The financial services industry is changing faster than most fintech startups can manage. Within these institutions, borrowers want quick credit decisions, investors expect portfolio transparency, and regulators need clear audit trails. Creating a formidable infrastructure for lending platforms that can compete with institutions that have refined their processes over decades is a tough task.

Additionally, the divide between a good lending idea and a platform ready for production is larger than most founders realize. This gap involves credit policy, data structure, compliance processes, and capital strategy all at once. Over the years, our fintech experts at Intellivon have assisted fintech leaders in facing this challenge by building lending systems that handle real volume, real risk, and real regulatory scrutiny without collapsing under growth pressure.

This blog addresses everything important, from how we build these platforms from the ground up to their structure, compliance systems, data strategies, and the choices that decide whether your lending platform expands smoothly or turns into a bottleneck.

Why Fintech Startups Are Building Lending Infrastructure

Fintech startups are building lending infrastructure to gain control over the credit lifecycle. By using API-first designs, they enable embedded finance, faster loan approvals, and automated risk management across global markets.

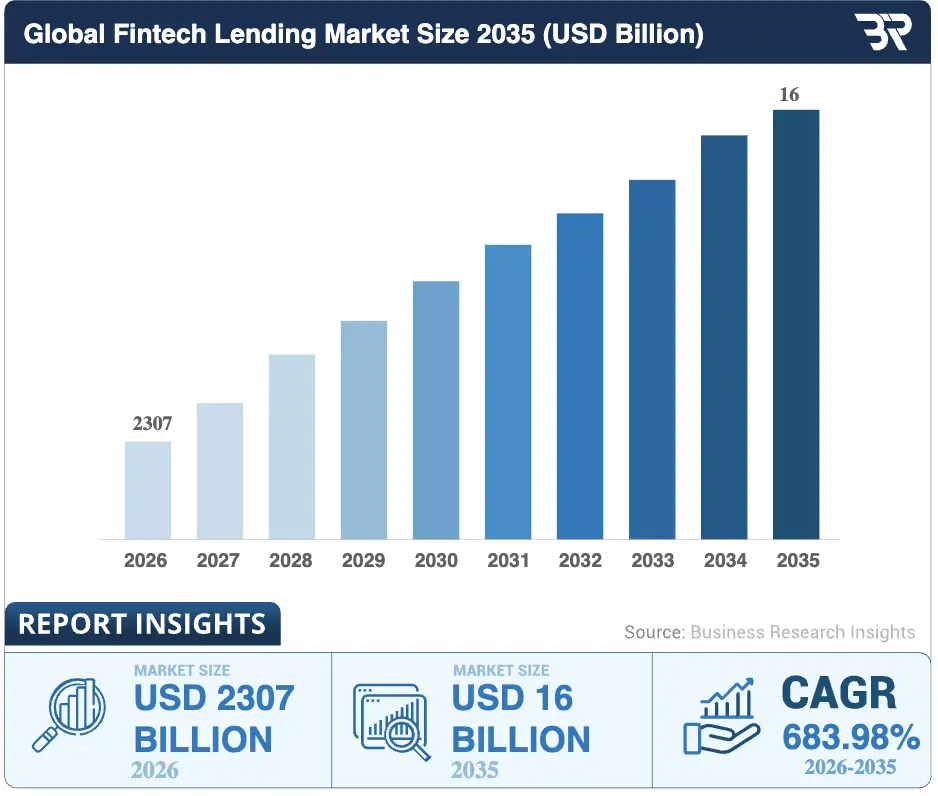

The global fintech lending market is expected to reach $2,307 billion in 2026. It is projected to grow rapidly and reach $16 trillion by 2035. This represents an extraordinary 683.98% CAGR between 2026 and 2035.

Startups are now choosing to build the internal tools that power loans rather than just selling loans themselves. This strategic shift allows companies to own the technology and scale much faster in a crowded market.

1. Shift from Lending Products to Lending Infrastructure

In the past, fintechs focused on getting individual loans to customers. Now, the trend has moved toward building the underlying “engine” that makes lending possible. This means creating a system where credit can be issued, tracked, and collected through a single digital platform.

Therefore, a company can provide the technology to other businesses instead of taking on all the financial risk alone. This approach turns a risky lending business into a steady software service. It allows for a more predictable way to grow without needing massive amounts of cash upfront.

2. Growth of API-Based Lending Platforms

Modern lending relies on APIs, which are simple sets of rules that let different software programs talk to each other. These tools allow a lending platform to instantly pull data from banks or credit bureaus. Consequently, the time it takes to approve a loan has dropped from days to just a few seconds.

In addition, these platforms make it easy to add “buy now, pay later” features to almost any website. This connectivity helps businesses reach customers exactly when they are ready to make a purchase. Because the system is automated, it reduces the chance of human error during the application process.

3. Startups Prefer Infrastructure over Traditional Lenders

Old-fashioned banks often use slow, manual processes that do not work well with modern apps. Startups prefer building their own infrastructure because it gives them total heart-and-soul control over the customer experience. However, the biggest draw is the ability to change rules and interest rates instantly based on new data.

Furthermore, using a digital-first setup is much cheaper than running a traditional bank branch. This efficiency lets startups offer better deals to customers who might be ignored by larger institutions. It also makes it easier to fix bugs or update features without shutting down the whole system.

4. Market Opportunities in Digital Lending Infrastructure

There is a massive gap in the market for companies that provide the “pipes” for digital money. As more people shop and work online, every business wants to offer some form of credit to its users. Thus, the companies building the tech behind these loans are seeing a huge surge in demand.

Moreover, a solid infrastructure makes it much easier to launch in new countries. Since the software handles the complex math and local rules, expanding the business becomes a matter of clicks rather than years of paperwork. Leaders who invest in this tech now will lead the next generation of finance.

This move toward infrastructure is changing how we think about borrowing money. It makes credit a flexible tool that fits perfectly into our daily digital lives.

What Is a Lending Infrastructure Platform?

A lending infrastructure platform is a modular software stack that automates the loan lifecycle. It uses APIs to integrate credit data, underwriting, and servicing for scalable financial operations.

A lending infrastructure platform is the core technology stack that manages a loan from start to finish. It acts as the digital engine connecting borrowers, data sources, and capital.

Therefore, this modular system automates complex tasks like identity checks, risk scoring, and payment tracking. In addition, it uses APIs to link different financial services into one flow. Consequently, businesses can launch new credit products quickly without building everything from scratch.

This architecture turns complicated banking rules into a simple, automated process. At the same time, it is the foundation for any modern digital credit service.

Role of APIs, Automation, and Credit Engines

These three components form the mechanical heart of any modern lending platform. They work together to replace slow human decisions with instant, data-driven actions.

1. Connecting Systems with APIs

APIs act as the digital bridges that pull in data from bank accounts and credit bureaus instantly. This automation removes the need for manual data entry, which drastically reduces errors. Therefore, the credit engine can analyze this information and deliver a loan decision in seconds.

2. Driving Decisions with Credit Engines

The credit engine is the brain that calculates risk based on the data provided. It uses specific rules to determine if a borrower qualifies for a loan.

Consequently, businesses can scale their operations without hiring a massive team of underwriters. In addition, these engines ensure that every decision is consistent and fair.

3. Streamlining Workflows through Automation

Automation ensures that every step, from identity checks to monthly collections, happens on time. It keeps the entire process compliant with financial laws by following pre-set digital rules.

Consequently, the business stays agile while maintaining a high level of accuracy and security.

These tools turn a complex manual process into a fast, reliable software service. They are the essential parts that make digital lending both possible and profitable.

Why Infrastructure Models Scale Faster For Startups

Infrastructure models allow startups to focus on customer acquisition rather than building complex backend systems. By using pre-built financial “pipes,” companies can expand their reach without the traditional growing pains of a bank.

1. Low Capital Requirements and High Agility

Startups often struggle with the massive costs of building a custom lending stack. However, infrastructure models provide ready-made tools that reduce these initial expenses significantly.

This setup allows a team to launch a product in weeks instead of years. Therefore, they can test the market and pivot their strategy without losing millions in sunk costs.

2. Automated Compliance and Risk Management

Managing global financial regulations is a slow and expensive process for any growing business. Fortunately, infrastructure providers build compliance directly into their code. This means the platform automatically handles identity checks and anti-money laundering rules.

In addition, these systems update themselves as laws change, which keeps the startup safe and focused on growth.

3. Seamless Integration with Global Ecosystems

Modern platforms use standardized APIs to connect with banks and payment networks worldwide. Consequently, a startup can launch in a new country by simply adjusting a few lines of code.

This modularity ensures that the business stays compatible with the latest financial technologies. Therefore, the company remains relevant as the industry evolves toward embedded finance.

Scaling a business becomes a technical task rather than a logistical nightmare. This model provides the leverage needed to dominate a fast-moving digital economy.

Lending Infrastructure vs Lending Apps: What Startups Should Build

Choosing between a user-facing app and the underlying infrastructure is a defining strategic move. One focuses on winning the customer, while the other aims to power the entire ecosystem.

1. Product Lending Platforms vs Infrastructure Platforms

Fintech startups can approach digital lending in two different ways. Some build product lending platforms, which focus on acquiring borrowers and managing the entire lending experience. Others build lending infrastructure platforms, which provide the technology that powers lending services for other businesses.

Understanding the difference is important. Each model has different operational priorities, revenue structures, and growth paths.

Product Lending Platforms vs Infrastructure Platforms

| Aspect | Product Lending Platforms | Infrastructure Platforms |

| Core Focus | Deliver lending directly to borrowers through a branded application. | Provide lending technology that other platforms can integrate into their products. |

| Customer Ownership | Own the brand experience and maintain the direct borrower relationship. | Do not interact directly with borrowers. Clients own the customer relationship. |

| Revenue Model | Earn revenue from interest margins, loan origination fees, and servicing fees. | Generate revenue through API usage fees, platform licensing, or transaction-based pricing. |

| Growth Strategy | Growth depends on customer acquisition, marketing efficiency, and brand loyalty. | Growth depends on the number of platforms integrating the lending infrastructure. |

| Operational Focus | Focus on marketing, customer acquisition, borrower support, and collections management. | Focus on platform reliability, developer tools, APIs, and scalable infrastructure. |

Product lending platforms compete for borrowers and build strong consumer brands. In contrast, infrastructure platforms operate behind the scenes and enable many companies to offer lending services.

For fintech startups looking to scale quickly, infrastructure models often provide broader market reach and more scalable growth opportunities.

2. Single-Loan Apps vs Multi-Product Lending Systems

Many fintech startups launch with a single-loan application that solves a specific credit need. Examples include payday advances, invoice financing, or student loans. This focused approach makes it easier to launch quickly. However, as the business grows, limitations begin to appear.

More mature fintech platforms often evolve into multi-product lending systems that support multiple credit products and financial services.

Single-Loan Apps vs Multi-Product Lending Systems

| Aspect | Single-Loan Apps | Multi-Product Lending Systems |

| Product Scope | Designed to offer one specific type of loan or credit product. | Support multiple lending products within the same platform. |

| Time to Market | Faster to launch because the system has fewer features and regulatory requirements. | Requires longer development due to broader financial capabilities. |

| Customer Acquisition | Often faces high acquisition costs due to a narrow product offering. | Can cross-sell multiple services to the same user base. |

| Scalability | Limited scalability when expanding into new financial products. | Built to support multiple credit products without major system changes. |

| Data Utilization | Customer data is limited to one lending product. | Shared customer data enables better credit analysis and cross-selling opportunities. |

Single-loan apps are useful for early-stage startups that want to validate a market quickly. However, long-term growth often requires a multi-product lending platform that can support multiple financial services and deeper customer relationships.

When Startups Should Choose Infrastructure Over Apps

A startup should build an app if it has discovered a unique, underserved audience with a specific pain point. If you have a “secret sauce” for reaching customers cheaply, the app model is your best bet.

However, if your strength lies in data science or software engineering, building infrastructure is the better path.

- Technical Strength: Choose infrastructure if your team excels at building high-throughput, secure financial systems.

- Capital Efficiency: Infrastructure models allow for growth without the need to raise massive debt funds.

- Long-Term Vision: Seek this path if you want to be the “operating system” of the fintech industry.

This choice ultimately dictates your path to profitability. Whether you want to be the face of the brand or the engine of the industry, clarity in your model is essential.

Core Capabilities of a Lending Infrastructure Platform

Enterprise lending infrastructure must feature automated onboarding, real-time credit decisioning, and seamless payment orchestration. By integrating collections management and deep portfolio analytics, these platforms provide the end-to-end control needed for scalable financial operations.

A robust lending engine must move beyond simple data entry to provide a fully automated, end-to-end financial ecosystem. It serves as the intelligent layer that bridges the gap between raw capital and the final borrower experience.

1. Borrower Onboarding and Digital Verification

Modern onboarding must be frictionless to prevent high drop-off rates during the application process. High-performing platforms use automated identity verification to confirm a user’s credentials in real time.

This process involves cross-referencing biometric data, government IDs, and corporate registries. Therefore, the system builds a secure profile without requiring a single physical document.

- KYC/KYB Integration: Automatically screen individuals and entities against global watchlists.

- Liveness Detection: Use facial recognition to ensure the applicant is physically present.

- Document Parsing: Utilize OCR technology to extract data from tax returns and bank statements instantly.

2. Credit Decision and Underwriting Automation

Traditional underwriting is often the most significant bottleneck in the lending lifecycle. By implementing an automated credit engine, businesses can analyze hundreds of data points in milliseconds.

This engine evaluates traditional credit scores alongside alternative data, such as cash flow patterns and social sentiment. Consequently, the platform can approve thin-file borrowers who might be rejected by legacy banks.

In addition, these models allow for dynamic risk pricing. This means interest rates can be adjusted automatically based on the real-time risk profile of the borrower. Therefore, the lender maximizes their returns while offering the most competitive rates possible to low-risk clients.

3. Loan Origination and Approval Workflows

The origination phase is where the technical architecture meets the legal reality of lending. A modular platform allows for highly customizable workflows that can be adapted for different regions or loan types.

This includes the automated generation of digital contracts and the collection of e-signatures. Consequently, the time from “apply” to “disburse” is shortened from days to minutes.

- Multi-Step Approvals: Set up custom logic for loans that require manual oversight by a senior officer.

- E-Signature Integration: Link directly with providers like DocuSign or HelloSign for legally binding agreements.

- Audit Logging: Record every change in the loan status to ensure full regulatory transparency.

4. Repayment Tracking and Payment Orchestration

Managing the flow of money back into the system is just as critical as sending it out. Payment orchestration layers allow the platform to connect with various payment rails, such as ACH, SEPA, or instant card transfers.

This ensures that repayments are processed smoothly and credited to the correct ledger account. In addition, automated reminders can be sent to borrowers before a due date to minimize missed payments.

Furthermore, the system should handle partial payments and complex interest recalculations automatically.

This level of precision prevents accounting errors that often plague manual systems. Therefore, the platform maintains a “clean” ledger that is always ready for a financial audit.

5. Collections Management and Delinquency Handling

When a borrower misses a payment, the platform must transition into a proactive recovery mode. Automated delinquency workflows trigger specific actions based on the age of the debt.

For example, a system might send a text message after three days and a formal letter after ten. This structured approach increases the chances of recovery while staying within the bounds of debt collection laws.

- Tiered Escalation: Automatically move accounts from “late” to “default” status based on pre-set timelines.

- Promise-to-Pay Tracking: Log and monitor agreements made with borrowers during the recovery process.

- Third-Party Handoff: Seamlessly export data to external collection agencies if internal efforts fail.

6. Portfolio Analytics and Lender Dashboards

Data is the ultimate currency for any enterprise-grade lending operation. Decision-makers need high-level views of their total exposure, default rates, and expected cash flow.

Detailed dashboards provide these insights in real time, allowing for better strategic planning. Consequently, the business can identify which market segments are performing well and which require a change in strategy.

Moreover, these analytics tools help in reporting to investors or regulatory bodies. Having a “single source of truth” for all portfolio data reduces the time spent on manual reporting. Therefore, the leadership team can focus on growth rather than searching for missing data in spreadsheets.

This suite of capabilities transforms a simple lending tool into a powerful enterprise asset. It provides the transparency and control necessary to thrive in a competitive financial landscape.

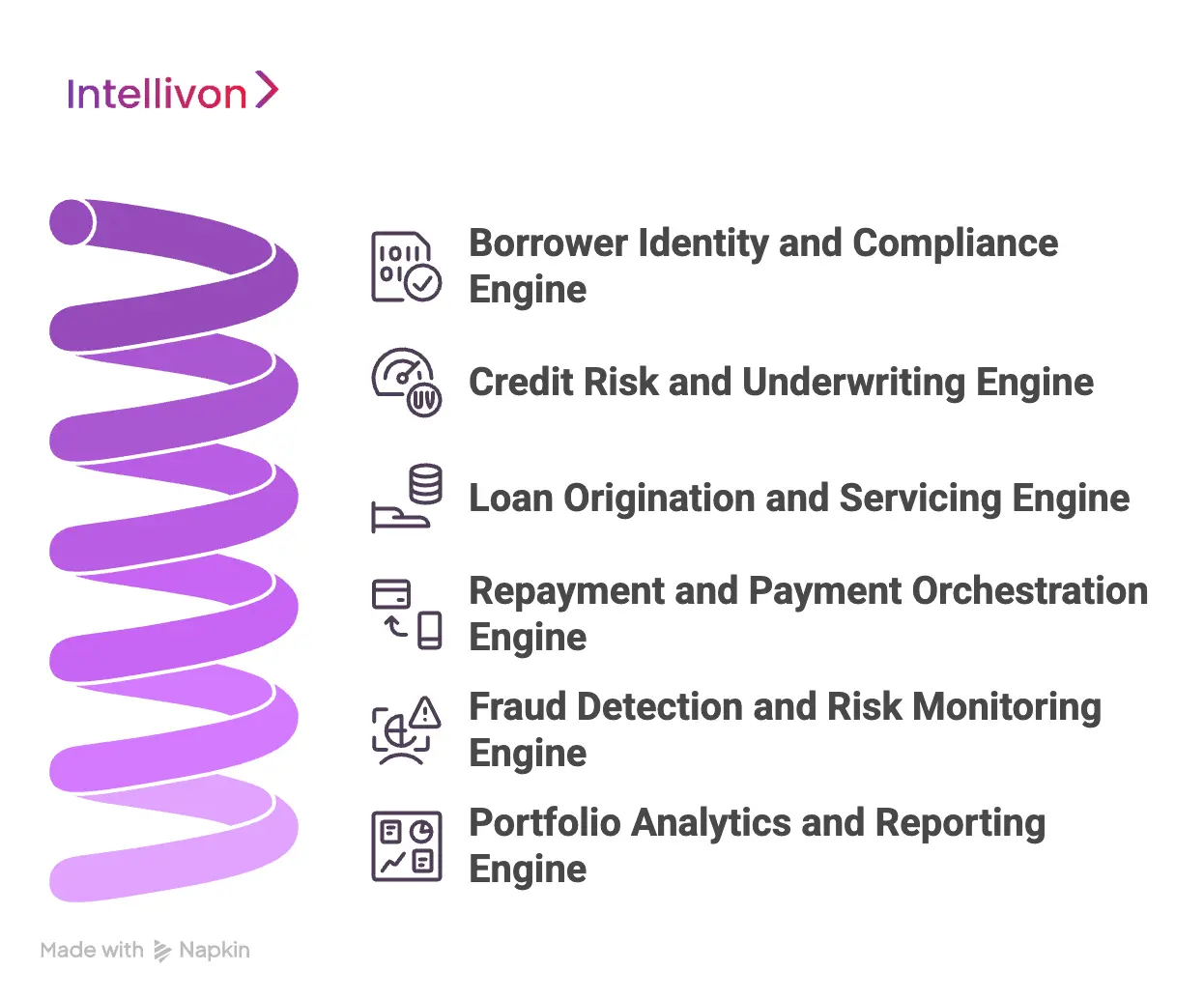

Core Engines That Power Modern Lending Infrastructure

Modern lending infrastructure is powered by specialized engines for identity, risk, servicing, and fraud.

By orchestrating these components through a unified API layer, enterprises achieve real-time credit processing and scalable portfolio management.

Every high-performance lending platform relies on specialized engines that work together to manage the financial lifecycle. These engines act as the “brains” of the operation, turning raw data into profitable credit decisions.

1. Borrower Identity and Compliance Engine

The first point of contact for any borrower is the identity engine, which ensures every user is who they claim to be. This system connects to global databases to verify government IDs and conduct biometric scans in seconds.

Therefore, it acts as a digital gatekeeper that prevents bad actors from entering the system.

- KYC Automation: Instantly screens applicants against international sanctions and anti-money laundering lists.

- Regulatory Alignment: Automatically updates workflows to meet local financial laws across different jurisdictions.

- Audit Readiness: Maintains a permanent, unchangeable record of all verification steps for future inspections.

2. Credit Risk and Underwriting Engine

The credit engine is the most critical part of the platform, as it determines the likelihood of a loan being repaid. It uses a mix of traditional credit scores and alternative data, such as utility payments or merchant transaction history. Consequently, this engine allows for more accurate pricing of risk and higher approval rates.

In addition, the engine can be tuned to match the specific risk appetite of the enterprise. This flexibility allows leaders to tighten or loosen credit requirements instantly as market conditions shift.

Therefore, the business remains resilient during economic volatility while maximizing its lending volume.

3. Loan Origination and Servicing Engine

Once a loan is approved, the origination engine takes over to handle contract generation and fund disbursement. It ensures that the terms agreed upon are legally documented and that the money reaches the borrower’s account without delay.

In addition, the servicing side of the engine manages the ongoing life of the loan, including interest accrual.

- Contract Management: Automatically generates customized legal agreements based on the borrower’s specific loan terms.

- Lifecycle Tracking: Monitors the status of every active loan, from the initial payout to the final closing.

- Event Triggering: Sends automated notifications for upcoming due dates or changes in interest rates.

4. Repayment and Payment Orchestration Engine

A successful lending platform must be able to collect money as efficiently as it lends it. The payment orchestration engine manages the complex flow of funds through various channels like ACH, bank transfers, or card payments.

Therefore, it ensures that repayments are accurately recorded on the ledger without manual intervention.

Furthermore, this engine can automatically retry failed payments and suggest alternative methods to the borrower. This proactive approach reduces the number of missed payments and improves the overall health of the loan book.

Consequently, the business experiences more predictable cash flows and lower operational stress.

5. Fraud Detection and Risk Monitoring Engine

Fraudsters are constantly evolving, so the platform needs an engine that monitors behavior in real-time. This system looks for anomalies, such as unusual login locations or sudden changes in spending patterns.

In addition, it uses machine learning to identify “synthetic identities” that might bypass traditional credit checks.

- Anomaly Detection: Flags transactions that deviate from the borrower’s historical behavior for manual review.

- Device Fingerprinting: Identifies the specific hardware used during an application to prevent multi-account fraud.

- Velocity Checks: Limits the number of applications or transfers from a single source within a short timeframe.

6. Portfolio Analytics and Reporting Engine

The reporting engine turns millions of data points into actionable insights for the leadership team. It provides a high-level view of the entire portfolio, highlighting trends in delinquency, yield, and sector exposure.

Therefore, stakeholders can make data-driven decisions about where to allocate capital for the best returns.

Moreover, these reports are essential for maintaining transparency with investors and regulatory bodies. Having an automated engine means that complex financial statements can be generated with a single click.

These engines provide the structural integrity required to run a massive lending operation. They ensure that speed never compromises security or financial accuracy.

Architecture of a Lending Infrastructure Platform

A lending infrastructure architecture is composed of modular layers for identity, underwriting, servicing, and risk management. By using an API-first design and decoupled payment rails, fintechs can achieve the agility needed for rapid scaling and global compliance.

Building an enterprise lending platform requires a layered approach where each component handles a specific part of the financial lifecycle. This modular architecture ensures that a startup can update one part of the system without breaking the entire flow.

1. Borrower Identity and Compliance Layer

The identity layer is the digital gateway where every borrower interaction begins. It focuses on converting raw applicant data into a verified, compliant persona that the system can trust.

Therefore, it integrates directly with external databases for biometric checks and government ID validation.

- KYC/KYB Integration: Automatically cross-references identities against international sanctions and anti-money laundering lists.

- Consent Management: Captures and stores user permissions for data processing, ensuring full alignment with privacy laws like GDPR.

- Document Verification: Uses high-speed OCR to pull data from tax filings and bank statements without manual entry.

2. Credit Scoring and Underwriting Layer

This layer functions as the decision-making “brain” of the platform. It takes the verified borrower data and applies complex logic to determine creditworthiness. Unlike legacy systems, modern underwriting layers use both traditional bureau data and alternative signals to build a more complete risk profile.

In addition, this layer supports non-linear data orchestration, where multiple sources are analyzed simultaneously rather than in sequence. Consequently, a startup can offer credit to a wider audience while keeping default rates low. Therefore, the underwriting layer is where the “secret sauce” of a fintech’s risk model truly lives.

3. Loan Management and Servicing Layer

Once a loan is approved, the servicing layer manages its day-to-day existence. This includes generating repayment schedules, calculating interest accruals, and tracking the remaining balance.

A well-designed servicing layer acts as the immutable “source of truth” for every contract on the books.

- Amortization Engine: Automatically calculates principal and interest splits for every payment cycle.

- Lifecycle Automation: Moves a loan through different stages, such as “active,” “grace period,” or “closed,” based on real-time data.

- Accounting Integration: Syncs every transaction with the general ledger to ensure financial records are always audit-ready.

4. Payment Rails and Repayment Processing

The payment layer is the plumbing that moves money between the lender and the borrower. It connects the platform to various “payment rails,” such as ACH for bank transfers or card networks for instant payouts. Therefore, the speed of your platform depends heavily on the efficiency of this specific layer.

Furthermore, a “multi-rail” strategy allows the system to choose the best path for a transaction based on cost or speed. For example, it might use an instant payment network for an urgent disbursement but switch to a low-cost ACH transfer for a monthly repayment. Consequently, the enterprise can optimize its operational costs while providing a better user experience.

5. Risk Monitoring and Fraud Prevention

Security is not a one-time event but a continuous process that happens in the background. This layer monitors every login and transaction for signs of suspicious activity.

It uses machine learning to flag anomalies, such as a user suddenly changing their repayment behavior or accessing the app from an unusual location.

- Velocity Checks: Limits the number of transactions or applications from a single IP to prevent automated bot attacks.

- Device Fingerprinting: Identifies the specific hardware used by an applicant to detect “synthetic identity” fraud.

- Real-time Alerts: Instantly notifies the risk team if a high-value transaction appears fraudulent or out of character.

6. Data Analytics and Reporting Systems

Data is the ultimate asset for any enterprise leader looking to scale a lending operation. This final layer collects information from all other parts of the system to provide a high-level view of the business.

Consequently, it allows executives to see which products are most profitable and which regions are showing higher delinquency.

This layered structure provides the resilience needed to survive in a volatile financial market. It ensures that the enterprise stays fast, secure, and always in control of its capital.

Key Integrations a Lending Platform Must Support

Critical lending platform integrations include real-time payment processors, open banking APIs, and automated KYC services. By connecting these systems, enterprises can achieve end-to-end automation from identity verification to debt recovery.

A lending platform cannot exist in a vacuum. Its strength lies in its ability to communicate with the broader financial world through a web of secure, real-time integrations.

1. Banking Infrastructure and Payment Processors

The connection to banking networks moves actual capital. Therefore, the system must link with modern payment processors to handle loan payouts instantly.

In addition, these tools manage the incoming flow of repayments from different bank accounts. Consequently, the platform reduces the time borrowers wait for their funds.

- Instant Payouts: Use networks like RTP to send money in seconds.

- Virtual Accounts: Use these to track individual payments without manual effort.

- Global Rails: Support diverse methods like ACH or SEPA for wider reach.

2. Credit Bureaus and Financial Data Providers

Accurate decisions depend on fresh financial data. Consequently, the platform should pull reports from traditional credit bureaus via secure APIs.

In addition, open banking tools provide a clear view of a user’s actual cash flow. Therefore, the risk model becomes much more precise than the old manual methods.

3. Identity Verification and KYC Providers

Trust begins with knowing exactly who is applying for credit. Therefore, the platform must integrate with automated identity services for instant checks.

These tools verify government documents and perform biometric scans to stop fraud. Consequently, the onboarding process stays fast while meeting all legal standards.

- Biometric Checks: Use facial scans to confirm the user is present.

- Watchlist Scans: Check names against global lists to stay compliant.

- Auto-Filling: Pull data from IDs to save the user time.

4. Accounting and Financial Reporting Tools

Lending data must flow into the general ledger without errors. In addition, integrating with accounting software ensures the business sees its true cash position.

Therefore, every loan issued and cent collected is recorded automatically. Consequently, the finance team avoids the stress of manual month-end reconciliations.

5. Collection and Recovery Service Integrations

Late payments require a structured and legal response. However, automated collection tools can handle this outreach through text and email.

These systems offer simple repayment links to help the borrower catch up. Therefore, the business recovers more debt while maintaining a professional relationship.

These integrations build a complete ecosystem for credit management. They turn a simple app into a powerful, connected financial machine.

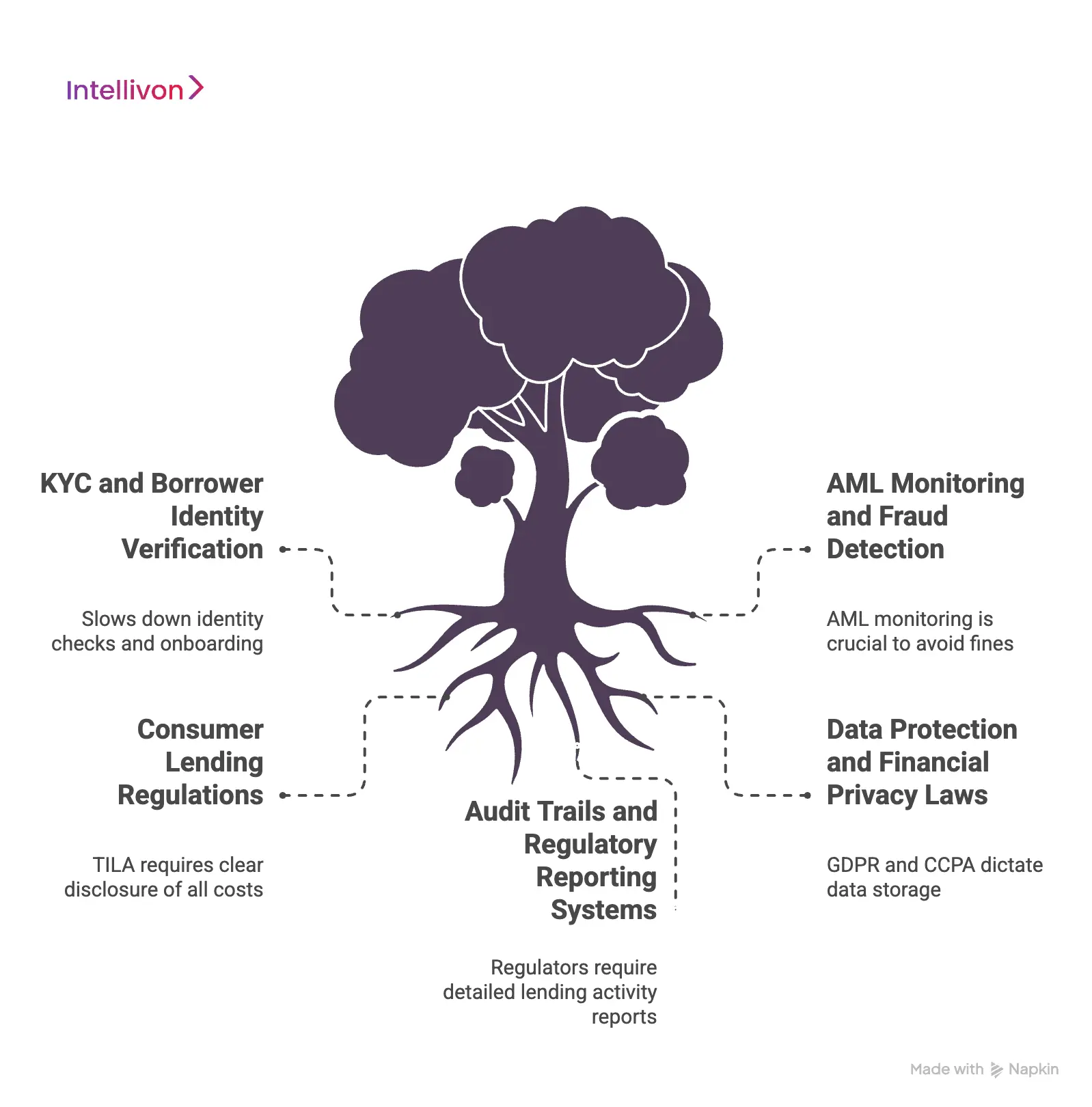

Compliance Requirements for Fintech Lending Platforms

Compliance for lending platforms centers on automated KYC/AML, data privacy encryption, and transparent reporting. Building these features natively ensures startups stay aligned with global financial regulations while maintaining operational speed.

Financial laws change quickly and vary by region. Therefore, building compliance into the core code is the only way to scale safely.

1. KYC and Borrower Identity Verification

Identity checks are the first step in every loan application. However, manual verification is too slow for modern fintech. Consequently, platforms use automated KYC to confirm the user’s name, age, and address.

In addition, these systems verify government IDs against official databases to prevent identity theft.

- Digital Onboarding: Use mobile cameras to scan passports and licenses.

- Liveness Tests: Require a quick video or selfie to prove the person is real.

- Instant Matching: Cross-reference data with tax or utility records immediately.

2. AML Monitoring and Fraud Detection

Anti-Money Laundering (AML) rules require firms to watch for suspicious money flows. Therefore, the system must monitor every transaction for patterns that suggest illegal activity.

In addition, it should flag any user on a global sanctions list before a loan is issued. Consequently, the business avoids heavy fines and protects its reputation.

3. Consumer Lending Regulations

Lenders must follow strict rules regarding interest rates and fee transparency. For example, laws like the Truth in Lending Act (TILA) require clear disclosure of all costs.

In addition, the platform must ensure that it does not use biased data for credit decisions. Therefore, every loan offer must be fair and legally defensible.

4. Data Protection and Financial Privacy Laws

Protecting borrower data is a legal and ethical requirement. Laws like GDPR and CCPA dictate how you must store and encrypt personal information.

Consequently, the platform should use high-level encryption for all data at rest and in transit. In addition, users must have the right to request their data or have it deleted.

5. Audit Trails and Regulatory Reporting Systems

Regulators often require detailed reports on lending activity. Therefore, the platform needs an immutable audit trail that records every system action. This includes every credit score change, payment made, and document signed.

Consequently, the enterprise can generate accurate reports for government agencies with a single click.

Strong compliance builds trust with both users and investors. It turns a legal burden into a long-term competitive advantage.

Liquidity Infrastructure Behind Lending Platforms For Fintech Startups

Liquidity infrastructure for lending involves warehouse credit lines, partner bank models, and marketplace funding. By balancing debt facilities with automated cash flow monitoring, fintechs can scale their loan volumes while mitigating the risk of a capital crunch.

Modern lending requires a steady flow of capital to match the speed of digital applications. Therefore, startups must build a robust funding architecture that supports rapid disbursement without draining their own cash.

1. How Lending Platforms Fund Loan Capital

Fintechs rarely use their own equity to fund every loan they issue. Instead, they act as a bridge between large pools of capital and the individual borrower.

Consequently, they use a mix of debt facilities and investor funds to keep the lending cycle moving. This approach allows the business to scale its volume far beyond its initial balance sheet.

- Debt Facilities: Borrowing large sums from banks at a lower cost to lend out at higher rates.

- Equity Contributions: Using a small portion of the company’s own cash to satisfy lender requirements.

- Securitization: Bundling loans together and selling them as investment products to free up cash.

2. Warehouse Credit Lines and Institutional Funding

Warehouse financing is a specialized revolving credit line used to fund daily loan originations. It allows a startup to draw down funds to issue loans, using those very loans as collateral.

Therefore, the warehouse acts as a temporary “storage” for assets until they are sold or refinanced. In addition, institutional investors like hedge funds often provide the senior debt that powers these lines.

3. Marketplace and Peer-to-Peer Funding Models

Marketplace models turn the platform into a matchmaker rather than a direct lender. In this setup, individual or institutional investors pick specific loans they wish to fund.

Consequently, the platform earns fees for its technology and servicing without taking on the primary credit risk. Therefore, this model is highly capital-efficient and allows for a diverse range of loan types.

4. Balance-Sheet Lending vs Partner Bank Models

Balance-sheet lenders keep the loans they make, earning the full interest margin but taking all the risk. However, many startups prefer the “partner bank” model to avoid the heavy burden of a full banking license.

In this arrangement, a regulated bank originates the loan while the fintech provides the technology and branding. Consequently, the startup stays agile while the bank ensures the capital is fully compliant.

- Direct Control: Balance-sheet lending offers more flexibility over loan terms and pricing.

- Regulatory Ease: Partner banks handle the complex legal filings required for lending.

- Capital Velocity: Using a partner’s balance sheet allows a startup to grow faster with less equity.

5. Managing Liquidity Risk in Lending Platforms

Liquidity risk occurs when a platform cannot meet its financial obligations because its cash is tied up in long-term loans.

Therefore, managers must carefully track the “current ratio” to ensure enough cash is available for daily operations.

In addition, diversifying funding sources prevents the business from collapsing if one lender pulls out. Consequently, a strong liquidity plan is essential for surviving sudden market shifts.

Managing the “pipes” of capital is just as important as the software itself. It ensures the platform remains solvent and ready to fund the next borrower.

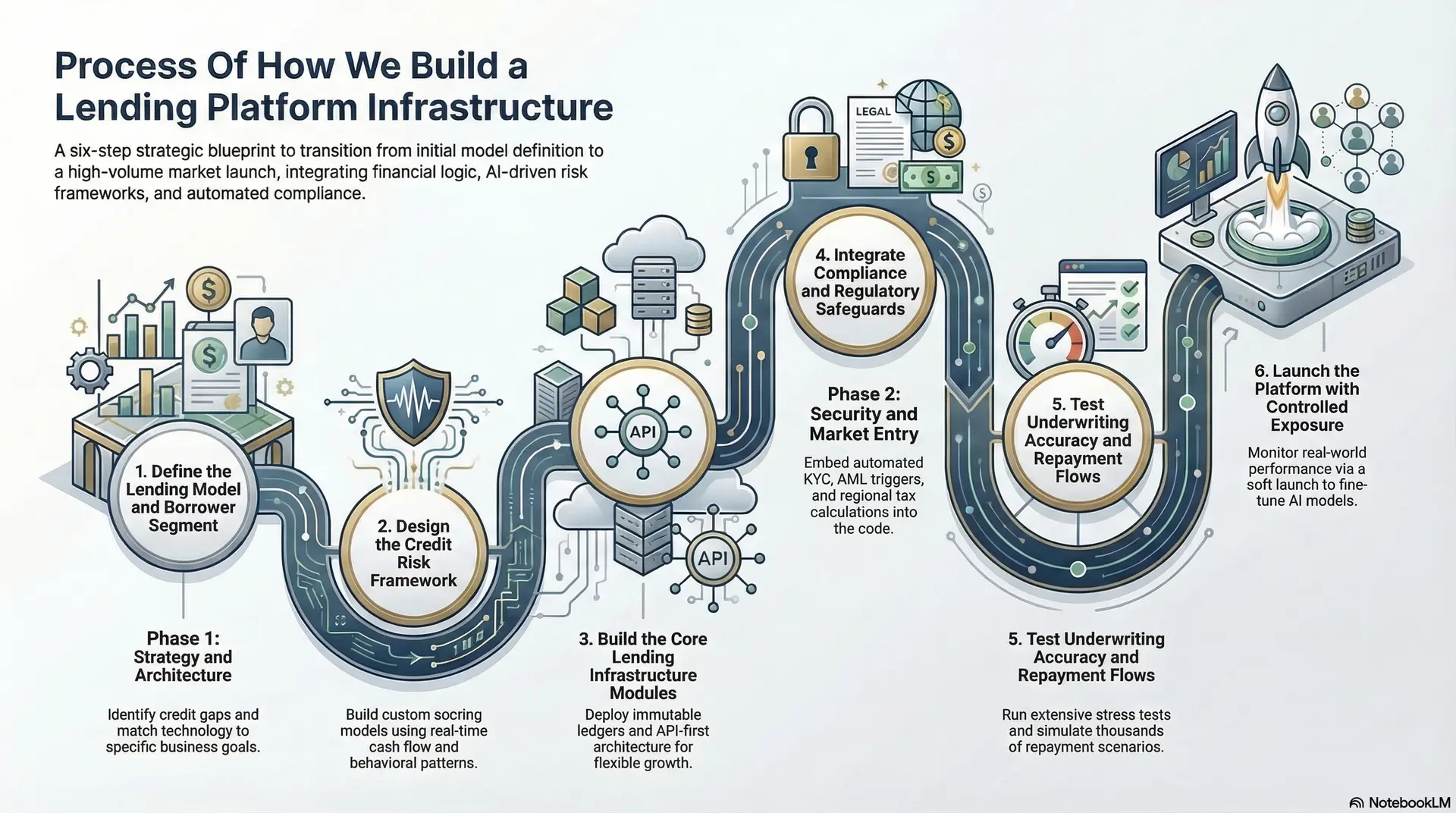

Process Of How We Build a Lending Platform Infrastructure

The lending infrastructure build process involves defining credit models, designing risk frameworks, and deploying modular engines. By integrating compliance and testing repayment flows, Intellivon ensures a secure transition from development to a high-volume market launch.

Building a professional lending engine requires a disciplined, multi-phase approach. At Intellivon, we combine financial logic with enterprise-grade AI to ensure your platform is both scalable and secure.

1. Define the Lending Model and Borrower Segment

The first step is identifying the specific credit gap your platform will fill. Therefore, we help you decide between models like installment loans, revolving lines, or “buy now, pay later” (BNPL) structures.

In addition, we analyze your target audience to determine what data points will best predict their behavior. Consequently, this foundation ensures the technology matches your specific business goals.

2. Design the Credit Risk Framework

Risk is the most critical variable in any financial system. We build custom scoring models that look beyond basic bureau data to include real-time cash flow and behavioral patterns.

Therefore, your system can accurately price risk even for users with limited credit history. Consequently, you achieve a higher approval rate without increasing your default exposure.

3. Build the Core Lending Infrastructure Modules

Once the strategy is clear, we deploy the modular “engines” that power the daily operation. This includes the immutable ledger for tracking debt and the automated servicing layer for managing interest.

In addition, we use an API-first architecture so your platform can easily connect to any front-end app. Therefore, the system remains flexible as your product offerings grow.

4. Integrate Compliance and Regulatory Safeguards

Compliance is not an afterthought; it is built into the code from day one. We integrate automated KYC and AML triggers that screen every applicant against global databases instantly.

In addition, our systems handle the complex task of regional tax calculations and legal disclosures automatically. Consequently, your enterprise remains audit-ready and legally protected at all times.

5. Test Underwriting Accuracy and Repayment Flows

Before going live, we run extensive “stress tests” on your credit models using historical data. Therefore, we can predict how your portfolio will perform during different economic cycles.

In addition, we simulate thousands of repayment scenarios to ensure the payment orchestration layer is flawless. Consequently, you can be confident that the money flows correctly in both directions.

6. Launch the Platform with Controlled Exposure

We recommend a “soft launch” approach to manage initial risk. By starting with a small, invite-only group, we can monitor the system’s real-world performance and fine-tune the AI models.

Therefore, you gather valuable data without risking a large amount of capital. Consequently, you build a track record of success that attracts larger institutional investors for future growth.

Intellivon transforms this complex build process into a secure and compliant technical journey. Therefore, your enterprise launches a scalable lending engine that drives growth from day one.

Challenges Fintech Startups Face in Building Lending Platforms

Fintechs face major hurdles in data scarcity, multi-jurisdictional compliance, and capital liquidity. Overcoming these challenges requires a mix of alternative data underwriting, automated regulatory tracking, and a scalable, multi-funder capital strategy.

Building a credit engine involves navigating a landscape of shifting risks and strict legal barriers. Therefore, startups must anticipate these roadblocks to prevent costly operational stalls.

1. Limited Credit Data for Underwriting Models

New lenders often struggle to assess borrowers who lack a traditional credit history. Without deep data, the risk engine cannot accurately predict the likelihood of a default. Consequently, the business may either reject good customers or approve high-risk ones by mistake.

Therefore, successful startups must find alternative data sources to fill these information gaps.

- Thin-File Barriers: Traditional scores often ignore younger or unbanked populations.

- Information Asymmetry: Borrowers may hide existing debts that are not yet on official reports.

- Data Latency: Bureau information can be weeks old, missing recent financial changes.

2. Regulatory Complexity Across Jurisdictions

Financial laws are not universal and change the moment you cross a state or national border. However, keeping up with these shifts manually is nearly impossible for a small team.

In addition, a single mistake in a loan disclosure can lead to massive government fines. Consequently, the platform must be flexible enough to handle different legal rules in every market.

3. Managing Default Risk and Collections

Every lending business eventually deals with borrowers who cannot or will not pay. Therefore, the startup must have a clear strategy for recovering these funds without damaging its brand.

In addition, aggressive collection tactics can lead to legal trouble and poor public reviews. Consequently, the challenge lies in balancing firm recovery efforts with empathy and legal compliance.

4. Maintaining Liquidity During Growth

Fast growth is usually a goal, but in lending, it can actually trigger a cash crisis. If loan demand outpaces the available capital, the platform may have to turn away profitable customers.

Therefore, the finance team must constantly secure new funding lines to stay ahead of the growth curve. In addition, relying on a single source of cash makes the business vulnerable to market shocks.

5. Scaling Infrastructure with Rising Loan Volume

A system that works for a thousand loans may crash when trying to handle a million. However, migrating a live financial ledger to a larger server is a high-risk technical task.

Consequently, developers must build for “infinite scale” from the very beginning to avoid system downtime. Therefore, choosing a modular, cloud-native architecture is a strategic necessity for long-term survival.

Intellivon helps startups navigate these hurdles by providing the robust, pre-tested architecture needed to handle high volumes. Therefore, you can focus on your customers while we manage the technical and compliance complexity.

Examples of Lending Infrastructure Platforms Of Fintech Startups

Leaders like Stripe, Shopify, and Upstart demonstrate the power of embedded lending and AI underwriting. By utilizing platform data and automated risk scoring, these companies provide faster, more accessible credit than traditional financial institutions.

Real-world success stories prove that modular infrastructure is the fastest way to scale credit. These leaders use technology to bridge the gap between financial data and capital.

1. How Stripe Capital Powers Embedded Lending

Stripe Capital allows software platforms to offer financing directly to their business users. Therefore, a SaaS company can provide loans without building its own lending bank.

In addition, Stripe uses its existing payment data to approve these loans in minutes. Consequently, businesses get the cash they need based on their actual sales history.

- API-First: Platforms integrate credit features using just a few lines of code.

- Auto-Repayment: Loan payments are taken as a small percentage of daily sales.

- No Manual Apps: Eligibility is determined automatically by the user’s transaction data.

2. How Shopify Enables Merchant Financing

Shopify Capital helps small businesses grow by providing quick access to working capital. However, unlike traditional banks, it does not require lengthy paperwork or personal guarantees.

In addition, the system uses the merchant’s store performance to set loan terms. Consequently, Shopify has issued billions in funding to help brands scale their inventory.

3. How Upstart Uses AI Underwriting

Upstart has replaced traditional FICO scores with a layered neural network for credit scoring. Therefore, it can approve more borrowers at lower interest rates than legacy lenders.

In addition, its AI analyzes over 1,600 variables, including education and employment history. Consequently, the platform has automated over 90% of its loan approvals.

4. How Funding Circle Built SME Lending Infrastructure

Funding Circle connects small businesses directly with institutional and individual investors. Therefore, it serves as a marketplace that bypasses the slow processes of traditional commercial banks.

In addition, it uses a proprietary risk model to assign credit ratings to SMEs instantly. Consequently, the platform has become a primary source of capital for thousands of growing firms.

These examples show that the right infrastructure can turn data into a powerful financial product. They set the standard for what a modern lending engine should achieve.

Monetization Models for Lending Infrastructure Platforms

Monetization for lending infrastructure includes interest spreads, SaaS licensing, and transaction-based fees. By combining recurring software revenue with embedded finance “take rates,” platforms can achieve high-margin growth with reduced credit risk.

Revenue in lending infrastructure comes from a mix of software fees and financial margins. Therefore, choosing the right model depends on your capital access and risk appetite.

1. Interest Margin and Loan Spread Models

This model is the most traditional way to earn money from credit. The platform borrows capital at a low rate and lends it to users at a higher rate. Consequently, the “spread” between these two rates becomes the primary source of profit.

However, this requires the platform to hold loans on its own balance sheet. Therefore, the enterprise must manage the direct risk of borrower defaults.

- Net Interest Margin: The difference between interest earned and interest paid to funders.

- Risk-Adjusted Yield: Calculating profit after accounting for expected loan losses.

- Cost of Funds: Minimizing the interest paid to warehouse lenders to increase the total spread.

2. Infrastructure Licensing to Fintech Companies

Many platforms choose to sell their technology as a “Software-as-a-Service” (SaaS) product. In addition, they charge other fintechs a recurring license fee to use their lending engine.

This creates a predictable income stream that does not depend on loan performance. Consequently, the platform scales its revenue based on the number of clients it serves. Therefore, this model is highly attractive to investors who prefer low-risk software margins.

2. Embedded Lending Partnerships

Embedded lending allows non-financial brands to offer credit through your infrastructure. Therefore, you can earn a “take rate” or a small percentage of every loan processed by a partner. For example, an e-commerce site might pay you a fee for every “buy now, pay later” transaction.

Consequently, your platform grows as your partners’ transaction volumes increase. In addition, this model lowers your own marketing costs since the partner brings the customers.

3. Origination Fees and Servicing Fees

These are transactional fees charged at specific points in the loan lifecycle. An origination fee is a one-time charge collected when a loan is first issued to a borrower. In addition, servicing fees are ongoing charges for managing the monthly collections and reporting.

Therefore, these fees provide immediate cash flow even before interest starts to accrue. Consequently, they help cover the operational costs of running the platform’s daily technology.

- Front-End Fees: Charges applied during the initial application and disbursement phase.

- Maintenance Fees: Recurring costs for keeping an active credit line open for a user.

- Late Fees: Additional revenue generated when borrowers miss their scheduled payment dates.

These models offer multiple paths to profitability in the fintech space. Intellivon transforms this complex build process into a secure and compliant technical journey. Therefore, your enterprise launches a scalable lending engine that drives growth from day one.

Conclusion

Building a lending infrastructure platform is a strategic move for any modern fintech. It replaces slow, manual processes with fast, data-driven systems. Therefore, your business gains the agility to enter new markets while keeping costs low.

Consequently, this architecture becomes a foundation for long-term growth and recurring revenue. Intellivon provides enterprise-grade AI solutions to make this vision a reality. Let us build your future together.

Build a Lending Infrastructure Platform With Intellivon

At Intellivon, lending platforms are engineered as financial infrastructure systems, not as standalone loan applications layered onto basic fintech products. Each platform is designed to coordinate credit decisioning, borrower onboarding, loan servicing, repayment management, and risk monitoring across complex digital lending environments.

Every solution is built for regulated financial ecosystems. Lending infrastructure must process large volumes of borrower data, evaluate creditworthiness in real time, integrate with financial institutions, and maintain governance across lending operations through secure and scalable system architecture.

Why Partner With Intellivon?

- Governance-First Lending Architecture: Lending platforms are designed with embedded policy controls, underwriting governance frameworks, and role-based access systems to ensure accountability across lending operations.

- AI-Driven Credit Decision Engines: Our systems include real-time credit scoring models, behavioral risk analytics, and adaptive underwriting logic to evaluate borrower eligibility while maintaining portfolio stability.

- Integrated Loan Origination and Servicing Infrastructure: Platforms coordinate borrower onboarding, loan approvals, disbursement workflows, repayment tracking, and collections management within a unified lending environment.

- Configurable Credit Policy and Risk Frameworks: Enterprises can define lending rules, credit limits, repayment structures, and underwriting policies through configurable rule engines aligned with internal risk strategies.

- Provider-Agnostic Financial Integrations: Lending platforms integrate with credit bureaus, identity verification providers, payment processors, and financial data sources to enable accurate borrower evaluation and compliance.

- Scalable Infrastructure for Lending Ecosystems: Architecture supports expanding borrower bases, increasing loan volumes, and evolving credit products while maintaining high system reliability and decision speed.

Organizations exploring lending infrastructure platform development can work with Intellivon’s fintech specialists to design and deploy secure, scalable, and compliance-ready lending systems built for modern digital credit ecosystems.

FAQs

Q1. What are the 5 C’s of lending?

A1. The 5 C’s of lending are character, capacity, capital, collateral, and conditions. Lenders use these factors to evaluate a borrower’s creditworthiness before approving a loan. They help determine the borrower’s ability to repay and the overall risk of lending.

Q2. How to build a fintech platform?

A2. Building a fintech platform starts with defining the financial service and target users. The next step is designing a secure platform architecture and core financial modules. After that, developers integrate banking APIs, payment systems, and compliance tools. Finally, the platform is tested for security, performance, and regulatory readiness before launch.

Q3. What are the 5 D’s of fintech?

A3. The 5 D’s of fintech typically refer to digitalization, disruption, democratization, decentralization, and data. These forces explain how financial technology is transforming traditional financial services and expanding access to digital financial products.

Q4. What is the fintech lending process?

A4. The fintech lending process begins with digital borrower onboarding and identity verification. The platform then evaluates credit risk using financial data and scoring models. If approved, the system disburses the loan and manages repayments through automated payment processing.