approach allows you to stay ahead of organized fraud rings that use automated tools to test thousands of stolen cards simultaneously.

2. Reducing false positives through deep context

One of the biggest frustrations for high-growth platforms is having a legitimate customer’s payment declined. AI reduces these false positives by looking at a wider range of context, such as the time of day, the type of device used, and even the typical shipping speeds for that specific user.

Consequently, the system can distinguish between a loyal customer traveling abroad and a fraudster using a stolen credential from a different country.

3. Identifying synthetic identities and deepfakes

As fraudsters use AI to generate fake IDs and realistic personas, traditional KYC checks are no longer enough.

AI-native systems use advanced pattern recognition to spot the subtle inconsistencies that reveal a synthetic identity.

They can detect if a face in a video is a deepfake or if a set of financial documents has been digitally altered, providing a level of security that human reviewers simply cannot match.

4. Adaptive friction for a better user experience

Not every suspicious transaction needs to be blocked. Instead, sometimes, it just needs an extra layer of proof. AI-native infrastructure uses adaptive friction to challenge only the transactions that look genuinely risky.

For example, a trusted user on their home device might never see a verification screen, while a new user making a large purchase might be asked for a quick biometric check. This keeps your checkout process fast for most people while remaining extremely secure.

By integrating these intelligent layers, you turn your fraud department from a cost center into a trust-building engine.

How Does ISO 20022 Unlock AI Capabilities?

The global shift to ISO 20022 provides the structured foundation necessary for truly autonomous financial systems. By using a standardized XML-based language, this format ensures that every participant in the payment chain speaks the same technical tongue.

This uniformity eliminates the data gaps that typically trigger manual reviews. Consequently, your AI can operate at full speed because it no longer has to pause to interpret “unstructured” or “messy” data strings from different global banks.

1. Structured vs Unstructured Payment Data

| Feature | Legacy Unstructured Data (MT/ACH) | ISO 20022 Structured Data (MX) |

| Data Format | Limited text fields with character caps. | Rich XML tags with unlimited capacity. |

| AI Interpretation | Uses “fuzzy logic” and guesswork to identify parties. | Direct, 1:1 mapping of data to specific labels. |

| Error Rate | High, truncated names lead to false fraud flags. | Low, full legal entity identifiers (LEI) are included. |

| Contextual Depth | Minimal; only shows sender, receiver, and amount. | Maximum; includes invoices, tax IDs, and purpose. |

| Processing Speed | Slow, requires cleaning before the AI can use it. | Instant, “AI-Ready” the moment it enters the stack. |

2. AI use cases enabled by richer data formats

With richer data, your AI moves from a simple gatekeeper to a strategic business advisor. It can analyze the “purpose codes” within an ISO message to predict your company’s seasonal cash flow needs or automatically flag a vendor whose pricing has deviated from your contract.

This depth of information allows the system to offer personalized financial insights that were previously locked away in unreadable text fields.

3. Impact on reconciliation and automation

The most expensive part of a payment platform is the back-office team manually matching payments to orders. ISO 20022 includes structured remittance info that links a payment directly to its specific invoice number and tax data.

Therefore, the AI can perform “Zero-Touch Reconciliation,” automatically updating your ledger and closing open accounts. This allows you to scale your business to millions of transactions without adding a single person to your finance team.

4. Why legacy formats limit AI performance

Legacy formats act like a filter that strips away the detail an AI needs to be smart. When a system “truncates” a name because the field is too short, the AI loses the ability to distinguish between a legitimate client and a sanctioned individual.

This lack of detail forces the AI to be overly cautious, leading to high rejection rates. In the competitive market of 2026, relying on these thin data formats is a strategic bottleneck that prevents your platform from providing a frictionless user experience.

Adopting an ISO 20022-native infrastructure is the only way to ensure your AI is working with a full deck of cards. Intellivon specializes in deploying these data-rich frameworks, turning your payment messages into a powerful engine for automated growth and perfect compliance.

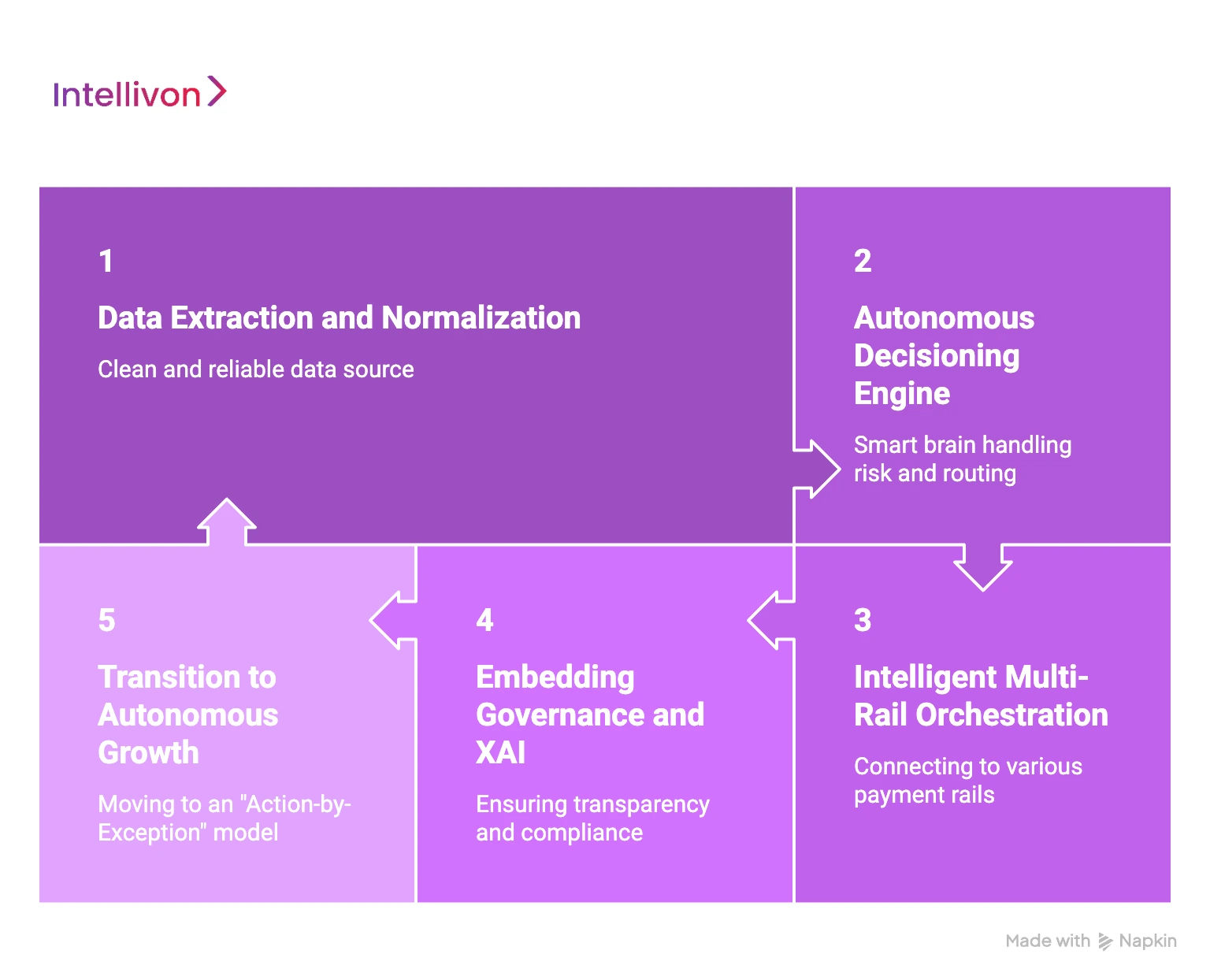

How We Build An AI-Native Payment Infrastructure For Banks

Intellivon’s deployment methodology follows a “Modular Transformation” framework. We begin by establishing a real-time data shadow of your current ledger, allowing our AI models to learn and optimize in a “dark mode” environment before taking over live transaction orchestration, ensuring zero downtime and 100% safety.

Phase 1: High-Fidelity Data Extraction and Normalization

The first step is ensuring the AI has a clean, reliable source of truth. We break the data silos that banks have by implementing real-time streaming pipelines that feed into a unified data lake.

- Schema Mapping: We translate fragmented legacy records into the ISO 20022 standard automatically.

- Latency Reduction: Our pipelines ensure data moves from the core to the AI in under 5 milliseconds.

- Cleaning Protocols: Automated scripts remove duplicates and fix inconsistent merchant descriptors.

| Step | Action | Outcome |

| Connectivity | API-first hooks into the Core Banking System. | Unified view of all transaction silos. |

| Ingestion | Real-time event streaming via Kafka or similar. | Moving from batch to continuous data. |

| Refining | AI-driven data cleansing and labeling. | “Machine-Ready” data for model training. |

Phase 2: Deploying the Autonomous Decisioning Engine

Once the data is flowing, we deploy the intelligence layer that will handle risk and routing. This engine sits on top of your existing rails, acting as a smart “brain” that directs traffic based on real-time business goals.

- Model Training: We use your historical data to create a “digital twin” of your bank’s risk profile.

- Routing Logic: We define high-level policies for cost and speed that the AI executes autonomously.

- Behavioral Baselines: The system begins building unique identity profiles for every account holder.

Phase 3: Implementing Intelligent Multi-Rail Orchestration

In this phase, we connect the decisioning engine to various payment rails (ACH, SWIFT, RTGS, and Digital Currencies). The AI now has the power to choose the most efficient path for every individual payment request.

- Dynamic Failover: If a specific network experiences high latency, the AI automatically reroutes the payment.

- Liquidity Management: The system predicts cash flow needs to ensure enough capital is always in the right rail.

- Cost Arbitrage: The AI constantly scans for the lowest-fee path across different banking partners.

Phase 4: Embedding Governance and Explainable AI (XAI)

For banks, transparency is non-negotiable. We build a comprehensive audit layer that records exactly why the AI made every single decision, ensuring you remain fully compliant with regional and global regulators.

- Audit Trails: Every automated block or approval is logged with a human-readable “Reason Code.”

- Policy Guardrails: You set the “red lines” that the AI can never cross, regardless of optimization goals.

- Bias Detection: Continuous monitoring ensures the AI treats all customers fairly and consistently.

Phase 5: Transition to Autonomous Growth

The final step is moving from manual oversight to an “Action-by-Exception” model. Your team no longer manages individual payments; they manage the high-level strategy and parameters that the AI follows.

- Strategic Dashboards: Real-time visibility into approval rates, leakage, and total savings.

- Automated Scaling: The infrastructure scales its processing power automatically during peak volumes.

- Continuous Feedback: The system keeps learning from every transaction, getting smarter every day.

We provide a blueprint for the future of institutional finance. Intellivon acts as your strategic partner, ensuring that your journey to an AI-native infrastructure is fast, compliant, and built for the long-term demands of 2026.

Conclusion

The shift to AI-native infrastructure marks the end of passive payment processing. By embedding intelligence into the core architecture, enterprises move beyond rigid rules to embrace autonomous, real-time decisioning that scales without friction.

This transition is no longer a luxury but a strategic necessity for those seeking to lead in a high-velocity digital economy. Now is the time to build a financial foundation that is truly built for the future.

Build AI-Native Payment Infrastructure With Intellivon

Building an AI-native payment infrastructure rests on designing a system where every payment decision is made in real time, across fraud, routing, settlement, and compliance.

At Intellivon, we build payment infrastructure where AI is embedded into the core decisioning layer, enabling faster transactions, lower risk, and seamless scalability across modern payment rails.

Our approach ensures your platform can operate in real-world conditions, handling high transaction volumes, evolving fraud patterns, and complex regulatory requirements without performance trade-offs.

A. Designing Real-Time Payment Decision Architectures

Payment infrastructure today operates in milliseconds. We design systems where every transaction is evaluated, routed, and executed instantly without latency.

- Low-latency decision pipelines for sub-second transaction processing

- Event-driven systems using streaming frameworks like Kafka

- Unified decision engines across fraud, routing, and compliance

- Seamless orchestration across card, ACH, RTP, and cross-border rails

This ensures every payment decision happens within the transaction flow, not after it.

B. Enabling Agent-Ready Payment Architectures

As agentic commerce evolves, payment systems must support AI-initiated transactions safely and reliably.

- Separation of decisioning and execution layers

- Secure handling of credentials through tokenization

- Delegation frameworks for controlled payment authority

- Compatibility with emerging agentic protocols and standards

This ensures your infrastructure is ready for AI agents without compromising control or security.

C. Embedding Explainability and Compliance Into the Core

AI in payments must be transparent and compliant by design. We build systems that meet regulatory requirements without slowing operations.

- Transaction-level explainability for AI decisions

- Continuous audit trails across all system actions

- Compliance-ready architecture aligned with PCI DSS and GDPR

- Role-based controls for governance and investigation workflows

This ensures your system remains auditable, compliant, and regulator-ready at all times.

D. Integrating AI Across the Payment Ecosystem

AI-native infrastructure only works when it connects seamlessly across systems. We design integration layers that unify your payment stack.

- API-first architecture for modular system connectivity

- Integration with gateways, processors, and core banking systems

- Unified intelligence across card, ACH, RTP, and cross-border flows

- Phased modernization without disrupting existing operations

This allows you to evolve your infrastructure without replacing everything at once.

At Intellivon, we help you map your transaction volume, system complexity, and business goals into a clear AI-native architecture and roadmap.

Talk to our team to get a tailored payment infrastructure strategy and project estimate.

FAQs

Q1. What defines AI-native vs AI-powered payments?

A1. AI-powered systems bolt external machine learning tools onto legacy frameworks. AI-native infrastructure builds intelligence into the core architecture. This allows for unified data flows and sub-millisecond decisioning, whereas powered systems often struggle with latency and fragmented data silos that require manual reconciliation.

Q2. Can legacy systems support AI payments?

A2. Legacy systems can integrate AI via APIs, but they face inherent bottlenecks. Built for batch processing, they lack the real-time data depth AI requires. While a hybrid approach works during a transition, only native stacks fully unlock autonomous routing and complex behavioral analysis.

Q3. How does AI improve payment routing?

A3. AI replaces static rules with dynamic orchestration. It analyzes real-time variables like network health, success rates, and interchange fees across multiple rails. If a specific banking partner experiences a slowdown, the AI instantly redirects the transaction to the most efficient, cost-effective path available.

Q4. Are AI payment systems secure and compliant?

A4. Yes, they enhance security by identifying subtle anomalies that manual rules miss. For compliance, they utilize Explainable AI to provide human-readable audit logs for every decision. This transparency ensures that automated blocks or approvals satisfy strict regulatory requirements while reducing human error.

Q5. What is the cost to build AI-native systems?

A5. Initial investment depends on data complexity, but the long-term ROI is significant. Because the system is autonomous, operational costs stay flat as transaction volumes grow. Most enterprises recover costs within a year through reduced fraud leakage, lower fees, and higher authorization rates.