Financial compliance used to focus on documentation. Today, it centers on data. Regulations like AML, KYC, MiFID II, and Basel IV create thousands of obligations for every transaction, customer interaction, and reporting cycle. Compliance teams in fintech enterprises struggle with the workload, and this is because the massive scale of modern financial operations cannot be reviewed alone by humans.

Rule-based automation has helped, but only to a certain point. It manages what you already expect. When a regulation changes, a new risk pattern appears, or a cross-border obligation shifts, those systems get stuck. Someone needs to rewrite the rules manually, and by then, the exposure window is already open. Agentic AI for compliance automation works differently. It does not wait for instructions. Instead, it monitors, interprets, and acts in real time, adjusting as conditions change. For financial companies facing growing regulatory pressure, this is where the real operational advantage lies.

At Intellivon, we build these enterprise-grade AI agents for high-stakes financial environments. This blog draws from that hands-on experience to show you exactly how agentic AI works inside compliance operations, where it delivers the most impact, and what it takes to implement it at scale.

Why Compliance Teams Need Agentic AI Now

Compliance teams face growing regulatory pressure and heavy manual workloads. As a result, agentic AI enables autonomous monitoring, faster adaptation, and real-time risk control. It helps enterprises scale compliance efficiently while improving accuracy and delivering measurable ROI across fintech and healthcare.

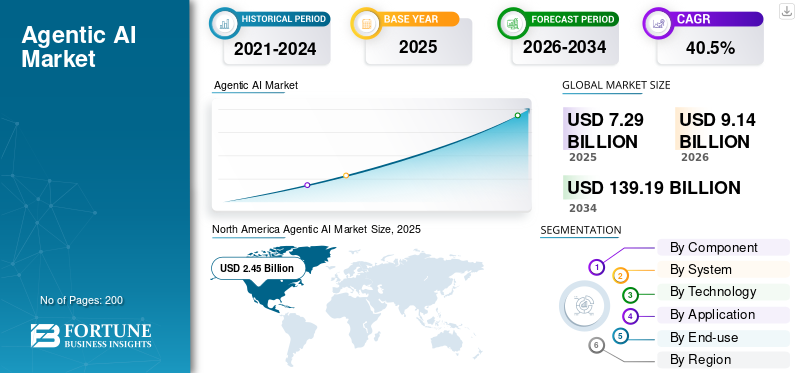

The global agentic AI market reached USD 7.29 billion in 2025. It is expected to grow to USD 139.19 billion by 2034, at a 40.50% CAGR. North America led the market in 2025, holding a 33.60% share.

The financial sector has reached a tipping point where traditional oversight can no longer keep pace with the speed of digital transactions. Agentic AI provides the necessary evolution from passive software to autonomous systems that act with intent and precision.

1. Rising regulatory pressure across financial systems

Global financial institutions currently navigate a labyrinth of evolving mandates, from updated AML (Anti-Money Laundering) directives to complex cross-border data privacy laws. Regulatory bodies now expect granular, real-time transparency into every transaction.

This shift places an immense burden on institutions to prove their integrity instantly. Consequently, the volume of required documentation has scaled beyond what human teams can feasibly manage without specialized technical assistance.

2. Limits of manual and rule-based compliance systems

Standard rule-based software operates on “if-then” logic, which fails when encountering the nuanced patterns of modern financial fraud. These systems often trigger excessive false positives, forcing human analysts to waste hours on non-threats.

Furthermore, manual intervention is slow and inherently prone to fatigue-related oversights. When a system cannot learn or adapt to new tactics used by bad actors, it becomes a liability rather than a shield. Static rules simply cannot counter the dynamic nature of sophisticated financial crimes.

3. Cost of delays, errors, and audit failures

In the enterprise world, a single compliance error can result in multi-million dollar fines and irreparable brand damage. Beyond the direct financial penalties, audit failures often lead to restrictive operational mandates from regulators. These delays in clearing transactions or onboarding clients directly impact the bottom line by stalling capital flow.

Therefore, the cost of maintaining an inefficient system is often higher than the investment required to modernize it. Precision is no longer a luxury; it is a fundamental requirement for maintaining market trust.

4. Need for real-time, autonomous compliance execution

Agentic AI moves beyond simple automation by making informed decisions within pre-defined ethical and legal boundaries. These agents can monitor vast data streams, identify anomalies, and take corrective action immediately without waiting for human triggers.

For instance, an agent could freeze a suspicious account and simultaneously draft a SAR (Suspicious Activity Report) for review. This shift toward autonomous execution ensures that compliance is a proactive force rather than a reactive one. It allows organizations to scale their operations globally without a linear increase in headcount.

Transitioning to agentic systems allows your organization to turn a defensive cost center into a streamlined, strategic asset. By removing the friction of manual oversight, you empower your leadership to focus on expansion rather than damage control.

What Agentic AI Means in Financial Compliance

Agentic AI represents a shift from passive automation to goal-oriented reasoning. Unlike basic bots, these agents understand regulatory intent. They can plan tasks, use financial tools, and self-correct during complex workflows.

This technology manages end-to-end processes like identity verification or risk scoring autonomously. Therefore, it acts as a digital compliance officer. It bridges the gap between static data and decisive, real-time regulatory action for the modern enterprise.

Difference Between AI Tools and AI Agents

AI is widely used in compliance today. However, most implementations still rely on tools that assist human teams, not systems that act independently. This is where the shift to agentic AI becomes critical.

AI tools analyze data and generate outputs. In contrast, AI agents go further. They make decisions, trigger actions, and manage workflows autonomously. For enterprise compliance, this difference directly impacts scalability, speed, and operational efficiency.

AI Tools vs AI Agents in Compliance

| Aspect | AI Tools | AI Agents |

| Role | Assist human decision-making | Execute decisions autonomously |

| Function | Analyze data and generate insights | Monitor, decide, and act on compliance workflows |

| Dependency | Requires manual intervention | Operates with minimal human input |

| Workflow ownership | Humans manage workflows | Agents manage end-to-end workflows |

| Speed | Limited by human response time | Real-time execution and response |

| Adaptability | Static or rule-based updates | Continuously learns and adapts |

| Integration | Works as a layer on systems | Interacts across systems via APIs |

| Use in compliance | Flagging alerts, reporting | Handling alerts, triggering actions, reporting |

| Scalability | Limited by team capacity | Scales across systems and transactions |

| Auditability | Partial traceability | Full decision traceability with logs |

What This Means for Enterprise Compliance

The shift from AI tools to AI agents is architectural. This is because AI tools improve efficiency, but they still depend on human workflows. As a result, compliance teams remain constrained by manual processes and delays.

AI agents, on the other hand, take ownership of compliance operations. They monitor transactions, evaluate risks, trigger actions, and maintain audit trails in real time. This allows enterprises to move from reactive compliance to continuous, automated compliance execution at scale.

In short, AI tools support compliance, while AI agents run it.

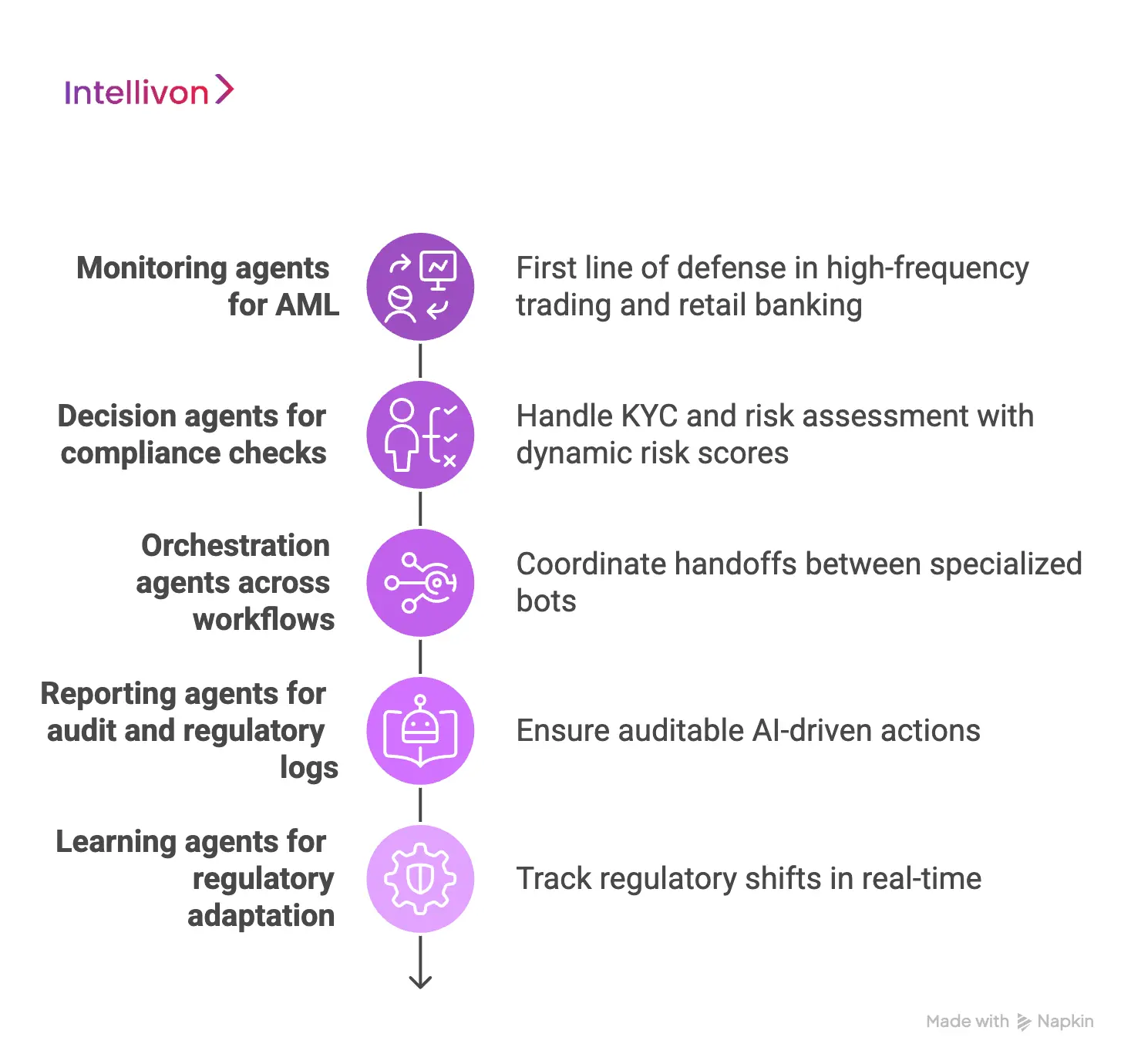

Types of AI Agents in Compliance Systems

Modern compliance infrastructure is transitioning from monolithic software to a decentralized ecosystem of specialized agents. Each agent type focuses on a specific regulatory pillar, ensuring that no single point of failure disrupts the enterprise.

This modular approach allows for greater scalability and precision in high-stakes environments.

1. Monitoring agents for AML

Anti-Money Laundering (AML) monitoring agents act as the first line of defense in high-frequency trading and retail banking. Unlike traditional filters, these agents analyze multi-dimensional data points, including geographic velocity and hidden counterparty links.

They identify “mule” activity and sophisticated layering techniques that standard rules often miss. Therefore, they significantly reduce false positives by understanding the context of a transaction rather than just the amount. This precision ensures that legitimate capital flows remain uninterrupted while high-risk activity is flagged for immediate review.

2. Decision agents for compliance checks

Decision agents are engineered to handle the “gray areas” of Know Your Customer (KYC) and risk assessment. These agents evaluate vast datasets, from adverse media mentions to complex beneficial ownership structures, to assign a dynamic risk score.

They weigh the evidence against institutional risk appetite and regulatory thresholds. By automating the initial adjudication process, they allow human experts to focus only on the most complex escalations. Consequently, onboarding times are slashed from weeks to hours, providing a tangible competitive advantage in client acquisition.

3. Orchestration agents across workflows

Orchestration agents serve as the “brain” of the compliance ecosystem, coordinating the handoffs between other specialized bots. In a typical workflow, an orchestration agent might trigger a monitoring agent’s alert, route the findings to a decision agent, and then notify the legal team.

They manage the state and memory of these interactions to ensure nothing falls through the cracks. This high-level coordination prevents data silos and ensures a unified response to potential threats. For the enterprise, this means a cohesive, end-to-end automation strategy that scales without adding operational friction.

4. Reporting agents for audit and regulatory logs

Transparency is the cornerstone of trust in finance, and reporting agents ensure every AI-driven action is fully auditable. These agents maintain “reasoning logs” that explain exactly why a particular decision was made or an alert was triggered.

When a regulatory inquiry arrives, these agents can instantly compile comprehensive reports that meet the specific formatting requirements of bodies like FinCEN or the SEC. This proactive documentation eliminates the frantic “audit prep” cycles that often plague financial firms. Strategic leaders benefit from a continuous state of audit-readiness, protecting the firm’s license to operate.

5. Learning agents for regulatory adaptation

The regulatory landscape is in a constant state of flux, and learning agents are designed to track these shifts in real-time. These agents monitor updates from global registries, news outlets, and legislative bodies to identify new compliance requirements.

They can simulate how a new law might impact current workflows and suggest necessary adjustments to the underlying logic of other agents. This ensures that the compliance system evolves as quickly as the laws themselves. By automating regulatory intelligence, firms can pivot their strategies rapidly without the traditional delays of manual legal review

Building a multi-agent architecture ensures that your compliance program is not just a checkbox, but a resilient, self-improving engine. This structure provides the flexibility to adapt to new market demands while maintaining the rigorous standards expected by global regulators.

How AI Agents Automate Compliance Workflows

The true power of Agentic AI lies in its ability to handle “unstructured” decision-making. While legacy automation follows a straight line, AI agents can navigate curves, loops, and obstacles in a workflow.

This shift transforms compliance from a series of manual hurdles into a fluid, self-managing stream.

1. Replacing manual compliance checks with agents

High-level due diligence often involves searching through disparate databases, news archives, and international watchlists. Traditionally, analysts spend 60% of their time simply gathering this data. AI agents automate this by:

- Autonomous Data Retrieval: Agents connect to various APIs to pull real-time data on entities.

- Contextual Analysis: They read and interpret news articles to identify genuine “adverse” mentions versus irrelevant noise.

- Identity Resolution: Agents can cross-reference multiple data points to verify that a “John Doe” in one database is the same individual in another. Therefore, the agent delivers a finished dossier rather than a pile of raw data, allowing leaders to make faster, informed decisions.

2. Automating alert handling and escalation flows

The “alert fatigue” phenomenon is a significant risk factor in modern banking. Thousands of transactions trigger flags every hour, most of which are false positives. Agentic AI addresses this by acting as a sophisticated triage layer. When a flag is raised, an agent immediately investigates the transaction’s history and the user’s typical behavior.

If the activity is low-risk, the agent clears the alert and logs the reasoning. However, if the risk is substantiated, it gathers all necessary evidence and pushes the case to the senior legal team. This ensures that human experts only deal with high-value threats.

3. Real-time compliance execution without delays

In the world of instant payments and crypto-assets, a five-minute delay is too long. Agentic AI functions at the speed of the network, processing compliance checks in milliseconds.

- Instant Verification: KYC and KYB checks happen during the session, not after.

- Dynamic Blocking: If a transaction violates a specific sanction, the agent blocks it instantly.

- Automated Messaging: The agent can communicate with the client to request missing documentation in real-time. This eliminates the “pending” state that often frustrates customers and stalls business operations. In addition, it ensures the firm is never out of compliance, even for a second.

4. Reducing operational overhead in compliance teams

Operational costs in finance are heavily weighted toward the maintenance of large “back-office” teams. Agentic AI allows for a radical restructuring of these expenses. By automating the repetitive elements of investigation and reporting, firms can reduce the physical infrastructure required to support these teams.

Furthermore, the accuracy of AI agents reduces the “re-work” caused by human error in data entry or form filing. Consequently, capital can be redirected from administrative upkeep to core product innovation and market expansion.

5. Scaling compliance without increasing headcount

For an enterprise looking to enter new markets, the traditional hurdle is the cost of hiring local compliance experts. Agentic AI breaks the linear relationship between business volume and employee count.

- Global Portability: Agents can be programmed with the regulatory rules of different jurisdictions (e.g., GDPR in Europe, CCPA in California).

- 24/7 Operation: Agents do not have shifts; they provide consistent oversight across all time zones simultaneously.

- Elastic Capacity: During high-volume events, the AI scales its processing power instantly without needing new hires. This elasticity allows an organization to double its transaction volume without doubling its compliance payroll. It provides a strategic lever for growth that was previously impossible.

By integrating these agents, your enterprise moves from a reactive posture to a proactive one. You gain the ability to scale rapidly, knowing that your digital “guardians” are evolving alongside your business.

Where Agents Fit Across Compliance Workflows

Deploying agentic AI lies in their strategic integration into existing pipelines. These agents act as intelligent connective tissue, filling the gaps where data usually stalls or requires human intervention.

By placing agents at critical nodes, an enterprise can transform fragmented processes into a unified, high-velocity compliance engine.

1. KYC and onboarding compliance workflows

The “Know Your Customer” (KYC) process is often the first point of friction for new high-value clients. Agentic AI streamlines this by managing the entire verification lifecycle. An agent can ingest a client’s documents, verify their authenticity against government databases, and perform biometric liveness checks in seconds.

Furthermore, it can perform “Deep Web” searches for UBO (Ultimate Beneficial Ownership) structures that are often hidden in shell companies. This reduces the time-to-revenue for new accounts. Therefore, the onboarding experience becomes a competitive advantage rather than a bureaucratic deterrent.

2. AML monitoring and alert management workflows

Anti-Money Laundering (AML) efforts often fail because they lack the context of a customer’s “normal” behavior. AI agents solve this by maintaining a long-term memory of user patterns. When a transaction triggers a flag, the agent conducts an immediate investigation. It looks at the history, the counterparty’s risk profile, and current global sanctions lists.

If the agent determines the risk is negligible, it auto-resolves the alert with a detailed justification log. In addition, this triage ensures that your most expensive human assets are not bogged down by repetitive, low-risk false positives.

3. Transaction screening and fraud checks

In high-frequency financial environments, screening must happen in the “hot path” of the transaction. Agents are uniquely suited for this because they can make complex decisions with minimal latency.

- Velocity Checks: Agents monitor how quickly funds are moving across accounts to detect “smurfing” or rapid layering.

- Geospatial Analysis: They verify if the transaction location aligns with the user’s known travel patterns or digital footprint.

- Behavioral Biometrics: Agents can even detect if the way a user interacts with an app suggests a “takeover” by a bot or a malicious actor. By catching these issues before the funds leave the institution, the agent prevents the massive costs associated with clawbacks and fraud losses.

4. Regulatory reporting and audit workflows

Reporting is the most labor-intensive part of compliance, often requiring weeks of data consolidation. Reporting agents eliminate this “crunch” by maintaining a continuous, machine-readable log of every decision made within the system.

- Automated SAR Filing: When a suspicious activity is confirmed, the agent drafts the Suspicious Activity Report (SAR) automatically.

- Data Mapping: It translates internal data into the specific XML or JSON formats required by different global regulators.

- Reasoning Transparency: Every report includes a “chain of thought” explaining the AI’s logic, ensuring total transparency during an audit. This proactive approach ensures that the firm is always ready for a “surprise” inspection without needing to halt regular business operations.

5. Continuous compliance monitoring across systems

Compliance is a 24/7 requirement. Continuous monitoring agents act as “always-on” sentinels that watch for changes in both the market and the firm’s internal state. If a long-time client suddenly appears on a new sanctions list, the agent detects it instantly and freezes the relationship.

They also monitor internal employee communications for signs of insider trading or policy violations. Consequently, the enterprise maintains a state of “perpetual compliance.” This constant vigilance protects the board and leadership from the legal fallout of undetected systemic failures.

Real Use Cases of Compliance AI Agents

Theoretical potential is valuable, but for the enterprise, the true measure of technology lies in its application to high-stakes environments. Agentic AI is already reshaping how global firms handle the friction of regulatory oversight.

By moving from static rules to dynamic agents, organizations are achieving levels of precision that were previously physically impossible.

1. AML monitoring with autonomous AI agents

Anti-Money Laundering (AML) efforts typically struggle with a 95% false-positive rate. In contrast, an AI agent acts as an autonomous investigator. It doesn’t just see a large transfer; it analyzes the sender’s historical behavior and cross-references news for adverse data.

- Pattern Recognition: Agents identify “smurfing” or layering tactics in real-time.

- Contextual Vetting: They distinguish between legitimate high-net-worth activity and suspicious spikes. Therefore, the compliance team receives a vetted lead rather than a raw alert. This shift allows a lean team to manage the volume of a global Tier-1 bank effectively.

2. Agents executing real-time payment checks

In the era of instant payments like SEPA or FedNow, compliance must happen in milliseconds. AI agents sit directly in the payment path, evaluating every transaction before it is cleared.

- Sanctions Screening: Instant matching against OFAC and international watchlists.

- Behavioral Biometrics: Detecting account takeovers by analyzing typing speed or navigation patterns. If a match is found, the agent triggers an automated request for information (RFI) to the customer. This ensures that the flow of legitimate capital remains “frictionless” while high-risk movements are halted instantly.

3. Agents generating audit-ready compliance logs

Audit cycles are traditionally a period of high stress. Reporting agents transform this by maintaining “living” documentation. Every decision, from clearing a KYC flag to blocking a login, is recorded in a machine-readable “reasoning log.”

This log explains the why behind the action, citing specific regulatory clauses. Consequently, the firm moves from a reactive “prep” mode to a state of perpetual audit-readiness. This transparency builds immense trust with regulators and reduces the risk of massive non-compliance fines.

4. Lending compliance via decision agents

Automated lending often faces the challenge of “fair lending” regulations. Decision agents navigate this by evaluating data points while strictly adhering to anti-discrimination laws.

- Verification: Agents ingest thousands of pages of tax filings to verify debt-to-income ratios.

- Legal Disclosure: They ensure every loan offer complies with local usury laws and disclosure requirements. If a loan is rejected, the agent generates a specific “adverse action” notice that meets all legal standards. This level of automated precision allows lenders to scale their portfolios safely.

5. Cross-border compliance via agent orchestration

Operating in multiple countries means juggling conflicting regulations. Orchestration agents act as the “regulatory switchboard” for global operations. For instance, a transaction from London to Singapore requires adherence to both UK and Singaporean laws.

The orchestration agent identifies these requirements and “hires” sub-agents specialized in each jurisdiction to perform the necessary checks. This prevents “regulatory arbitrage” and protects the firm from accidental violations. In addition, it allows for rapid expansion into new territories without a massive local compliance infrastructure.

Implementing these use cases converts compliance from a “necessary evil” into a strategic growth driver. When your systems can handle the complexity of global regulations autonomously, you gain the freedom to innovate at the speed of the market.

Laws and Frameworks Financial AI Agents Must Support

For an enterprise leader, the value of Agentic AI is inextricably linked to its ability to navigate a fragmented legal landscape. As of 2026, the regulatory environment is defined by a “great divergence”, where some regions centralize authority while others deregulate to spur innovation.

AI agents must be programmed with the intelligence to recognize these shifts and apply the “highest common denominator” approach to minimize cross-border risk.

1. AML and KYC regulations across jurisdictions

Anti-Money Laundering (AML) and Know Your Customer (KYC) mandates remain the primary focus of global financial supervisors.

The emergence of the European Anti-Money Laundering Authority (AMLA) as a central supervisor in 2026 has standardized expectations across the EU. Agents must now support the Anti-Money Laundering Regulation (EU 2024/1624), which removes national loopholes.

- Customer Due Diligence (CDD): Agents must perform real-time verification of beneficial owners.

- Expanded Perimeter: New 2026 rules bring real estate agents and lawyers into the AML fold; agents must adapt to these new “obliged entities.”

- Explainability: Regulators now demand that AI systems provide a clear rationale for every flagged transaction to prevent “black box” compliance.

2. FATF guidelines and risk-based compliance

The Financial Action Task Force (FATF) 40 Recommendations continue to be the gold standard for global compliance. In early 2026, FATF introduced new strategic reports specifically targeting cyber-enabled fraud and virtual asset risks.

AI agents must operate on a “Risk-Based Approach” (RBA), which requires:

- Dynamic Risk Scoring: Automatically adjusting a client’s risk level based on emerging threats or “grey list” updates (e.g., changes from the February 2026 FATF Plenary).

- Proportionate Controls: Applying stricter scrutiny to high-risk PEPs (Politically Exposed Persons) while maintaining simplified flows for low-risk entities.

- Continuous Monitoring: Unlike periodic reviews, agents must provide “always-on” oversight to detect changes in transaction patterns instantly.

3. GDPR and data privacy requirements

The General Data Protection Regulation (GDPR) has entered a more aggressive enforcement phase regarding AI. In 2026, over 80% of enterprises are expected to use GenAI, making “Privacy by Design” a mandatory architectural choice.

- Automated Data Mapping: Agents must create detailed inventories of where personal data flows through an organization.

- Right to Explanation: Under GDPR, individuals have the right to know why an automated decision was made; agents must generate these justifications on demand.

- Cross-Border Restrictions: Agents must flag and potentially block data transfers to jurisdictions that do not meet EU adequacy standards. By automating these privacy workflows, firms avoid the “human error” that leads to the massive fines seen in recent years.

4. PCI DSS for payment compliance systems

As of March 31, 2025, the “best practice” requirements of PCI DSS 4.0.1 became mandatory for all entities handling cardholder data. AI agents in the payment path must support these updated security controls.

- Multi-Factor Authentication (MFA): Agents must monitor and log all administrative access to the Cardholder Data Environment (CDE).

- Keyed Cryptographic Hashes: Agents must manage the integrity of Primary Account Numbers (PAN) using updated encryption standards.

- Vulnerability Monitoring: Systems must conduct quarterly scans and maintain tamper-resistant logs. Furthermore, agents help maintain the “segmentation” required to keep the CDE isolated from other business networks, significantly reducing the scope of annual audits.

5. Regional regulations across the US, EU, and APAC

Navigating 2026 requires understanding the distinct postures of major markets. The US is moving toward a more structured regime for digital assets through the Digital Asset Market Clarity Act (CLARITY) and the GENIUS Act for stablecoins.

- US Market: Focus is shifting from enforcement-led oversight to a framework that integrates tokenization and stablecoins into the regulated banking system.

- APAC Region: Singapore and Hong Kong continue to lead with high-expectation regimes, particularly for Virtual Asset Service Providers (VASPs).

- UK/EU: The focus remains on operational resilience and systemic interconnectedness between banks and non-bank financial institutions. Therefore, an orchestration agent is essential to “switch” between these regional rulesets as a transaction moves globally.

Relying on legacy, manual processes to manage these global shifts is no longer a viable strategy for growth. By embedding these frameworks directly into your AI’s “logic core,” you ensure that your enterprise remains resilient, regardless of which way the regulatory wind blows.

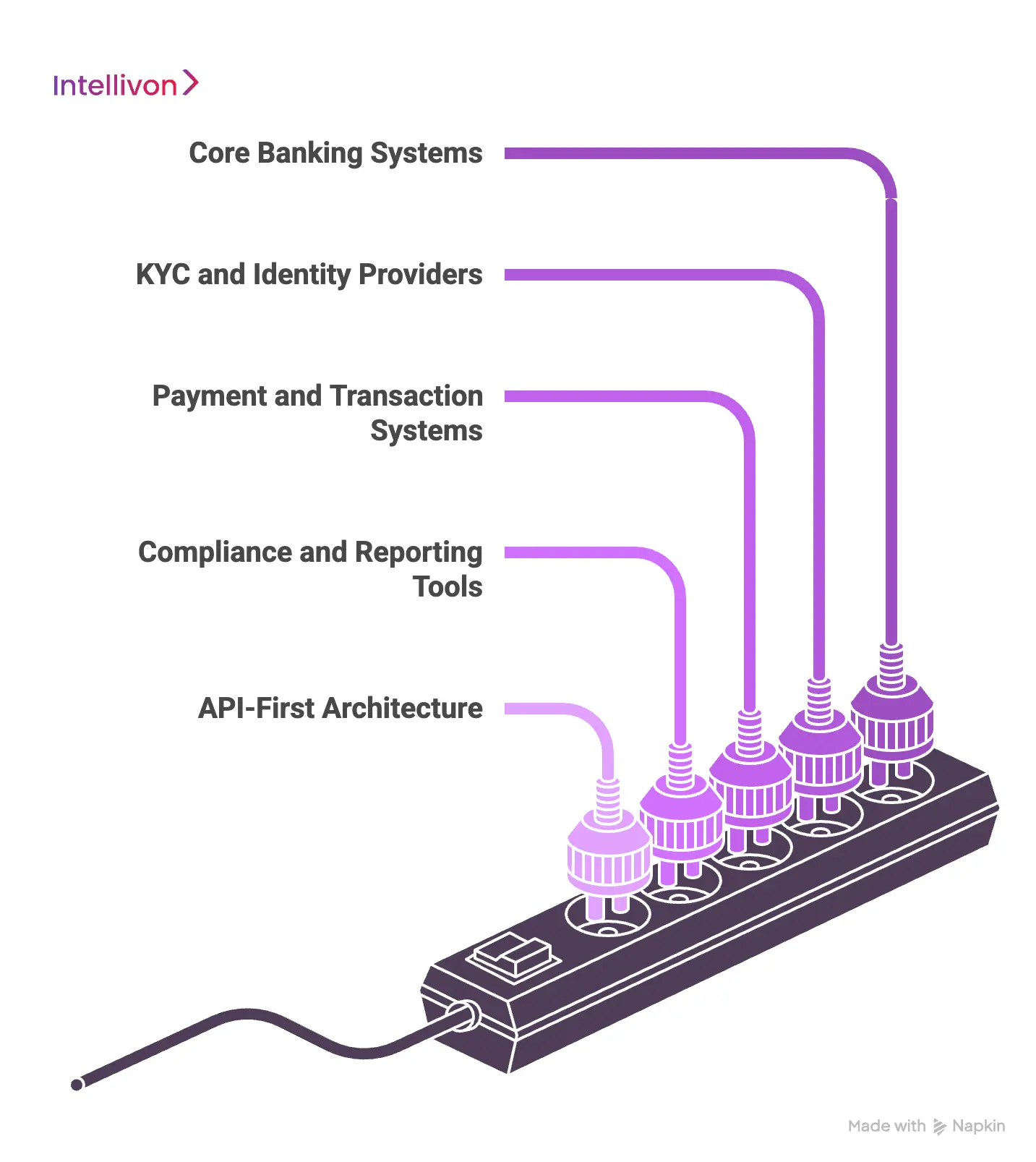

How Agents Integrate With Financial Systems

For an enterprise to transition from manual oversight to autonomous compliance, the underlying architecture must be resilient. Modern AI agents function as an intelligent “overlay” across your existing technology stack.

By creating a unified data environment, these agents can act with the same authority and context as a seasoned compliance officer.

1. Integration with core banking systems

The core banking system (CBS) is the foundational ledger of any financial institution. In 2026, the trend has shifted toward “thin cores” that decouple transaction processing from business logic.

- Real-Time Data Access: Agents connect to the CBS via high-speed data streams to monitor account balances and ledger entries.

- Automated Remediation: If a compliance breach is detected, the agent can trigger a “hold” status directly within the core system.

- Scalable Interoperability: This integration allows banks to plug in new AI capabilities without performing risky, multi-year system overhauls. Therefore, the AI agent becomes the new operating layer that orchestrates end-to-end services, from retail deposits to corporate lending.

2. Connecting with KYC and identity providers

Identity is the perimeter of modern finance. AI agents act as the orchestrator between your internal systems and third-party identity verification (IDV) services.

- Biometric Sync: Agents pull data from facial recognition providers to match live selfies against government-issued IDs.

- Database Cross-Referencing: They query global watchlists and PEP (Politically Exposed Person) databases in parallel.

- Document Parsing: Agents use advanced extraction to validate data from passports and utility bills with 99% accuracy. Consequently, the time required to “know” a customer drops from days to seconds. This seamless connection ensures that your growth isn’t throttled by manual data entry or fragmented verification steps.

3. Monitoring payment and transaction systems

Transaction monitoring happens in the “hot path” of the payment.

- Anomaly Detection: Agents identify subtle spikes in rejection rates or provider outages that human teams often miss.

- Autonomous Optimization: In 2026, leading platforms like Yuno use agents to adjust routing rules instantly, ensuring high approval rates.

- Cost Management: Agents analyze interchange fees at the transaction level to optimize for both performance and cost. By monitoring these systems 24/7, agents ensure that your payment rails are not only compliant but also commercially efficient.

4. Syncing with compliance and reporting tools

The final stage of any compliance workflow is the documentation of truth. Reporting agents sync directly with tools like NetSuite, Salesforce, and regulatory portals to ensure alignment. They categorize financial data into sections required by IFRS or GAAP.

Furthermore, they organize control evidence into “audit-ready” folders, summarizing why specific risks were mitigated. In addition, this synchronization eliminates the frantic “end-of-quarter” rush, replacing it with a continuous stream of accurate, pre-verified filings.

5. API-first architecture for agent execution

In 2026, the industry has moved from “API-first” to “API-native” platform design. This means your infrastructure is built with the assumption that the primary consumer is an AI agent, not a human.

- Actionable Interfaces: APIs are no longer just data endpoints; they are “action surfaces” that agents can call to execute trades or block accounts.

- Fine-Grained Authorization: Security is managed through contextual, policy-driven models that restrict what an agent can do based on its specific task.

- Standardized Contracts: Using FAPI (Financial-grade API) standards ensures that your agent can securely talk to any other regulated system in the world. This architecture provides the structural stability needed for long-term evolution, allowing you to swap out AI models or add new agents without breaking your core workflows.

By focusing on these integration points, you move beyond “pilot” projects and into production-scale AI. Your compliance infrastructure becomes a dynamic, interconnected web that supports rapid innovation while maintaining an ironclad grip on regulatory safety.

Architecture of Agentic Compliance Systems

To move from a simple automation bot to a sophisticated AI agent, an enterprise must rethink its technical foundation. A robust architecture ensures that the AI doesn’t just act, but acts with context, safety, and accountability.

By layering these capabilities, organizations can build a “ubiquitous agent fabric” that spans every department while maintaining a single source of regulatory truth.

1. Data layer for compliance and governance

The foundation of any agentic system is a unified, real-time data layer that merges operational and analytical streams. In 2026, leading firms have moved away from fragmented silos toward a “governed data fabric” that feeds high-quality, timely information to agents.

- Metadata Foundation: Accurate sensitivity labels and ownership lineage ensure agents understand the “privacy context” of the data they access.

- Vector Embeddings: Regulatory handbooks and internal policies are converted into a searchable format, allowing agents to ground their actions in legal reality.

- Dynamic Synthesis: Unlike static databases, this layer continuously updates, providing agents with a fresh view of global sanctions and market shifts.

2. Agent layer for decision and execution

The agent layer is where the “reasoning” happens. This is the home of specialized, domain-specific workers, such as a “KYC Agent” or an “AML Investigator”, who possess the autonomy to fulfill specific financial objectives.

These agents utilize Large Action Models (LAMs) to not only suggest outcomes but to execute them across various enterprise systems.

They operate within a “Least Privilege” standard, meaning they only have the permissions necessary for their specific role. Therefore, if an agent is compromised or drifts in its logic, the blast radius is strictly contained.

3. Orchestration layer across workflows

Orchestration is the “command and control” center that coordinates multi-agent teams to solve complex, multi-step problems.

- Goal Decomposition: The orchestrator breaks a broad mission, like “onboard a corporate client”, into sub-tasks for specialized agents.

- Conflict Resolution: If a monitoring agent flags a transaction that a decision agent thinks is safe, the orchestrator manages the tie-breaking logic.

- Dynamic Routing: It reroutes tasks in real-time based on system load or agent performance, ensuring high-throughput execution without bottlenecks. This layer ensures that the individual agents work as a cohesive unit rather than a collection of disconnected scripts.

4. Integration layer with financial systems

For an agent to be effective, it must be able to “reach out” and touch the systems of record. This integration layer utilizes a “thin core” architecture, decoupling heavy transaction processing from the intelligence layer.

- API-Native Connectors: Agents use standardized financial-grade APIs (FAPI) to communicate with core banking and payment rails.

- Legacy Bridges: Specialized middleware allows modern AI agents to interact with older, monolithic systems without requiring a full rip-and-replace.

- Action Surfaces: The integration layer exposes specific functions, like “freeze account” or “generate SAR”, as actionable commands the AI can invoke securely.

5. Audit layer for traceability and control

In a regulated environment, “black box” decisions are a non-starter. The audit layer acts as the “flight recorder” of the entire agentic system, capturing every thought and action.

- Chain of Thought (CoT) Logging: The system records not just the final decision, but the step-by-step reasoning and the options the agent rejected.

- Immutable Logs: Audit data is stored in append-only, tamper-proof environments to meet strict SEC and ESMA requirements.

- Circuit Breakers: This layer monitors for “operational drift” or excessive autonomy, automatically pausing an agent if it exceeds pre-defined risk thresholds. Consequently, auditors can reconstruct the exact state of the system at any given moment, ensuring total transparency and institutional trust.

Building this multi-layered stack turns your compliance program into a living capability. It allows your organization to innovate at the speed of AI while remaining firmly rooted in the principles of governance and control. Moving to this model is the most effective way to future-proof your institution against the rising tide of regulatory complexity.

How Agents Execute Compliance Workflows

The transition from static automation to agentic execution is defined by the shift from “following recipes” to “understanding goals.” In the 2026 financial ecosystem, agents do not wait for human triggers.

Instead, they operate as persistent, goal-oriented entities that navigate the entire compliance lifecycle autonomously. This allows the enterprise to maintain a state of “perpetual readiness” without manual bottlenecks.

1. Agents ingesting data across systems

Effective compliance starts with the ability to “see” across the entire organization. Modern AI agents function as high-speed data aggregators that connect directly to disparate sources.

- Unified Visibility: Agents pull data from ERPs, banking ledgers, and identity providers simultaneously.

- Unstructured Intelligence: They process non-tabular data, such as PDFs of incorporation articles, with 99% accuracy.

- Real-time Velocity: Unlike batch processing, agents ingest information the moment a transaction is initiated. Therefore, the agent operates with a 360-degree view of every entity. This eliminates the “data gaps” that often lead to regulatory oversights.

2. Agents making context-aware decisions

Industry standards now move beyond simple “if-then” logic. Agentic systems utilize Large Action Models (LAMs) to reason through complex scenarios like a human analyst.

If a customer moves funds to a new jurisdiction, the agent evaluates the business profile and geopolitical risk.

Consequently, it distinguishes between legitimate expansion and “layering” attempts. This nuanced judgment reduces false positives by over 60%.

3. Agents triggering actions across workflows

The “agency” in AI refers to the ability to take meaningful action. Once a decision is reached, the agent executes the necessary next steps.

- Immediate Remediation: An agent can freeze a suspicious account and revoke API keys in milliseconds.

- Automated Communication: It triggers encrypted requests to clients for missing documentation, such as proof of address.

- Escalation Management: If risk exceeds a threshold, the agent compiles a pre-investigated dossier for the legal team. This proactive execution ensures that compliance is a live process.

4. Multi-agent coordination and feedback loops

Complex tasks require a “swarm” of specialized agents working in tandem. An orchestration layer coordinates these units to ensure a cohesive outcome. For example, a “KYC Agent” verifies identity while a “Reporting Agent” logs the sequence.

Furthermore, every human intervention acts as a “learning event.” Agents analyze why their decision was corrected and adjust their internal weights. This ensures that your compliance engine becomes more accurate every day.

By deploying these autonomous workflows, your organization moves to a proactive posture. You gain the ability to scale globally, confident that your digital guardians manage complexity with machine precision.

Scaling Compliance Agents in Enterprises

Moving from a pilot project to an enterprise-grade agentic ecosystem requires a shift in how infrastructure is managed. When an organization scales, the complexity of maintaining oversight grows non-linearly.

To address this, leaders must move toward a decentralized yet governed model where agents can operate across borders without sacrificing central control.

1. Handling multi-entity and multi-region compliance

Global enterprises often struggle with “regulatory fragmentation,” where the rules in Singapore differ sharply from those in the European Union. Scaling agentic AI requires a “hierarchical logic” where a global master policy is refined by local sub-agents.

- Localized Reasoning: Agents are programmed with specific regional jurisdictional data, such as the EU AI Act’s 2026 enforcement mandates.

- Entity Isolation: Data remains within its legal boundary while agents share only the high-level “compliance signals” with headquarters.

- Dynamic Adaptation: As new laws emerge, agents update their logic gates without a system-wide reboot. Therefore, your organization maintains a unified global posture while respecting the nuances of every local market.

2. Orchestrating workflows across systems and teams

At scale, the challenge is no longer about individual agent performance but about how those agents interact with human stakeholders. An orchestration layer acts as the “connective tissue” that routes tasks based on risk and expertise.

For instance, low-risk identity renewals are handled fully autonomously, while complex corporate structures are routed to senior analysts with a pre-generated agent summary. Furthermore, these systems synchronize with existing project management and communication tools.

This ensures that every automated action is visible to the relevant business units. Consequently, the enterprise avoids “automation silos” and maintains a cohesive operational flow.

3. Ensuring reliability and uptime of agent systems

In a financial environment, a five-minute outage can lead to thousands of non-compliant transactions. To ensure “five-nines” (99.999%) reliability, agentic systems utilize a “self-healing” architecture.

- Redundant Reasoning: Multiple agents evaluate the same high-stakes transaction to ensure consensus and prevent “hallucinations.”

- Circuit Breakers: If an agent encounters an “unknown unknown” or a data mismatch, the system automatically pauses that specific workflow and alerts a human supervisor.

- Predictive Maintenance: Agents monitor their own latency and error rates, proactively scaling their compute resources before a bottleneck occurs. This approach treats AI agents as critical infrastructure, ensuring they remain as stable and predictable as your core banking ledger.

4. Managing performance at enterprise scale

Performance at scale is measured by “time-to-decision” and “cost-per-action.” As transaction volumes grow, agentic systems must maintain efficiency without an exponential increase in API costs.

Organizations achieve this by using a “multi-tier” model approach. Large, complex models handle high-stakes adjudication, while smaller, faster agents manage routine data ingestion and labeling.

Furthermore, “rate limiting” and “token budgeting” prevent agents from performing redundant actions that waste resources. In addition, using a “governed data fabric” ensures that agents do not have to search the entire internet for answers, keeping their reasoning focused and fast.

5. Adapting to changing regulations globally

The 2026 regulatory landscape is defined by “The Great Divergence,” where laws are updated monthly rather than annually. Adaptive AI agents are designed to ingest these updates directly from regulatory feeds.

- Automated Impact Analysis: When a regulator like the SEC or ESMA issues a new guidance, agents simulate how it will affect current workflows.

- Versioned Compliance: The system maintains a “compliance history,” allowing you to prove you were in line with the specific rules active at any point in the past.

- Human-Verified Updates: While agents ingest the data, a human compliance officer “signs off” on the new logic before it goes live. This creates a “continuous compliance” loop, where the distance between a legal change and its operational implementation is reduced to near-zero.

By focusing on these scaling pillars, you ensure that your compliance investment grows with your business. You move away from “brute-force” human oversight toward a nimble, intelligent system that thrives on complexity rather than being paralyzed by it.

How We Build Agentic AI for Compliance Automation Systems

Deploying autonomous systems in a high-stakes financial environment requires more than just raw processing power. It demands a structured, time-tested approach that prioritizes safety, explainability, and regulatory alignment.

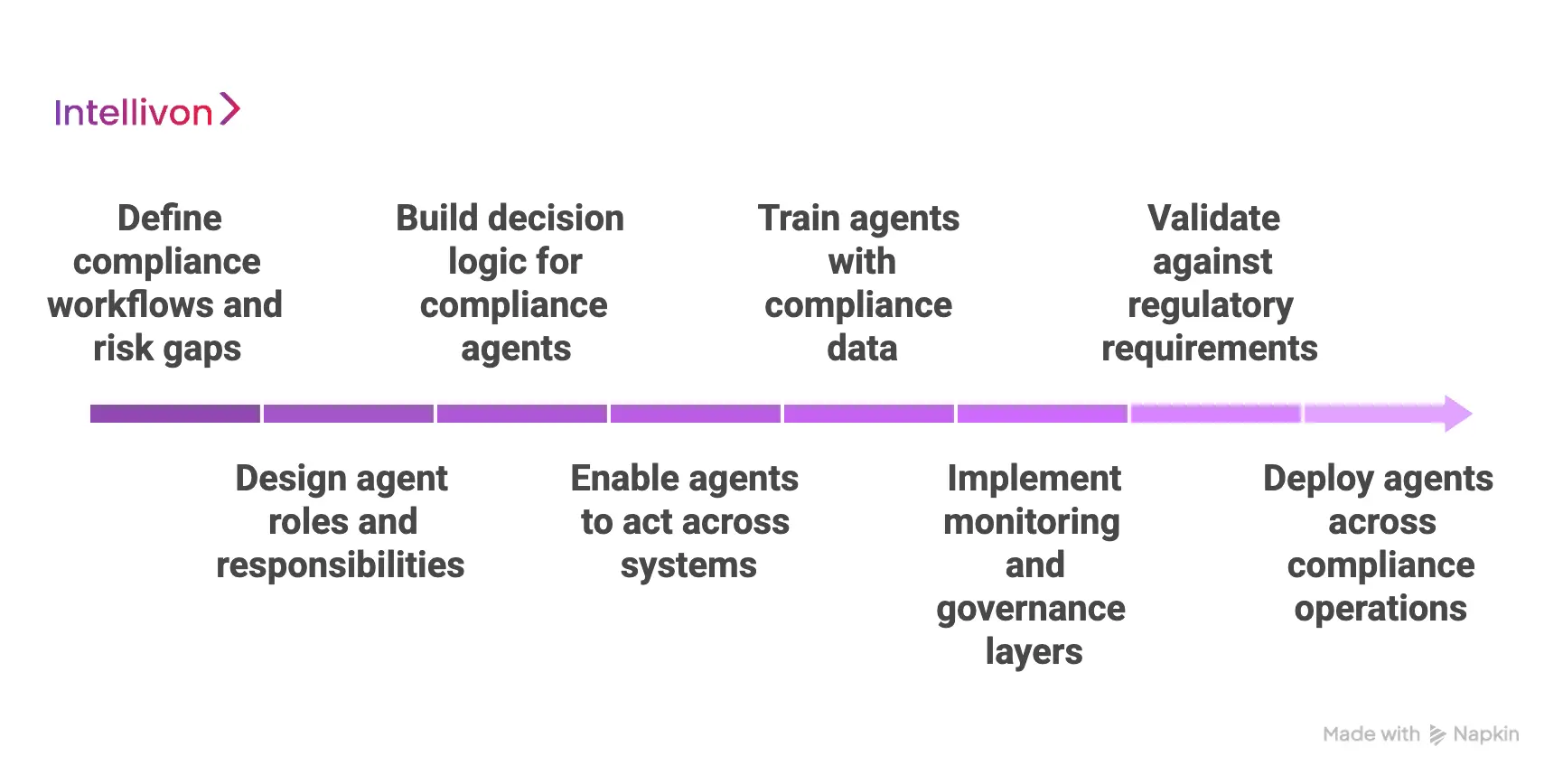

At Intellivon, we follow a rigorous eight-step methodology to transform manual compliance burdens into strategic, AI-driven assets.

1. Define compliance workflows and risk gaps

The first step involves a comprehensive current-state analysis of your existing regulatory processes. We identify the specific “friction points” where manual intervention causes delays or where rule-based systems generate excessive false positives.

- Process Mapping: We document every step of your KYC, AML, and reporting cycles.

- Gap Analysis: Our team pinpoints areas where unstructured data is currently overwhelming human staff.

- Risk Prioritization: We rank these gaps based on potential regulatory fines and operational impact. Therefore, the foundation is built on solving your most critical business problems rather than just automating for the sake of technology.

2. Design agent roles and responsibilities

Once the gaps are identified, we define the specialized “personas” for each AI agent. Instead of a single, monolithic bot, we create a team of experts with clear boundaries and objectives.

- Specialization: One agent may focus exclusively on identity verification, while another handles transaction velocity monitoring.

- Authority Levels: We define exactly what an agent can do autonomously versus what requires a human “sign-off.”

- Communication Protocols: We establish how these agents will share data and trigger handoffs between departments. Consequently, your compliance ecosystem functions like a well-organized department with clear accountability at every level.

3. Build decision logic for compliance agents

The “brain” of the agent is constructed using advanced Large Action Models (LAMs) and custom decision trees. Unlike simple bots, these agents are programmed to understand the intent behind a regulation, such as the nuances of the EU’s AMLA or the US Bank Secrecy Act.

We embed your institutional risk appetite directly into the agent’s logic gates. Furthermore, we use “Chain of Thought” reasoning to ensure that every decision the agent makes is logical and explainable. In addition, this logic is designed to be modular, allowing for rapid updates as global laws evolve.

4. Enable agents to act across systems

For an agent to be effective, it must have the “tools” to execute its decisions. We build secure, financial-grade API connectors that allow agents to interact with your core banking ledgers, ERPs, and CRM systems.

- Write Access: Agents can update a client’s risk score or place a temporary hold on a suspicious account.

- Cross-Platform Sync: They can push alerts to Slack, create tickets in Jira, or update records in Salesforce simultaneously.

- Legacy Bridging: For older systems, we implement secure middleware that translates AI intent into legacy commands. This “agency” ensures that compliance is not just a reporting function but an active, real-time defense mechanism.

5. Train agents with compliance data

Training is the most critical phase for ensuring precision and reducing “hallucinations.” We use your historical transaction data, past audit reports, and localized regulatory handbooks to fine-tune the agent’s judgment.

- Supervised Learning: We use “labeled” data from your past successful investigations to teach the agent what a genuine threat looks like.

- Synthetic Stress Testing: We generate “edge case” scenarios to see how the agent handles rare or highly sophisticated fraud attempts.

- Knowledge Retrieval: We implement RAG (Retrieval-Augmented Generation) so the agent can cite specific sections of your internal policy when justifying an action. This tailored training ensures the system reflects your unique business context and regional requirements.

6. Implement monitoring and governance layers

At enterprise scale, “trust but verify” is the golden rule. We implement a secondary governance layer that monitors the primary agents in real-time.

- Drift Detection: The system flags any changes in an agent’s decision-making patterns over time.

- Circuit Breakers: If an agent encounters an anomaly it wasn’t trained for, the system automatically pauses and alerts a human.

- Audit Logging: Every “thought” and “action” is recorded in an immutable, tamper-proof log for future regulatory review. Therefore, you maintain total control over your autonomous workforce, ensuring they never operate outside of their pre-defined guardrails.

7. Validate against regulatory requirements

Before going live, the entire system undergoes a “mock audit” to ensure it meets the highest global standards. We test the agents against frameworks like GDPR, SOC2, and HIPAA, as well as specific financial mandates like PCI DSS 4.0.

- Accuracy Benchmarking: We verify that the agent identifies compliance gaps with the high precision expected by global regulators.

- Explainability Audit: We ensure that every automated SAR or KYC rejection includes a clear, defensible rationale.

- Bias Testing: We run rigorous checks to ensure the AI’s decision-making remains fair and non-discriminatory. This validation phase provides the documented proof your board and regulators need to trust the new system.

7. Deploy agents across compliance operations

The final step is a staged rollout, where Intellivon integrates the agents into your live production environment. We start with low-risk “shadow mode” operations, where agents suggest actions for human approval, before transitioning to full autonomy.

- Seamless Integration: Our 11+ years of expertise ensure that deployment happens without disrupting your core services.

- Scalability Setup: We use Kubernetes-based architectures to ensure the agents can scale their processing power during high-volume events.

- Continuous Support: We provide ongoing maintenance to ensure the agents stay ahead of emerging threats and new regulatory updates. Consequently, your organization achieves a 3X ROI through reduced overhead and faster decision-making.

Partnering with Intellivon means navigating the complexity of the “Agentic Era,” ensuring your compliance program is not just a cost center, but a growth enabler.

Contact our experts today to start building a future where your compliance is as fast and intelligent as your business.

Cost to Build Compliance AI Agent Systems

Building AI agents for compliance automation is not a fixed-cost project. The total investment depends on how deeply the system integrates with regulatory workflows, financial infrastructure, and enterprise compliance operations.

Unlike standalone AI tools, compliance agents operate within a real-time, multi-agent system that monitors, decides, and executes actions across workflows.

As a result, costs are driven more by orchestration, integrations, governance, and auditability than just model development.

1. Cost Breakdown by Modules and Complexity

| Component | Scope | Estimated Cost |

| Data Ingestion Layer | Transaction data, KYC data, regulatory inputs | $15,000 – $35,000 |

| Compliance Monitoring Agents | AML checks, transaction screening | $25,000 – $60,000 |

| Decision Agents | Risk scoring, compliance validation logic | $20,000 – $50,000 |

| Orchestration Layer | Workflow coordination across agents | $20,000 – $55,000 |

| Reporting & Audit Agents | Regulatory reports, audit logs | $15,000 – $40,000 |

| Monitoring & Feedback Systems | Model tracking, adaptive compliance logic | $10,000 – $25,000 |

Compliance agents are built as part of a unified compliance system, not isolated components. Therefore, system design and workflow orchestration significantly influence overall costs.

2. Infrastructure and Integration Costs

| Component | Scope | Estimated Cost |

| Cloud Infrastructure (AWS/GCP/Azure) | Compute, storage, scaling | $10,000 – $30,000/year |

| Real-Time Data Pipelines | Event streaming, transaction processing | $15,000 – $40,000 |

| API & Integration Layer | Core banking, KYC, payment systems | $25,000 – $60,000 |

| Event-Driven Architecture | Real-time triggers and workflows | $20,000 – $50,000 |

A cloud-native, API-first architecture ensures real-time execution and scalability. However, costs increase with transaction volume, system complexity, and integration depth.

3. Security and Compliance Costs

| Component | Scope | Estimated Cost |

| Data Encryption & Access Control | PII protection, role-based access | $10,000 – $25,000 |

| Audit Logs & Explainability | Decision traceability for regulators | $10,000 – $25,000 |

| Regulatory Compliance Setup | AML, GDPR, FATF alignment | $15,000 – $40,000 |

| Security Testing | Penetration testing, vulnerability scans | $8,000 – $20,000 |

Compliance systems operate in highly regulated environments. Therefore, security, governance, and auditability are core system layers, not add-ons.

Hidden Costs Enterprises Often Miss

- Integration with legacy banking and compliance systems

- Data normalization across fragmented financial sources

- Redesigning workflows for autonomous agent execution

- Continuous agent retraining and rule updates

- Ongoing regulatory changes and audit requirements

These factors typically increase total project costs by 20–30%.

Estimated Total Cost Range

| Platform Scope | Estimated Cost |

| MVP (Single-Agent Compliance System) | $80,000 – $150,000 |

| Mid-Level Compliance Automation System | $150,000 – $300,000 |

| Enterprise Multi-Agent Compliance Platform | $300,000 – $450,000+ |

Most financial institutions underestimate compliance automation costs by focusing only on AI models. In reality, the majority of investment goes into integrations, real-time infrastructure, and regulatory compliance layers.

At Intellivon, compliance AI agent systems are built as enterprise financial infrastructure, not standalone tools. As a result, they scale across workflows, regions, and regulatory environments without requiring constant rework.

Conclusion

Adopting Agentic AI transforms compliance from a reactive burden into a strategic pulse. By embedding autonomous reasoning directly into financial workflows, enterprises eliminate manual bottlenecks and mitigate systemic risks in real-time.

This shift ensures your organization remains resilient against shifting global regulations while reclaiming hundreds of operational hours. Ultimately, investing in an intelligent, agent-driven infrastructure is the most decisive move toward sustainable, high-velocity growth in a complex regulatory era.

Build Compliance AI Agents With Intellivon

At Intellivon, compliance AI agents are built as an enterprise decision infrastructure, not automation layers added to fragmented systems. The goal is to create a unified platform where agents continuously monitor, evaluate, and execute compliance workflows across your financial operations.

Each system is designed around how compliance actually works in your organization. This includes KYC verification, AML monitoring, transaction screening, regulatory reporting, audit management, and cross-border compliance, connected through a single, agent-driven architecture. As a result, teams reduce manual effort, improve accuracy, and move from reactive checks to real-time, autonomous compliance execution.

Our engineering approach combines multi-agent architectures with API-first, cloud-native systems. This ensures seamless integration with core banking platforms, payment systems, KYC providers, compliance tools, and third-party data sources—without disrupting ongoing operations.

Why Build With Intellivon

- Infrastructure-First Approach: We build scalable compliance systems, not short-term automation tools that break with growing regulatory complexity.

- Built for Real Compliance Workflows: Every system is aligned with actual regulatory processes, audit requirements, and enterprise risk controls.

- Agent-Based Execution at Scale: Our systems enable agents to monitor, decide, and act across workflows in real time, reducing manual dependency.

- Seamless System Integration: API-first architecture ensures smooth integration with existing banking and compliance ecosystems.

- Compliance and Audit Built In: Every action is traceable, explainable, and aligned with global regulatory requirements.

Whether you are modernizing legacy compliance systems or building a new automation layer, Intellivon helps you design and deploy AI agent systems that scale with your operations and regulatory landscape.

Talk to our team to build your compliance AI agent system.

FAQs

Q1. What are AI agents in compliance systems?

A1. AI agents in compliance systems are autonomous software components that monitor transactions, evaluate risks, and execute compliance actions in real time. Unlike traditional AI tools, they take actions such as flagging transactions, triggering alerts, updating records, and generating audit logs. As a result, enterprises move from manual compliance processes to continuous, automated execution.

Q2. How accurate are compliance AI agents?

A2. Compliance AI agents can achieve high accuracy when trained on quality data and supported by strong governance layers. In most enterprise setups, accuracy improves over time through feedback loops and continuous learning. However, performance also depends on data quality, model design, and regulatory alignment. Therefore, human oversight and audit mechanisms remain critical to ensure reliability and compliance.

Q3. Can agents meet global regulatory standards?

A3. Yes, AI agents can be designed to meet global regulatory standards such as AML, KYC, GDPR, and FATF guidelines. They are built with compliance rules, audit trails, and explainability features that align with regulatory requirements. However, enterprises must configure systems based on regional laws and continuously update them as regulations evolve across jurisdictions.

Q4. How long does it take to build such systems?

A4. The development timeline depends on system complexity, integrations, and regulatory scope. A basic compliance AI agent system can take 8–12 weeks, while a mid-level system may take 3–5 months. Enterprise-scale, multi-agent platforms with deep integrations and compliance layers typically take 6–9 months or more to build and deploy.

Q5. What data is required for compliance agents?

A5. Compliance AI agents rely on multiple data sources, including transaction data, customer KYC information, behavioral patterns, device signals, and regulatory datasets. They may also integrate with external data providers such as credit bureaus, sanctions lists, and identity verification services. The effectiveness of the system depends on how well this data is structured, integrated, and governed.