Key Takeaways

-

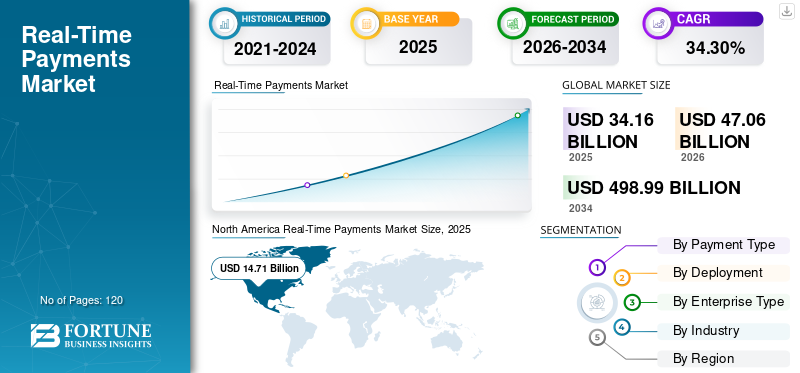

The real-time payments market is growing at a 34% CAGR toward $500 billion by 2034, making settlement infrastructure one of the highest-conviction technology investments a financial institution can make today

-

Choosing between RTGS, DNS, and Hybrid models is a strategic call that shapes liquidity management, credit exposure, and transaction throughput from the ground up

-

Production-grade systems require compliance-first design, ISO 20022 native messaging, intraday liquidity intelligence, and tight integration across core banking, payment rails, and treasury systems

-

Legacy replacement is not always required. A phased overlay strategy can unlock real-time capabilities without operational disruption if the middleware is engineered correctly

-

Build costs range from $50,000 to $150,000, depending on integration depth and compliance scope, with most institutions taking a phased MVP-to-scale approach to manage risk and investment simultaneously

Banks process several transactions every day, yet the systems handling that money were built decades ago. Payments still move in batches, settlements take days, and money sits in transit instead of working for anyone. That delay inevitably ties up capital, increases risk, and frustrates the businesses and customers your institution is trying to serve.

The market is already moving on. Central banks across the US, UK, Europe, and Asia-Pacific have rolled out or mandated faster payment systems, and global businesses are actively choosing banking partners based on how quickly and transparently money moves. At the same time, speed is becoming a baseline expectation and not a premium feature, and institutions that cannot meet it are losing ground to those that can.

Building a real-time settlement system is one of the most important infrastructure decisions a bank or fintech platform can make today, because getting the foundation right determines whether the system grows with you or creates compounding problems further down the line.

At Intellivon, we build enterprise-grade financial platforms with hands-on experience in settlement infrastructure, compliance workflows, and real-time data systems, and that depth shapes everything covered in this article. This blog breaks down every key layer of building such a system, giving founders and decision-makers a clear, practical starting point to move forward with confidence.

Why Are Banks Adopting Real-Time Settlement Systems Now?

Real-time payment volumes crossed 266 billion transactions in 2023 and are projected to surpass 575 billion by 2028. The market itself is moving from $47 billion in 2026 toward nearly $500 billion by 2034, growing at a 34% CAGR. These reflect a structural shift already playing out across banking systems globally.

Customer expectations are driving a significant portion of this growth. Businesses and consumers alike now expect funds to move and settle instantly, and banks that cannot deliver that experience are visibly losing relevance in their own markets.

Real-time settlement has moved from a competitive differentiator to an operational necessity. Banks that still rely on legacy batch processing are actively losing customers, revenue, and regulatory standing in a 24/7 economy where 78% of consumers now expect instant access to their funds.

1. Meeting Customer Expectations

Instant settlement is now the baseline. Research shows 93% of banks report higher retention among customers receiving real-time payouts for refunds, insurance claims, and gig economy disbursements.

When delays become routine, customers leave. In fact, 70% of users abandon providers after repeated slow transfers, making speed a direct driver of loyalty and lifetime value.

2. Countering Fintech Competition

Fintechs like Venmo and Wise already process 40% of US peer-to-peer payments instantly, pulling deposits away from traditional institutions. In response, 80% of banks now prioritize real-time payment rails to reclaim market share and unlock premium services like just-in-time treasury.

Without this capability, banks risk losing 15 to 20% of potential revenue from high-value B2B flows to faster, leaner competitors.

3. Reducing Settlement Risk

Batch processing creates real exposure. Intraday liquidity shortfalls and fraud windows widen every hour a transaction sits unresolved. RTGS systems eliminate this by delivering atomic finality, reducing settlement risk to near zero.

Additionally, 44% of SMEs identify real-time settlement as critical for cash flow stability, particularly in volatile market conditions.

Regulatory pressure is accelerating this transition further. This is because Europe’s 2025 instant payment mandate signals where global compliance standards are heading, and early movers will carry a structural advantage.

What Is Real-Time Settlement in Banking?

Real-time settlement is a digital process that moves money between banks instantly. Unlike batch systems that delay transfers, it processes each transaction individually as it occurs.

This ensures payments are final and irrevocable, giving businesses immediate access to funds and removing the uncertainty of waiting periods.

What “Settlement Finality” Means (and Why it’s Legally Significant)

Settlement finality is the point where a transfer of funds becomes irrevocable and unconditional under the law. In real-time systems, this usually occurs when the transaction is recorded in central bank money, meaning the payment cannot be reversed even if a participant later faces insolvency.

This legal certainty protects the entire financial network by preventing a chain reaction of failed obligations.

3 Key Characteristics: Atomicity, Irreversibility, Availability

High-performance settlement systems rely on three pillars to ensure financial integrity and trust for enterprise users.

1. Atomicity

Atomicity ensures a transaction is never partially completed. The system operates on an all-or-nothing logic where the entire transfer succeeds or fails together. This prevents data mismatches and ensures that funds are never debited from one account without being credited to another.

2. Irreversibility

Once a transaction reaches finality, it cannot be canceled or altered. This characteristic provides absolute certainty for merchants and banks. It eliminates the risk of chargebacks or payment disputes that often plague traditional credit networks.

3. Availability

Real-time systems must operate 24/7 without maintenance windows. Constant availability ensures that global trade and instant payments function across all time zones.

Building these features creates a robust foundation for any modern banking platform. These characteristics collectively minimize risk while maximizing the speed of capital.

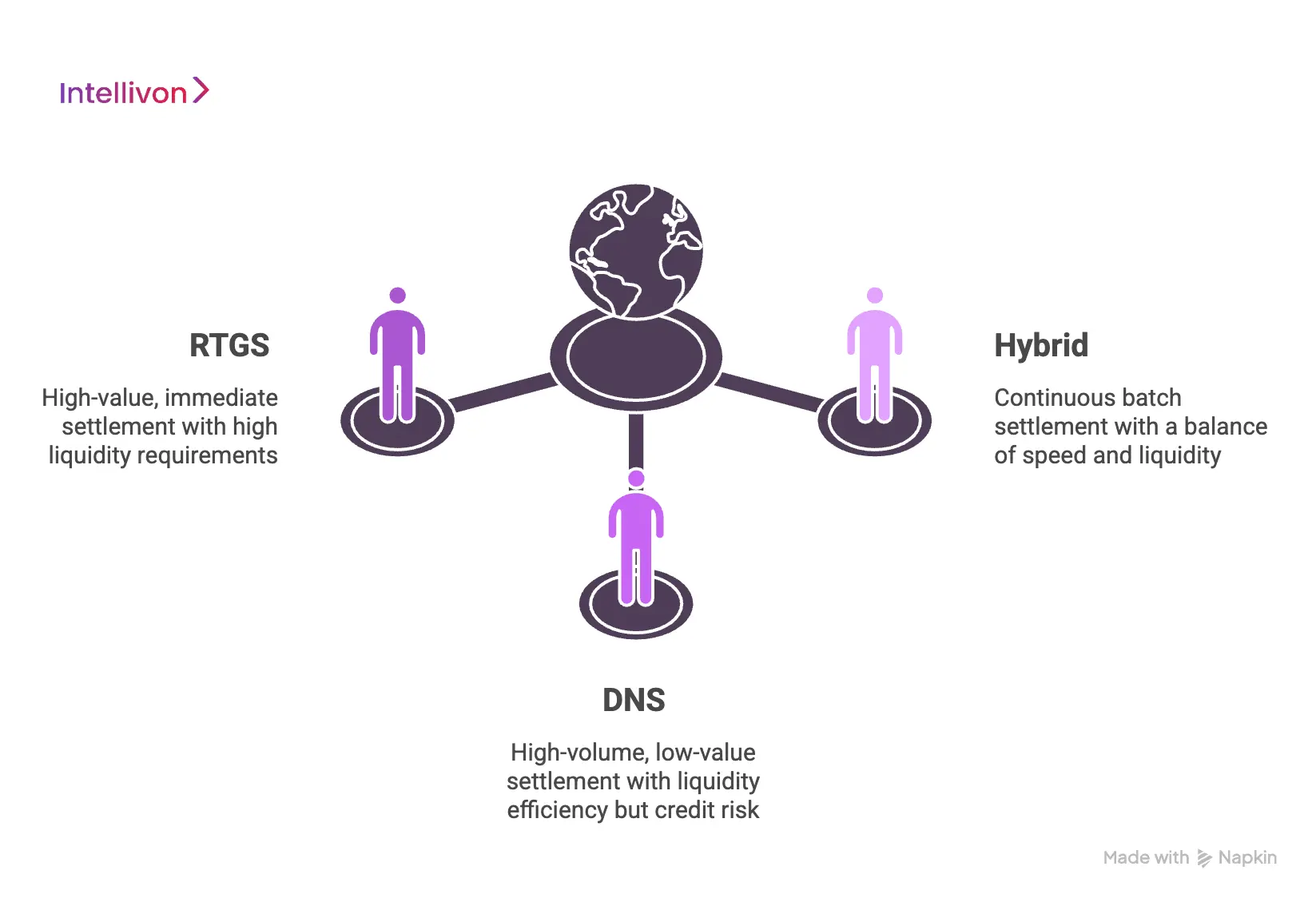

The 3 Payment Settlement Models Banks Use

Understanding how money moves at an enterprise level requires a clear grasp of the underlying settlement logic. Financial institutions choose their architecture based on a balance between speed, liquidity, and risk management.

Each model serves a distinct purpose within the global economic framework, ranging from high-value corporate transfers to everyday retail payments.

1. Real-Time Gross Settlement (RTGS)

RTGS is the gold standard for high-value transactions that require immediate finality. In this model, every payment is processed individually and settled across central bank books in real time.

Because there is no grouping of payments, the system requires the sending bank to have the full amount of liquidity available at the moment of execution. This eliminates the risk of a settlement gap, making it the preferred choice for large-scale interbank transfers.

2. Deferred Net Settlement (DNS)

DNS is a more liquidity-efficient model designed for high-volume, low-value retail transactions. Instead of settling each payment instantly, the system batches multiple transactions over a set period.

At the end of the cycle, only the net difference between what banks owe each other is moved. While this reduces the amount of cash a bank needs to keep on hand, it introduces a period of credit risk between the initiation and the final settlement.

3. Hybrid settlement models

Hybrid models attempt to capture the benefits of both RTGS and DNS. These systems use sophisticated algorithms to settle transactions in continuous batches throughout the day.

By offsetting payments against each other in short cycles, they provide faster finality than traditional DNS while requiring less immediate liquidity than a pure RTGS system. This flexibility makes them ideal for modern instant payment networks.

RTGS vs DNS vs Hybrid: Comparison Table

| Feature | RTGS | DNS | Hybrid |

| Settlement Timing | Immediate / Continuous | Periodic / Batched | Frequent / Continuous Batches |

| Finality | Instant | End of Cycle | Near-Instant |

| Liquidity Need | Very High | Low | Moderate |

| Risk Profile | Lowest (No Credit Risk) | Higher (Settlement Lag) | Low (Managed Risk) |

| Best Suited For | Low-Volume, High-Value | High-Volume Retail | Instant Retail & B2B |

| Example Systems | Fedwire, CHIPS | ACH, Local Clearing | Faster Payments, SEPA Inst |

Selecting the right model is a strategic decision that dictates how your platform manages liquidity and systemic risk. By aligning your architecture with these established frameworks, you ensure your system remains both capital-efficient and legally sound.

Where Settlement Fits in the Banking Architecture

Developing a financial platform requires a precise understanding of where the movement of value actually occurs. Many observers confuse the act of initiating a payment with the complex backend process that confirms and completes it.

By isolating the settlement layer, you can build a more resilient system that manages funds with the accuracy required by global regulators.

1. Payments vs clearing vs settlement

These three functions represent the administrative, technical, and financial phases of a transaction. While a payment is the intent and clearing is the reconciliation, settlement is the only stage where legal ownership of money actually changes hands.

| Phase | Purpose | Final Result |

| Payment | Initiation of intent | Instruction sent |

| Clearing | Validation and netting | Verified obligation |

| Settlement | Legal transfer of value | Debt discharged |

2. Where settlement sits in the end-to-end transaction lifecycle

Settlement acts as the final gatekeeper in the banking stack, occurring only after clearing confirms funds and security protocols. It is the destination point where the digital ledger records the permanent movement of capital.

| Stage | Process Type | Importance |

| Frontend | User Authorization | Capture of intent |

| Middleware | Clearing and Risk Check | Compliance and verification |

| Backend Core | Final Settlement | Irrevocable fund transfer |

3. How settlement systems interact with treasury and liquidity management

Real-time systems feed live data directly into treasury modules to provide an exact snapshot of available cash. This integration removes the need for large liquidity buffers and allows for more aggressive capital deployment.

| Factor | Legacy Interaction | Real-Time Interaction |

| Visibility | End-of-day reports | Instantaneous dashboard |

| Idle Cash | High buffers required | Minimal buffers needed |

| Decision Speed | Reactive/Delayed | Proactive/Immediate |

4. Domestic settlement vs cross-border settlement

Domestic settlement happens within a single sovereign network, while cross-border transfers require navigating multiple currencies and time zones.

International flows often introduce intermediary “correspondent” banks, which can increase costs and delay finality.

| Feature | Domestic | Cross-Border |

| Regulator | Single Central Bank | Multiple Jurisdictions |

| Currency | Unified (e.g., USD) | FX Conversion Required |

| Complexity | Low (Direct) | High (Intermediary Banks) |

Each architectural layer must be designed to handle specific volumes and risks to ensure the platform remains stable. A properly segmented stack allows your system to process high-frequency payments without compromising legal or financial finality.

How Real-Time Settlement Systems Work (Step-by-Step)

Building a system that moves value instantly requires a high-speed sequence of events. Each phase must execute with perfect precision to maintain the integrity of the financial network.

This process transforms a simple user request into a legally binding transfer of ownership in milliseconds.

Step 1: Transaction initiation and authentication

The journey begins when a sender submits a payment instruction through a digital interface. The system immediately verifies the identity of the user via multi-factor authentication protocols. It also checks digital signatures to ensure that the request remains untampered during transmission.

Step 2: Real-time validation, AML screening, and risk checks

Once authenticated, the system subjects the transaction to rigorous compliance filters. It scans the sender and receiver against global sanctions lists in real time to prevent financial crime. Automated risk engines evaluate the transaction behavior to detect potential fraud before the money moves.

Step 3: Liquidity verification and funding confirmation

The architecture then queries the ledger to ensure sufficient funds exist for the transfer. In an enterprise environment, this step also checks against intraday liquidity limits set by the treasury department. Therefore, the system only proceeds if the bank can cover the obligation without breaching regulatory capital requirements.

Step 4: Settlement instruction and ledger update

After passing all checks, the central settlement engine issues a command to update the accounts. This involves a simultaneous debit and credit to the respective ledgers to maintain an accounting balance. This step is the moment where the actual exchange of value occurs across the banking network.

Step 5: Finality confirmation and notification

The system generates a unique transaction reference once the ledger update succeeds. This notification serves as the legal proof of payment for both the sender and the receiving institution. At this point, the transaction is complete, and the funds are available for the recipient to use immediately.

How Exception Handling Works in Real Time

Real-time systems must manage errors without slowing down the entire network. When a transaction fails, the system issues specific R-messages or return codes to explain the rejection. These codes indicate whether the failure was due to insufficient funds or a technical timeout.

Therefore, the platform can automatically trigger retry logic or notify the user to take corrective action. This robust handling of exceptions ensures that the system remains reliable even during peak traffic periods.

This structured workflow provides the speed that modern markets demand while maintaining strict security. By automating each step, you can reduce the operational costs associated with manual intervention and human error.

Intraday Liquidity Management in Real-Time Settlement Systems

Managing capital in a live environment requires a shift from daily balancing to millisecond precision. Banks must ensure they have enough cash on hand to settle payments the moment they are initiated. This operational challenge is the most critical factor in maintaining a stable and functional real-time network.

1. What Intraday Liquidity Means in an RTGS Context

Intraday liquidity is the amount of money a bank can access during business hours to settle its obligations. In a real-time gross settlement system, payments happen one by one without waiting for incoming funds.

Therefore, a bank needs sufficient ready cash to cover outgoing transfers even before receiving payments from other participants.

2. Four Sources of Intraday Liquidity (BIS framework)

The Bank for International Settlements defines four primary ways banks maintain their cash levels during the day.

- First, they use their existing central bank reserves.

- Second, they rely on incoming transfers from other banks.

- Third, they can access credit lines from the central bank.

- Finally, they may borrow from other institutions in the interbank market to bridge any temporary gaps.

3. How Prefunded Settlement Models Work (TCH RTP model)

In a prefunded model, banks must deposit a specific amount of cash into a joint account before they can start transacting. This money acts as a locked buffer that the system uses to settle payments instantly.

Because the funds are already there, the system never has to wait for a bank to find liquidity during the transaction process.

4. How Central Bank Ledger Settlement Works (FedNow model)

This model settles payments directly on the books of the central bank rather than using a separate prefunded pool. It allows banks to use their master accounts to move money around the clock.

This approach provides a direct link to the highest level of financial authority, which simplifies the legal status of every transfer.

5. Prefunded vs Central Bank

Choosing between these models depends on how a bank prefers to manage its idle capital. Each has different implications for speed and regulatory oversight.

| Model | How Funded | Liquidity Risk | Finality Point | Example System |

| Prefunded | Separate joint account | Higher due to locked funds | Joint account update | TCH RTP |

| Central Bank | Direct master account | Lower via direct access | Central bank ledger | FedNow |

6. Intraday Liquidity Risk Tools

Financial institutions use automated monitoring tools to track their cash flows in real time. These systems alert treasury teams if balances drop below a certain threshold.

They also follow strict guidelines like the Fed Policy on Payment System Risk to ensure they do not exceed their allowed intraday credit limits.

Maintaining this balance is essential for the long-term health of any payment platform. By using the right tools and frameworks, you can build a system that remains liquid and reliable even during periods of high market volatility.

Core Components of a Real-Time Settlement System

Constructing an enterprise-grade settlement platform requires a modular architecture that prioritizes speed and extreme reliability. Each component must function as a high-performance link in a chain that handles billions in value without a single point of failure.

For investors, this technical stack represents the intellectual property and operational moat of the business.

1. Settlement Engine and Transaction Processor

The settlement engine is the brain of the platform, where the actual debit and credit logic resides. It must handle thousands of transactions per second while maintaining strict ACID compliance to ensure data integrity.

This processor coordinates with the ledger to update balances in real time and provides the definitive record of all fund movements.

2. Messaging and Orchestration Layer

This layer handles the communication between different banks and financial networks. Using an ISO 20022 native approach allows the system to carry rich data like invoice details and tax information directly within the payment message.

While a translation layer can bridge older systems, a native architecture is far more efficient for modern global interoperability.

3. Liquidity and Funding Management Module

This module tracks the available cash positions of every participant in the network. It prevents the system from processing payments that would result in a negative balance or a breach of credit limits.

Therefore, it acts as a financial safeguard that protects the platform from systemic liquidity risks.

4. Compliance and AML Screening Systems

Security must be embedded directly into the transaction flow rather than treated as an afterthought. These systems use machine learning to scan for suspicious patterns and check users against global watchlists in milliseconds.

By automating these checks, you ensure the platform meets strict regulatory standards without delaying the settlement process.

5. Monitoring, observability, and audit trail infrastructure

A transparent record of every system action is mandatory for regulatory audits and troubleshooting. Observability tools provide real-time dashboards that show system health and transaction latency.

This infrastructure ensures that every movement of money is fully traceable and that technical issues are identified before they impact users.

Investing in a robust core architecture ensures that your platform can adapt to changing market demands. By building with these components, you create a foundation that supports both domestic growth and international expansion.

ISO 20022: The Global Standard Powering Settlement Infrastructure

The shift toward instant payments is inseparable from the adoption of a unified global data language. ISO 20022 has emerged as the definitive standard for financial messaging, replacing fragmented legacy systems with a common framework.

Building a proprietary settlement system requires a shift from traditional monolithic architectures to event-driven, microservices-based designs. This ensures that the platform can scale horizontally as transaction volumes grow while maintaining the sub-second latency expected by modern enterprises.

1. The settlement engine and processor

The core engine manages the simultaneous debiting and crediting of accounts to ensure mathematical balance. It must be designed with high-concurrency locks to prevent double-spending while maintaining massive throughput.

This component is the primary source of truth for all fund movements within the network.

2. Messaging and orchestration layers

This layer manages the flow of information between participants using standardized protocols like ISO 20022. It ensures that payment instructions are correctly routed, validated, and acknowledged across different banking environments.

Therefore, it acts as the central nervous system that keeps all parts of the platform synchronized.

3. Liquidity and funding modules

Enterprises use this module to monitor and manage their available cash reserves in real time. It prevents settlement failures by checking available balances against outgoing obligations before a transaction is finalized.

This proactive management reduces the need for expensive overnight credit and optimizes capital efficiency.

4. Compliance and fraud detection

Automated screening systems scan every transaction for potential money laundering or fraudulent activity within milliseconds.

By integrating these checks directly into the settlement flow, you eliminate the delays typically associated with manual compliance reviews. This allows the platform to remain both fast and fully compliant with global regulations.

5. Monitoring and audit infrastructure

A robust audit trail provides a permanent, immutable record of every action taken within the system. Observability tools allow technical teams to track system health and identify bottlenecks before they affect the user experience.

For investors, this transparency is critical for meeting the stringent reporting requirements of financial regulators.

Each of these components must be built for resilience and high availability. Investing in a modern, modular stack ensures that your platform remains competitive as the global financial landscape continues to evolve toward instant, 24/7 operations.

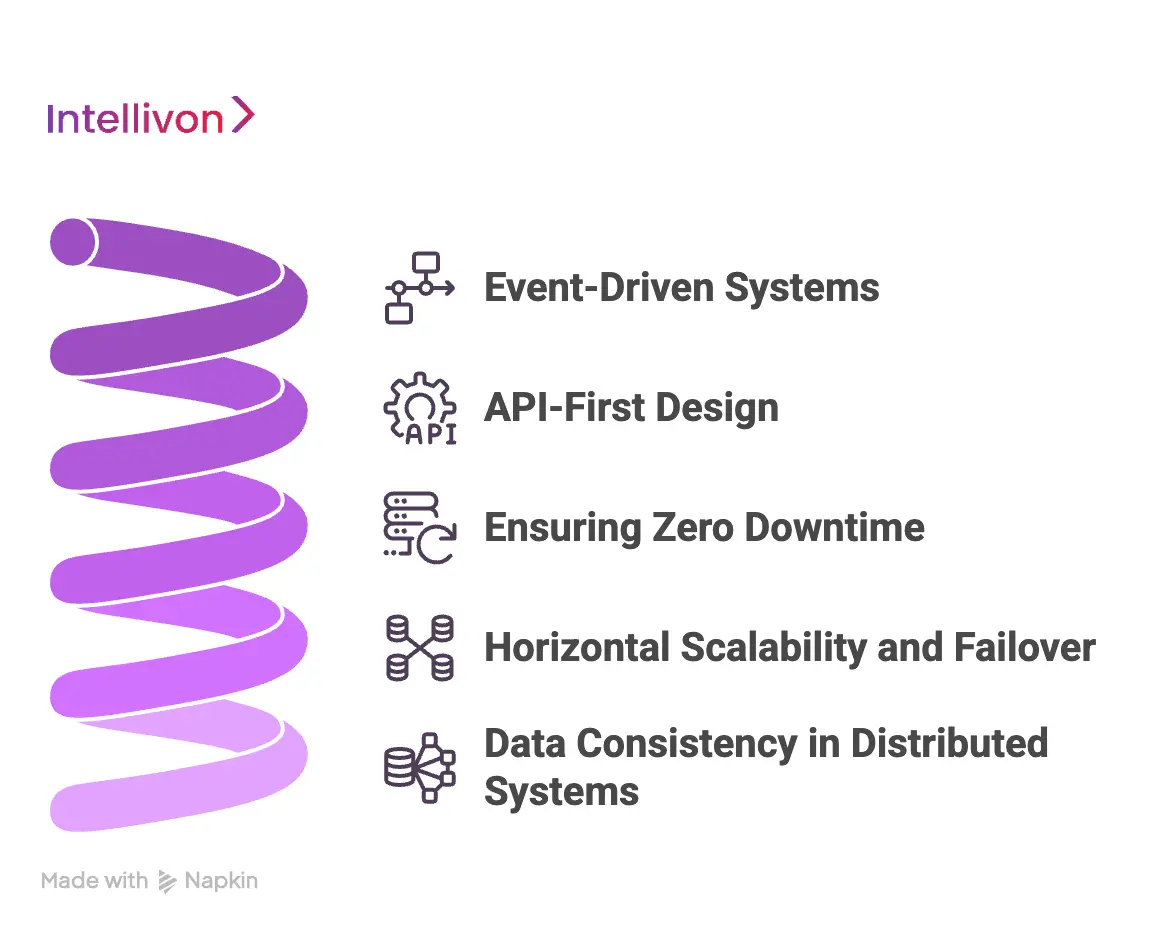

Architecture of Real-Time Settlement Systems

Designing a platform for the movement of capital requires a departure from legacy batch processing. The architecture must prioritize speed without sacrificing the absolute accuracy demanded by financial regulators.

This technical foundation determines how well the system handles peak volumes and critical failures during live operations.

1. Event-Driven Systems

An event-driven architecture allows the platform to react to payment instructions as individual triggers rather than grouped files. When a transaction enters the system, it initiates a series of parallel actions across the ledger and compliance modules.

Therefore, the system remains highly responsive because it processes each message in a continuous, flowing stream.

2. API-First Design

Using an API-first approach ensures that the settlement engine can integrate seamlessly with various banking cores and third-party fintech tools. This modularity allows for the rapid deployment of new features like instant notifications or automated treasury reporting.

By building on standardized endpoints, your platform becomes an extensible ecosystem rather than a closed silo.

3. Ensuring Zero Downtime

Financial markets operate 24/7, making planned maintenance windows a significant competitive disadvantage. Real-time systems utilize active-active configurations where multiple server clusters run simultaneously across different geographic zones.

This redundancy ensures that if one site fails, another takes over instantly without interrupting the flow of transactions.

4. Horizontal Scalability and Failover

As transaction volumes grow, the system must be able to scale by adding more computing power rather than replacing existing hardware. Horizontal scalability allows the platform to distribute the workload across many nodes to prevent bottlenecks.

Failover protocols ensure that even in a total hardware crash, the system state is preserved and recovered in milliseconds.

5. Data Consistency in Distributed Systems

Maintaining a single version of truth across multiple databases is the greatest challenge in distributed banking. Real-time platforms use consensus algorithms to ensure that every node in the network agrees on the account balances at any given time.

This prevents errors like double-spending and ensures that the ledger remains perfectly synchronized at all times.

| Architectural Pillar | Technical Strategy | Business Benefit |

| Responsiveness | Event-Driven Streams | Sub-second latency |

| Integration | RESTful/gRPC APIs | Faster partner onboarding |

| Reliability | Active-Active Clusters | Constant 24/7 availability |

| Growth | Elastic Node Scaling | Handles unlimited volume |

Building with these architectural principles ensures your platform remains resilient under the most demanding market conditions. A well-designed technical core serves as a long-term asset that reduces operational risk while supporting rapid business expansion.

Global Real-Time Settlement Systems Examples

The global financial landscape is undergoing a transformation as nations replace legacy infrastructure with instant networks. For investors, these models provide a blueprint for successful implementation.

Examining these systems reveals how different regulatory environments balance speed with systemic stability.

1. FedNow (United States)

Launched in 2023, FedNow enables banks to provide instant payment services. It settled over 8.4 million payments in 2025, showing explosive growth from its launch phase. Because it settles directly on the Federal Reserve ledger, it offers maximum security for its 1,600-plus participants.

2. TCH RTP Network (United States)

The RTP network from The Clearing House operates on a prefunded model where participants maintain a joint account. It reaches 71% of US demand deposit accounts and processed 107 million transactions in Q2 2025. This proves private sector networks can handle massive volumes and billions in daily value.

3. CHAPS (United Kingdom)

CHAPS is the high-value payment system for the UK, operated by the Bank of England. It utilizes an RTGS engine renewed in 2024 to enhance resilience. It remains the primary choice for time-sensitive, large-scale corporate and interbank transfers.

4. TIPS and SEPA Instant (European Union)

The European Central Bank operates TIPS to ensure instant payments across the Eurozone. With an October 2025 mandate deadline, adoption has surged to ensure sub-10-second settlement finality. This provides a unified framework for money to move across borders as easily as domestic transfers.

5. PIX (Brazil), PromptPay (Thailand)

PIX in Brazil has seen staggering adoption, becoming the primary payment method for millions. Similarly, PromptPay in Thailand has transformed the economy by linking mobile numbers to bank accounts for instant settlement.

6. SWIFT and Cross-Border Settlement

International transfers still largely rely on the SWIFT network and correspondent banking relationships. While slower than domestic RTGS, new initiatives like SWIFT gpi are bringing more transparency to this complex global infrastructure.

How these systems compare

| System | Country | Operator | Settlement Model | Latency | ISO 20022 |

| FedNow | USA | Federal Reserve | Central Bank Ledger | < 10 Seconds | Yes |

| TCH RTP | USA | The Clearing House | Prefunded Joint | < 10 Seconds | Yes |

| CHAPS | UK | Bank of England | RTGS | Real-Time | Yes |

| SEPA Inst | EU | Various/ECB | RTGS / Hybrid | < 10 Seconds | Yes |

| PIX | Brazil | Central Bank | RTGS | < 2 Seconds | Yes |

Observing these diverse models highlights that there is no single way to achieve settlement finality. However, the move toward structured data and instant processing is universal. Aligning your development strategy with these global leaders ensures your platform is built on proven, scalable principles.

Integrations Required for Real-Time Settlement Systems

Successfully deploying a settlement platform depends on its ability to communicate with a wide web of external and internal systems. For an entrepreneur, these integrations represent the primary technical scope and the most significant portion of the development timeline.

Each connection must be high-speed and secure to maintain the real-time promise of the architecture.

1. Core Banking System Integration

The core banking system is the master record for all customer accounts and balances. Integrating with it requires a real-time bridge that can handle immediate debits and credits without causing database locks.

Because many legacy cores were built for batch processing, this often requires a middleware layer to translate instant requests into a format the older system can accept.

2. Connecting to Domestic Payment Networks

Direct connectivity to national payment rails is essential for moving money outside of your own platform. Each network has its own gateway requirements and security protocols, such as dedicated hardware security modules or private cloud connections.

Therefore, your system must be flexible enough to manage multiple network protocols while maintaining a unified internal workflow.

3. AML, KYC, and sanctions screening platforms

Compliance checks must happen in the millisecond window between the payment request and the final settlement. Integrating with modern identity and screening platforms allows for automated, real-time verification against global watchlists.

This ensures that the system can block high-risk transactions instantly without slowing down legitimate users.

4. Treasury and Liquidity Management Systems

A settlement engine must feed live data into treasury modules so that the bank can manage its cash positions. This integration allows for automated funding of settlement accounts when balances run low.

By connecting these systems, you ensure that the platform remains liquid and operational without requiring manual intervention from a finance team.

5. Open Banking APIs

To be truly competitive, a settlement platform must work with the broader fintech ecosystem. Integrating with open banking APIs allows your system to initiate payments directly from external bank accounts or share real-time data with accounting software.

This connectivity turns a simple settlement tool into a versatile financial hub for businesses.

6. Monitoring and Regulatory Reporting Systems

Every transaction must be traceable and reported to financial authorities in a specific format. Integrating with automated reporting tools ensures that your platform remains compliant with regulations like the Bank Secrecy Act without manual effort.

At the same time, monitoring tools provide live alerts if an integration point fails, allowing for immediate technical response.

The quality of these integrations determines the overall reliability and speed of your platform. By building a well-connected ecosystem, you create a solution that is deeply embedded in the daily financial operations of your users.

Transitioning from Legacy to Real-Time Settlement Infrastructure

Moving from traditional batch systems to an instant environment is one of the most significant projects a financial institution will ever undertake.

The challenge lies in modernizing the core without disrupting existing services or violating regulatory mandates.

1. Overlay Approach vs Full Replacement

The overlay approach acts as a modern skin on top of existing legacy systems. It translates real-time instructions into formats the older core can understand, allowing for faster time-to-market.

Conversely, a full replacement involves tearing out the old infrastructure and building a cloud-native, real-time core from the ground up.

| Feature | Overlay Approach | Full Core Replacement |

| Speed to Market | Fast (6-12 months) | Slow (2-4 years) |

| Implementation Cost | Lower ($500K–$2M) | Higher ($5M–$20M+) |

| Technical Debt | High (Maintains legacy) | Low (Clean slate) |

| Operational Risk | Moderate | Very High |

2. Phased Migration Strategy

Most successful transitions follow a strict sequence to minimize system shock.

- Phase 1: Readiness Assessment. Evaluate existing data quality and API capabilities.

- Phase 2: Messaging Upgrade. Implement ISO 20022 messaging standards while still settling in batches.

- Phase 3: Pilot Connectivity. Connect a single, low-volume product line to a real-time rail like FedNow.

- Phase 4: Full Scale-Out. Gradually migrate all remaining payment types to the new infrastructure.

3. Running Hybrid Systems during Transformation

During the transition, banks must often run legacy and real-time systems in parallel. This hybrid state requires a sophisticated orchestration layer to ensure that accounts are not debited twice or missed entirely.

Therefore, data synchronization between the old and new ledgers must happen in sub-seconds to maintain a single, accurate view of customer balances.

4. Managing Regulatory and Compliance Continuity

Regulators do not grant exceptions for system upgrades. Compliance teams must ensure that AML and sanctions screening remain active and effective across both the legacy and new settlement paths.

Using a unified compliance engine that serves both environments is the most effective way to maintain a consistent audit trail and prevent regulatory gaps.

This transition is a marathon rather than a sprint. By selecting a strategy that matches your institutional risk appetite, you can modernize your infrastructure while keeping your daily operations stable and secure.

Step-by-Step: How to Build a Real-Time Settlement System

Building an enterprise-grade settlement platform is a high-stakes engineering feat that requires merging financial logic with massive technical scale. To succeed, you must move beyond simple code and design a system that manages liquidity, risk, and legal finality in a single heartbeat.

Following this structured roadmap ensures you build a foundation that is not just functional but market-ready and compliant.

Step 1 — Define Use Cases and Settlement Model

The first step involves identifying exactly who your platform serves. A system designed for high-frequency retail micro-payments requires a different architecture than one meant for billion-dollar interbank transfers.

Therefore, we begin by defining the transaction volume, average value, and the specific regulatory jurisdictions you will operate within. This clarity prevents over-engineering and ensures every technical decision aligns with your business goals.

Step 2 — Select Settlement Model (RTGS/DNS/Hybrid)

Once we understand your use case, we choose the financial logic that governs the movement of funds.

- RTGS is ideal for high-value transactions where immediate finality is non-negotiable.

- DNS works best for high-volume retail apps where saving on liquidity is a priority.

- Hybrid models offer a middle ground for modern fintechs. This decision dictates how much capital your participants must keep on hand and how we manage credit risk during the settlement window.

Step 3 — Select Technology Stack and Infrastructure

A real-time system is only as fast as its slowest component. We prioritize a cloud-native, event-driven architecture using languages like Go or Java for high-concurrency processing. For the database, we implement a distributed ledger or a high-performance SQL variant that guarantees ACID compliance.

This ensures that every debit has a corresponding credit and that data remains consistent even if a server fails.

Step 4 — Build Integrations

This is where the platform connects to the real world. We build secure, low-latency bridges to core banking systems and domestic rails like FedNow or SEPA Instant. Using an ISO 20022 native messaging layer at this stage is a strategic move.

It ensures that your platform speaks the global language of finance, making it significantly easier to onboard international bank partners later.

Step 5 — Performance Testing and Compliance Validation

Before a single dollar moves, the system must survive extreme stress. We run simulations that push the transaction volume to five times your expected peak to identify bottlenecks. Simultaneously, we validate the automated AML and fraud engines.

These systems must be able to flag suspicious activity in milliseconds without causing delays for legitimate users.

Step 6 — Phased Deployment and Production Rollout

We never launch a settlement system with a big bang approach. We start with a pilot or a single low-risk payment type to monitor the system in a live environment.

Gradually, we increase the volume and the complexity of the transactions. This phased approach allows us to fine-tune your exception handling and liquidity monitoring tools while the stakes are still manageable.

Following this path allows you to transform a complex vision into a reliable financial utility. When these steps are executed with precision, the resulting platform offers the speed, security, and scalability that modern enterprises demand.

Cost to Build a Real-Time Settlement System

Building a real-time settlement system is not a fixed-cost project. The total investment depends on how deeply the system integrates with core banking, payment rails, and compliance infrastructure.

For most banks and fintech platforms starting with a focused scope, the cost typically falls between $50,000 and $150,000.

Cost Breakdown by System Scope

| Build Scope | Timeline | Estimated Cost |

| Basic MVP (single flow, limited integrations) | 2–3 months | $50,000 – $75,000 |

| Mid-Level System (multi-flow, core integrations) | 3–5 months | $75,000 – $110,000 |

| Advanced System (multi-rail, real-time scaling) | 5–7 months | $110,000 – $150,000 |

Cost Breakdown by Core Modules

| Module | % of Total Cost | Notes |

| Settlement Engine & Processing | 20–25% | Core transaction orchestration and finality |

| Integrations (Core Banking, APIs) | 20–30% | Highly variable based on the systems involved |

| Liquidity Management Layer | 10–15% | Prefunding, balance checks, risk controls |

| Compliance & Fraud Systems | 10–15% | AML, monitoring, and audit requirements |

| Infrastructure & DevOps | 10–15% | Cloud setup, scaling, and failover systems |

| Monitoring & Reporting | 5–10% | Dashboards, logs, reconciliation tools |

Key Factors That Impact Cost

- Number of integrations with banking and payment systems

- Real-time performance requirements (latency, throughput)

- Compliance complexity across regions and regulations

- System scalability needs (transaction volumes, growth)

- Deployment model (cloud-native vs hybrid infrastructure)

Timeline vs Cost Trade-Off

Faster delivery often requires larger teams and parallel development, increasing cost.

On the other hand, phased builds reduce upfront investment but extend timelines.

Most banks choose a phased MVP → scale approach, balancing speed, cost, and risk.

If you’re evaluating the cost for your specific use case, the fastest way to get clarity is to map your system requirements to a real architecture.

Talk to Intellivon’s experts to get a tailored cost estimate and system blueprint for your real-time settlement platform.

Conclusion

Modern real-time settlement is the new baseline for global financial competitiveness. By eliminating transaction delays and settlement risk, you unlock superior capital efficiency and operational agility.

Investing in this infrastructure transforms your platform from a simple payment processor into a high-performance engine capable of powering the future of digital commerce.

Why Choose Intellivon To Build Real-Time Settlement Systems

Engineering a real-time settlement system equires designing a financial infrastructure that can process transactions instantly, manage liquidity continuously, and operate 24/7 without failure.

At Intellivon, we build settlement-grade infrastructure that connects payments, liquidity, compliance, and integrations into a single, high-performance system. Our approach focuses on turning real-time complexity into a scalable, reliable advantage for your organization.

A. Bridging Legacy Systems with Real-Time Settlement

Most banks operate on legacy cores that were never designed for instant settlement.

We build the integration layer that enables real-time capabilities without disrupting existing systems.

- Middleware connecting core banking, payment systems, and ledgers

- Real-time data synchronization across legacy and modern systems

- Gradual migration without operational downtime

This allows you to enable real-time settlement without replacing your entire infrastructure.

B. Building Always-On Real-Time Settlement Infrastructure

Real-time settlement requires continuous processing with zero tolerance for downtime.

We design systems that operate 24/7 across multiple transaction flows and payment rails.

- Real-time transaction orchestration and settlement engines

- High-availability architecture with failover and redundancy

- Event-driven systems for instant processing and updates

This ensures your system can handle peak volumes without latency or failure.

C. Embedding Liquidity Intelligence into Settlement Systems

Settlement systems are only as strong as their liquidity management. We build intelligence directly into the system to manage funds in real time.

- Prefunding and real-time balance validation mechanisms

- Liquidity forecasting and optimization models

- Automated exception handling for settlement failures

This reduces risk while ensuring continuous transaction flow.

D. Compliance-First Architecture for Real-Time Systems

Real-time systems must remain compliant even at high speed. We design systems where compliance is embedded into every transaction layer.

- Built-in AML, KYC, and transaction monitoring frameworks

- Real-time audit trails and regulatory reporting

- Configurable compliance rules across jurisdictions

This ensures your system remains compliant without slowing down operations.

E. Deep Integration Across Payment Ecosystems

Settlement systems must connect seamlessly across financial networks. We build integration-ready architectures that operate across the full ecosystem.

- Integration with payment rails (ACH, RTP, card networks, SWIFT)

- Connectivity with fintech tools and third-party APIs

- Integration with treasury, ERP, and accounting systems

This creates a unified financial infrastructure instead of fragmented systems.

F. Scalable Architecture for High-Volume Settlement

Real-time settlement systems must scale without performance degradation. We design architectures that support increasing transaction volumes and complexity.

- Microservices-based architecture for modular scaling

- Cloud-native infrastructure for elasticity and resilience

- Observability and monitoring for real-time system performance

This allows your system to grow without requiring re-engineering.

System Milestones and Business Impact

| System Milestone | Intellivon’s Engineering Focus | Business Outcome |

| Launch Phase | Core settlement engine and integrations | Faster go-to-market and early adoption |

| Growth Phase | Scaling transactions and integrations | Stable performance with rising volumes |

| Mature Phase | Liquidity optimization and automation | Lower costs and higher efficiency |

By partnering with Intellivon, you are creating a real-time financial infrastructure layer that supports instant transactions, continuous liquidity, and long-term scalability.

Ready to build a real-time settlement system that performs under real-world banking demands?

Talk to Intellivon’s experts and get a tailored architecture and cost estimate for your platform.

FAQs

Q1. What is real-time settlement in banking?

A1. Real-time settlement in banking is the process of completing a transaction instantly, where funds are transferred and made available to the recipient within seconds, with finality. Unlike batch settlement, there is no delay between transaction initiation and completion, which enables 24/7 payments and immediate fund availability.

Q2. How is it different from real-time payments?

A2. Real-time payments refer to the movement of money instantly, while real-time settlement refers to the final transfer of funds between banks. A payment can be initiated instantly, but true real-time systems ensure that settlement also happens immediately, eliminating delays, reconciliation gaps, and counterparty risk.

Q3. What integrations are required?

A3. Real-time settlement systems require integration with multiple banking and financial systems, including core banking platforms, payment networks (RTP, ACH, card rails), treasury and liquidity systems, and compliance tools like AML and KYC. APIs and middleware are typically used to ensure real-time data exchange across these systems.

Q4. How secure are settlement systems?

A4. Real-time settlement systems are highly secure when built with enterprise-grade architecture. They use encryption, secure APIs, identity access controls, and real-time fraud monitoring to protect transactions. Additionally, compliance frameworks and audit trails ensure that every transaction is traceable and meets regulatory standards.

Q5. How much does it cost to build one?

A5. The cost to build a real-time settlement system typically ranges between $50,000 and $150,000, depending on complexity, integrations, and scalability requirements. Systems with multiple payment rails, advanced compliance features, and high transaction volumes tend to fall on the higher end of this range.