Key Takeaways

-

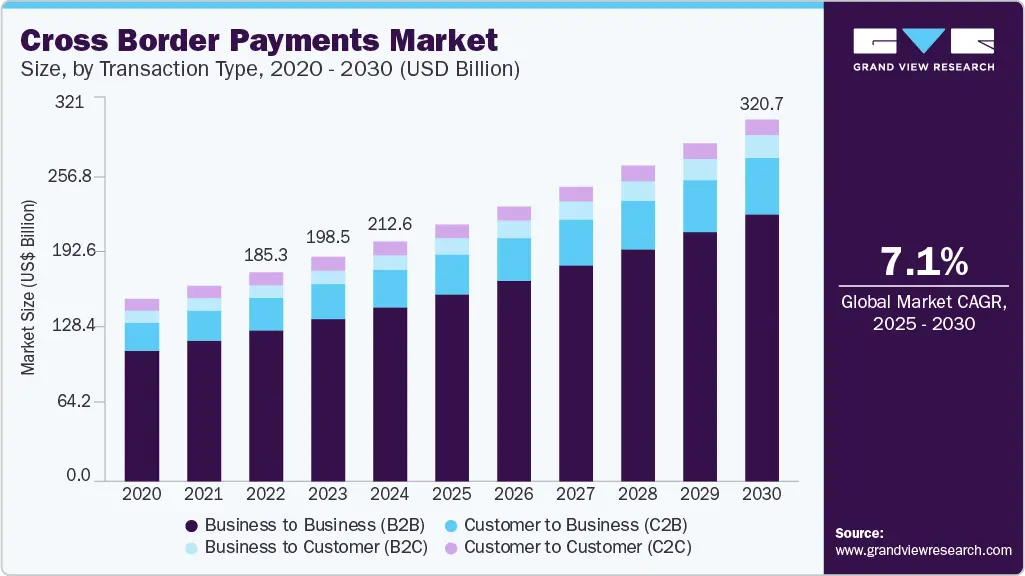

The global cross-border payments market is projected to reach $320.73 billion by 2030, yet legacy systems continue trapping billions in idle capital across jurisdictions

-

Building cross-border liquidity software requires decisions across five critical layers: visibility, movement, FX optimization, routing, and AI-powered forecasting

-

Compliance is not a final checkpoint. It must be embedded directly into transaction logic from day one to avoid costly regulatory friction at scale

-

A focused MVP covering core corridors and routing can be delivered between $50,000 and $80,000, with full-scale platforms scaling based on corridor depth and compliance complexity

-

Enterprises that solve cross-border liquidity infrastructure early build a structural competitive advantage that compounds as they expand into new markets

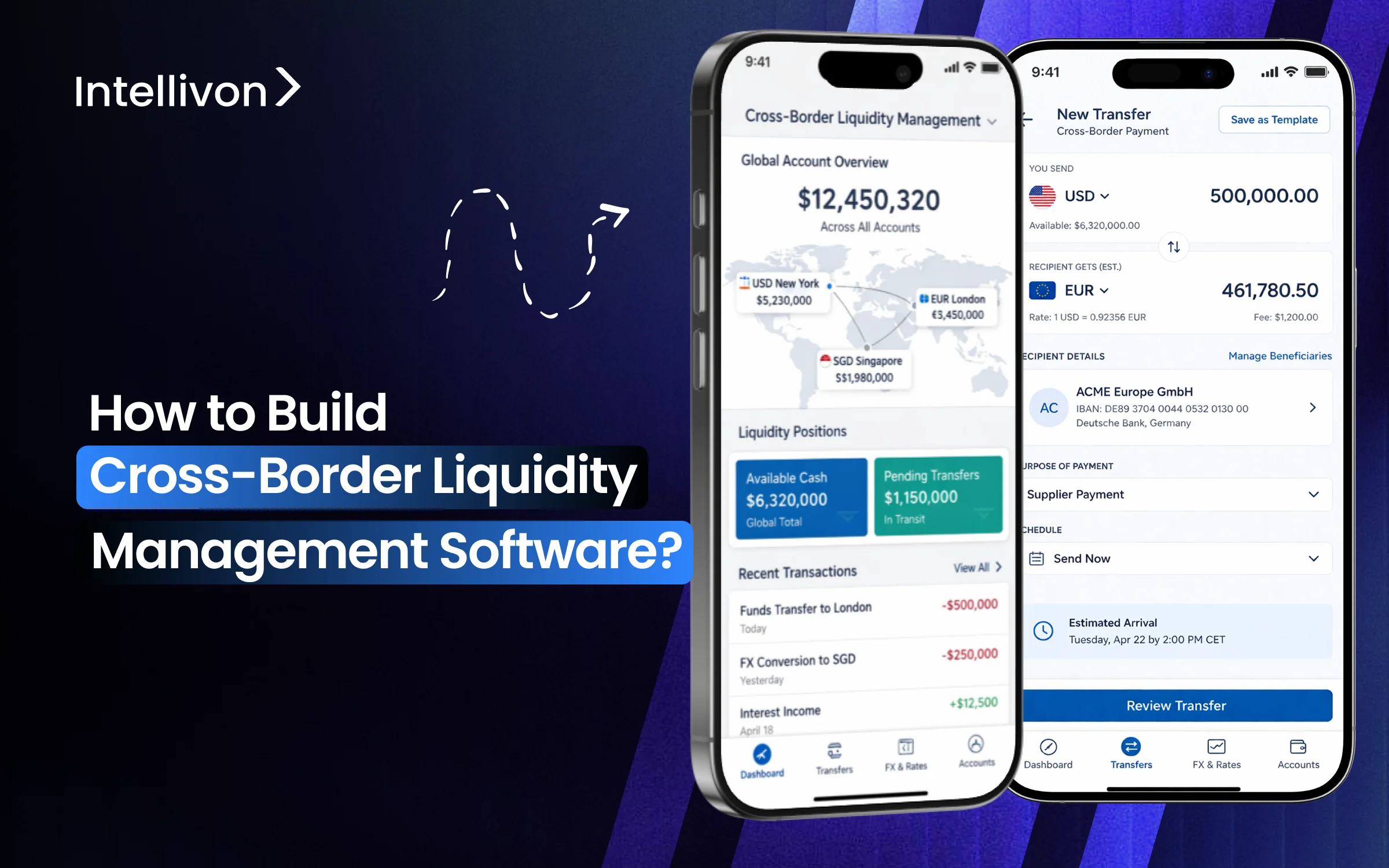

What if your treasury infrastructure could track, transfer, and optimize cash across every currency and jurisdiction in real time, without any manual steps? Cross-border liquidity management has reached a turning point now. Enterprises that are leading this market are creating financial infrastructures that view capital as a dynamic, strategic resource instead of just a static balance.

Building cross-border liquidity management software is a foundational infrastructure decision that touches treasury operations, regulatory compliance, currency risk, and real-time data architecture simultaneously. The difference between software that scales across jurisdictions and software that breaks under regulatory or volume pressure comes down to architectural decisions made early in the build.

At Intellivon, we have worked deep inside this problem. We draw from direct experience building enterprise-grade financial platforms to show you exactly how we approach these systems from the ground up, from core liquidity architecture and multi-currency engines to compliance workflows and AI-powered forecasting layers. This blog covers how we build such a platform from the ground up.

Why Cross-Border Liquidity Has Become a Critical Infrastructure Problem

Cross-border liquidity management has become a core infrastructure crisis. Legacy systems were never built for the speed global trade now demands. The market tells the story: $212.55 billion in 2024, projected to hit $320.73 billion by 2030 at a 7.1% CAGR, yet settlement delays and fragmented banking rails continue trapping billions in idle capital.

In 2026, trade volumes are surging, and real-time domestic payments are now standard across 70+ countries. However, international settlement has not kept pace. These gaps are stifling growth, inflating costs, and exposing enterprises to risks their competitors are quietly capitalizing on.

1. Legacy Correspondent Banking Bottlenecks

Cross-border payments still depend on a fragile chain of correspondent banks. Funds sit idle in nostro accounts for days, waiting on batch settlement cycles that belong to a different era.

Think of it this way: domestic payments clear in seconds, but sending money across borders often takes 2 to 5 days through the same intermediary-heavy process banks used in the 1990s.

The cost impact is significant:

- Average transaction fees run between 5% and 7%

- Settlement delays disrupt cash flow planning for both SMEs and large corporates

- Reconciliation across multiple intermediaries creates operational overhead that compounds at scale

For enterprises managing high transaction volumes, these are not minor inconveniences. They are structural drains on working capital.

2. Regulatory Fragmentation and De-Risking

Every jurisdiction has its own compliance rulebook. AML and KYC standards in the EU differ from those across Asia. Capital requirements shift country by country. Building a platform that operates globally, therefore, means engineering redundant compliance layers, which drives up cost and slows down expansion.

Banks have responded to this complexity through de-risking, withdrawing correspondent relationships from entire regions they consider high-risk. The result is a more fragmented global network, not a more connected one.

Geopolitical tensions have made this worse. Payment rails are increasingly being used as strategic tools, adding another layer of uncertainty for enterprises trying to move capital reliably across borders.

4. Rising Costs and Transparency Deficits

Cross-border payments cost roughly six times more than domestic transactions. Much of that cost is not visible upfront. Hidden FX spreads, intermediary markups, and opaque fee structures erode margins quietly.

Beyond cost, visibility is a serious operational problem:

- Poor payment tracking creates disputes and delays

- Limited transparency increases fraud exposure

- Enterprises scaling trade finance or remittance operations hit walls that legacy infrastructure simply cannot handle

The 24/7 nature of global commerce demands infrastructure that matches that pace. Most legacy systems were not designed for it.

5. Geopolitical and Tech Disruptions

The global payments landscape is fracturing. Competing systems like CIPS and SWIFT are pulling enterprises in different directions. Central bank digital currency pilots are advancing across dozens of countries, but without consistent standards, liquidity pools remain siloed rather than connected.

Blockchain and stablecoins offer genuine promise for cross-border settlement. However, enterprise adoption remains cautious. Immature infrastructure, regulatory uncertainty, and fraud concerns slow the transition.

The critical missing piece is standardization. Until ISO 20022 reaches full adoption across major corridors, fragmentation will continue to limit what even well-funded platforms can achieve.

Cross-border liquidity has become mission-critical infrastructure. Enterprises that invest now in interoperable real-time payment architecture, open APIs, and embedded compliance will not just reduce costs. They will build a structural advantage that compounds over time.

What Is Cross-Border Liquidity Management Software?

Cross-border liquidity management software is a technology system that gives financial institutions and fintechs real-time visibility and automated control over cash positions, FX exposure, and fund movements across multiple currencies, banks, and regulatory jurisdictions. It functions as a centralized engine for optimizing global capital flows while minimizing idle balances.

How It Differs from a Treasury Management System (TMS)

| Dimension | Treasury Management System (TMS) | Cross-Border Liquidity Platform |

| Core function | Cash flow forecasting and reporting | Real-time fund movement and optimization |

| Update frequency | End-of-day / batch | Sub-second / real-time |

| FX handling | Manual or scheduled | Automated rate optimization |

| Settlement | Instructional | Execution-level |

| Regulatory scope | Single jurisdiction | Multi-jurisdiction, built-in |

| Typical user | CFO / treasury team | Treasury + payments + engineering |

Three Platform Archetypes

Choosing the correct architecture is a critical decision that dictates your tax efficiency and regulatory footprint. Every organization requires a model that aligns with its specific legal structure and capital movement needs.

1. Centralized Pooling Model

This model utilizes one master account to control sub-account funding across various entities. It is the most effective approach for single-entity fintechs that manage multiple currencies but maintain a centralized treasury.

By consolidating funds into a primary hub, you maximize oversight and simplify your reporting processes. Consequently, this reduces the administrative burden of managing fragmented balances across different time zones.

2. Notional Pooling Model

In this archetype, balances are aggregated virtually without the physical movement of funds. This structure is ideal for multi-entity groups and tax-sensitive organizations that want to offset debits and credits to minimize interest costs.

Because money stays in its original account, you avoid the regulatory friction associated with cross-border transfers. Therefore, you gain the benefits of a consolidated balance while maintaining local autonomy.

3. Distributed Orchestration Model

Modern regulated fintechs often prefer this model, where each node maintains autonomous liquidity coordinated by a central decision engine. It allows you to meet jurisdiction-specific capital requirements while ensuring the entire network remains efficient.

The central engine monitors each node and triggers rebalancing only when necessary. This balance between local compliance and global efficiency is essential for scaling in complex, high-growth markets.

Selecting the right archetype ensures your platform remains compliant as you expand into new jurisdictions. It creates a solid foundation for sustainable growth and long-term financial stability.

How We Build A Cross-Border Liquidity Management Software

Building a platform for global capital orchestration requires more than standard engineering. It demands a fusion of financial logic, regulatory precision, and scalable architecture. At Intellivon, we specialize in delivering enterprise-grade AI solutions that transform these complex requirements into a streamlined competitive advantage.

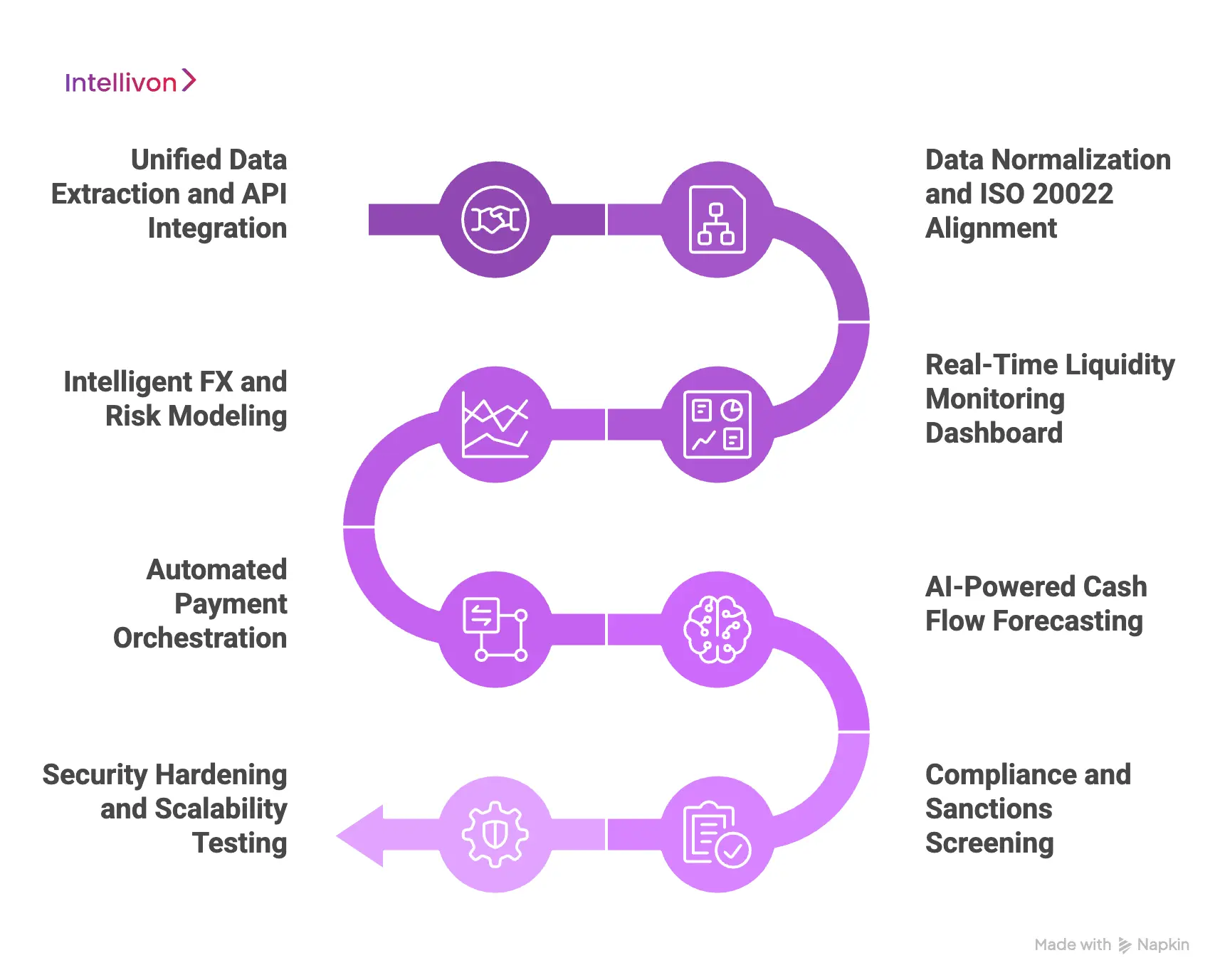

Step 1: Unified Data Extraction and API Integration

The foundation of any liquidity system is its ability to communicate with global banking partners. We begin by building robust connectors to your existing bank accounts through SWIFT, regional networks, or direct APIs.

- Bank Connectivity: Establish secure handshakes with Tier-1 and regional banks to pull raw balance data.

- Real-Time Polling: Implement webhooks or high-frequency polling to ensure data reflects the latest intraday movements.

- Data Integrity: Capture every detail from pending settlements to current available balances instantly.

Without this real-time visibility, any subsequent automation is based on outdated information, leading to inaccurate funding decisions.

Step 2: Data Normalization and ISO 20022 Alignment

Global banks use varying formats for financial messaging, which often leads to data silos. We implement a normalization layer that converts disparate data into a standardized format, specifically ISO 20022.

- Standardization: Mapping MT messages and proprietary CSV formats into a unified XML structure.

- Enrichment: Adding metadata to transactions to allow for better categorization and searching later in the workflow.

- Interoperability: Ensuring that transaction details remain intact as they move across different jurisdictions and clearing systems.

Standardized data is the absolute prerequisite for automated reconciliation and accurate reporting at scale.

Step 3: Real-Time Liquidity Monitoring Dashboard

Once the data is standardized, we build a centralized command center. This interface provides a single source of truth for your global cash positions across all entities.

- Visibility: Decision makers can view liquidity by currency, region, or specific legal entity in a single view.

- Drill-Down Capabilities: Move from a global macro-view down to individual transaction logs with one click.

- Operational Agility: This eliminates the need for manual spreadsheet updates and provides the transparency required for high-stakes financial maneuvers.

Step 4: Intelligent FX and Risk Modeling

Managing multiple currencies introduces significant exchange rate risk that can erode profits. We integrate predictive models that analyze market volatility and suggest the most opportune times for conversion.

- Exposure Analysis: Automatically identify which currencies are over-exposed based on upcoming payables.

- Hedging Strategies: Provide recommendations for spot or forward contracts to lock in favorable rates.

- Cost Minimization: This step minimizes the “hidden tax” of unfavorable exchange rates and protects margins during periods of extreme market instability.

Step 5: Automated Payment Orchestration

This is where the software becomes proactive rather than reactive. We build rules-based engines that automatically route funds based on cost, speed, and liquidity needs.

- Smart Routing: The system decides whether a payment should take a local ACH, a wire transfer, or a blockchain-based rail.

- Pre-funding Automation: Automatically move funds to specific accounts just-in-time to cover expected outflows.

| Feature | Impact on Operations | Business Value |

| Auto-Rebalancing | Prevents account overdrafts and failed payments | Reduces borrowing costs and penalty fees |

| Smart Routing | Selects the lowest-fee payment rails dynamically | Increases transaction margins significantly |

| Real-time FX | Executes trades at optimal rates via API | Protects against sudden currency dips |

Step 6: AI-Powered Cash Flow Forecasting

We leverage Intellivon’s deep expertise in AI to build predictive engines that look into the future. By analyzing historical transaction patterns, the software forecasts upcoming liquidity gaps before they happen.

- Pattern Recognition: Identify seasonal trends and recurring payment cycles unique to your business.

- Scenario Modeling: Run “what-if” simulations to see how a large acquisition or market shift affects your cash position.

- Proactive Planning: Therefore, you can pre-fund accounts or move capital strategically to meet future obligations without last-minute stress.

Step 7: Compliance and Sanctions Screening

Every cross-border movement must pass through a gauntlet of complex international regulations. We embed automated KYC, AML, and sanctions screening directly into the transaction flow.

- Real-time Screening: Check every sender and receiver against global watchlists (OFAC, UN, EU) before funds move.

- Audit Trails: Maintain immutable records of why a transaction was approved or flagged for review.

- False-Positive Reduction: AI filters out common naming mismatches, allowing your compliance team to focus on actual risks.

Step 8: Security Hardening and Scalability Testing

The final phase focuses on making the system impenetrable and future-proof. We implement multi-factor authentication, end-to-end encryption, and rigorous audit trails.

- Hardening: Ensuring SOC 2 and PCI DSS compliance standards are met at every infrastructure layer.

- Stress Testing: We simulate high-load environments to ensure the architecture handles sudden spikes in transaction volume.

- Future-Proofing: This guarantees that your platform remains stable and responsive as your enterprise scales globally into new markets.

Building a cross-border liquidity management system is a transformative investment that turns treasury from a cost center into a strategic engine. However, the technical and regulatory hurdles are significant. You need a partner who understands the nuance of enterprise AI and the rigors of global finance.

Architecture Behind Scalable Cross-Border Liquidity Systems

Building an enterprise platform requires a modular framework that can grow with your transaction volume. At Intellivon, we utilize a proprietary methodology to ensure global systems remain resilient and cost-effective.

This structured approach moves beyond generic development by treating liquidity as a multi-layered orchestration challenge.

The Unified Liquidity Orchestration Framework (ULOF)

Intellivon’s ULOF is a five-layer architecture model for building enterprise-grade cross-border liquidity systems. Each layer is independently deployable and horizontally scalable to meet global demand.

| Layer | Name | Core Function | Typical Build Time |

| Layer 1 | Visibility & Aggregation | Real-time account balance consolidation | 6–10 weeks |

| Layer 2 | Movement & Sweeping | Automated fund transfers and pooling | 8–12 weeks |

| Layer 3 | FX & Rate Optimization | Smart currency conversion and spreads | 8–14 weeks |

| Layer 4 | Routing & Settlement | Payment network orchestration | 10–16 weeks |

| Layer 5 | Intelligence & Forecasting | Predictive cash positioning | 12–20 weeks |

Total parallel development with an experienced team generally takes 9–14 months for a Minimum Viable Product (MVP). Full production deployment usually requires 14–20 months.

Layer 1: Real-Time Liquidity Visibility Across Accounts

This is a unified data layer that aggregates live balance and transaction data from every bank account. It covers every currency and jurisdiction to provide a single consolidated view.

- Multi-bank API Integration: Connects with SWIFT gpi, Open Banking, and proprietary bank APIs.

- Nostro/Vostro Tracking: Maintains intraday position updates for complex internal account structures.

- Reconciliation Engine: Matches credits and debits across entities in real time to ensure data accuracy.

Production-grade systems should deliver a balance refresh latency of under 30 seconds across all accounts. Leading implementations achieve sub-5-second refreshes via event-driven architecture. One key decision is choosing between polling and event-driven architecture.

Layer 2: Automated Liquidity Sweeping and Pooling

The execution layer automatically moves funds between accounts to maintain target balances and fund settlements. It optimizes capital deployment without requiring manual treasury intervention.

- Zero-Balancing: Sub-accounts drain to zero at the end of the day while the master account funds them on demand.

- Target-Balancing: Sub-accounts maintain a defined minimum and sweep any excess to the master account.

- Cross-Currency Pooling: Creates virtual notional pools across currency accounts using integrated FX logic.

Automated sweep execution should complete in under 90 seconds for intrabank transfers. However, cross-border SWIFT transfers may take up to 4 hours. Founders often miss the need for jurisdiction-specific logic. A sweep that works in the EU might trigger strict reporting in Singapore. Consequently, compliance-aware configuration adds several weeks to this build.

Layer 3: FX Conversion and Rate Optimization Engine

This automated system selects the optimal FX provider and rate for every cross-currency transaction. It uses real-time market data and volume thresholds to minimize costs.

- Rate Aggregation: Pulls real-time rates from multiple banks, ECNs, and non-bank FX providers.

- Smart Order Routing: Chooses the best rate across all available providers for every specific transaction.

- Hedging Triggers: Automatically initiates forward contracts when currency exposure crosses defined safety thresholds.

A well-configured engine typically reduces blended FX costs by 15–35 basis points per transaction. Therefore, the architecture must maintain sub-second rate refreshes. Latency above 2 seconds creates material slippage risk during high-volume periods.

Layer 4: Payment Routing and Settlement Orchestration

The network layer selects and executes payments across multiple clearing systems like SWIFT, SEPA, and ACH. It makes decisions based on speed, cost, and regulatory eligibility rules.

- Supported Networks: Integrates SWIFT MT/MX, SEPA Instant, US RTP, and regional rails like PIX or UPI.

- Regulatory Checks: Verifies if a specific payment is eligible for a chosen rail before execution.

- Fallback Logic: If the primary rail fails, the system automatically routes to the next best eligible option.

Production routing engines should maintain a settlement success rate with automatic fallback enabled.

Manual intervention rates should ideally stay under 0.5% of total volume. Because each rail has unique requirements, the system must sequence payments intelligently to avoid bottlenecks.

Layer 5: Liquidity Forecasting and Cash Positioning

The intelligence layer uses historical patterns and real-time signals to predict future cash positions. It proactively funds accounts before shortfalls occur to prevent transaction failures.

- Intraday Projections: Forecasts cash positions on a 1–24 hour horizon to manage immediate liquidity.

- ML-Based Models: Use machine learning trained on transaction history for 1–30 day forecasts.

- Early Warnings: Triggers alerts when projected positions are likely to breach minimum buffer thresholds.

ML-based models achieve 85–92% accuracy on intraday projections after 90 days of training. In contrast, rule-based models without machine learning only achieve 65–75% accuracy. Therefore, you must plan for at least 6 months of clean transaction history to train these models effectively. This data architecture should be a priority from day one.

Implementing a cross-border liquidity system is a major technical undertaking that defines your operational efficiency. We help you transition from fragmented manual processes to a unified, intelligent framework.

Advanced Capabilities Of Cross-Border Liquidity Software

Competitive differentiation in global finance rests in the intelligence and autonomy embedded within your infrastructure. Leaders in this space move beyond manual oversight toward a system that anticipates needs and executes complex maneuvers with minimal friction.

1. Real-Time Decision Engine for Autonomous Liquidity Moves

The most advanced platforms utilize a hybrid engine that combines logic-based rules with machine learning to execute actions without human intervention. This engine operates within strict risk parameters defined by your treasury team.

For example, if a specific currency balance drops below a set threshold while exchange rates remain favorable, the system can automatically trigger a sweep and conversion.

- Speed of Execution: These engines target a decision-to-execution window of under 500 milliseconds.

- Auditability: A core design principle is that every autonomous action must generate an immutable log entry.

- Risk Mitigation: Automated safeguards prevent the system from executing large moves during periods of extreme market volatility.

2. AI-Based Liquidity Forecasting

Relying on simple historical averages is insufficient for global scale. Leading organizations implement advanced neural network models that significantly outperform basic rule-based forecasting.

These models require clean, labeled transaction data and a real-time pipeline to engineer features from market signals.

- Long-Term Accuracy: These models provide a clearer picture of cash needs over seven-day horizons or longer.

- Development Roadmap: This is rarely a day-one feature. It requires several months of data collection and model validation post-launch.

- Corridor Tagging: Successful implementation depends on tagging data at the corridor level to account for regional payment nuances.

3. Multi-Entity and Multi-Jurisdiction Control Layer

Global enterprises must manage separate liquidity pools for each regulated entity while maintaining a consolidated group-level view. This layer ensures that capital is utilized efficiently without violating local laws.

- Embedded Agreements: Intercompany lending rules are built directly into the sweep logic to ensure tax efficiency.

- Local Compliance: The system respects jurisdiction-specific “lock” rules, such as ring-fencing requirements in strictly regulated markets.

- Visibility: Management maintains a macro-view of the entire group’s health while local teams manage their specific entity.

4. Embedded Compliance Across the Stack

Security and compliance should never be an afterthought. Leaders embed transaction screening directly into the routing layer, rather than bolting it onto the end of the process. This proactive approach identifies risks before funds ever leave an account.

- Real-Time Sanctions: Checks are performed against global watchlists including OFAC, the EU, and the UN in milliseconds.

- Pattern Detection: AI identifies unusual cross-border flows that may signal money laundering or fraud.

- Automated Reporting: The system generates required documentation for suspicious activities automatically, reducing the burden on human compliance officers.

5. Liquidity-as-a-Service (LaaS) API Layer

Modern platforms treat their liquidity functions as a product. By exposing core features as APIs, you can empower downstream partners or provide embedded treasury solutions to your own B2B customers.

- API Endpoints: Partners can access real-time positions, trigger sweeps, or request FX quotes through a secure gateway.

- Business Growth: This capability allows you to white-label your infrastructure for partner banks.

- Monetization: Transforming your internal tools into an API-driven service creates a new revenue stream for the business.

Building these advanced features ensures your platform remains a strategic asset as your transaction volume and geographic footprint expand. It moves the business from a state of constant reaction to a position of total operational control.

System Architecture for Cross-Border Liquidity Platforms

Designing a platform for global capital movement requires a shift from traditional monolithic structures to highly resilient, decoupled systems. The architecture must handle the volatility of foreign exchange markets while maintaining absolute data integrity across multiple time zones.

Building a system that remains responsive even under extreme transaction loads is a foundational requirement for any serious financial infrastructure project.

1. Event-Driven Architecture

Modern liquidity management demands immediate action as soon as a balance change or FX rate update occurs. Therefore, every significant event should emit a signal to a central message broker to trigger downstream actions.

Relying on a polling-based architecture creates unacceptable latency windows that can lead to inaccurate funding decisions.

- Real-Time Throughput: An event-driven approach allows the system to process high volumes of updates during peak settlement windows without bottlenecks.

- Decoupling: Services can act on information independently, which increases the overall speed and reliability of the platform.

- Accuracy: Because the system reacts to events as they happen, your treasury team always views a precise reflection of current global positions.

2. Microservices Decomposition

Breaking the system into specialized services allows for independent scaling and easier maintenance.

Each module should have a clear responsibility and a defined boundary to prevent cascading failures during market volatility.

| Service | Responsibility | Technical Requirement |

| Account Aggregation | Consolidates balances across global banks | High read throughput and caching |

| Sweep Orchestrator | Evaluates and executes movement rules | Idempotent execution to prevent duplicates |

| FX Engine | Manages rate aggregation and routing | Minimal latency with in-memory storage |

| Payment Router | Selects and executes network rails | Distributed transaction integrity |

| Compliance Engine | Handles screening and AML checks | Synchronous blocking for high-risk flags |

| Audit Service | Maintains an immutable record of all actions | Append-only storage for security |

3. High-Volume Stream Architecture

A sophisticated liquidity platform requires a tiered data strategy to balance speed with long-term reliability. Implementing different storage solutions based on how quickly the data needs to be accessed and the level of consistency required is critical.

- The Hot Path: Use in-memory stores for real-time balance positions to ensure sub-millisecond read times during peak hours.

- The Warm Path: Relational databases provide strong consistency for transactional records where data accuracy is the highest priority.

- The Cold Path: Columnar storage solutions are utilized for historical analysis, training forecasting models, and generating complex regulatory reports.

- The Event Store: A durable message log retains transaction events for a set period to allow for system recovery and detailed compliance audits.

4. Resilience and High Availability Design

Enterprise-grade systems must remain operational around the clock to support global markets. Designing for high availability involves ensuring that no single point of failure can bring down the entire payment infrastructure.

- Multi-Region Deployment: Running the system in an active-active configuration across different geographic regions ensures continuous service during local outages.

- Circuit Breaker Pattern: This prevents a failing external bank API from slowing down the rest of your system by temporarily isolating the integration.

- Graceful Degradation: If a non-essential service like the FX engine experiences issues, the system should fall back to pre-agreed rates rather than blocking vital payments.

Implementing these architectural principles ensures your platform is not only fast but also fundamentally reliable. This technical foundation allows your business to scale into new jurisdictions with the confidence that your infrastructure can handle the increased complexity.

Integration Architecture For Cross-Border Liquidity Software

Efficient liquidity management relies on a seamless web of connections between internal ledgers and global financial networks. This architecture ensures that capital remains mobile and visible across diverse banking ecosystems.

1. Core Banking and Ledger Integration

The platform must communicate directly with your system of record to manage balance queries and payment instructions. Most organizations utilize RESTful or ISO 20022-compliant APIs to facilitate this data flow.

- Connectivity: Integration is straightforward with modern providers like Mambu or Thought Machine due to their well-documented cloud APIs.

- Legacy Challenges: Older systems from providers like FIS often require custom middleware to bridge the gap between modern software and mainframe logic.

- Development Velocity: Organizations should budget approximately three to six weeks for each core banking partner integration.

2. SWIFT Integration (gpi and ISO 20022)

Direct connectivity to the SWIFT network is essential for handling international correspondent banking. This provides the necessary rails for high-value cross-border transfers and real-time tracking.

- Tracking Capabilities: Implementing SWIFT gpi is necessary to provide users with end-to-end visibility of their funds.

- Messaging Standards: Systems must be built for MX message adoption from the start to meet global ISO 20022 requirements.

- Cost Models: While direct membership involves significant annual fees, utilizing a service bureau model can reduce upfront capital expenditure.

3. FX Liquidity Provider Integration

To achieve genuine best-execution capabilities, a platform should integrate with at least two or three distinct FX providers. This diversity protects margins and ensures liquidity remains available during market stress.

- Provider Mix: Leaders combine Tier-1 bank desks with non-bank market makers and ECNs for deeper liquidity.

- Performance Targets: High-performance systems require rate quote responses in under 100 milliseconds to prevent slippage.

- Confirmation Speed: Execution confirmations should ideally return in under 500 milliseconds to maintain a smooth user experience.

4. Local Payment Rail Integration by Region

Connecting to local rails is the only way to ensure fast, low-cost domestic payouts within international corridors. Each region presents unique technical hurdles and regulatory requirements.

| Region | Primary Rail | Typical Build Time |

| Europe | SEPA CT / SCT Inst | 4–8 weeks |

| United States | ACH / RTP | 4–6 weeks |

| United Kingdom | Faster Payments | 3–5 weeks |

| India | IMPS / UPI | 5–8 weeks |

| Brazil | PIX | 3–5 weeks |

| Singapore | FAST / PayNow | 4–6 weeks |

| Nigeria | NIP / RTGS | 6–10 weeks |

5. ERP and Treasury System Integration

For enterprise clients, the liquidity platform must sync bi-directionally with their existing ERP systems. This allows for automated cash position reporting and the direct receipt of payment instructions.

- Common Partners: Standard integrations usually include SAP Treasury, Oracle Financials, and NetSuite.

- Protocols: Systems typically use ISO 20022 or MT940 for balance reporting while utilizing REST APIs for instruction intake.

- Complexity Factors: Heavily customized ERP environments often extend the build time beyond the standard four-to-eight-week window.

Mastering these integrations transforms a fragmented financial setup into a unified global engine. A well-integrated stack reduces manual overhead and ensures capital is always positioned for maximum utility.

Compliance and Regulatory Architecture

A global liquidity system must be designed as a compliance-first environment where regulatory checks are integrated into the transaction logic. Failure to automate these workflows leads to significant operational bottlenecks and increased legal risk.

Organizations must build their architecture to respect both international standards and the specific mandates of each jurisdiction they enter.

1. KYC and AML Integration Layer

Compliance checks should be a fundamental part of the payment routing decision tree rather than a final, separate step. By embedding these checks early, you ensure that high-risk transactions are flagged before capital is ever committed to a movement.

- Identity Verification: Integrate with established providers at the onboarding stage and link every entity ID to all subsequent downstream transactions.

- Transaction Monitoring: Combine rules-based logic for known risks with machine learning to identify unusual patterns that may signal new types of fraud.

- Operational Efficiency: Industry data shows that AML false positive rates often range between 85% and 95%. Therefore, focus on fine-tuning models to reduce alert fatigue, which otherwise consumes hundreds of analyst hours.

2. Intraday Liquidity Reporting (Basel III Compliance)

Regulators increasingly require detailed oversight of how organizations manage their daily cash inflows and outflows. Your system must be capable of generating standardized metrics that reflect your immediate financial health under both normal and stressed conditions.

- Core Metrics: The platform should calculate the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) to ensure sufficient high-quality liquid assets are available.

- Real-Time Visibility: While regulators may only require daily reports, internal risk teams need a real-time view of intraday peak usage to prevent shortfalls.

- Data Tagging: Every account movement must be timestamped and categorized by regulatory type in a reporting data mart to ensure immediate availability for audits.

3. Data Residency and Sovereignty Requirements by Region

As data protection laws evolve, a centralized international infrastructure is often no longer viable for global payment processors. You must architect your system to respect local laws regarding where financial data is stored and processed.

| Region | Primary Requirement | Architectural Implication |

| European Union | GDPR Compliance | Personal data must stay in the EU; no cross-region replication of PII. |

| United States | State-level Variation | Multi-region cloud deployments with strict contractual data controls. |

| Singapore | MAS TRM Guidelines | Risk-based cloud usage is generally allowed subject to MAS approval. |

4. Audit Trail Architecture

A robust audit trail is the final line of defense during a regulatory examination. It provides a comprehensive, immutable record of every state change within the system, from balance updates to final settlement confirmations.

- Retention Standards: Most jurisdictions require financial records to be kept for at least seven years, while AML-related data in the EU often requires ten years.

- Integrity Features: The log must be tamper-evident, often using hash-chaining to ensure that records cannot be altered after they are written.

- Technology Choice: For early-stage platforms, a cost-effective solution is a relational database with specific triggers, while high-assurance environments often utilize purpose-built immutable ledgers.

Designing with these compliance pillars in mind protects your business from the “compliance debt” that often halts the expansion of growing fintechs. It ensures that your platform is ready for the scrutiny of global regulators from the very first transaction.

Challenges in Building Cross-Border Liquidity Systems (And How to Solve Them)

Building global financial infrastructure involves navigating a series of high-stakes technical and operational hurdles. Failure to address these core challenges early in the development cycle often leads to catastrophic capital fragmentation or regulatory friction.

Successful organizations prioritize solving these systemic issues to ensure their platform remains both scalable and secure.

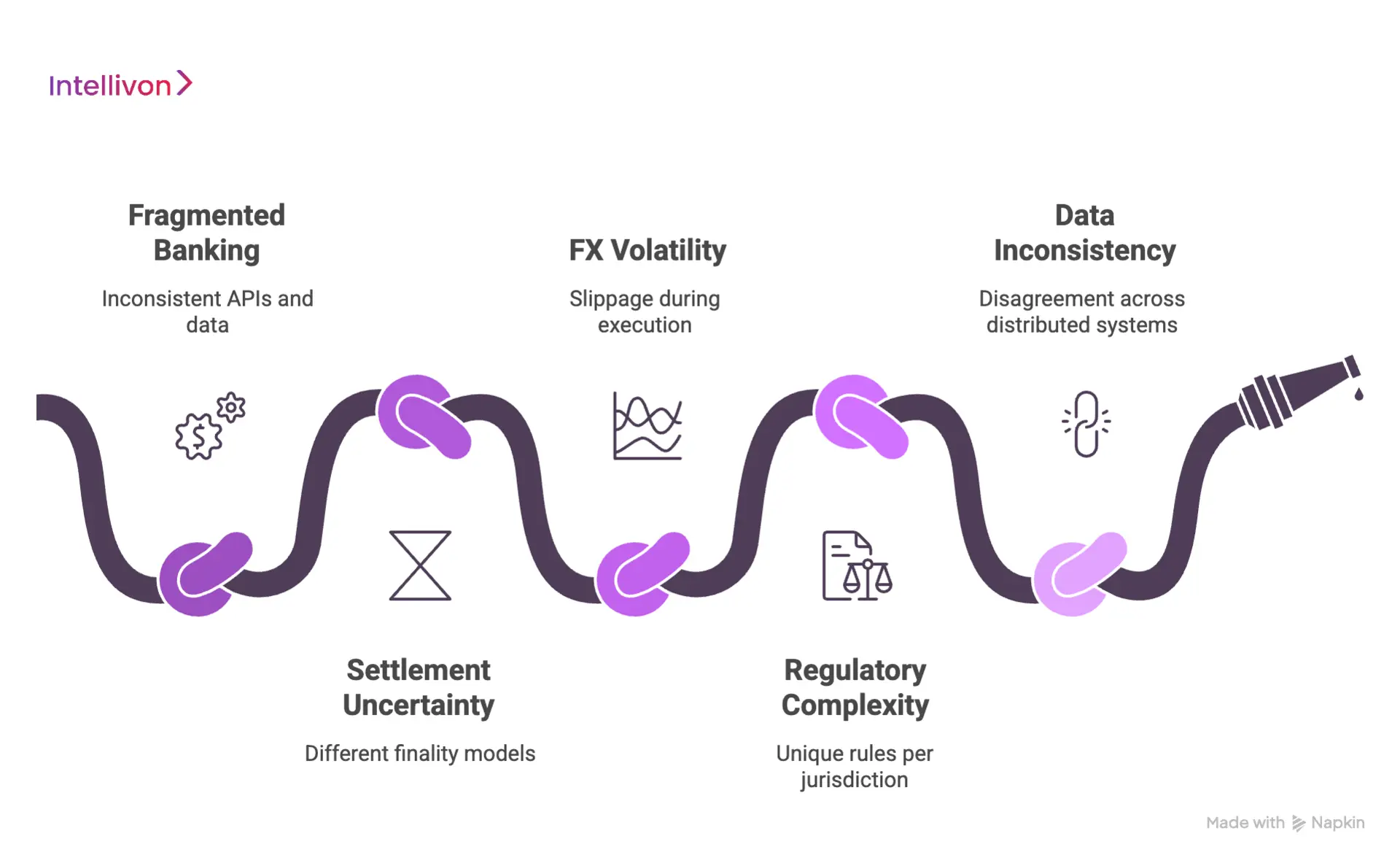

Problem 1: Fragmented Banking Infrastructure

The most immediate hurdle is that no two banks share the same API schema, authentication method, or data format. Therefore, integrating with ten different banking partners effectively becomes ten separate, unaligned engineering projects.

This fragmentation slows down deployment and makes maintaining the system a constant struggle.

- The Solution: Build a dedicated bank adapter layer with a normalized internal schema.

- Implementation: Every external bank API maps to your internal account and transaction model so that upstream systems never interact with bank APIs directly.

- Impact: While this adds several weeks of upfront development, it saves months of downstream refactoring as you scale your banking network.

Problem 2: Settlement Finality Uncertainty

Different payment rails operate on vastly different finality models. For instance, Real-Time Payments (RTP) are typically instant and final, whereas ACH transfers carry a multi-day return window.

Building liquidity logic on top of these inconsistent models creates a significant risk of double-spending or inaccurate reporting.

- The Solution: Implement a finality state machine specifically tailored to each rail.

- Logic: Funds are not considered “settled” within the liquidity model until the specific finality state for that rail is reached.

- Resilience: Your system must maintain separate reserve buffers to account for the difference between pending and final positions.

Problem 3: FX Volatility During Execution Windows

Market volatility can cause significant slippage between the time an FX quote is received and the moment it is executed. For large-scale conversions, even a few seconds of delay can result in substantial financial losses.

Consequently, protecting margins requires a highly responsive and intelligent execution strategy.

- The Solution: Implement a rate lock with a strict Time-to-Live (TTL).

- Mechanism: The system ensures execution occurs within a 30 to 60-second window provided by the liquidity provider.

- Advanced Tactics: For high-volume conversions, utilizing a Time-Weighted Average Price (TWAP) execution helps reduce market impact and smooths out price fluctuations.

Problem 4: Regulatory Complexity Across Multiple Jurisdictions

Each new market introduces a unique layer of payment rules, reporting requirements, and capital restrictions. Hardcoding these rules into your core logic makes global expansion nearly impossible.

What may be an automated process in one region might be strictly prohibited in another.

- The Solution: Build a jurisdiction-specific rules engine as a standalone configuration layer.

- Strategy: Express each market’s requirements as data rather than code.

- Outcome: Adding a new jurisdiction becomes a configuration exercise rather than a complex software release, allowing for much faster international growth.

Problem 5: Data Consistency Across Distributed Systems

In a microservices architecture, different services, such as the sweep orchestrator and the payment router, must all maintain an accurate state. However, network partitions or service delays can cause these systems to disagree on current balances. This lack of consistency can lead to overdrawn accounts or failed transactions.

- The Solution: Use the Saga pattern for distributed transactions to ensure integrity.

- Rollback Logic: Implement compensating transactions to reverse changes if a multi-step process fails.

- Data Integrity: Utilize event sourcing so that the current state of any account is always derivable from an immutable event log. Therefore, you should never trust a balance read that does not include a precise timestamp.

Addressing these five problems directly ensures your infrastructure is robust enough to handle the pressures of global finance. It transforms your liquidity system from a collection of fragile connections into a resilient, strategic asset for the business.

How Much Does It Cost to Build Cross-Border Liquidity Software?

Building cross-border liquidity software is not a fixed-cost project. The total investment depends on how deeply the platform integrates with banks, payment rails, FX providers, and compliance systems.

Unlike full-scale banking infrastructure, early-stage or focused builds can be delivered within a controlled budget by limiting corridors, integrations, and automation layers.

Total Investment Range by Scope

| Build Scope | Timeline | Investment Range |

| MVP (1–2 corridors, basic visibility + routing) | 3–5 months | $50,000–$80,000 |

| Early-stage platform (2–4 corridors, FX + pooling) | 4–7 months | $80,000–$120,000 |

| Scaled MVP (4–6 corridors, automation layers) | 6–9 months | $120,000–$150,000 |

Note: These ranges assume a focused build with limited geographies and API-based integrations. Expanding corridors or adding compliance layers increases cost significantly.

Cost Breakdown by Module

| Module | % of Total Cost | Notes |

| Account aggregation and bank integrations | 20–25% | Driven by the number of banking partners and APIs |

| Sweep and pooling engine | 10–15% | Simpler for single-region setups |

| FX optimization engine | 12–18% | Depends on provider integrations and pricing logic |

| Payment routing and settlement | 15–20% | Limited rails reduce complexity significantly |

| Liquidity forecasting (rule-based) | 8–12% | ML models increase cost beyond the MVP scope |

| Compliance and basic monitoring | 8–12% | Minimal viable compliance layer only |

| Infrastructure, DevOps, security | 10–15% | Cloud-native setups optimize cost at this stage |

Key Cost Variables Founders Underestimate

- Bank integrations complexity: Even API-based integrations vary widely across banks and regions

- FX provider dependencies: Pricing feeds and execution APIs often come with hidden costs

- Compliance tooling: Even basic AML/KYC tools can cost $10K–$50K annually

- Data hosting requirements: Multi-region deployment increases infrastructure costs

- Scalability planning: Systems built without scale in mind require costly rework later

What Drives Cost Beyond $150,000?

Once you move beyond MVP scope, costs increase due to:

- Multi-region regulatory compliance (EU, US, APAC)

- SWIFT and real-time payment rail integrations

- Advanced liquidity forecasting (AI/ML models)

- 24/7 real-time processing infrastructure

- Enterprise-grade security and audit systems

If you’re evaluating scope or budget, it’s worth mapping your corridors, integrations, and compliance needs early. Intellivon’s team can help you define a realistic build plan and cost estimate aligned with your growth stage.

Conclusion

Effective cross-border liquidity management transforms fragmented treasury operations into a unified strategic engine. By addressing architectural complexity, regulatory hurdles, and integration depth, organizations can unlock trapped capital and drive global growth.

Partnering with a specialist ensures your infrastructure remains resilient, compliant, and ready for the future of finance.

Build Cross-Border Liquidity Software With Intellivon

Engineering a global liquidity management system is a specialized discipline that sits at the intersection of high-frequency distributed systems and rigorous financial regulation.

At Intellivon, we architect the high-trust digital rails that allow global enterprises to move capital at the speed of the internet. Our approach turns the complexities of multi-bank orchestration and AI into a seamless competitive advantage for your organization.

A. Bridging Fragmented Banking

We integrate fragmented global partners into one programmable interface. Our middleware ensures real-time visibility and unified control across banking grids.

B. Predictive Liquidity Intelligence

Our AI handles variables that erode margins. We automate cash positioning, optimize FX execution, and eliminate manual reconciliation through machine learning.

C. Regulatory and Global Resilience

We build compliance into the source code, ensuring your platform adapts to regional laws. Our high-concurrency stack handles massive volumes without lag.

| Milestone | Priority | Value |

| Launch | Core Rails | Trust |

| Growth | Scaling | Stability |

| Mature | AI Optimization | Margins |

Contact Intellivon today to transform your vision into production-ready reality.

FAQs

Q1. What is cross-border liquidity management software?

A1. This technology platform provides real-time visibility and automated control over cash balances and fund movements across multiple currencies and jurisdictions.

It replaces manual treasury tasks with automated sweeping and intelligent routing. Unlike standard reporting tools, it executes payments autonomously to optimize global capital efficiency and reduce idle balances.

Q2. How much does it cost to build a cross-border liquidity platform?

A2. A production-grade platform costs between $350,000 and $2,500,000+. A focused MVP covering core visibility and FX optimization typically requires $350,000–$650,000. Full-scale systems with global compliance and AI forecasting layers reach the higher range, with ongoing annual infrastructure costs adding $100,000–$300,000 post-launch.

Q3. How long does it take to build a cross-border liquidity management platform?

A3. Development usually spans 9 to 20 months. An experienced team can deliver a core MVP in 9–12 months. However, full-scale platforms covering 10+ markets with advanced compliance layers require 14–20 months. Timeline risks often stem from complex bank API integrations and regional regulatory approval processes.

Q4. What is the difference between a liquidity management platform and a TMS?

A4. A Treasury Management System (TMS) focuses on reporting and forecasting positions in batches. Conversely, a liquidity management platform is an execution engine that moves money in real time. While a TMS shows where capital is, a liquidity platform actively optimizes it using autonomous rules and real-time signals.

Q5. What integrations are required for a cross-border liquidity platform?

A5. Platforms require four key integrations: bank APIs for balance data, payment networks like SWIFT or SEPA, FX provider APIs for rates, and compliance services for AML screening. Each new jurisdiction requires additional local rail integrations. These technical connections typically account for 40–60% of the total project build time.