There is an interesting shift happening in banks these days. Institutions that lead in lending are the ones that have fundamentally changed how they make credit decisions. Under these systems, the borrower expectations have shifted, and the need for speed, accuracy, and consistency has become a basic requirement. However, many lending institutions still rely on manual review cycles, separated data, and document-heavy workflows that cannot keep pace. Approval timelines stretching to 30, 60, or even 90 days slowly reduce deal velocity and give market share to faster competitors.

AI agents designed for loan underwriting change that equation significantly. These systems manage the entire credit decision workflow by pulling borrower data, running risk models, flagging issues, and routing exceptions to human reviewers without manual handoffs. Banks that use AI underwriting report a 50 to 75% reduction in time-to-decision for commercial loans.

At Intellivon, we create AI agent-led systems for enterprise lenders. They are built around real underwriting logic, compliance needs, and the realities of core banking integration. Drawing from this hands-on experience, in this blog, we will cover every facet of how we build AI agents for loan underwriting in banks from the ground up.

Why Banks Are Adopting AI Agents Into Loan Underwriting Systems

Banks are quickly adopting AI agents in loan underwriting to automate complex workflows, reduce processing time, and improve risk accuracy. As digital lending becomes more competitive, institutions need faster, smarter decision systems.

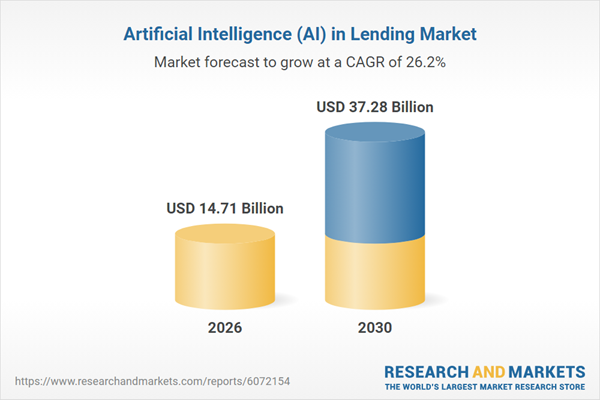

This shift reflects the rapid growth of AI in banking, driven by the need for efficiency, scalability, and compliance in high-volume lending environments. The AI in the lending market is projected to grow from $11.63 billion in 2025 to $14.71 billion in 2026, at a CAGR of 26.5%. This growth reflects increasing demand for faster, data-driven lending decisions.

1. Improving Operational ROI Through Process Efficiency

Banks are seeing a 25% increase in operational ROI by removing manual bottlenecks. AI agents handle the “stare and compare” work of auditing bank statements and tax filings.

This allows human experts to focus on high-level deal structuring. Consequently, the cost-per-loan drops significantly as processing capacity scales without adding headcount.

2. Lowering Default Rates with Granular Risk Analysis

Advanced agents reduce credit risk by up to 15% through multi-dimensional data analysis. Unlike traditional scoring, AI identifies subtle behavioral patterns and cash-flow trends.

This precision prevents losses by flagging high-risk indicators that standard models miss, ensuring a healthier and more resilient loan book.

3. Competing on Speed to Secure Market Share

In a digital-first market, reducing approval times from weeks to minutes is a major growth lever.

AI agents provide instant pre-approvals, capturing borrowers before they turn to competitors. This speed often results in a 10% lift in origination volume.

Given the high ROI signals and 2x faster loan-closure outcomes achieved through the adoption of AI agents, this market trajectory is inevitable.

What Are AI Agents For Loan Underwriting in Banks?

AI agents for loan underwriting are intelligent software systems that automate the end-to-end process of evaluating a borrower’s creditworthiness, without requiring manual intervention at every step.

Think of them as a highly efficient digital underwriter. They collect borrower data, verify documents, run risk assessments, cross-check compliance requirements, and surface a credit decision, all within minutes. Where a human underwriter juggles spreadsheets, credit bureau pulls, and income verification documents sequentially, an AI agent handles all of it simultaneously.

What separates these agents from basic automation is their ability to learn. They continuously refine their decision logic based on historical loan performance, repayment patterns, and borrower behavior, getting sharper over time.

For banks, this means faster approvals, consistent risk assessments, and underwriting teams that focus on complex judgment calls rather than administrative groundwork. That is the core value proposition.

What AI Agents Change in Underwriting Systems

AI agents transform underwriting from a passive data-entry task into an active, reasoning-driven workflow. These digital workers move beyond simple calculations to execute complex, multi-step financial investigations autonomously.

1. Static Scoring to Autonomous Decision Systems

Traditional models provide a frozen snapshot of risk, often missing current financial nuances. AI agents replace this with dynamic profiling, evaluating the “why” behind cash flow shifts rather than just the “what.”

For example, an agent can distinguish between a one-time capital expense and a fundamental decline in revenue, allowing for more precise, context-aware approvals.

2. How Agents Execute Underwriting

While legacy AI merely predicts defaults, agents proactively execute the verification process. They independently fetch tax transcripts, verify business registrations, and flag inconsistencies in bank statements.

This shift turns the agent into a functional team member that completes the administrative “legwork” before a human underwriter even opens the file.

3. Real-time Decision Orchestration

Enterprise lending suffers from fragmented data across CRMs and credit bureaus. AI agents act as connective tissue, orchestrating real-time data flows across these silos.

If a borrower’s credit profile changes during the application window, the agent instantly recalibrates the risk posture, ensuring decisions never rely on stale or incomplete information.

4. Human-in-the-Loop vs. Fully Autonomous Approvals

Banks can toggle between full autonomy for retail loans and “human-in-the-loop” assistance for complex commercial credit. In high-stakes scenarios, the agent drafts the complete credit memo and highlights specific risk anomalies for expert review.

This hybrid approach ensures 100% oversight while achieving the rapid throughput of an automated system.

This evolution replaces rigid software with intelligent orchestration, turning underwriting into a scalable, high-velocity growth engine.

Types of AI Agents in Loan Underwriting Systems

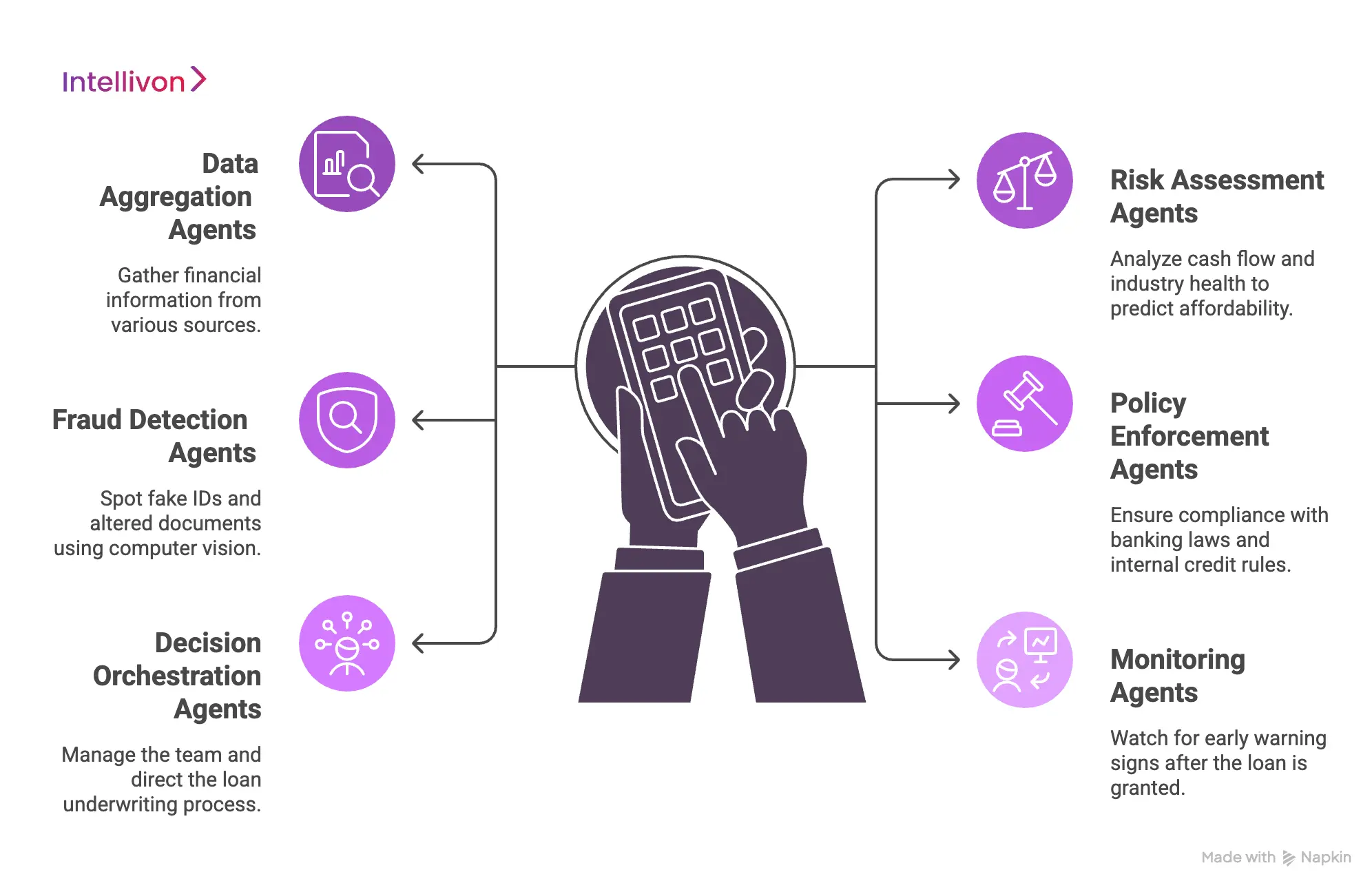

Banks no longer use a single program for loans. They use a team of specialized AI agents. Here, each agent has a specific job, and they work together like a digital department to process applications in parallel.

1. Data Aggregation Agents for Financial Profiles

These agents act as digital investigators who gather a borrower’s full financial story. They instantly pull tax records and bank statements through secure, encrypted links.

For instance, they automatically compare sales records with actual bank deposits to confirm revenue. This confirms the income is real without any manual intervention required from staff.

2. Risk Assessment Agents for Credit Evaluation

These agents specifically analyze cash flow trends and industry health to predict true affordability.

By looking at these deeper patterns, they safely approve “thin-file” borrowers. Old systems would simply reject these leads. As a result, the bank expands its market reach safely.

3. Fraud Detection Agents within Underwriting Flows

These agents act as a high-tech security layer to spot fake IDs or altered documents. They use computer vision to find tiny edits in PDF bank statements instantly.

Consequently, catching these red flags during the application saves banks millions in losses. It stops fraud before the money ever leaves the building.

4. Policy Enforcement Agents for Compliance Checks

These agents act as 24/7 internal auditors to keep the bank compliant with regulations. They check every application against strict banking laws and internal credit rules. However, if a loan gets too close to a legal limit, the agent flags it. A senior manager then reviews it to ensure total regulatory safety.

5. Decision Orchestration Agents across Workflows

This agent is the manager who directs the rest of the team through the process. It knows exactly when to send a file for a fraud check or data fetch.

By managing these steps, the orchestrator keeps the process moving forward. A loan never gets stuck in a digital inbox for days as a result.

6. Monitoring Agents for Post-loan Performance

The work continues even after the bank grants the loan to the borrower. Monitoring agents watch for early warning signs like a sudden drop in daily sales.

This allows the bank to reach out to a struggling borrower early. Specifically, they can offer help months before the borrower actually misses a payment.

This team-based approach ensures every loan receives expert-level care at an incredible speed.

How These Agents Work Together in Production

Deploying AI agents in production requires a shift from linear software to a coordinated, multi-agent ecosystem. These agents function as a digital assembly line where each specialist hands off an “enriched” loan file to the next.

Specifically, this orchestration allows banks to process complex applications in parallel rather than waiting for manual sequential reviews. As a result, the entire lifecycle from intake to decisioning becomes a fluid, high-velocity operation.

Step 1: Intelligent Intake and Data Harvesting

The process begins the moment a borrower submits their initial application data. Immediately, the Data Aggregation Agent springs into action to harvest supporting evidence from integrated APIs and documents.

It pulls bank statements, tax filings, and payroll data in real-time. Furthermore, it reconciles this information against the applicant’s stated income. If a document is missing or illegible, the agent proactively notifies the borrower to rectify the issue before a human ever sees the file.

Step 2: Concurrent Fraud and Identity Verification

While data is being gathered, the Fraud Detection Agent performs a deep-tissue scan of the application’s integrity. It uses computer vision to analyze document metadata for any signs of digital tampering or “pixel-level” alterations.

Simultaneously, it cross-references the identity against global watchlists and internal “known-fraudster” databases. Therefore, this concurrent processing ensures that high-risk applications are flagged and isolated within seconds. This stops bad actors from entering the deeper, more expensive stages of the funnel.

Step 3: Multi-Dimensional Risk and Policy Analysis

Once the data is verified, the Risk Assessment and Policy Enforcement agents evaluate the borrower’s creditworthiness. Specifically, the Risk Agent analyzes cash flow volatility and debt-to-income ratios to predict future repayment capacity.

Meanwhile, the Policy Agent checks the application against the bank’s current “credit box” and federal regulations. If the borrower meets all criteria, the agents generate a comprehensive risk score. However, if any anomalies exist, they draft a detailed summary explaining the specific concerns.

Step 4: Decision Orchestration and Human Handoff

The Decision Orchestration Agent acts as the final traffic controller for the entire workflow. It reviews the outputs from all previous agents to determine the final path for the application.

For low-risk retail loans, it may trigger an instant, fully autonomous approval and generate the loan contract. In contrast, for complex commercial files, it packages the “credit memo” and assigns it to a human underwriter.

Consequently, the underwriter receives a pre-vetted file, allowing them to make a final decision in minutes.

Step 5: Active Disbursement and Performance Monitoring

After the loan is approved, the orchestration agent coordinates with the core banking system to initiate disbursement. However, the system’s job is not yet complete.

The Monitoring Agent begins tracking the loan’s performance against real-time market data and borrower behavior. If it detects a drift in repayment patterns or a sudden drop in the borrower’s industry health, it alerts the risk team. This allows the bank to move from reactive collections to a proactive financial partnership.

This synchronized workflow turns underwriting into a scalable, 24/7 operation that grows alongside the enterprise.

Integration Architecture for Enterprise Banks

An AI agent is only as powerful as the data it can access and the systems it can influence. For enterprise banks, this requires a robust integration layer that connects modern intelligence with legacy stability.

1. Integrating with LOS and Loan Origination Systems

AI agents must plug directly into your existing Loan Origination System (LOS) to avoid workflow disruption. Furthermore, they act as an intelligent orchestration layer that automates manual tasks within the familiar LOS interface.

This allows underwriters to see AI-generated insights without switching applications. Consequently, team adoption is faster because the AI enhances existing tools rather than replacing them.

2. Connecting Core Banking and Payment Systems

True automation requires a deep connection to the bank’s core ledger and payment rails. Agents use secure APIs to verify account balances and past transaction histories instantly.

As a result, they can automate the disbursement of funds once a loan is approved. This bi-directional sync ensures the core system remains the single source of truth for all financial data.

3. Credit Bureau Integrations (Experian, Equifax, TransUnion)

Agents pull real-time reports from major credit bureaus to assess borrower risk profiles. Specifically, they use “Analytics Orchestrator Agents” to translate natural-language queries into complex bureau data requests.

This reduces the time spent on credit analytics from weeks to minutes. Therefore, the bank can make decisions based on the most current credit signals available in the market.

4. Open Banking APIs for Real-Time Financial Data

Open banking provides agents with permissioned access to a borrower’s live cash-flow signals. By connecting to external bank accounts, the agent analyzes actual spending patterns rather than just historical snapshots.

Furthermore, this real-time data allows for more accurate “affordability” assessments. This is especially useful for “thin-file” borrowers who lack a traditional credit history.

5. KYC, AML, and Identity Verification Integrations

Identity agents use computer vision and OCR to verify passports and licenses against global databases. They also perform real-time AML (Anti-Money Laundering) screening to ensure regulatory compliance.

However, if a high-risk flag is detected, the agent immediately isolates the application for human review. This keeps the bank safe from sophisticated synthetic identity fraud and legal penalties.

6. Data Pipelines Across Internal and External Systems

Enterprise-grade agents rely on automated ETL (Extract, Transform, Load) pipelines to move data between disparate silos. These pipelines reconcile information from CRMs, ERPs, and market feeds into a unified borrower profile.

Specifically, they use AI-driven data mapping to ensure information is consistent across all systems. As a result, the bank maintains a 360-degree view of risk at all times.

Modern architecture ensures that AI agents are not just “add-ons” but core drivers of banking efficiency and growth.

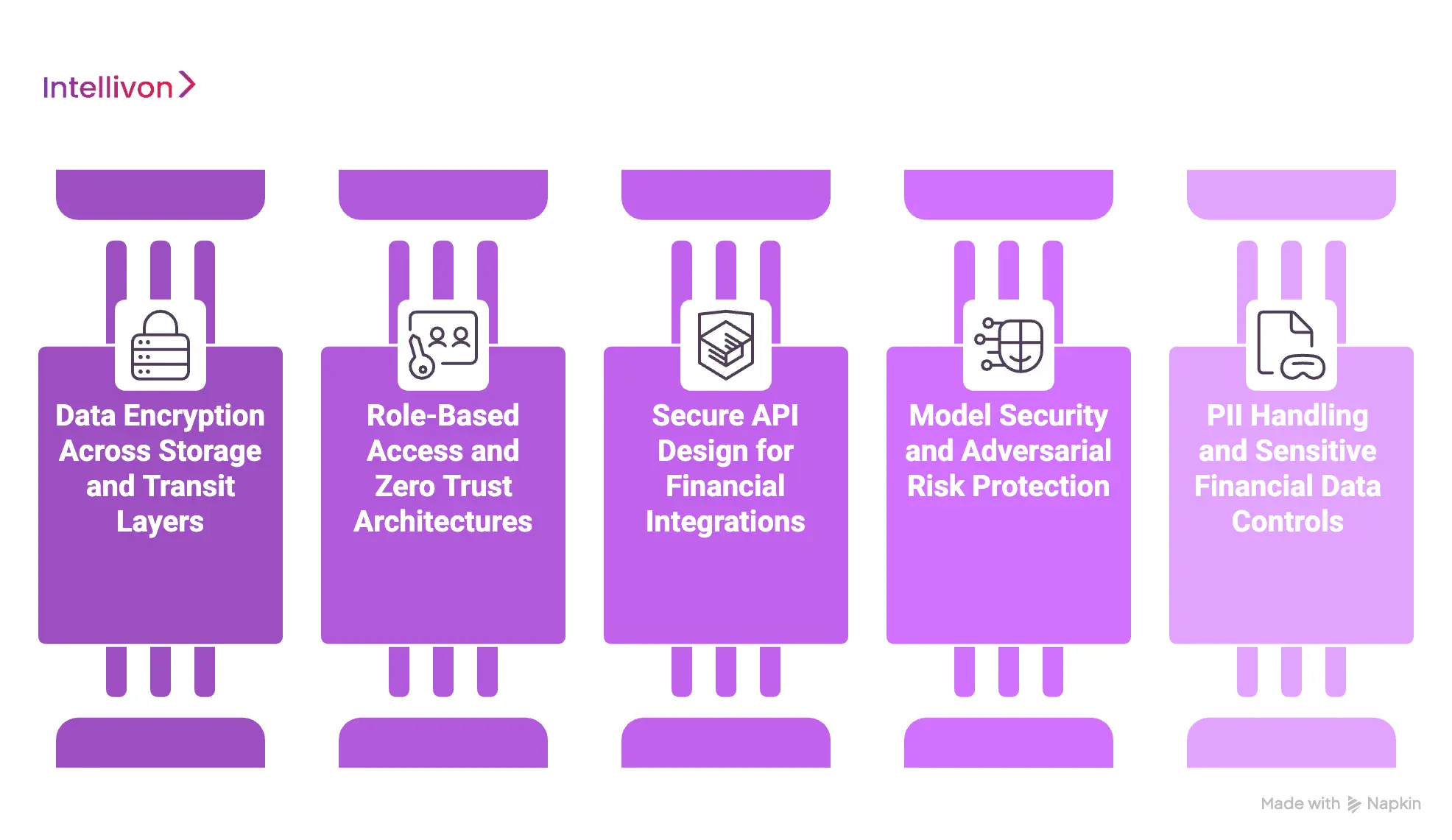

Security Architecture for Underwriting AI Systems

Security is the non-negotiable foundation of any AI deployment within a regulated financial environment. Consequently, enterprise leaders must prioritize a “security-by-design” approach that protects both proprietary models and sensitive borrower data.

1. Data Encryption Across Storage and Transit Layers

Banks must ensure that all financial data remains encrypted at rest and in motion. AI agents use Transport Layer Security (TLS 1.3) to protect data moving between the borrower’s browser and the bank’s servers.

Furthermore, high-performance hardware security modules (HSMs) manage the encryption keys for stored credit files. As a result, even in the event of a perimeter breach, the actual data remains unreadable and useless to unauthorized actors.

2. Role-Based Access and Zero Trust Architectures

A Zero Trust model assumes that no user or system is inherently “safe,” requiring constant verification. Specifically, AI agents operate under the principle of “least privilege,” meaning they only access the specific data points needed for a single task.

For example, a fraud agent can see identity metadata but cannot access the borrower’s full transaction history. This granular control prevents lateral movement by attackers and significantly reduces the internal “blast radius” of any security incident.

3. Secure API Design for Financial Integrations

Every connection between an AI agent and a core banking system is a potential entry point for threats. Therefore, banks must use “hardened” APIs with multi-factor authentication (MFA) and rate-limiting to prevent brute-force attacks.

Each API call is digitally signed and logged to create an immutable audit trail of every automated decision. This ensures that the agent’s interactions with the core ledger are both transparent and highly resistant to interception.

4. Model Security and Adversarial Risk Protection

Generative models are susceptible to “prompt injection” or adversarial attacks designed to trick the AI into approving a bad loan. To counter this, banks deploy “guardrail models” that sit in front of the primary underwriting agent to filter out malicious inputs.

Furthermore, these systems undergo regular “red-teaming” to identify vulnerabilities in the reasoning logic. This proactive defense ensures the AI remains objective and cannot be manipulated by sophisticated bad actors.

5. PII Handling and Sensitive Financial Data Controls

Handling Personally Identifiable Information (PII) requires strict adherence to global privacy laws. AI agents use “data masking” and anonymization techniques to process credit signals without exposing the borrower’s actual identity to the underlying model.

Specifically, names and social security numbers are swapped with unique tokens during the risk-analysis phase. This allows the bank to gain deep insights while remaining fully compliant with GDPR and CCPA regulations.

By building security into the code rather than treating it as an afterthought, banks can scale AI with total confidence.

Compliance Requirements Across Key Markets

Navigating the global regulatory landscape is the most significant hurdle for scaling AI in banking. Therefore, enterprise leaders must ensure their AI agents are “compliance-native” to avoid heavy penalties and reputational risk.

1. US: Fair Lending Laws and Model Explainability

The Consumer Financial Protection Bureau (CFPB) mandates that AI models must not result in “disparate impact.” Consequently, AI agents must be programmed to ignore protected characteristics like race or gender. Furthermore, as of 2026, new rules prevent using medical debt in credit decisions.

Under the Equal Credit Opportunity Act (ECOA), banks must provide clear “adverse action notices” for every denial. Specifically, these notices must explain the exact reasons for the rejection in plain English.

2. UK: FCA Guidelines and Credit Risk Transparency

The Financial Conduct Authority (FCA) recently launched the Mills Review to evaluate AI in financial services. Specifically, UK banks must demonstrate that their AI agents align with “Consumer Duty” rules. This requires rigorous testing to ensure that automated systems do not encourage unaffordable lending.

As a result, transparency in how the agent calculates credit risk is essential. Therefore, maintaining a UK banking license now depends on proving the AI is acting in the customer’s best interest.

3. Canada: OSFI Compliance in Lending Systems

Canada’s Office of the Superintendent of Financial Institutions (OSFI) focuses on “Model Risk Management” through Guideline E-23. Specifically, algorithmic engines now require formal validation and ongoing monitoring.

AI agents in Canada must undergo regular stress tests to ensure stability. Furthermore, banks must maintain a human-in-the-loop to override AI decisions that carry non-negligible risk. Consequently, this keeps the Canadian financial system resilient against automated errors.

4. Australia: APRA Regulations and Risk Governance

The Australian Prudential Regulation Authority (APRA) requires strict governance over automated technology under standards like CPS 230. Specifically, Australian banks must treat credit-focused AI as a “high-risk” deployment.

Therefore, every piece of data used by the agent must be traceable to its source. This ensures that the bank remains accountable for its automated portfolio. As a result, lenders can scale their operations without sacrificing regulatory integrity.

5. Audit Trails and Explainable AI in Decisions

Regardless of the region, every automated approval must generate a permanent, immutable audit trail. AI agents use “Shapley values” to explain which specific factors influenced the outcome most.

Specifically, this “Explainable AI” (XAI) allows regulators to see exactly why a decision was made. Consequently, the bank can defend its actions during a formal audit. This builds long-term trust with both regulators and customers.

Adhering to these global standards transforms compliance from a mandatory burden into a competitive advantage.

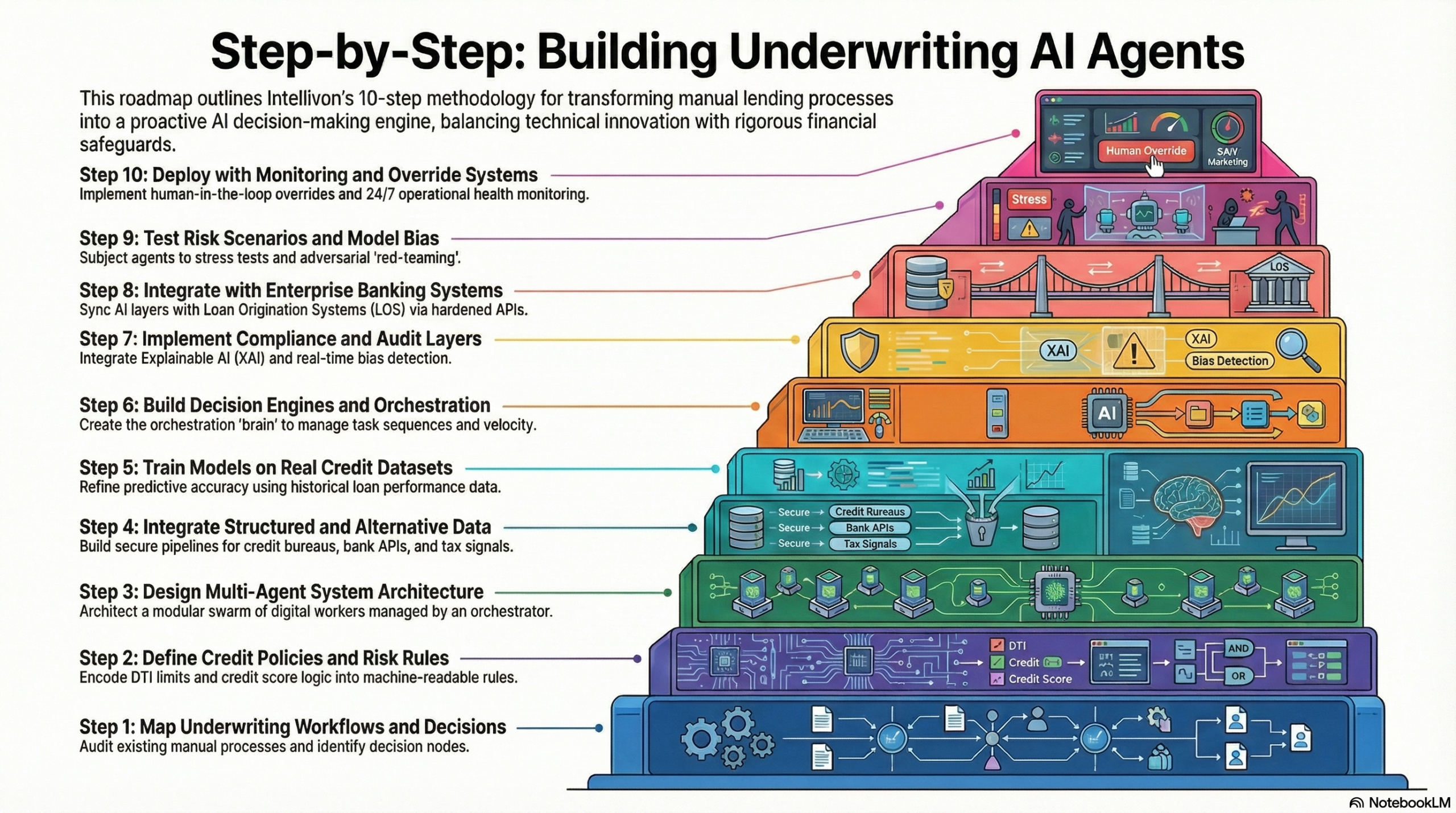

Step-by-Step: Building Underwriting AI Agents

Building a production-grade AI agent requires a structured approach that balances technical innovation with rigorous financial safeguards. At Intellivon, we follow a battle-tested roadmap to ensure your lending agents are both high-performing and regulatory-compliant.

Consequently, this methodology transforms your existing data into a proactive decision-making engine.

Step 1: Map Underwriting Workflows and Decisions

First, we audit your existing manual processes to identify specific bottlenecks and decision nodes. We document every touchpoint where an underwriter currently intervenes to verify data or assess risk.

Furthermore, we define the “ground truth” for what constitutes a successful approval within your specific portfolio. This baseline allows us to design an agent that mirrors your best human experts.

Step 2: Define Credit Policies and Risk Rules

Next, we translate your internal “credit box” into machine-readable logic and guardrails. Specifically, we encode your debt-to-income (DTI) limits and minimum credit score requirements into the agent’s core reasoning layer.

This ensures the AI never deviates from your established risk appetite. Therefore, the system remains a loyal execution arm of your credit committee.

Step 3: Design Multi-Agent System Architecture

We then architect a modular ecosystem where specialized agents handle data, fraud, and risk in parallel. Instead of a single “black box,” we build a transparent swarm of digital workers that communicate through a central orchestrator.

Consequently, this modularity allows you to update individual risk models without disrupting the entire underwriting pipeline.

Step 4: Integrate Structured and Alternative Data

At this stage, we build secure pipelines to ingest data from credit bureaus, bank APIs, and tax authorities. We also integrate alternative signals like utility payments or cash-flow volatility for a 360-degree borrower view.

Furthermore, we use AI-driven data mapping to ensure consistency across these disparate sources. As a result, your agents make decisions based on the most current financial signals.

Step 5: Train Models on Real Credit Datasets

We refine the agent’s predictive accuracy by training it on your historical loan performance data. These models learn to identify the subtle patterns that led to both successful repayments and defaults in the past.

This training is conducted in a secure environment to protect sensitive information. This step ensures the agent’s “intuition” is grounded in your bank’s actual performance history.

Step 6: Build Decision Engines and Orchestration

The “brain” of the system is the orchestration layer that manages the sequence of tasks. We build logic that determines when a file is ready for a final decision or when it needs more data.

Specifically, the orchestrator triggers different agents based on the loan type or complexity. Consequently, this keeps the workflow moving forward at maximum velocity without any manual oversight.

Step 7: Implement Compliance and Audit Layers

We integrate “Explainable AI” (XAI) modules to provide a clear rationale for every automated decision. These layers generate the audit trails required by regulators like the CFPB or FCA.

Furthermore, we implement real-time bias detection to ensure the agent remains fair and objective. Therefore, your bank stays protected against legal and reputational risks.

Step 8: Integrate with Enterprise Banking Systems

Our team ensures the agents plug seamlessly into your existing Loan Origination System (LOS) and core ledger. We use hardened APIs to sync data between the AI layer and your legacy infrastructure.

This bi-directional connection allows for automated loan disbursement and real-time account updates. As a result, your team can work within their familiar tools while benefiting from AI.

Step 9: Test Risk Scenarios and Model Bias

Before going live, we subject the agents to rigorous stress tests and adversarial “red-teaming.” Specifically, we simulate extreme economic shifts to see how the agent’s risk appetite reacts.

We also perform deep-dive bias audits to ensure no protected groups are unfairly disadvantaged. This phase guarantees the system is resilient and ethically sound.

Step 10: Deploy with Monitoring and Override Systems

Finally, we deploy the agents with a robust “human-in-the-loop” override system. Specifically, your senior underwriters retain the final authority to review and reverse any AI-generated decision.

We also implement 24/7 monitoring to track model drift and operational health. Consequently, you maintain total control over your portfolio while enjoying the benefits of full automation.

By following this precise blueprint, Intellivon ensures your transition to agentic underwriting is seamless, secure, and highly profitable.

Real Challenges in Agentic AI Underwriting Systems

Transitioning to an agentic model involves navigating complex structural and regulatory hurdles. Specifically, enterprise leaders must address these friction points to ensure their AI investment delivers long-term stability.

At Intellivon, we specialize in overcoming these specific engineering and compliance bottlenecks.

1. Fragmented Financial Data Across Systems

Data silos between the LOS, core banking, and credit bureaus often create incomplete borrower profiles. This fragmentation leads to inaccurate risk assessments and missed opportunities.

- The Fix: We deploy a unified data layer with automated ingestion pipelines.

- The Outcome: Your agents receive consistent, real-time inputs for every decision.

2. Integration with Legacy Banking Systems

Monolithic cores and outdated APIs frequently break automated workflows. Consequently, this results in partial automation that still requires heavy manual intervention.

- The Fix: We implement API-first middleware to act as a bridge.

- The Outcome: You achieve a seamless decision flow across all internal systems.

3. Lack of Explainability in AI Decisions

Regulators reject “black-box” models that cannot justify a loan denial. Specifically, a lack of transparency creates massive legal and audit risks for the bank.

- The Fix: We integrate explainable AI layers and detailed decision trace logs.

- The Outcome: Every automated action is audit-ready and fully regulator-compliant.

4. Bias and Fairness in Credit Decisions

Biased training datasets can inadvertently lead to unfair lending practices. Therefore, without active intervention, your AI might mirror historical human prejudices.

- The Fix: We use bias detection pipelines and strict fairness constraints.

- The Outcome: Your lending remains compliant, fair, and transparent across all demographics.

5. Real-Time Decisioning at Scale

Batch-based legacy systems cannot support the “instant” approvals modern customers expect. Specifically, this latency causes high lead abandonment and lost market share.

- The Fix: We build event-driven agent orchestration systems.

- The Outcome: You deliver instant, scalable underwriting decisions at any volume.

6. Compliance Across Multiple Regions

Different regulatory frameworks make it difficult to maintain consistent global policies. As a result, scaling an AI solution across borders often leads to compliance failures.

- The Fix: We deploy policy-driven compliance engines tailored for each region.

- The Outcome: You gain global scalability with localized regulatory precision.

7. Model Drift and Changing Risk Patterns

Borrower behavior evolves, which means a model that worked last year may fail today. Specifically, failing to account for “drift” leads to declining accuracy and higher default rates.

- The Fix: We implement continuous learning and real-time monitoring pipelines.

- The Outcome: Your risk evaluation remains adaptive and accurate as market conditions shift.

Addressing these challenges directly allows your institution to build a resilient and future-proof lending engine.

Case Study: Multi-Agent Underwriting Platform

Transforming a traditional lending operation into an automated powerhouse requires a strategic shift in architecture. Specifically, this case study highlights how moving from manual workflows to an agentic ecosystem creates measurable enterprise value.

Problem: Fragmented and Manual Underwriting System

The institution struggled with disconnected data sources and a high dependency on manual reviews. Specifically, underwriters spent 60% of their time on data entry rather than risk analysis. Furthermore, these bottlenecks led to delayed approvals and high customer abandonment rates.

As a result, the bank could not scale its loan volume without significantly increasing its headcount.

Solution: Multi-Agent Orchestration Platform

Intellivon designed and deployed a custom multi-agent underwriting system to modernize the entire funnel. We introduced a central orchestration layer to coordinate decisions between specialized agents.

Furthermore, we automated underwriting workflows end-to-end while embedding human checkpoints for risk-sensitive cases. Consequently, this hybrid approach maintained total institutional control while achieving machine-level speed.

System Architecture and Integrations

Our team successfully integrated the platform with the bank’s existing LOS and core banking systems. Specifically, we connected real-time KYC, AML, and open banking APIs into a single decision engine.

We also built a unified data pipeline that fed consistent information to every specialized agent. Therefore, the system eliminated data silos and provided a 360-degree view of every applicant.

How Automation Worked in Practice

Applications are now routed dynamically across the agent swarm based on complexity. Specifically, low-risk retail loans receive instant, fully autonomous approvals within seconds.

However, complex edge cases are automatically flagged and packaged for manual human review. Furthermore, the system continuously learns from repayment behavior to refine its future risk predictions.

Results: Measurable Business Impact

The implementation delivered immediate and transformative results for the bank’s bottom line.

- Approval Time: Reduced by 92%, moving from days to minutes.

- Manual Workload: Decreased by 80% through automated document verification.

- Risk Accuracy: Improved default prediction by 18% using alternative data signals.

- Scalability: The bank doubled its loan origination volume without increasing its team size.

By partnering with Intellivon, the institution turned a slow cost center into a high-speed engine for growth.

Cost to Build AI Agents for Underwriting

Building AI agents for loan underwriting is not a fixed-cost project. The total investment depends on how deeply the system integrates with core banking, credit bureaus, compliance layers, and underwriting workflows.

Unlike standalone AI models, underwriting agents operate within a multi-agent, decision-driven architecture. As a result, costs are shaped more by system design, orchestration, and integrations than just model development.

1. Cost Breakdown by Modules and Complexity

| Component | Scope | Estimated Cost |

| Data Aggregation Layer | Banking data, bureau APIs, and alt-data ingestion | $15,000 – $35,000 |

| Risk Assessment Agents | Credit scoring, behavioral models | $20,000 – $50,000 |

| Fraud Detection Agents | Identity checks, anomaly detection | $10,000 – $30,000 |

| Policy & Compliance Engine | Rule enforcement, audit logic | $15,000 – $40,000 |

| Decision Orchestration Layer | Multi-agent workflow routing | $25,000 – $60,000 |

| Monitoring & Feedback Systems | Model tracking, performance loops | $10,000 – $25,000 |

Agents are built as part of a unified underwriting system, not isolated components.

2. Infrastructure and Integration Costs

| Component | Scope | Estimated Cost |

| Cloud Infrastructure (AWS/GCP/Azure) | Compute, storage, scaling | $8,000 – $20,000/year |

| Data Pipelines | Real-time data processing | $10,000 – $25,000 |

| API & Integration Layer | LOS, core banking, external APIs | $15,000 – $40,000 |

| Event-Driven Architecture | Workflow triggers and automation | $10,000 – $30,000 |

A cloud-native, API-first setup ensures scalability. Costs increase with transaction volume, integrations, and real-time decision requirements.

3. Security and Compliance Costs

| Component | Scope | Estimated Cost |

| Data Encryption & Access Control | PII protection, role-based access | $8,000 – $20,000 |

| Audit Logs & Explainability | Decision traceability | $5,000 – $15,000 |

| Regulatory Compliance Setup | US, UK, CA, AU standards | $10,000 – $25,000 |

| Security Testing | Penetration testing, audits | $5,000 – $12,000 |

Financial systems cannot compromise on compliance. These are core system requirements, not optional features.

Hidden Costs Enterprises Often Miss

- Integration with legacy banking systems

- Data normalization across multiple financial sources

- Workflow redesign for automated underwriting

- Continuous model retraining and monitoring

- Regulatory updates and audit requirements

These factors typically increase total project costs by 20–30%.

Estimated Total Cost Range

| Platform Scope | Estimated Cost |

| MVP (Single-Agent System) | $80,000 – $150,000 |

| Mid-Level AI Underwriting System | $150,000 – $300,000 |

| Enterprise Multi-Agent Platform | $300,000 – $600,000+ |

Most banks underestimate the cost of AI underwriting by focusing only on model development. In reality, the majority of investment goes into integration, orchestration, and compliance layers.

At Intellivon, underwriting systems are built as financial decision infrastructure, and not just AI tools. This ensures the platform scales across products, geographies, and regulatory environments without constant rework.

Conclusion

AI agents are transforming loan underwriting from manual processes into scalable decision systems. However, success depends on how well these systems are designed, integrated, and governed.

Banks that treat this as infrastructure, and not experimentation, gain faster approvals, better risk control, and long-term efficiency. With the right architecture and partner, underwriting becomes a competitive advantage, not a bottleneck.

Build AI Underwriting Agents With Intellivon

At Intellivon, AI underwriting agents are built as a financial decision infrastructure, not isolated AI models layered onto existing systems. The focus is to create a unified platform that connects data, decision logic, and execution across your entire lending workflow.

As a result, banks reduce manual effort, improve decision accuracy, and scale underwriting without increasing operational overhead.

Our engineering approach combines multi-agent architectures with API-first, cloud-native systems. This ensures seamless integration with loan origination systems, core banking platforms, credit bureaus, KYC/AML tools, and third-party data sources without disrupting ongoing operations.

Why Build With Intellivon

- Infrastructure-First Approach: We build systems that scale with your lending operations, not short-term automation layers that require constant rework.

- Built for Real Underwriting Workflows: Every system is designed around actual credit decision processes, ensuring alignment with operational and risk management needs.

- API-First, Integration-Ready Architecture: Seamless connectivity across banking systems, financial APIs, and third-party services without breaking existing workflows.

- Compliance and Explainability Built In: Every decision is traceable, auditable, and aligned with regulatory requirements across global markets.

- Multi-Agent Orchestration at Scale: Coordinated AI agents handle complex underwriting workflows with built-in automation and human checkpoints where required.

If you’re planning to modernize your underwriting systems, the next step is not adding another tool. It is building a decision system that scales with your business.

Talk to Intellivon to design and deploy AI underwriting agents tailored to your lending workflows.

FAQs

Q1. What are AI agents in underwriting systems?

A1. AI agents in underwriting systems are autonomous decision units that handle specific parts of the loan approval process. These include data collection, risk assessment, fraud detection, and policy checks. Unlike traditional models, agents do not just predict outcomes. They execute decisions, interact with systems, and operate within defined workflows to automate underwriting end-to-end.

Q2. How do they integrate with banking systems?

A2. AI underwriting agents integrate through API-first architectures that connect with loan origination systems, core banking platforms, and third-party services. These include credit bureaus, KYC/AML tools, and open banking APIs. Integration layers ensure real-time data flow, allowing agents to operate within existing workflows without disrupting legacy systems.

Q3. Are AI underwriting systems compliant globally?

A3. Yes, AI underwriting systems can be designed to meet regulatory requirements across regions such as the US, UK, Canada, and Australia. Compliance is achieved through explainable decision logic, audit trails, data protection measures, and policy-based controls. Systems must align with local regulations like fair lending laws and financial governance frameworks.

Q4. What is the cost of building such systems?

A4. The cost depends on system complexity, number of agents, integrations, and compliance requirements. A basic system may cost between $80,000 and $150,000. Mid-level systems range from $150,000 to $300,000, while enterprise-grade multi-agent platforms can exceed $300,000. Most of the cost comes from integration, orchestration, and compliance layers.

Q5. How long does deployment take?

A5. Deployment timelines vary based on system scope and integration complexity. A basic underwriting AI system can take 8 to 12 weeks. Mid-scale systems typically take 3 to 6 months. Enterprise-grade platforms with multiple integrations and compliance layers may take 6 to 9 months for full deployment.