Key Takeaways

-

Cross-border B2B volumes are heading toward $62.9 trillion by 2030, making multi-rail infrastructure a strategic necessity, not a technical upgrade

-

Single-rail dependency is an operational liability. Multi-rail orchestration cuts payment costs by 20 to 30% and compresses settlement from days to minutes

-

Choosing between ACH, RTP, SWIFT, cards, and stablecoins is a business decision first, as each rail carries different costs, speed, and compliance implications that compound at volume

-

Production-grade systems require five layers working in sync: smart routing, a canonical ledger, compliance architecture, liquidity management, and a resilient API integration layer

-

Compliance must be embedded into every transaction flow, not bolted on. KYC, AML, ISO 20022, and audit trails need to run natively across every rail and jurisdiction

-

The embedded payments market sits at $6.7 billion, growing at 16% CAGR, meaning multi-rail infrastructure doubles as a direct revenue opportunity for platforms that build it right

When a single payment failure costs your enterprise a client relationship, the question stops being “which payment gateway should we use?” and starts becoming “why are we still dependent on a single payment rail?”

Enterprises moving serious transaction volume have outgrown the single-processor model. This is because the cracks show up in cross-border settlement lags, card network downtime during peak periods, and the operational friction of reconciling payments across regions with different regulatory frameworks.

The shift happening now is structural, where payment orchestration has moved from a technical consideration to a board-level conversation, driven by the reality that routing flexibility, redundancy, and compliance agility directly affect revenue and margins.

Intellivon has spent years building enterprise-grade payment infrastructure for organizations operating at this scale, translating complex multi-rail architecture into systems that actually perform under real-world conditions. This blog breaks down how we build such platforms from the ground up.

Why Enterprises Are Moving to Multi-Rail Payments

Enterprises are shifting toward multi-rail payment strategies for reasons that go beyond convenience. Single-rail setups create real operational risk, whether through network downtime, settlement timing mismatches, or fees that quietly compound at scale.

By routing across ACH, RTP, SEPA, and SWIFT based on transaction requirements, enterprises gain control over speed, cost, and reliability simultaneously.

The scale of this shift is significant. Cross-border B2B payment volumes are projected to reach $58.9 trillion in 2026. Around 45% of community banks have already adopted multi-rail approaches. For enterprise finance and operations teams, this is an active infrastructure decision, not a future one.

1. Overcoming Single-Rail Limitations

Single-rail dependency creates a single point of failure. When one network experiences downtime or a cut-off mismatch, transactions stall.

Multi-rail systems auto-route to backup rails, keeping uptime above 99% for critical payables and receivables. Enterprises gain genuine redundancy across cards, wires, and instant payment systems without manual intervention.

2. Optimizing Cost and Speed

Payment rails differ significantly in fees and settlement timelines. Multi-rail orchestration routes low-value payments through ACH, where fees stay under 1%, and pushes time-sensitive transactions through RTP.

This approach typically reduces overall payment costs by 20 to 30% while compressing settlement from days to minutes. For global operations, it also balances SWIFT’s security for high-value transfers with local faster payment system speed.

3. Enhancing Global Reach and Flexibility

Enterprises can serve vendors across regions through a single integration. A vendor pays by card, while the enterprise settles to a bank account. No per-rail technical setup required. At the same time, the U.S. real-time payment transactions are projected to reach 8.9 billion by 2026, reflecting 61% growth.

Cross-border volumes are expected to hit $62.9 trillion by 2030, making scalable multi-rail infrastructure a strategic necessity.

4. Boosting Revenue and Retention

Higher payment completion rates directly reduce churn. When vendors and partners receive payments through their preferred method, the relationship holds stronger. Beyond retention, B2B platforms built on multi-rail infrastructure can monetize through markup, float management, and premium routing options.

The embedded payments market for enterprise platforms is valued at $6.7 billion and growing at a 16% CAGR, representing a tangible revenue opportunity for platforms that build this capability.

Multi-rail payment infrastructure is a revenue and resilience decision. Enterprises that build this capability now will operate with a structural advantage that their single-rail competitors simply cannot match.

What Is Multi-Rail Payment Infrastructure?

Multi-rail payment infrastructure is a unified system connecting enterprises to various transfer networks like ACH, wire, and digital assets. It acts as a central hub that automatically directs transactions through the best possible channel.

This setup optimizes every payment for speed and cost while ensuring constant financial connectivity and reliability.

How It Differs From Traditional Payment Gateways

Traditional payment gateways typically serve as a simple bridge between a merchant and a specific acquiring bank. These legacy systems usually focus on credit card processing and operate within a rigid, single-channel environment.

In contrast, a multi-rail payment system functions as a high-level orchestration engine that oversees multiple financial networks simultaneously. While a gateway is a point solution, multi-rail infrastructure is a comprehensive strategic framework.

| Feature | Traditional Payment Gateway | Multi-Rail Payment Infrastructure |

| Connectivity | Single network or bank | Multiple rails (ACH, Card, RTP, Web3) |

| Routing | Static and linear | Dynamic and rule-based |

| Settlement | Fixed timelines (T+2 or T+3) | Real-time or optimized per rail |

| Scalability | Limited to gateway capabilities | Agnostic to network expansion |

| Data Flow | Siloed per transaction | Unified across all channels |

Strategic leaders recognize that relying on a traditional gateway creates a single point of failure and limits cost-saving opportunities. A multi-rail approach allows an organization to bypass the limitations of a single provider by switching between networks in real time.

This agility ensures that high-value enterprise transactions are never stalled by a specific bank’s technical constraints. Consequently, the business gains the power to dictate terms to the market rather than being restricted by a single vendor’s infrastructure.

The Rail Accumulation Principle

The rail accumulation principle focuses on expanding financial reach by layering multiple payment networks. This modular approach ensures redundancy and efficiency.

- Network Diversity: Integrating diverse rails prevents reliance on a single provider.

- Redundancy: Secondary paths activate immediately if a primary network fails.

- Optimization: Each added rail provides new opportunities for lower fees.

The Role of Orchestration Layers in Routing

The orchestration layer acts as the primary intelligence center within a multi-rail payment system. It functions by evaluating every transaction against real-time variables such as network traffic, geographical regulations, and processing fees.

Instead of following a hardcoded path, the system uses logical workflows to determine the most efficient route for every dollar.

- Smart Routing: Systems evaluate speed and cost to select the optimal network path.

- Failover Logic: Transactions shift to secondary rails immediately if a primary connection fails.

- Data Normalization: Fragmented bank messages transform into a single, clean reporting format.

This automation removes the need for manual treasury decisions and significantly reduces human error during high-volume periods. Consequently, the orchestration layer ensures that payments remain resilient against localized bank outages or regional network spikes.

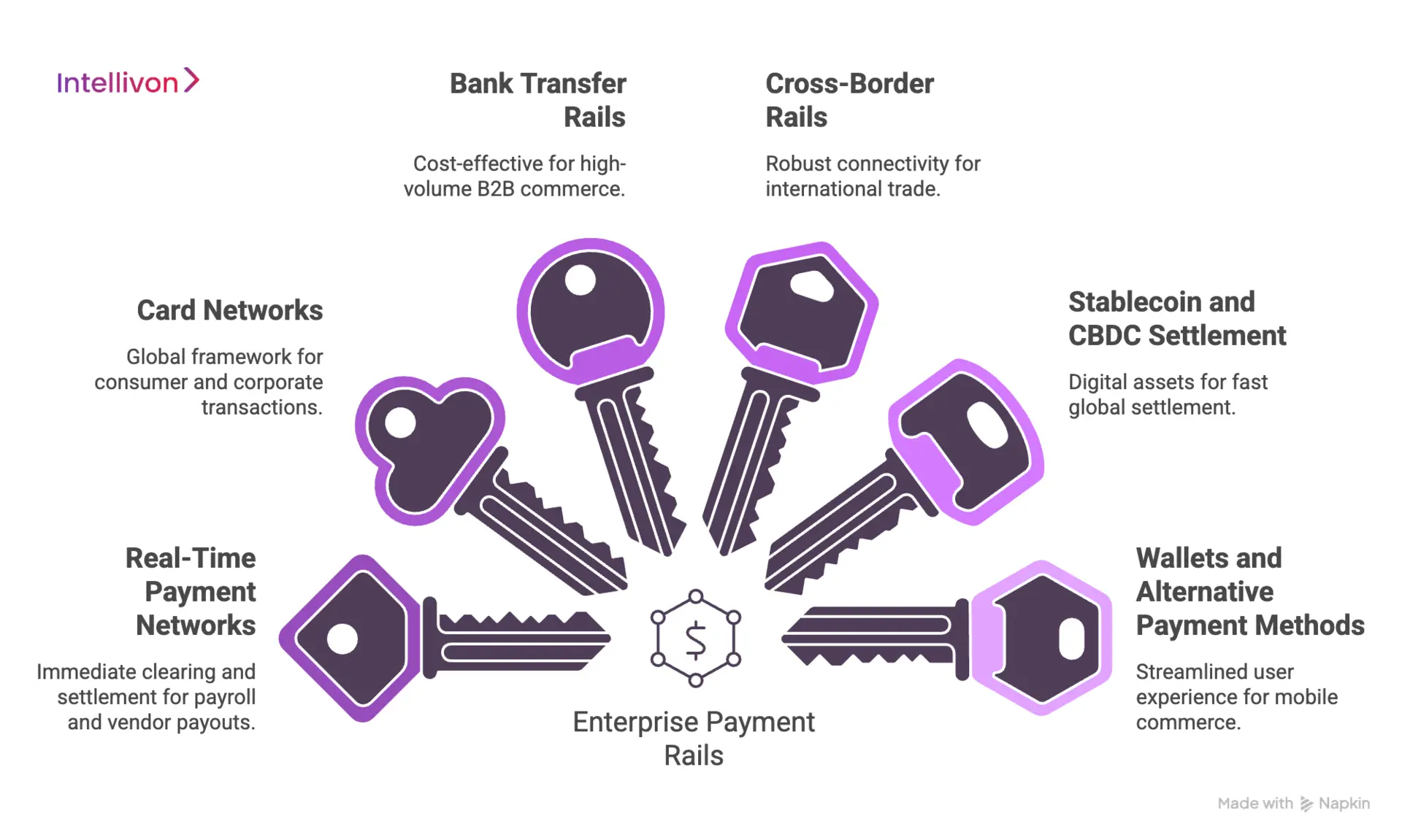

What Payment Rails Enterprises Must Support

A diverse rail strategy ensures an enterprise remains agile and competitive in a shifting global economy. Supporting these various networks allows businesses to meet specific regional demands while maintaining maximum operational flexibility.

1. Real-Time Payment Networks

Real-time networks represent the modern standard for liquidity management. These systems offer immediate clearing and settlement, which is critical for payroll and instant vendor payouts.

By removing the traditional waiting period, businesses maintain better control over daily cash flows.

- Instant Liquidity: Funds move in seconds rather than days.

- 24/7 Availability: Networks operate continuously without bank holiday interruptions.

- Irreversibility: Immediate settlement finality reduces the risk of payment reversals.

2. Card Networks (Visa, Mastercard, Amex)

Card rails remain the primary choice for consumer-facing transactions and corporate procurement.

They provide a standardized global framework for credit and debit processing. While fees are higher, the extensive reach and fraud protection offer significant security for enterprise users.

- Global Acceptance: Card networks work across nearly every international market.

- Chargeback Protection: Built-in dispute mechanisms provide a safety net for buyers.

- Tokenization: Advanced security protocols replace sensitive data with secure identifiers.

3. Bank Transfer Rails (ACH, SEPA, NEFT, RTGS)

Traditional bank transfers are the backbone of high-volume and high-value B2B commerce. These rails are cost-effective for recurring payments like subscriptions or bulk supplier invoices.

Although slower than real-time options, they offer the highest level of regulatory familiarity and stability.

- Cost Efficiency: Transaction fees are significantly lower than card-based networks.

- Bulk Processing: Ideal for managing thousands of simultaneous payouts.

- Regional Standards: SEPA and ACH provide predictable frameworks for local markets.

4. Cross-Border Rails (SWIFT, FX APIs)

International trade requires robust connectivity between disparate banking jurisdictions. SWIFT remains the legacy standard for global messaging, while modern FX APIs allow for real-time currency conversion.

Combining these ensures that cross-border friction does not stall international expansion.

- Interoperability: Connects thousands of financial institutions worldwide.

- Transparency: Modern tracking allows for real-time visibility of international funds.

- Compliance: Integrated checks ensure all transfers meet global anti-money laundering standards.

5. Stablecoin and CBDC Settlement Architecture

Digital assets are transforming the speed of global settlement by utilizing blockchain technology. Stablecoins pegged to fiat currency allow for near-instant movement of value across borders without traditional banking intermediaries. This architecture is increasingly vital for 24/7 global treasury operations.

- Programmability: Smart contracts can automate payments based on specific conditions.

- Atomic Settlement: Delivery and payment happen simultaneously, reducing counterparty risk.

- Low Friction: Bypasses the complex web of correspondent banking for faster delivery.

6. Wallets and Alternative Payment Methods

Digital wallets like Apple Pay, Google Pay, and regional apps have become essential for modern commerce. These methods often sit on top of existing rails but provide a more streamlined user experience.

Supporting these alternatives is mandatory for enterprises looking to capture diverse global markets.

- User Experience: Simplified checkout processes increase conversion rates significantly.

- Mobile-First: Designed specifically for the growing segment of mobile-only users.

- Regional Dominance: Certain markets prefer local wallets over traditional card networks.

| Rail | Speed | Cost | Settlement Finality | Best For |

| Real-Time | Seconds | Low | Immediate | Payroll, Instant Payouts |

| Card | Seconds (Auth) | High | Delayed | B2C Sales, Procurement |

| ACH/SEPA | 1-3 Days | Very Low | High | Bulk Invoicing, Subscriptions |

| SWIFT | 1-5 Days | Medium | High | International B2B |

| Stablecoin | Minutes | Low | Immediate | Cross-Border Liquidity |

Selecting the right mix of rails transforms a standard payment department into a strategic asset. By aligning the specific strengths of each network with unique business goals, organizations can ensure every transaction drives growth and reduces friction.

Core Architecture of Multi-Rail Payment Systems

Building a resilient financial core requires more than simple connectivity. It demands a sophisticated architectural stack that can handle high-volume data flows while remaining flexible enough to adopt new protocols.

A well-designed system ensures that every transaction is a data-driven event rather than a manual process.

1. Payment Orchestration Engine Design

The orchestration engine serves as the brain of the entire infrastructure. It abstracts the complexity of multiple banking relationships into a single manageable layer. This design allows developers to write code once while accessing dozens of different payment pathways.

- Abstraction Layer: Engineers interact with a unified API instead of managing separate bank integrations.

- Workflow Automation: Custom logic triggers specific actions based on transaction status or external triggers.

- Resilience: The engine handles retries and status updates across different rails automatically.

2. Smart Routing and Decision Engines

Smart routing transforms static payment instructions into dynamic strategic decisions. By analyzing real-time data, the engine selects the most efficient path for every individual transaction.

This process considers variables like current liquidity, network health, and processing fees to protect the margin of every transfer.

- Cost Optimization: The system prioritizes the least expensive rail that meets the deadline.

- Speed Management: Urgent payments are routed through real-time networks like RTP or FedNow.

- Dynamic Failover: If a specific bank portal goes down, the engine instantly reroutes the traffic to a secondary provider.

3. Unified Canonical Ledger and Settlement Layer

Maintaining a single source of truth is the greatest challenge in a multi-rail environment. A unified canonical ledger standardizes data from diverse sources into a consistent format. This ensures that the finance team sees one clear picture of the global cash position at any given moment.

- Data Normalization: Variations in bank messaging are converted into a standardized internal record.

- Real-Time Visibility: Stakeholders gain instant access to cleared funds across all accounts.

- Automated Reconciliation: The system matches outgoing payments with bank statements without manual intervention.

3. API Gateway and Integration Layer

The gateway acts as the secure entry point for all internal and external communication. It ensures that sensitive financial data is protected while allowing seamless connectivity with ERP systems and third-party fintech tools.

A robust integration layer reduces the time required to onboard new financial partners.

- Security Protocols: High-level encryption and tokenization protect data in transit.

- Developer Experience: Clear documentation and sandbox environments accelerate the deployment of new features.

- Legacy Compatibility: Modern APIs can communicate with older banking systems through translation layers.

4. Event-Driven and Microservices Architecture

Modern payment systems must be highly scalable and fault-tolerant. An event-driven architecture allows the system to process thousands of transactions per second by treating each step as a discrete event.

Microservices ensure that a failure in one component does not bring down the entire payment network.

- Scalability: Each service can be scaled independently based on current transaction volume.

- Asynchronous Processing: Tasks like fraud checking and notification happen in parallel to the main payment flow.

- System Isolation: Decoupled services make it easier to update individual parts of the stack without downtime.

5. ISO 20022 and What It Changes for Your Stack

ISO 20022 is the new global standard for financial messaging that brings unprecedented depth to payment data. It replaces older, limited formats with rich XML-based messages.

For an enterprise, this means every transaction can now carry detailed remittance information and compliance data.

- Rich Data: Payments include structured information about invoices, tax, and counterparty details.

- Global Interoperability: A standardized language simplifies cross-border communication between different banks.

- Improved Compliance: Enhanced data clarity reduces the number of payments flagged for manual review.

A robust architecture provides the foundation for sustainable growth and operational security. By investing in these core components, an enterprise creates a future-proof system capable of navigating any financial landscape.

How Payment Routing Decisions Are Made

Strategic payment routing is the process of selecting the most appropriate financial path for a transaction based on a set of predefined business rules. Instead of sending every payment through a single bank, the system evaluates the specific requirements of each transfer in real-time.

This granular control ensures that every dollar moved contributes to the overall efficiency of the organization.

1. Cost-Based Routing Logic

Cost-based routing prioritizes the preservation of margins by selecting the least expensive network available for a given transaction. The engine compares interchange fees, processing costs, and bank surcharges across all integrated rails.

This logic is particularly effective for high-volume, low-urgency payments where every cent saved scales into significant annual reductions in overhead.

- Fee Comparison: The system calculates the total cost of ownership for each rail before execution.

- Volume Incentives: Routing logic can prioritize specific banks to meet monthly volume tiers for better pricing.

- Currency Optimization: For international transfers, the engine selects the rail with the most favorable exchange rates.

2. Speed and SLA-Based Routing

When time is the critical factor, the routing engine prioritizes networks that offer the fastest settlement finality. This is essential for maintaining Service Level Agreements with vendors or providing instant gratification to consumers.

The system identifies which rails are currently operating at peak speed and directs urgent traffic accordingly.

- Network Latency Checks: Real-time monitoring ensures the selected rail is not experiencing delays.

- Urgency Tagging: Business units can tag specific payments as high-priority to trigger faster routing.

- Settlement Mapping: The engine matches the payment deadline with the historical performance of available networks.

3. Risk and Compliance-Based Routing

Enterprise payments must navigate a complex landscape of regulatory requirements and security threats. Compliance-based routing directs transactions through paths that offer the necessary level of scrutiny or data protection required for a specific region.

This ensures that high-risk transfers undergo additional verification without slowing down standard operational flows.

- Regional Compliance: Transactions are routed through banks that satisfy local KYC and AML regulations.

- Fraud Scoring: Payments with high-risk profiles are directed to rails with advanced biometric or multi-factor authentication.

- Sanction Screening: Integrated checks ensure that no payment violates international trade restrictions before it leaves the internal system.

4. Failover and Redundancy Routing

Operational resilience is non-negotiable for enterprise-grade financial systems. Failover routing acts as a digital insurance policy, ensuring that payment flows remain uninterrupted even if a primary bank partner experiences a technical outage.

The system detects connectivity issues in milliseconds and shifts the traffic to a secondary, pre-configured rail.

- Health Monitoring: Constant pings to bank APIs detect downtime before a transaction is even attempted.

- Automatic Switching: The engine transitions to backup rails without requiring manual intervention from the IT team.

- Load Balancing: Traffic can be distributed across multiple banks to prevent any single system from becoming a bottleneck.

5. AI-Driven Dynamic Routing Optimization

Advanced payment systems leverage machine learning to predict the best routing paths based on historical data and emerging trends.

These AI models analyze millions of previous transactions to identify patterns that human operators might miss, such as a specific bank’s tendency to delay settlements on Friday afternoons.

- Predictive Analytics: The system forecasts potential network failures or fee hikes before they occur.

- Anomaly Detection: AI identifies unusual payment patterns that could indicate a sophisticated security breach.

- Continuous Learning: The routing engine becomes more efficient over time as it ingests more performance data.

What Is the Difference Between Static and Dynamic Payment Routing?

The shift from static to dynamic routing represents the evolution from manual banking to automated treasury management. While static routing relies on fixed paths, dynamic routing adapts to the environment in real-time.

| Feature | Static Routing | Dynamic Routing |

| Decision Base | Pre-set, fixed rules | Real-time data and conditions |

| Flexibility | Rigid; requires manual updates | Fluid; adjusts automatically |

| Outage Response | The system stops until fixed | Immediate shift to healthy rails |

| Cost Control | Fixed per vendor | Optimized per transaction |

| Performance | Inconsistent | Optimized for speed and success |

Managing these decisions effectively allows an enterprise to treat its payment infrastructure as a competitive advantage.

By automating the selection process, leadership ensures that financial operations are always aligned with the broader strategic goals of the company.

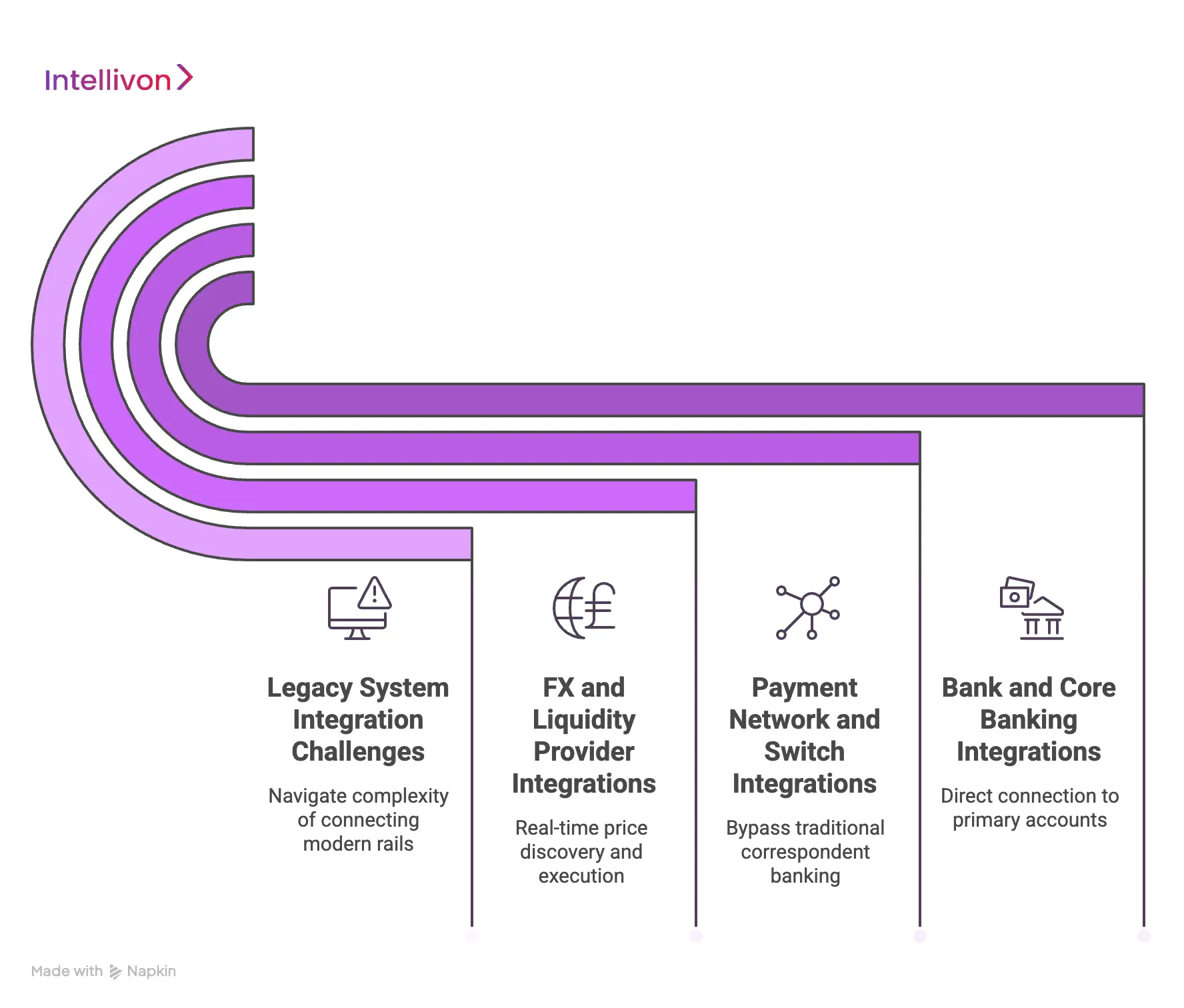

Integration Strategy for Multi-Rail Payment Systems

Successfully deploying a multi-rail architecture requires a disciplined approach to technical connectivity. An enterprise must bridge the gap between modern agile software and the often rigid infrastructures of global financial institutions.

A well-executed integration strategy ensures that data flows seamlessly across the entire stack without creating new silos or security vulnerabilities.

1. Bank and Core Banking Integrations

Directly connecting to core banking systems is the first step in establishing a robust payment foundation. These integrations allow an enterprise to initiate transfers and retrieve real-time balance information directly from its primary accounts.

While complex, these deep connections provide the highest level of control over liquidity and settlement timing.

- Host-to-Host Connectivity: Secure file transfer protocols allow for high-volume batch processing directly with a bank’s server.

- Real-Time API Hooks: Modern banking APIs provide instant notifications for incoming and outgoing transaction status.

- Balance Synchronization: Automated polling ensures that the internal ledger matches the bank’s records at all times.

2. Payment Network and Switch Integrations

To move beyond a single bank, an organization must integrate with broader payment switches and regional networks. These connections provide the “rails” that move money between different financial entities.

By integrating with these switches, an enterprise gains the ability to bypass traditional correspondent banking delays for faster local settlements.

- Direct Network Access: Connecting to regional switches like SEPA or Faster Payments reduces intermediary fees.

- Switch Messaging Standards: Standardizing communication protocols ensures that the system can speak to diverse international networks.

- Traffic Balancing: Integrating multiple switches allows the system to distribute transaction loads to prevent bottlenecks.

3. FX and Liquidity Provider Integrations

International operations demand seamless currency conversion and liquidity management. Integrating with specialized Foreign Exchange (FX) providers and liquidity pools allows for real-time price discovery and execution.

This prevents the business from being locked into the often unfavorable rates offered by a single commercial bank.

- Automated FX Execution: The system triggers currency trades automatically based on the needs of the payment rail.

- Multi-Currency Wallets: Virtual accounts allow the enterprise to hold and manage dozens of currencies without local bank branches.

- Rate Aggregation: The integration layer compares rates from multiple providers to ensure the best possible conversion price.

4. Legacy System Integration Challenges

Most established enterprises must navigate the complexity of connecting modern payment rails to aging ERP and accounting software. These legacy systems often lack the flexibility to handle real-time data or the rich messaging formats required by ISO 20022.

Addressing these friction points is essential to preventing manual workarounds that slow down the entire operation.

- Data Mapping Friction: Translating modern XML messages into legacy flat-file formats can result in data loss.

- Batch Processing Constraints: Older systems often cannot handle the continuous, 24/7 nature of real-time payment rails.

- Security Gaps: Bridging modern encrypted APIs with older mainframe systems requires sophisticated middleware to maintain security.

5. API vs Middleware vs Direct Integrations

Choosing the right integration method depends on the required speed, security, and technical resources available within the organization.

| Method | Speed to Deploy | Performance | Maintenance | Best For |

| API Integration | High | High | Moderate | Modern Fintech and SaaS tools |

| Middleware | Moderate | Moderate | High | Bridging legacy ERPs with new rails |

| Direct (H2H) | Low | Very High | Low | High-volume corporate banking |

Establishing these connections effectively allows a business to scale its financial operations across borders without a proportional increase in headcount. Therefore, the integration layer is not just a technical necessity but a critical driver of operational efficiency.

Compliance and Regulatory Architecture Of Multi-Rail Payment Systems

Operating a global payment infrastructure requires navigating a complex web of international laws and financial standards. A multi-rail system must not only move money efficiently but also serve as a robust compliance shield for the organization.

By embedding regulatory logic directly into the technical stack, enterprises can automate risk management and ensure every transaction remains within legal boundaries.

1. KYC, AML, and Transaction Monitoring

Modern financial systems must verify the identity of every participant and monitor for suspicious activities in real time. In a multi-rail environment, this process becomes more complex as different networks have varying levels of scrutiny.

Integrated monitoring tools analyze transaction patterns across all rails to detect anomalies that might indicate money laundering or fraud.

- Identity Verification: The system performs automated Know Your Customer(KYC) checks before allowing a participant to join the network.

- Velocity Tracking: Real-time monitoring flags accounts that show unusual spikes in transaction frequency or volume.

- Pattern Recognition: Advanced algorithms identify known laundering techniques across disparate banking jurisdictions.

2. Data Localization and Cross-Border Rules

Many countries now require that sensitive financial data remain within their physical borders, a concept known as data residency.

For a multi-rail system, this means the architecture must be capable of routing data and transactions while adhering to specific regional storage laws. Failure to comply can result in massive fines and the loss of operating licenses in key markets.

- Geographic Sharding: The system stores user data in local servers based on their country of origin.

- Privacy Filters: Sensitive information is redacted or encrypted before being transmitted across international lines.

- Regulatory Mapping: The routing engine automatically identifies which rails comply with the specific data laws of a destination country.

3. PCI-DSS, GDPR, PSD2, and Financial Compliance

Enterprises must adhere to a strict set of global security and privacy standards to protect cardholder data and consumer rights. A multi-rail stack integrates these requirements through tokenization and secure communication protocols.

This ensures that even as the business scales across different payment methods, the underlying security posture remains unbreakable.

- Tokenization Services: Sensitive card information is replaced with secure tokens to minimize the risk of data breaches.

- Consent Management: The infrastructure manages user permissions in accordance with GDPR and PSD2 requirements for open banking.

- Secure Enclaves: Critical processing tasks occur within isolated environments to prevent unauthorized access.

4. ISO 20022 Compliance Requirements

The transition to ISO 20022 is a regulatory mandate for many global banking networks rather than a technical choice. This standard requires that every payment message contain detailed, structured data about the sender, receiver, and purpose of the funds.

Adapting to this standard is essential for ensuring that international payments are not rejected by recipient banks.

- Structured Remittance: Every transaction carries detailed invoice data to satisfy bank reporting requirements.

- Extended Character Sets: The standard allows for more detailed information than previous legacy formats.

- Universal Translation: The system converts non-compliant messages into the ISO standard before they hit the global rail.

5. Audit Trails and Explainable Transactions

Transparency is the foundation of institutional trust and regulatory approval. Every decision made by a multi-rail system, especially those driven by AI routing, must be recorded in an immutable audit trail.

This allows compliance officers and external auditors to trace the lifecycle of any transaction and understand exactly why a specific path was chosen.

- Immutable Logs: The system records every transaction event in a tamper-proof database for future review.

- Routing Rationale: The engine logs the specific business rules or data points that triggered a routing decision.

- Reporting Automation: Compliance teams can generate detailed regulatory reports with a single click based on live system data.

Strategic compliance management transforms a potential liability into a significant business advantage. By ensuring that every payment is secure, transparent, and legal, an enterprise builds the reputation necessary to expand into new territories and financial sectors with total confidence.

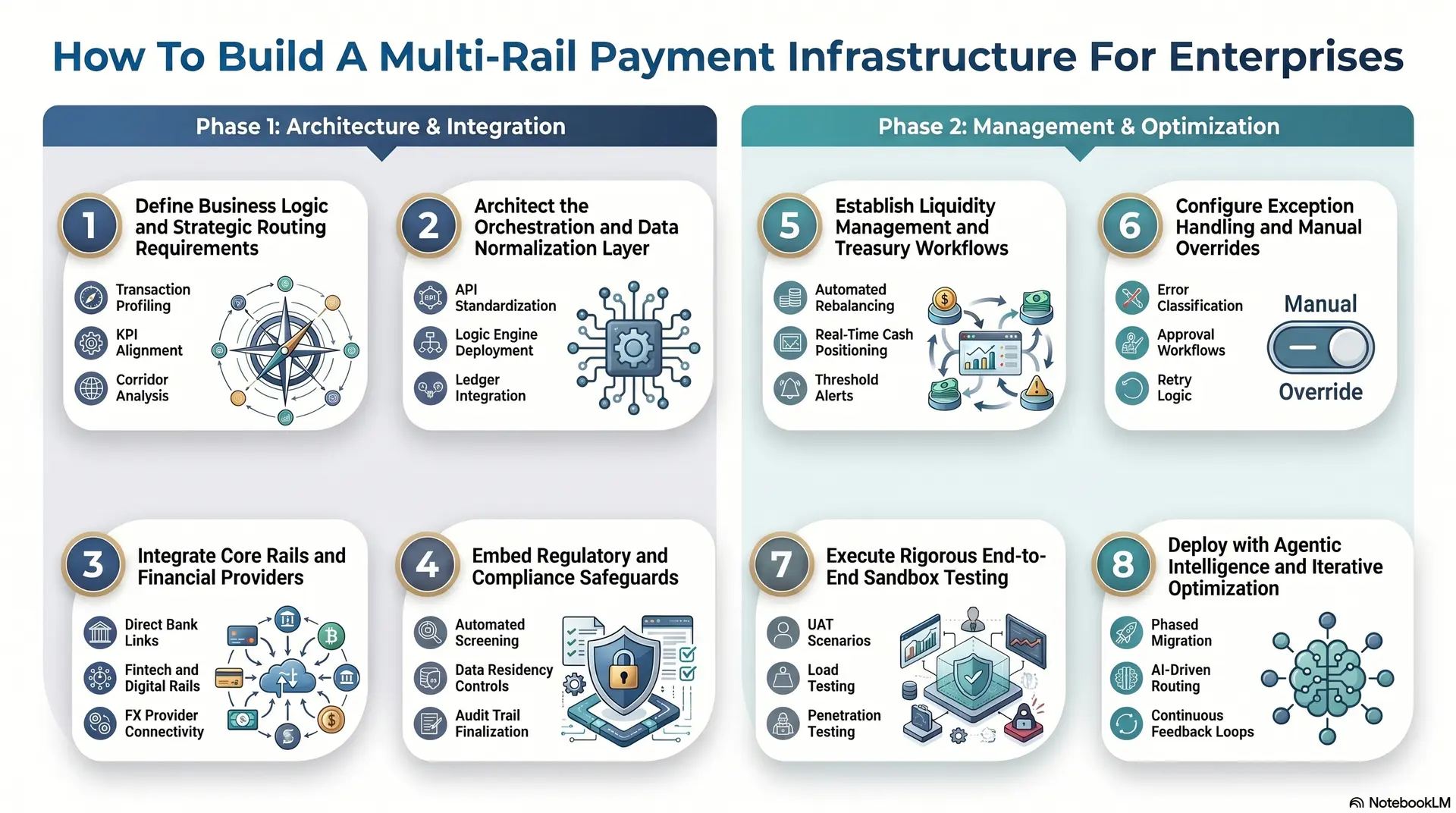

How To Build A Multi-Rail Payment Infrastructure For Enterprises

Building a robust, future-proof financial engine requires more than just connecting to a few bank APIs. It demands a strategic, multi-layered approach that prioritizes scalability, security, and operational intelligence.

Therefore, following a structured deployment roadmap is essential for high-stakes enterprise environments.

Step 1: Define Business Logic and Strategic Routing Requirements

Before a single line of code is written, leadership must define the parameters that will govern the movement of capital. This phase involves mapping out every possible payment scenario to determine the business rules that the orchestration layer will eventually automate.

- Transaction Profiling: Identify the typical volume, frequency, and geographic destination of your corporate payments.

- KPI Alignment: Determine whether the system should prioritize cost savings, settlement speed, or maximum redundancy for specific business units.

- Corridor Analysis: Evaluate which regional rails are necessary to support your current and future international expansion goals.

Step 2: Architect the Orchestration and Data Normalization Layer

The second phase involves building the central “brain” of the infrastructure. This layer must be capable of translating fragmented bank data into a unified format while executing complex routing logic in milliseconds.

- API Standardization: Develop a unified interface that allows internal systems to communicate with diverse external networks using a single protocol.

- Logic Engine Deployment: Implement the smart routing algorithms that will decide which rail to use based on real-time network conditions.

- Ledger Integration: Establish a canonical ledger that acts as the single source of truth for all transactions across every integrated bank and digital rail.

Step 3: Integrate Core Rails and Financial Providers

With the architecture in place, the enterprise must establish physical connectivity to the global financial ecosystem. This involves a mix of legacy host-to-host connections for bulk processing and modern API integrations for real-time liquidity.

- Direct Bank Links: Establish secure, high-bandwidth connections with primary global banking partners for mission-critical transfers.

- Fintech and Digital Rails: Integrate secondary providers like stablecoin issuers or regional real-time payment switches to provide alternative pathways.

- FX Provider Connectivity: Plug in specialized foreign exchange APIs to ensure competitive rates for all cross-border activity.

Step 4: Embed Regulatory and Compliance Safeguards

A multi-rail system is only as strong as its weakest compliance link. This step ensures that every transaction is automatically screened against global regulations without slowing down the user experience.

- Automated Screening: Integrate real-time KYC and AML tools directly into the payment flow to flag high-risk transactions instantly.

- Data Residency Controls: Configure the system to store and process sensitive financial data according to the specific laws of each jurisdiction.

- Audit Trail Finalization: Ensure that every routing decision and status change is recorded in an immutable, timestamped log for regulatory review.

Step 5: Establish Liquidity Management and Treasury Workflows

Effective multi-rail systems require a sophisticated approach to managing funds across multiple accounts. This step focuses on ensuring that every rail has sufficient liquidity to fulfill payments without creating trapped capital.

- Automated Rebalancing: Implement logic that moves funds between bank accounts and digital wallets based on predicted transaction volume.

- Real-Time Cash Positioning: Provide the treasury team with a live dashboard showing the exact status of funds across all global rails.

- Threshold Alerts: Set up automated triggers that notify the finance team when liquidity in a specific rail falls below a safe margin.

Step 6: Configure Exception Handling and Manual Overrides

Even the most advanced automated systems encounter edge cases that require human intervention. Building a robust exception management framework ensures that failed or flagged payments are resolved quickly without disrupting the entire system.

- Error Classification: Define specific protocols for different types of failures, such as network timeouts or bank rejection codes.

- Approval Workflows: Create a secure portal where authorized personnel can manually review and release payments flagged by the compliance engine.

- Retry Logic: Configure the system to automatically attempt a second or third rail if a primary connection returns a temporary error.

Step 7: Execute Rigorous End-to-End Sandbox Testing

Before going live, the entire stack must undergo stress testing in a secure, non-production environment. This phase validates that the routing logic, security protocols, and bank integrations work together as intended.

- UAT Scenarios: Run simulated transactions that mimic every possible business case, from local payroll to complex cross-border settlements.

- Load Testing: Bombard the system with high-volume traffic to ensure the orchestration layer can handle peak enterprise demands.

- Penetration Testing: Hire third-party security experts to attempt to breach the system and identify any vulnerabilities in the API or ledger.

Step 8: Deploy with Agentic Intelligence and Iterative Optimization

The final stage involves a phased rollout to production followed by the integration of AI-driven tools. This ensures that the system doesn’t just function but actually improves its own efficiency over time.

- Phased Migration: Gradually shift transaction volume from legacy systems to the new multi-rail architecture to mitigate risk.

- AI-Driven Routing: Utilize machine learning models to analyze performance data and suggest even more efficient routing paths.

- Continuous Feedback Loops: Use transaction success data to refine business rules and further reduce processing costs.

As a leader in enterprise technology, Intellivon provides the cutting-edge AI solutions and strategic engineering expertise required to build these complex systems. Our team specializes in developing high-performance orchestration layers that integrate seamlessly with your existing stack while unlocking the full potential of modern payment rails.

Multi-Rail Settlement, Liquidity, and Reconciliation

Strategic financial operations depend on the precise movement and accounting of capital across diverse networks. Managing these elements in a multi-rail environment requires a shift from traditional batch processing to a real-time, data-driven architecture.

This ensures that liquidity remains optimized and that the internal ledger reflects the true state of global funds at every second.

1. Real-Time vs Deferred Settlement Models

Understanding the timing of fund availability is critical for treasury management. Real-time models provide immediate finality, while deferred models operate on traditional banking cycles.

| Feature | Real-Time Settlement (RTP, FedNow) | Deferred Net Settlement (ACH, SEPA) |

| Availability | Instant (Seconds) | Delayed (1-3 Days) |

| Credit Risk | Zero (Finality is immediate) | Moderate (Risk of reversals) |

| Liquidity Need | High (Requires 24/7 funding) | Lower (Can be managed in cycles) |

| Operational Window | 24/7/365 | Standard Banking Hours |

| Best For | Payroll, Gig payouts, Refunds | Bulk vendor payables, Subscriptions |

2. Prefunding, Float Management, and Liquidity Architecture

A multi-rail system must intelligently manage the “float” to prevent capital from becoming trapped in low-yield accounts. Effective liquidity architecture ensures that every rail has exactly the amount of funding required to process anticipated transaction volumes without overextending the company’s cash reserves.

- Dynamic Prefunding: The system calculates necessary account balances based on historical daily payout patterns.

- Just-In-Time Liquidity: Funds move from a central treasury account to specific rails only when a transaction is triggered.

- Sweep Automation: Excess capital is automatically moved back into interest-bearing accounts at the end of a processing window.

3. Multi-Currency Settlement Handling

Operating across international borders introduces the complexity of managing multiple currency denominations. The system must handle the conversion, local settlement, and reporting for each currency while minimizing exposure to foreign exchange volatility.

- Virtual Multi-Currency Accounts: These allow the enterprise to receive and hold local currencies without opening physical bank branches.

- Real-Time FX Lock-In: The orchestration layer captures a guaranteed exchange rate at the moment of payment initiation.

- Local Rail Access: Payments are settled in the local currency of the recipient to avoid expensive cross-border wire fees.

4. Reconciliation Across Multiple Rails

Reconciliation is the process of matching internal transaction records with external bank statements. In a multi-rail setup, this must happen across dozens of different data formats and time zones.

Automating this process removes the burden of manual intervention and ensures the finance team can close the books faster.

- Automated Matching: The engine uses unique transaction IDs to pair internal entries with bank confirmations instantly.

- Data Aggregation: Information from ACH, Card, and RTP rails is pulled into a single dashboard for unified viewing.

- Discrepancy Flagging: The system identifies missing or duplicate entries and alerts the treasury team for immediate investigation.

5. Ledger Synchronization Challenges

Maintaining a synchronous state between the corporate ERP and multiple bank ledgers is a significant technical hurdle.

Network latency or bank downtime can cause temporary data gaps where the internal records do not match the actual bank balance.

- Event-Driven Updates: Every change in transaction status triggers an immediate update to the central canonical ledger.

- Idempotency Keys: These prevent the same transaction from being processed twice in the event of a network retry.

- Polling vs Webhooks: The system uses a mix of real-time push notifications and scheduled polling to ensure data integrity.

6. Exception Handling and Dispute Resolution

No payment system is perfect, and exceptions like insufficient funds or incorrect account details are inevitable.

A robust multi-rail infrastructure includes a standardized framework for managing these failures across all networks, ensuring that disputes do not derail the customer experience.

- Error Mapping: The system translates cryptic bank error codes into actionable instructions for the finance team.

- Automated Reversals: If a payment fails on a secondary rail, the system can automatically trigger a reversal on the internal ledger.

- Evidence Management: For card-based chargebacks, the system gathers transaction data and delivers proof to automate the dispute response.

Mastering the nuances of settlement and reconciliation transforms the treasury department from a cost center into a strategic nerve center. By ensuring that every transaction is accounted for and every dollar is utilized, an organization creates the financial stability needed for aggressive global growth.

Security Architecture for Multi-Rail Payment Infrastructure

Securing a fragmented payment environment requires a defense-in-depth strategy that protects data as it traverses multiple third-party networks.

Because each rail introduces a new potential vector for compromise, the security architecture must be centralized and proactive. A resilient system ensures that sensitive financial data is never exposed in its raw form, even during cross-border transitions or internal routing.

1. End-to-End Encryption and Tokenization

Protecting data at rest and in transit is the first line of defense against sophisticated financial cyber threats. Tokenization goes a step further by replacing sensitive account numbers or card data with non-sensitive digital identifiers.

This ensures that even if a database is breached, the information obtained is useless to the attacker and cannot be used to initiate fraudulent transactions.

- Asymmetric Encryption: High-level cryptographic keys secure communication between the enterprise orchestration layer and various bank APIs.

- Vaultless Tokenization: Advanced systems generate tokens mathematically without storing a central lookup table, further reducing the attack surface.

- PCI Compliance Scope: Implementing robust tokenization significantly reduces the number of systems that must adhere to strict PCI-DSS auditing.

2. Secure API and Access Control Systems

The API gateway acts as the gatekeeper for all incoming and outgoing financial instructions. Securing these gateways involves implementing granular access controls to ensure that only authorized services and users can interact with specific payment rails.

This prevents unauthorized movement of funds and protects against automated bot attacks on bank interfaces.

- Mutual TLS (mTLS): Both the sender and receiver must authenticate each other using digital certificates before any data is exchanged.

- OAuth 2.0 and OpenID Connect: These industry-standard protocols manage authorization and identity for internal microservices.

- Rate Limiting and Throttling: Automated controls prevent brute-force attacks and ensure that API calls remain within safe operational limits.

3. Fraud Detection and Behavioral Analytics

In a multi-rail environment, fraud can manifest differently depending on the network used. A centralized fraud engine analyzes transaction data from all rails simultaneously to identify patterns that deviate from established norms.

By utilizing behavioral analytics, the system can detect compromised accounts or insider threats before funds are irreversibly settled on a real-time network.

- Velocity Analysis: The system flags accounts that attempt to move large sums of money in small increments across different banks.

- Geospatial Tracking: Payments initiated from unexpected or high-risk geographic locations trigger immediate manual review.

- Machine Learning Models: Continuous training on historical fraud data allows the engine to adapt to new, emerging attack patterns in real-time.

4. Zero Trust and Identity Management

The Zero Trust model operates on the principle of “never trust, always verify.” Every request for access to the payment infrastructure must be authenticated, authorized, and continuously validated.

This approach is essential for distributed systems where employees, developers, and third-party vendors may all be accessing the core ledger from different environments.

- Multi-Factor Authentication (MFA): Critical actions, such as changing routing rules or approving high-value transfers, require a second layer of verification.

- Least Privilege Access: Users and services are granted only the minimum level of access necessary to perform their specific functions.

- Micro-Segmentation: The payment stack is divided into isolated zones to prevent lateral movement by an attacker within the network.

5. Data Protection in Distributed Systems

Managing payments across multiple rails often involves data residing in different clouds or regional jurisdictions. Ensuring data integrity and privacy in this distributed environment requires a unified governance framework.

This prevents data leakage and ensures that the organization remains compliant with global privacy mandates like GDPR or CCPA.

- Encryption Key Management: Centralized control over cryptographic keys ensures that data can be rotated or revoked across all rails instantly.

- Secure Enclaves: High-value processing tasks take place in hardware-isolated environments that are invisible to the rest of the operating system.

- Audit Logging: Every access request and data modification is captured in an immutable log for forensic analysis and compliance reporting.

Implementing a rigorous security architecture transforms the payment infrastructure from a vulnerability into a bastion of institutional trust.

By prioritizing data protection at every level of the stack, an enterprise can confidently adopt new payment technologies without compromising its integrity or its reputation in the global market.

Common Challenges in Multi-Rail Systems (And How We Solve Them)

Building and managing a multi-rail payment infrastructure is a complex endeavor that involves more than just technical connectivity. Enterprises frequently encounter deep-seated operational hurdles that can stall innovation and increase overhead.

Understanding these friction points is the first step toward building a resilient system that truly scales.

1. Fragmented Payment Ecosystems

The payment landscape is a patchwork of legacy banking protocols, modern fintech APIs, and emerging digital asset networks. Each rail operates on its own set of rules, messaging standards, and settlement timelines. Managing these separately creates massive operational inefficiency.

- The Challenge: Siloed workflows and disjointed data formats force teams to perform manual reconciliations across different platforms.

- Intellivon Solution: We deploy a unified orchestration layer that normalizes all data into a single canonical format. This transforms a disjointed ecosystem into a cohesive financial engine managed through one central dashboard.

2. Complex Integration Dependencies

Integrating with multiple financial institutions involves months of technical labor and specialized security certificates. Every time a bank updates an API or a new regional rail is added, the enterprise must dedicate significant engineering resources to maintain the connection.

- The Challenge: Technical debt and rigid host-to-host configurations create bottlenecks that prevent businesses from reacting to market changes.

- Intellivon Solution: We utilize an API-first strategy with a pre-built library of connectors for global banks and switches. Our managed layer handles all protocol shifts in the background, ensuring your connectivity remains future-proof.

3. Real-Time Processing Limitations

While the world moves toward 24/7 operations, many internal systems still rely on legacy batch-processing cycles. Bridging the gap between “instant” external rails and “delayed” internal ledgers often results in liquidity gaps and data discrepancies.

- The Challenge: Legacy systems cannot handle the sub-second latency required for modern real-time networks like RTP or FedNow.

- Intellivon Solution: We implement event-driven microservices that process transactions as discrete events. This ensures internal ledgers synchronize instantly with external confirmations, providing immediate visibility into cash positions.

4. Regulatory and Compliance Complexity

Moving money across different jurisdictions triggers an avalanche of requirements, from AML and KYC to regional data residency laws. Manually managing these risks across dozens of networks is virtually impossible at scale.

- The Challenge: One missed regulatory update or a failure in cross-border data localization can result in frozen accounts and heavy fines.

- Intellivon Solution: Our systems feature embedded compliance logic that applies the correct filters based on the specific rail and geography. We automate the audit trail to ensure adherence to standards like ISO 20022 and GDPR.

5. Scaling Without Downtime

As transaction volumes grow, legacy systems struggle to maintain performance, leading to timeouts during peak periods. For an enterprise, even a few minutes of downtime can result in millions of dollars in lost revenue and broken vendor trust.

- The Challenge: Scaling a live financial system requires surgical precision to ensure updates do not interrupt active money flows.

- Intellivon Solution: We build on a cloud-native, auto-scaling architecture that dynamically adjusts resources. By utilizing failover routing and blue-green deployments, we ensure your infrastructure grows alongside your business with 99.99% uptime.

Addressing these challenges head-on allows an organization to move beyond simple money transfer and into the realm of strategic capital orchestration. By removing the technical and regulatory friction, leadership can focus on what matters most: expanding market share and driving long-term value.

Conclusion

Building a multi-rail payment infrastructure transforms financial operations from a static cost center into a strategic growth engine. It ensures total resilience, cost efficiency, and global scalability for the modern enterprise.

By deploying sophisticated orchestration layers and real-time intelligence, organizations can future-proof their capital movement and unlock new competitive advantages today.

Build Multi-Rail Payment Systems With Intellivon

Engineering a multi-rail payment system requires building an intelligent infrastructure that can route transactions dynamically, optimize costs in real time, and operate seamlessly across global payment networks.

At Intellivon, we design multi-rail payment infrastructure that unifies orchestration, routing, compliance, and settlement into a single, high-performance system. Our approach focuses on turning fragmented payment ecosystems into a scalable, reliable financial backbone for enterprises.

A. Bridging Legacy Systems with Multi-Rail Infrastructure

Most enterprises rely on legacy banking and payment systems that were never designed for multi-rail flexibility.

We build the integration layer that enables seamless connectivity across modern and legacy rails.

- Middleware connecting core banking, gateways, and payment rails

- Real-time data synchronization across systems and networks

- Phased migration without disrupting existing operations

This allows you to adopt multi-rail capabilities without replacing your entire infrastructure.

B. Building Intelligent Payment Orchestration Layers

We design routing engines that optimize decisions in real time.

- Dynamic routing based on cost, speed, and success rates

- Failover mechanisms for uninterrupted transaction processing

- Rule-based and AI-driven decision engines

This ensures every transaction takes the most efficient and reliable path.

C. Designing Always-On Multi-Rail Infrastructure

Enterprise payment systems must operate continuously across multiple rails and geographies.

We build infrastructure that ensures uptime, performance, and resilience.

- High-availability architecture with redundancy and failover

- Event-driven systems for real-time processing

- Infrastructure designed for 24/7 transaction flows

This ensures consistent performance even during peak transaction loads.

D. Embedding Compliance Across All Payment Rails

Operating across multiple rails introduces complex regulatory requirements. We embed compliance into every layer of the system architecture.

- Built-in AML, KYC, and transaction monitoring systems

- Real-time audit trails and reporting frameworks

- Configurable compliance rules for different regions

This ensures your infrastructure remains compliant without slowing down transactions.

E. Deep Integration Across Global Payment Ecosystems

Multi-rail systems must connect across banks, networks, and financial tools. We design integration-ready architectures that unify the entire ecosystem.

- Integration with RTP, ACH, card networks, and SWIFT

- Connectivity with fintech APIs and third-party services

- Integration with ERP, treasury, and accounting systems

This creates a unified payment infrastructure instead of disconnected systems.

F. Scalable Architecture for Multi-Rail Expansion

As transaction volumes and rails increase, systems must scale without failure. We design architectures that support growth without re-engineering.

- Microservices-based modular system design

- Cloud-native infrastructure for elasticity

- Real-time observability and performance monitoring

This allows your platform to expand across rails, regions, and volumes seamlessly.

System Milestones and Business Impact

| System Milestone | Intellivon’s Engineering Focus | Business Outcome |

| Launch Phase | Core orchestration and rail integrations | Faster go-to-market |

| Growth Phase | Routing optimization and scaling | Stable performance at scale |

| Mature Phase | Cost optimization and automation | Lower costs, higher efficiency |

By partnering with Intellivon, you are creating a multi-rail financial infrastructure layer that optimizes transactions, reduces costs, and scales with your business.

Ready to build a multi-rail payment system that performs across rails, regions, and real-world demand?

Talk to Intellivon’s experts and get a tailored architecture and cost estimate for your platform.

FAQs

Q1. What is multi-rail payment infrastructure, and how does it work?

A1. Multi-rail payment infrastructure is a system that allows enterprises to process transactions across multiple payment networks from a single platform.

It works through a central payment orchestration layer that dynamically selects the best rail for each transaction based on cost, speed, success rate, and compliance requirements.

Instead of relying on a single payment method, the system routes transactions intelligently in real time. This approach improves transaction success rates, reduces costs, and ensures uninterrupted payment processing across regions and networks.

Q2. How long does it take to build a multi-rail payment system from scratch?

A2. The timeline depends on system complexity, the number of integrations, and compliance requirements.

- MVP (2–3 rails, basic routing): 4–6 months

- Mid-scale system (4–6 rails, full orchestration): 6–12 months

- Enterprise-grade platform (global rails, compliance layers): 12–18+ months

Timelines increase when integrating with multiple banks, legacy systems, or cross-border payment networks.

Many enterprises start with a focused MVP and expand gradually to reduce risk and accelerate time-to-market.

Q3. What integrations does a multi-rail payment infrastructure need?

A3. A multi-rail system requires deep integration across financial and enterprise ecosystems:

- Payment rails: RTP networks, ACH/SEPA, card networks, SWIFT

- Banking systems: Core banking, payment processors, settlement systems

- Liquidity providers: FX platforms, treasury systems

- Compliance systems: KYC, AML, fraud detection tools

- Enterprise systems: ERP, accounting, reconciliation platforms

- Third-party APIs: Fintech tools, wallets, and gateways

The complexity of these integrations is often the biggest driver of cost and timeline.

Q4. How does real-time payment routing work in a multi-rail system?

A4. Real-time payment routing uses a decision engine to select the most efficient payment rail at the moment a transaction is initiated.

The system evaluates multiple factors simultaneously:

- Transaction cost across available rails

- Processing speed and settlement time

- Success rates and network reliability

- Compliance and regulatory constraints

- Available liquidity and balances

Based on these inputs, the orchestration engine routes the transaction instantly. If a rail fails, the system automatically switches to a backup route (failover).

Advanced systems also use AI-driven routing to continuously optimize decisions based on historical performance.

Q5. How much does it cost to build a multi-rail payment infrastructure?

A5. There is no fixed cost, as pricing depends on system scope, integrations, and regulatory complexity.

Typical investment ranges:

- MVP (limited rails, basic orchestration): $300,000 – $700,000

- Mid-scale platform (multi-rail + compliance): $700,000 – $1.5M

- Enterprise-grade infrastructure (global rails): $1.5M – $4M+

Key cost drivers include:

- Number of payment rails and geographies

- Integration complexity with banks and networks

- Compliance and security requirements

- Real-time processing and infrastructure scale

Enterprises usually reduce risk by starting with a phased rollout, then expanding into a full multi-rail infrastructure.