In fintech enterprises, payment delays, issues with third-party checkouts, and disconnected lending steps represent revenue that is being missed. The companies that are progressing the fastest right now are the ones that integrate financial tools directly into their products, workflows, and customer interactions.

While building embedded finance platforms solves these bottlenecks, integrating the platform into an enterprise is not a simple decision. The regulatory challenges alone can delay a project for months if the foundation isn’t set properly. When you add integration issues, limitations of old systems, and the need for input from different teams, most internal groups struggle before they can deliver anything worthwhile.

Intellivon has helped companies navigate this complex landscape. From making design choices to establishing compliance rules and planning rollout strategies, our approach to developing and integrating embedded finance platforms is specific, organized, and based on how large enterprises actually function. This blog outlines our complete development roadmap that it takes to build such a scalable platform.

Why Enterprises are Adopting Embedded Finance Platforms

Enterprises are quickly embracing embedded banking to bring services such as payments, lending, and treasury management directly into their platforms and workflows. The push comes from growing demand for smoother user experiences and new ways to generate revenue.

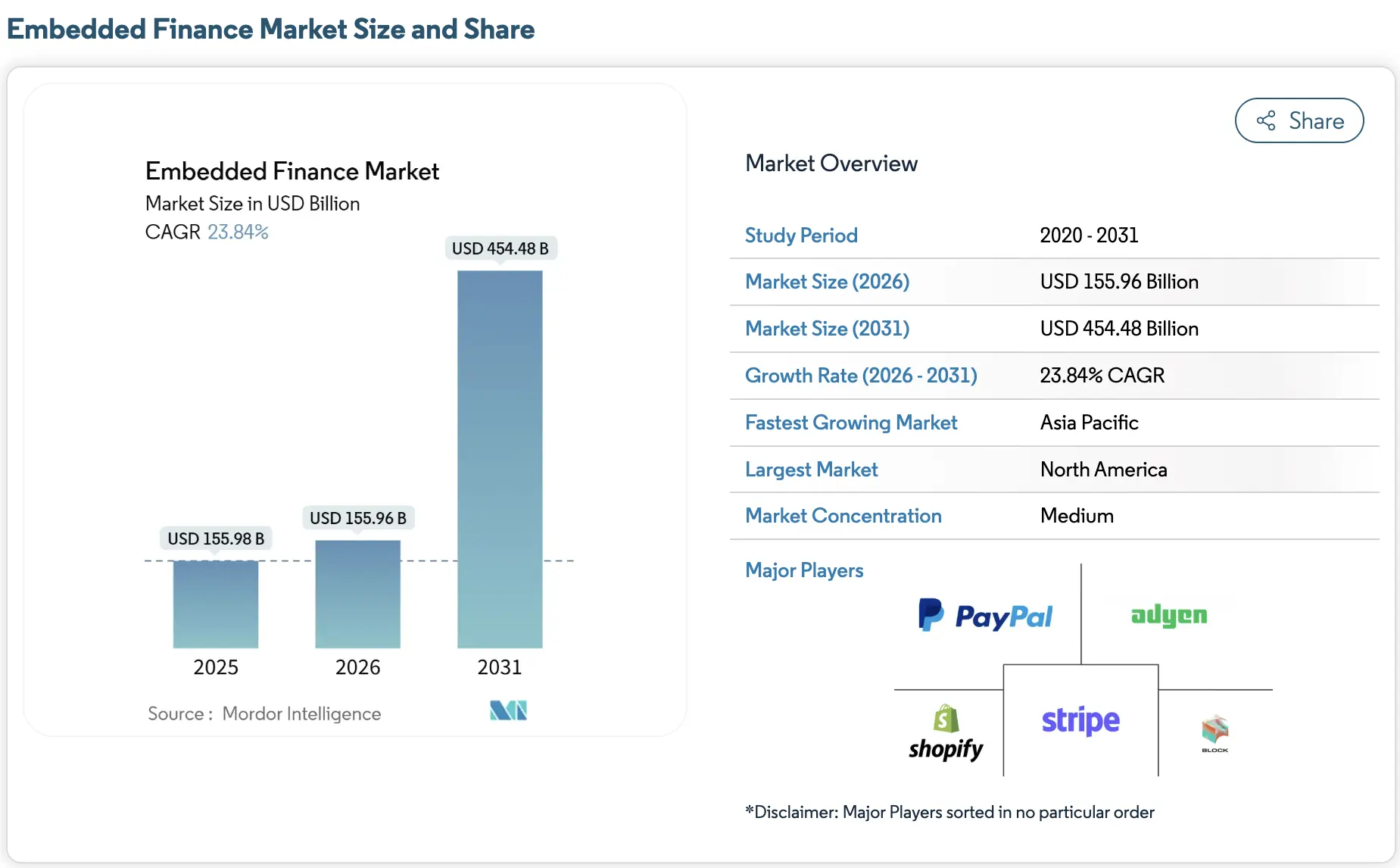

At the same time, strong market expansion and rising competition in B2B sectors are accelerating this shift. The global embedded finance market is growing at a strong pace. It was valued at roughly USD 104.8 to 155.96 billion between 2024 and 2026. Analysts expect it to expand at a CAGR of about 23 to 25 percent, reaching nearly USD 454 to 622.9 billion by 2031 to 2032.

In addition, transaction volumes could climb to about 7.2 trillion dollars by 2030. This growth is being driven largely by digital payments adoption and the rapid expansion of Banking-as-a-Service infrastructure.

Market Insights:

- Customer expectations are shifting toward instant, contextual financial services delivered without app switching. This demand is rising as platforms like Shopify and Salesforce continue to dominate digital ecosystems.

- By embedding financial services within trusted environments, banks and enterprises gain wider distribution, deeper transaction-level data insights, and lower customer acquisition costs.

- SMBs, which represent 57% of B2B card volume, are leading embedded finance adoption.

- Many use one-click payment mechanisms to reduce late payments and improve cash flow. As a result, penetration is projected to rise from 5% in 2021 to 15% by 2026.

- Large enterprises are also modernizing their platforms to embed treasury and credit capabilities. Their priority is API-driven, SaaS-like agility so they can scale faster while keeping pace with evolving Fortune 500 digital strategies.

Enterprises adopt embedded banking to unlock new revenue, improve retention, accelerate innovation, and gain real-time financial visibility without becoming regulated banks.

1. Expanding New Revenue Streams

For many enterprises, embedded banking starts with economics. Financial transactions unlock revenue streams that traditional software cannot generate.

When platforms embed payments, credit, or treasury services, they introduce new income sources. These include interchange revenue, lending spreads, and float earnings.

Research shows that platforms adopting embedded finance can increase customer lifetime value by two to five times. In addition, customer acquisition costs may fall by nearly 30 percent when financial services are delivered directly inside the product.

As a result, finance becomes more than a support function. It becomes a core engine for revenue growth and stronger unit economics.

2. Owning the Customer Financial Journey

Customer experience is another major driver of embedded banking adoption. When users leave a platform to complete payments or financing, friction increases, and conversions often decline.

Embedded banking removes this disruption. Financial transactions happen directly within the product environment.

As a result, enterprises maintain full control over the financial journey. Platforms that integrate payments and credit into user workflows often see stronger engagement and repeat activity.

In addition, keeping financial activity inside the ecosystem creates natural opportunities for cross-selling and upselling services.

3. Building Stronger Platform Ecosystems

Financial workflows tend to become deeply integrated into everyday operations. Once users rely on in-platform wallets, payouts, or credit tools, switching platforms becomes harder.

This dynamic explains the ecosystem strength of companies such as Stripe, Adyen, and Shopify. Embedded financial services increase platform dependency while raising customer lifetime value.

Over time, this reduces churn and strengthens platform loyalty. For enterprises operating in competitive markets, this ecosystem stickiness can become a powerful strategic advantage.

4. Accelerating Fintech Innovation

Launching financial products historically required significant regulatory investment. Companies often need banking licenses, compliance infrastructure, and complex financial systems.

However, Banking-as-a-Service infrastructure has lowered these barriers. Enterprises can now embed accounts, payments, and lending products without building a full banking stack from scratch.

As a result, companies can deliver fintech-level innovation while avoiding the complexity of becoming a licensed bank.

5. Unlocking Real-Time Financial Data Intelligence

Financial transactions generate highly valuable behavioral data. Embedded banking gives enterprises direct visibility into payment activity, cash flow patterns, and customer risk signals.

This insight supports better credit decisions, dynamic pricing strategies, and more personalized financial offers.

At the same time, financial data improves forecasting and liquidity management across the organization.

For many platforms, financial telemetry is no longer a byproduct. Instead, it becomes a strategic data asset powering AI and analytics initiatives.

6. Improving Operational Efficiency and Automation

Embedded banking also streamlines internal operations. Integrated financial workflows reduce manual reconciliation, fragmented payment systems, and back-office complexity.

This improvement is especially important in B2B ecosystems. Small and medium businesses account for roughly 57% of card transaction volume and often struggle with delayed payments.

Embedded one-click payment flows and real-time treasury visibility help solve these issues.

As transaction volumes grow, automation becomes increasingly valuable. Finance teams gain clearer cash visibility while reducing operational errors and manual effort.

Forward-looking enterprises now treat embedded banking as a strategic growth layer, not just a payment feature.

What Is An Enterprise Embedded Finance Platform?

An enterprise embedded finance platform integrates financial services directly into a non-financial business ecosystem. It allows large-scale organizations to offer banking, payments, or lending features through existing digital infrastructure.

Instead of redirecting users to third-party banks, the enterprise manages the transaction flow internally. This technical framework utilizes robust APIs and cloud architecture to bridge the gap between traditional capital markets and modern corporate software.

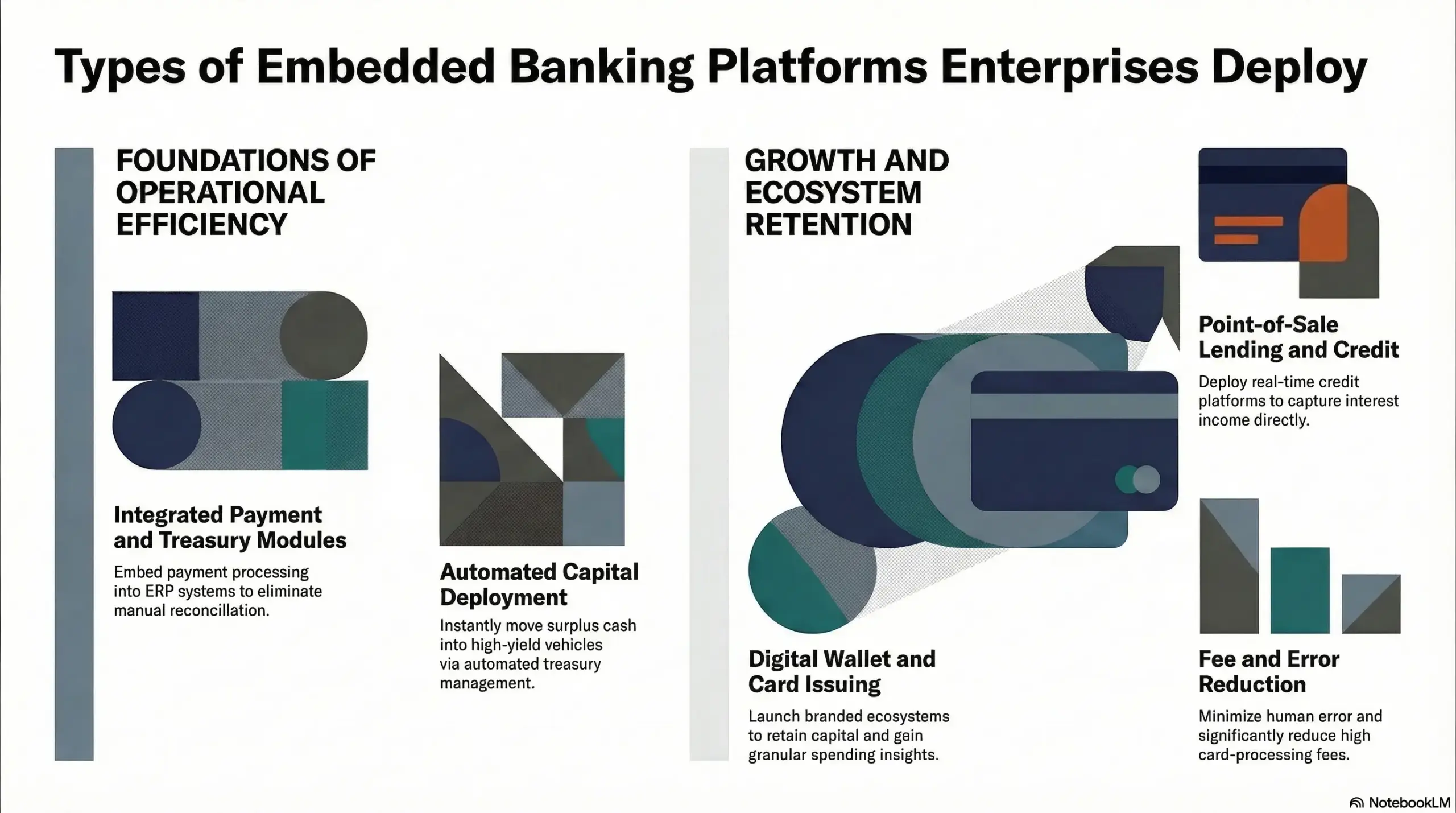

Types of Embedded Banking Platforms Enterprises Deploy

Modern leaders categorize these systems based on specific operational goals. Each model serves a distinct financial purpose within the corporate hierarchy. Selecting the right architecture is vital for maximizing capital efficiency.

Therefore, businesses must evaluate their existing infrastructure before committing to a specific deployment. This strategic choice defines how much control the organization retains over its liquidity.

1. Integrated Payment and Treasury Modules

Many corporations begin by embedding payment processing directly into their ERP systems. This eliminates the need for manual reconciliation between sales and bank statements. Furthermore, these modules allow for automated treasury management.

Surplus cash moves into high-yield vehicles instantly. Consequently, the finance department streamlines the entire order-to-cash cycle. This approach reduces human error and speeds up capital deployment.

2. Point-of-Sale Lending and Credit Facilities

Enterprises with high-value transactions often deploy embedded credit platforms. These systems analyze customer data in real-time. They offer instant loans or structured credit at the moment of purchase.

However, the enterprise captures the interest income instead of an external bank. This creates a powerful incentive for long-term customer loyalty. In addition, it provides a seamless experience for the end-user.

3. Digital Wallet and Card Issuing Ecosystems

Companies with massive user bases are now launching branded digital wallets. These platforms allow users to hold balances and earn rewards. Users spend funds using virtual or physical cards issued by the brand.

Therefore, capital remains within the corporate ecosystem for longer periods. The business gains granular insights into spending patterns. Moreover, it significantly reduces high card-processing fees over time.

Modern embedded banking is no longer an experiment for the tech-savvy. It is a foundational requirement for any enterprise. By deploying these specialized platforms, leaders ensure their organizations remain data-rich. In conclusion, these systems provide the infrastructure for sustainable, tech-driven financial expansion.

Infrastructure Behind Embedded Finance Platforms

Building a resilient financial ecosystem requires more than just connecting to a bank; it necessitates a robust, high-availability architecture. This technical foundation ensures that every transaction is secure, compliant, and instantly verifiable across the entire enterprise network.

1. Banking-as-a-Service Partner Integrations

Modern enterprises rarely seek to become licensed banks due to the immense regulatory burden. Instead, they leverage Banking-as-a-Service (BaaS) providers to access core banking functions through sophisticated API layers.

These integrations allow your platform to issue branded cards, open virtual accounts, and hold deposits under a partner’s charter. Therefore, the strength of your platform depends on the stability and latency of these external connections.

2. Payment Orchestration and Transaction Routing

A sophisticated orchestration layer acts as the brain of your payment operations. It intelligently routes transactions through various gateways based on cost, speed, or geographic requirements.

This redundancy ensures that if one provider experiences downtime, your business continuity remains intact. Consequently, your enterprise can optimize processing fees while maintaining a consistent checkout experience for global users.

3. Ledger Infrastructure and Reconciliation Engines

At the heart of every financial platform lies an immutable double-entry ledger system. This engine tracks the movement of every cent in real-time, ensuring that internal balances always match external bank statements.

Automated reconciliation engines eliminate the need for manual accounting audits by flagging discrepancies instantly. In addition, this level of precision is vital for maintaining stakeholder trust and ensuring financial transparency at scale.

4. Risk Engines and Financial Decision Systems

Decision-making in finance must happen in milliseconds to prevent fraud without hindering legitimate users. Advanced risk engines utilize machine learning to analyze behavioral patterns and transaction metadata.

By evaluating creditworthiness or fraud probability instantly, these systems protect your capital from sophisticated digital threats. Strategic leaders prioritize these systems because they balance aggressive growth with necessary capital preservation.

5. Compliance and Financial Governance Controls

Governance is the most critical hurdle in financial product deployment. Your platform must automate KYC, AML, and Sanctions screening to meet global standards. These controls are integrated workflows that adapt to changing laws in different jurisdictions.

However, by embedding these rules into the code, you ensure that your enterprise remains shielded from massive regulatory fines and reputational damage.

Effective infrastructure transforms financial services from a complex liability into a powerful, automated growth engine. By mastering these five layers, your organization can deploy scalable financial solutions with total confidence.

Architecture of Embedded Finance Platforms

Architecting a financial platform requires a move toward a high-concurrency, zero-failure paradigm. This structure ensures every monetary movement is tracked with absolute precision. It also maintains the agility needed for enterprise-scale integration.

1. API orchestration for financial service providers

An effective architecture acts as a traffic controller between business logic and external utilities. Instead of rigid connections, use an orchestration layer to manage complex sequences.

For example, you can verify identity before triggering a fund transfer. This abstraction allows your team to swap providers without rewriting the entire backend. In addition, your enterprise gains the flexibility to adapt to market shifts with minimal friction.

2. Financial ledger and transaction architecture

The ledger is the source of truth for every transaction in your ecosystem. Unlike standard databases, financial ledgers must be immutable. They use double-entry principles to ensure every credit has a matching debit.

This specific design prevents balance errors and keeps your records audit-ready. Consequently, a high-performance ledger system is non-negotiable for maintaining the credibility of your platform.

3. Risk monitoring and fraud detection systems

Security in embedded finance must be proactive rather than reactive. Your architecture should include dedicated pipelines for real-time data analysis. These pipelines feed transaction metadata into models that flag suspicious activity.

By isolating these risk engines, you ensure checks do not slow down legitimate users. Strategic implementation of these systems allows you to mitigate losses from fraud automatically.

4. Compliance automation and audit infrastructure

Enterprise leaders face pressure to adhere to evolving global regulations. Your architecture must embed compliance checks directly into the transaction flow. This ensures every user is vetted before they access financial features.

Building a dedicated audit trail allows you to generate reports for regulators instantly. Therefore, you can drastically reduce legal overhead while maintaining high security standards.

5. Cloud infrastructure for financial platforms

Deploying on resilient cloud environments provides the high availability required for financial operations. Multi-region deployments allow your platform to handle spikes in transaction volume.

Furthermore, cloud-native security tools provide the encryption necessary to protect sensitive customer data. This foundational layer ensures your financial services remain performant across international borders.

A well-designed architecture serves as the skeleton for your entire financial strategy. By prioritizing modularity, you turn technical infrastructure into a long-term competitive asset.

Detailed Development Roadmap for Embedded Finance Platforms

Execution determines the success of any financial venture. Moving from a conceptual model to a live transactional ecosystem requires a disciplined, phase-based approach. Each step must mitigate risk while building the technical depth required for enterprise-grade performance. Our methodology focuses on speed to market without compromising on security or regulatory integrity.

Phase 1: Financial Product Strategy and Modeling

We begin by defining the specific financial value proposition for your ecosystem. Our team analyzes your user workflows to identify where integrated credit or payments drive the most impact.

This stage establishes the unit economics and the long-term ROI of the project. Consequently, we ensure your investment aligns with real-world user demand and business goals.

Phase 2: Selecting Banking and Fintech Partners

A platform is only as strong as its underlying regulatory foundation. We guide you through the selection of Banking-as-a-Service (BaaS) providers or direct bank partners. Our experts vet these partners based on API uptime, geographic reach, and balance sheet strength.

Therefore, you receive a partner ecosystem that supports your specific scale and compliance requirements.

Phase 3: Platform Architecture and Infrastructure

Our engineers build the core engine to handle high-volume, concurrent transactions. We focus on a modular, cloud-native environment that ensures five-nines availability for your users.

During this phase, we also establish the immutable ledger system for perfect accounting. In addition, this architecture allows for future feature expansion without requiring a total system overhaul.

Phase 4: Compliance Frameworks and Governance

Governance is the bedrock of every financial service we develop. We integrate automated KYC and AML workflows directly into your user onboarding process.

This ensures your platform meets global standards without creating friction for legitimate customers. Because regulations change frequently, we build a flexible framework that adapts to new legal requirements automatically.

Phase 5: Financial Service API Integrations

We move into the technical “plumbing” by connecting your system to payment gateways and card networks. Our developers prioritize low-latency connections and robust error-handling protocols.

This ensures that fund movements occur in real-time with maximum reliability. Furthermore, this phase secures the data flow between all internal and external endpoints.

Phase 6: Risk and Fraud Monitoring Systems

Before the launch, we deploy sophisticated defense mechanisms to protect your capital. We implement AI-driven risk engines that monitor transactions for behavioral anomalies in real-time.

These systems block fraudulent attempts before they can impact your bottom line. Consequently, you can scale your financial offerings with total confidence in your ecosystem’s security.

Phase 7: Platform Launch and Ecosystem Scaling

The final phase focuses on a controlled rollout to your enterprise user base. We start with a pilot program to gather data and refine the interface. Once validated, we help you scale the platform across your entire global footprint.

As your strategic partner, Intellivon provides the ongoing technical support and innovation needed to keep your platform at the cutting edge.

Strategic development transforms a complex technical challenge into a repeatable growth engine. By following this structured roadmap, we help your enterprise lead the market in the rapidly evolving financial landscape.

Data Architecture for Embedded Finance Platforms

Data is the lifeblood of any modern financial system. However, managing this data requires a sophisticated architecture that balances real-time processing with absolute accuracy. This structure ensures that every transaction is recorded, analyzed, and protected according to the highest enterprise standards.

1. Transaction Event Pipelines and Financial Data Flows

We design transaction pipelines to handle massive volumes of concurrent data without bottlenecks. These event-driven architectures capture every user action and translate it into a financial instruction.

By using distributed streaming platforms, we ensure that data moves from the interface to the backend in milliseconds. Consequently, your enterprise can support real-time payments and instant balance updates across global markets.

2. Real-Time Ledger Synchronization Architecture

Consistency is the most critical requirement for financial data. Our architecture utilizes a synchronization layer that keeps internal ledgers perfectly aligned with external banking partners.

This prevents “double-spending” and ensures that the user always sees an accurate account balance. Therefore, we implement strict atomicity in our database transactions to guarantee that every entry is either fully completed or safely rolled back.

3. Financial Analytics and Reporting Layers

Data is only valuable if it provides actionable insights for your leadership team. We build a dedicated analytics layer that sits on top of your transactional data without slowing down core operations.

This allows you to monitor cash flow, track customer spending habits, and identify new revenue opportunities in real-time. In addition, these systems provide the granular data needed to refine your financial products and increase user lifetime value.

4. Handling Financial Data

Security and privacy are non-negotiable when dealing with sensitive financial information. Our architecture incorporates data encryption at rest and in transit as a foundational layer.

We also automate data residency protocols to ensure you comply with local laws like GDPR or CCPA. Furthermore, Intellivon implements rigorous access controls and audit logging. This ensures that every data touchpoint is tracked and fully ready for regulatory inspections.

A disciplined data architecture turns raw information into a strategic asset. By prioritizing integrity and scalability, we provide the technical foundation your enterprise needs to dominate the financial landscape.

Risk and Fraud Systems in Embedded Finance Platforms

Operating a financial platform requires a proactive stance against increasingly sophisticated digital threats. A resilient system must distinguish between legitimate growth and fraudulent exploitation in real-time. This necessitates a layered defense strategy that integrates deep data analysis with automated enforcement protocols.

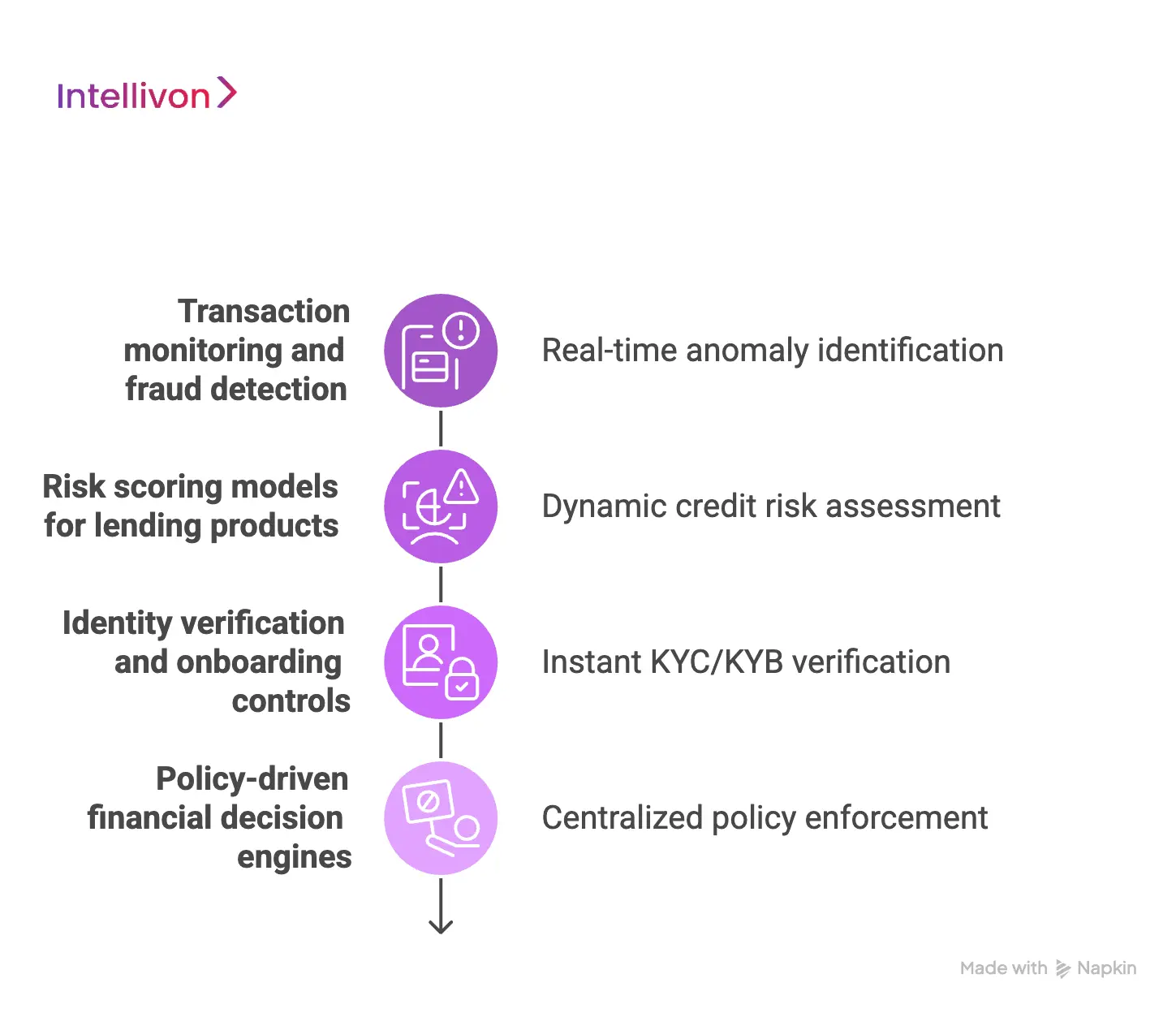

1. Transaction monitoring and fraud detection

Effective fraud detection moves faster than the transaction itself. Modern systems utilize behavioral biometrics and velocity checks to identify anomalies as they occur. For example, a sudden spike in high-value transfers from a dormant account will trigger an immediate freeze.

Consequently, these monitoring tools protect the platform’s liquidity while maintaining a low-friction experience for honest users.

2. Risk scoring models for lending products

Credit risk management has evolved beyond traditional static scoring methods. Embedded platforms leverage alternative data, such as transaction history and cash flow patterns, to build dynamic risk profiles.

These models predict the probability of default with high precision by analyzing real-time financial health. Therefore, enterprises can extend credit to underserved segments while maintaining a healthy and predictable balance sheet.

3. Identity verification and onboarding controls

The onboarding phase is the first and most critical line of defense. Robust platforms integrate automated Know Your Customer (KYC) and Know Your Business (KYB) workflows to vet participants instantly.

These controls verify government IDs, perform facial matching, and screen against global sanctions lists. In addition, these automated checks ensure that your ecosystem remains compliant with international anti-money laundering (AML) regulations without slowing down user growth.

4. Policy-driven financial decision engines

Strategic control over financial operations requires a centralized engine that enforces business logic across the platform. These engines allow leaders to set specific parameters for transaction limits, geographic restrictions, and merchant categories.

If a request violates a predefined policy, the system automatically denies or flags it for manual review. Furthermore, these programmable rules allow the organization to scale its risk appetite up or down based on current market conditions or regulatory shifts.

A comprehensive risk framework ensures that financial innovation does not come at the cost of security. By embedding these protections into the core architecture, a platform becomes a stable environment for long-term capital appreciation.

Cost to Develop an Embedded Finance Platform

At Intellivon, embedded finance platforms are built as enterprise financial infrastructure, not as payment widgets layered onto existing digital products. The objective is to create a governed platform that orchestrates payments, wallets, lending, and financial data flows directly inside a company’s core ecosystem.

However, building an enterprise embedded finance platform requires more than integrating financial APIs. The platform must manage financial ledgers, regulatory compliance, banking integrations, and transaction monitoring while maintaining operational reliability.

When implemented correctly, embedded finance platforms allow enterprises to launch branded financial services while maintaining control over compliance, customer experience, and financial data intelligence.

Estimated Phase-Wise Development Cost

| Phase | Description | Estimated Cost Range (USD) |

| Product Strategy & Financial Design | Define financial products, regulatory scope, partner strategy, and embedded finance roadmap | $5,000 – $10,000 |

| Platform Architecture Design | Design system architecture, financial service orchestration, and cloud infrastructure | $7,000 – $15,000 |

| Financial Ledger & Transaction Systems | Implement double-entry ledger, transaction management, and reconciliation engines | $8,000 – $18,000 |

| Banking & Payment Integrations | Integrate Banking-as-a-Service providers, payment gateways, and financial APIs | $10,000 – $25,000 |

| Compliance & Risk Infrastructure | Implement KYC verification, AML monitoring, fraud detection, and audit frameworks | $8,000 – $18,000 |

| Financial Product Development | Develop wallets, payments, credit modules, or other embedded financial services | $7,000 – $15,000 |

| Security & Data Protection Systems | Encryption, authentication systems, and financial data security architecture | $5,000 – $10,000 |

| Testing & Financial Validation | Transaction testing, financial accuracy validation, and performance optimization | $3,000 – $8,000 |

| Deployment & Infrastructure Setup | Cloud deployment, monitoring tools, and operational infrastructure configuration | $4,000 – $8,000 |

Total initial investment:

$50,000 – $150,000

Ongoing maintenance and optimization: Approximately 15–20% of the initial development cost per year.

Timeline to Launch an Enterprise Platform

The timeline for launching an embedded finance platform depends on the financial products being introduced and the complexity of integrations.

| Phase | Estimated Timeline |

| Product strategy & partner selection | 2 – 3 weeks |

| Platform architecture & infrastructure | 3 – 4 weeks |

| Financial service integrations | 4 – 6 weeks |

| Compliance systems & testing | 3 – 4 weeks |

| Deployment & launch preparation | 2 – 3 weeks |

Typical development timeline:

3 – 5 months for an enterprise embedded finance platform.

Hidden Costs Enterprises Should Plan For

Even well-architected embedded finance platforms face operational pressure when indirect costs are overlooked.

- Banking partner fees increase as transaction volume grows and additional financial services are introduced.

- Compliance operations expand as platforms scale across regions with different regulatory requirements.

- Infrastructure costs rise as transaction processing and financial data storage increase.

- Fraud monitoring systems require ongoing updates to adapt to evolving financial threats.

- Operational training becomes necessary for finance teams, product teams, and support staff managing financial services.

Best Practices to Avoid Budget Overruns

Based on Intellivon’s experience building enterprise fintech platforms, several practices help organizations control embedded finance development costs.

- Define the financial products and banking partners early in the planning stage.

- Design a modular platform architecture so financial services can scale independently.

- Implement financial ledgers and compliance controls directly within the platform architecture.

- Plan banking, payment, and compliance integrations before development begins.

- Build infrastructure that can support new financial products without major system redesign.

- Maintain observability across financial transactions, compliance systems, and operational workflows.

Organizations planning to build an embedded finance platform can work with Intellivon’s fintech experts to design a development roadmap aligned with financial product strategy, regulatory requirements, and long-term platform scalability.

Conclusion

Implementing an embedded finance platform represents a major leap toward enterprise modernization. This roadmap provides the structural clarity required to turn financial services into a scalable revenue driver. Success depends on choosing a partner who understands both high-level strategy and technical execution.

Consequently, the transition from a traditional model to a financial ecosystem becomes a strategic growth move. Partner with Intellivon today to build your future-ready financial platform.

Build an Embedded Finance Platform With Intellivon

At Intellivon, embedded finance platforms are engineered as enterprise financial infrastructure, not as payment tools layered onto existing digital products.

Embedded finance platforms must operate across complex financial environments. They integrate with banking infrastructure, payment networks, compliance systems, and enterprise platforms while maintaining regulatory governance, financial accuracy, and secure transaction processing.

Why Partner With Intellivon?

- Enterprise Embedded Finance Architecture: We design scalable financial orchestration platforms that integrate banking services, payment networks, lending infrastructure, and financial data systems within enterprise digital ecosystems.

- Financial Ledger and Transaction Infrastructure: Our platforms include real-time ledger systems that track balances, process financial events, and maintain accurate reconciliation across payments, wallets, and financial services.

- Compliance and Regulatory Frameworks: Every platform incorporates KYC verification, AML monitoring, fraud detection, and regulatory reporting systems to support compliant financial operations.

- Banking and Fintech Partner Integrations: We integrate embedded finance platforms with Banking-as-a-Service providers, payment processors, card networks, and financial APIs required for enterprise financial products.

- Secure Financial Infrastructure: Our platforms implement encryption systems, role-based access controls, and secure authentication frameworks to protect sensitive financial data and transaction flows.

- Scalable Cloud-Native Platforms: Embedded finance platforms are deployed on scalable cloud infrastructure designed to support high transaction volumes, real-time financial events, and enterprise growth.

Organizations planning to build an embedded finance platform can partner with Intellivon’s fintech experts to design and deploy secure financial infrastructure aligned with their platform strategy, regulatory requirements, and long-term financial ecosystem goals.

FAQs

Q1.What is an embedded finance platform?

A1. An embedded finance platform allows companies to offer financial services directly inside their products. These services can include payments, wallets, lending, or insurance.

Q2. How do companies launch embedded financial services?

A2. Companies launch embedded finance by integrating banking infrastructure, payment networks, and compliance systems into their digital platforms using financial APIs.

Q3. What technologies power embedded finance platforms?

A3. Embedded finance platforms use API orchestration, financial ledgers, cloud infrastructure, identity verification systems, and real-time payment processing networks.

Q4. How long does it take to develop an embedded finance platform?

A4. Most enterprise embedded finance platforms take 3 to 5 months to develop, depending on financial products, integrations, and regulatory requirements.

Q5. Which industries benefit most from embedded finance?

A5. Marketplaces, SaaS platforms, ecommerce companies, logistics platforms, and travel businesses benefit the most from embedded financial services.