Embedded banking is becoming something every enterprise needs, and not just a nice extra. Companies in all sorts of industries are adding accounts, payments, cards, and financing right into their digital products. This makes things easier for customers and opens up new ways to make money. But from what we’ve seen working in complex financial environments, getting started with embedded banking isn’t usually the biggest challenge.

Banking-as-a-Service tools make it simpler to connect with financial systems, but they don’t take away the real work that comes with growing these programs. As embedded initiatives expand, many organizations encounter new pressure around financial controls, reconciliation accuracy, risk visibility, and sponsor bank expectations.

This blog is here to help you understand what it really takes to build a strong embedded banking platform. Using Intellivon’s hands-on experience in regulated, high-volume financial systems, we’ll walk you through how we build these enterprise-grade financial platforms you can trust, and not just quick fixes that might break under pressure.

Why Enterprises Are Rapidly Adopting Embedded Banking

Enterprises are quickly embracing embedded banking to bring services such as payments, lending, and treasury management directly into their platforms and workflows. The push comes from growing demand for smoother user experiences and new ways to generate revenue.

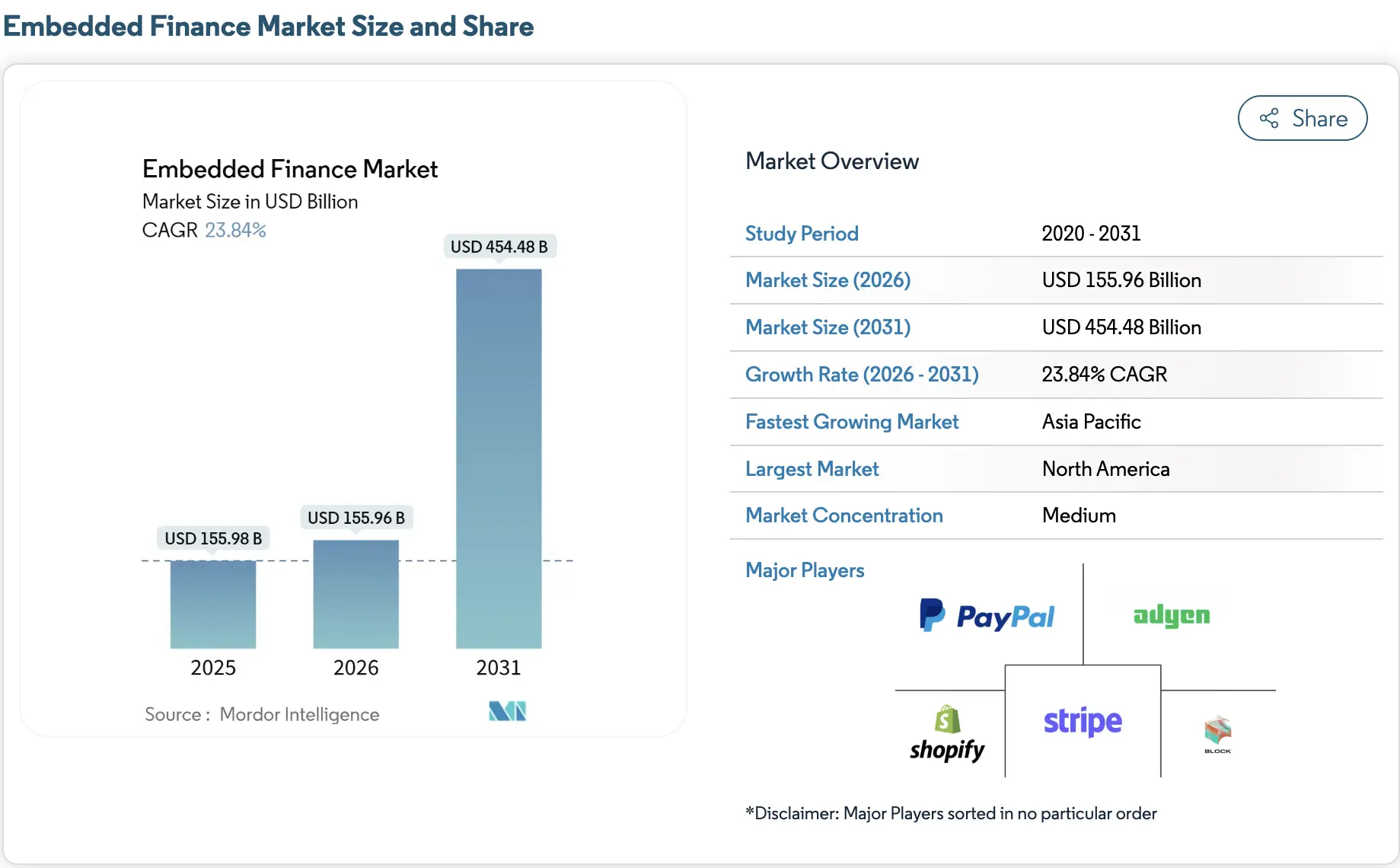

At the same time, strong market expansion and rising competition in B2B sectors are accelerating this shift. The global embedded finance market is growing at a strong pace. It was valued at roughly USD 104.8 to 155.96 billion between 2024 and 2026. Analysts expect it to expand at a CAGR of about 23 to 25 percent, reaching nearly USD 454 to 622.9 billion by 2031 to 2032.

In addition, transaction volumes could climb to about 7.2 trillion dollars by 2030. This growth is being driven largely by digital payments adoption and the rapid expansion of Banking-as-a-Service infrastructure.

Market Insights:

- Customer expectations are shifting toward instant, contextual financial services delivered without app switching. This demand is rising as platforms like Shopify and Salesforce continue to dominate digital ecosystems.

- By embedding financial services within trusted environments, banks and enterprises gain wider distribution, deeper transaction-level data insights, and lower customer acquisition costs.

- SMBs, which represent 57% of B2B card volume, are leading embedded finance adoption.

- Many use one-click payment mechanisms to reduce late payments and improve cash flow. As a result, penetration is projected to rise from 5% in 2021 to 15% by 2026.

- Large enterprises are also modernizing their platforms to embed treasury and credit capabilities. Their priority is API-driven, SaaS-like agility so they can scale faster while keeping pace with evolving Fortune 500 digital strategies.

Enterprises adopt embedded banking to unlock new revenue, improve retention, accelerate innovation, and gain real-time financial visibility without becoming regulated banks.

1. New Revenue Stream Expansion

For many organizations, embedded banking development begins with economics. Financial flows create monetization opportunities that traditional software models cannot match. By embedding payments, credit, or treasury capabilities, platforms can generate interchange income, float revenue, and lending spreads.

Industry data shows enterprises can achieve 2–5x higher customer lifetime value through embedded financial models. In addition, customer acquisition costs can drop by nearly 30% when financial services are delivered within the product experience. Therefore, finance becomes a built-in growth engine rather than a supporting feature. Over time, this shift can materially strengthen unit economics across digital platforms.

2. Customer Journey Ownership

Customer experience remains a major adoption driver. When users must leave a platform to complete payments or financing, friction increases, and conversion often suffers. Embedded banking removes that break in the journey.

As a result, organizations maintain tighter control over the full financial experience. Platforms that integrate payments and credit directly into workflows often see stronger engagement and repeat usage.

In addition, keeping financial activity inside the ecosystem creates more timely cross-sell opportunities. This level of ownership is becoming essential as digital expectations continue to rise.

3. Ecosystem Platform Lock-In

Financial workflows tend to become deeply embedded in daily operations. Once customers rely on in-platform wallets, payouts, or credit lines, switching becomes more difficult.

This is one reason platforms such as Stripe, Adyen, and Shopify have gained strong ecosystem gravity. Embedded financial services increase platform dependency while raising lifetime value.

Therefore, churn typically declines as financial features mature. For enterprise platforms competing in crowded markets, this stickiness can become a meaningful strategic moat that extends well beyond payments.

4. Faster Fintech Innovation

Historically, launching financial products required heavy regulatory investment. Today, Banking-as-a-Service infrastructure has lowered the entry barrier for non-financial companies.

Enterprises can now embed accounts, payments, and lending into their products without building a full banking stack.

When executed correctly, embedded banking enables fintech-level innovation while avoiding the burden of becoming a licensed bank.

5. Real-Time Financial Data Intelligence

Financial transactions generate some of the richest behavioral data available. Embedded banking gives enterprises direct visibility into cash flow patterns, payment timing, and customer risk signals.

This intelligence supports better underwriting, smarter pricing, and more personalized offers. It also strengthens forecasting and liquidity planning across business units. Many platforms now treat financial telemetry as a strategic asset rather than a byproduct. Therefore, embedded banking increasingly sits at the center of enterprise AI and analytics initiatives.

6. Operational Efficiency and Automation

Beyond growth, embedded banking also improves internal efficiency. Integrated financial workflows reduce manual reconciliation, fragmented payment handling, and back-office overhead.

This is especially important in B2B environments, where SMBs account for 57% of card volume and frequently struggle with late payments. Embedded one-click payment flows and real-time treasury visibility directly address these pain points.

As transaction volumes increase, automation becomes even more valuable. Finance and operations teams gain clearer cash visibility while reducing error rates and manual effort.

Forward-looking enterprises now view embedded banking as a strategic growth layer rather than a payment feature.

What Is an Embedded Banking Platform?

An embedded banking platform enables enterprises to offer regulated financial services such as payments, accounts, and lending directly inside their digital products.

An embedded banking platform allows a business to build financial services directly into its own app, portal, or software environment. Instead of sending users to a traditional bank, the enterprise delivers capabilities like payments, accounts, cards, or lending within the same workflow. This keeps the financial experience seamless and under the company’s control.

Behind the scenes, the platform connects to licensed banking partners and financial rails. However, the user interacts only with the enterprise interface. As a result, organizations can create smoother journeys while opening new revenue opportunities.

For enterprises focused on scale, embedded banking development is less about adding payments and more about building governed financial infrastructure that fits naturally into existing products and operations.

How Embedded Banking Differs From Traditional Banking

Traditional banking was built around the bank as the center of the customer experience. Users typically leave the primary product, visit a bank channel, and complete financial tasks there.

Embedded banking changes this model. Financial services now appear directly inside the platform people already use, which reduces friction and keeps the experience connected.

| Area | Traditional Banking | Embedded Banking |

| Customer journey | Users move to the bank’s app or branch | Financial services appear inside the enterprise platform |

| Experience control | The bank controls most of the flow | Enterprise controls the user experience |

| Speed and flexibility | Slower to adapt and launch | Faster through API-driven infrastructure |

| Data visibility | Data stays largely with the bank | Enterprise gains richer transaction insights |

| Platform value | Banking is a separate activity | Finance becomes part of the core product |

In simple terms, traditional banking pulls users toward the bank. Embedded banking brings financial services to where users already work.

Therefore, enterprises gain more control, better data visibility, and stronger customer engagement as financial capabilities become part of the product itself.

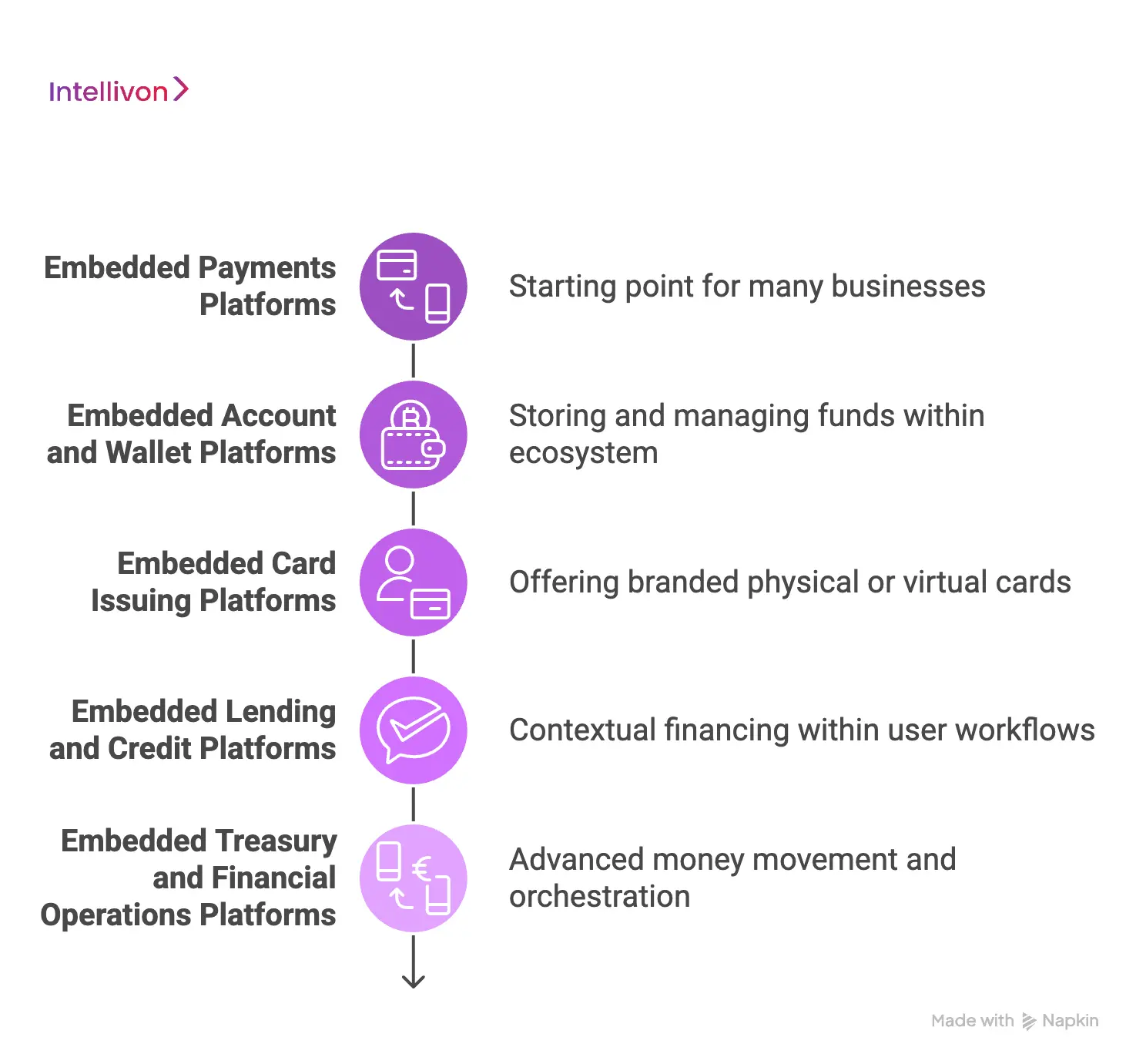

Types of Embedded Banking Platforms Enterprises Deploy

Enterprises deploy different types of embedded banking platforms based on use case, including payments, wallets, cards, lending, and treasury orchestration.

Enterprises adopt embedded banking in different ways depending on their business model and customer needs. Some begin with payments, while others focus on wallets, cards, or credit. The right path depends on which financial workflow the platform wants to control first.

However, mature organizations rarely stop at one capability. As programs expand, many combine multiple embedded banking models to support more complex financial journeys and revenue streams. Below are the most common types of enterprises deployed today:

1. Embedded Payments Platforms

This is often the starting point. These platforms allow businesses to accept, move, or disburse money directly within their product.

Common capabilities include:

- Payment acceptance

- In-app checkout

- Vendor and supplier payments

- Marketplace payouts

- Subscription billing

Example: Adyen

Adyen enables global enterprises to unify online, mobile, and in-store payments through one platform. Businesses gain a single view of transactions while maintaining full control of the customer experience.

Because payments sit at the center of many digital journeys, this model helps reduce friction and improve conversion. Therefore, many enterprises begin their embedded banking development here.

2. Embedded Account and Wallet Platforms

Wallet and account platforms allow enterprises to store and manage funds within their ecosystem. Instead of pushing money out immediately, the platform can hold balances and support internal transfers.

Typical features include:

- User wallets

- Virtual accounts

- Balance tracking

- Internal money movement

- Multi-party fund management

Example: GrabPay

Grab integrates a wallet into its super app, enabling users to pay for rides, food, and services from a stored balance. This keeps financial activity inside the platform.

This model increases platform stickiness and enables real-time financial workflows. However, it requires strong ledger design and reconciliation discipline.

3. Embedded Card Issuing Platforms

Card issuing platforms allow enterprises to offer branded physical or virtual cards linked to their ecosystem. These cards can support spending, payouts, or expense control.

Common use cases include:

- Employee expense cards

- Contractor payout cards

- Fleet and fuel cards

- Travel and benefit cards

- Virtual cards for controlled spending

Example: Brex

Brex provides corporate cards embedded into its spend management platform. Companies can issue cards instantly and control spending through built-in policies.

This approach creates new revenue opportunities through interchange. In addition, it gives enterprises tighter control over how funds move within their programs.

4. Embedded Lending and Credit Platforms

Credit and financing capabilities are one of the fastest-growing areas of embedded banking. These platforms allow businesses to offer contextual financing directly within user workflows.

Typical offerings include:

- Buy now, pay later

- Working capital loans

- Merchant financing

- Invoice financing

- Earned wage access

Example: Amazon Lending

Amazon offers working capital loans to eligible sellers directly within Seller Central. Merchants can access funding without leaving the platform.

Because financing appears at the point of need, adoption rates are often strong. As a result, many platforms use embedded credit to increase transaction volume and customer retention.

5. Embedded Treasury and Financial Operations Platforms

This is the more advanced category. These platforms focus on enterprise-grade money movement, liquidity visibility, and financial orchestration.

Capabilities often include:

- Multi-entity fund flows

- Automated reconciliation

- Cash position visibility

- Multi-bank routing

- Settlement orchestration

- Financial reporting alignment

Example: Stripe Treasury

Stripe Treasury allows platforms to offer financial accounts and manage fund flows within their ecosystem. Businesses can programmatically move and track money.

Large marketplaces and complex SaaS platforms often invest here as they scale. This layer becomes critical when transaction volume and ecosystem complexity increase.

Mature enterprises rarely rely on a single embedded banking model. Instead, they combine payments, wallets, cards, and credit capabilities to build fully integrated financial ecosystems that support long-term platform growth.

Architecture Of An Embedded Banking Platform For Enterprises

An enterprise embedded banking architecture includes sponsor banks, BaaS connectivity, payment rails, ledger systems, risk controls, and an orchestration layer that governs financial operations at scale.

Building an embedded banking platform is not just about plugging into payment APIs. Enterprise programs rely on a layered architecture that keeps money movement compliant, traceable, and reliable under real transaction load. Each layer plays a specific role. When one is weak, risk and operational issues surface quickly.

Below is how mature enterprises structure embedded banking development for long-term scale.

1. The Sponsor Bank Layer (Regulatory Foundation)

At the base sits the sponsor bank. This is the licensed financial institution that legally holds funds and enables regulated banking services. Without this layer, most embedded banking programs cannot operate in regulated markets.

The sponsor bank typically handles:

- Regulatory oversight

- Funds safeguarding

- Settlement access

- Program supervision

- Compliance alignment

For enterprises, this layer provides the legal foundation. However, the bank usually stays behind the scenes while the platform owns the user experience.

2. The Banking-as-a-Service (BaaS) Layer

The BaaS layer acts as the technical bridge between the sponsor bank and the enterprise platform. It exposes APIs that allow businesses to programmatically access accounts, payments, and card capabilities.

What BaaS provides:

- Account and payment APIs

- Card issuing connectivity

- Basic compliance primitives

- Bank network access

- Developer-friendly integration

This matters because it reduces the complexity of connecting directly to banking infrastructure. Enterprises can launch financial features much faster than before.

However, BaaS alone does not solve enterprise-scale challenges. Most providers focus on connectivity, not on the deeper controls large organizations require. As programs grow, gaps often appear in governance, reconciliation, and multi-entity oversight.

3. Payment Rails and Money Movement Infrastructure

Behind the APIs, money still moves through established payment rails. These networks determine how quickly and reliably funds travel between parties.

Common rails include:

- ACH and bank transfers

- RTP and instant payment networks

- Card networks such as Visa and Mastercard

- Regional systems such as UPI, NEFT, or SEPA

- Cross-border payment networks

Enterprises must design routing, settlement timing, and redundancy carefully. Otherwise, payment delays and reconciliation gaps can emerge as volume grows.

4. Ledger and Financial Accounting Engine

This is one of the most critical layers in embedded banking development. The ledger is the system of record that tracks every financial movement inside the platform.

A strong ledger enables:

- Accurate balance tracking

- Double-entry accounting

- Real-time financial visibility

- Automated reconciliation

- Full audit trail

Many platforms underestimate this layer early on. However, as transaction volume increases, finance teams depend on clean ledger integrity to maintain trust.

Intellivon typically treats the ledger as core financial infrastructure, not as a reporting add-on. This approach helps enterprises maintain financial truth even under complex, multi-entity conditions.

5. Risk, Fraud, and AML Intelligence Layer

Every transaction must pass through risk and fraud controls. This layer continuously monitors activity to detect suspicious behavior and reduce financial exposure.

Key capabilities include:

- Transaction monitoring

- Sanctions and watchlist screening

- Fraud detection models

- Velocity and behavioral checks

- Case management workflows

Strong programs embed these controls directly into payment flows. As a result, risk decisions happen in real time rather than after funds move.

6. Identity and Compliance Infrastructure

Before money can move, the platform must verify who the customer is. The identity and compliance layer supports regulated onboarding and ongoing due diligence.

Typical functions include:

- KYC and KYB verification

- Document validation

- Beneficial ownership checks

- Consent capture

- Ongoing customer monitoring

- Regulatory reporting support

Enterprises must design this layer carefully for each region in which they operate. Poor identity controls often become the first point of regulatory concern.

7. Enterprise Orchestration and Governance Layer

This is where enterprise programs either mature or struggle. The orchestration layer governs how financial workflows operate across the platform.

It typically manages:

- Role-based permissions

- Approval workflows

- Transaction limits

- Policy enforcement

- Multi-entity controls

- Program configuration

- Exception handling

In many large-scale environments, this layer becomes the true control center. Intellivon focuses heavily here because enterprises need more than basic connectivity. They need structured financial governance that remains stable as ecosystems grow.

When designed correctly, this layer turns embedded banking into a reliable enterprise infrastructure.

8. Enterprise Application and User Experience Layer

At the top sits the enterprise product where users interact with financial features. This includes the app, portal, or platform interface.

From the user’s perspective, this is all they see. They can:

- Make payments

- Access wallets

- view balances

- request financing

- manage cards

However, the experience only remains smooth when the deeper infrastructure layers work together reliably.

The strength of an embedded banking program depends far more on orchestration and control than on connectivity alone.

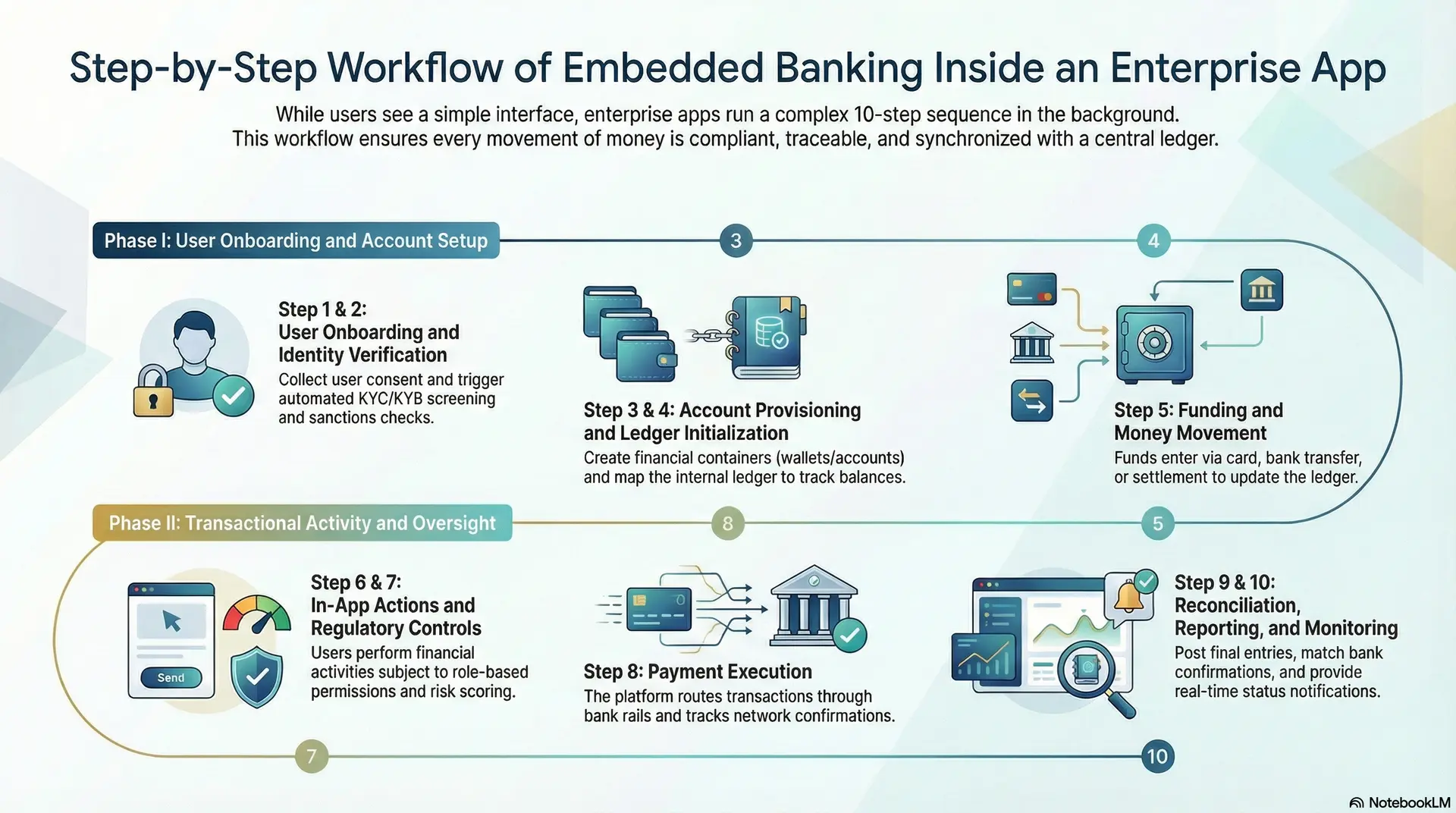

Step-by-Step Workflow of Embedded Banking Inside an Enterprise App

Embedded banking workflows move from user onboarding to identity verification, account creation, transaction execution, and real-time reconciliation within the enterprise platform.

Understanding the workflow helps clarify how embedded banking development actually operates in production.

While the user sees a simple interface, several controlled steps run in the background to keep money movement compliant and traceable. Mature enterprises design this flow carefully to avoid operational gaps later. Below is a typical step-by-step sequence inside a modern enterprise platform.

Step 1: User Onboarding and Consent

The process begins when a user signs up for a financial feature inside the platform. This could be a wallet, payment capability, or card access.

At this stage, the platform collects:

- Basic user information

- Terms acceptance

- Required disclosures

- Consent for data use

Clear consent is important because regulators expect full transparency before financial services are activated.

Step 2: Identity Verification

Once onboarding starts, the platform triggers identity checks. This step ensures the user or business meets regulatory requirements.

Typical checks include:

- KYC for individuals

- KYB for businesses

- Document validation

- Sanctions screening

- Beneficial owner verification

Strong identity controls help prevent fraud and reduce compliance exposure. Therefore, many enterprises automate this step with risk-based workflows.

Step 3: Account or Wallet Provisioning

After verification, the platform creates a financial container for the user. Depending on the use case, this may be:

- A virtual account

- A stored-value wallet

- A card-linked account

- A sub-ledger balance

At this point, the user can begin interacting with financial features inside the platform.

Step 4: Ledger Initialization

As soon as the account is created, the ledger system begins tracking balances. Every movement must be recorded accurately.

The ledger typically:

- Creates the opening balance

- Assigns internal identifiers

- Maps the account structure

- Prepares reconciliation links

This step is critical for maintaining financial truth as volume grows.

Step 5: Funding and Money Movement

Next, funds enter the system. This may happen through payments, transfers, settlements, or deposits.

Common funding methods include:

- Card payments

- Bank transfers

- Marketplace settlements

- Payroll loads

- Invoice payments

As funds arrive, the platform updates the ledger and confirms the balance in real time.

Step 6: In-App Financial Actions

Once funded, users can perform financial activities without leaving the enterprise platform.

Typical actions include:

- Sending payments

- Paying suppliers

- Requesting payouts

- Using issued cards

- Accessing credit

Because the experience stays inside the product, user friction drops and engagement improves.

Step 7: Controls and Approvals

Before transactions execute, the platform evaluates policy rules. This step protects the enterprise from risk and misuse.

Common controls include:

- Role-based permissions

- Transaction limits

- Velocity checks

- Risk scoring

- Multi-level approvals

Well-designed approval flows are especially important in B2B environments where multiple stakeholders may be involved.

Step 8: Payment Execution

After passing controls, the platform routes the transaction through the appropriate payment rail. The sponsor bank and network partners process the movement of funds.

At this stage, the system tracks:

- Transaction status

- Settlement timing

- Network confirmations

- Failure handling

Reliable execution is essential for maintaining user trust.

Step 9: Reconciliation and Reporting

Once the transaction completes, the platform updates financial records. This is where many weaker implementations struggle.

Strong enterprise systems:

- Post final ledger entries

- Match bank confirmations

- Flag discrepancies

- Generate audit records

- Update reporting dashboards

Accurate reconciliation ensures finance teams always have a clean view of cash movement.

Step 10: Notifications and Ongoing Monitoring

Finally, the platform sends real-time updates back to the user and internal teams. Monitoring continues even after the transaction completes.

Typical outputs include:

- User notifications

- Status webhooks

- Risk alerts

- Operational dashboards

- Compliance logs

Continuous monitoring helps enterprises detect issues early and maintain program stability.

When designed correctly, this workflow runs quietly in the background while delivering a seamless financial experience to end users.

Compliance and Regulatory Guardrails Enterprises Must Follow

Enterprise embedded banking platforms must meet regulatory licensing, KYC, and AML rules, funds safeguarding standards, PCI security, and strong operational resilience requirements.

Embedded banking development brings clear growth benefits. However, it also introduces serious regulatory responsibilities. Financial services are tightly supervised in most markets. Therefore, enterprises must build compliance into the platform from day one rather than adding it later.

Below are the key guardrails mature organizations put in place.

1. Regulatory and Licensing Structure

Every embedded banking program must operate under a valid regulatory model. In most cases, the enterprise partners with a licensed sponsor bank or regulated financial institution.

This structure typically defines:

- Who holds customer funds

- Who manages compliance obligations?

- How reporting flows to regulators

- What activities can the enterprise perform?

Enterprises must document roles clearly across the bank, BaaS provider, and platform operator. When this structure is vague, programs often face delays during audits or partner reviews. Therefore, early legal alignment is essential for long-term stability.

2. KYC and KYB Requirements

Before enabling financial activity, platforms must verify the identity of users and businesses. This process is known as Know Your Customer and Know Your Business.

A strong identity framework usually includes:

- Customer identification checks

- Document verification

- Beneficial ownership validation

- Risk-based onboarding

- Ongoing customer reviews

Enterprises should also support enhanced due diligence for higher-risk users. Regulators expect identity controls to remain active throughout the customer lifecycle, not only at onboarding.

3. AML and Transaction Monitoring

Anti-money laundering controls are critical once transactions begin to flow. Regulators expect continuous monitoring that can detect suspicious behavior in real time.

Mature platforms typically implement:

- Transaction monitoring rules

- Sanctions and watchlist screening

- Politically exposed person checks

- Behavioral risk scoring

- Case management workflows

- Regulatory reporting support

Weak monitoring is one of the most common reasons financial programs face regulatory pressure. Therefore, enterprises must treat AML as an always-on capability.

4. Funds Safeguarding Obligations

Enterprises that handle customer money must ensure those funds remain protected at all times. Regulators pay close attention to how balances are stored and reconciled.

Key expectations include:

- Segregation of customer funds

- Accurate sub-ledger tracking

- Daily reconciliation with banking partners

- Clear settlement visibility

- Dispute and chargeback handling

Strong safeguarding controls help maintain customer trust and reduce financial risk. In addition, they support smoother sponsor bank relationships as programs scale.

5. Data Security and Privacy Controls

Embedded banking platforms process highly sensitive financial and identity data. As a result, security and privacy requirements are strict.

These enterprises should implement:

- Encryption in transit and at rest

- Role-based access controls

- Secure key management

- API protection and rate limiting

- Data retention policies

- Regional privacy compliance

Organizations operating across regions must also align with local data regulations. Poor data controls can quickly become a regulatory concern.

6. Card Network and PCI Requirements

If the platform issues or processes cards, additional network rules apply. Card schemes and security standards impose strict technical and operational controls.

Typical requirements include:

- PCI DSS compliance

- Tokenization support

- Chargeback management

- Fraud monitoring thresholds

- Secure card data handling

Enterprises should treat PCI readiness as foundational infrastructure. Retrofitting card security later often becomes expensive and disruptive.

7. Operational Resilience Expectations

Financial platforms are expected to remain reliable even under stress. Regulators and sponsor banks increasingly review operational resilience during program evaluations.

Strong enterprise programs typically include:

- High-availability architecture

- Disaster recovery planning

- Idempotent transaction handling

- Incident response procedures

- Third-party risk management

- Continuous system monitoring

Operational discipline ensures financial services remain stable as transaction volumes grow.

Enterprises that treat compliance as built-in infrastructure, rather than a checklist, are far better positioned to scale embedded banking programs with confidence.

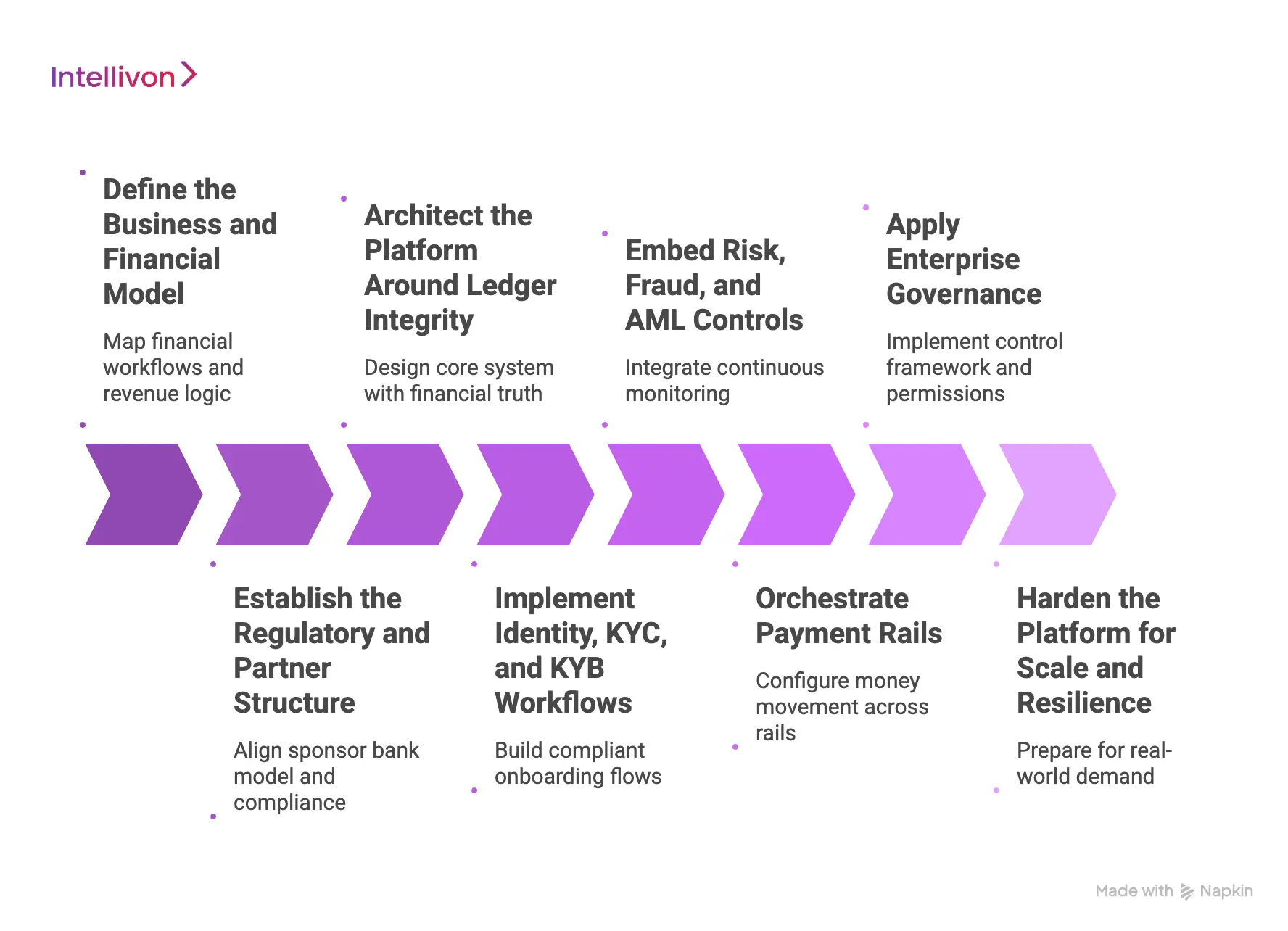

How We Build an Embedded Banking Platform for Enterprises

Building embedded banking for enterprise scale requires more than connecting APIs. The platform must stay stable under growth, pass partner scrutiny, and maintain clean financial records at all times.

At Intellivon, we follow a structured delivery approach that balances speed with long-term control. Each step focuses on reducing risk while preparing the platform for real transaction volume. Below is the process we typically use.

1. Define the Business and Financial Model

We begin by mapping the exact financial workflows the enterprise wants to support. This includes users, money movement paths, and revenue logic.

Early clarity prevents redesign later. It also aligns product, finance, and risk teams around one operating model. As a result, the platform starts with a clear commercial and operational foundation.

2. Establish the Regulatory and Partner Structure

Next, we define how the program will operate within regulated frameworks. We align the sponsor bank model, BaaS connectivity, and compliance ownership.

This step ensures roles are clearly documented. It also reduces friction during bank reviews and audits. A strong legal structure early on supports smoother scaling later.

3. Architect the Platform Around Ledger Integrity

We design the core system with financial truth at the center. The ledger must accurately track every movement from day one. Therefore, we focus on balance accuracy, posting rules, and reconciliation readiness.

This prevents finance teams from losing visibility as volume increases. Over time, it builds trust in the platform’s financial reporting.

4. Implement Identity, KYC, and KYB Workflows

Once the foundation is set, we build compliant onboarding flows. These workflows verify users while keeping the experience simple. We include document checks, beneficial ownership validation, and risk-based reviews.

Ongoing monitoring is also built in. This keeps the platform aligned with regulatory expectations across the customer lifecycle.

5. Embed Risk, Fraud, and AML Controls

We then integrate continuous monitoring into the transaction flow. Risk checks run in real time rather than after funds move.

This includes sanctions screening, transaction monitoring, and behavioral controls. Early detection reduces financial exposure. It also strengthens sponsor bank confidence in the program.

6. Orchestrate Payment Rails

Next, we configure how money moves across rails such as ACH, RTP, and card networks. We design routing, retries, and status tracking carefully.

This ensures payments remain reliable under load. Clear settlement visibility also helps finance teams reconcile faster. As transaction volume grows, this discipline becomes critical.

7. Apply Enterprise Governance

At this stage, we implement the control framework enterprises rely on. We configure role-based permissions, approval flows, and transaction limits. Every action becomes traceable.

This layer helps organizations maintain oversight across multiple users and entities. Therefore, governance remains strong even as the ecosystem expands.

8. Harden the Platform for Scale and Resilience

Finally, we prepare the platform for real-world demand. We add monitoring, failover readiness, and operational dashboards. Continuous observability helps teams detect issues early. In addition, resilience planning keeps services stable during peak load. This step ensures the platform can support long-term growth with confidence.

By following this structured approach, Intellivon helps enterprises launch embedded banking platforms that are not only fast to deploy but also stable, compliant, and ready to scale.

Conclusion

Embedded banking is no longer a side capability. It is becoming core digital infrastructure for enterprises that want tighter control over financial flows and customer experience.

However, long-term success depends on building with discipline from the start. Connectivity alone is not enough. Platforms must combine strong governance, clean ledger integrity, and continuous risk visibility to remain stable as they scale.

Enterprises that invest early in the right architecture position themselves for faster innovation and stronger unit economics. With Intellivon’s enterprise-grade approach, organizations can move beyond basic integrations and build embedded banking platforms designed for durable growth and operational confidence.

Build an Embedded Banking Platform With Intellivon

At Intellivon, embedded banking platforms are engineered as governed financial infrastructure, not as payment features layered onto disconnected systems. Every architectural and delivery decision focuses on financial integrity, workflow alignment, and real-time reliability across complex enterprise environments.

As embedded programs expand across regions, entities, and partner ecosystems, consistency becomes essential. Governance, reconciliation accuracy, and risk visibility remain stable even as transaction volume, user growth, and financial complexity increase.

Therefore, organizations retain full control over financial operations while continuing to unlock new revenue and efficiency gains at scale.

Why Partner With Intellivon?

- Enterprise-grade embedded banking architecture designed for regulated financial ecosystems

- Proven delivery across high-volume platforms, marketplaces, and digital enterprise environments

- Compliance-by-design approach with built-in governance, audit readiness, and sponsor bank alignment

- Secure, modular infrastructure supporting cloud, hybrid, and on-prem deployments

- AI-enabled risk intelligence, financial monitoring, and workflow automation with strong oversight controls

Book a strategy call to explore how Intellivon can help you design and scale embedded banking platforms with confidence, control, and long-term enterprise value.

FAQs

Q1. What is embedded banking development, and how is it different from embedded finance?

A1. Embedded banking development focuses specifically on integrating regulated banking capabilities such as accounts, payments, cards, and treasury functions into enterprise platforms.

Embedded finance is broader and may include insurance or investment features. In enterprise environments, embedded banking usually requires deeper compliance controls and stronger ledger infrastructure because it directly handles regulated money movement.

Q2. How long does it take to build an enterprise embedded banking platform?

A2. Timelines vary based on scope, regulatory complexity, and integration depth. Most enterprise programs take between four and nine months for a production-ready launch.

However, large multi-entity environments may take longer. Early alignment with sponsor banks and strong architecture planning usually reduces delays later in the build cycle.

Q3. Do enterprises need a banking license to launch embedded banking?

A3. In most cases, enterprises do not need their own banking license. Instead, they partner with a licensed sponsor bank and use Banking-as-a-Service infrastructure to access regulated rails.

However, the enterprise still carries significant compliance and operational responsibilities. Therefore, strong governance and risk controls remain essential even without direct licensing.

Q4. What are the biggest risks when scaling embedded banking programs?

A4. The most common risks appear after launch rather than during initial deployment. Enterprises often face challenges around reconciliation gaps, weak transaction monitoring, unclear fund flows, and limited program governance.

As transaction volume grows, these issues can create audit pressure and operational stress. Building with financial truth and control in mind helps reduce these risks early.

Q5. How can enterprises ensure long-term success with embedded banking?

A5. Long-term success depends on treating embedded banking as core financial infrastructure rather than a simple feature. Enterprises should prioritize clean ledger design, real-time risk monitoring, strong identity controls, and enterprise-grade governance workflows.

In addition, choosing an experienced implementation partner such as Intellivon helps ensure the platform remains stable, compliant, and ready to scale.