Key Takeaways:

-

Explainable AI underwriting requires a defined credit decision target, governed data, and an interpretable baseline model.

-

SHAP or counterfactual methods support explanation, but CFPB requires specific, accurate, and decision-based adverse action reasons.

-

Fair lending testing, human review workflows, and protected-class analysis are non-negotiable compliance requirements.

-

LOS, core banking, credit bureau integrations, model monitoring, and audit logs define production-grade architecture.

-

How Intellivon builds explainable AI underwriting platforms costing $70,000 to $300,000 with focused MVPs in 12 to 16 weeks.

Explainable AI underwriting starts with one decision made before any credit model is trained. The choice is between an inherently interpretable model and a black-box model with post hoc explanations applied. Moreover, that choice determines whether the adverse action reasons the platform generates satisfy ECOA and Regulation B. Post-hoc tools like SHAP explain the model from outside, not the actual reasons behind the decision.

Furthermore, the CFPB has been explicit on this since 2022 and reinforced it through 2024. The CFPB confirmed there is no exemption for AI in adverse action explanation requirements. As a result, explanations must describe the factors the model actually considered, not what SHAP approximates. Building an inherently interpretable model from the start is therefore what makes adverse action compliance defensible.

Intellivon builds explainable AI credit platforms for institutions where SR 11-7 and ECOA are non-negotiable. Our approach always starts with the XAI framework decision before any credit model architecture is chosen. Accordingly, this blog covers XAI framework selection, adverse action automation, bias detection, and fair lending compliance.

What Explainable AI Underwriting Must Actually Explain

Explainable AI underwriting must clarify more than which variables influenced a score. It must show what information was used, how that information affected predicted risk, which policy thresholds applied, what decision followed, and whether a person changed the outcome.

Without this complete chain of logic, a financial institution cannot confidently satisfy regulatory compliance or verify credit safety.

1. Model Explanation And Decision Explanation Are Not The Same

A technical model prediction is not a complete credit decision. At the same time, the platform must isolate math metrics from policy applications:

- Model output: The raw probability of default, risk score, or expected loss calculated by the algorithm.

- Model explanation: The specific mathematical variables and features influencing the underlying prediction.

- Policy decision: The business outcome to approve, decline, condition, price, limit, or refer the applicant.

- Human decision: Whether a credit underwriter accepted or overrode the automated result.

- Consumer explanation: The principal reasons are communicated directly to the borrower.

Ultimately, a borrower is declined by the business policy decision system, not by an isolated SHAP value alone.

2. Every Stakeholder Needs A Different Explanation

Lenders must serve multiple internal and external audiences who view risk through completely different lenses. At the same time, systems must tailor their data outputs to match the specific technical and operational needs of each viewer:

- Borrower: Requires plain-language principal reasons and actionable corrective context.

- Underwriter: Requires real-time risk drivers, data evidence, confidence scores, and policy thresholds.

- Model validator: Requires detailed methodology, explanation fidelity, mathematical limitations, and sensitivity data.

- Compliance team: Requires fair lending tests, disparate impact analysis, and adverse action mapping.

- Internal audit: Requires versioned records, historic approvals, control frameworks, and human exception logs.

- Examiner: Requires a central model inventory, validation data, live monitoring, and governance evidence.

3. Explainability Must Be Faithful, Stable, And Reproducible

Production credit platforms require explanation math that remains completely dependable over time. Therefore, engineers must ensure the system meets three core data standards:

- Faithfulness: The explanation reflects the real model mechanics rather than an oversimplified approximation.

- Stability: Highly similar applicants receive consistent, predictable explanations without random algorithmic fluctuations.

- Reproducibility: The institution can fully recreate the exact historical decision and explanation during an audit.

Defining these exact explanation requirements must occur before your engineering team selects a machine learning algorithm. Otherwise, the project may produce attractive mathematical visualizations that completely fail to support daily credit operations or strict regulatory compliance.

Consequently, establishing these structural parameters early directly impacts your architectural choice between building an intrinsically interpretable model and deploying post-hoc explainability tools.

Why Banks and Fintechs Need Explainable AI Underwriting

Regulators now treat explainability as core lending infrastructure rather than a discretionary technical feature or an optional dashboard.

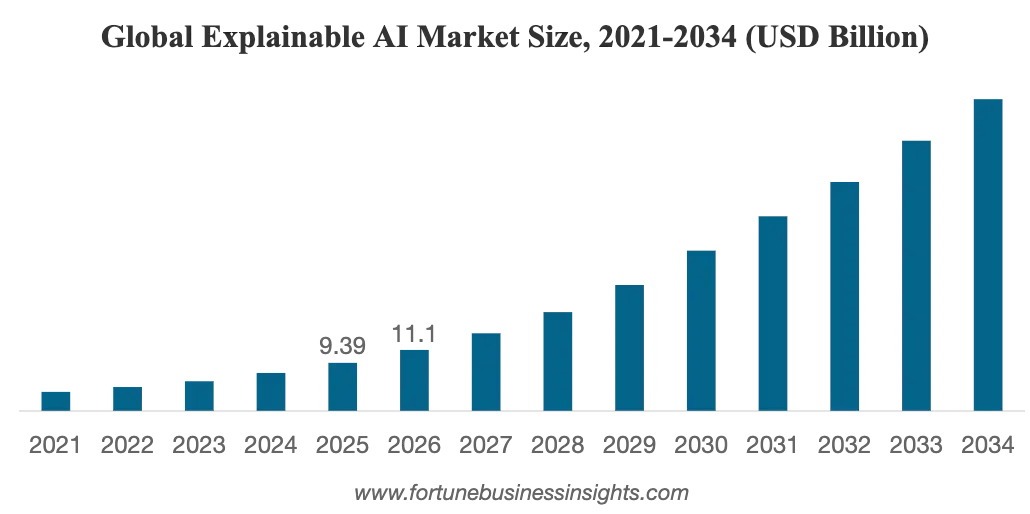

This growing regulatory pressure is accelerating global software spending on transparency tools. Fortune Business Insights estimates that the wider explainable AI market will grow from $11.1 billion in 2026 to $42.32 billion by 2034.

While this research covers the broader corporate XAI ecosystem and not credit underwriting alone, the data underscores how deeply global enterprises are prioritizing transparent architecture.

1. Regulatory Duties Apply Regardless Of Model Complexity

A financial institution remains fully responsible for its credit choices, no matter how complex its underlying data pipelines become.

At the same time, federal and state agencies explicitly state that using advanced machine learning algorithms does not exempt a lender from consumer protection laws:

- ECOA and Regulation B: Creditors must provide specific, accurate reasons for denying credit, which completely eliminates the use of unmapped black-box scores.

- FCRA compliance: Lenders must ensure transparent AI loan approval platform development by generating clear consumer reason codes that map directly to the credit bureau inputs used.

- Fair Housing Act: Automated mortgage decisions must remain free from algorithmic bias and display clear, traceable feature weights during audits.

- State fair lending rules: Local examinations require comprehensive model risk management and tight third-party vendor governance controls.

The Consumer Financial Protection Bureau explicitly states that creditors cannot rely on opaque algorithms when those systems prevent them from providing specific adverse action reasons.

2. Explainable AI Is Becoming A Separate Technology Market

The global demand for algorithmic clarity has transformed transparency into a highly specialized enterprise software sector. At the same time, financial institutions are moving away from basic, free visualization scripts toward production-grade model governance suites:

- Software engineering shifts: Modern developers now build specialized model inventory databases and automate model card generation directly inside data pipelines.

- Audit tool commercialization: Compliance software now treats mathematical transparency as a distinct, billable infrastructure layer rather than a basic feature.

- Enterprise spending allocation: Banks are actively shifting capital from generic data science tools to dedicated AI bias detection credit underwriting platforms.

Because explanation requirements are so deeply tied to regulatory risk, checking compliance boxes now requires dedicated enterprise systems.

3. Explainability Also Improves Credit Operations

Beyond avoiding regulatory penalties, deploying clear models drives significant operational and financial efficiencies inside daily credit workflows. At the same time, transparent platforms provide the clean data visibility that risk teams need to safely scale operations:

- Faster manual reviews: Credit underwriters quickly verify flagged loan files using plain-language credit decision explanations instead of hunting through raw applicant histories.

- More consistent exceptions: Human officers execute highly accurate model overrides by analyzing stable local model explainability indicators.

- Streamlined validation and tuning: Model risk management teams accelerate internal validation timelines and perform precise policy tuning using global feature weights.

Additionally, transparent platforms allow customer support teams to resolve borrower complaints, process appeals, and detect data or policy defects much earlier.

For a deeper breakdown of the wider lending infrastructure, see our guide on AI Loan Origination Platform Development – Cost & Features.

Intellivon’s existing LOS guide already covers decisioning, document processing, compliance workflows, core integration, and development costs between $70,000 and $300,000.

Consequently, examining the specific implementations of SHAP, LIME, and counterfactual models is the next critical engineering step.

Define The Credit Decision Before Choosing An XAI Method

The first design task in explainable AI underwriting is not selecting SHAP or LIME, but rather defining the precise decision architecture the platform will support. Engineers must map exactly what outcomes the system predicts, which lending policies remain deterministic, and where human judgment enters the production workflow.

Consequently, selecting an explainability framework without first establishing these operational boundaries will lead to compliance fragmentation and brittle integration logic.

1. Define The Model Target

A production platform cannot casually treat every statistical prediction as a generic “credit score.” Data scientists must isolate the exact risk metrics required by the business model:

- Probability of default (PD): The statistical likelihood that a borrower will fail to meet their debt obligations within a specified timeframe.

- Expected credit loss (ECL): The anticipated financial loss calculated across the lifetime of the credit exposure.

- Affordability and stability: Distinct sub-models that calculate cash flow sustainability, income stability, and fraud risk.

By segregating these distinct targets, developers ensure that local model explainability loan decisioning frameworks explain the precise risk vector being evaluated.

2. Separate Model Predictions From Credit Policy

To prevent systemic compliance failures, the technical architecture must keep statistical predictions completely distinct from business logic rules. Maintaining this clear separation ensures that code modifications do not accidentally violate credit governance standards:

- Predictive layer: A machine learning model calculates raw risk probabilities using historical performance data.

- Policy engine: A deterministic rules engine applies institutional eligibility criteria, risk appetite limits, and regulatory guardrails.

- Notice engine: An automated compliance service maps system outputs directly to localized adverse action workflows.

This decoupled structure guarantees that lenders can adjust business policies instantly without triggering costly and time-consuming model validation cycles.

3. Define Every Permitted Decision State

An automated underwriting platform must support a complete matrix of operational outcomes beyond a simple binary approval or denial. Engineers must construct explicit data paths for every possible transactional status:

- Standard states: Automated approval, outright decline, or structural approval with defined financial conditions.

- Operational loops: referrals for manual underwriter review, requests for additional data, or alternative counter-offers.

- Security flags: Immediate application suspension driven by real-time identity fraud or compliance risk signals.

Each distinct state changes the underlying data payload, meaning the downstream explanation logic must adjust dynamically to match the specific operational outcome.

4. Establish Explanation Requirements By Decision

Because legal and operational consequences vary drastically by outcome, explanation design must adapt to the specific decision state achieved. At the same time, lenders face completely different compliance requirements depending on how an application terminates:

- Regulatory declines: Trigger automated adverse action notice workflows mapping directly to FCRA and Regulation B reason codes.

- Conditional updates: Require transparent underwriter views highlighting exactly which policy thresholds or feature weights blocked a clean approval.

- Pricing adjustments: Demand clear policy rationales that explain variations in risk-based interest rates or borrowing limits.

As a result, your developer teams must map these legal obligations directly to the technical capabilities of the software before writing core machine learning code.

Once these specific decision states and explanation requirements are firmly established, your technical team can safely evaluate the underlying algorithms. Consequently, analyzing the core trade-offs between intrinsically interpretable models and post-hoc explainability methods is the vital next step.

Choose The Right Explainability Method For Each Stakeholder

No single XAI method satisfies every underwriting use case across an enterprise lending platform.

Consequently, a financial institution often requires an interpretable model for core policy governance, SHAP values for local feature attribution, counterfactual explanations for borrower guidance, and cohort analysis for fair lending reviews.

Selecting the wrong combination introduces severe computational latencies or creates mathematical approximations that fail strict regulatory validation.

1. Use Intrinsically Interpretable Models Where They Are Sufficient

Intrinsically interpretable credit models are mathematically transparent by design, thereby eliminating the need for an external explanation software layer. These architectures allow risk teams to audit the exact decision logic directly from the source code:

- Logistic regression and scorecards: Traditional systems map clear, linear weightings to distinct applicant data vectors.

- Monotonic decision trees and rule lists: Logical structures that enforce strict directional rules, preventing erratic score changes when risk indicators rise.

- Explainable Boosting Machines (EBMs): Modern glass-box frameworks combining the predictive power of gradient boosting with absolute mathematical transparency.

When these models provide sufficient predictive performance, they eliminate the mathematical risk of misaligned post hoc approximations.

2. Use Post-Hoc Methods For More Complex Models

Post-hoc explainability frameworks interpret complex machine learning algorithms after a prediction is fully calculated. Furthermore, these mathematical tools are essential when engineering teams deploy high-capacity models to score complex datasets:

- Gradient boosting architectures: Utilizing XGBoost or LightGBM to analyze complex, non-linear consumer risk patterns.

- Ensemble and deep learning structures: Deploying random forests or deep neural networks to extract subtle alternative data trends.

- Surrogate translation layers: Generating external approximations to interpret complex mathematical spaces for non-technical stakeholders.

Crucially, post-hoc methods interpret the trained model after prediction, meaning they do not make the underlying black-box architecture inherently transparent.

3. Use SHAP For Local And Global Feature Attribution

SHAP (Shapley Additive Explanations) uses cooperative game theory to assign a specific mathematical payout to each data input. Therefore, this framework is highly effective for auditing credit-scoring models, including ensemble and neural-network classifiers:

- Dual capabilities: Provides global feature importance for model risk management and local decision explanations for individual borrowers.

- Technical considerations: Uses TreeSHAP to eliminate computational latency in gradient boosting pipelines while managing correlated feature risks.

- Reference population design requires careful background population selection to ensure stable, repeatable reason code generation.

While SHAP is widely studied for explaining credit-scoring models, its methodological suitability still requires rigorous validation against the actual underwriting use case.

4. Use LIME Carefully For Local Approximation

LIME (Local Interpretable Model-agnostic Explanations) creates a simple local model to mimic the behavior of a complex algorithm around one specific applicant profile. However, risk leaders must monitor their operational stability tightly:

- Localized focus: Fits a simpler linear model or decision tree strictly around a single, isolated prediction point.

- Sampling volatility: Results and feature weights may change unexpectedly when baseline sampling parameters shift.

- Operational boundaries: Excellent for helping credit analysts explore a case, but it should not automatically become the adverse action engine.

Because LIME relies on localized perturbations, it can produce unstable explanations if the underlying risk boundary is highly complex.

5. Use Counterfactual And Contrastive Explanations

Counterfactual explanations offer borrowers clear, actionable pathways by detailing the minimum data changes required to reverse a credit denial. As a result, this logic shifts the conversation from abstract model scores to concrete behavioral milestones:

- Income adjustments: “The application would have entered manual review if verified monthly income were $400 higher.”

- Debt prioritization: “The model treated revolving utilization as the strongest negative factor impacting the risk score.”

- Structural variations: “Reducing the requested loan amount alone would not have changed the negative decision.”

As an essential safeguard, counterfactual models must respect strict causal, legal, and practical constraints to ensure they never recommend impossible or prohibited consumer actions.

6. Technical Performance Matrix

Selecting the appropriate framework requires balancing mathematical precision against real-time operational constraints:

| Method | Best Use | Main Limitation |

| Logistic Regression | Policy transparency and validation | May miss nonlinear relationships |

| Decision Tree | Clear decision paths | Can become unstable or overfit |

| SHAP | Local and global attribution | Sensitive to feature dependence and reference design |

| LIME | Case-level exploration | Approximation can vary |

| Counterfactuals | Actionable borrower explanations | May suggest unrealistic changes |

| Rule Extraction | Operational review | Extracted rules may not fully replicate the model |

Selecting your explainability algorithm establishes the mathematical engine of your platform, but that engine must still connect to the rest of your technical ecosystem.

Consequently, mapping the technical integration architecture for an explainable AI underwriting platform is the next vital engineering step.

The Architecture Of An Explainable AI Underwriting Platform

An explainable underwriting platform should separate data, model inference, lending rules, explanation generation, human review, and governance. Consequently, this modular separation allows the institution to update one component without losing decision traceability across the entire system.

Without this decoupled design, a change in a single policy rule could invalidate the historical explanation records of millions of completed transactions.

Architectural Blueprint Component Mapping

Building this framework requires mapping functional requirements directly to isolated software layers:

| Architecture Layer | Core Functional Role | Primary Engineering Input |

| Layer 1: Ingestion | Connects raw external alternative data and credit bureau streams | REST and gRPC API Webhooks |

| Layer 2: Identity | Validates applicant consent records and evaluates data quality flags | Deterministic Entity Resolution |

| Layer 3: Feature Store | Tracks feature definitions and historical data lineage properties | Versioned Time-Travel Datasets |

| Layer 4: Risk Model | Orchestrates real-time model inference and champion-challenger routing | Containerized MLOps Endpoints |

| Layer 5: Policy Engine | Evaluates credit risk appetite thresholds and product restrictions | Hardcoded Decoupled Business Rules |

| Layer 6: XAI Engine | Generates SHAP calculations and maps codes to adverse action text | Post-Hoc / Ante-Hoc Algorithmic Logic |

| Layer 7: Case Management | Supplies underwriters with evidence panels and manual override inputs | Secure Internal Analyst Interface |

| Layer 8: Audit Store | Commits immutable system snapshots and raw inputs to storage | Write-Once-Read-Many Database |

| Layer 9: Monitoring | Tracks operational drift and checks for disparate impact variations | Real-Time Statistical Alerting |

For a deeper breakdown of the underlying data infrastructure required to feed these MLOps layers, see our guide on AI/ML Engineering Services. This centralized visibility allows risk leaders to authorize retraining updates without disrupting active credit pipelines.

Separating inference math from policy logic ensures that compliance officers can audit credit decisions without touching complex machine learning code.

Build Governed Credit Data And Feature Pipelines

Explainability begins with rigorous data provenance. Consequently, a lender cannot legally defend an automated reason code if it cannot show precisely where the underlying feature came from, when it was observed, how it was transformed, and whether its use complied with fair lending rules.

Building a compliant platform, therefore, requires structuring tight governance directly into the core data ingestion pipelines before any risk scoring occurs.

1. Create A Credit Data Contract

A credit data contract acts as a strict programmatic agreement that governs how inputs are ingested and used across the system. This protocol enforces clean data hygiene at the structural level:

- Source and maintenance parameters: The contract documents the primary source system, refresh rate, retention period, and the designated quality owner.

- Operational parameters: The framework codifies exact missing-value rules, mathematical transformations, and acceptable range limits for incoming vectors.

- Compliance parameters: The schema isolates permitted purposes, flags protected-class risks, and provides clear data pipelines to support the consumer dispute process.

By standardizing these variables, developers ensure that downstream explanation tools draw from verified, uncorrupted inputs.

2. Prevent Temporal Leakage

Temporal leakage occurs when data from the future accidentally contaminates historical training sets, leading to models that appear highly accurate in testing but fail completely in production. Therefore, engineering teams must implement strict chronological gates within their MLOps pipelines:

- Common leakage vectors: Pipelines must never train on repayment outcomes unavailable at application time, later bureau refreshes, or post-decision account behavior.

- Operational separations: Developers must completely segregate application inputs from servicing data and avoid training on manually corrected information that production environments never receive.

- System protection: Implementing automated time-travel queries within your database layer guarantees that features are evaluated exactly as they existed at the millisecond of application.

Eliminating these lookahead biases prevents your explainable AI loan underwriting platform development from generating inaccurate or misleading feature attributions.

3. Detect Proxy Variables

Simply removing explicit protected class fields like race, gender, or age from your training data is completely insufficient for fair lending compliance. Because advanced algorithms excel at finding hidden patterns, they frequently recreate systemic biases using highly correlated proxy variables:

- High-risk proxy vectors: The compliance engine must continuously test fields such as ZIP code, device data, application language, and educational history.

- Behavioral proxy vectors: Risk teams must closely monitor employment patterns, merchant categories, location history, and complex household relationships.

- Automated detection: Platforms require active statistical monitoring to flag and suppress features that display strong correlation to protected characteristics.

For a deeper breakdown of lending data, feature engineering, and credit-risk infrastructure, see our guide on How To Develop A Fintech Credit Risk AI System.

4. Treat Missing Data As A Model Feature Risk

The complete absence of a data point is often a strong risk indicator that requires deliberate structural handling rather than random imputation. This platform must isolate the underlying cause of incomplete records to prevent unfair denials:

- Borrower profiles: Missingness frequently reflects thin-file borrowers, specific income types, product channels, or individual applicant choices.

- System dynamics: Incomplete data fields may stem from data access differences, geographic availability, or failed vendor integrations.

- Algorithmic handling: Platforms should distinguish genuine data absence from technical connection failures to avoid penalizing borrowers for platform downtime.

As a result, your feature engineering layer must assign distinct, explainable null codes that interpret missing data as a specific operational state.

Securing your data lineage provides the necessary foundations for generating faithful, compliant model explanations across your portfolio. Once these data contracts and feature pipelines are robustly built, the engineering focus shifts directly to evaluating the total financial capital required to put this system into production.

Consequently, analyzing the complete development phases, resource timelines, and total investment ranges is the next vital decision-making step.

Test Fair Lending Risk Before The Model Reaches Borrowers

Fair lending testing must comprehensively examine model predictions, final policy decisions, risk-based pricing, manual overrides, and adverse action reasons. Consequently, testing only mathematical model accuracy can easily miss systemic disparities introduced by rigid business rules, data availability, channel design, or human judgment.

Financial institutions must implement comprehensive automated fairness audits across every single phase of the application life cycle before code reaches production.

1. Measure Outcomes Across The Entire Decision Funnel

Fair lending analysis cannot look at final approvals in isolation, but must instead trace applicants through every step of the decision funnel. Disparities often hide within early automated stages or operational routing handoffs:

- Top-of-funnel tracking: Platforms must monitor application completion rates, data verification drops, and identity fraud referral frequencies.

- Core decision metrics: Engineering teams test the raw distribution of model scores, manual underwriter review triggers, and final approval ratios.

- Terms and conditions: Lenders must evaluate variations in assigned credit limits, risk-adjusted interest rates, conditional approval terms, and appeal outcomes.

By mapping these steps, risk officers can see if specific cohorts are disproportionately routed to high-friction manual reviews.

2. Use Multiple Fairness Measures

Lenders must deploy a balanced suite of mathematical fairness metrics because no single statistical measure can resolve every competing lending objective. At the same time, modern explainable AI fair lending compliance software builds require a multi-layered analytical framework:

- Group parity metrics: Compliance systems measure approval-rate ratios, adverse impact ratios (AIR), and error-rate balances across cohorts.

- Predictive performance balance: Validators evaluate true positive and false positive rates alongside equal opportunity and equalized odds constraints.

- Advanced fairness testing: Advanced frameworks analyze statistical calibration by group, individual fairness indicators, and counterfactual fairness models.

Balancing these metrics allows institutions to optimize risk prediction while maintaining strict alignment with Equal Credit Opportunity Act (ECOA) standards.

3. Test Intersections, Not Only Broad Categories

Evaluating fair lending risk solely through broad, isolated categories can completely mask deep algorithmic biases that occur at sub-demographic levels. Consequently, platforms must run advanced intersectional audits to detect hidden proxy variables and compound disparities:

- Demographic intersections: The software cross-references variables such as age combined with gender, or race proxies combined with specific geographies.

- Financial and channel variations: Risk teams monitor income types mixed with disability-related income, alongside thin-file status combined with language indicators.

- Operational parameters: Compliance engines analyze differences between product channels, retail locations, and small business ownership characteristics.

These granular checks ensure that complex machine learning ensembles do not inadvertently penalize overlapping vulnerable groups.

4. Search For Less Discriminatory Alternatives

When standard testing reveals disparate impact within a credit algorithm, the development team is legally obligated to search for a Less Discriminatory Alternative (LDA). This optimization process aims to maintain predictive power while minimizing group variances:

- Feature adjustments: Engineers compare different feature sets, enforce strict monotonic constraints, or swap complex ensembles for transparent interpretable models.

- Policy re-tuning: Data scientists test alternative threshold settings, create separate manual-review bands, or integrate alternative cash-flow variables.

- Model selection: Risk leaders explicitly choose models that demonstrate highly similar predictive performance but significantly lower demographic disparity.

Documenting this comprehensive search process provides crucial evidence for regulatory examination credit for AI readiness.

5. Monitor Fairness After Deployment

A credit model can pass internal validation with perfect scores but subsequently develop significant demographic disparities once exposed to live production environments.

Therefore, automated MLOps tracking tools must continuously monitor for fairness degradation driven by real-world shifts:

- Exogenous shocks: Systemic imbalances frequently follow rapid population changes, sudden economic shocks, or aggressive new marketing campaigns.

- Data quality movements: Platforms must track variances caused by alternative data-provider changes, missing-data distribution shifts, and policy updates.

- Human variables: Compliance officers closely audit manual override patterns to ensure human underwriters are not introducing new biases into the system.

For a deeper breakdown of production monitoring architectures, see our guide on XAI credit platform MLOps pipelines. This continuous feedback loop ensures the platform remains fair and compliant through fluctuating credit cycles.

Govern Credit Models Under The Revised SR 26-2 Framework

In early 2026, the Federal Reserve, OCC, and FDIC jointly issued the revised SR 26-2 framework to modernise model risk governance. Consequently, this updated guidance formally supersedes and replaces the long-standing SR 11-7 standard.

The new framework moves away from rigid annual mandates, explicitly prioritising a risk-based, tailored approach that scales directly to an institution’s size, complexity, and specific model use case.

1. Maintain A Complete Model Inventory

Financial institutions must maintain an active, centralized ledger of all quantitative tools running across their business lines. Therefore, risk teams are deploying relational knowledge graphs to track interconnected credit model dependencies instead of using flat compliance spreadsheets:

- Administrative metadata: The tracking system logs the formal model name, primary business purpose, designated owner, and affected portfolios.

- Technical characteristics: Registries document underlying machine learning methodologies, baseline data sources, model versions, and active dependencies.

- Governance logs: The dashboard displays historical validation dates, operational limitations, third-party component ties, and eventual retirement statuses.

Maintaining this clear visibility ensures that risk managers can evaluate aggregate model risks across the entire enterprise.

2. Document Model Development And Intended Use

Comprehensive documentation provides the foundational proof needed to satisfy rigorous validation teams and regulatory examiners. As a result, developers must explicitly capture the entire model lifecycle context from the moment code is written:

- Strategic design: Documentation outlines the exact business objective, target variables, data windows, and feature-selection rationales.

- Algorithmic execution: Engineers record algorithm comparison tests, hyperparameter settings, mathematical threshold selections, and known product limitations.

- Operational boundaries: Profiles specify the expected system users, permitted business environments, and prohibited deployment use cases.

This granular record-keeping guarantees that model users fully understand an algorithm’s structural boundaries.

3. Establish Independent Validation And Effective Challenge

The SR 26-2 framework preserves the foundational requirement for objective review but redefines how evaluation rigor is measured. Specifically, the regulatory focus shifts from rigid organizational design to the demonstrable quality, influence, and impact of the challenge itself:

- Core soundness: Objective experts critically test conceptual soundness, data suitability, implementation accuracy, and raw model performance.

- Advanced auditing: Validators execute benchmarking, sensitivity analysis, fair lending checks, and post hoc explainability fidelity testing.

- Operational reviews: Teams verify ongoing performance monitoring designs and evaluate historical outcomes analysis.

To support this transparency, platforms require dynamic workflow engines that log the complete query-and-remediation dialogue between validators and developers.

4. Set Change-Control Thresholds

Lenders must establish objective, tiered triggers to manage model updates systematically throughout changing economic cycles. Consequently, these metrics prevent silent algorithmic modifications from bypassing institutional oversight controls:

- Routine maintenance: Systems automate low-risk recalibrations and execute continuous data drift monitoring protocols.

- Material variations: Pre-defined threshold breaches force immediate partial revalidations, full revalidations, or model rollbacks.

- Governance actions: Major structural changes require formal policy approval, compliance review, or complete model retirement.

Tying these actions to specific performance stability metrics ensures your platform remains stable without creating operational bottlenecks.

5. Govern Third-Party Models And Data

Outsourcing model development to third-party providers does not transfer or reduce an institution’s ultimate responsibility for model risk. Thus, lenders must enforce strict vendor governance protocols to maintain regulatory defensibility:

- Lineage and visibility: Agreements must mandate full documentation access, historical performance evidence, and explicit data lineage tracking.

- Testing and transparency: Vendors must supply clear explanation methodologies, fairness-testing support, and permission for independent internal testing.

- Risk mitigation: Contracts must establish urgent incident procedures, automatic version notifications, and clear exit or portability rights.

Adopting the principles-based SR 26-2 framework allows financial institutions to replace rigid annual review cycles with a highly tailored, materiality-driven model validation strategy.

Adapt Explainability By Credit Product And Borrower Context

The same explanation architecture cannot be copied unchanged across every lending product inside a financial institution.

Consumer loans, mortgages, SMB lending, and commercial credit use drastically different data inputs, decision policies, adverse action obligations, approval authorities, and evidence standards.

Consequently, engineering teams must build flexible, context-aware platforms that adapt explanation outputs to match the specific structural requirements of each line of business.

1. Product-Specific Underwriting Framework Mapping

Lenders must configure distinct explainability engines to handle the operational nuances of different portfolios:

| Product Category | Core Data Inputs | Primary Target User | Key Explanation Output |

| Consumer & BNPL | Bureau data, cash flow APIs | Consumer, Frontline Agent | Real-time automated reason codes |

| Mortgages | Tax returns, property appraisals | Underwriter, Fannie/Freddie | GSE compliance, manual conditions |

| Small Business (SBA) | Tax returns, banking cash flow | Commercial Credit Analyst | Blended business and guarantor logs |

| Commercial & CRE | Debt service coverage, NOI tables | Credit Committee, Sponsors | Scenario stress tests, credit memos |

2. Consumer Loans, Cards, Auto, And BNPL

Consumer and Buy Now, Pay Later (BNPL) platforms require high-velocity explanation engines that operate within tight real-time API latency limits. Therefore, these systems must automate reason generation to support sub-second loan approvals:

- High-volume pipelines: Platforms ingest micro-features from bureau files and open banking affordability variables to evaluate millions of transactions instantly.

- Alternative scoring: Systems use local model explainability to safely evaluate thin-file borrowers without increasing portfolio default rates.

- Notice automation: Engines map feature weights instantly to automated Regulation B reason codes for credit limits, pricing, and outright denials.

Maintaining low latency ensures that compliance checks never disrupt the consumer application journey.

3. Mortgage Underwriting

Residential mortgage platforms must balance automated machine learning inputs with highly structured federal documentation frameworks. Consequently, the explanation architecture must trace how automated findings interact with manual validation checks:

- Core financial checks: Software tracks feature weights across income verifications, debt-to-income (DTI) calculations, and loan-to-value (LTV) limits.

- Property evaluations: Pipelines ingest structural property details, historical appraisal data, and localized Home Mortgage Disclosure Act (HMDA) data.

- Investor compliance: Software maps model choices directly to FHA, VA, USDA, Fannie Mae, or Freddie Mac underwriting criteria.

This comprehensive tracking provides the detailed data trails needed to support intricate adverse action and counteroffer workflows.

4. Small Business And SBA Lending

Small business and SBA underwriting requires a blended explainability design that evaluates both the commercial enterprise and the individual owner simultaneously. As a result, systems must cleanly separate company performance signals from personal credit attributes:

- Business health parameters: The platform analyzes tax returns, accounting software registers, cash flow variables, and revenue concentration risks.

- Risk cross-referencing: Engines evaluate specific industry risk codes, historical obligations, personal guarantees, and individual guarantor credit profiles.

- Narrative compilation: The software generates clear summaries that outline how business trends and personal credit histories influenced the final decision.

This unified reporting enables commercial loan officers to navigate complex credit committee approvals efficiently.

5. Commercial And CRE Underwriting

Commercial real estate (CRE) and corporate credit deals operate through high-touch manual workflows rather than high-volume automated scoring queues. Therefore, the XAI platform functions primarily as an advanced decision support tool for institutional analysts:

- Property cash flows: System inputs capture net operating income (NOI), debt service coverage ratios (DSCR), and current tenant concentration risks.

- Strategic assessments: Algorithms weigh sponsor strength, projected market assumptions, covenant structures, and complex scenario analyses.

- Committee support: The platform exports versioned feature attributions directly into comprehensive credit risk memos.

Providing these clear data summaries helps credit committees defend complex pricing choices during internal risk reviews.

Adjusting explainability to fit each product line ensures that lenders meet strict regulatory mandates without introducing unnecessary latency into fast consumer funnels.

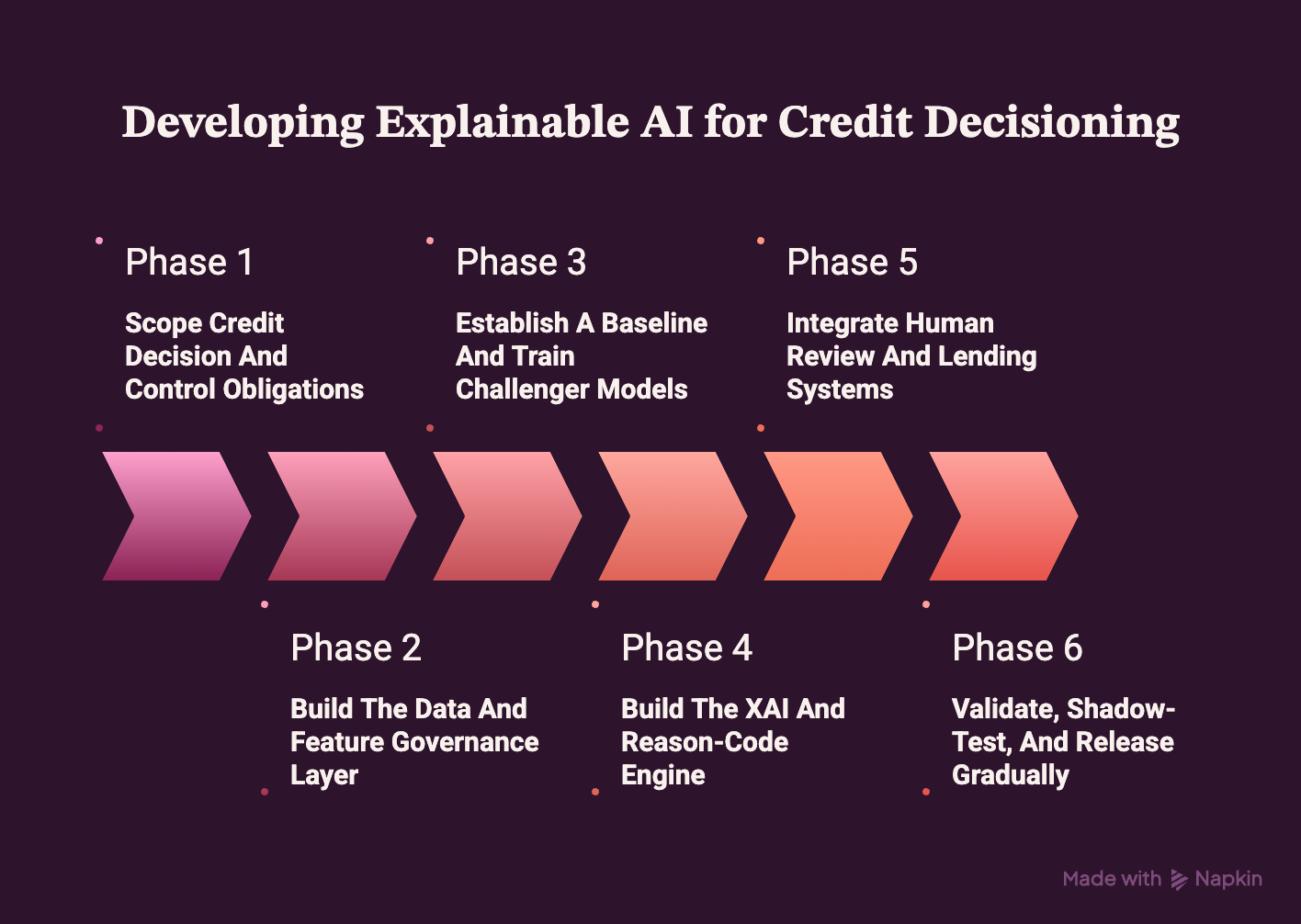

How To Develop Explainable AI For Credit Decisioning

Building a production-grade explainable AI lending platform requires a disciplined engineering sequence that balances mathematical rigor with strict regulatory compliance. Consequently, financial institutions must move away from isolated data science experiments and instead deploy structured pipelines that govern data, models, and policy choices uniformly.

Following a comprehensive multi-phase development roadmap ensures that the resulting software safely passes model risk validation while driving operational efficiencies.

Phase 1 — Scope Credit Decision And Control Obligations

Before writing code, teams must define the loan product, model target, permitted decision states, adverse action obligations, fair lending tests, human authorities, and performance thresholds.

Without this early agreement, different teams will build incompatible definitions of what the model predicts and what the platform decides:

- Technical execution: Engineers compile an explicit decision inventory, map federal regulatory obligations, establish risk-appetite thresholds, and evaluate existing underwriter workflows. Concurrently, product leaders document precise user explanation requirements, set performance success metrics, and complete a formal model-materiality assessment.

- The Intellivon practice: We map each functional requirement directly to an isolated service, automated workflow, immutable evidence record, and designated test before model development begins. This architectural mapping guarantees that the technical build matches the legal obligations of the financial institution from day one.

Phase 2 — Build The Data And Feature Governance Layer

Developers must create versioned data pipelines that can completely reproduce every underwriting feature from its original raw source.

Therefore, the platform should know exactly which bureau field, transaction record, document value, or application answer produced each model input:

- Technical execution: Engineers build resilient API data connectors, codify strict data contracts, and assemble historical training datasets containing clear outcome labels. Additionally, they implement point-in-time joins, structure a centralized feature store, script automated missing-data handling routines, execute proxy reviews, and map feature lineage trees.

- The Intellivon practice: We intentionally separate raw ingested data, normalized data streams, processed model features, and final decision evidence into decoupled database schemas. This strict isolation ensures that a future feature transformation or code update cannot silently alter historical credit results or invalidate compliance records.

Phase 3 — Establish A Baseline And Train Challenger Models

Data science teams must build an intrinsically interpretable baseline model before introducing highly complex machine learning ensembles.

At the same time, comparing traditional scorecards or explainable boosting models against XGBoost, LightGBM, random forests, or neural alternatives using identical data windows ensures that performance lift is objectively measured:

- Technical execution: The team trains a transparent baseline model alongside advanced challenger models, executing iterative hyperparameter tuning and temporal validation checks. Data scientists then evaluate model calibration curves, enforce strict monotonic constraints, run segment-specific tests, and document benchmark comparisons.

- The Intellivon practice: We position the ultimate model selection as a documented, auditable trade-off among predictive lift, explanation fidelity, operational latency, and regulatory defensibility. This formal documentation provides bank examiners with clear evidence of conceptual soundness and rigorous model selection governance.

Phase 4 — Build The XAI And Reason-Code Engine

Engineering teams must deploy explanation generation as a highly governed backend service rather than a basic, post-prediction visualization dashboard.

At the same time, the service should calculate validated attributions, test explanation stability, connect model drivers to policy outcomes, and map approved principal reasons into consumer-facing language:

- Technical execution: Developers configure TreeSHAP or alternative attribution calculators, deploy an automated counterfactual engine, and execute explanation fidelity tests. The pipeline continuously monitors fair lending metrics, runs proxy detection routines, builds a reason-code dictionary, structures adverse action templates, and exposes a secure explanation API.

- The Intellivon practice: We keep reason code selection completely deterministic within the software architecture. While generative AI tools may be used to format approved compliance language for clarity, an LLM never decides why credit was denied or which risk factors drove the decision.

Phase 5 — Integrate Human Review And Lending Systems

The explainable platform must be embedded directly inside the institution’s real-world underwriting systems to deliver operational value.

Therefore, applications should move from the Loan Origination System (LOS) through data verification, notice generation, and decision write-back without losing the original evidence:

- Technical execution: Engineers build secure integrations with the core LOS, establish bureau and open banking API handoffs, and construct an interactive case management interface. The workspace exposes clear underwriter dashboards, accommodates conditional approvals, tracks manual overrides, processes appeals, logs audit events, and handles core banking write-backs.

- The Intellivon practice: We treat systemic integration endpoints as a core component of overall decision integrity. Every API response receives an immutable trace identifier that permanently links the external borrower application to the exact internal model version and policy rule execution used.

Phase 6 — Validate, Shadow-Test, And Release Gradually

Risk teams must run the new explainable platform alongside the existing legacy underwriting process before allowing it to make production decisions.

Therefore, operating in shadow mode reveals hidden disagreements, missing data anomalies, unstable reason codes, fairness issues, and integration failures without immediately affecting live applicants:

- Technical execution: Internal teams perform independent validation assessments, run User Acceptance Testing (UAT), execute historical backtesting, and monitor live shadow scoring queues. Analysts perform champion-challenger comparisons, evaluate underwriter disagreement metrics, initiate a limited portfolio rollout, set monitoring thresholds, and draft a model rollback plan.

- The Intellivon practice: We position production deployment as a controlled, gradual expansion that moves systematically from one simple product and single decision path to additional borrower segments and complex lending products. This phased release minimizes balance sheet risk while ensuring operational workflows adapt safely.

Enterprise Development Estimation Lifecycle

Project timelines scale predictably based on the complexity of your core integration endpoints and the volume of alternative data streams utilized:

| Development Scope | Recommended Timeline | Essential Resource Requirements |

| Focused Proof of Value | 8–12 weeks | 1 Data Scientist, 1 Data Engineer, 1 Compliance Advisor |

| Explainable Underwriting MVP | 12–16 weeks | 2 Data Scientists, 2 Full-Stack Engineers, 1 MLOps Engineer |

| Integrated Production Platform | 5–8 months | 3 Developers, 2 Data Scientists, Dedicated QA, Security Lead |

| Multi-Product Enterprise Rollout | 8–12 months | Full Platform Team, Core Systems Integrators, Risk Executives |

Run your explainable credit platform in shadow mode for at least 30 to 60 days to catch data anomalies before the system impacts live borrower applications.

Executing this comprehensive development roadmap provides the necessary foundations for scaling automated decisioning with absolute compliance confidence.

Once these development phases, resource timelines, and platform milestones are fully understood, leadership can objectively evaluate the total capital allocation required to build the platform.

Explainable AI Credit Underwriting Development Cost

Explainable AI credit underwriting development usually costs $70,000 to $300,000, depending on model complexity, lending products, explanation methods, adverse action workflows, fair lending controls, data integrations, and model governance requirements.

Consequently, lenders must evaluate their institutional scale and compliance constraints to determine the appropriate platform tier.

Building a custom system ensures the underlying software architecture aligns perfectly with your existing risk frameworks without forcing you into restrictive vendor licensing models.

1. Platform Cost Tiers and Capabilities

Budget requirements map directly to the operational scope, deployment environments, and regulatory burdens of the financial institution:

| Platform Scope | Cost Range | Included Scope |

| Focused XAI MVP | $70,000–$110,000 | One credit product, interpretable baseline, one challenger model, SHAP explanations, basic reason codes, underwriter dashboard, one LOS or bureau integration |

| Integrated Production Platform | $120,000–$210,000 | Multiple data sources, advanced model, adverse action automation, fairness testing, appeals, audit records, MLOps, LOS, and core integration |

| Enterprise Multi-Product Platform | $220,000–$300,000 | Multiple credit products, model inventory, independent validation workflows, advanced monitoring, mortgage or commercial modules, private deployment, extensive integrations |

2. Component Development Phase Breakdown

Bespoke platform budgeting requires breaking down allocations across core engineering, security, and compliance workstreams:

- Discovery and data layers: Credit workflow and compliance discovery cost $8,000–$15,000, while engineering data pipelines and feature governance require $15,000–$40,000.

- Algorithmic engines: Baseline and challenger model development requires $18,000–$45,000, whereas building the dedicated XAI and reason-code engine budgets at $15,000–$35,000.

- Control and network connectivity: Fair lending and model governance controls require $12,000–$30,000, while execution of LOS, bureau, core, and workflow integrations ranges from $20,000–$60,000.

- Operations and deployment: MLOps pipelines, security setups, validation testing, and final release engineering cost between $15,000 and $40,000.

These specific component ranges overlap because the final budget is scoped as one single, cohesive platform. Therefore, they should not be added mechanically when calculating total investment targets.

3. Calculating Annual Maintenance Commitments

Lenders must budget approximately 15%–22% of their initial build cost annually to cover long-term support and compliance validation. This operational fund ensures the system adjusts safely to real-world environmental shifts:

- Data and code variations: Capital covers data-provider API changes, cloud infrastructure fees, security patches, and ongoing explanation and reason-code maintenance.

- Performance and safety loops: Funds support continuous model monitoring, live statistical recalibration, and routine independent validation work.

- Regulatory tracking: Teams utilize these resources to execute regular fairness reviews and update models for evolving compliance changes.

Properly maintaining these pipelines prevents mathematical explanation drift while defending your credit choices against sudden market fluctuations.

Build Explainable AI Credit Underwriting Software With Intellivon

Build explainable AI credit underwriting software with Intellivon when your financial institution requires absolute control over its models, lending policies, reason-code logic, fair lending tests, human review workflows, and system integrations.

Intellivon acts as your specialized engineering partner, connecting these complex components into a reproducible, production-ready decision system.

By drawing on over 500,000 engineering hours and deep ex-MAANG engineering experience, we deliver compliance-ready development practices and a production-first architecture optimized for complex financial system integrations.

Production-First Technical Capabilities

- Decision architecture: We strictly separate risk prediction, policy logic, pricing engines, human reviews, and borrower communications.

- XAI engineering: Our teams implement intrinsically interpretable models, SHAP values, counterfactual explanations, fidelity tests, and continuous explanation monitoring.

- Adverse action controls: We link actual model and policy drivers directly to approved consumer reason codes to eliminate compliance risk.

- Fair lending testing: The system evaluates outcomes, pricing, referrals, overrides, reasons, and appeals across different applicant groups.

- Model governance: We build automated model inventories, versioned documentation, validation workflows, and change controls aligned with the revised SR 26-2 standard.

- Lending integration: Pipelines connect seamlessly to bureau data, open banking APIs, LOS platforms, core banking ledgers, and CRM applications.

- Human control: Interfaces provide explicit review bands, evidence workspaces, override logging, escalations, appeals, and formal data reconsideration tracking.

- Production MLOps: Systems utilize our AI, LLM, MLOps, and agentic workflow expertise to monitor performance, calibration, drift, fairness, and rollback conditions.

Our primary objective will be determining whether your institution needs a focused explanation service layer, an integrated production underwriting framework, or a complete multi-product XAI decisioning platform.

Conclusion

Deploying explainable AI underwriting converts regulatory compliance into a distinct balance sheet advantage. By replacing opaque risk scores with a modular architecture that separates mathematical predictions from business policy rules, lenders drastically reduce manual review bottlenecks while insulating themselves against systemic fair lending risks.

Ultimately, establishing this granular data lineage and auditable explanation framework ensures your lending infrastructure remains perfectly resilient through fluctuating credit cycles and evolving regulatory examinations.

FAQs

Q1. Is SHAP Enough To Make An Adverse Action Notice Compliant?

A1. No. SHAP identifies which features influenced a prediction, but it does not prove they were the actual principal reasons for adverse action. Therefore, lenders need controlled reason-code logic, policy traceability, and validation. Moreover, every disclosed reason must accurately reflect the final credit decision and the evidence used to support it.

Q2. Should A Lender Use Logistic Regression Or XGBoost?

A2. Use logistic regression when interpretability, policy transparency, and easier validation matter most. However, choose XGBoost when nonlinear patterns deliver meaningful, validated predictive gains. Keep the simpler model as a benchmark. Then compare performance, calibration, fairness, explanation stability, and validation cost before deciding whether added complexity creates sufficient clear operational value.

Q3. How Much Historical Data Is Needed To Build Explainable AI Credit Risk Assessment Software?

A3. There is no universal row count. Instead, use at least one complete performance window with enough good and bad outcomes for stable validation. Also include point-in-time application data, product coverage, economic variation, and separate development, validation, and out-of-time samples. For low-default portfolios, use pooled data, expert models, or limited automation.

Q4. How Does XAI Integrate With An Existing Loan Origination System?

A4. Use an API-based decision service between the LOS and the XAI platform. First, the LOS sends the application identifier and verified data. Then, the platform returns the risk score, policy decision, reason codes, conditions, review status, model version, and trace identifier. Finally, the LOS stores the outcome and notice securely.

Q5. Can Alternative Data Create Proxy Discrimination?

A5. Yes. Alternative data can create proxy discrimination because cash flow, location, device, education, employment, rental, utility, or behavioral patterns may correlate with protected characteristics. Therefore, test every feature before approval. Also compare less discriminatory alternatives, monitor group outcomes, document business necessity, and remove variables that create risk without sufficient value.

Q6. What Should Happen When An Underwriter Disagrees With The Model?

A6. The platform should allow a controlled override, not an informal judgment. Therefore, the underwriter must select a reason, attach evidence, record authority, and obtain second-line approval when required. In addition, monitor overrides by reviewer, branch, product, applicant group, reason, and subsequent loan performance to identify inconsistency or emerging systemic bias.

To Sum Up:

- A compliant explanation must reproduce the actual credit decision. A plausible narrative is not enough.

- SHAP can identify influential features, but adverse action compliance still needs controlled reason-code logic and validation.

- The safest production launch begins with shadow scoring and human review, not immediate end-to-end automation.

- A $70,000 MVP can prove one product and one decision path, while multi-product governance and integrations move the build toward $300,000.