Key Takeaways:

-

AI AML copilot costs $60,000 to $250,000, depending on integrations, AI depth, and compliance controls.

-

A focused MVP supports evidence retrieval, alert summaries, policy search, and controlled SAR drafting.

-

Production builds add KYC context, sanctions inputs, entity analysis, governed RAG, and audit trails.

-

Annual maintenance should be planned at 18 to 25% of the initial build cost.

-

How Intellivon builds AML copilots as a controlled compliance infrastructure where accountable officers retain all final decisions.

Regulatory pressure on banks is constantly mounting, and banks that have already built AI AML compliance copilots are handling both at a fraction of the cost you are currently paying to manage them manually. Building an AI AML compliance copilot costs between $60,000 and $250,000, depending on which modules you build, whether the LLM runs on private infrastructure or a cloud API, and how many core banking systems need integration.

The number that actually determines your build decision is not the upfront cost but what you are currently spending to manage the same alert volume manually, and for most institutions, that number is significantly higher.

Intellivon has built fintech AI systems for a decade, with costs laid out from the first conversation. This blog breaks down every development phase, what drives cost within each, the ongoing maintenance figure your business case needs, and an ROI comparison against commercial licensing. By the end, you have a complete cost framework ready to take into a build decision.

What is An AI AML Compliance Copilot?

An AI AML compliance copilot is a decision-support system built into a bank’s existing AML infrastructure to improve investigation throughput, evidence quality, and reporting preparation.

The cost conversation differs from buying a generic AI tool because compliance accountability stays with your team regardless of what the platform automates.

1. What the Copilot Improves

Financial institutions already run transaction monitoring, KYC, sanctions screening, and SAR workflows. Specifically, the copilot improves three things within these existing systems.

- Alert review speed and prioritization

- Evidence retrieval and case summarization

- SAR narrative and CTR workflow preparation

2. Why the Cost Conversation Is Different

Unlike a generic AI assistant, an AML copilot carries governance, audit trail, and model validation obligations that shape the build budget directly.

- Operational savings come from reduced investigation time per alert

- Regulatory accountability stays with the compliance officer at every filing decision

- Maintenance costs reflect ongoing model monitoring and regulatory updates

HSBC’s implementation with Google Cloud demonstrates production-scale impact. HSBC screens more than 1.2 billion transactions monthly, reduced alert volumes by more than 60%, and identified two to four times more confirmed suspicious activity. This is a named example, not a guaranteed outcome for every institution.

The investment case begins with the investigation workload and evidence quality. However, approving a build budget needs a clear definition of what the copilot will and will not do.

What Is an AI AML Compliance Copilot Built to Do?

An AI AML compliance copilot is a controlled assistance layer that helps compliance teams investigate alerts, retrieve supporting evidence, connect customer and transaction context, prepare case summaries, and draft SAR narratives for review.

At the same time, it supports the people making decisions rather than making those decisions themselves. Additionally, the compliance officer still reviews, approves, and files everything that carries regulatory weight.

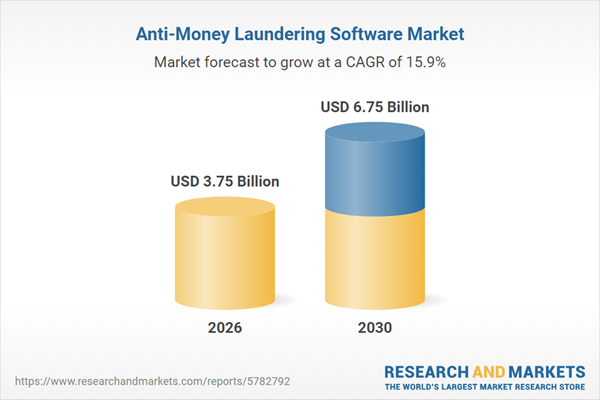

The AML software market is valued at $3.75B in 2026, projected to reach $6.75B by 2030 at 15.9% CAGR, driving banks to evaluate AI copilots for measurable productivity and regulatory defensibility.

Think of it this way: the copilot does the research, and your team does the deciding.

The table below shows exactly where the copilot helps, where human control must stay, and what each workflow costs to build.

Workflow Coverage Table

| AML Workflow | What the Copilot Can Support | What Must Stay With Your Team | What This Costs to Build |

| Alert triage | Rank alerts, summarize risk signals, and pull together evidence | Review anything flagged for escalation | Alert triage system development cost |

| KYC and CDD review | Retrieve customer profiles, ownership records, and prior review history | Confirm discrepancies and final risk decisions | KYC automation development cost; CDD workflow automation cost |

| Sanctions and PEP checks | Display match results and context from approved data providers | Resolve potential matches and escalation actions | Sanctions screening integration cost; PEP screening integration cost |

| Adverse media review | Retrieve and sort relevant articles or risk indicators | Confirm whether something is material | Adverse media API integration cost |

| Entity relationship analysis | Show links between accounts, customers, counterparties, and transactions | Interpret suspicious networks and case relevance | Entity resolution system cost; graph analytics implementation cost |

| SAR preparation | Draft narrative sections from approved evidence | Edit, approve, and file the SAR | SAR automation software development cost |

| Audit review | Preserve all inputs, outputs, approvals, and model versions | Approve evidence standards and examination responses | Audit trail system development cost |

This boundary matters for regulatory reasons, too. Consequently, the FFIEC BSA/AML Examination Manual defines suspicious-activity monitoring as five connected steps:

- Identifying unusual activity

- Managing alerts

- Making SAR decisions

- Completing and filing SARs

- Monitoring continuing activity

A copilot can support the first two steps significantly. The final three, however, must remain under documented human authority.

A copilot improves the investigative and documentation layers around AML decisions. Once the workflow boundary is defined, leaders can estimate which investment tier matches their actual operating need.

AI AML Compliance Copilot Cost: What Should Banks Budget?

An AI AML compliance copilot platform typically costs $60,000–$250,000 to build, depending on workflow scope, integrations, data readiness, AI model requirements, security controls, validation depth, and deployment complexity.

The lower range supports a focused investigation assistant. Additionally, the upper range supports a production-ready copilot integrated with broader compliance operations and governed AI workflows.

This targeted deployment model ensures compliance team velocity increases while managing the compliance AI total cost of ownership.

1. Cost Range by Solution Scope

| Solution Tier | What the Build Includes | Estimated Development Cost | Estimated Timeline |

| Focused AI AML Copilot MVP | Policy and evidence search, alert summaries, controlled SAR drafting, analyst dashboard, basic audit logging, one or two source connections | $60,000–$100,000 | 10–16 weeks |

| Integrated AML Investigation Copilot | Alert context, KYC/CDD records, sanctions or PEP inputs, case-management connection, governed RAG, reviewer workflows, detailed audit trails | $100,000–$175,000 | 16–24 weeks |

| Production-Ready Enterprise Copilot | Broader integrations, entity relationship views, graph-supported investigation context, advanced validation controls, MLOps, reporting support, security hardening | $175,000–$250,000 | 24–32 weeks |

The $60,000–$250,000 range prices a custom AML copilot that enhances investigation, review, reporting preparation, and governance workflows.

However, it does not represent a complete replacement for a bank-wide transaction-monitoring engine covering every product, payment rail, jurisdiction, entity type, or digital-asset risk programme.

Instead, it layers over existing core architecture to drive operational efficiency.

2. Bank AML AI Development Cost Breakdown

| AML Platform Development Phase | Estimated Cost Range | What the Phase Covers |

| Workflow discovery and compliance-control mapping | $5,000–$15,000 | Alert types, reviewer roles, SAR workflow, approval rules, evidence requirements, audit scope, MVP plan |

| Data preparation and entity context foundation | $10,000–$40,000 | Customer records, transaction context, KYC/CDD data, case history, entity matching, data normalisation |

| AI copilot and evidence-retrieval layer | $15,000–$55,000 | RAG pipeline, policy search, case summarisation, evidence retrieval, controlled SAR narrative assistance |

| AML and banking integrations | $10,000–$45,000 | Core banking, transaction monitoring, sanctions, PEP, adverse media, case management, reporting workflow |

| Compliance controls, validation, and security | $10,000–$45,000 | Human approvals, output logging, access controls, validation testing, explainability, audit evidence, security checks |

| Deployment, MLOps, analyst testing, and enablement | $5,000–$25,000 | Hosting, monitoring, release control, drift review setup, user acceptance testing, analyst training |

| Controlled implementation reserve | $5,000–$25,000 | Data remediation, connector limitations, policy revisions, additional testing, reporting adjustments |

3. AI Build Cost Breakdown

When analyzing the bank’s AML AI development cost breakdown, technical complexity drives the budget variation. As a result, the ultimate compliance AI build cost breakdown is shaped by three distinct deployment tiers:

- Focused MVP ($60,000–$100,000): This model remains closer to the minimum budget threshold because it limits integrations and minimizes workflow coverage.

- Integrated Copilot ($100,000–$175,000): This middle tier commonly enters a higher range because it connects evidence sources and establishes formal reviewer workflows.

- Production-Ready Build ($175,000–$250,000): This enterprise level represents the peak AML compliance AI software development cost because the institution adds stronger validation, entity analysis, broader integrations, controlled reporting support, monitoring, and governance controls.

4. Annual Maintenance Cost

Annual maintenance should be planned at 18–25% of the original build cost to maintain system integrity.

Cost Table

| Initial Build Cost | Annual Maintenance at 18% | Annual Maintenance at 25% |

| $60,000 | $10,800 | $15,000 |

| $100,000 | $18,000 | $25,000 |

| $175,000 | $31,500 | $43,750 |

| $250,000 | $45,000 | $62,500 |

5. Ongoing Maintenance Cost Factors

Consequently, this ongoing maintenance cost of the AML platform scope requires a structured operational budget. Specifically, the recurring investment covers the following operational layers:

- Model and retrieval-output evaluation.

- Data quality monitoring.

- API and vendor-source changes.

- Security updates and access reviews.

- Audit-log retention and reporting updates.

- Model drift monitoring cost parameters.

- Prompt and output-control testing.

- Regulatory workflow changes.

- Cloud deployment or private hosting operations.

- Analyst feedback and MLOps pipeline cost AML infrastructure required for continuous drift review.

Ultimately, the user interface does not create most of the budget. Data access, evidence grounding, integrations, validation, security, and governance do. Therefore, the next section will show exactly which workflow capabilities belong at each investment tier.

Which AML Copilot Capabilities Fit Each Budget Tier?

The correct feature set depends entirely on how much operational responsibility the copilot will support within your bank’s compliance ecosystem. A $60,000 MVP focuses on improving narrow, review-heavy tasks without introducing governance complexity. Conversely, a $250,000 production build connects extensive AML evidence sources, automates analyst escalation loops, maps relationship context, and deploys rigorous model monitoring controls while maintaining human accountability.

Capability-by-Budget Tiering

| Capability | $60K–$100K MVP | $100K–$175K Integrated Copilot | $175K–$250K Production-Ready Copilot |

| Policy and procedure retrieval | Included | Included | Included with version control and access rules |

| Alert evidence summary | Included for selected alerts | Included across connected workflows | Included with advanced review routing |

| SAR narrative assistance | Controlled drafts | Evidence-grounded drafts with reviewer workflow | Controlled drafts with stronger validation and reporting linkage |

| KYC/CDD context | Limited connection or uploaded evidence | Connected customer-risk context | Broader entity and relationship context |

| Sanctions and PEP context | Optional single-provider connection | Connected approved providers | Broader screening context and escalation records |

| Adverse media context | Optional | API-supported retrieval | API-supported workflow with audit evidence |

| Entity relationship view | Basic or excluded | Limited relationship mapping | Graph-supported investigation context |

| Case-management integration | Basic export or one workflow | Included | Included with workflow routing and escalation controls |

| Audit logs | Core activity logs | Detailed user and output history | Full traceability, approval history, versioning, and monitoring |

| Model and output testing | Basic UAT and output checks | Formal evaluation plan | Stronger validation, drift checks, and release controls |

| MLOps and monitoring | Basic production monitoring | Included | Expanded operational monitoring and change management |

Importantly, selecting a lower-tier budget does not imply a reduction in engineering quality or mathematical accuracy. Instead, these implementation tiers scale dynamically based on the following structural criteria:

- Architectural Scope: The total number of separate operating environments and custom user interfaces required.

- Connected Core Systems: The number of live core banking platforms, transaction systems, and external databases that must sync in real-time.

- Historical Evidence Depth: The volume and formatting complexity of unstructured compliance records ingested into the retrieval layer.

- Governance Workload Volume: The complexity of the internal multi-tiered approval paths and specialized reporting pipelines.

Consequently, an entry-level build uses the exact same rigorous security standards as an enterprise installation but limits its operational footprint to a standalone investigative workbench.

Ultimately, each added capability creates specific technical and data dependencies within your infrastructure:

- Alert Summarization: Demands highly clean source data feeds and structured schema mapping to prevent model hallucinations.

- Entity Relationship Views: Requires advanced graph database logic and identity resolution pipelines to map complex transaction paths.

- Automated Reporting Assistance: Relies on multi-stage human approval workflows, cryptographic audit logs, and fine-grained access control permissions.

The upcoming architecture breakdown makes these backend system dependencies visible.

Which Architecture Layers Drive AI AML Compliance Copilot Development Cost?

An institutional AI AML compliance copilot platform development cost is fundamentally shaped by six core architectural layers: data ingestion, entity context, risk and investigation intelligence, evidence-grounded language assistance, workflow integrations, and governance operations. Each independent layer supports a distinct regulatory or operational compliance need.

Consequently, removing a single layer might decrease initial engineering hours, but it simultaneously introduces structural risks by limiting evidence quality, analyst system utility, or audit defensibility.

Architecture Layer Spend Allocation

| Architecture Layer | What It Does | Cost Drivers | Why It Matters |

| Data Ingestion and Normalisation | Collects customer, transaction, alert, KYC/CDD, case, and reporting records. | Core banking integration cost, SWIFT transaction monitoring connection fees, cloud deployment cost, compliance AI allocations. | The copilot cannot produce reliable narrative summaries from structurally inconsistent records. |

| Identity and Entity Context Layer | Resolves linked customers, beneficial owners, accounts, counterparties, businesses, and relationships. | Entity resolution system cost, graph analytics implementation cost, and graph neural networks AML data formatting. | Investigators require a holistic relationship context rather than analyzing isolated, disparate transaction alerts. |

| Alert and Investigation Intelligence Layer | Supports prioritisation, typology signals, risk context, and automated investigator queues. | Alert triage system development cost, AML model training cost, transactional risk scoring models optimization. | Compliance teams require enhanced prioritization to optimize the alert-to-SAR conversion rate. |

| Governed RAG and LLM Assistance Layer | Retrieves approved evidence before drafting case summaries or mandatory narratives. | RAG pipeline development cost, LLM fine-tuning cost, compliance parameters, and private model hosting cost. | Generated reporting text must remain strictly grounded in controlled, verifiable bank information. |

| Compliance Workflow Integration Layer | Connects KYC/CDD, sanctions, PEP, adverse media, case management, SAR, and reporting operations. | Sanctions screening automation cost, OFAC compliance module cost, and regulatory reporting automation cost. | System value comes from fitting into existing legacy compliance workflows and case management engines. |

| Governance, Security, and Monitoring Layer | Preserves permissions, immutable logs, models, output testing, release history, drift signals, and approvals. | Model validation cost, audit trail system development cost, SOC 2 compliance implementation cost, and zero-trust architecture fintech cost. | Production financial AI must remain fully reviewable, explainable, and controlled under regulatory scrutiny. |

Building these systems requires an intimate knowledge of regulated transaction flows.

Ultimately, these layers must align directly with strict institutional playbooks to withstand regulatory examinations

- Data Engineering Realities: Ingestion and normalization consume a significant portion of the timeline because financial data fields vary across legacy databases.

- Graph Resolution Needs: Constructing the entity context layer prevents the copilot from evaluating transactions in isolation, which reduces overall false positive rates.

- Deterministic Guardrails: The integration layer ensures that generative outputs cannot bypass standard banking controls, enforcing strict human-in-the-loop review.

Architecture determines whether the copilot can securely retrieve evidence, explain its internal risk calculations, and survive intense regulatory audit scrutiny. However, technical architecture alone does not answer which specific intelligence methods are worth funding.

The next section will separate complex, model-driven machine learning work from basic deterministic database checks.

Which AI Models Should an AML Copilot Use?

An AML copilot should combine deterministic screening controls, machine learning, entity resolution, graph analytics, governed retrieval, and limited language-model assistance. Banks should use AI where evidence volume and investigation complexity create meaningful manual effort.

They should retain controlled rules and human approval wherever decisions require exact matching, formal escalation, or regulatory filing accountability.

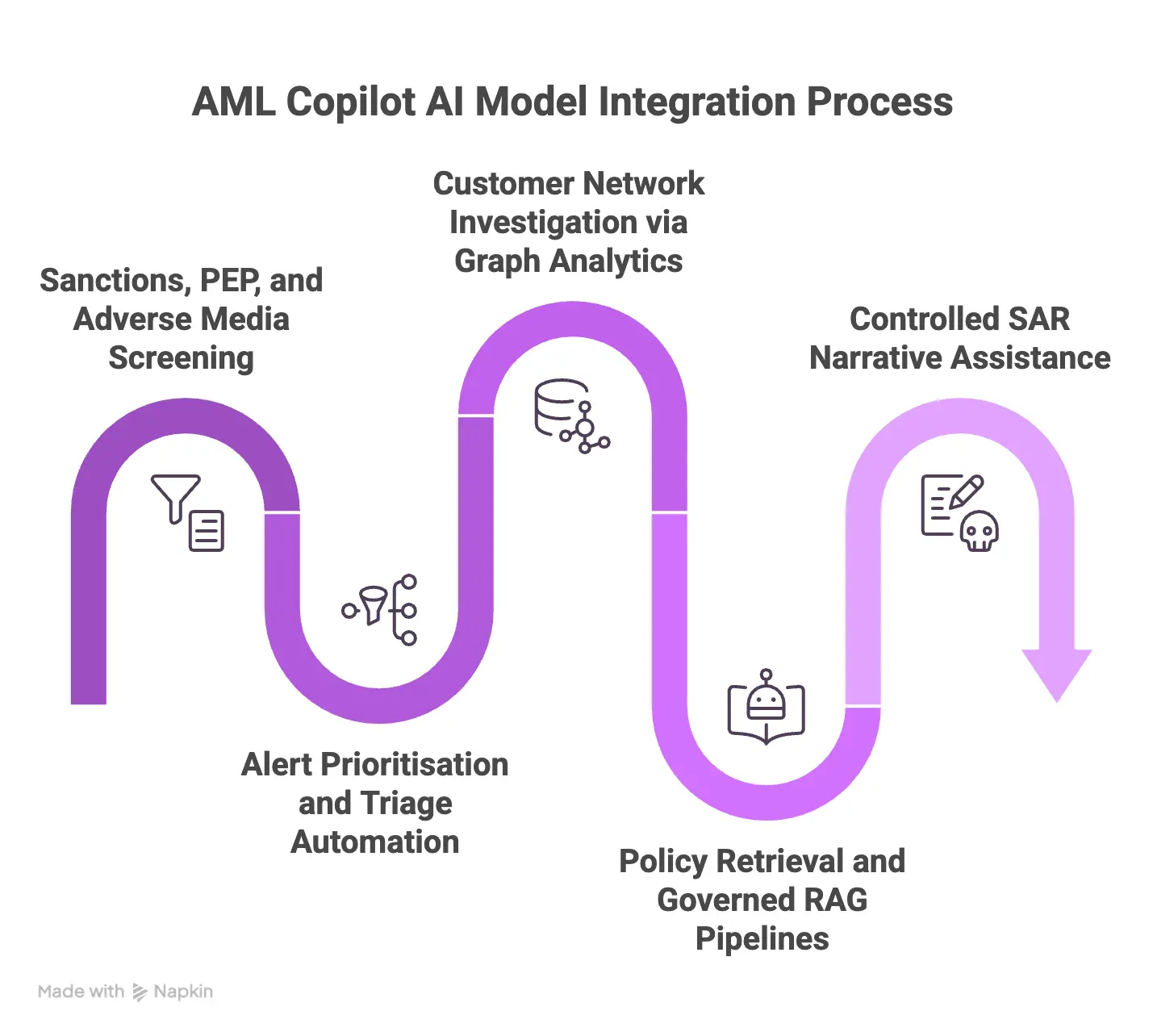

1. Sanctions, PEP, and Adverse Media Screening

Screening workflows depend heavily on absolute data integrity, historical consistency, and reproducible review evidence.

- The Technical Approach: These tasks rely on approved external data provider APIs coupled with deterministic fuzzy-name matching algorithms and secondary relevance classification models.

- Operational Integration: The system passes incoming names against official lists, while a light natural language processing layer filters out unrelated unstructured data. This layout ensures analysts only evaluate genuine risk matches.

- The Budget Factor: Engineering teams must clarify the exact third-party vendor connection fees and API integration costs before finalizing the software design.

2. Alert Prioritisation and Triage Automation

Processing high volumes of system-generated transaction alerts requires an intelligent mechanism to rank risk severity.

- The Technical Approach: This layer employs interpretable machine learning ranking models trained on historical case outcomes and specialized financial crime typologies.

- Operational Integration: The algorithm calculates a risk priority score based on past analyst behavior, alert history, and data anomalies. This prioritization directly increases the overall alert-to-SAR conversion rate.

- The Budget Factor: This model introduces a distinct model validation cost, as internal risk management units must formally review the scoring weights to prevent unintended algorithmic drift.

3. Customer Network Investigation via Graph Analytics

Uncovering hidden financial patterns like structuring, layering, or shell company networks requires analyzing systemic connection points.

- The Technical Approach: This infrastructure blends advanced entity resolution software with graph neural networks and AML frameworks.

- Operational Integration: The platform links separate accounts, shared addresses, beneficial owners, and cross-border wire transfers into a singular visual entity profile. This approach provides an immediate view of counterparty risk.

- The Budget Factor: Implementing this visualization capability drives up the graph analytics implementation cost, which scales depending on data normalization depth and transaction volume.

4. Policy Retrieval and Governed RAG Pipelines

When investigators draft case summaries, the extracted background information must remain completely accurate and legally sound.

- The Technical Approach: This layer utilizes a strict retrieval-augmented generation compliance structure using internal bank manuals, FinCEN regulations, and FATF recommendations.

- Operational Integration: The RAG pipeline development cost provides an alternative to expensive model training by locating relevant regulatory updates and anchoring the AI’s data access.

- The Budget Factor: Banks can completely avoid initial LLM fine-tuning cost compliance parameters by relying on a governed RAG pipeline to pull static text, which also controls the private model hosting cost.

5. Controlled SAR Narrative Assistance

The final stage of the investigation workflow involves compiling complex summaries for suspicious activity reporting.

- The Technical Approach: This application uses large language models solely as drafting assistance utilities under a rigid human-in-the-loop workflow cost structure.

- Operational Integration: The assistant reads verified case folder notes and structures an initial regulatory narrative template, complete with evidence citations.

- The Budget Factor: To maintain absolute defensibility, the software records all original model outputs alongside final human edits, factoring into the explainable AI implementation cost.

The correct model mix avoids forcing every AML task into generative AI. Yet model selection still needs a controlled delivery process.

What Is the ROI of Building an AI AML Compliance Copilot?

The financial return of an AI AML compliance copilot platform is realized through direct operational cost reductions, increased analyst capacity, and lower regulatory risk exposure. Historically, legacy transaction screening software forces financial institutions to waste valuable resources clearing non-actionable alerts.

By deploying an intelligent, evidence-grounded layer, banks can significantly compress investigation cycle times while simultaneously improving their overall risk detection accuracy.

1. Baseline Financial Impact Metrics

| Metric Category | Baseline Legacy Performance | Post-AI Copilot Performance | Measurable Business Value |

| False Positive Alert Volume | 85% – 95% of total flags (Facctum, 2026) | 70% reduction in false positives (Hawk AI, 2025) | Eliminates hours spent on low-risk investigations. |

| Suspicious Activity Detection | Baseline rules-based limits | Up to 40% identification improvement (McKinsey & Company) | Uncovers hidden risk patterns and financial crime networks. |

| Annual Operational Expense | Linear headcount cost scaling | Up to 25% total compliance cost savings (KPMG) | Delivers operational scale without adding permanent staff. |

| Account Validation Rejections | High manual review bottleneck | 15% – 20% reduction in rejection rates (J.P. Morgan, 2025) | Drives frictionless onboarding and faster client conversion. |

2. Operational Efficiency and Headcount Scale

Manually investigating thousands of false positive flags annually drains capital and limits compliance team agility.

- Alert Triage Acceleration: A custom copilot optimizes internal queues by scoring alerts based on historical case data, which prevents level-one analysts from reviewing redundant system noise.

- SAR Narrative Drafting: Automating the initial compilation of complex reporting text saves hours per case, directly compressing the standard alert-to-SAR conversion timeline.

- Perpetual Customer Reviews: Shifting from periodic customer due diligence reviews to continuous monitoring prevents sudden risk exposure without overloading your staff.

3. Risk Mitigation and Regulatory Cost Avoidance

Failing to identify complex financial crime structures leads to catastrophic regulatory penalties and severe institutional reputational damage.

- Hidden Typology Detection: Advanced graph neural networks AML models link seemingly unrelated accounts and wire transfers to immediately identify complex money mule rings.

- Audit Trail Immutability: The copilot captures all underlying retrieval evidence, system risk calculations, and human modifications within a cryptographic log structure.

- Defensible Model Validation: Maintaining fully explainable AI outputs ensures the entire automated system easily survives strict regulatory examinations.

Ultimately, building a custom copilot balances software development costs with immediate, long-term efficiency gains. This strategy ensures the institution improves operational velocity while defending against complex financial crime.

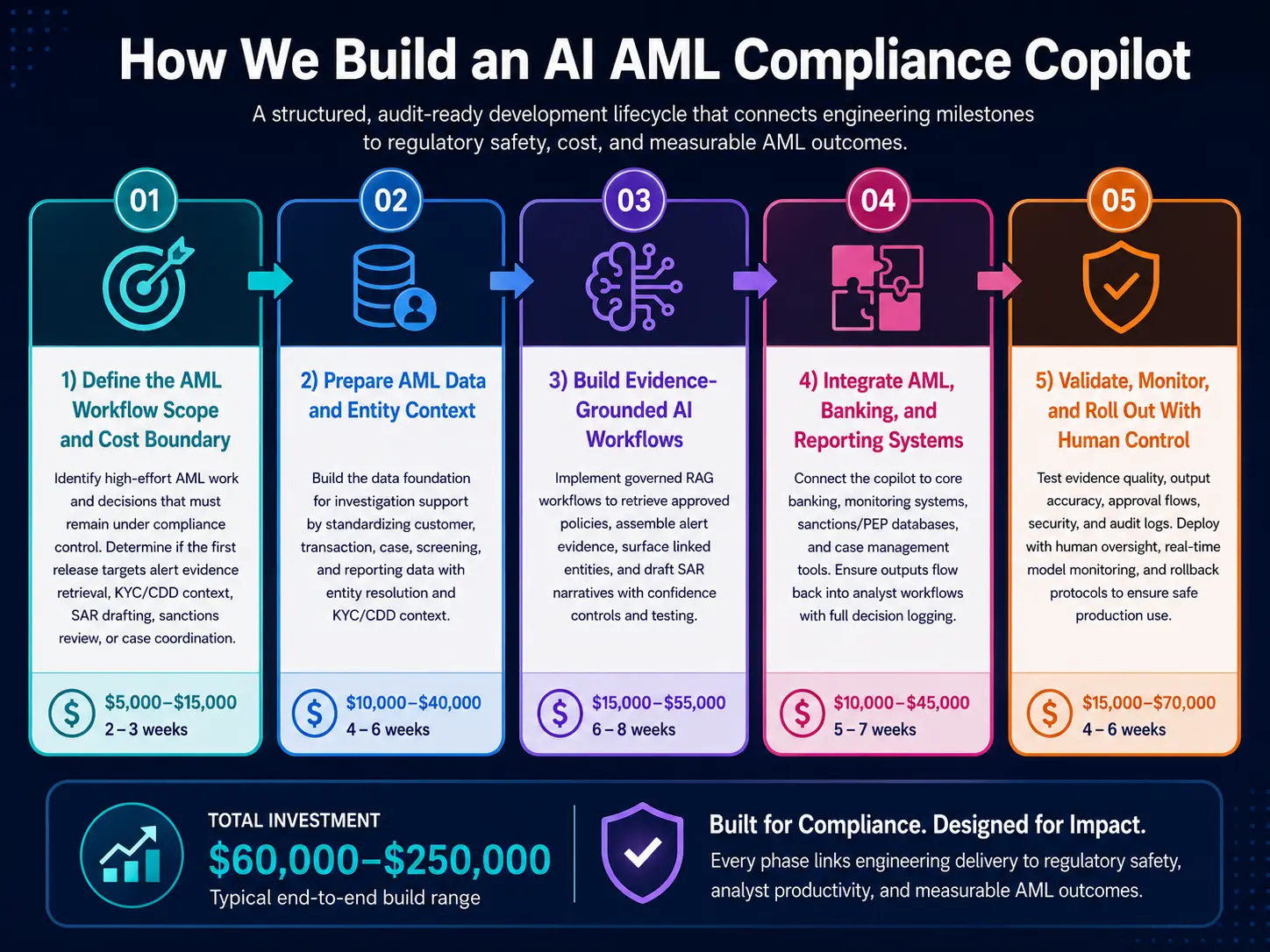

How We Build an AI AML Compliance Copilot

Implementing a resilient, audit-ready compliance copilot requires a structured development lifecycle that systematically links engineering milestones to regulatory safety nets. Moving from abstract project scoping to live banking operations demands specific phases where costs, data models, and human oversight checkpoints are explicitly defined.

This step-by-step roadmap details how financial institutions can execute a controlled deployment strategy that maximizes analyst output without introducing compliance vulnerabilities.

Step 1 — Define the AML Workflow Scope and Cost Boundary

The build should begin by identifying which AML work consumes the most investigator effort and which decisions must remain controlled by compliance officers.

This defines whether the first release addresses alert evidence retrieval, KYC/CDD context, SAR drafting, sanctions review support, adverse media, or case workflow coordination.

- Technical Coverage: Engineering leads must explicitly audit current alert categories, monthly alert review volumes, and the core transaction databases feeding into the alert triage pipeline. Furthermore, the scoping phase defines user roles, granular analyst approval rights, and existing case management connections to isolate clear MVP boundaries.

- Cost and Timeline: This discovery and compliance-control mapping phase typically requires an investment of $5,000–$15,000 and takes exactly 2 to 3 weeks to finalize.

Consequently, setting clear parameters ensures the development team targets structural workflow bottlenecks. Once the scope is defined, the next requirement is determining whether the available data can support reliable investigation assistance.

Step 2 — Prepare AML Data and Entity Context

An AML copilot can only support investigations when customer, transaction, case, screening, and reporting records can be retrieved in consistent forms. This step creates the data foundation required for evidence-backed summaries, entity comparison, customer-risk review, and later model testing.

- Technical Coverage: This architectural phase targets customer and account identifiers, historical KYC/CDD profiles, beneficial ownership data, and past SAR metadata. Engineers execute data normalization scripts to standardize disparate SWIFT strings and implement core entity matching rules to populate identity resolution engines.

- Cost and Timeline: Building out the data preparation and entity context layer costs between $10,000–$40,000 and requires 4 to 6 weeks of dedicated engineering time.

As a result, building controlled ingestion and entity-context pipelines prior to generating outputs ensures the copilot draws insights from fully traceable source records. After the evidence layer is reliable, AI functions can be selected around specific AML tasks.

Step 3 — Build Evidence-Grounded AI Workflows

The AI layer should be designed around repeatable investigator work rather than open-ended chatbot responses.

It can retrieve approved policies, assemble alert evidence, surface linked entities, prepare case summaries, and draft SAR narrative sections with supporting records attached for reviewer confirmation.

- Technical Coverage: Developers implement a governed RAG architecture that connects strictly to verified internal bank policies and regulatory source manuals. To prevent hallucinations, the software applies rigid prompt controls, enforces confidence thresholds, and runs continuous automated testing on all generated output drafts.

- Cost and Timeline: Engineering the core AI copilot logic and the evidence-retrieval engine requires a budget of $15,000–$55,000 and spans a 6 to 8-week development block.

Thus, utilizing language models solely where generated assistance optimizes manual narrative compilation keeps the system predictable. However, useful AI outputs only create business value when they connect to the compliance systems analysts already use.

Step 4 — Integrate AML, Banking, and Reporting Systems

Integration turns an AI model into an operational AML copilot. The platform must retrieve data from approved systems, return outputs to analyst workflows, preserve decision records, and support the reporting path without introducing uncontrolled filing or closure actions.

- Technical Coverage: This phase builds bidirectional API integrations connecting the copilot directly to core banking systems, third-party transaction monitoring tools, and approved sanctions or PEP screening databases. It also sets up secure pathways to pipe completed audit data straight into internal case management tools.

- Cost and Timeline: Achieving robust system integration and configuring specialized reporting automation loops costs $10,000–$45,000 and takes 5 to 7 weeks to implement.

By mapping precise integration rights, matching data fields, and establishing human approval checkpoints, the institution eliminates systemic software single points of failure. Once workflows connect end to end, validation and governance determine whether teams can deploy safely.

Step 5 — Validate, Monitor, and Roll Out With Human Control

Production rollout should begin only after the bank can test evidence retrieval, generated summaries, recommendation quality, approval flows, security controls, and audit logs.

The copilot must show what information supported its output and which person accepted, edited, escalated, or rejected its recommendation.

- Technical Coverage: Teams run rigorous user acceptance testing, multi-scenario hallucination tests, and thorough access-control reviews. Security engineers establish cryptographic audit logging frameworks, deploy real-time model drift monitoring dashboards, and prepare concrete system rollback protocols.

- Cost and Timeline: Executing the final validation, security hardening, and deployment phase costs $15,000–$70,000 and takes 4 to 6 weeks to finalize.

Packaging the final AI deployment with automated model monitoring tools ensures the bank retains full operational control over time.

A controlled delivery process keeps the $60,000–$250,000 budget connected to measurable AML outcomes and governance requirements.

One current regulatory development makes this design especially important: the treatment of generative and agentic AI after the April 2026 model-risk guidance updates.

What Does the April 2026 Reset Add to Your Copilot Budget?

A 2026 AML copilot budget should separate quantitative AML model governance from generative-AI copilot controls. Revised interagency model-risk guidance covers risk-based model development, validation, monitoring, governance, and third-party use.

However, the guidance states that generative AI and agentic AI models are outside its scope, creating a separate governance-design requirement for copilots.

1. Understanding the Interagency Recalibration

The Office of the Comptroller of the Currency (OCC), alongside the Federal Reserve and the FDIC, jointly announced revised supervisory guidance on model risk management on April 17, 2026.

- Target Asset Threshold: This updated framework primarily impacts institutions with more than $30 billion in total assets.

- Broader Market Impact: It simultaneously sets the operational tone for smaller financial institutions with material model-risk exposure.

- Generative Technology Exclusion: Crucially, the update narrows the definition of a quantitative model and explicitly excludes generative AI and agentic AI tools.

- Validation Friction: Consequently, a banking organization cannot simply reuse a singular quantitative model-validation checklist to govern an LLM-based investigation workbench or an automated SAR narrative drafting helper.

Attempting to force generative linguistic engines through a validation path designed for numerical risk scoring creates immediate regulatory friction.

Therefore, procurement teams must structure separate budget lines for both the quantitative analytical layer and the generative assistance workflow to maintain full FFIEC examination readiness cost parameters.

2. Two-Lane Governance Budget Allocation

| Governance Lane | What It Covers | Controls the Budget Must Include |

| Quantitative AML Model Lane | Risk ranking, anomaly detection, transactional alert prioritisation, customer-risk scoring, and network relationship analysis. | Data testing, objective validation, performance thresholds, model drift monitoring cost metrics, challenger analysis, and model portfolio inventory registers. |

| Generative Copilot Lane | Regulatory policy retrieval, historical case summaries, text-based investigation guidance, and automated SAR narrative support drafting. | Approved-source grounding rules, prompt version controls, immutable output logging, continuous hallucination testing, and human approval gates. |

Operating these dual governance structures requires a deliberate separation of your software infrastructure:

- Analytical System Tuning: This line ensures machine learning engines optimize alert triage using traditional mathematical validation techniques.

- Generative Grounding Controls: This lane ensures linguistic assistants remain strictly tethered to auditable source documents via explicit retrieval guardrails.

- Cryptographic Data Lineage: Both tracks must pipe execution histories into a centralized audit trail system development cost allocation block.

Ultimately, budgeting for comprehensive model risk management compliance cost variables upfront prevents costly system retrofitting down the line. Building a defensible, explainable AI implementation cost structure directly into your platform ensures your internal compliance reviewers can confidently explain every step of an investigation.

Once leaders understand this additional budget layer, they can compare real market examples and decide which implementation approach fits their institution.

AI AML Platform Build vs Buy Cost: What Should Leaders Compare Over Three Years?

An AI AML platform build vs buy cost should be evaluated thoroughly through three-year cumulative ownership, exact workflow fit, governance evidence depth, integration control, and long-term change-management effort. Commercial vendor software may allow an institution to launch faster for standard requirements.

Conversely, a custom copilot becomes significantly more defensible when the bank requires controlled workflows, owned data integrations, institution-specific evidence retrieval pipelines, or absolute transparency over localized AI behavior.

Three-Year TCO Evaluation Framework

| Decision Factor | Vendor AML Copilot or AI Platform | Custom AI AML Compliance Copilot | Procurement Question |

| Initial Implementation Cost | Upfront subscription fees, configuration markup, onboarding overhead, and implementation fees. | $60,000–$250,000 dedicated full-stack development budget. | Which specific services, data connectors, and custom controls are included in the year-one fee? |

| Licence or Usage Charges | Varies unpredictably by seat count, customer volume, alert spikes, ingested parties, or model experiments. | In-house hosting and software operational costs remain strictly institution-defined. | What specific pricing metric grows exponentially as our transactional usage expands? |

| Workflow Fit | Product-defined templates, rigid out-of-the-box user interfaces, and configurable options. | Designed natively around your institution-specific review and escalation procedures. | Will the platform natively fit the bank’s real, audit-approved SAR and internal approval process? |

| Integration Ownership | Dependency on vendor connectors, black-box data pipelines, and paid change requests. | Controlled integration roadmap, fully owned data models, and direct code base access. | Who handles future core source-system changes, schema modifications, and banking upgrades? |

| AI Evidence & Explainability | Closed vendor artifacts, proprietary testing regimes, and standard pre-packaged reporting scope. | Custom evidence generation, granular database logs, tailored test plans, and immutable approval records. | What underlying data can our internal validation team and regulatory examiners actually review? |

| Governance Updates | Dependent entirely on the vendor’s public product roadmap and multi-tenant release schedule. | Institution-approved release cycles, dedicated environments, and customized monitoring frameworks. | Who owns the generative-AI prompt control and model protection updates? |

| Exit and Portability | Contract-dependent database exports, manual migrations, and vendor lock-in risks. | The banking institution fully controls all implementation assets, data layers, and migration plans. | Can our complete historical investigation and evidence trail move cleanly to another environment? |

| Annual TCO Model | Compounding licence cost structures, API call surcharges, tiered support, and internal oversight. | 18–25% standard annual maintenance cost plus baseline internal oversight allocations. | Which option produces the clearer, more predictable three-year cash flow forecasting model? |

Custom vs Commercial

Weighing a custom vs. a commercial AML platform involves looking closely at your underlying infrastructure complexity.

- Vendor Scaling Penalties: Opting for third-party tools often yields a deceptive initial build vs buy AML software ROI because the vendor AML software licensing cost escalates rapidly alongside transactional growth, creating an unpredictable AML AI platform scalability cost.

- Custom Maintenance Efficiency: Building internally anchors your long-term expenditure to a stable AML compliance AI total cost of ownership baseline since maintenance maps directly to your existing internal DevOps structure.

- Localization Realities: Custom engineering lets you bypass the multi-jurisdiction compliance cost add-ons that commercial platforms routinely charge for multi-regional alert tuning.

A commercial vendor platform may suit a highly standardized operation or an exceptionally urgent deployment timeline. However, a custom software build fits a bank that demands absolute control over data lineage, case evidence, backend system integrations, and multi-layered compliance governance.

Finance leaders must therefore evaluate both distinct implementation routes through measurable workflow returns.

Build an AI AML Copilot Roadmap With Intellivon

An AML copilot business case needs more than a price estimate. It needs a defined workflow scope, connected evidence sources, AI model boundaries, reviewer authority, governance ownership, annual operating costs, and measurable ROI assumptions. Intellivon helps banking and fintech teams turn these requirements into a phased roadmap for controlled AML automation.

Intellivon can help your team:

- Prioritise alert triage, KYC/CDD review, case summarisation, or SAR drafting based on evidence availability and compliance risk.

- Map core banking, transaction monitoring, KYC/CDD, sanctions, case-management, and regulatory reporting integrations.

- Design evidence-grounded AI, RAG workflows, validation controls, SAR confidentiality safeguards, audit trails, and human-review checkpoints.

- Build a three-year cost, maintenance, rollout, and ROI case for executive or board approval.

If your bank, credit union, digital bank, or fintech platform is evaluating a custom AI AML compliance copilot, Intellivon can structure its architecture, implementation budget, governance requirements, and phased production roadmap before development begins.

Conclusion

A custom AI AML compliance copilot cost estimate should begin at $60,000–$250,000, depending on workflow depth, connected banking systems, validation, and security controls. While a focused copilot improves immediate evidence retrieval, an integrated build scales across complex reviewer workflows.

Ultimately, the choice between build-versus-buy should be tested through three-year total ownership costs and measurable operational ROI, factoring in a clear 18–25% annual maintenance model.

Things To Know About AI AML Compliance Copilot Cost

Q1. How Much Does It Cost to Build an AML AI Platform for a Bank?

A1. A custom AI AML copilot typically costs $60,000–$250,000. A focused MVP supports evidence retrieval, alert summaries, controlled SAR drafting, and core audit logs. At the same time, an integrated or production-ready build adds KYC/CDD context, screening integrations, entity analysis, governed RAG, stronger testing, MLOps, and reporting-support workflows. A full bank-wide monitoring replacement requires a separate budget.

Q2. How Long Does AI AML Compliance Copilot Development Take?

A2. A focused AI AML copilot MVP usually takes 10–16 weeks. An integrated build connected to KYC/CDD records, screening sources, and case workflows commonly takes 16–24 weeks. However, a production-ready implementation with broader integrations, validation, monitoring, and security controls usually requires 24–32 weeks before controlled rollout.

Q3. Is an AI AML Platform Build vs Buy Cost Lower Over Three Years?

A3. Vendor software often costs less to launch when the institution needs standard workflows and faster implementation. At the same time, a custom copilot becomes more defensible when the bank needs controlled integrations, institution-specific evidence retrieval, data ownership, specialised review steps, or greater transparency over AI outputs. Additionally, the decision should compare three-year TCO, not initial expense alone.

Q4. How Should Banks Measure False Positive Reduction Without Missing Risk?

A4. Banks should measure false-positive reduction alongside high-risk escalation quality, analyst overrides, sampled missed-activity reviews, alert-to-SAR conversion, investigation time, case completeness, and cost per SAR. At the same time, cutting alerts alone does not prove operational value. Additionally, the business case becomes defensible only when lower review effort is paired with maintained or improved detection quality.

Q5. What Governance Question Changed for AML Copilots in 2026?

A5. The April 2026 revised model-risk guidance states that generative and agentic AI models are outside its scope. Therefore, procurement teams should ask how the copilot will govern retrieval, generated summaries, SAR drafting support, human approvals, sensitive data, monitoring, and audit logs separately from traditional quantitative AML model validation.