Building a Banking-as-a-Service (BaaS) platform in the United States is much more than launching a new product. For many companies, this shift is a strategic effort to gain control over embedded finance offerings, create new revenue streams, and reduce reliance on external providers. The question then lies in what the true costs are involved in developing a secure and compliant BaaS platform.

In the US market, costs are shaped by several factors, including regulatory requirements, sponsor bank relationships, platform design, security measures, and ongoing operational needs. Under these circumstances, treating BaaS as a simple fintech project often leads to underestimated budgets and missed challenges, especially when aiming for enterprise-level reliability and scalability.

Intellivon approaches BaaS platform development as a regulated fintech infrastructure, and not merely as an add-on to existing systems. This blog draws from our experience and will explain what the main cost drivers are, the potential hidden expenses, architectural considerations, and strategic decisions that influence the process of building a BaaS platform in the United States.

Why Enterprises Are Investing in BaaS Platforms Now

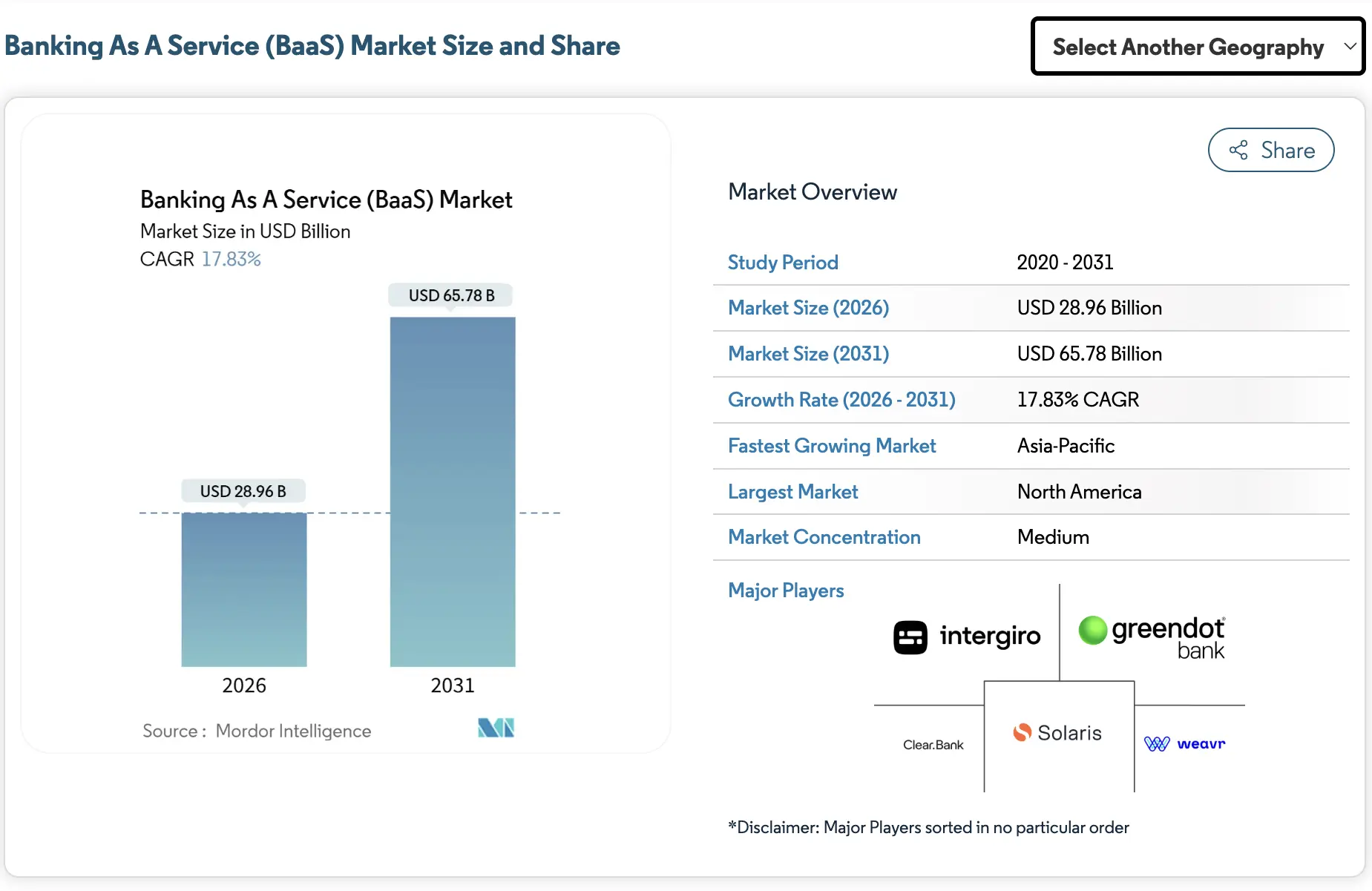

Enterprises are increasingly adopting Banking-as-a-Service platforms to embed payments, lending, and account services directly into their operations. This approach helps them launch financial features quickly without investing in complex, expensive infrastructure.

Demand from small and mid-sized businesses continues to grow. At the same time, modern technology makes it easier to innovate and scale these services with confidence.

Small and mid-sized businesses are expected to drive this growth, capturing around 56.2% of revenue as they prioritize affordable digital wallets and credit over legacy systems.

Market Insights:

- Open banking rules and modern APIs enable smooth integrations, so non-banks can launch financial services quickly and expand financial inclusion.

- Cloud-native platforms improve scalability and cost efficiency, reducing development timelines from years to just months for personalized offerings.

- Trusted distribution channels can reduce customer acquisition costs by more than 30%.

- Small and mid-sized businesses, expected to capture about 56% of revenue, are driving the adoption of affordable wallets and credit solutions.

Enterprises are moving quickly toward Banking-as-a-Service because financial capabilities are becoming a core part of digital strategy. Instead of relying on external providers for every financial function, organizations now want more control and flexibility. BaaS makes this shift practical. It allows teams to embed regulated financial services into existing products without building a full banking infrastructure from scratch.

As competition intensifies, leaders are also looking for faster ways to launch new offerings and capture additional revenue streams.

Therefore, BaaS is becoming a strategic platform decision that directly affects growth, customer experience, and long-term economics.

1. New Embedded Finance Revenue Streams

BaaS opens new monetization paths that traditional product models cannot easily support. Companies can generate revenue from payments, card programs, lending products, and value-added financial services.

In addition, embedded finance increases customer lifetime value because users can complete more activities within one ecosystem.

For many enterprises, this shift turns financial services from a cost center into a measurable growth driver.

2. Faster Product Launch Cycles

Speed to market has become a competitive requirement. BaaS platforms provide pre-built financial rails, which significantly reduce development time. As a result, organizations can introduce new financial features in months instead of years.

This faster launch cycle also supports rapid experimentation. Teams can test new offerings, refine pricing models, and respond quickly to market changes without rebuilding core infrastructure.

3. Greater Control Over Financial Data

Financial data is becoming one of the most valuable enterprise assets. When organizations rely heavily on third-party providers, visibility and control often become limited. BaaS platforms help bring that control back in-house.

With better data access, teams can improve risk models, personalize financial products, and strengthen compliance monitoring. Therefore, many enterprises see BaaS as both a growth and governance investment.

4. Ecosystem and Partner Expansion

Modern digital platforms rarely operate in isolation. They depend on marketplaces, partners, and developer ecosystems. BaaS supports this model by enabling secure financial capabilities across multiple participants.

For example, platforms can onboard partners faster, support multi-party payment flows, and create new embedded finance experiences across their ecosystem. This flexibility becomes especially valuable as platforms scale across regions and business lines.

5. Tokenized Asset and Digital Finance Opportunities

Forward-looking enterprises are also preparing for programmable and tokenized financial models. While not every organization needs these capabilities immediately, platform readiness matters.

Systems designed with flexible ledgers and strong identity controls can support future digital asset use cases without costly redesign.

This is where architecture decisions made today influence long-term platform economics. Enterprises that plan early gain more room to innovate as financial products continue to evolve.

What Is a Banking-as-a-Service (BaaS) Platform?

A Banking-as-a-Service platform is a regulated technology layer that allows companies to offer financial services such as payments, accounts, cards, and lending through APIs. Instead of building a bank from scratch, the enterprise connects to licensed sponsor banks and financial networks through the BaaS provider.

This model lets organizations launch embedded finance features faster while staying within regulatory boundaries. The platform typically manages core functions like ledger operations, compliance checks, identity verification, and transaction processing.

As a result, businesses can deliver banking capabilities inside their existing products without owning a full banking infrastructure.

How BaaS Differs from Embedded Banking

BaaS provides the regulated financial infrastructure, while embedded banking delivers the user-facing financial experience inside digital products.

Many teams use the terms BaaS and embedded banking as if they mean the same thing. However, they operate at different layers of the financial stack. Banking-as-a-Service focuses on the regulated infrastructure that powers financial features. Embedded banking, on the other hand, describes how those features appear inside customer-facing products.

Understanding this distinction matters during platform planning. It affects architecture decisions, compliance, ownership, and long-term cost. Enterprises that confuse the two often underestimate the effort required to scale safely.

BaaS vs Embedded Banking Comparison

| Area | Banking-as-a-Service (BaaS) | Embedded Banking |

| Primary role | Provides a regulated financial infrastructure | Delivers financial features within the user experience |

| Position in the stack | Back-end platform layer | Front-end product layer |

| Compliance responsibility | Managed through the sponsor bank and BaaS controls | Depends on the underlying BaaS infrastructure |

| Typical users | Fintech platforms, large enterprises, and SaaS providers | Marketplaces, apps, digital platforms |

| Key focus | APIs, ledger, compliance, processing | Customer experience and workflows |

| Implementation effort | Higher architectural complexity | Faster feature-level integration |

In simple terms, BaaS is the engine that makes embedded finance possible. Embedded banking is the experience customers see. Therefore, enterprises evaluating the true BaaS platform cost must assess both the infrastructure layer and the product layer together to avoid gaps later.

Core Components of a BaaS Platform

A BaaS platform typically includes API orchestration, a ledger system, compliance controls, identity management, payment processing, and partner management capabilities.

A Banking-as-a-Service platform works because several tightly connected components operate together. Each layer supports a different part of the financial workflow.

When enterprises evaluate the true BaaS platform cost, they must look beyond APIs and consider the full infrastructure stack. Below are the core building blocks that power a modern BaaS environment.

1. API Gateway and Developer Layer

The API gateway acts as the front door to the platform. It allows enterprise applications and partners to securely access banking functions. In addition, it manages authentication, rate limits, and traffic routing.

A well-designed developer layer also includes documentation, sandbox environments, and version control. These features help teams launch and scale integrations faster.

2. Core Ledger System

The ledger is the financial source of truth. It records every transaction, balance change, and settlement movement. Therefore, accuracy and real-time visibility are critical.

Enterprise-grade platforms typically use a double-entry ledger model. This approach improves reconciliation, auditability, and financial integrity at scale.

3. Identity and Compliance Engine

Financial services require strong identity verification and regulatory checks. This layer handles KYC, AML monitoring, sanctions screening, and consent management.

In addition, the compliance engine enforces rules across the transaction lifecycle. This helps organizations meet regulatory obligations without slowing down the user experience.

4. Payment and Card Processing Layer

This component connects the platform to payment rails and card networks. It supports functions such as ACH transfers, wire payments, real-time payments, and card issuing.

Because this layer interacts with external networks, reliability and monitoring are especially important. Any disruption here directly affects customer trust.

5. Partner and Program Management

Most BaaS platforms serve multiple clients or business units. The partner management layer handles onboarding, permissions, revenue sharing, and program configuration.

As ecosystems grow, this component becomes essential for maintaining control and visibility across participants.

Together, these components form the operational backbone of a scalable BaaS platform. Understanding how they interact helps enterprises estimate costs more accurately and avoid architectural surprises later.

How a Banking-as-a-Service Platform Actually Works (Enterprise Workflow)

A BaaS workflow connects the enterprise app, compliance engine, sponsor bank, and payment rails to process financial transactions securely in real time.

At a high level, a Banking-as-a-Service platform sits between the enterprise application and regulated financial networks. It orchestrates identity checks, transaction processing, ledger updates, and settlement flows. Although the user experience appears simple, several coordinated steps happen behind the scenes.

Understanding this workflow helps leaders estimate the real BaaS platform cost. It also clarifies where compliance, risk, and performance controls must operate.

Step 1: Customer Initiates a Financial Action

The process begins when a user performs an action inside the enterprise product. This could be opening an account, making a payment, or requesting a loan.

From the user’s perspective, the experience feels native to the platform. However, the request immediately moves into the BaaS orchestration layer for validation and routing.

Step 2: Enterprise App Sends Secure API Request

Next, the enterprise system sends the request through secure APIs to the BaaS platform. The API gateway authenticates the call and checks permissions.

At this stage, the platform ensures the request format, user credentials, and session controls meet security requirements. Clean API design is critical because every transaction flows through this entry point.

Step 3: Identity Verification and Compliance Checks

Before any funds move, the platform runs identity and regulatory checks. This typically includes KYC verification, AML screening, and sanctions monitoring.

If the transaction passes all rules, processing continues. If not, the system flags or blocks the activity. Therefore, this step plays a major role in managing regulatory risk.

Step 4: Transaction Processing Through Sponsor Bank

Once approved, the BaaS platform routes the transaction to the licensed sponsor bank. The bank executes the regulated financial action, such as holding deposits or issuing cards.

The platform maintains orchestration control while the bank provides the regulated backbone. Strong alignment between these layers is essential for reliable operations.

Step 5: Ledger Update and Balance Reconciliation

After the bank processes the transaction, the BaaS ledger records the balance change. The ledger acts as the system of record for all financial movements.

Real-time updates help maintain accuracy across accounts, reports, and downstream services. In addition, automated reconciliation reduces operational overhead.

Step 6: Payment Rail Execution and Settlement

For payment flows, the platform connects to the appropriate network. This may include ACH, card rails, wires, or real-time payment systems.

Settlement timing depends on the rail used. However, the BaaS platform continues to track status updates and exceptions throughout the process.

Step 7: Confirmation Returned to the Application

Finally, the platform sends a confirmation response back to the enterprise product. The user sees the completed action inside the application interface.

Behind the scenes, monitoring, audit logging, and reporting continue to run. This ensures full traceability for compliance and operational teams.

In practice, a modern BaaS platform coordinates many moving parts in milliseconds. Therefore, enterprises evaluating platform investment should assess not only feature scope but also the depth of orchestration required to run these workflows safely at scale.

Typical BaaS Architecture for US-Regulated Environments

In the United States, Banking-as-a-Service platforms must operate under strict regulatory and security expectations. Therefore, architecture decisions made early have a direct impact on compliance posture, scalability, and long-term cost. Many platforms work well at a small scale but struggle once transaction volume and regulatory scrutiny increase.

At Intellivon, BaaS systems are designed as regulated fintech infrastructure from the ground up. This architecture-first approach helps enterprises avoid expensive rework while maintaining performance and audit readiness as programs grow.

Below are the core architectural layers that define an enterprise-grade BaaS environment.

1. Multi-Tenant vs Single-Tenant Design

Tenant strategy shapes both scalability and operational control. A single-tenant model gives each client isolated infrastructure, which can simplify certain compliance scenarios. However, it often increases infrastructure cost and slows ecosystem expansion.

A multi-tenant design allows multiple programs to run on shared, logically separated infrastructure. When implemented correctly, it improves efficiency and speeds partner onboarding. Therefore, many enterprise platforms prefer a secure multi-tenant approach with strong isolation controls.

2. Core Ledger and Double-Entry Accounting Layer

The ledger is the financial backbone of the platform. Every balance change, fee, and settlement event must pass through this system. Accuracy and real-time visibility are essential.

Enterprise BaaS platforms typically use double-entry accounting to maintain financial integrity. This method ensures that every debit has a matching credit. As transaction volume grows, a well-architected ledger prevents reconciliation issues and reporting gaps.

3. API Gateway and Developer Platform

The API gateway manages how external applications interact with the BaaS environment. It handles authentication, traffic management, throttling, and request validation.

A mature developer platform also includes sandbox access, version control, and detailed documentation. These capabilities help internal teams and partners integrate faster while maintaining security standards. As ecosystems expand, strong API governance becomes increasingly important.

4. Identity and Access Infrastructure

Identity controls sit at the center of regulatory compliance. This layer manages user verification, role-based access, consent tracking, and session security.

In US-regulated environments, identity systems must support KYC workflows and continuous risk monitoring. Weak identity design often creates downstream compliance exposure. Therefore, enterprises benefit from building this layer with long-term scale in mind.

5. Event Streaming and Real-Time Processing

Modern financial experiences depend on real-time data movement. Event streaming infrastructure allows the platform to process transactions, risk signals, and balance updates instantly.

This architecture improves responsiveness and supports advanced capabilities such as real-time fraud detection and dynamic limits. In addition, it reduces reliance on slow batch processes that can create operational delays.

6. Observability and Audit Infrastructure

Regulated financial systems require deep visibility. Observability tools monitor system health, transaction flows, and performance metrics across the platform.

At the same time, audit infrastructure captures detailed logs for compliance reviews and investigations. Strong monitoring helps teams detect anomalies early and maintain regulatory confidence. As oversight increases in the US market, this layer becomes essential rather than optional.

When these architectural components work together, the BaaS platform can scale safely under regulatory pressure.

Enterprises evaluating long-term investment should focus on architectural strength early, because redesigning regulated financial infrastructure later is significantly more expensive.

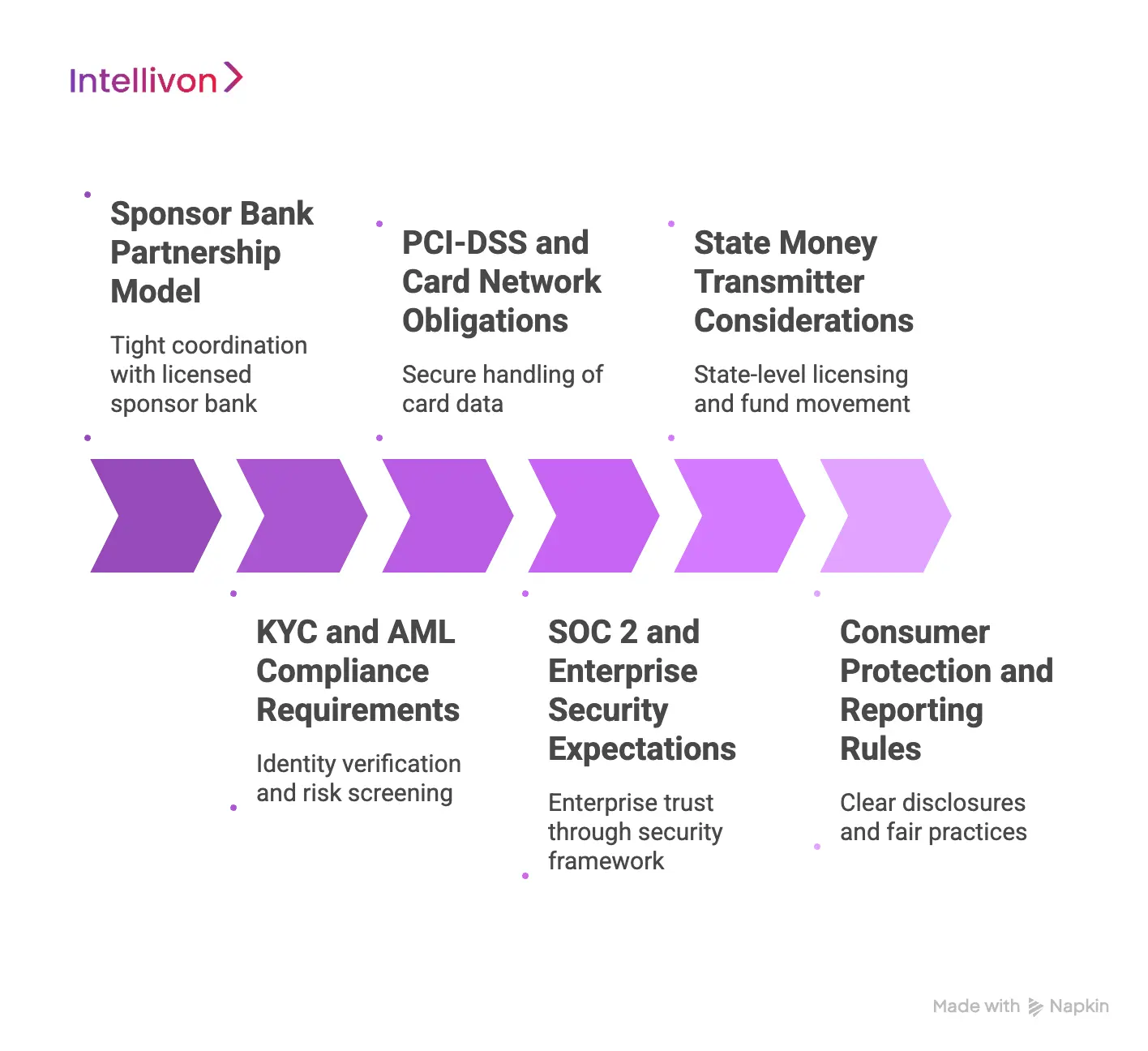

Regulatory Landscape for BaaS Platforms in the USA

BaaS platforms in the United States must align with sponsor bank oversight, KYC and AML rules, PCI-DSS standards, SOC 2 controls, and state-level regulations.

Launching a Banking-as-a-Service platform in the United States requires more than strong engineering. It demands careful alignment with banking partners, federal expectations, and state-level rules. Therefore, regulatory planning should begin early in the platform design phase.

Enterprises that underestimate this landscape often face delays, added cost, and operational friction later. A structured compliance approach helps reduce risk while supporting sustainable scale. Below are the major regulatory areas that shape BaaS platform design in the US market.

1. Sponsor Bank Partnership Model

Most BaaS programs operate through a licensed sponsor bank. The bank holds deposits, issues cards, and provides the regulated foundation for financial activities. Meanwhile, the BaaS platform manages orchestration, user experience, and program controls.

This relationship requires tight coordination. Banks expect strong risk management, clear reporting, and ongoing program oversight. Therefore, platform architecture must support transparency and real-time visibility across all financial flows.

2. KYC and AML Compliance Requirements

Know Your Customer and Anti-Money Laundering rules form the core of financial compliance. Every customer onboarding flow must verify identity and screen for risk signals.

In addition, ongoing transaction monitoring is required to detect suspicious activity. Automated alerts, case management tools, and audit trails are essential. Without these controls, programs can face regulatory action and reputational damage.

3. PCI-DSS and Card Network Obligations

Any platform that handles card data must meet PCI-DSS requirements. These standards govern how payment information is stored, transmitted, and protected.

Card networks also impose their own program rules and certification steps. As a result, enterprises must plan for secure tokenization, encryption, and network testing. Strong controls in this layer help protect both customers and the broader payment ecosystem.

4. SOC 2 and Enterprise Security Expectations

Enterprise buyers increasingly expect SOC 2 alignment as part of vendor due diligence. This framework focuses on security, availability, processing integrity, confidentiality, and privacy.

While SOC 2 is not a banking regulation, it plays a major role in enterprise trust. Platforms that build these controls early often move through partner reviews faster and with fewer remediation cycles.

5. State Money Transmitter Considerations

Depending on the business model, some BaaS programs may trigger state money transmission requirements. These rules vary by jurisdiction and can affect how funds move through the platform.

Because the landscape is complex, many enterprises rely on sponsor bank structures to reduce licensing exposure. However, legal review is still essential to confirm the correct regulatory posture.

6. Consumer Protection and Reporting Rules

US financial programs must also follow consumer protection expectations. These include clear disclosures, fair fee practices, dispute handling, and regulatory reporting.

In addition, agencies expect consistent audit trails and complaint management processes. Platforms that build these safeguards early are better prepared for supervisory review.

In the US market, regulatory readiness directly influences both launch speed and long-term BaaS platform cost. Enterprises that treat compliance as core infrastructure, rather than an afterthought, are better positioned to scale with confidence.

Key Factors That Influence BaaS Platform Development Cost

The cost to build a BaaS platform depends on compliance scope, architecture complexity, integrations, security depth, feature set, and operating model.

Estimating the true BaaS platform cost requires more than counting features. In regulated fintech environments, expenses are driven by architecture depth, compliance coverage, and long-term scalability needs. Two platforms with similar user experiences can have very different build costs behind the scenes.

Therefore, enterprises should evaluate the full technical and regulatory footprint before setting budgets. The table below highlights how major factors typically affect investment levels.

Cost Impact Comparison

| Cost Factor | Lower Cost Scenario | Higher Cost Scenario |

| Compliance scope | Basic KYC only | Full AML, monitoring, reporting |

| Architecture design | Single-tenant, limited scale | Multi-tenant, high availability |

| Banking integrations | One sponsor bank | Multiple banks and payment rails |

| Security controls | Standard protection | Advanced fraud and risk systems |

| Feature scope | Payments only | Cards, lending, multi-product stack |

| Delivery model | Offshore build | Hybrid or US-heavy teams |

| Tokenization readiness | Not supported | Multi-asset programmable design |

Understanding where your program sits on this spectrum helps explain why BaaS development budgets vary so widely.

1. Compliance and Regulatory Scope

Compliance is often the largest hidden cost driver. Basic onboarding checks are relatively straightforward. However, full KYC, AML monitoring, sanctions screening, and regulatory reporting require deeper infrastructure.

In the US market, sponsor bank expectations and audit readiness also increase effort. As compliance requirements expand, both engineering and operational costs rise.

2. Platform Architecture Complexity

Architecture choices directly influence long-term economics. A simple, single-tenant build may cost less initially. However, it can create scaling challenges later.

Enterprise-grade platforms typically require:

- multi-tenant isolation

- high availability

- real-time processing

- resilient data design

While these capabilities raise upfront investment, they reduce expensive redesign work as the platform grows.

3. Core Banking and Payment Integrations

Every external financial connection adds effort. Integrating with sponsor banks, card networks, ACH, wires, and real-time payment rails requires careful orchestration.

In addition, each integration introduces certification, testing, and monitoring requirements. Programs that support multiple rails or cross-border flows should plan for higher build and maintenance costs.

4. Security and Fraud Infrastructure

Security cannot be treated as a lightweight layer. Enterprise BaaS platforms require strong identity controls, transaction monitoring, and fraud detection capabilities.

Advanced risk scoring, behavioral analytics, and real-time alerts increase development scope. However, they also reduce long-term exposure to losses and compliance action. Many enterprises view this investment as risk prevention rather than pure cost.

5. Feature Scope and Product Modules

The breadth of financial products has a major impact on the budget. A payments-only platform is far simpler than a multi-product environment.

Cost typically increases as programs add:

- account management

- card issuing

- lending workflows

- treasury capabilities

- partner management tools

Clear product prioritization helps control early investment while preserving room to expand later.

6. Team Location and Delivery Model

Where and how the platform is built also affects total cost. Fully US-based teams usually command higher rates. Offshore models can reduce development expense but may require stronger coordination and governance.

Many enterprises adopt a hybrid approach to balance cost efficiency with domain expertise. The right model depends on regulatory complexity and internal oversight capacity.

7. Tokenization and Digital Asset Support

Forward-looking platforms often plan for tokenized or programmable financial products. Supporting multi-asset ledgers and flexible ownership models adds architectural depth.

Although this increases initial effort, it can prevent expensive platform rewrites later. Enterprises focused on long-term innovation often factor this into their early design decisions.

In practice, the BaaS platform cost is shaped by strategic choices rather than a single price point. Organizations that align architecture, compliance, and product scope early are better positioned to control investment while building a platform that scales safely over time.

Estimated Cost Breakdown to Build a BaaS Platform in the USA

In the United States, building a Banking-as-a-Service platform typically ranges from about USD 150,000 for a focused MVP to around USD 500,000 for an enterprise-ready deployment.

Enterprises often look for a clear budget range early in planning. In reality, the BaaS platform cost depends on compliance depth, architecture maturity, and product scope. However, many US-focused programs fall within a more practical range.

A focused minimum viable platform may start near USD 150,000. Meanwhile, a robust, enterprise-ready BaaS environment can approach USD 500,000 when stronger controls and integrations are required.

The table below shows how costs typically scale by platform tier.

Tiered BaaS Development Cost Overview

| Platform Tier | Estimated Cost (USD) | Typical Timeline | Recommended For |

| Focused MVP BaaS | $150,000 – $250,000 | 4–6 months | Early-stage embedded finance programs |

| Growth-Ready Platform | $250,000 – $400,000 | 6–9 months | Scaling fintech and SaaS platforms |

| Enterprise-Ready BaaS | $400,000 – $500,000 | 9–12 months | Regulated, multi-product environments |

In practice, most enterprises land in the middle tier first, then expand capabilities over time. Therefore, leaders should treat these figures as directional planning ranges rather than fixed quotes. The final investment depends on regulatory scope, integration depth, and long-term scalability requirements.

1. Focused MVP BaaS

A focused MVP is designed to validate the embedded finance strategy quickly and with controlled investment. At this stage, the platform usually supports a narrow feature set such as basic accounts, simple payments, or limited card functionality. Compliance coverage is present but streamlined, and integrations are kept minimal to reduce complexity.

This tier works well for enterprises that want to test product-market fit before committing to deeper infrastructure. However, it is not intended for heavy transaction volume or multi-product expansion.

Most organizations treat this phase as a structured starting point rather than the final architecture.

2. Growth-Ready BaaS Platform

The growth-ready tier supports platforms that are moving beyond experimentation into active scale. At this level, the system typically includes stronger compliance automation, improved fraud controls, and support for multiple financial features.

In addition, the architecture begins to incorporate multi-tenant capabilities and higher availability standards.

Enterprises often choose this tier when embedded finance becomes a core product driver. It balances cost control with operational maturity. Therefore, many organizations remain in this phase while they expand partners, users, and transaction volume.

3. Enterprise-Ready BaaS Platform

An enterprise-ready deployment is built for regulated, high-volume environments where reliability and audit visibility are critical. The platform usually includes advanced risk monitoring, deeper sponsor bank integration, and robust observability across all financial flows. It also supports multi-product expansion and complex partner ecosystems.

This tier is appropriate for organizations that treat financial services as strategic infrastructure rather than an add-on feature.

While the upfront investment is higher, the architecture is designed to support long-term scale and regulatory scrutiny with fewer structural changes later.

In practice, the right tier depends on business goals, regulatory exposure, and growth expectations. Enterprises that align platform scope with their near-term roadmap can control the BaaS platform cost more effectively while preserving room to scale when demand increases.

Phase-Wise Development Cost Of Building A BaaS Platform

A Banking-as-a-Service platform is not built in one step. The investment unfolds across several structured phases, each with its own effort and risk profile. Therefore, enterprises that understand phase-wise spending can plan budgets more accurately and avoid surprises mid-project.

In the US market, early stages focus heavily on architecture and compliance alignment. Later phases shift toward integrations, testing, and operational readiness. The table below shows how costs typically distribute across the lifecycle.

Phase-Wise Cost Breakdown

| Development Phase | Key Activities | Estimated Cost (USD) |

| Discovery and Regulatory Alignment | Requirements, sponsor bank planning, and compliance mapping | $20,000 – $40,000 |

| Architecture and Platform Design | System design, ledger modeling, security planning | $30,000 – $60,000 |

| Core Platform Development | APIs, ledger build, core workflows | $60,000 – $150,000 |

| Banking and Payment Integrations | Sponsor bank, ACH, card rails, testing | $40,000 – $120,000 |

| Compliance and Security Validation | KYC/AML setup, audits, penetration testing | $25,000 – $70,000 |

| Pilot Launch and Optimization | Monitoring, fixes, performance tuning | $15,000 – $40,000 |

In practice, spending patterns vary based on regulatory scope and feature depth. However, most enterprises find that architecture quality and integration complexity drive the largest share of investment.

Organizations that invest carefully in early design phases often reduce rework and control total BaaS platform cost more effectively as the program scales.

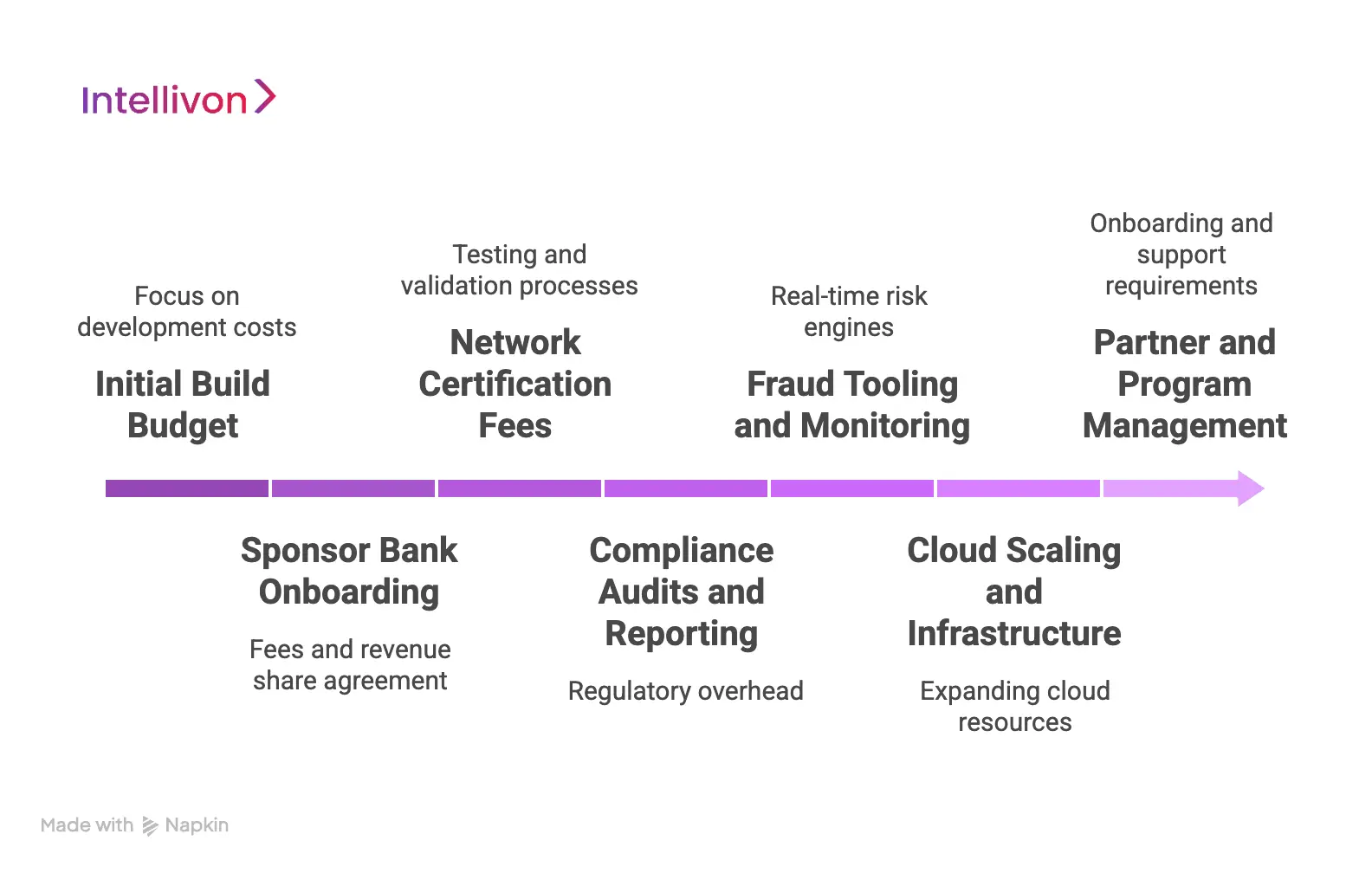

Hidden Costs Of Building BaaS Platforms That Enterprises Often Miss

Beyond development, BaaS programs incur ongoing costs such as sponsor bank fees, certifications, compliance operations, fraud monitoring, and cloud scaling.

Many business cases focus heavily on initial build budgets. However, the long-term BaaS platform cost is often shaped by operational expenses that appear after launch. These hidden costs can affect margins, timelines, and program scalability if they are not planned early.

Enterprises that model these expenses upfront usually avoid budget shocks later. Below are the most common cost areas that teams tend to underestimate.

1. Sponsor Bank Onboarding and Revenue Share

Working with a sponsor bank involves more than technical integration. Banks typically charge onboarding fees and require an ongoing revenue share tied to program activity.

In addition, banks expect continuous reporting, risk reviews, and program oversight. As transaction volume grows, these costs can scale alongside revenue. Therefore, contract structure and volume projections should be modeled carefully.

2. Network Certification Fees

Payment networks and card schemes often require formal certification before programs can go live. These processes include testing, validation, and periodic reviews.

Certification is not always a one-time event. Updates to card programs or payment flows may trigger additional testing cycles. As a result, enterprises should budget for both initial and ongoing network compliance work.

3. Compliance Audits and Reporting

Regulatory compliance introduces recurring operational overhead. Programs must maintain audit trails, generate regulatory reports, and support periodic reviews from banking partners and regulators.

In addition, internal compliance teams or external specialists may be required to manage alerts and investigations. These ongoing obligations can significantly influence the total cost of ownership.

4. Fraud Tooling and Monitoring

Fraud risk grows as financial programs scale. Basic controls may work during early rollout, but higher transaction volume usually requires more advanced monitoring tools.

Costs often include real-time risk engines, behavioral analytics, case management systems, and dedicated risk teams. Although this investment protects revenue, it should be included in long-term financial planning.

5. Cloud Scaling and Infrastructure Overhead

Cloud infrastructure costs rarely stay flat. As user activity increases, transaction processing, data storage, and real-time monitoring workloads expand.

In addition, high-availability environments require redundancy, backup systems, and performance monitoring. Enterprises that plan only for early-stage usage often underestimate how quickly infrastructure costs can rise.

6. Partner and Program Management Costs

BaaS platforms frequently support multiple partners, business units, or embedded finance programs. Each participant introduces onboarding, support, and oversight requirements.

Over time, enterprises may need dedicated program managers, support workflows, and partner reporting tools. These operational layers add steady overhead that should be factored into the business model.

Hidden costs do not mean BaaS programs are inefficient. However, they do reinforce the need for realistic planning. With a clear view of both build and operating expenses, enterprises can evaluate the full BaaS platform cost with greater confidence and fewer surprises ahead.

Operational Costs After Launching BaaS Platforms

After launch, BaaS programs incur ongoing costs for compliance, fraud monitoring, platform reliability, customer support, and regulatory updates.

Launching the platform is only the beginning. The long-term BaaS platform cost is largely shaped by steady operational spending. In the US market, regulatory oversight, fraud exposure, and uptime expectations require continuous investment.

Most enterprises underestimate these recurring expenses during early planning. However, mature programs typically allocate between $15,000 and $60,000 per month depending on scale, transaction volume, and compliance depth. The table below shows how these costs usually distribute.

Typical Monthly Operational Cost Breakdown

| Cost Area | Estimated Monthly Range (USD) | Cost Drivers |

| Compliance operations | $3,000 – $12,000 | KYC reviews, AML alerts, reporting |

| Fraud and risk monitoring | $4,000 – $15,000 | Risk tools, analysts, and case handling |

| Platform reliability and SRE | $3,000 – $10,000 | Uptime, monitoring, and incident response |

| Customer support and disputes | $2,000 – $12,000 | Tickets, chargebacks, investigations |

| Regulatory change management | $1,000 – $6,000 | Policy updates, legal reviews |

These ranges vary by program maturity. High-volume fintech environments often trend toward the upper end.

1. Ongoing Compliance Operations

Compliance work continues long after launch. Teams must review KYC exceptions, monitor AML alerts, and generate regulatory reports. In addition, sponsor banks typically require periodic reviews and program oversight.

Because these tasks are ongoing, enterprises often maintain either an internal compliance team or a managed service model. As transaction volume grows, alert handling and reporting complexity also increase.

2. Fraud and Risk Monitoring Teams

Fraud exposure expands as user activity rises. Early-stage rule engines may be sufficient at low scale. However, mature programs usually require behavioral analytics, real-time scoring, and dedicated risk analysts.

Costs in this category include both technology and human review. Organizations that invest early in strong risk controls often reduce loss exposure later.

3. Platform Reliability and SRE Costs

Financial platforms must maintain high availability. Even short outages can affect customer trust and partner confidence. Therefore, most BaaS environments require continuous monitoring and incident response coverage.

Site reliability engineering costs typically include infrastructure monitoring, performance tuning, and failover management. As the platform scales, these responsibilities become more demanding.

4. Customer Support and Dispute Handling

Embedded finance introduces customer service obligations that many enterprises initially overlook. Payment disputes, chargebacks, and account inquiries require structured workflows and trained support teams.

In addition, regulatory expectations often require documented resolution timelines. As customer volume grows, support costs usually rise in parallel.

5. Regulatory Change Management

Financial regulations continue to evolve in the United States. Programs must adjust policies, update disclosures, and refine monitoring rules over time.

This work may involve legal review, compliance updates, and system changes. While monthly costs may appear modest, they are essential for maintaining long-term regulatory alignment.

Operational spending is a permanent part of running a BaaS platform. Enterprises that plan for these recurring costs early are better positioned to protect margins and scale with confidence. Therefore, evaluating the full BaaS platform cost requires looking well beyond the initial build budget.

Security and Risk Controls Required in Enterprise BaaS Platforms

Enterprise BaaS platforms require layered security, including strong identity controls, real-time risk monitoring, data protection, role-based access, and full audit visibility.

Financial platforms operate in high-trust environments. Therefore, security and risk controls must be built into the core architecture, not added later. In the United States, sponsor banks and regulators expect continuous visibility into how user access, transactions, and data flows are protected.

Enterprises that invest early in strong controls usually avoid costly remediation and reputational risk. The areas below represent the minimum security foundation for a scalable BaaS environment.

1. Identity Orchestration and MFA

Identity orchestration ensures that every user and administrator is verified before accessing financial services. This layer typically combines Know Your Customer checks with authentication controls such as multi-factor authentication.

Strong identity design reduces account takeover risk and improves regulatory confidence. In addition, centralized identity orchestration allows enterprises to apply consistent policies across products and partners as the platform grows.

2. Transaction Monitoring and Risk Scoring

Every financial transaction should pass through real-time monitoring. Risk scoring engines evaluate patterns such as unusual behavior, velocity spikes, and geographic anomalies.

When the system detects suspicious activity, it can trigger alerts or temporarily block the transaction. Over time, machine learning models often enhance detection accuracy. This continuous monitoring helps reduce fraud losses and supports AML obligations.

3. Token and Data Protection

Sensitive financial data must be protected both in transit and at rest. Most enterprise platforms use encryption, tokenization, and secure key management to safeguard card and account information.

In addition, data protection strategies should support regulatory reporting and breach response readiness. As data volume increases, disciplined protection controls become even more important for maintaining trust.

4. Access Governance and RBAC

Role-based access control ensures that users only see and modify what they are authorized to handle. This principle applies to customers, partners, and internal teams.

Granular permission models help reduce insider risk and simplify audit reviews. As organizations expand their partner ecosystems, strong access governance becomes essential for maintaining operational control.

5. Audit Logging and Traceability

Regulated financial systems must maintain a complete activity trail. Audit logs record user actions, configuration changes, transaction events, and system responses.

These records support investigations, regulatory reviews, and internal governance. More importantly, they provide real-time visibility into platform health and risk posture. Enterprises that design robust traceability early typically move through compliance reviews faster.

Security in BaaS platforms is not a single feature. It is a coordinated control system that protects identity, data, and financial flows at every stage. Organizations that treat security as core infrastructure are better prepared to scale safely in regulated markets.

Conclusion

Banking-as-a-Service is quickly becoming a strategic foundation for modern digital platforms. However, the true BaaS platform cost depends on far more than initial development effort.

Architecture depth, regulatory readiness, security controls, and long-term operations all shape the real investment required. Therefore, enterprises that plan early and design for scale usually achieve better outcomes and fewer surprises.

At Intellivon, we build enterprise-grade BaaS platforms as regulated fintech infrastructure that supports growth, resilience, and future innovation. If you are evaluating your next move in embedded finance, our team can help you design a platform that balances cost efficiency with long-term strategic value.

Build An Enterprise-Grade Baas With Intellivon

At Intellivon, Banking-as-a-Service platforms are engineered as regulated fintech infrastructure, not lightweight payment layers added onto existing systems. Every architectural decision focuses on compliance depth, operational resilience, and long-term scalability. As financial programs expand across products, partners, and regions, this foundation helps enterprises maintain control without introducing hidden risk or technical debt.

Our teams work closely with enterprise stakeholders to align platform design with sponsor bank expectations, security requirements, and evolving regulatory standards. Therefore, organizations can launch embedded finance capabilities with confidence while preserving flexibility for future growth, including tokenized and programmable finance models.

Why Partner With Intellivon?

- Enterprise-grade BaaS architecture built for regulated US environments

- Compliance-by-design approach with strong audit and reporting controls

- Scalable multi-tenant infrastructure supporting complex partner ecosystems

- Advanced security, risk monitoring, and fraud prevention capabilities

- Future-ready platform design aligned with digital asset and tokenization trends

Book a strategy session with Intellivon to design and scale a Banking-as-a-Service platform that balances cost efficiency, regulatory confidence, and long-term enterprise growth.

FAQs

Q1. What is the typical BaaS platform cost in the USA?

A1. The BaaS platform cost in the United States usually ranges from about $150,000 for a focused MVP to around $500,000 for an enterprise-ready build. The final investment depends on compliance scope, integrations, and architecture depth. Programs with multi-product support and advanced security typically fall toward the higher end.

Q2. What factors increase the cost of building a BaaS platform?

A2. Several elements can raise the total cost. The biggest drivers include regulatory requirements, sponsor bank integrations, fraud monitoring, and multi-tenant architecture. In addition, adding cards, lending, or real-time payments increases development and testing effort. Therefore, clear product prioritization helps control early spending.

Q3. How long does it take to launch a BaaS platform?

A3. Most focused BaaS implementations take between four and nine months to reach initial launch. Enterprise-grade deployments with deeper compliance and multiple integrations may take nine to twelve months. Timelines often depend on sponsor bank coordination and certification requirements.

Q4. Is it better to build or partner for Banking-as-a-Service?

A4. The right choice depends on your strategic goals. Building offers greater control over data, economics, and product flexibility. However, partnering can reduce early complexity and speed up market entry. Many enterprises start with a focused build and expand capabilities as the program matures.

Q5. Why is compliance so important in BaaS platforms?

A5. BaaS platforms operate in regulated financial environments, especially in the United States. Strong KYC, AML, and reporting controls help prevent fraud and regulatory action. In addition, sponsor banks expect continuous oversight. Enterprises that design compliance into the platform early usually scale more smoothly and avoid costly remediation later.