Digital care delivery is reshaping how healthcare organizations manage money, which has become as complicated as handling clinical data. Payments, reimbursements, benefits, and patient contributions now move between providers, payers, employers, and platforms. These transactions rarely stay within a single system. As a result, financial operations cannot keep up with evolving digital care models.

This is where a digital health wallet app becomes important. For businesses, a health wallet serves as a financial control layer integrated into regulated healthcare workflows. Every transaction must comply with eligibility rules, consent requirements, audit trails, and settlement logic. If this context is overlooked, wallets can introduce risks rather than minimize them.

At Intellivon, digital health wallets are designed as enterprise-grade financial systems for healthcare and not as separate payment apps. Design choices focus on governance, interoperability, and regulatory strength from the beginning. This blog explains how our healthcare app developers build a digital health wallet app from the ground up.

Why Healthcare Organizations Are Investing in Digital Health Wallets

Healthcare systems are under pressure to manage identity, access, and financial eligibility across increasingly digital care journeys. As services expand beyond physical facilities into virtual, cross-border, and hybrid models, enterprises need a reliable way to govern who can access care, under what conditions, and how associated transactions are authorized.

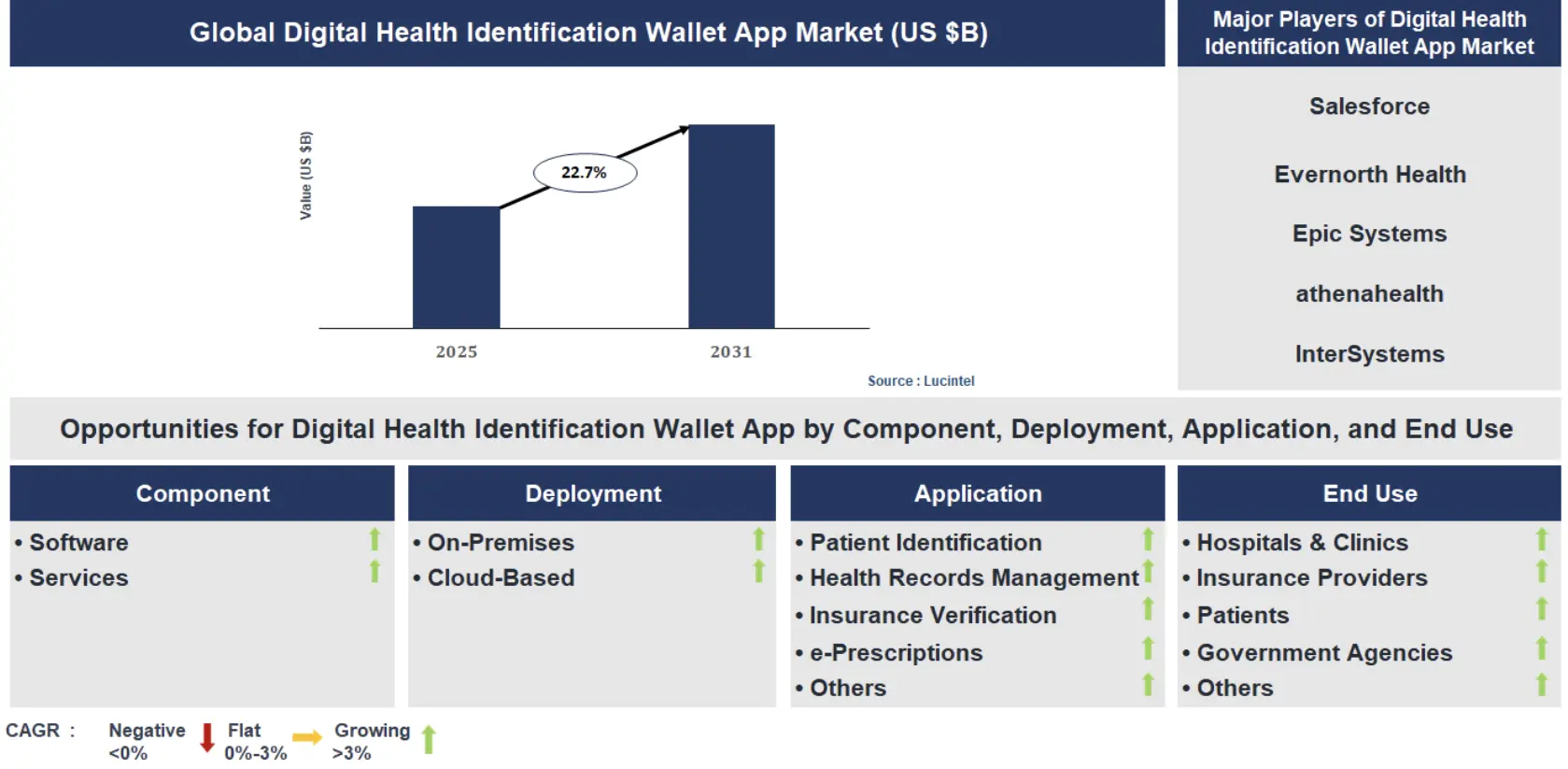

This shift is reflected in market growth shown in a Lucintel Insights report. The global digital health identification wallet app market is projected to grow at a compound annual growth rate of 22.7% between 2025 and 2031. Adoption is expected across hospitals and clinics, insurance providers, patients, and government health agencies, driven by demand for secure digital identity, interoperable access, and regulated data exchange.

For healthcare enterprises, this growth signals a move toward digital health wallets as foundational infrastructure supporting identity, eligibility, and financial workflows across healthcare ecosystems.

Market Insights:

- AI is being used to detect fraud, flag anomalies, and monitor risk across wallet transactions.

- Blockchain is applied to maintain immutable records for identity, consent, and audit trails.

- Hybrid cloud and on-premises deployments support telehealth platforms and wearable data securely.

- In Asia-Pacific markets, ABHA-linked wallets improve interoperability and chronic care management.

- Enterprises are adopting compliant wallet integrations with EHRs to reduce coordination overhead.

These growth drivers and market forecast pointers reaffirm why leading enterprises are investing in building these apps. Healthcare enterprises invest in digital health wallets to reduce payment fragmentation, manage rising patient financial responsibility, and enable embedded finance across regulated care ecosystems.

1. Fragmentation in Healthcare Payments

Healthcare payments rarely move through a single system. Billing platforms, insurance systems, reimbursement engines, and co-pay collection tools often operate independently. As a result, reconciliation becomes manual, slow, and error-prone. Finance teams lose real-time visibility into where money sits and why delays occur.

This fragmentation creates administrative leakage over time. Digital health wallets address this by centralizing financial logic. Instead of chasing transactions across systems, enterprises can govern eligibility, authorization, and settlement from one controlled layer. This simplifies oversight while reducing downstream correction work.

2. Rising Financial Responsibility

Patient financial responsibility has increased steadily. Deductibles, co-pays, and uncovered services now form a significant portion of healthcare revenue. However, most enterprises still rely on fragmented tools to manage patient payments. This creates confusion and delays at the point of care.

Patients expect visibility into what they owe and why. They also expect payments to reflect coverage rules accurately. When systems cannot provide real-time balances, trust erodes quickly. Therefore, enterprises face higher drop-offs, disputes, and collection costs.

A digital health wallet brings clarity to this process. It allows patient-controlled spending while enforcing payer and policy rules in the background. As a result, enterprises improve transparency without losing financial governance.

3. Embedded Finance in Healthcare

Healthcare is steadily adopting embedded finance models. Payments, reimbursements, and benefits are being integrated directly into care journeys. This reduces friction but increases complexity behind the scenes. Financial logic must now respond dynamically to care events.

Digital health wallets enable this shift by acting as orchestration layers across payers, providers, employers, and patients. Instead of triggering payments after the fact, wallets align financial actions with care workflows in real time. This improves coordination across stakeholders.

Because of this, enterprises can support new care models without redesigning financial systems repeatedly. Wallets provide a stable foundation as services evolve.

Micro Case Insight

A payer-provider network reduced claims settlement time by integrating a wallet-based co-pay and reimbursement flow. Authorization, collection, and reimbursement were governed through a single wallet layer. As a result, settlement cycles shortened significantly, and manual reconciliation dropped.

What Is a Digital Health Wallet App?

A digital health wallet app is a secure system that manages healthcare identity, eligibility, and payments in one place. It connects patients, providers, payers, and programs through governed financial and access rules.

Unlike consumer payment apps, it operates inside regulated healthcare workflows. The wallet controls how co-pays, reimbursements, benefits, and subsidies are authorized and settled. It also enforces consent, audit trails, and compliance requirements automatically.

For enterprises, a digital health wallet functions as infrastructure. It supports care delivery, financial coordination, and data integrity at scale, without fragmenting operations or increasing regulatory risk.

Difference Between Consumer Payment Wallets and Healthcare-Grade Financial Platforms

As digital wallets become common, the distinction between consumer payment tools and healthcare-grade financial platforms is often blurred. However, the two serve fundamentally different purposes.

Consumer wallets focus on convenience and speed. At the same time, healthcare-grade platforms prioritize control, compliance, and coordination across regulated environments. Understanding this difference is critical before making architectural decisions.

Comparison: Consumer Payment Wallets vs Healthcare-Grade Financial Platforms

| Aspect | Consumer Payment Wallets | Healthcare-Grade Financial Platforms |

| Primary purpose | Enable fast, simple consumer transactions | Govern healthcare payments and eligibility |

| Regulatory scope | Limited financial compliance | Healthcare and financial regulations combined |

| Data sensitivity | Basic payment data | Clinical, identity, and financial data |

| Consent management | User-initiated, lightweight | Policy-driven, auditable consent controls |

| Integration depth | Retail and banking systems | EHRs, insurers, TPAs, government programs |

| Audit and traceability | Transaction logs only | End-to-end financial and access traceability |

| Scalability focus | Transaction volume | Multi-stakeholder, multi-region operations |

Consumer wallets optimize ease of use for everyday spending, while healthcare-grade financial platforms coordinate payments within complex care and coverage workflows. Therefore, enterprises must design digital health wallets as regulated infrastructure. This approach protects operations, supports scale, and prevents compliance gaps as programs expand.

Types Of Digital Health Wallet Apps You Can Build

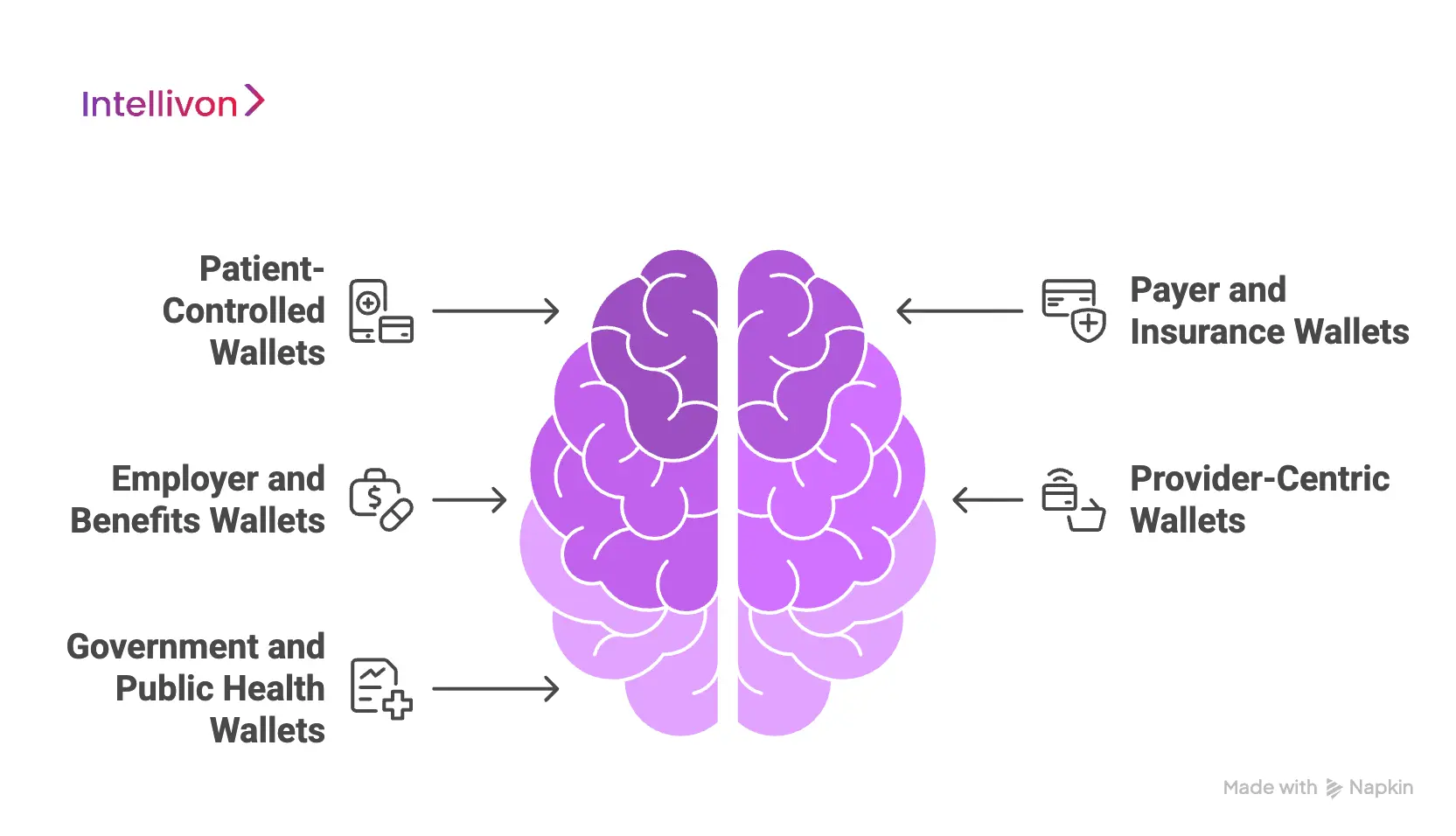

Digital health wallet apps vary by ownership, fund control, and regulatory scope, including patient-led wallets, payer-governed wallets, employer wallets, provider wallets, and government-backed health wallets.

Digital health wallets are not one-size-fits-all platforms. Enterprises design them based on who controls funds, how eligibility is enforced, and where regulatory responsibility sits.

Choosing the right wallet type early prevents rework later. Therefore, this decision should align with operating models, risk appetite, and long-term scale plans.

1. Patient-Controlled Health Wallets

Patient-controlled wallets place spending visibility and payment initiation with the individual. These wallets manage co-pays, uncovered services, reimbursements, and personal health allowances. However, enterprises still enforce rules in the background. Eligibility, consent, and coverage logic remain governed.

This model improves transparency and engagement. It works well where out-of-pocket responsibility is high and clarity matters.

2. Payer and Insurance Wallets

Insurance-led wallets focus on claims settlement, benefits distribution, and reimbursement flows. Funds are released based on policy rules and care events. As a result, settlement cycles shorten and leakage reduces.

These wallets integrate deeply with claims engines and EHR systems. They suit insurers, TPAs, and payer-provider networks managing high transaction volumes.

3. Employer and Benefits Wallets

Employer wallets manage health allowances, wellness budgets, and preventive care incentives. They align spending with corporate health programs and compliance policies. Therefore, finance and HR teams gain clearer oversight.

This model supports workforce health strategies without creating fragmented payment tools.

4. Provider-Centric Wallets

Provider wallets streamline co-pay collection, refunds, and bundled payments. They reduce front-desk friction and manual reconciliation. In addition, they improve cash flow predictability.

Hospitals and clinic networks often adopt this model to simplify patient financial interactions.

5. Government and Public Health Wallets

Government-backed wallets distribute subsidies, scheme benefits, and public health entitlements. They require strict identity validation, audit trails, and interoperability. Consequently, governance takes priority over speed.

This model supports national health programs and population-scale initiatives.

Each wallet type solves a different operational problem. Enterprises succeed when wallet design reflects who governs funds, how rules apply, and where accountability sits.

Compliance Rules A Digital Health Wallet App Must Follow

Digital health wallet apps must comply with healthcare, financial, data protection, and identity regulations to ensure secure, auditable, and scalable payment and access workflows.

Compliance defines whether a digital health wallet can operate at enterprise scale. These platforms sit at the intersection of healthcare data, financial transactions, and identity management. Therefore, regulatory alignment shapes architecture, workflows, and operating models from day one.

Enterprises that treat compliance as an afterthought face rework, delays, and risk exposure. Those who design for compliance early gain stability and speed later.

1. Healthcare Data Protection Regulations

Healthcare wallets handle protected health information alongside financial data. In the United States, HIPAA governs how this data is stored, accessed, and shared. Platforms must enforce minimum necessary access, audit logging, and breach controls.

In Europe, GDPR adds stricter requirements around consent, purpose limitation, and the right to be forgotten. Similar privacy laws apply across the UK, Canada, and Australia. As a result, wallets must support region-specific data handling without fragmenting systems.

2. Financial and Payment Compliance

Digital health wallets process regulated financial transactions. PCI DSS compliance is mandatory for handling card payments and payment credentials. Encryption, tokenization, and secure key management are non-negotiable.

In addition, wallets that manage stored value or reimbursements must align with local financial regulations. Anti-money laundering and KYC controls apply where wallets hold or disburse funds. These safeguards protect enterprises from misuse and fraud.

3. Consent, Identity, and Access Governance

Consent management is central to healthcare wallets. Users must explicitly authorize how data and funds are used. At the same time, consent must also be revocable and auditable.

Role-based access control ensures that providers, payers, and administrators only see what they are permitted to access. Therefore, identity governance directly impacts compliance and trust.

4. Data Residency and Cross-Border Rules

Many regions restrict where health and financial data can reside. Data residency laws require platforms to store or process information within specific geographies. Consequently, wallets often need hybrid cloud or on-premises deployments to remain compliant.

Cross-border care models add further complexity. Here, wallets must separate access rights and transaction flows by jurisdiction.

5. Interoperability and Audit Readiness

Healthcare wallets integrate with EHRs, claims systems, and government registries. Standards such as HL7 and FHIR support compliant data exchange. In addition, full audit trails are required to demonstrate regulatory adherence during reviews.

Compliance is the framework that makes scale possible. Enterprises that build compliance into wallet design protect operations, maintain trust, and stay prepared for regulatory change.

How Digital Health Wallets Cut Payment Friction by 65%

Digital health wallets reduce payment friction by consolidating billing, co-pay, and reimbursement workflows into a governed financial layer aligned with care delivery.

Healthcare enterprises experience payment friction long before it shows up in financial statements. Delayed settlements, manual reconciliation, and disconnected systems quietly increase cost and risk. Over time, these issues reduce cash flow predictability and strain operations.

1. Fragmented Payment Flows Slow Everything Down

Healthcare payments rarely move through a single system. Billing platforms, insurance engines, reimbursement tools, and co-pay systems often operate in isolation. As a result, finance teams chase transactions instead of managing outcomes.

In one large provider environment, introducing a wallet-based patient payment portal with automated payments and eStatements improved Days in Accounts Receivable by 65%. This improvement came from consolidating payment logic, not from adding staff or changing care delivery. Consequently, reconciliation cycles shortened and visibility improved.

Digital health wallets centralize authorization and settlement rules. Therefore, enterprises reduce handoffs and eliminate blind spots that cause delays.

2. Rising Patient Responsibility Increases Collection Risk

Patient-paid revenue now represents a larger share of healthcare income. However, legacy systems provide limited clarity at the point of care. Patients often see fragmented balances, while staff manage disputes after services are delivered.

Wallet-based payment layers provide real-time balance visibility tied to coverage rules. In addition, co-pays and reimbursements align with eligibility before services occur. This reduces disputes and improves collections without adding pressure to care teams.

3. Embedded Finance Aligns Payments With Care Workflows

Healthcare is steadily embedding finance into care journeys. Payments now trigger alongside appointments, prescriptions, and follow-ups. Without coordination, this complexity introduces new failure points.

Digital health wallets act as orchestration layers across payers, providers, and patients. Therefore, financial actions remain synchronized with clinical events, even as services scale.

Payment friction reflects how fragmented systems operate at scale. Digital health wallets reduce this friction by restoring structure, visibility, and timing across healthcare payment flows.

Core Features of a Digital Health Wallet App

Enterprise-grade digital health wallets require layered capabilities spanning core financial functions, governance controls, and scalable infrastructure to operate safely in regulated healthcare environments.

Digital health wallets fail when they are treated as flat feature sets. Enterprises succeed when wallets are designed as layered systems. Each layer solves a different class of risk, from daily operations to regulatory survival at scale. Therefore, enterprise-grade wallets combine functional capability with governance and infrastructure from the start.

Layer 1: Core Wallet Capabilities

These features enable the wallet to function in real healthcare workflows. They form the operational foundation but do not, on their own, guarantee enterprise readiness.

- Secure User Identity and KYC: Verifies patients, providers, and organizations while enforcing role-based access.

- Multi-Source Balance Management: Supports insurance coverage, employer credits, personal funds, and government subsidies within a single view.

- Transaction Authorization and Consent Controls: Ensures payments occur only within approved eligibility and consent boundaries.

- Care-Linked Payment Triggers: Aligns financial actions with appointments, procedures, prescriptions, and outcomes.

- Claims, Refunds, and Reimbursement Engine: Automates settlement logic across payers, providers, and patients.

- Wallet Activity Logs and Financial Transparency: Provides real-time visibility into balances, transactions, and usage history.

- Provider and Payer Settlement Dashboards: Improves oversight of inflows, outflows, and settlement cycles.

- API Layer for EHRs, Claims, and Payment Gateways: Connects the wallet with clinical, insurance, and financial systems.

Layer 2: Governance, Compliance, and Risk Controls

This layer determines whether a wallet survives audits, scale, and regulatory scrutiny. Enterprises evaluate this before approving long-term rollout.

- Policy-Driven Rules Engine: Controls who can pay, when payments trigger, and under what conditions.

- Consent Versioning and Audit Trails: Maintains historical records of consent and transaction decisions, often supported by immutable ledgers or blockchain.

- AI-Assisted Fraud and Anomaly Detection: Flags unusual spending, velocity breaches, and misuse in real time.

- Regulatory Reporting and Evidence Generation: Produces audit-ready outputs for healthcare and financial regulators.

- EHR and Identity Registry Integration: Supports deep interoperability, including government-linked identity systems such as ABHA, where applicable.

Layer 3: Enterprise Deployment and Scale Infrastructure

This layer supports multi-region operations, data residency, and long-term growth without system redesign.

- Hybrid Cloud and On-Premises Deployment: Meets data residency and security requirements across jurisdictions.

- Tenant Isolation and Environment Controls: Separates data and workflows across enterprises, programs, and regions.

- High-Availability and Disaster Recovery: Ensures continuity during outages and peak transaction loads.

- Operational Monitoring and SLA Visibility: Provides performance, reliability, and compliance oversight at scale.

Enterprise-grade digital health wallets are defined by how well capability, governance, and infrastructure work together. Organizations that design wallets in layers reduce risk, avoid rework, and build platforms that scale with confidence.

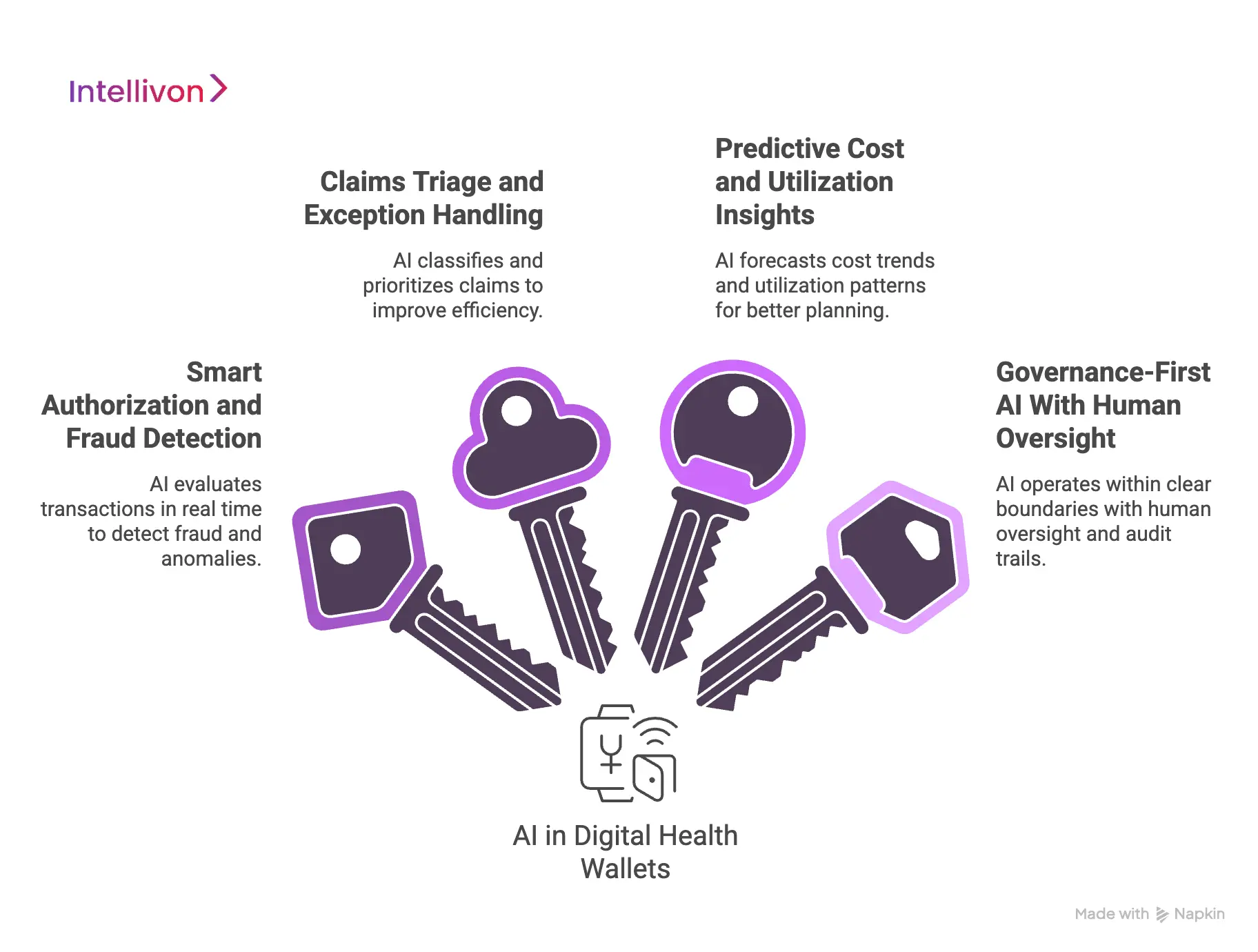

How AI Can Enhance Digital Health Wallets (Safely)

AI enhances digital health wallets by supporting authorization, claims handling, and cost insights, while remaining governed, explainable, and subject to mandatory human oversight.

AI can improve how digital health wallets operate. However, in regulated healthcare finance, AI must remain constrained, explainable, and accountable.

Enterprises adopt AI not to replace judgment, but to reduce friction while preserving control. Therefore, every AI capability must operate within clearly defined boundaries.

1. Smart Authorization and Fraud Detection

AI can evaluate transaction context in real time. It reviews patterns such as frequency, amount, eligibility alignment, and historical behavior. As a result, wallets can flag anomalies faster than rule-based systems alone.

However, AI does not approve or deny high-risk transactions autonomously. It generates risk scores and recommendations that map back to policy rules. Explainable outputs show why a transaction was flagged. Finance and compliance teams retain final authority for exceptions.

Bias controls monitor whether alerts disproportionately affect specific groups or programs. This prevents uneven enforcement across populations.

2. Claims Triage and Exception Handling

Claims workflows generate delays when exceptions pile up. AI helps by classifying claims, prioritizing anomalies, and routing edge cases to the right teams. Consequently, routine claims move faster while attention stays focused where it is needed.

AI does not adjudicate claims independently. It assists by highlighting inconsistencies between clinical records, coverage rules, and submitted amounts. Each recommendation includes traceable inputs and confidence levels. Human reviewers make the final determination.

This structure improves throughput without weakening accountability.

3. Predictive Cost and Utilization Insights

AI models can forecast cost trends and utilization patterns across populations. These insights help enterprises plan budgets, detect leakage, and optimize care programs. Therefore, leaders gain foresight instead of reacting to overruns later.

AI outputs remain advisory. They inform planning decisions but do not trigger financial actions automatically. Models are monitored for drift and retrained as care patterns change. Data quality checks run before insights are generated to reduce noise and bias.

4. Governance-First AI With Human Oversight

Governance defines how AI is allowed to operate. Enterprises set clear decision boundaries, confidence thresholds, and escalation rules. When thresholds are exceeded, workflows route decisions to human reviewers automatically.

All AI actions are logged with timestamps, inputs, and outcomes. This creates replayable audit trails for internal reviews and regulators. By design, AI supports decision-making but never replaces responsibility.

AI Risks and Safeguards in Digital Health Wallets

| AI Risk | Enterprise Safeguard |

| Incorrect transaction approvals | AI generates recommendations only; humans approve exceptions |

| Lack of decision transparency | Explainable models with traceable inputs and rule mapping |

| Bias across populations or programs | Continuous bias monitoring and demographic impact reviews |

| Model drift over time | Ongoing validation, retraining, and performance monitoring |

| Regulatory non-compliance | Policy-aligned AI outputs with audit-ready logs |

| Over-automation of financial decisions | Hard decision boundaries and mandatory human oversight |

AI adds value to digital health wallets when it supports decisions, not replaces them. Clear boundaries, explainability, and human oversight prevent risk while improving efficiency. When governed properly, AI strengthens trust and enables scale without compromising compliance.

How We Build a Digital Health Wallet App

Intellivon builds digital health wallet apps through a step-by-step process focused on governance, compliance, interoperability, and scalable deployment across regulated healthcare and payment ecosystems.

Enterprises do not fail because they lack features. They fail because the wallet cannot survive real operating conditions. Regulations change, stakeholders multiply, and integrations expand. Therefore, Intellivon treats digital health wallets as enterprise financial infrastructure, not app projects. Delivery stays compliance-led, integration-first, and designed for controlled scale.

Step 1: Define the Wallet Model

Every build starts by clarifying what the wallet is allowed to do. Ownership of funds, eligibility enforcement, and jurisdictional scope are mapped early. This avoids building workflows that later violate financial or healthcare regulations. In addition, decision rights are assigned across payer, provider, and enterprise teams.

Intellivon documents boundaries in plain language. This helps legal, compliance, and finance align before architecture begins.

Step 2: Map End-to-End Money Flows

Next, the wallet is anchored to real workflows. Co-pays, reimbursements, claims, refunds, and subsidies are traced from trigger to settlement. This includes exceptions, disputes, reversals, and partial payments.

As a result, the design reflects operational reality, not idealized flows. This step also defines where automation is safe and where human review must remain final.

Step 3: Design a Layered Architecture

Intellivon designs wallets in layers. Core wallet functions sit separately from governance, risk controls, and infrastructure. Therefore, enterprises can adjust policies without rewriting payment logic. The design supports multi-tenant operations, audit readiness, and program-level rule changes.

Where audit depth is critical, immutable records can be implemented using blockchain-backed ledgers. This strengthens traceability for consent and transaction history.

Step 4: Choose the Right Deployment Model

Deployment choices follow compliance requirements, not developer preference. Many enterprises require hybrid cloud or on-prem deployments for data residency, latency, or security controls.

Consequently, Intellivon designs for portability and environment isolation from the start. This approach also supports future expansion across regions without rebuilding the platform.

Step 5: Build Interoperability Around EHR

A wallet cannot function as an isolated layer. It must connect with EHR workflows, claims engines, payer systems, and payment gateways. Intellivon prioritizes EHR-integrated architecture using standards such as FHIR where applicable.

In addition, event-driven integration ensures payments align with clinical and administrative triggers.

Step 6: Implement Identity and Access Governance

Identity and consent are built into every workflow. Role-based access ensures each stakeholder sees only what they are permitted to see. Consent is versioned, auditable, and enforceable across transactions.

Therefore, enterprises can demonstrate compliance during audits without manual effort. KYC and verification workflows are applied based on the wallet model and jurisdiction.

Step 7: Add Risk Controls and Safe AI Support

Intellivon adds transaction controls such as thresholds, velocity checks, and anomaly detection. AI can support fraud detection, claims triage, and operational insights.

However, AI does not approve high-risk financial decisions autonomously. Human oversight remains mandatory for exceptions and regulated actions. All AI outputs remain explainable and logged for audit review.

Step 8: Test for Edge Cases

Enterprise wallets fail in the edge cases. Therefore, testing focuses on reversals, partial settlements, benefit conflicts, multi-party disputes, and downtime scenarios.

Load testing validates peak transaction handling. Audit simulations validate traceability across identity, consent, and financial actions. This reduces surprises during rollout.

Step 9: Roll Out in Controlled Phases

Rollout follows a phased model. Enterprises start with one program, one region, or one payer-provider network.

Metrics such as settlement time, cost-to-collect, dispute volume, and Days in A/R guide expansion. As a result, scale happens with evidence, not assumptions.

Building a digital health wallet is a governance and interoperability challenge before it is a UI challenge. Intellivon delivers wallets that operate safely across regulated environments, integrate cleanly with EHR and payer ecosystems, and scale without losing control.

Cost to Build a Digital Health Wallet App

At Intellivon, digital health wallet apps are built as a regulated healthcare financial infrastructure, not as payment features layered onto existing systems. The focus stays on creating platforms that operate safely across providers, payers, regions, and evolving financial regulations. Every design decision accounts for governance, interoperability, and long-term risk exposure from the start.

When budget constraints exist, scope is refined with intent. However, security controls, consent enforcement, settlement logic, and auditability are never reduced. Therefore, enterprises avoid remediation costs that surface after launch. Predictability replaces rework, and long-term ROI remains protected.

Estimated Phase-Wise Cost Breakdown

| Phase | Description | Estimated Cost Range (USD) |

| Discovery & Regulatory Alignment | Wallet model definition, payment scope, jurisdiction mapping, financial compliance assessment | $8,000 – $14,000 |

| Secure Architecture Design | Layered wallet architecture, identity flows, consent logic, settlement design | $10,000 – $18,000 |

| Governance & Policy Framework | Eligibility rules, authorization policies, audit workflows, exception handling | $9,000 – $16,000 |

| Backend & Enterprise Integrations | EHRs, claims engines, insurers, payment gateways, identity registries | $16,000 – $30,000 |

| Frontend & Role-Based Interfaces | Patient, provider, payer, and admin dashboards with access controls | $11,000 – $19,000 |

| Wallet Ledger & Balance Management | Multi-source balances, transaction history, reconciliation logic | $10,000 – $18,000 |

| Security & Financial Controls | Encryption, fraud monitoring, thresholds, access enforcement | $10,000 – $18,000 |

| Testing & Compliance Validation | Functional testing, security testing, financial audits, compliance readiness | $7,000 – $12,000 |

| Deployment & Scale Readiness | Cloud or hybrid deployment, monitoring, performance tuning | $8,000 – $14,000 |

Total initial investment: $90,000 – $190,000

Ongoing maintenance and optimization: ~15–20% of the initial build per year

Hidden Costs Enterprises Should Plan For

Even well-scoped digital health wallet programs face pressure when indirect cost drivers are ignored. Planning for these early protects budgets, timelines, and compliance posture as transaction volume grows.

- Integration complexity increases as EHRs, claims systems, and payer rules expand

- Compliance overhead grows due to audits, financial reporting, and regulation updates

- Governance requires continuous policy tuning, consent reviews, and exception handling

- Infrastructure costs rise with transaction volume, analytics, and monitoring workloads

- Change management includes onboarding finance, operations, and support teams

- Continuous monitoring becomes critical as financial scrutiny increases

Best Practices to Avoid Budget Overruns

Based on Intellivon’s experience delivering enterprise healthcare and fintech platforms, these practices consistently lead to controlled costs and predictable outcomes.

- Start with a clearly defined wallet model before expanding programs or regions

- Embed governance, auditability, and financial controls into core architecture

- Use modular components that scale without redesign

- Plan interoperability early to avoid expensive retrofitting

- Maintain observability across performance, fraud, and compliance

- Design for regulatory evolution rather than one-time certification

Request a tailored proposal from Intellivon’s healthcare and fintech experts to receive a delivery roadmap aligned with your budget constraints, compliance exposure, and long-term digital health wallet strategy.

How We Make Sure Your Digital Health Wallet App Is Secure

Intellivon secures digital health wallet apps through layered security controls covering identity, data, transactions, infrastructure, and continuous monitoring.

Security is not a layer added at the end of a digital health wallet build. It is the condition that allows the platform to operate at enterprise scale. Wallets handle identity, healthcare data, and regulated financial transactions simultaneously. Therefore, even minor gaps create outsized risk.

At Intellivon, security is designed as a system, not a checklist. Controls are embedded across architecture, workflows, and operations. This approach reduces exposure without slowing delivery.

1. Security Starts With Architecture

Security decisions begin at the architecture stage. Wallet services are separated by function, access level, and risk profile. This limits the blast radius when issues occur. In addition, sensitive operations are isolated from user-facing components.

Hybrid cloud and on-prem deployments are supported where data residency or latency requires it. This ensures compliance without forcing compromises in security posture.

2. Enforced Identity, Access, and Consent

Every user and system interaction is authenticated and authorized. Role-based access ensures patients, providers, payers, and administrators only see permitted data. Consent rules are enforced consistently across transactions and integrations.

At Intellivon, consent is versioned and auditable. Historical states can be reconstructed during reviews. This strengthens trust during regulatory audits and internal investigations.

3. Data Is Protected End to End

All data is encrypted at rest and in transit. Transaction flows use tokenization and secure key management. Thresholds and velocity limits reduce misuse and fraud exposure.

Where audit depth is critical, immutable ledgers can be used to preserve transaction and consent history. This provides tamper resistance without sacrificing performance.

4. Continuous Monitoring and Incident Readiness

Security does not stop at launch. Wallet activity is monitored continuously for anomalies, misuse, and operational drift. Alerts are routed to the right teams with clear escalation paths.

Intellivon designs incident response playbooks alongside the platform. Therefore, enterprises know how issues are contained, investigated, and resolved before they occur.

5. Security Scales With the Platform

As transaction volume and integrations increase, security controls scale with them. Logging, monitoring, and access reviews adjust automatically as programs expand across regions or partners. This prevents security from becoming a bottleneck.

Secure digital health wallets are built through discipline, not shortcuts. By embedding security into architecture, governance, and operations, Intellivon helps enterprises protect sensitive data, maintain compliance, and scale with confidence.

Conclusion

Digital health wallets are becoming core infrastructure for modern healthcare enterprises. When designed correctly, they reduce payment friction, strengthen governance, and support new care models.

However, success depends on building with security, compliance, and interoperability as foundational requirements. Shortcuts create risk that surfaces later at a higher cost.

Enterprises that invest in disciplined design gain stability, visibility, and long-term flexibility. With experience across regulated healthcare and financial systems, Intellivon builds digital health wallets that operate reliably at scale.

These platforms protect sensitive data, align financial flows with care, and support growth without compromising control.

Build a Digital Health Wallet App With Intellivon

At Intellivon, digital health wallet platforms are built as regulated healthcare-fintech infrastructure, not as payment features layered onto care systems. Every architectural and delivery decision prioritizes compliance, financial governance, and interoperability. This ensures wallet platforms operate reliably across providers, payers, employers, and government programs, not just during initial rollout.

As wallet programs expand across regions, populations, and payment models, stability becomes critical. Governance, performance, and audit readiness remain consistent as transaction volume increases. Organizations retain control over identity, funds, and consent without introducing fragmentation, regulatory exposure, or operational complexity.

Why Partner With Intellivon?

- Enterprise-grade health-fintech architecture designed for regulated healthcare ecosystems

- Proven delivery across providers, insurers, employers, and public health programs

- Compliance-by-design approach with audit readiness and policy enforcement

- Secure, modular infrastructure supporting cloud, hybrid, and on-prem deployments

- AI enablement for fraud detection, insights, and automation with governance and oversight

Book a strategy call to explore how Intellivon can help you build and scale a digital health wallet app with confidence, control, and long-term enterprise value.

FAQs

Q1. What is a digital health wallet app in healthcare?

A1. A digital health wallet app is an enterprise platform that manages healthcare identity, eligibility, payments, and reimbursements within regulated workflows. It connects providers, payers, employers, and patients through governed financial logic.

Unlike consumer wallets, it enforces consent, auditability, and compliance across every transaction. For enterprises, it functions as a healthcare-fintech infrastructure rather than a payment feature.

Q2. How is a digital health wallet different from a consumer payment wallet?

A2. Consumer payment wallets focus on speed and convenience for everyday transactions. Digital health wallets operate inside regulated healthcare and financial environments. They integrate with EHRs, claims systems, and payer rules while enforcing consent and audit controls.

Every transaction aligns with care events and coverage logic. This makes them suitable for enterprise-scale healthcare operations.

Q3. Is a digital health wallet app HIPAA and GDPR compliant by default?

A3. No, compliance is not automatic. A digital health wallet must be designed with HIPAA, GDPR, PCI DSS, and local regulations in mind. This includes role-based access, consent enforcement, audit trails, and data residency controls.

Compliance depends on architecture and governance decisions made early. Retrofitting compliance later increases risk and cost.

Q4. How long does it take to build a digital health wallet app?

A4. An enterprise-grade digital health wallet typically takes four to six months for an initial production-ready release. Timelines depend on regulatory scope, integrations, and deployment requirements.

Wallets built with phased rollouts often deliver value earlier. Governance and interoperability planning significantly influence delivery speed.

Q5. Can AI be used safely in digital health wallet platforms?

A5. Yes, when AI is governed properly. In digital health wallets, AI supports fraud detection, claims triage, and cost insights. It does not make autonomous financial or eligibility decisions. Explainability, bias controls, and human oversight remain mandatory. This approach improves efficiency without compromising compliance or trust.