Key Takeaways:

-

Agentic fraud platforms combine real-time transaction scoring, behavioral analytics, graph intelligence, and AI case orchestration.

-

Governed actions, including step-up verification, holds, escalation, and evidence gathering, require human approval gates.

-

Explainability, audit logs, model governance, and real-time integrations are non-negotiable production architecture requirements.

-

Custom platforms cost $70,000 to $300,000 and take 4 to 9 months, depending on complexity.

-

How Intellivon builds agentic fraud platforms around institution-specific fraud typologies and controlled decision limits.

The gap between agentic fraud platform vendors that hold up in production is architectural, not feature-based. The leading companies cover payment fraud, account takeover, and synthetic identity across banking, fintech, and ecommerce. In each segment, the evaluation question is whether the platform detects fraud networks or scores individual transactions. That architectural choice determines accuracy for organized fraud rings, mule networks, and synthetic identity schemes at scale.

The evaluation criterion that comparison guides consistently miss is graph-based fraud network detection. Consequently, platforms that score individual transactions miss the patterns behind fraud rings and mule schemes. INTERPOL’s 2026 assessment found global financial fraud losses reached $442 billion in 2025. Graph-based detection is therefore what determines whether a platform addresses fraud at its actual scale.

This guide evaluates leading companies against detection architecture, AI model design, and compliance posture. Accordingly, this blog covers vendors by fraud type, detection architecture, and total cost of ownership to build such a platform from the ground up.

What is An Agentic Fraud Detection System?

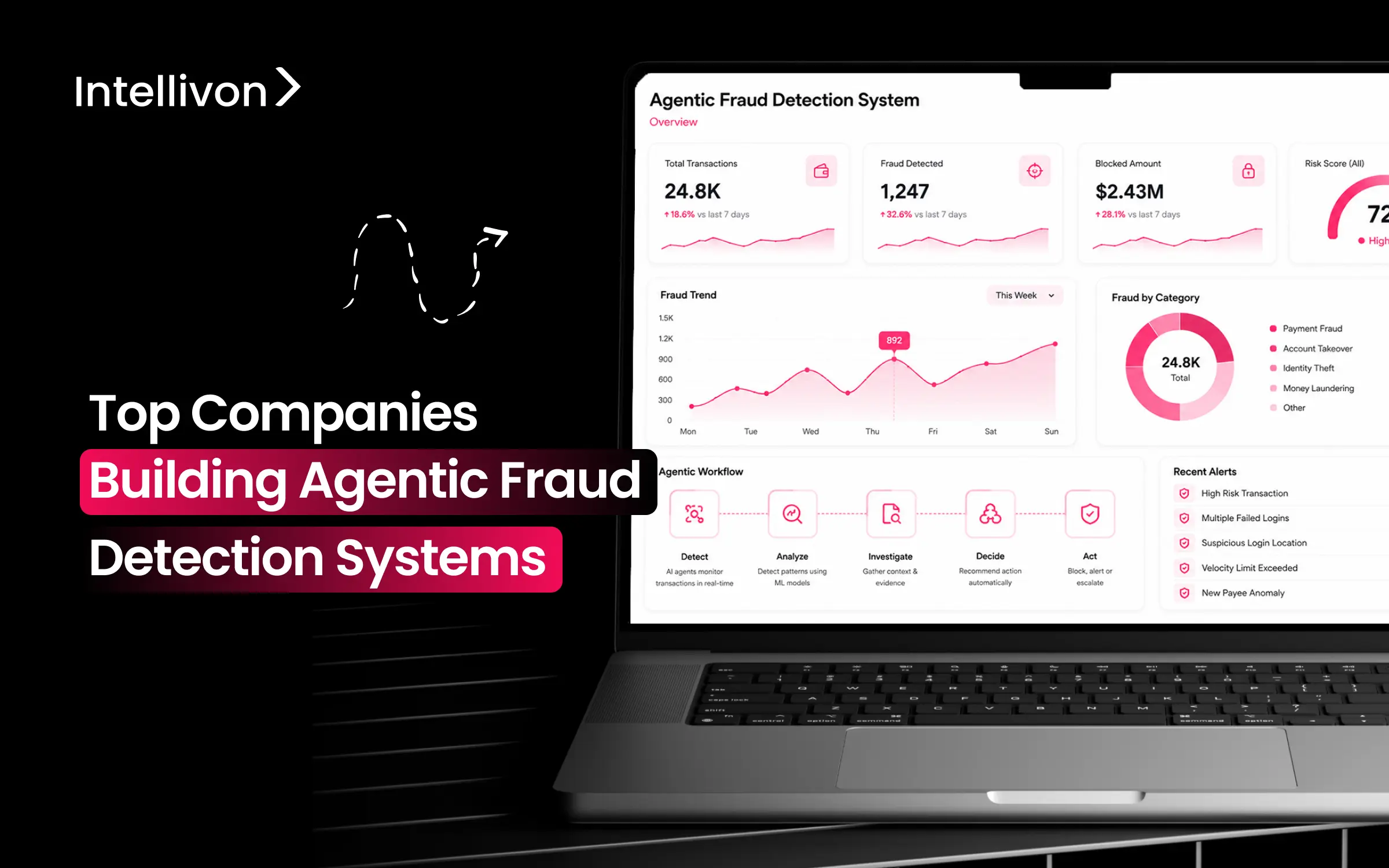

An agentic fraud platform is an autonomous AI system that thinks and acts like an expert investigator. Unlike old systems that only follow fixed rules, this platform uses self-directed AI agents to continuously monitor transactions in real time.

The software can automatically gather evidence, analyze complex patterns, and rewrite its own fraud rules. Consequently, it stops new financial crimes instantly without needing constant human intervention.

What Makes a Fraud Detection Platform Agentic?

An agentic fraud platform does more than calculate risk or generate an alert. It can interpret the event, identify missing evidence, select approved tools, gather context, recommend a response, route the case, and record every step for review.

Therefore, it shifts financial crime operations from passive monitoring to active, autonomous defense.

1. Move Beyond Rule-Based Fraud Alerts

An agentic fraud platform converts static compliance checks into a self-directed investigative workflow. Traditional systems rely on fixed logic that fraud rings can easily bypass.

In contrast, modern architectures use an autonomous fraud rule generation platform to adapt to new threat vectors instantly.

- Static rules: Traditional systems flag a flat $10,000 transfer if it originates from a new IP address, creating rigid binary outcomes.

- Predictive scoring: Predictive models go one step further by assigning a 92% risk score based on historical data patterns.

- Adaptive machine learning: An adaptive fraud detection AI system automatically modifies its parameters as new data flows into the system.

- AI-assisted investigation: The architecture automatically extracts user device fingerprints, checks beneficiary account ages, and builds visual entity graphs.

- Governed agent action: An AI fraud detection agent orchestration platform inspects all telemetry data and pauses the transaction before funds leave the institution.

2. Separate GenAI Copilots From Autonomous Agents

True autonomous fraud detection system design requires independent execution, not just conversational chat interfaces. At the same time, many platforms offer basic copilots that merely summarize alerts for a human analyst.

A real agentic fraud prevention workflow automation engine uses specialized, tool-using AI fraud detection agent architectures to execute tasks without constant prompts.

- Copilot: Responds to an analyst’s text request to summarize case notes or search history.

- Rule assistant: Converts natural language instructions into basic, structured fraud rules.

- Investigation agent: Autonomously retrieves, cleans, and analyzes cross-border case evidence.

- Decisioning agent: Chooses the most appropriate, approved next action based on compliance risk.

- Orchestrator agent: Assigns specific tracking tasks to specialist agents and manages system memory.

- Execution agent: Calls permitted operational API tools to lock accounts or trigger step-up authentication.

This distinction remains critical because legacy risk platforms like NICE Actimize have cautioned that some vendors describe conventional workflow automation or RPA as agentic AI. At the same time, true agentic deployment requires a goal-oriented fraud detection engine design that actively handles unexpected data anomalies.

Establish an Agentic Fraud Maturity Model

Transitioning to an agentic fraud platform requires a structured upgrade path. Organizations must evaluate their current infrastructure against a standardized maturity model to identify automation gaps.

The table below outlines the five operational levels of financial crime detection capabilities.

| Level | Capability | Enterprise Example |

| Level 0 | Static rules | Block transactions from a prohibited country |

| Level 1 | Predictive models | Scorecard fraud probability using historical data |

| Level 2 | Adaptive intelligence | Adjust risk scores using changing behavioral patterns |

| Level 3 | Agent-assisted investigation | Retrieve cross-border evidence and prepare a case file |

| Level 4 | Governed autonomous workflow | Close low-risk alerts or trigger approved interventions |

Moving up this maturity model drastically reduces the time investigators spend on manual data retrieval. Level 4 systems utilize an adaptive fraud detection AI system framework to safely automate high-volume triage.

Controlled execution within documented risk policies remains the absolute baseline requirement for enterprise deployment; unrestricted autonomy is never the goal. Therefore, by enforcing strict programmatic boundaries, financial institutions can eliminate the threat of unexpected agent behavior.

This clear governance structure paves the way for inspecting the core engineering components that power these autonomous platforms.

Why Fraud Teams Are Moving Beyond Alert-Only Systems

Fraud teams are adopting agentic workflows because risk scoring alone does not resolve cases. The largest operational burden begins after the platform creates an alert. Consequently, migrating to an autonomous, goal-oriented architecture is essential for teams struggling with manual backlogs.

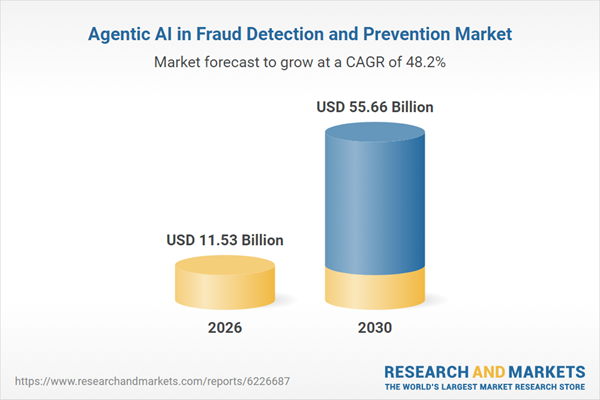

The global market for agentic AI in fraud detection and prevention is expanding rapidly, growing from $7.73 billion in 2025 to $11.53 billion in 2026 at a compound annual growth rate (CAGR) of 49.1%. Driven by cashless payments, it is projected to hit $55.66 billion by 2030.

1. Investigators Spend Too Much Time Gathering Context

Manual context gathering drains investigative resources and delays crucial risk decisions. Analysts routinely log into multiple disjointed systems to reconstruct a single fraudulent event sequence, which dramatically increases operational overhead. However, an agentic fraud platform solves this by executing automated workflows the moment an anomaly is detected.

- Data retrieval: The platform instantly pulls complete transaction histories and customer profile metadata across multiple legacy systems.

- Device analysis: It compares device fingerprint records and geolocations against established baseline behavioral patterns.

- Case preparation: The system reviews previous historical alerts and constructs comprehensive, regulatory-ready case narratives automatically.

Furthermore, a 2025 industry survey by Hawk AI confirmed that case investigations remain the most critical target for automation. At the same time, narrative drafting and background research also ranked as high-priority areas where compliance teams experience the most severe operational bottlenecks.

2. Instant Payments Require Decisions Before Funds Move

Real-time payment networks leave zero window for traditional, delayed manual fraud reviews. Because transactions settle in seconds, security systems must make deterministic choices before funds are permanently transferred.

Therefore, a real-time fraud detection AI agent must dynamically choose the exact operational path for every transaction.

- Payment types: The platform actively monitors FedNow, RTP, ACH, wire transfers, digital wallets, and cross-border clearings.

- Attack vectors: It dynamically intercepts authorized push payment fraud (APP fraud) and complex money muling operations.

- Routing actions: The orchestrator instantly decides whether to approve, challenge, temporarily hold, route for review, reject, or escalate the transaction.

To achieve this level of security, engineering teams specialize in deploying low-latency event processing architectures for financial institutions. These high-throughput real-time transaction fraud scoring AI systems process complex risk logic in under 50 milliseconds, effectively blocking fraud before settlement.

3. False Positives Affect Both Cost and Customer Experience

Relying purely on model accuracy metrics can hide massive operational costs and user friction. High false-positive rates alienate legitimate users while burying compliance teams under mountains of low-risk alerts.

On the other hand, an agentic fraud platform uses multi-layered context to drastically reduce unnecessary transaction declines.

- User friction: Legitimate transactions get declined, leading directly to high shopping cart abandonment and broken customer trust.

- Operational drain: Manual review volumes spike, forcing companies to scale up headcount to handle identical alerts.

- Alert fatigue: Investigators miss actual fraud rings because they are exhausted by thousands of safe, mislabeled transactions.

Consequently, traditional models generate excessive noise because they analyze highly imbalanced data distributions. By focusing heavily on precision-recall optimization, platforms can tune models for real-world production distributions and lower false positives by up to 60%.

4. Fraud and AML Workflows Increasingly Overlap

Modern financial crime operations require a unified infrastructure because fraud and money laundering have functionally merged. Bad actors use identical networks of synthetic accounts to both steal funds and clean dirty capital. As a result, defensive architectures must analyze these threats through a single, coordinated lens.

- Identity fraud: The platform checks for synthetic identity fraud, credential stuffing, and account takeover indicators simultaneously.

- Network threats: It intercepts business email compromise (BEC), money muling networks, and large-scale organized fraud rings.

- Compliance exposure: The engine tracks transaction laundering patterns while shielding the institution from immediate sanctions exposure.

This integrated approach connects fraud events to underlying anti-money laundering workflows through advanced entity resolution engines. This ensures your data stays synchronized, fully auditable, and compliance-ready across every corporate department.

The modern financial market does not simply require a slightly more accurate predictive model. Instead, banks need a highly coordinated detection, investigation, intervention, and automated SAR reporting infrastructure to survive. Building this defensive foundation requires evaluating the specific architectural components that make these autonomous systems function.

How We Ranked the Agentic Fraud Platform Companies

Evaluating the top providers across the fraud prevention landscape requires distinguishing between fundamentally different deployment models.

Specifically, this ranking compares two distinct provider categories: custom software engineering firms like Intellivon and Idea Usher that build custom, client-owned systems, and specialized vendor companies that license proprietary fraud technology products.

1. Evaluate Custom Builders on Development Capability

Custom software engineers do not sell fixed software licenses; instead, they build bespoke multi-agent fraud detection system development architectures tailored to an enterprise’s exact infrastructure.

Therefore, evaluating these partners requires looking at their engineering depth, domain expertise, and MLOps lifecycle maturity rather than standard product feature lists.

The table below outlines the core criteria used to score custom development firms.

| Custom Development Criterion | Strategic Weight | Technical Focus Area |

| Agentic AI & Orchestration Expertise | 20% | Multi-agent state preservation, memory management, and deterministic planning. |

| Fintech & Fraud Domain Knowledge | 15% | Real-time payment rails (FedNow, RTP), banking compliance, and AML crossovers. |

| Custom Architecture Capability | 15% | Event-driven architecture, zero-trust data ingestion, and sub-50ms processing. |

| Model Development Depth | 15% | Precision-recall optimization, graph neural networks, and anomaly models. |

| Integration Experience | 15% | Legacy core banking connectors, payment processors, and biometric APIs. |

| Governance & Explainability | 10% | Strict audit trail logging, bias controls, and interpretable fraud scoring. |

| Production Engineering & MLOps | 10% | Continuous model retraining, drift monitoring, and CI/CD pipelines. |

A major benefit of this custom approach is that the enterprise buyer typically owns the underlying code, model weights, and intellectual property.

As a result, companies can eliminate recurring per-transaction SaaS licensing fees while maintaining complete operational control over their detection models.

2. Evaluate Product Vendors on Platform Capability

Proprietary product vendors deliver ready-made software ecosystems designed for rapid out-of-the-box deployment.

Consequently, the evaluation framework for these off-the-shelf platforms focuses strictly on immediate feature availability, vendor-managed model updates, and pre-built API ecosystem integrations.

- Demonstrated agentic functionality (20%): The platform must prove it uses autonomous fraud rule generation platform tools rather than basic, static robotic process automation.

- Real-time decisioning and speed (15%): The engine must achieve sub-50ms transaction latency to successfully support instant settlement networks like FedNow.

- Fraud coverage and model depth (15%): Out-of-the-box models must comprehensively cover card-not-present fraud, identity theft, and synthetic identity fraud.

- Case automation and integration (20%): The system must offer tool-using AI fraud detection agent structures that integrate into standard case managers and orchestrate auto-triage pipelines.

- Explainability, governance, and deployment (30%): Platforms must deliver clear audit logging for suspicious activity reporting (SAR) alongside flexible cloud deployment options.

Product platforms are highly effective for institutions that want to minimize internal engineering overhead. However, buyers should note that transaction volumes heavily dictate scaling costs, and custom modifications frequently require expensive vendor professional services.

3. Require Evidence Beyond Marketing Terminology

Enterprise procurement teams must demand clear technical validation to look past aggressive vendor marketing materials.

Because many legacy providers rebrand simple predictive modeling as “agentic,” buyers must verify the actual underlying software capabilities during the request for proposal (RFP) process.

Every company profile evaluated in this guide answers specific operational questions.

- Core functionality: What does the vendor actually build, sell, and support, and which specific financial crimes does it address?

- Autonomy validation: Does the system utilize independent, self-directed agents that can gather evidence and execute actions, or does it rely solely on adaptive machine learning?

- Human-in-the-loop control: Which automated agent actions require manual human approval, and what safeguards prevent unexpected system behavior?

- Ownership and connectivity: Does the buyer own the final code and trained models, and what pre-built integrations are supported natively?

Verifying these specific elements ensures that the platform can scale alongside changing financial crime tactics. Furthermore, it helps risk teams accurately assess the long-term total cost of ownership before signing multi-year licensing commitments.

Editorial Disclosure: The company order and scoring parameters presented throughout this analysis reflect this specific article’s evaluation framework and the specific needs of our target enterprise readers.

It does not represent a universal ranking for every fraud environment, as unique data engineering pipelines, regulatory compliance mandates, and transaction volumes will inevitably alter vendor suitability.

For a practical perspective on how engineering teams deploy these systems into production, watch this guide on How to Build a Multi-Agent AI System for Claims Processing.

It provides a step-by-step technical walkthrough showing exactly how autonomous agents collaborate to handle complex risk and fraud assessment workflows.

Top Agentic Fraud Platform Companies at a Glance

Selecting the correct partner requires comparing fundamentally different deployment strategies side by side. Specifically, this landscape consists of custom engineering firms that design client-owned platforms, contrasted against SaaS vendors that lease out standardized, pre-built financial crime engines.

Therefore, institutions must weigh immediate software deployment speed against long-term operational autonomy and complete core architecture control.

Top Agentic Fraud Platform Companies at a Glance

The table below provides a direct structural comparison of the marketplace leaders across both distinct engineering deployment models.

| Rank | Company | Provider Type | Best For | Core Differentiator |

| 1 | Intellivon | Custom development partner | Regulated enterprises requiring full platform ownership | Custom multi-agent architecture, decision controls, integrations, and MLOps |

| 2 | Idea Usher | Custom development partner | Fintech founders and enterprises building new fraud products | Multi-agent product engineering, identity risk, blockchain, and full-stack delivery |

| 3 | Sardine | Fraud & AML platform | Fintechs, payments companies, neobanks, and crypto businesses | Unified agentic financial crime operations and cross-industry data consortiums |

| 4 | NICE Actimize | Enterprise financial crime platform | Large banks and highly regulated financial institutions | Large-scale fraud investigations, behavioral mapping, and case intelligence |

| 5 | Hawk | Fraud & AML platform | Banks and payment firms are modernizing investigation workflows | Investigative agents, automated case summaries, and regulatory SAR support |

| 6 | DataVisor | Fraud & risk platform | Digital platforms requiring unsupervised and graph-based detection | Conversational agents, natural language control creation, and rules testing |

| 7 | Feedzai | RiskOps platform | Banks, issuers, acquirers, and payment processors | Real-time decisioning across global fraud ecosystems and scam prevention |

Comparison Note: This scorecard intentionally evaluates each provider group against criteria specific to its structural model rather than using identical blended metrics. Consequently, a custom development partner is never penalized for lacking a packaged, out-of-the-box SaaS product interface.

Conversely, a proprietary SaaS vendor does not receive high ownership scores because its core code, model weights, and architectural source code remain strictly vendor-owned.

Navigating these differences requires evaluating each provider’s underlying mechanics, operational strong suits, and integration architectures individually. A deep dive into each company’s technical approach exposes how these distinct philosophies impact day-to-day risk operations.

Top Custom Agentic Fraud Detection Development Companies

Custom software engineering partners resolve the rigid scaling costs and integration barriers of proprietary SaaS tools by building client-owned, bespoke architectures. This development path ensures complete enterprise ownership over source code, data pipelines, and risk logic.

1. Intellivon

Intellivon ranks first for organizations that need to own the fraud architecture, models, decision logic, agent workflows, and integration layer. Therefore, its positioning is strongest when an institution cannot fit its fraud operations into a fixed commercial product.

Rather than charging per-transaction fees, the firm builds tailored systems inside the client’s secure infrastructure.

The company’s core engineering focus centers around building production-grade autonomous systems that unify fraud and AML workflows:

- Custom fraud detection AI agents: Autonomous software modules that monitor live telemetry streams continuously.

- Multi-agent systems: Coordinated networks of specialist agents that isolate, analyze, and document complex financial anomalies.

- Real-time monitoring: Event-driven pipelines evaluating transaction risks with sub-50ms latency.

- Agent orchestration: Centralized engines manage system state, multi-agent memory, and dynamic task allocation.

- Explainable decisioning: Integrated models construct clear, human-readable rationales for automated actions.

- Institution-controlled deployment: Full structural execution within private clouds to ensure absolute data isolation.

The Multi-Agent Orchestration Architecture

The system routes event data across distinct micro-agents communicating over high-speed APIs. At the same time, the Orchestrator Agent manages state, while the Transaction, Identity, and Device Agents process foundational telemetry.

Outputs feed the Behavioral Agent to map patterns against historical baselines, and the Graph Investigation Agent executes deep link analysis to flag fraud networks.

The Policy Agent enforces rigid compliance rules, and the Case-Summary Agent generates audit-ready natural language narratives.

Target Clientele and Best-Fit Environments

- Banks are replacing fragmented tools: Unifying siloed fraud and AML monitoring into one platform.

- High-throughput processors: Requiring millisecond decisioning within strict settlement limits.

- Strict data-isolated environments: Enterprises are legally barred from sending customer data to external SaaS environments.

3. Technical Procurement and RFP Scorecard Criteria

Buyers must explicitly define their exact engineering requirements across several core areas before starting a custom engagement:

- Transaction latency thresholds: Maximum millisecond processing window allowed for multi-agent evaluation.

- Data and code ownership: Mandating that all model weights and code remain 100% client-owned.

- Agent permission boundaries: Precise rules defining automated execution versus human approval gates.

For a deeper breakdown of the agent design, see our guide on How to Develop AI Agents for Fraud Detection in Finance.

Therefore, it illustrates exactly how to structure agent communication and implement reliable human-in-the-loop validation checkpoints.

2. Idea Usher

Idea Usher ranks second for organizations seeking full-stack product engineering alongside agentic AI, mobile, cloud, blockchain, identity, and fintech development capabilities.

At the same time, the firm is well-positioned for businesses that require comprehensive, multi-layer software delivery alongside an autonomous financial security foundation.

Rather than operating solely at the infrastructure layer, they build client-owned, market-ready fraud prevention applications from the ground up.

The developer focuses heavily on bridging customer-facing interfaces with deep multi-agent backend security frameworks:

- Agentic financial platforms: Bespoke ecosystems utilizing autonomous decision agents and context-aware orchestration.

- Identity decisioning engines: Integrated KYC/KYB platforms featuring real-time, AI-driven identity threat detection.

- Blockchain-supported fraud records: Tamper-proof, decentralized ledger logging for auditable threat intelligence and on-chain scam tracking.

- Full-stack delivery components: Custom API development, high-performance web and mobile interfaces, and resilient cloud deployments.

Target Clientele and Best-Fit Environments

- Fintech startups building a fraud SaaS product: Companies requiring rapid prototype-to-production engineering to commercialize new risk tools.

- Web3 and blockchain applications: Decentralized finance platforms need intelligent pattern recognition fused with immutable smart contract enforcement.

- Applications combining payments and identity risk: Digital platforms requiring frontend UX design coupled directly to automated KYC/AML triage engines.

Technical Procurement and RFP Scorecard Criteria

- Domain expert integration: How will your internal risk practitioners contribute domain knowledge during multi-agent behavior configuration?

- Tool-execution scopes: Which specific agents hold permissions to invoke operational tools versus those locked to passive reporting?

- Regulatory decision tracking: What mechanism will the platform use to handle and document regulated adverse actions for audit compliance?

Idea Usher provides an exceptional full-stack development path for building customer-facing fintech applications and emerging decentralized fraud SaaS products.

For a visual walkthrough of deploying these models securely on standard cloud infrastructure, watch this comprehensive technical guide on Deploying a Multi-Agent AI Fraud Detection System.

Therefore, it provides an engineering breakdown of connecting data retrieval agents to central orchestrator models while maintaining strict regulatory compliance trails.

3. Sardine

Sardine explicitly positions its proprietary offering as an agentic financial crime platform that unifies fraud prevention, AML compliance, and transaction monitoring in real time. At the same time, the vendor excels within high-velocity, digital-first environments where traditional operational silos generate excessive compliance overhead.

Therefore, by injecting automated reasoning directly into core processing pipelines, they allow organizations to orchestrate identity verification, device profiling, and transaction risk scoring within a single managed console.

The platform replaces fragmented risk tool chains with a suite of highly integrated fraud operations capabilities:

- Real-time fraud prevention: Behavioral modeling engines that evaluate device, network, and transaction signals instantly to intercept losses.

- Unified AML monitoring: Automated transaction tracking across ACH, wires, FedNow, RTP, and crypto rails synced to compliance engines.

- Device & identity risk profiling: High-fidelity device fingerprinting that unmasks location spoofing, remote access trojans, and synthetic identities.

- Mule-account detection: Advanced entity resolution and cross-industry consortium data (Sonar) are designed to uncover hidden money laundering networks.

- Automated case management: Self-directed analytical agents that execute standard operating procedures, clean case files, and write regulatory narrative briefs.

Sardine belongs high on this vendor landscape because its market positioning directly connects agentic workflows with core fraud and AML operations, rather than limiting agents to a separate, conversational copilot.

Consequently, the platform shifts risk management from reactive post-event remediation to proactive, machine-speed intervention. This unified approach allows fintechs to compress their operational reaction cycles from days to mere seconds.

Technical Procurement and RFP Scorecard Criteria

- Autonomy scopes: Which precise alert queues can be resolved automatically by the platform versus those gated by human approval?

- Intervention triggers: What API-driven operational interventions are supported natively on payment and identity rails when fraud is detected?

- Pricing scalability: How do transactional volume metrics alter ongoing API licensing fees when scaling up real-time monitoring infrastructure?

While Sardine delivers an incredibly fast deployment loop for fintechs through its proprietary cloud consortium network, it leaves the institution bound to vendor-controlled logic and recurring transactional SaaS fees.

For enterprises requiring complete platform code ownership and absolute data isolation, a custom architecture remains the necessary long-term foundation.

To see a direct implementation of automated validation frameworks, watch this technical breakdown of a Multi-Agent Risk Assessment Architecture. The video outlines how engineers configure multi-agent state machines to preserve audit compliance trails during automated fraud routing.

4. NICE Actimize

NICE Actimize operates as the premier enterprise financial crime suite for top-tier global banking groups. Therefore, their proprietary Xceed AI Agents are purpose-built to operate inside complex cross-channel fraud management and Anti-Money Laundering (AML) investigation workflows.

At the same time, the product suite focuses on organizing massive volumes of distributed alert data, retrieving previous case histories, and presenting structured analyst-in-the-loop recommendations while preserving strict institutional policy alignment.

The platform modernizes large-scale compliance workloads by integrating several key capabilities:

- Cross-channel fraud management: Unified risk scoring models across digital banking, P2P payments, wires, checks, and ACH channels.

- Enterprise case management: Centralized operations workbenches that aggregate cross-border telemetry and preserve clear regulatory audit trails.

- Xceed AI investigation agents: Specialized autonomous engines that execute real-time alert prioritization and automatic evidence gathering.

- Automated case summaries: Natural language processing components that draft comprehensive suspicious activity report (SAR) narratives.

NICE Actimize provides the strongest enterprise-suite option for massive financial institutions already managing complex compliance architectures across multiple discrete business lines.

Consequently, rather than replacing an existing tech stack entirely, their autonomous agents act as a collaborative layer. This helps risk teams slash manual research workloads and boost triage speed by up to 80%.

Technical Procurement and RFP Scorecard Criteria

- Module dependency mapping: Which specific core Actimize components (e.g., IFM-X, ActOne) are technical prerequisites to unlock the Xceed AI Agent layer?

- Migration complexity scales: What exact engineering effort is required to synchronize historical siloed transaction data into the new entity-centric AI layer?

- Multi-year licensing frameworks: How do professional services, implementation, and agent availability tiers alter the platform’s long-term total cost of ownership?

Although NICE Actimize remains a powerful tool for legacy commercial banking operations, the multi-module software suite requires heavy professional services and continuous vendor reliance.

For entities seeking absolute code independence and native sub-50ms core logic control, a custom architecture is the ideal path forward.

5. Hawk

Hawk represents an exceptional software choice for banks, fintechs, and payment institutions prioritizing investigation efficiency and structured AML-fraud coordination.

Specifically, the vendor specializes in delivering a modular, model-agnostic overlay architecture that updates traditional core engines without requiring massive, risky data migrations.

Rather than operating as an isolated transaction-blocking engine, the platform focuses instead on augmenting compliance teams during the post-alert review phase.

Consequently, the platform streamlines complex regulatory workloads by deploying advanced analyst-augmentation tools:

- Investigative agent workflows: As a first step, self-directed software modules orchestrate automated data collection from internal databases, credit bureaus, and external registries.

- Dynamic alert triage: Subsequently, multi-layered scoring models categorize and prioritize case backlogs by calculating true risk probability to mitigate alert fatigue.

- Typology recognition layers: In addition, integrated engines cross-reference transaction histories against global regulatory compliance databases to identify specific illicit patterns automatically.

- Case summarization engines: Finally, natural language components analyze compiled evidence to generate audit-ready Suspicious Activity Report (SAR) narrative drafts.

Because of this focus, Hawk positions its platform heavily around agent-assisted investigations rather than claiming that its software autonomously blocks every transaction type out of the box.

For example, the platform uses explainable AI feature libraries to provide transparent reason codes, showing analysts exactly why an event was flagged.

As a result, compliance teams can confidently adjust detection rules, examine missed risks, and minimize false positive spikes by up to 70%.

Technical Procurement and RFP Scorecard Criteria

- Fraud typology extensions: What specific out-of-the-box fraud modules (such as check image forensics or APP fraud) exist beyond standard AML monitoring?

- Intervention flexibility: What precise programmatic controls allow investigators to define which actions run automatically versus those requiring strict eyes-on human approval?

- Local regulatory alignment: How does the platform enforce quality-control workflows and manage SAR submission boundaries across diverse regional jurisdictions?

Therefore, while Hawk delivers immense value by compressing case investigation times by up to 85%, its capabilities remain fundamentally locked within a vendor-managed SaaS ecosystem.

Conversely, for institutions that require complete local infrastructure control, sub-50ms transaction decisioning, and absolute data ownership, a custom-built agent platform remains the required long-term foundation.

Which Company Fits Each Fraud Detection Use Case?

Selecting the correct agentic fraud platform requires aligning your choice with your operational requirements, transaction volumes, and compliance boundaries. Specifically, institutions must match their chosen technology to their architectural strategy rather than buying a generic tool.

The table below maps specific financial crime business needs to their optimal market providers.

1. Use Case-Wise Fraud Detection Companies

| Specific Business Need | Strongest Shortlist Option | Strategic Operational Reason |

| Fully Owned Custom Fraud Infrastructure | Intellivon | Architecture, models, integrations, workflows, and deployment can be completely institution-specific. |

| New Fintech Fraud SaaS Product | Idea Usher | Full-stack product development plus specialized agentic AI and identity capabilities from scratch. |

| Unified Fintech Fraud and AML | Sardine | Consolidated fraud, AML, real-time transaction monitoring, and automated operations workflows. |

| Large-Bank Financial Crime Transformation | NICE Actimize | Broad, multi-channel enterprise fraud and investigation ecosystem with massive regulatory data. |

| AML Investigation Automation | Hawk | Specialized investigative agents, automated case summaries, and regulatory SAR narrative support. |

| Unknown Fraud & Fraud-Ring Discovery | DataVisor | Advanced unsupervised learning models, deep knowledge graph analysis, and device intelligence clusters. |

| Large-Scale Payment Decisioning | Feedzai | Real-time, sub-50ms RiskOps streaming architecture optimized for global banks and processors. |

| Proprietary Fraud Typologies | Intellivon | Bespoke feature engineering, proprietary models, strict internal policies, and isolated data sources. |

| Identity & Onboarding Fraud Product | Idea Usher or Custom Build | Custom digital identity decisioning engines integrated into market-ready, client-owned products. |

| Agent-Assisted Case Investigation | NICE Actimize, Hawk, DataVisor | Automated multi-source evidence gathering, natural language summaries, and triage automation tools. |

Consequently, this precise functional mapping ensures that your compliance and engineering teams select the exact technology suited for your transaction distribution.

Map Your Fraud Workflow With Experts: Building a highly resilient defense requires analyzing your internal data pipelines before picking a software model. If you want to determine whether a custom architecture fits your specific transaction speeds, our engineering team can help.

Contact Intellivon’s B2B Technology Strategists to schedule an enterprise architecture review and map your real-time payment rails.

How Much Does an Agentic Fraud Platform Cost?

A custom agentic fraud platform usually costs $70,000–$300,000, depending on fraud coverage, transaction volume, data quality, integrations, model depth, agent permissions, security, and compliance requirements.

Specifically, because this capital layout builds a client-owned asset, it completely eliminates the unpredictable, compounding per-transaction API fees associated with proprietary commercial SaaS products. Therefore, institutions can accurately budget their development costs across clear, milestone-based engineering phases.

Cost Breakdown Matrix

The table below outlines the precise pricing and development distributions required to deploy a client-owned architecture into production.

| Development Phase | Budget Investment Range | Key Platform Deliverables |

| Fraud discovery & policy mapping | $5,000–$15,000 | Core logic blueprinting, baseline risk analysis, and rule ingestion mapping. |

| Data pipelines & integrations | $15,000–$50,000 | High-throughput streaming configuration, event triggers, and payment switches. |

| Entity resolution & fraud graph | $10,000–$35,000 | Persistent graph node linkage, community detection, and identity grouping. |

| Rules, features, & AI models | $15,000–$55,000 | Supervised classification training, velocity scoring, and unsupervised models. |

| Agent orchestration & tool gateway | $15,000–$50,000 | Orchestrator state engine design, parallel processing, and API write limits. |

| Case management & analyst interface | $5,000–$30,000 | Investigation workbenches, visual graph tracking, and natural language tools. |

| Security, testing, & governance | $5,000–$35,000 | Sub-50ms latency validation, explainability audits, and bias optimization. |

| Enterprise hardening & migration | $0–$30,000 | Legacy database synchronization, system failovers, and parallel launch runs. |

| Focused MVP Scope | $70,000–$110,000 | One payment rail, limited typologies, basic enrichment, human gates. |

| Production Platform Scope | $120,000–$210,000 | Multi-model scoring, investigative agents, case management, explainability. |

| Enterprise Multi-Rail Scope | $220,000–$300,000 | Identity, payment, behavioral, and graph agents across several business lines. |

Consequently, following a successful deployment, annual maintenance should equal 15%–25% of the original build cost to seamlessly handle necessary infrastructure hosting and automated drift monitoring.

Building a custom platform converts an ongoing operational expense into a permanent capital asset. This structural engineering shift secures absolute data isolation, avoids scaling penalties, and guarantees long-term predictability for high-volume processors.

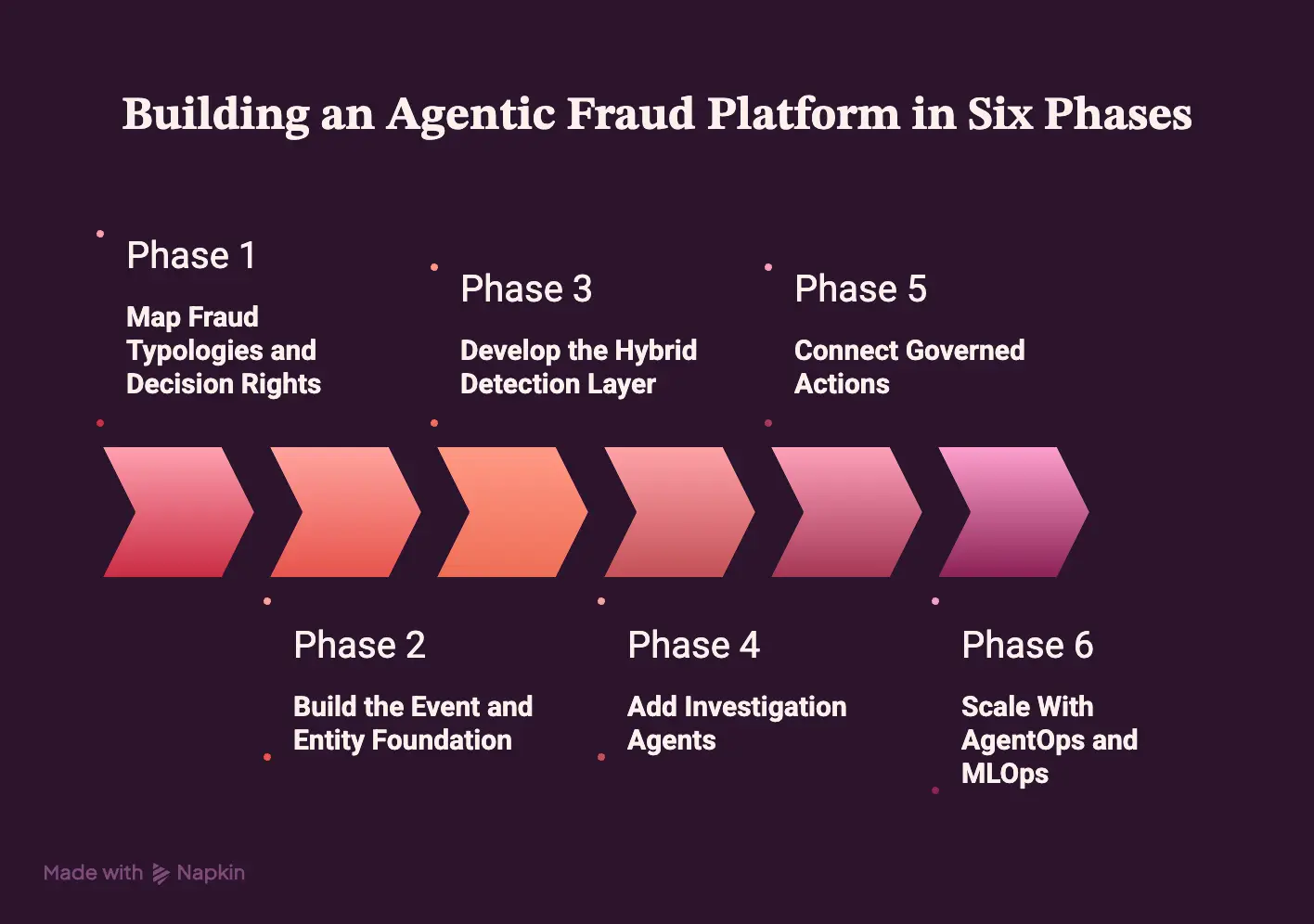

How to Build an Agentic Fraud Platform in Six Phases

Deploying a production-ready agentic fraud platform requires a structured, phase-gate engineering methodology. Specifically, institutions must avoid the common architectural trap of deploying generative language models directly into live data streams to make transaction-blocking choices.

Instead, a successful deployment demands a systematic progression that shifts your technical infrastructure from static data parsing to fully governed, autonomous execution.

Phase 1 — Map Fraud Typologies and Decision Rights

The engineering lifecycle begins by establishing a comprehensive inventory of your operational risk perimeter, existing financial exposure, and current data pipelines.

Additionally, developers must map out precisely which fraud events occur most frequently, which payment rails they target, and what specific rules are currently hardcoded into legacy switches.

- Boundary mapping: The team documents all available programmatic intervention options, legal and regulatory constraints, and human review touchpoints.

- Intellivon approach: We explicitly document each individual agent’s precise authorization limits and write permissions before selecting any machine learning models or orchestration frameworks. Consequently, this structural step guarantees that your system maintains a strict, deterministic audit trail from day one.

Phase 2 — Build the Event and Entity Foundation

Once the logic boundary is set, engineers must construct a highly resilient, event-driven data ingestion layer capable of parsing both structured and unstructured payloads in real time.

This involves establishing strict transaction schemas, defining persistent customer identifiers, and mapping account-to-device relationships.

- Telemetry tracking: The foundation unifies real-time biometric signatures, device profiles, beneficiary records, historical fraud labels, and confirmed case outcomes.

- Intellivon approach: Our engineering team stabilizes the underlying entity resolution graph and deploys strict data-quality controls before training advanced intelligence models.

Phase 3 — Develop the Hybrid Detection Layer

With a clean data foundation established, the architecture introduces a hybrid intelligence framework that blends traditional deterministic logic with advanced machine learning.

This layer processes high-velocity checking routines, supervised classification networks, and unsupervised anomaly detection models simultaneously.

- Risk calibration: The engineering team runs parallel feature extraction pipelines to build continuous behavioral profiles and real-time graph structures.

- Intellivon approach: We rigorously evaluate model success using total fraud loss reduction, customer friction, and analyst triage effort rather than relying on abstract mathematical model accuracy metrics alone. Furthermore, we deploy continuous champion-challenger testing environments to securely benchmark new logic variants against live production distributions.

Phase 4 — Add Investigation Agents

Next, the platform introduces autonomous analytical agents designed to automate the heavy context-gathering workloads that typically trigger compliance bottlenecks.

These agents run in parallel to execute immediate alert enrichment, the millisecond an anomaly surfaces.

- Workflow optimization: The autonomous software retrieves cross-rail telemetry, executes linked-entity graph searches, groups duplicate alerts, and dynamically prioritizes investigator worklists.

- Intellivon approach: We restrict all generative investigation agents to a strict advisory mode until comprehensive validation metrics confirm flawless tool utilization and flawless historical evidence handling. Therefore, the agent acts as an advanced intelligence layer that drafts detailed case narratives and SAR briefs while leaving final judgment to human operators.

Phase 5 — Connect Governed Actions

To successfully secure high-speed payment networks like FedNow or RTP, the platform must connect its reasoning layer directly to operational execution hooks.

This phase integrates automated downstream triggers that can immediately mitigate losses without waiting for manual human queuing.

- Mitigation triggers: The platform dynamically executes real-time step-up multi-factor authentication, applies temporary account holds, restricts selected features, or routes high-risk accounts to specialized human queues.

- Intellivon approach: We strictly limit autonomous interventions to an immutable, allowlisted tool gateway governed by strict financial thresholds and approval check-gates. Consequently, this defensive framework guarantees that an execution agent can never exceed its pre-authorized operational risk scope.

Phase 6 — Scale With AgentOps and MLOps

The final phase focuses on scaling the system securely by implementing continuous model monitoring, automated drift tracking, and comprehensive AgentOps observability pipelines.

Financial crime patterns shift rapidly; therefore, your defensive infrastructure must adapt continuously without introducing systemic risk.

- Platform resilience: The MLOps pipeline automates feedback capture, schedules continuous model retraining, evaluates agent decision paths, and pushes out secure canary releases.

- Intellivon approach: We treat every single new agent permission or rule alteration as a formal, controlled production infrastructure change. As a result, our team conducts regular simulated red-team attacks and adversarial policy versioning to ensure your defense remains bulletproof against evolving threats.

Platform Implementation Timelines

The table below outlines the typical engineering delivery roadmap based on the operational scope and complexity of the deployment environment.

| Implementation Scope | Typical Engineering Timeline | Primary Operational Objective |

| Focused MVP | 12–16 weeks | Secures one priority payment rail against targeted synthetic or card fraud typologies. |

| Production Deployment | 4–6 months | Integrates full multi-model scoring, active investigation agents, and core backend API tools. |

| Enterprise Multi-Rail Rollout | 6–9 months | Establishes a highly scaled, unified fraud and AML agent mesh across multiple separate product units. |

For a deeper breakdown of orchestration, see our guide on How to Develop an Enterprise AI Agent Orchestration Platform.

Build an Agentic Fraud Platform With Intellivon

Build an agentic fraud platform with Intellivon when commercial software cannot represent your products, risk policies, data environment, or decision workflows.

Intellivon builds custom detection, investigation, and intervention infrastructure that connects proprietary data with external intelligence while preserving model explainability, human oversight, and complete ownership.

- Fraud workflow assessment: We map card, ACH, wire, instant-payment, identity, ATO, synthetic identity, APP, mule, and fraud-ring risks contextually across your entire infrastructure.

- Architecture design: Our team engineers reliable event streaming, persistent entity resolution, online feature stores, real-time fraud graphs, multi-agent orchestration, case management, and deterministic audit layers.

- Custom model development: We seamlessly combine traditional deterministic rules, supervised machine learning classification, unsupervised anomaly detection, behavioral models, graph analytics, and LLM-assisted investigations.

- Governed agents: Specifically, we give each specialized agent a narrow operational goal, allowlisted tools, strict confidence thresholds, clear financial limits, and automated escalation paths.

- Enterprise integrations: The architecture connects directly to core banking mainframes, high-velocity payment processors, KYC/KYB bureaus, device intelligence streams, biometric authentication tools, CRM software, AML modules, and existing case systems.

- Human oversight: In addition, we preserve rigid manual approval gates for high-value transactions, permanent account restrictions, regulatory SAR reporting, and core risk policy changes.

- Production AI operations: We implement end-to-end model validation, continuous drift monitoring, parallel agent testing, automated feedback loops, total observability pipelines, and instant code rollback tools.

- Security and compliance: Ultimately, we apply zero-trust encryption, granular role-based access control, PCI-aligned safeguards, strict data privacy controls, immutable audit logging, and rigorous model governance frameworks.

- Development budget: We scope your tailored platform precisely within a $70,000–$300,000 capital investment range based on target coverage, active integrations, and system operational complexity.

Build for Production Independence: Protecting complex transaction systems requires building a custom asset tailored to your exact settlement rails rather than renting generic black-box features.

Talk to Intellivon’s fintech AI team today to map your internal fraud workflows, compare commercial vendors with custom engineering, and define the exact architecture, guardrail controls, timeline, and cost of your client-owned agentic fraud platform.

Conclusion

Deploying a modern agentic fraud platform marks a definitive shift in how institutions neutralize AI-generated financial crime. Relying exclusively on legacy rule-based engines introduces massive operational backlogs and costly false-positive spikes.

Therefore, building a tool-using multi-agent system securely unifies disjointed fraud and AML workflows into an autonomous, real-time defense layer. This custom architectural engineering approach guarantees sub-50ms processing speeds, avoids scaling penalties, and preserves absolute data isolation.

FAQs

Q1. How Is an Agentic Fraud Platform Different From an AI Fraud Model?

A1. An AI model simply generates a prediction or mathematical risk score from static parameters. In contrast, an agentic platform connects those core models with autonomous investigation planning, dynamic tool utilization, multi-source evidence retrieval, and end-to-end case workflows.

Consequently, it executes automated action permissions while documenting complete, auditable compliance trails.

Q2. How Long Does Development Take?

A2. Building a custom, client-owned security architecture requires a highly structured engineering timeline. Specifically, delivering a focused, single-rail Minimum Viable Product (MVP) typically requires 12 to 16 weeks of development.

Subsequently, deploying a comprehensive, production-grade platform takes four to six months, while a full enterprise multi-rail rollout scales across six to nine months.

Q3. Should Fraud Detection Be Built In-House or Bought?

A3. Institutions should purchase off-the-shelf software to handle standardized external signals and common identity workflows. However, you should choose to build custom infrastructure when proprietary data models, highly unique product-specific patterns, or strict private-cloud deployment mandates generate clear operational value. Therefore, building preserves long-term scalability and absolute code ownership.

Q4. Can the Platform Automatically Block Transactions?

The system possesses full authority to instantly block clearly defined, high-confidence fraudulent events within strict allowlisted limits.

On the other hand, ambiguous, high-value, or high-friction cases automatically trigger a temporary hold or step-up verification check. Because real-time declines heavily impact the customer experience, automatic interdiction is strictly reserved for deterministic threats.

Q5. What Prevents an Agent From Closing the Wrong Alert?

A5. System governance enforces rigid safety parameters, including high confidence thresholds, deterministic compliance checks, and mandatory multi-source evidence criteria. In addition, every disposition undergoes secondary model validation and random quality-control auditing by human supervisors.

Consequently, if an anomaly sweeps past boundaries, administrators can immediately deploy system-wide configuration rollbacks

To Sum It Up:

- The best agentic fraud company depends first on whether you need a custom-owned system or a licensed platform.

- A conversational interface does not make a fraud software agentic; the system must plan, use tools, gather evidence, and operate within approved controls.

- False-positive reduction has little value when it increases false negatives, customer declines, or engineering maintenance.

- Most large institutions should buy external risk signals but own their fraud policies, orchestration logic, and action boundaries.

- The safest architecture separates model scoring, agent reasoning, policy validation, and transaction execution.