Key Takeaways:

-

AI lending platforms require credit-policy depth, adverse-action traceability, model governance, and core banking integration.

-

Packaged systems like nCino, Blend, and Finastra work when standardization matters more than platform ownership.

-

Focused MVPs cost $70,000 to $110,000 while complex enterprise builds reach $220,000 to $300,000.

-

Evaluating vendors means assessing document AI, data ownership, implementation capacity, and post-launch support depth.

-

How Intellivon builds AI loan origination platforms: governed lending infrastructure with explainable decisioning, compliance controls, and MLOps.

An AI loan origination platform is the operating system behind every credit decision a lender makes. Because of that, choosing the right one matters more than any other technology decision in the lending stack. The right choice comes down to three criteria, which include lending segment fit, AI compliance capability, and integration depth. In practice, a mortgage lender needs entirely different AI capabilities than a consumer lender or a commercial bank.

The evaluation criterion that comparison guides consistently miss is ECOA-compliant adverse action generation. Without it, a credit engine is non-compliant for US lending regardless of its predictive accuracy. Freddie Mac’s 2024 study found that lenders using digital tools originate loans 14% less expensively, and against a market average of $11,076 per loan in 2024, that gap compounds significantly at scale. Platform selection is therefore both a compliance decision and a long-term cost structure decision.

Accordingly, this guide evaluates the leading platforms against segment fit, ECOA compliance, and integration depth. Intellivon builds custom AI loan origination platforms where off-the-shelf solutions fall short on compliance or workflow requirements. In this blog, we will cover the top AI loan origination platforms in the USA in 2026.

What Are AI Loan Origination Platforms?

An AI loan origination platform is a software system that automates lending. Specifically, this platform uses machine learning to assess risk and process applications. Traditional setups require manual document reviews. However, these modern systems ingest data automatically from bureaus.

Consequently, banks verify identity and calculate debt ratios in seconds. Therefore, lenders reduce application bottlenecks immediately. Ultimately, this infrastructure ensures accurate compliance.

Why Businesses Are Investing In AI Loan Origination Platforms

Financial institutions invest in an AI loan origination platform to scale lending capacity, remove operational bottlenecks, and lower acquisition friction. Specifically, this modern infrastructure replaces outdated manual reviews with algorithmic orchestration. Therefore, businesses can automate credit decisioning, systematically enforce regulatory rules, and accelerate time-to-market.

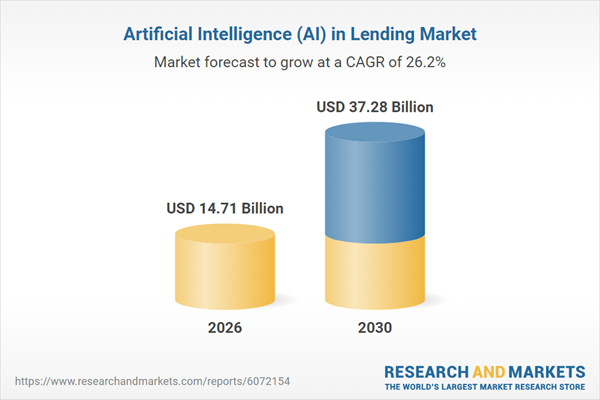

The global market for AI in lending is experiencing exponential expansion. Specifically, the industry size is projected to grow from 11.63 billion dollars in 2025 to 14.71 billion dollars in 2026. This trajectory represents a compound annual growth rate (CAGR) of 26.5 percent, driven by deep enterprise digital transformation.

1. Reduce Loan Processing Time

An AI loan origination platform significantly shortens decision cycles by processing unstructured data in real time. Consequently, it isolates application-to-decision speed from application-to-funding latency:

- Automated Intake & Review: Immediate parsing of applicant payloads reduces early queue stagnation.

- Document Verification & Analysis: Instant OCR matches income tax data and payroll stubs against bank records.

- Condition & Route Management: Algorithmic systems prepare credit files and trigger approval routing instantly.

2. Increase Straight-Through Processing

True automation routes loans directly from submission to closing with no human intervention. However, you must measure Straight-Through Processing (STP) across separate system modules rather than generalized vendor claims:

- True End-to-End STP: Integrates digital identity verification, real-time documentation checks, and credit scoring.

- Modular Automation Checking: Evaluates single steps like intake and funding independently.

- Vendor Validation: Prevents software providers from hiding human manual steps under broad “automated” labels.

3. Improve Borrower Conversion

Modern software infrastructure actively prevents application drop-offs by optimizing user journey touchpoints. Specifically, this results in modern digital lending workflows:

- Frictionless Form Layouts: Shorter digital applications use data prefill via API connections.

- Active Status Transparency: Save-and-resume modules combine with real-time status updates for immediate visibility.

- Velocity to Offer: Automated reminders and rapid conditional decisions keep borrowers engaged.

4. Expand Lending Without Linear Staff Growth

Deploying intelligent infrastructure breaks the direct link between higher loan volumes and head count expenses. Consequently, institutions scale efficiently:

- Processor & Underwriter Protection: Systems manage high data volumes without increasing staff burnout.

- Targeted Human Oversight: Document reviewers and quality-control staff focus purely on complex exceptions.

- Scalable File Preparation: Machine learning absorbs seasonal demand spikes seamlessly.

5. Launch New Lending Products Faster

Configurable cloud architecture enables rapid deployment of diverse financing options without core banking overhauls. Specifically, lenders can launch new market offers quickly:

- Retail & Auto Asset Lines: Pre-built modules accelerate auto lending and home equity workflows.

- Specialized Business Assets: Highly adaptive engines support commercial credit, SBA workflows, and equipment finance.

- Modern Lending Models: API-first backends power embedded lending solutions and personal loan applications.

The investment case is strongest when automation improves both operational speed and decision control. However, the platform must still match the institution’s lending segment, risk model, compliance obligations, and integration environment.

How We Ranked AI Loan Origination Platform Companies

To build an authoritative AI loan origination platform vendor scorecard, financial institutions must evaluate a partner’s ability to construct legally compliant, production-grade infrastructure rather than assessing superficial brand visibility.

Specifically, our framework isolates critical operational capabilities across seven weighted technical categories.

This methodology scores providers based on true deployment compliance, underlying data sovereignty, and transactional risk controls.

Platform Evaluation Model and Weighting Framework

The following scorecard framework establishes objective criteria for comparing enterprise technology providers across technical capability, data handling, and regulatory readiness:

| Evaluation Dimension | Weight | Target Technical Criteria and Capabilities Covered |

| Fintech & Lending Domain Experience | 20% | Proven delivery across commercial banks, credit unions, mortgage lenders, non-bank asset managers, and embedded finance providers. |

| AI Engineering Capability | 15% | Deep implementation of predictive risk models, Document AI (OCR/NER), automated fraud detection, and production MLOps pipeline monitoring. |

| Loan Origination Architecture | 15% | Custom rule engines, dynamic workflow orchestration, localized decision services, immutable system audit trails, and human-in-the-loop review queues. |

| Compliance & Model Governance | 15% | Hardcoded logic supporting ECOA, Regulation B, automated adverse-action notices, HMDA reporting, TRID disclosures, and rigorous model bias testing. |

| Integration Depth | 15% | Native API connectivity to legacy core banking rails, primary credit bureaus, KYC/AML platforms, open banking networks, and e-signature portals. |

| Platform Ownership & Customization | 10% | Full source-code access, data ownership guarantees, model portability, customizable workflows, and independent vendor exit paths. |

| Delivery & Post-Launch Support | 10% | Comprehensive technical discovery, functional prototyping, rigorous security QA, release management, and proactive maintenance SLA monitoring. |

Enterprise risk management requires that technical selection prioritize explainable algorithmic attribution and integration depth over vendor marketing narratives.

Ultimately, a balanced selection scorecard helps lenders mitigate compliance liabilities while optimizing straight-through processing rates.

Top AI Loan Origination Platforms

The top AI loan origination platforms differ by lending segment, architecture, implementation burden, and system ownership. Some operate as full loan origination systems. Others focus on borrower experience, decisioning, document intelligence, or workflow automation.

Therefore, lenders should compare platform fit rather than assume one vendor serves every lending model equally well.

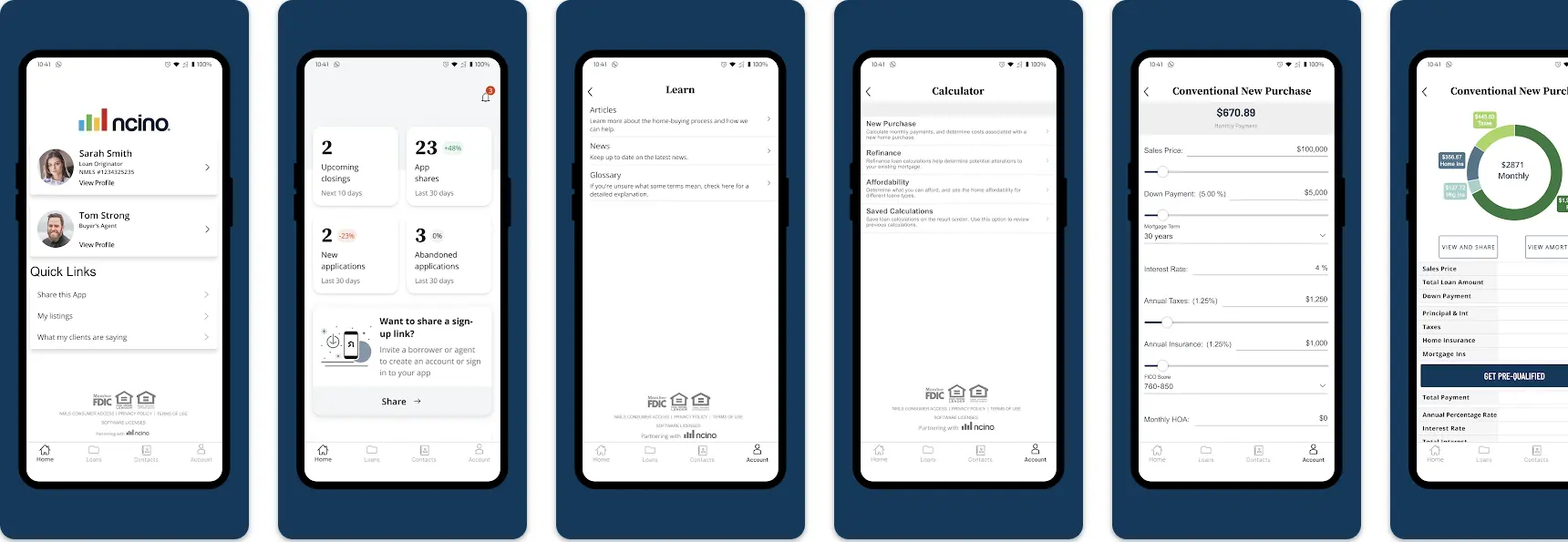

1. nCino — Best Overall For Multi-Line Bank Lending

nCino supports commercial, consumer, small-business, and mortgage lending within one cloud banking environment.

It is strongest for banks and credit unions that want to standardize several lending lines, connect front- and back-office workflows, and introduce AI without creating separate systems for every product.

A. What the Platform Covers

- Commercial Credit Workflows: Manage intricate business lending, complex tier tracking, and multi-entity relationship mapping.

- Consumer and Small-Business Lending: Speeds up retail and small-business loan applications through unified digital intake.

- Mortgage Origination & Underwriting: Orchestrates compliant real estate workflows from application to active portfolio monitoring.

- Core Operational Lifecycle: Handles automated credit decisioning, dynamic approval routing, document collection, and regular loan renewals.

B. AI and Automation Capabilities

- Intelligent Credit Decisioning: Deploys embedded machine learning algorithms to evaluate borrower profiles and risk tiers instantly.

- Loan-File Summarization: Uses natural language processing to condense sprawling text and financial reports for underwriters.

- Automated Task Routing: Triggers prescriptive workflow recommendations and active banking agent tasks based on real-time data.

C. Integration Considerations

The system requires deep connectivity with core banking systems, external credit bureaus, and specialized KYC/AML validation tools.

Because it is built directly on the Salesforce platform, it integrates natively with existing Salesforce CRM architectures. However, linking it to legacy internal record systems or downstream servicing systems demands structured data mapping.

- Best For: Regional banks, community banks, credit unions, and multi-product financial institutions with existing Salesforce deployments.

- Strongest Capability: Enterprise lending workflow and AI orchestration across several disparate lending products.

- Main Limitation: Implementation can require extensive configuration, integration, data migration, process redesign, training, and change management.

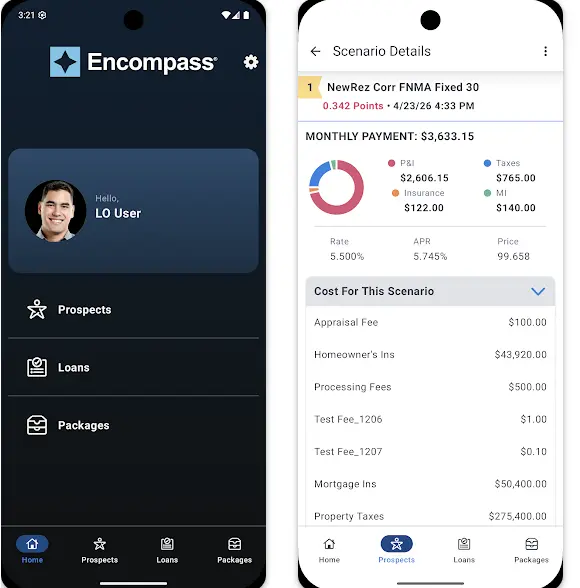

2. ICE Encompass — Best For Mortgage Loan Origination

ICE Encompass offers one of the deepest mortgage origination environments in the United States. It connects application intake, underwriting, disclosures, conditions, closing, investor delivery, and compliance inside one mortgage-specific system of record.

A. What the Platform Covers

- Multi-Channel Mortgage Manufacturing: Supports retail mortgage origination, wholesale lending, and correspondent lending workflows.

- Processing & Underwriting: Manages full loan-file processing, automated underwriting conditions, and product pricing verification.

- Closing & Delivery: Handles complete closing preparation, secondary market funding, investor delivery, and servicing handoffs.

B. AI and Automation Capabilities

- Mortgage Document Classification: Uses advanced computer vision to automatically identify, tag, and sort mortgage documents.

- Income & Asset Analysis: Automatically extracts and validates borrower income statements, tax forms, and asset records.

- Quality-Control Automation: Tracks missing-document detection and runs real-time loan-file validation to spot underwriting errors.

C. Compliance Strength

The platform features hardcoded regulatory safeguards for TRID, RESPA, and HMDA reporting requirements.

It automatically manages Loan Estimate (LE) and Closing Disclosure (CD) workflows, enforces strict fee tolerance controls, verifies disclosure timing, and logs every system action to maintain clean audit trails according to state and federal mortgage rules.

D. Integration Considerations

Encompass links natively to primary credit bureaus, Automated Underwriting Systems (AUS like Fannie Mae Desktop Underwriter), appraisal systems, title registries, and flood verification services.

It also requires tight integration with custom product and pricing engines (PPE) and e-closing portals.

- Best For: Independent mortgage banks, depository mortgage lenders, wholesale lenders, and high-volume multi-channel mortgage originators.

- Strongest Capability: End-to-end US mortgage manufacturing depth and absolute regulatory compliance tracking.

- Main Limitation: Encompass requires significant configuration and administration. It is also less suitable for non-mortgage consumers, SMB, auto, or commercial lending.

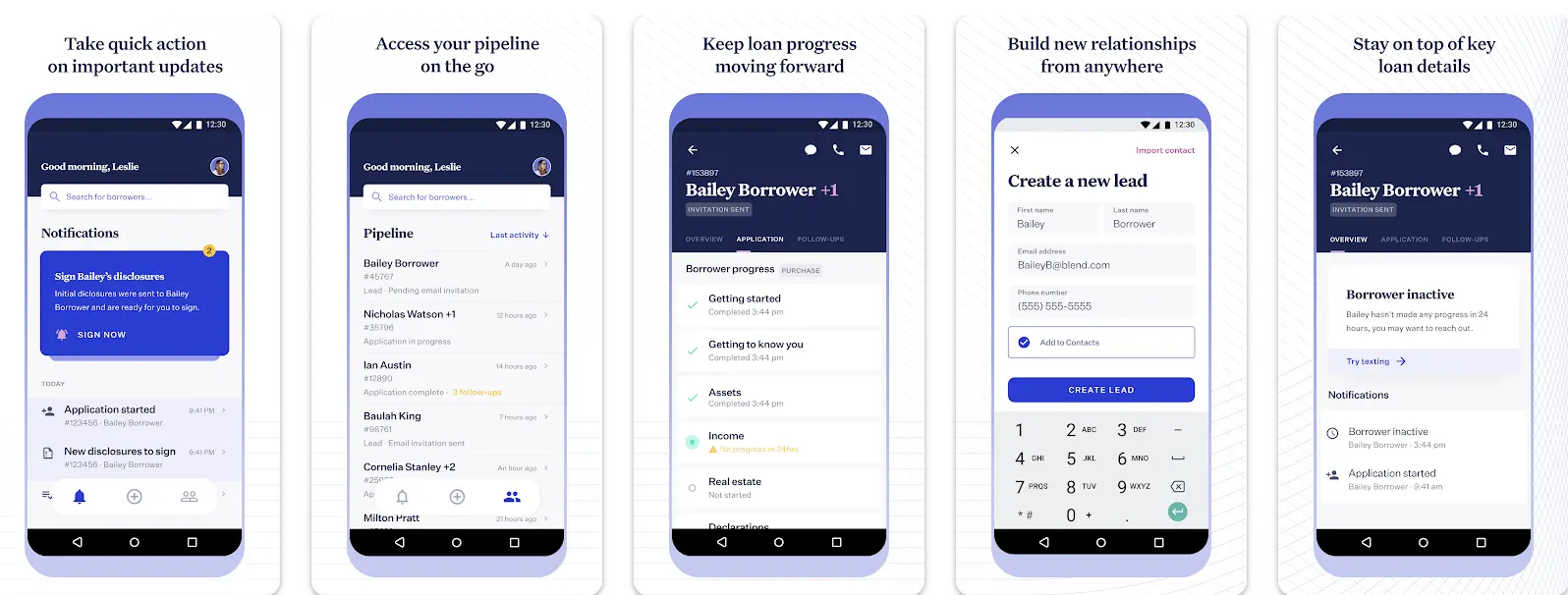

3. Blend — Best For Intelligent Digital Origination

Blend improves borrower-facing origination across mortgage, consumer lending, home equity, and deposits.

It is especially valuable for institutions that want faster digital applications, connected financial data, automated verification, and AI-assisted loan processing without immediately replacing the existing LOS.

A. What the Platform Covers

- Omnichannel Digital Intake: Delivers mobile and web applications for mortgage, home equity, consumer loans, and deposit account opening.

- Frictionless Form Execution: Populates fields with verified data prefill, manages secure document uploads, and handles save-and-resume logic.

- Borrower Portal Interface: Hosts localized digital disclosures, e-signature execution, and real-time borrower task lists.

B. AI and Automation Capabilities

- Automated Loan-File Review: Uses Blend Autopilot to analyze documents and instantly flag missing information or data mismatches.

- Dynamic Workflow Automation: Generates automated borrower follow-ups, sends instant status updates, and streamlines credit checking.

- Intelligent Origination Reviews: Pre-validates fields to match credit policy guidelines before pushing data to downstream systems.

C. Borrower Experience Strengths

- Minimized Application Friction: Drives shorter applications by connecting directly to consumer payroll and bank APIs.

- Transparent Loan Journeys: Keep borrowers engaged with clear, real-time status visibility and contextual communication.

- Rapid Conditional Decisions: Accelerates early application touchpoints by rendering instant conditional approvals.

D. Integration Considerations

Blend serves as an intelligence and experience front-end layer. Therefore, it requires bidirectional API synchronization with existing underlying LOS platforms like ICE Encompass, core banking databases, verification providers, and downstream servicing infrastructure.

- Best For: Banks, credit unions, and consumer lenders modernizing digital origination while retaining an existing underlying LOS.

- Strongest Capability: Digital borrower experience optimization and AI-assisted front-end loan processing.

- Main Limitation: Blend may operate as a front-end layer while another LOS remains the system of record. This can increase integration, licensing, and reconciliation requirements.

4. MeridianLink One — Best For Credit Unions And Consumer Lending

MeridianLink One provides connected lending technology for consumer, mortgage, and small-business products.

It is particularly strong for credit unions, community banks, auto lenders, and institutions managing both direct and indirect consumer-lending channels.

A. What the Platform Covers

- Consumer Loan Origination: Manages high-volume workflows for auto lending, personal loans, credit cards, and home equity lines.

- Indirect Dealer Lending: Coordinates auto dealer network submissions, indirect vehicle financing, and dealer portal communications.

- Account Opening Connectivity: Synchronizes new user application intake with backend core membership databases.

B. AI and Automation Capabilities

- AI-Assisted Underwriting: Powers automated credit decisions, instant pre-approvals, and dynamic application routing using DecisionLender tools.

- Cross-Sell Insights: Evaluates real-time credit data to recommend relevant complementary banking products to active applicants.

- Risk-Based Workflows: Flag applicant profiles matching specific risk vectors to establish manual override paths for loan officers.

C. Consumer Lending Strengths

The platform excels at credit union operations, leveraging cross-product borrower data to evaluate memberships holistically. It integrates with indirect dealer channels and credit bureau networks to handle rapid, automated decisioning for consumer financing.

D. Integration Considerations

The system links directly to core banking structures, primary credit bureaus, membership enrollment applications, and indirect auto dealer networks. It also requires stable data connections to collection systems, CRM platforms, and e-signature engines.

- Best For: Credit unions, community banks, auto lenders, consumer finance providers, and lenders with high-volume indirect channels.

- Strongest Capability: High-velocity consumer lending automation and automated decision workflows.

- Main Limitation: MeridianLink may offer less flexibility for highly customized commercial lending, proprietary AI models, or unusual credit products.

5. Finastra Originate — Best For Commercial And Complex Bank Lending

Finastra Originate supports digital loan and deposit origination across retail, commercial, business, and mortgage use cases.

It is particularly relevant to institutions that need complex lending workflows, broad banking connectivity, and access to Finastra’s wider lending ecosystem.

A. What the Platform Covers

- Complex Multi-Line Banking: Manages retail, commercial, and business loan origination alongside deposit account opening.

- Credit Analysis Workflows: Directs complex product configuration, multi-level approval routing, and commercial documentation generation.

- Portfolio Handoff Systems: Structure data packages to transition funded commercial credits directly into backend accounting cores.

B. AI and Automation Capabilities

- AI-Assisted Credit Analysis: Automates commercial financial-document processing, data extraction, and deep credit-risk assessments.

- Fraud & Compliance Monitoring: Scans business entities for fraud patterns and enforces Section 1071 compliance tracking.

- Operational Analytics Support: Delivers predictive analytics and workflow recommendations to optimize commercial underwriting pipelines.

C. Commercial Lending Strengths

The platform handles complex borrower structures, multi-layered business entities, and detailed financial analysis. It connects business lending workflows directly to broader commercial banking rails and compliance document frameworks.

D. Integration Considerations

Finastra Originate integrates with Finastra core systems and surrounding lending modules, including Finastra Loan IQ, Finastra LaserPro, and Mortgagebot. Connecting it to non-Finastra third-party applications or specialized fintech components requires planning around API alignment.

- Best For: Commercial banks, regional financial institutions, business lenders, and banks already running Finastra product ecosystems.

- Strongest Capability: Commercial loan origination and deep, multi-layered banking-system connectivity.

- Main Limitation: Finastra’s lending environment includes several products and modules. Buyers must confirm which components are required, how they integrate, and whether additional licenses or implementation services are necessary.

Platform Comparison Summary

Lenders can evaluate the core differences across the top five AI loan origination platforms using the matrix below:

| Rank | Platform | Best For | Strongest Capability | Primary Limitation |

| 1 | nCino | Multi-product banks and credit unions | Enterprise lending and AI orchestration | Complex implementation timelines |

| 2 | ICE Encompass | Dedicated US mortgage lenders | End-to-end mortgage manufacturing | Highly specialized to real estate |

| 3 | Blend | Digital banks and mortgage lenders | Borrower experience and digital workflows | Often requires an underlying LOS |

| 4 | MeridianLink One | Credit unions and consumer lenders | Automated consumer decisioning | Less flexible for custom commercial loans |

| 5 | Finastra Originate | Commercial and multi-product banks | Commercial workflows and core connectivity | Multi-product ecosystem complexity |

No platform leads every lending segment. nCino provides the brightest multi-line capability. ICE Encompass leads mortgage origination. Blend improves digital borrower journeys. MeridianLink One fits consumer and credit-union lending. Finastra Originate supports complex commercial banking environments. The final shortlist should follow the lender’s product mix, integrations, compliance burden, and ownership requirements.

What Are the AI Loan Origination Platform Development Costs

Custom AI loan origination platform development usually costs $70,000 to $300,000, depending on lending products, AI complexity, compliance scope, integrations, migration, and deployment architecture.

Specifically, a focused platform with standard decision parameters stays near the lower end of the capital range. Conversely, a multi-product bank system with custom decisioning and extensive legacy integration reaches the upper end of estimation.

Cost Breakdown By Development Phase

Constructing an enterprise lending platform requires planning across distinct architectural layers. The table below outlines the specific budget allocations per delivery cycle phase:

| Development Phase | Expected Engineering Cost Range | Core Engineering Tasks & Deliverables Covered |

| Workflow and Compliance Discovery | $8,000–$18,000 | Mapping existing policy rules, tracking data lineage, and establishing Fair Lending constraints. |

| Architecture and Lending Data Design | $10,000–$25,000 | Designing database models, setting encryption states, and detailing core banking API topologies. |

| Borrower and Employee Applications | $15,000–$40,000 | Developing responsive web portals, multi-channel intake forms, and underwriter workspaces. |

| Workflow, Rules, and Decision Services | $18,000–$50,000 | Building the central credit policy engine, exception routing logic, and decision services. |

| AI Document Processing and Underwriting | $12,000–$45,000 | Training IDP models for OCR parsing, income verification, and risk-tier modeling. |

| Core and Third-Party Integrations | $15,000–$55,000 | Connecting credit bureau APIs, KYC systems, AML lists, and e-signature engines. |

| Compliance, Security, and Model Validation | $8,000–$25,000 | Running penetration tests, automated bias checks, and adverse-action verification. |

| Testing, Migration, and Deployment | $8,000–$25,000 | Executing end-to-end data migration, staging pipeline verification, and production launch. |

Because engineering cycles overlap throughout the delivery roadmap, project managers should not simply sum the maximum values of each category to calculate total capital expenditure.

Custom Implementation Tiers and Scope Boundaries

The total cost of ownership scales predictably based on structural features, target assets, and automation complexity. Financial institutions can plan around three distinct development tiers:

Focused MVP — $70,000 to $110,000

This tier targets startups and community lenders validating a single automated credit asset class.

- Asset Containment: Restricts scope to one lending product delivered through a single borrower channel.

- Decisioning Logic: Utilizes standard credit scorecard metrics rather than complex deep-learning layers.

- Processing Mechanics: Embeds basic Document AI text extraction paired with two to four standard bureau integrations.

- Human Oversight: Routes all final loan approvals through a mandatory human underwriter queue.

Production Platform — $120,000 to $210,000

This tier fits mid-sized institutions migrating core business lines into highly automated credit execution workflows.

- Asset Diversification: Supports multiple retail or consumer loan products simultaneously.

- System Connectivity: Integrates with existing core banking databases, major credit bureaus, and KYC/AML platforms.

- Automation Layer: Connects configurable workflow rules directly to automated adverse-action notice triggers.

- Governance Interface: Features real-time model performance monitoring alongside role-based operations dashboards.

Enterprise Platform — $220,000 to $300,000

This tier satisfies commercial banks requiring highly specialized risk environments and massive transaction capacity.

- Asset Scale: Coordinates complex commercial credit or multi-channel mortgage workflows across several business divisions.

- Advanced Intelligence: Deploys proprietary machine learning risk models alongside agentic AI loan operations tools.

- Infrastructure Security: Uses hybrid cloud architectures equipped with deep fair-lending analytics dashboards.

- Data Migration: migrates complex legacy file databases while maintaining comprehensive audit logs.

Ongoing Maintenance & Operational Budgets

Lenders must budget 15% to 22% of the initial development cost annually to maintain system stability and regulatory alignment. Specifically, this recurring operational expense preserves platform health across specific infrastructure categories:

- Model Drift & Validation Checks: Continuous tuning ensures predictive risk algorithms maintain precision as economic indicators shift.

- API Maintenance: Engineering support adjusts to breaking changes published by connected third-party data providers.

- Regulatory Compliance Updates: Dedicated sprints update code to match shifting CFPB, state lending, and TRID disclosure rules.

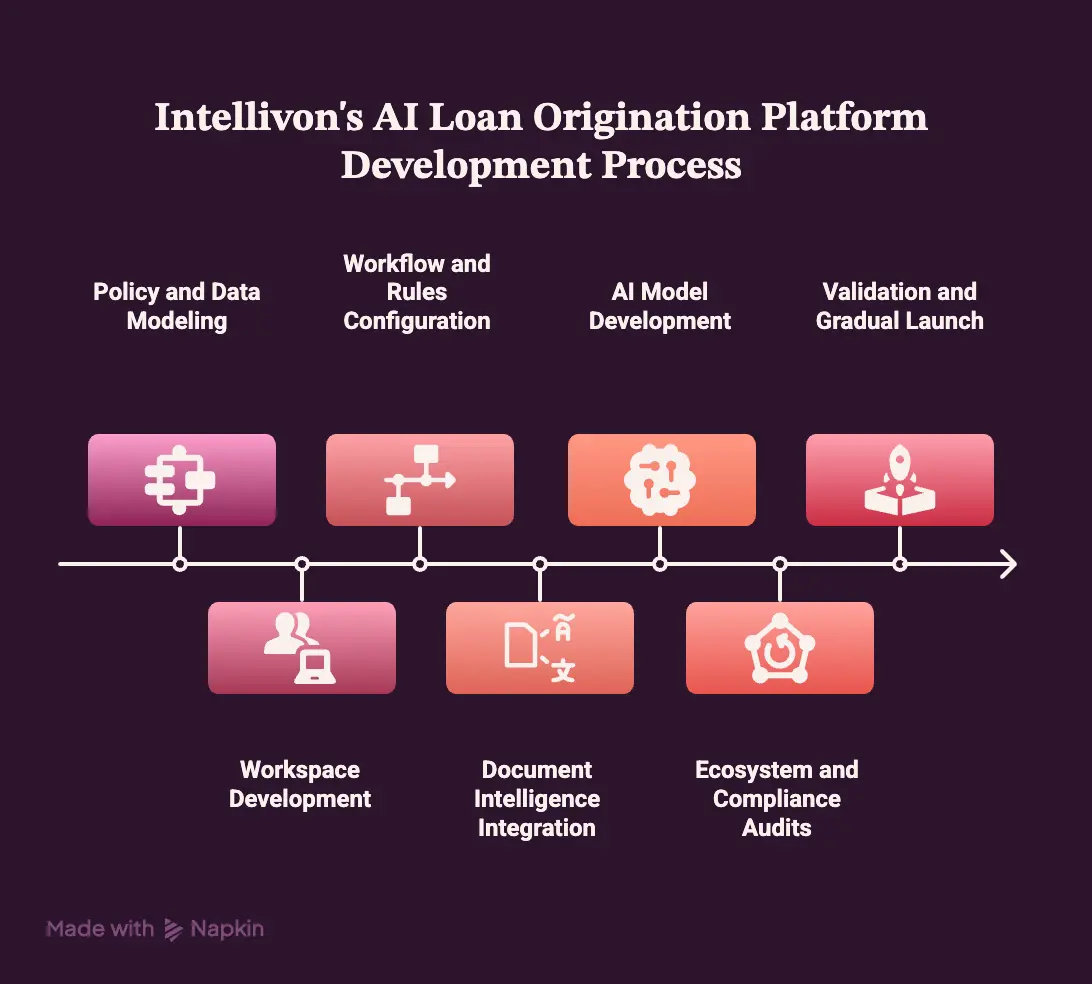

How Intellivon Builds You An AI Loan Origination Platform

Building an AI loan origination platform with Intellivon follows a phased process focused on compliance boundaries and credit policy. Development does not start with an AI model or a borrower interface.

Specifically, it begins by defining how applications, evidence, rules, decisions, exceptions, notices, integrations, and human authority move through the lending lifecycle.

1. Map Policy and Lending Data Models

The first phase translates lending policies into executable requirements. Specifically, Intellivon maps products, eligibility, pricing, documents, exposure limits, approval authority, exceptions, and adverse-action reasons before development begins. Technicians conduct workflow interviews, build policy decision tables, map entity relationships, and establish field ownership.

Consequently, our team separates mandatory compliance rules from changing credit policy, preventing developers from embedding policies directly into code. Therefore, this strategy creates one governed source of truth rather than allowing borrower, bureau, document, and decision data to diverge across systems.

2. Build Borrower and Employee Workspaces

The experience layer gives borrowers, loan officers, processors, underwriters, compliance teams, and administrators role-specific workflows. For example, each user sees the information, actions, and evidence required for their stage of the loan. This step involves web and mobile applications, dynamic forms, secure document upload, and role controls.

However, Intellivon interfaces are built around task completion and exception resolution rather than recreating paper forms on a screen.

3. Configure Workflow and Credit Rules

The workflow engine controls how applications move between intake, verification, underwriting, approval, conditions, closing, and funding. Meanwhile, the rules engine executes eligibility, pricing, and documentation requirements consistently. Technical work involves state machines, decision tables, and approval hierarchies.

Importantly, Intellivon keeps rules configurable outside the core application code. Therefore, lending teams can update policy without rebuilding the platform.

4. Integrate Document Intelligence

Document intelligence turns uploaded files into structured, source-linked lending data. Specifically, the system classifies documents, extracts fields, validates evidence, identifies missing information, and routes low-confidence results for review. Technicians build OCR parsing pipelines and confidence scoring.

Furthermore, every extracted field retains its source document page coordinates. This allows an employee or auditor to verify the original evidence easily.

5. Develop AI Credit and Fraud Models

AI models improve risk ranking, fraud detection, pricing, or manual-review prioritization without replacing policy controls. Instead, each model needs defined inputs, measurable performance, documented limitations, and lender-approved decision authority. Technical tasks include feature engineering, explainability tracking, and champion-challenger testing.

In addition, the team keeps deterministic eligibility and compliance rules completely outside predictive models, making decisions easy to govern and reproduce.

6. Connect Ecosystem and Compliance Audits

The integration phase connects the platform with core banking, credit bureaus, KYC/AML providers, e-signature engines, and servicing systems. Concurrently, compliance controls record which data, rules, models, users, and overrides produced every decision. Technical teams configure decision logs, model version histories, and notice timing controls.

Ultimately, integrations use documented APIs, resilient queues, retries, and failure alerts. Consequently, a third-party outage never silently corrupts a loan file, and the audit structure stands ready before launch.

7. Validate and Scale the Product Gradual Launch

Validation compares the platform against historical outcomes, policy expectations, and difficult applications before live credit decisions begin. Specifically, technical work covers historical replay, bias analysis, and user acceptance. A controlled launch begins with one lending product, one channel, and a defined application volume.

Indeed, the team evaluates operational exceptions as carefully as model accuracy. Therefore, the rollout follows measurable release gates rather than a single institution-wide launch.

Why Do Businesses Choose Intellivon For AI Loan Origination Platforms?

Build an AI loan origination platform with Intellivon when your lending model needs more control than a packaged LOS can provide.

At the same time, Intellivon develops custom and hybrid platforms that connect borrower journeys, credit policy, document intelligence, decisioning, compliance, and core banking integrations within one production-ready architecture.

- Architecture built around lending operations: Develop borrower portals, loan officer workspaces, rules engines, approval workflows, document pipelines, decision services, and audit trails.

- AI with clear governance: Use predictive underwriting, document extraction, fraud detection, credit copilots, and lending agents with explainability, confidence thresholds, model monitoring, and human review.

- Compliance-ready workflows: Support ECOA, Regulation B, adverse-action notices, fair-lending controls, HMDA, TRID, RESPA, Section 1071, KYC, AML, and OFAC requirements.

- Enterprise integration capability: Connect core banking systems, credit bureaus, open banking providers, CRM platforms, e-signature tools, pricing engines, closing systems, and servicing platforms.

- Cost clarity from the start: Plan-focused MVPs from $70,000 to $110,000, production platforms from $120,000 to $210,000, and enterprise builds up to $300,000.

Talk to Intellivon’s fintech AI team to compare packaged platforms against a custom or hybrid build and define the right architecture for your lending operation.

Conclusion

Choosing the right AI loan origination platform requires more than comparing AI features. The partner must understand lending policy, borrower data, documents, credit decisions, integrations, and compliance controls. Packaged platforms suit standardized workflows.

However, custom or hybrid development works better for differentiated credit models and complex system environments. With development costs ranging from $70,000 to $300,000, lenders should validate vendors through a real workflow, architecture review, and controlled pilot.

FAQs

Q1. How Much Does AI Loan Origination Platform Development Cost?

A1. Custom AI loan origination platform development usually costs $70,000 to $300,000. A focused MVP ranges from $70,000 to $110,000, while production platforms cost $120,000 to $210,000. Meanwhile, multi-product enterprise builds reach $220,000 to $300,000. Integrations, migration, compliance, private-cloud deployment, and complex credit models increase the final budget significantly.

Q2. Should A Bank Replace Its LOS Or Add AI Around It?

A2. Keep the current LOS when it still supports booking, disclosures, core connectivity, and reliable data access. However, add AI first for document processing, underwriting support, fraud detection, borrower follow-up, or analytics. Replace the LOS only when its architecture blocks integrations, product changes, workflow control, scalability, or consistent daily lending operations.

Q3. Is Custom Development Cheaper Than Licensing An LOS?

A3. Custom development becomes cheaper when licence fees, transaction charges, integration costs, customization limits, and vendor lock-in exceed long-term ownership costs. Therefore, compare both options across five years. Include implementation, internal staffing, maintenance, compliance, model governance, infrastructure, migration, upgrades, support, and exit costs before selecting either strategic approach very carefully.

Q4. What Is A Good Straight-Through Processing Rate?

A4. A good straight-through processing rate varies by lending product. Consumer lenders may target more than 60% of decision STP for standardized applications. However, commercial lenders may prioritize a 30% to 50% reduction in analyst preparation time. Therefore, measure intake, document, decision, closing, and funding STP separately rather than reporting one blended rate.

Key Takeaways

- A polished borrower application does not make a complete LOS. At the same time, the platform must also control policy, evidence, decisions, conditions, notices, and integrations.

- The safest AI lending architecture keeps compliance rules deterministic, uses predictive models for risk, and limits generative AI to evidence-linked assistance.

- A lender should measure straight-through processing by stage. At the same time, automating document intake does not mean the full loan is touchless.

- Custom AI loan origination platform development costs $70,000–$300,000, but ownership can reduce long-term licence, transaction, and customization costs.

- The best development company is the one that can reproduce every credit decision, not the one with the longest list of AI services.