Banks have spent the last decade using AI in their operations, including fraud detection, credit scoring, and customer service automation. While these tools add value, they have one major flaw. They operate in isolation, handling single tasks and requiring human input before progress can be made. This is where efficiency breaks down, and operational costs start to increase. The real issue in enterprise banking today is the lack of AI that can think across systems, link decisions to actions, and drive results without needing constant human support.

Agentic AI is the technology that fills this gap. It gives financial institutions the ability to use AI that reasons, plans, and carries out complex multi-step workflows on its own across their entire infrastructure. Early users in enterprise banking are already seeing returns of 2x or more within the first few months of implementation.

Intellivon has hands-on experience building and scaling these systems for large financial enterprises. This means the insights in this blog come from real-world experience rather than theoretical ideas. In this blog, we discuss what agentic AI means in banking today, where it offers the most strategic advantages within large institutions, and why the opportunity to lead this change rather than fall behind is closing faster than many leadership teams realize.

Why Traditional AI Is Failing in Banking Today

Traditional AI in banking, including rule-based and early ML systems, struggles to scale. Legacy systems and data silos slow integration. Many projects remain stuck in pilot stages despite heavy investment. As a result, banks cannot move toward real-time, autonomous operations. This gap becomes critical as fraud risks rise and regulatory pressure continues to increase.

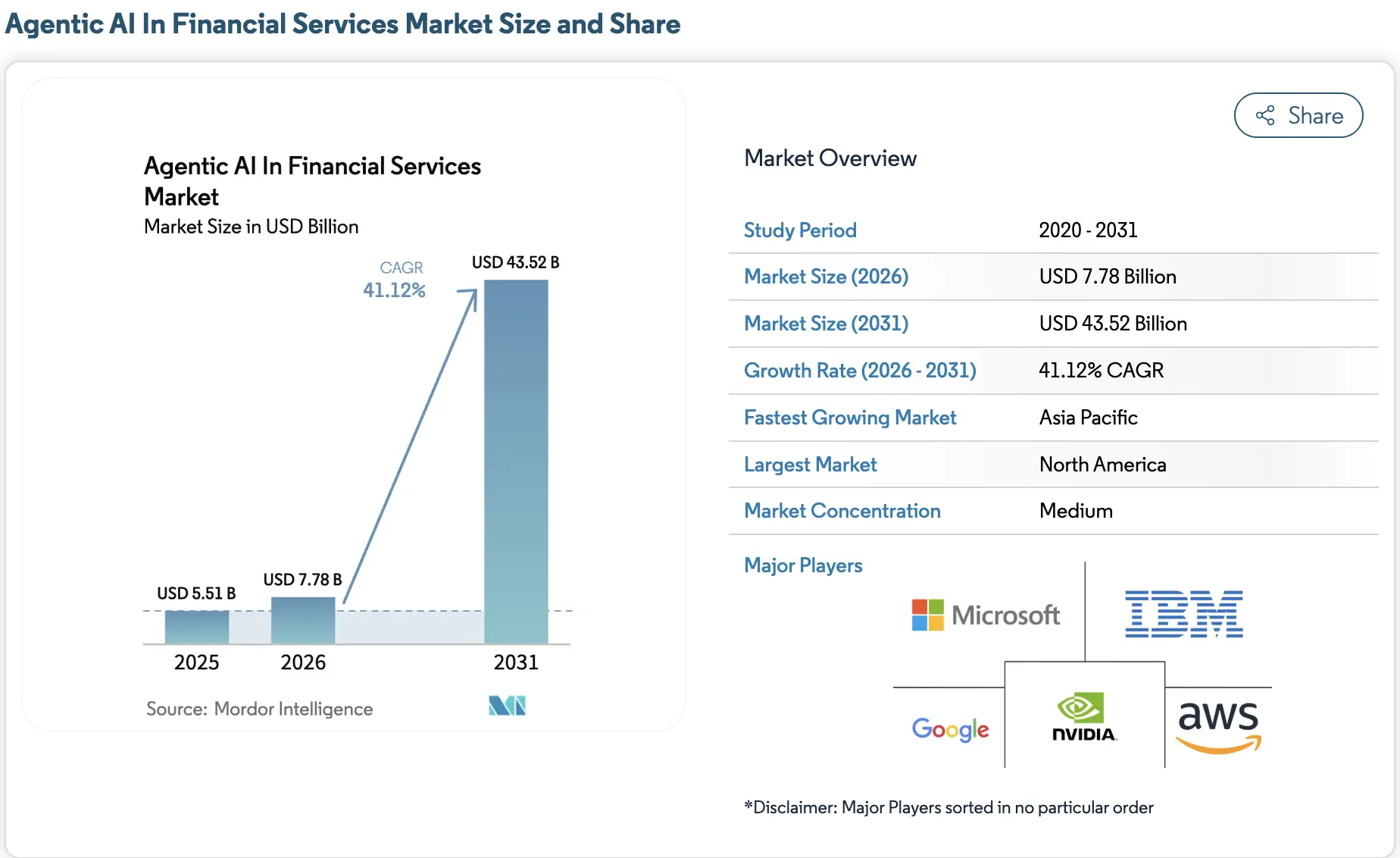

The agentic AI market in financial services is growing rapidly. It is valued at USD 7.78 billion in 2026, up from USD 5.51 billion in 2025. Projections show it reaching USD 43.52 billion by 2031. This reflects a strong CAGR of 41.12% from 2026 to 2031.

The banking sector has reached a saturation point with legacy technology. While previous investments in digital transformation provided a foundation, they are now struggling to keep pace with modern market demands and complexity.

1. Limits of Rule-Based Automation at Scale

Rule-based systems use rigid logic for data entry. However, these frameworks fail to handle the complexities of global finance. If a transaction deviates from a rule, the system stops. This creates massive backlogs and false fraud alerts.

Consequently, managing thousands of rules becomes a logistical burden. These systems stay reactive and leave enterprises exposed to new risks.

2. Why Predictive AI Cannot Execute Decisions

Predictive AI analyzes data to forecast events. Yet, it cannot take action on its own. A model might flag a liquidity risk, but cannot rebalance a portfolio. Therefore, leaders must act as the bridge to execution.

This manual step causes costly delays in fast markets. A system that only observes is no longer sufficient for high-stakes enterprise operations.

3. Fragmented Systems Slow Financial Operations

Banks often operate in departmental silos. For instance, data remains trapped in retail, wealth, or compliance units. Some of the AI tools live within these silos and lack a unified view. In addition, employees must manually move data between platforms to finish tasks.

This fragmentation increases operational friction significantly. Thus, institutions spend more on maintenance than on actual innovation.

4. Growing Need for Autonomous Banking Systems

The industry is shifting toward systems that act independently. Specifically, agentic AI navigates complex workflows and interacts with various software tools. These agents resolve issues using pre-set strategic parameters.

Furthermore, enterprises can scale without adding headcount. They gain the agility needed for volatile markets. Consequently, this shift to autonomy creates and protects long-term financial value.

Traditional technology has laid the groundwork. However, its limitations are now clear. Leaders must transition from systems that suggest to systems that act.

Agentic AI is reshaping banking by enabling autonomous, multi-step workflows. It improves fraud detection, compliance, and loan processing. As adoption grows, banks gain faster operations and higher efficiency. Many expect around 20% cost reduction and quicker ROI. In fact, 57% of banks plan to fully embed it in risk functions within three years.

Major players in agentic AI for banking include Kore.ai, Oracle, Salesforce, Intellectyx, BUSINESSNEXT, Deloitte’s Zora AI, BNY Mellon, and JPMorgan Chase. They have successfully paved the way for agentic-AI-based banking systems to be adopted at a large scale.

What Agentic AI Means in Enterprise Banking

Agentic AI in banking refers to systems that can understand goals, make decisions, and take actions with little human input. In large banks, it helps handle tasks like fraud checks, compliance, loan processing, and customer operations in one connected flow.

As a result, teams work faster, reduce manual effort, and keep better control over complex systems and daily operations.

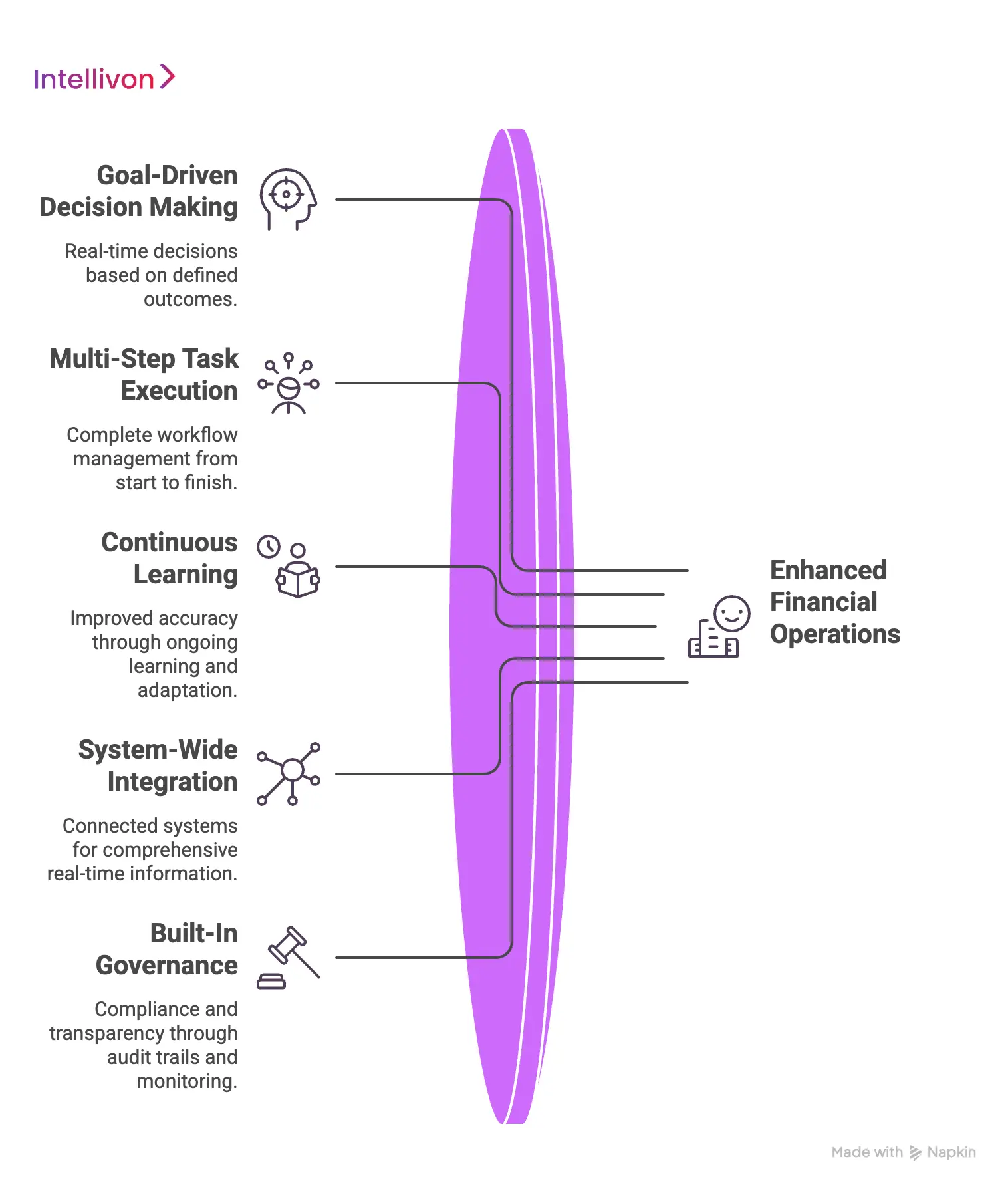

Core Traits of Agentic AI in Finance

Agentic AI introduces a different way of running financial operations. Instead of supporting teams, it takes ownership of tasks and decisions. This shift becomes important as banking workflows grow more complex and time-sensitive.

These systems are designed to act with purpose. They connect data, decisions, and execution into one continuous flow. As a result, banks can move faster while maintaining control across operations.

1. Goal-Driven Decision Making

Agentic systems work toward defined outcomes, not just instructions. For example, instead of flagging fraud, they can investigate, validate, and take action. This approach reduces delays between insight and execution. Therefore, decisions happen in real time, not in stages.

2. Multi-Step Task Execution

Traditional AI handles one task at a time. In contrast, agentic AI manages complete workflows from start to finish. For instance, in loan processing, it can verify data, assess risk, and trigger approvals. This removes the need for multiple manual handoffs.

3. Continuous Learning and Adaptation

Agentic AI improves with every interaction. It learns from outcomes, feedback, and changing conditions. As a result, systems become more accurate over time. This is especially useful in areas like fraud detection, where patterns evolve quickly.

4. System-Wide Integration

These systems connect across core banking platforms, APIs, and data sources. They do not operate in isolation. Because of this, decisions are based on complete, real-time information. In addition, it reduces dependency on fragmented tools.

5. Built-In Governance and Control

Agentic AI includes audit trails, monitoring, and explainability. Every action can be tracked and reviewed. This ensures compliance with financial regulations. At the same time, it gives leadership clear visibility into system behavior.

Agentic AI in finance is not just about automation. It brings together decision-making, execution, and control in one system. Therefore, banks can operate with more speed, accuracy, and confidence across critical workflows.

How Agentic AI Differs From AI Assistants

AI assistants have become common in banking. They help teams retrieve information, generate responses, and support decisions. However, they stop short of taking action.

Agentic AI moves beyond assistance. It can plan, decide, and execute tasks across systems without constant human input. This difference becomes critical in high-volume, time-sensitive banking operations.

Key Differences Between Agentic AI and AI Assistants

| Aspect | AI Assistants | Agentic AI Systems |

| Role in workflows | Supports human decisions | Executes decisions independently |

| Task handling | Handles single-step tasks | Manages multi-step workflows |

| Decision capability | Provides recommendations | Makes and acts on decisions |

| System interaction | Limited to queries and responses | Integrates across banking systems |

| Speed of execution | Depends on human action | Operates in real time |

| Learning ability | Improves responses over time | Adapts decisions based on outcomes |

| Operational impact | Improves productivity | Transforms entire workflows |

AI assistants improve efficiency at the surface level. They help teams move faster but still depend on manual execution.

Agentic AI changes how work gets done. It connects decisions directly with execution, which removes delays and reduces operational friction. Therefore, banks can handle complex workflows with greater speed, consistency, and control.

From AI Tools to Autonomous Banking Systems

The transition from separate tools to smart systems defines the next era of finance. Most banks have spent years collecting scattered software. However, the true advantage now lies in making these parts work together as one self-running unit.

1. Why Use Case AI Fails at Enterprise Scale

Many banks try to innovate by fixing small, isolated problems. They might buy one tool for a chatbot and another for reading documents. While these small wins look good, they fail to help the whole company.

These “point solutions” often cannot talk to each other. Consequently, the bank ends up with a messy pile of software that still needs humans to manage everything. This approach creates more work instead of reducing it.

2. Shift Toward End-to-End System Rewiring

Real change requires more than just adding a digital layer to old ways of working. It requires rewiring how the bank actually functions. Instead of using AI to help a person do a task, the goal is to let the system handle the work from start to finish.

This shift removes the “speed bumps” where data usually gets stuck or lost. Therefore, the institution becomes faster and more capable of fixing its own mistakes without being told.

3. AI as Financial Infrastructure, Not Feature

Smart leaders now treat artificial intelligence like the actual plumbing of the bank. It is no longer just a “cool feature” you add to an app. Instead, it is the basic foundation that handles rules, risk, and payments in real-time.

When intelligence is built into the base, every department gets more accurate. In addition, this ensures that safety and legal rules are followed automatically during every single transaction.

4. Rise of Multi-Agent Systems in Banking

The biggest breakthrough is the move toward “multi-agent” systems. In this model, different specialized AI “workers” work together like a team. One agent might find data, another checks for risks, and a third completes the trade.

These agents talk to each other and pass off tasks perfectly. As a result, the bank can handle thousands of complex jobs at once. This creates a level of stability that was once impossible to reach.

Investing in these systems is a smart way to protect the future of the company. It ensures your tech can grow as fast as the market moves.

How Agentic AI Systems Work in Banking

To understand why this technology is a game-changer, you have to look at the “brain” behind the operation.

Unlike older software that just follows a list, these systems actually understand the goal. They navigate the entire banking environment to get results.

1. Data Ingestion Across Banking Systems

An agentic system begins by connecting to every corner of the bank. It pulls information from legacy databases, real-time market feeds, and even unstructured emails. Most traditional tools struggle because they can only read one type of data at a time.

However, these new agents can digest diverse information simultaneously. This creates a “live map” of the entire financial landscape. Therefore, the system always operates with the most current facts available.

2. Goal-Oriented Agents and Planning Engines

The core of this tech is the ability to plan. You don’t give an agent a “step,” you give it a “goal,” such as “onboard this high-net-worth client.” The planning engine then breaks that goal into smaller tasks.

It decides which documents to verify and which background checks to run. In addition, if a document is missing, the agent doesn’t stop. It automatically pivots to find an alternative or requests the file. This creates a resilient workflow that moves toward the finish line.

3. Agent-to-Agent Communication and Orchestration

In a large enterprise, no single AI can do everything. Instead, multiple specialized agents talk to each other. One agent might be an expert in “Know Your Customer” (KYC) rules, while another is an expert in credit risk.

They hand off data and verify each other’s work instantly. This orchestration happens behind the scenes without needing a human manager. As a result, the bank can complete complex processes in seconds that used to take days of departmental back-and-forth.

4. Memory, Context, and Decision Loops

These systems possess something traditional automation lacks: a memory. They remember past interactions and learn from previous decisions. If a specific type of trade was flagged incorrectly last week, the system adjusts its logic for this week.

This “decision loop” allows the AI to get smarter over time. Consequently, the enterprise benefits from a system that evolves with the market. It doesn’t just repeat the same mistakes; it refines its strategy based on real-world outcomes.

5. Real-Time Execution Across Workflows

The final step is taking action. Once the plan is set and the risks are checked, the agents execute the task across different software platforms. They can log into a core banking system, move funds, and send a confirmation email all at once.

This removes the lag time between a decision and its result. Because the execution happens in real-time, the bank can react to market shifts instantly. This level of speed is the new standard for staying competitive.

Building this infrastructure is like giving your bank a digital nervous system. It ensures that every action is coordinated, fast, and focused on the ultimate business goal.

AI Agents as a New Banking Workforce Layer

Modern institutions are reimagining their organizational charts. Instead of just hiring more people to manage more data, they are deploying a digital layer of workers. This “workforce” doesn’t sleep, doesn’t make manual entry errors, and scales instantly with market demand.

1. How AI Agents Replace Operational Tasks

Most banking staff spend hours on “swivel-chair” tasks. This means moving data from one screen to another or checking documents for basic errors. Agentic AI takes over these repetitive actions completely. Unlike basic bots, these agents can log into legacy systems, read PDFs, and update records.

They understand the context of the work they do. Therefore, the bank can reassign human employees to high-value roles like strategy or client relations. This shift turns a cost center into a lean, high-output operation.

2. Human Oversight and Exception Handling

Deploying an AI workforce does not mean removing humans. Instead, it changes the human role to that of a “supervisor.” The agents handle 95% of routine transactions automatically. However, when a case is truly unique or high-risk, the agent flags it for a person.

This “human-in-the-loop” model ensures safety while maintaining speed. Consequently, managers only spend time on the most critical decisions. This approach balances the efficiency of a machine with the seasoned judgment of a professional.

3. Scaling Decisions With Multi-Agent Systems

A digital workforce scales in ways humans cannot. If a bank sees a sudden spike in loan applications, it doesn’t need to hire and train new staff. It simply deploys more agents. These agents work in “swarms” to process thousands of applications at once. They check credit scores, verify income, and assess collateral simultaneously.

Because they communicate instantly, there is no lag between steps. In addition, this allows the enterprise to capture market opportunities that would otherwise be lost to slow processing times.

4. Productivity Gains Across Banking Functions

The impact of this new layer is felt in every department. In compliance, agents monitor transactions for money laundering in real-time. In wealth management, they rebalance thousands of portfolios based on new market data.

Even in back-office accounting, they reconcile books without manual intervention. These gains represent a massive leap in how much work a single institution can handle. Thus, the bank achieves a level of productivity that was previously mathematically impossible.

The result is a bank that is leaner, faster, and more resilient. By treating AI as a workforce layer, you ensure that your operations are always ready for the next challenge.

Key Components of Agentic AI Systems

Building a system that can act on its own requires more than just a smart model. It needs a structured architecture that balances power with safety. These five components form the backbone of a true enterprise-grade agentic platform.

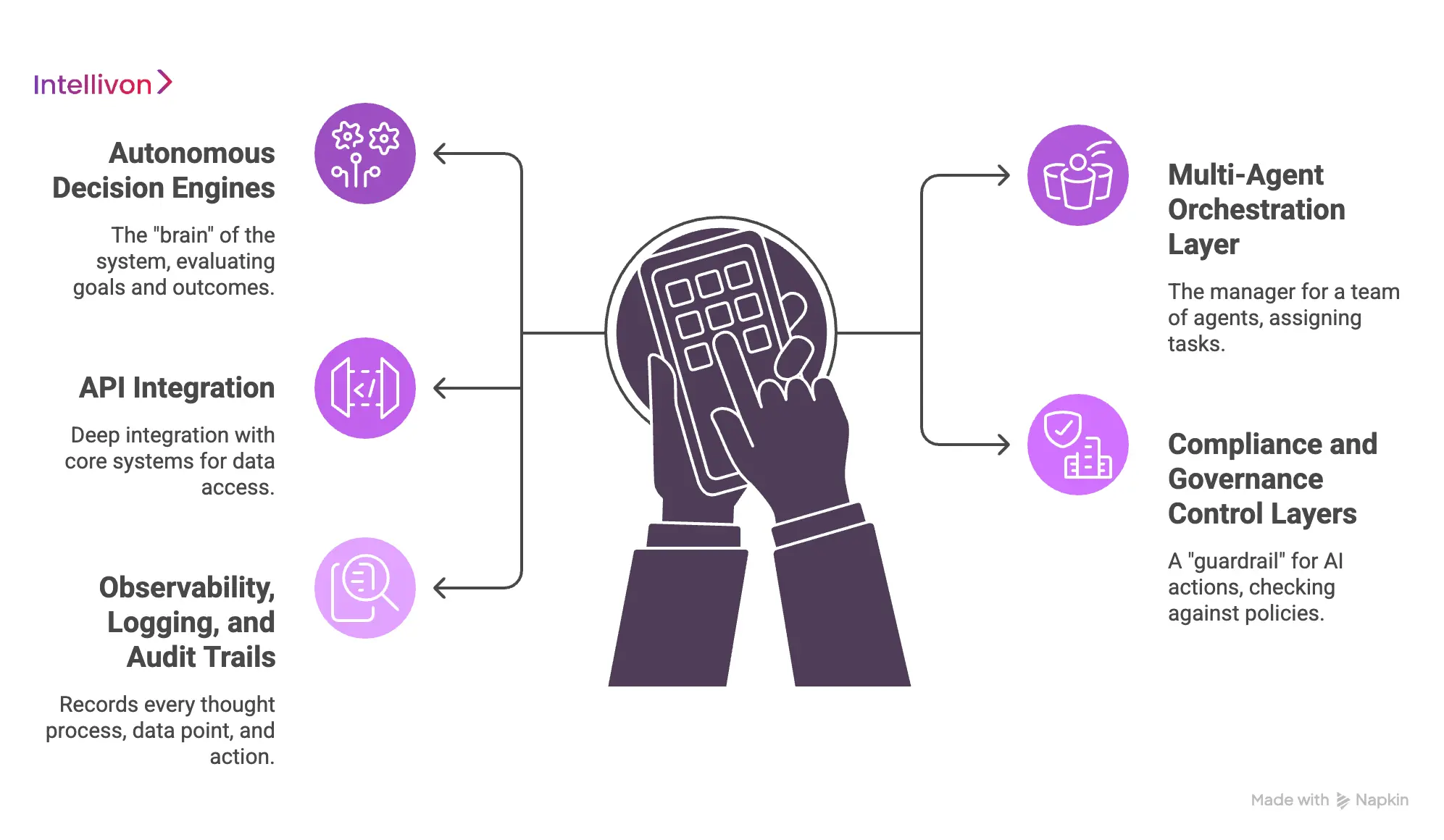

1. Autonomous Decision Engines for Finance

The decision engine is the “brain” of the system. Unlike basic programs that follow fixed steps, this engine evaluates goals and outcomes. For instance, in commercial lending, it analyzes credit scores, market trends, and cash flows to recommend a risk level.

It uses logic to determine the best path forward for each unique case. Therefore, the engine can handle complex financial scenarios that would normally stall a standard automation tool.

2. Multi-Agent Orchestration Layer

Large banks have many specialized needs, so they use a “team” of agents. The orchestration layer acts as the manager for this team. It assigns tasks to the right agent at the right time.

For example, one agent might collect tax data while another verifies legal identity. They work in parallel and share information instantly. As a result, the bank can process high-volume workflows without any internal bottlenecks or manual hand-offs.

3. API Integration With Core Banking Systems

For an agent to be useful, it must be able to “touch” the bank’s actual money and data. This requires deep integration with core systems through APIs. These connections allow the AI to read balances, trigger payments, and update client records directly.

In addition, a well-built integration layer ensures that the AI stays in sync with legacy software. This connectivity turns the AI from a simple advisor into a powerful tool that executes real-world actions.

4. Compliance and Governance Control Layers

In banking, safety is not optional. A dedicated control layer acts as a “guardrail” for every AI action. It checks every decision against internal policies and global regulations like KYC or AML.

If an agent tries to move funds that exceed a certain limit, the governance layer stops it for review. Consequently, the enterprise can innovate with confidence, knowing that the system cannot bypass the bank’s strict safety protocols.

5. Observability, Logging, and Audit Trails

Regulators demand to know exactly why a decision was made. This component records every thought process, data point, and action taken by the agents. It creates a transparent “paper trail” for every automated task.

If an auditor asks about a specific transaction from six months ago, the system can pull up the full logic used at that moment. Thus, the bank maintains perfect transparency while benefiting from the speed of autonomous operations.

The combination of these components creates a system that is both incredibly fast and fully accountable. It allows the enterprise to scale without losing control over its most critical processes.

Enterprise Use Cases Of Agentic AI in Banking

Theory is valuable, but the real worth of agentic systems lies in their ability to solve expensive, manual problems.

These five use cases show how large institutions are already moving from basic automation to fully autonomous operations.

1. Cross-Border Payments With AI Agents

Moving money across borders is traditionally slow because it involves many middleman banks. Each one has different rules and time zones. Agentic AI simplifies this by acting as a “navigator” for each payment.

The agent checks exchange rates, clears compliance rules in both countries, and picks the fastest route for the funds. Therefore, a process that used to take three days can now happen in minutes. This speed gives the bank a massive edge in the global trade market.

2. Autonomous Loan Underwriting Systems

Loan approvals usually require a human to check dozens of data points manually. An agentic system handles the entire “fact-finding” mission on its own. It pulls credit data, verifies tax returns, and even analyzes the borrower’s industry trends.

Instead of just giving a score, it builds a logical case for why the loan should be approved or denied. Consequently, the bank can process ten times more applications without increasing the risk of bad debt. In addition, customers get an answer in hours rather than weeks.

3. Dynamic Pricing for Financial Products

In a volatile market, fixed interest rates or fees can cost a bank millions in lost profit. Agentic AI monitors the market in real-time and adjusts pricing for products like mortgages or corporate loans.

If the central bank changes a rate, the agents update the bank’s entire catalog instantly. They balance the need for profit with the need to stay competitive for the customer. Thus, the enterprise ensures it is always offering the right price at the exact right moment.

4. AI Agents in Trade Finance Workflows

Trade finance is notorious for being “paper-heavy” and slow. It involves shipping documents, letters of credit, and complex legal contracts. AI agents can read these documents, match them against the trade agreement, and trigger payments once the conditions are met.

If a document is missing a signature, the agent contacts the sender to fix it immediately. As a result, the bank reduces the risk of fraud and speeds up the movement of goods across the globe.

5. Automated Dispute Resolution Systems

When a customer disputes a credit card charge, it usually starts a long manual investigation. Agentic AI can take over the “detective work” from the start. It reviews the transaction history, checks the merchant’s data, and applies the bank’s refund policies.

In simple cases, the agent can resolve the dispute and notify the customer in seconds. For complex cases, it prepares a full report for a human to review. This creates a much better experience for the customer while lowering the cost of support.

By applying these agents to specific workflows, banks can turn slow, manual departments into fast, digital profit centers. These systems don’t just help the staff; they change the way the bank delivers value.

Business Impact of Agentic AI in Banking

The shift toward autonomous systems is no longer a theoretical exercise for high-level research teams. It is a calculated move to protect margins and capture new market share in an increasingly digital economy.

For a large enterprise, the impact of agentic AI is measured by its ability to turn massive data sets into immediate, profitable action.

1. Cost Reduction Across Banking Functions

Operating a global bank is expensive, mostly due to the sheer volume of manual labor required for maintenance and compliance. Agentic AI addresses this by automating complex, multi-step workflows that were once the domain of specialized staff.

Recent industry data shows that institutions successfully deploying AI are seeing significant results. For example, 61% of financial institutions report cost reductions of more than 5% through AI, with a quarter of those seeing drops of over 10%.

These savings come from reducing “swivel-chair” tasks and eliminating human error in data processing. Consequently, the enterprise can process a higher volume of transactions without a linear increase in overhead. Therefore, the bank becomes more profitable even in a low-interest-rate environment.

2. Faster Decision-Making at Scale

In modern finance, speed is a competitive moat. Traditional systems often pause for manual reviews, creating bottlenecks that frustrate clients and lose deals. Agentic systems, however, operate in “goal-oriented” cycles that prioritize completion. By using autonomous routing, these systems can make complex decisions, such as transaction pathing, in under 200 milliseconds.

This speed allows a bank to approve a commercial loan or clear a high-risk payment before a human analyst could even open the file. Furthermore, because these agents communicate instantly, the entire organization moves at the speed of the market. Decisions are no longer delayed by departmental hand-offs or time-zone differences.

3. Operational Efficiency Improvements

Efficiency is about getting more output from the same set of resources. Agentic AI achieves this by acting as a digital nervous system that connects fragmented departments. Industry surveys indicate that 52% of financial leaders cite operational efficiency as the single largest improvement seen from AI adoption.

In addition, research into specialized implementations, like CRM and client engagement, shows that autonomous agents can increase operational efficiency by up to 30%. This improvement stems from agents handling routine inquiries and documentation autonomously. Thus, the human workforce is freed to focus on high-level strategy and complex client advisory roles.

4. Revenue Growth From Intelligent Systems

While cost-cutting is important, the true value of agentic AI is its ability to find new money. These systems use predictive insights to suggest the right product to the right client at the exact right moment. Data suggests that 64% of bank executives have seen revenue increases of over 5% directly attributed to AI.

Specific cases, such as the implementation at Mercedes-Benz Financial Services, demonstrate that agentic workflows can lead to a 20% increase in new business acquisitions. By automating cross-selling and upselling based on real-time behavior, the system acts as a 24/7 sales engine. As a result, the institution doesn’t just save money; it fundamentally expands its footprint in the market.

Investing in agentic AI is a strategic move that pays off on both the top and bottom lines. It transforms a bank from a passive storage unit for money into an active, intelligent growth engine.

Architecture Behind Agentic AI Systems in Banking

Building an autonomous bank requires more than just smart models. It demands a robust, layered architecture that allows agents to work safely and at scale. This technical foundation ensures that AI is not just a “siloed tool” but a core part of the bank’s digital nervous system.

1. API-First Integration With Banking Systems

An AI agent is only as powerful as the systems it can access. In 2026, the industry has shifted to an “API-first” approach. This means every banking function, from checking a balance to initiating a wire transfer, is available through a secure digital interface. Without these clean connections, an agent is just a chatbot that can’t take action.

Therefore, a modern architecture focuses on standardized APIs that allow agents to interact with legacy mainframes and modern apps alike. This connectivity is what turns “suggesting” into “doing.”

2. Cloud-Native Infrastructure for Scale

Autonomous systems require massive computing power that fluctuates based on market demand. Cloud-native designs allow a bank to “spin up” thousands of agents during peak hours, such as a sudden surge in loan applications.

Consequently, the enterprise doesn’t have to pay for idle servers during quiet times. In addition, using microservices ensures that if one part of the system fails, the rest of the agents keep working. This modularity is essential for maintaining the 99.9% uptime required by global financial institutions.

3. Real-Time Data Pipelines and Processing

Agents cannot make good decisions using old data. Traditional “batch processing,” where data is updated once a day, is no longer enough. Instead, agentic architectures use real-time pipelines that stream transaction and market data instantly.

Whether it is a shift in currency value or a new fraud pattern, the agents see it the millisecond it happens. Thus, the bank can react to risks and opportunities in real-time. This “live” data flow is the fuel that allows autonomous systems to outpace manual competitors.

4. Security, Compliance, and Governance Layers

In a regulated industry, every AI action must be controlled. Modern architectures include dedicated “guardrail” layers that act as a digital police force. These layers check every agent’s decision against laws like GDPR or internal risk limits.

For high-stakes tasks, the system triggers a “human-in-the-loop” approval process. Furthermore, every thought process and action is recorded in an immutable audit trail. As a result, the bank remains fully compliant while benefiting from the speed of automation.

By investing in this specific architecture, leaders ensure their AI isn’t just a pilot project. They are building a scalable, secure foundation that will define how their bank operates for the next decade.

Compliance and Risk in Agentic AI Systems

Trust remains the most valuable asset in banking. As systems move from suggesting actions to executing them, the burden of proof for safety increases. Transitioning to agentic AI requires a sophisticated approach to risk that satisfies both internal stakeholders and global regulators.

1. Regulatory Challenges in Autonomous Systems

Financial regulators are currently recalibrating for a “digital reset” in 2026. New frameworks, such as the EU AI Act, are creating a complex patchwork of requirements for autonomous agents.

The primary challenge is that agents operate at machine speed, while traditional regulation is designed for human-speed oversight.

- Data Sovereignty: Agents must navigate strict rules regarding where data is processed and stored across borders.

- Algorithmic Bias: Regulators demand proof that autonomous decisions in lending do not discriminate against protected groups.

- Liability Frameworks: If an agent makes an error, the institution must have a clear legal path for accountability.

Therefore, banks must ensure that their agents are built with compliance as their core programming. Failing to align with these evolving laws can turn a high-tech asset into a massive legal liability.

2. Explainability in AI-Driven Decisions

Regulators and clients alike demand to know why a specific decision was made. “Black box” AI, where the logic is hidden, is no longer acceptable in enterprise banking. Agentic systems must provide multi-level explainability to satisfy different audiences.

- Customer-Facing Logic: The AI must explain a loan denial in plain, non-technical language.

- Technical Logic: Developers need to see the specific data weights and model versions used for a trade.

- Strategic Logic: Executives must understand how an agent’s goal aligned with the bank’s risk appetite.

By making AI outputs explainable, leaders can build the necessary trust with boards and external agencies. In addition, this transparency helps identify and remove hidden biases before they impact the business.

3. Full Audit Trails and Traceability

In an autonomous environment, every action taken by an agent must leave a permanent digital trail. This level of traceability is essential for defending against enforcement actions or internal errors.

- Immutable Logs: Systems record every data point an agent accessed before making a decision.

- Version Control: The bank can prove which version of an AI model was active during a specific transaction.

- Execution Mapping: Every API call and fund movement is timestamped and linked to a specific goal.

Furthermore, governance architecture now serves as evidence of “best efforts” in cybersecurity. Thus, a robust logging system is not just a feature; it is a legal shield for the enterprise.

4. Governance Models for AI Agents

Effective governance for 2026 moves beyond simple policy documents into technical “runtime” enforcement. This means the system uses digital guardrails to block prohibited actions before they happen.

- Tiered Autonomy: Agents receive more power only after proving their reliability in low-risk environments.

- Human-in-the-Loop: High-value transactions automatically trigger a manual review by a senior officer.

- System Circuit Breakers: Automatic “kill switches” stop an agent if its behavior deviates from expected patterns.

Consequently, the enterprise maintains control over its digital workforce. Strategic risk management allows a bank to innovate without fear. By hard-coding compliance into the system, you ensure that your autonomous workforce always works within the safe boundaries of the law.

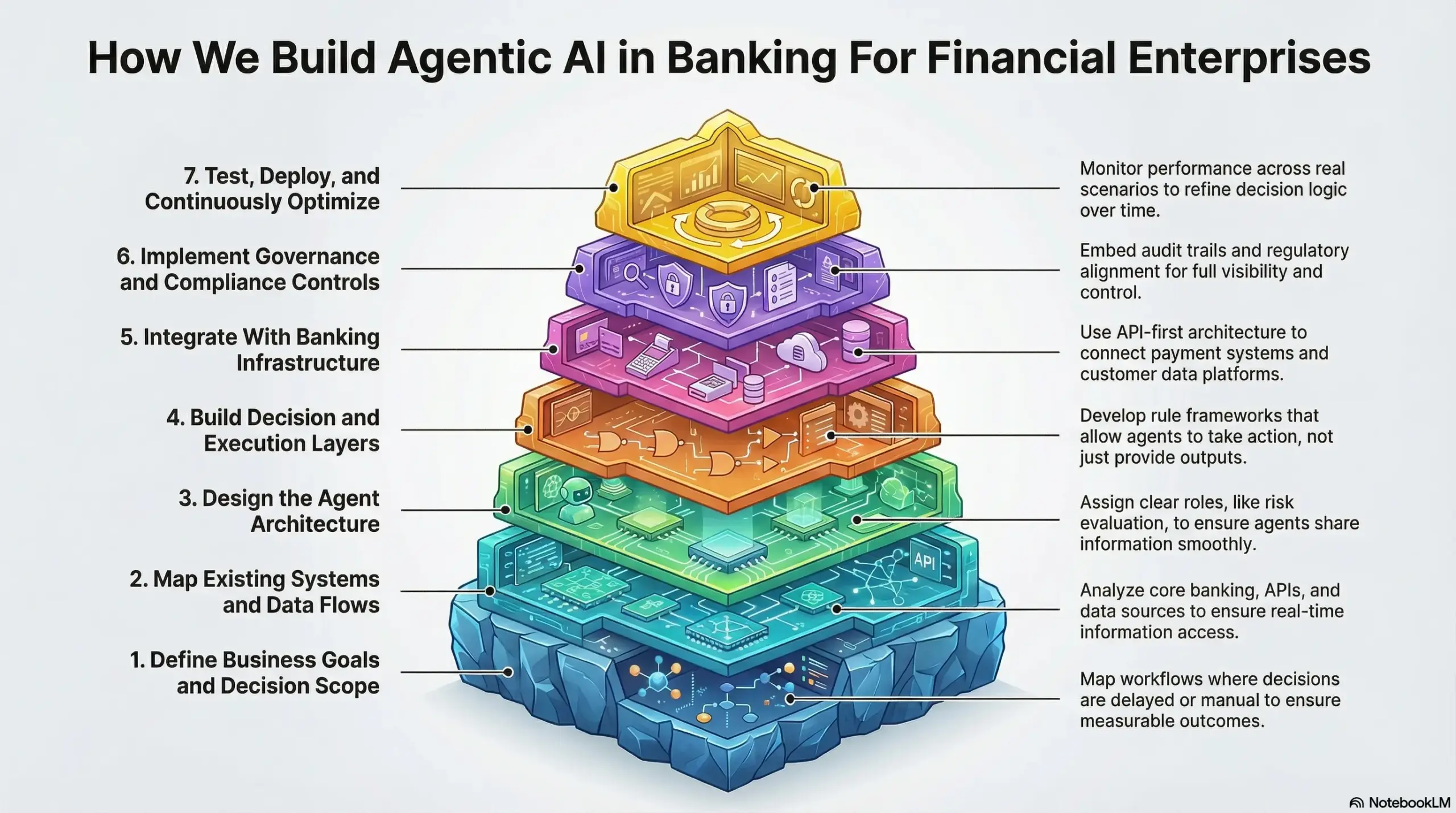

How We Build Agentic AI in Banking For Financial Enterprises

At Intellivon, we build agentic AI systems as core financial infrastructure. The goal is not to add AI on top of existing tools.

Instead, we design systems that connect data, decisions, and execution across banking workflows. This approach helps enterprises move from fragmented operations to fully coordinated systems. As a result, teams gain speed, control, and long-term scalability.

1. Define Business Goals and Decision Scope

We start by understanding what the system needs to achieve. This includes identifying key workflows such as fraud detection, underwriting, or compliance monitoring. We map where decisions are delayed or handled manually today.

This step ensures the system is built around real business impact. Therefore, every agent is aligned with measurable outcomes from the beginning.

2. Map Existing Systems and Data Flows

Next, we analyze the current technology landscape. This includes core banking systems, APIs, data sources, and third-party tools. We identify gaps, bottlenecks, and integration challenges.

This step is critical because agentic AI depends on connected data. As a result, we ensure the system has access to accurate, real-time information.

3. Design the Agent Architecture

We design a system of goal-driven agents based on the workflows identified. Each agent is assigned a clear role, such as risk evaluation or transaction monitoring. We also define how these agents interact and share information.

This creates a structured system rather than isolated components. Therefore, decisions can flow smoothly across the entire operation.

4. Build Decision and Execution Layers

At this stage, we develop the core logic of the system. This includes decision engines, rule frameworks, and execution pathways. We ensure that agents can take actions, not just provide outputs.

This is where the system moves beyond traditional AI. As a result, workflows become faster and require less manual intervention.

5. Integrate With Banking Infrastructure

We connect the system with existing banking platforms using API-first architecture. This includes integration with payment systems, risk engines, and customer data platforms. We ensure minimal disruption to ongoing operations.

This step allows the system to function in real-world environments. Therefore, enterprises can scale without replacing their entire infrastructure.

6. Implement Governance and Compliance Controls

We embed audit trails, monitoring systems, and explainability into the platform. Every decision and action is recorded and traceable. We also align the system with regulatory requirements.

This ensures the system operates within financial standards. At the same time, leadership gains full visibility and control.

7. Test, Deploy, and Continuously Optimize

Finally, we test the system across real scenarios and edge cases. After deployment, we monitor performance and refine decision logic over time. The system continues to learn from outcomes and feedback.

This ongoing improvement ensures long-term value. As a result, the platform evolves with changing business needs and market conditions.

Agentic AI in banking is not built through isolated models or quick integrations. It requires a structured approach that connects goals, systems, and execution into one environment. Each step plays a role in turning fragmented workflows into coordinated operations.

At Intellivon, the focus remains on building systems that work in real enterprise conditions. As a result, financial institutions gain faster decision-making, reduced manual effort, and stronger operational control. This is how agentic AI moves from concept to measurable impact.

Cost to Build Agentic AI in Banking

Building agentic AI in banking depends on how deeply the system integrates with existing operations. A simple workflow automation layer costs less. However, a fully integrated, multi-agent system requires more investment.

For most financial enterprises, the cost typically falls between $50,000 and $150,000. This range covers system design, development, integration, and initial deployment. The final cost depends on complexity, data readiness, and compliance requirements.

Below is a realistic cost breakdown based on enterprise implementations.

Estimated Cost Breakdown

| Component | Description | Estimated Cost |

| Strategy and Planning | Workflow analysis, goal definition, and architecture planning | $5,000 – $10,000 |

| Data Integration | Connecting core banking systems, APIs, and data pipelines | $10,000 – $25,000 |

| Agent Development | Building decision agents and workflow logic | $15,000 – $35,000 |

| Orchestration Layer | Multi-agent coordination and communication systems | $8,000 – $20,000 |

| UI and Monitoring | Dashboards, control panels, system visibility tools | $5,000 – $15,000 |

| Compliance and Security | Audit trails, governance, and regulatory alignment | $5,000 – $15,000 |

| Testing and Deployment | QA, real-world testing, rollout support | $2,000 – $10,000 |

| Total Estimated Cost | End-to-end agentic AI system development | $50,000 – $150,000 |

Factors That Influence the Cost

Several factors can increase or reduce the overall investment.

- System complexity: More workflows and agents increase development effort

- Integration depth: Legacy systems require more customization

- Data quality: Poor data requires additional processing layers

- Compliance needs: Heavily regulated environments need stronger controls

- Scalability requirements: Higher scale demands a more robust infrastructure

ROI and Long-Term Value

While the initial investment may seem significant, the returns are often clear. Agentic AI reduces manual work, speeds up decisions, and improves accuracy. Over time, this leads to lower operational costs and better efficiency.

As a result, many enterprises recover their investment quickly. More importantly, they gain a system that continues to improve and scale with their business.

Talk to Intellivon’s team today to get a precise cost estimate built around your enterprise needs.

Conclusion

Agentic AI in banking is shifting how financial operations are designed and executed. It connects data, decisions, and actions into one continuous system. As a result, banks move faster, reduce manual effort, and improve control across workflows.

Those who invest early will build stronger, more scalable operations. With the right approach, agentic AI becomes a foundation for long-term efficiency, resilience, and growth across enterprise banking systems.

Build Agentic AI Systems With Intellivon

At Intellivon, agentic AI systems are built as financial infrastructure, not as isolated automation tools. The focus is to create a unified system that connects data, workflows, and execution across financial operations. As a result, enterprises move from fragmented processes to coordinated, real-time systems.

Each solution is designed around how financial operations actually run. This includes reconciliation, reporting, compliance checks, fraud monitoring, and system integrations. Everything works together within a single architecture, ensuring consistency across workflows.

Our engineering approach combines AI-driven decision systems with API-first, cloud-native architecture. This allows seamless integration with ERPs, banking systems, payment gateways, and internal platforms. Therefore, organizations can scale without disrupting existing operations.

Why Build With Intellivon

- Infrastructure-First Approach: Systems designed for long-term scale and stability

- Deep Financial Systems Expertise: Built for real-world FinOps complexity

- API-First Architecture: Smooth integration across financial ecosystems

- Compliance Built In: Audit trails, controls, and approvals from day one

- End-to-End Ownership: From design to deployment and continuous optimization

If your financial operations still rely on manual workflows and disconnected tools, the gap will continue to grow. Agentic AI offers a way to close that gap with systems that can act, adapt, and scale.

Connect with Intellivon’s experts to build an agentic AI system tailored to your enterprise operations.

FAQs

Q1. What is the use of agentic AI in banking?

A1. Agentic AI is used to handle complex banking workflows with minimal human input. It supports areas like fraud detection, compliance checks, loan processing, and customer operations. Instead of only providing insights, it can take action across systems. As a result, banks reduce manual work and speed up decisions. In addition, teams gain better control over operations that usually require multiple handoffs.

Q2. What is the agentic AI strategy for enterprises?

A2. An effective agentic AI strategy focuses on building systems, not isolated use cases. Enterprises start by identifying high-impact workflows where decisions are slow or manual. Then, they design agent-driven systems that connect data, decision-making, and execution. This approach ensures long-term scalability. Therefore, instead of running pilots, organizations build infrastructure that supports continuous automation and growth.

Q3. Which banks are using agentic AI?

A3. Many large banks are exploring or adopting agentic AI in areas like risk, fraud, and operations. Global institutions are using it to automate compliance checks, monitor transactions, and improve decision-making speed. While full-scale adoption is still evolving, early movers are already testing multi-agent systems in production environments. As a result, adoption is expected to grow rapidly across enterprise banking.

Q4. How is agentic AI used today?

A4. Today, agentic AI is used in workflows that require speed and coordination. This includes fraud investigation, KYC processes, loan approvals, and transaction monitoring. These systems can manage multiple steps without constant human input. As a result, operations become faster and more consistent. In addition, banks can respond to risks and opportunities in real time across their systems.