Key Takeaways:

- Banks build AI AML copilots by connecting core banking, KYC, payment, screening, and case-management data.

-

Transaction monitoring, entity resolution, graph analytics, RAG retrieval, and controlled SAR narrative generation are core requirements.

-

BSA/AML controls, FinCEN SAR workflows, audit trails, and model monitoring ensure regulatory compliance readiness.

-

Custom builds cost $60,000–$250,000, with 5 to 9 months for a controlled first release.

-

How Intellivon builds compliance-ready enterprise AI systems designed for governed financial intelligence and regulatory auditability.

Somewhere between the alert that needs reviewing and the SAR that needs filing, your compliance team might run out of working hours, and that is the gap AI AML compliance copilot development is built to cater to. Banks can develop an AI AML compliance copilot platform by combining a transaction monitoring engine, an LLM-based alert triage and SAR generation layer, and a KYC/CDD processing module into their existing BSA/AML program. Each of these 3 layers targets a specific problem your compliance team is currently managing by hand.

The design decision that separates a platform that delivers ROI from one that gets abandoned is the AI-to-human escalation threshold. Without it calibrated as a compliance parameter, the platform eventually produces recommendations that your team stops trusting. Banks that design this layer correctly report throughput gains of 60–80%, with SAR filing backlogs cleared within 1 year.

Intellivon has built fintech AI systems for a decade, with a compliance architecture designed before the first sprint, not retrofitted after the first examination. This blog covers what the complete build looks like, including the architecture, development phases, cost by phase, and regulatory controls, all from scratch.

What Is an AI AML Compliance Copilot Platform?

An AI AML compliance copilot platform is a controlled decision-support system that sits inside your existing BSA/AML program and helps compliance officers move faster through alerts, investigations, and SAR preparation without taking over their filing authority. Essentially, it handles the volume so your team can focus on the judgment calls that actually require them.

1. What the Copilot Assists With

The platform takes on the tasks that consume the most investigator time first.

- Alert triage and prioritization

- Compliance case summarization

- KYC document review

- Customer Due Diligence automation

- Enhanced Due Diligence workflow preparation

- Beneficial ownership verification support

- SAR narrative generation

- CTR workflow support

- Regulatory change retrieval

2. What the Copilot Must Not Decide Alone

However, certain decisions must always stay with a human.

- Final SAR filing decision

- Automatic account closure

- Silent alert suppression

- Unreviewed sanctions clearance

- Autonomous regulatory submission

- Final adverse media disposition

That boundary is not a limitation of the technology. It is a regulatory requirement. HSBC’s deployment shows what happens when the boundary is respected correctly. Working with Google Cloud, HSBC screens more than 1.2 billion transactions monthly, cuts false-positive alerts by over 60%, and identifies 2 to 4 times more confirmed suspicious activity.

The value of an AML copilot is not that it replaces an investigator. Instead, it assembles evidence, ranks review effort, and improves decision quality while preserving accountable human sign-off.

Why Are Banks Evaluating AI AML Copilot Development Now?

Banks are evaluating AI AML compliance copilots because alert volumes, complex payment flows, customer-risk investigations, and regulatory documentation workloads now require faster evidence assembly and better prioritization. At the same time, regulators are emphasizing risk-based AML effectiveness, which makes measurable investigation quality more important than automating paperwork alone.

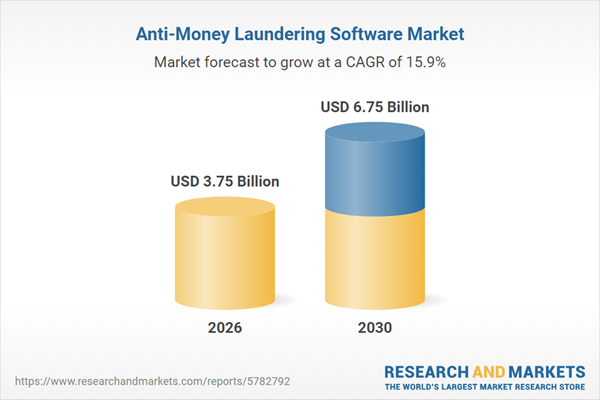

The AML software market is valued at $3.75B in 2026, projected to reach $6.75B by 2030 at 15.9% CAGR, driving banks to evaluate AI copilots for measurable productivity and regulatory defensibility.

1. Adoption is Accelerating

Only 18% of AML professionals have AI/ML in production, another 18% are piloting, and 25% plan implementation within 12–18 months, per a global survey of 850 ACAMS members.

Meanwhile, 58% of financial institutions have implemented AI-based AML solutions, with 78% planning to expand after successful pilots.

2. False positive reduction delivers immediate ROI

AI-powered AML systems reduce false positives by up to 50%, with one large retail bank achieving 33% reduction while maintaining 100% true positive recall, freeing 5 FTEs and saving 11,769 investigation hours annually.

At the same time, Industry data shows AI AML screening dropped false positive rates from 15% to 5%.

3. Efficiency gains and cost savings

AI systems increased monitoring efficiency by 60% in compliance departments, cutting investigation times by approximately 65%.

At the same time, AI compliance tools can automate up to 85% of routine checks, with solutions forecast to reduce overall compliance costs by up to 40%.

FinCEN’s April 2026 proposed rule requires risk-based, reasonably designed AML/CFT programs that prioritize higher-risk activities and demonstrate measurable effectiveness, and not just paperwork automation. This is a proposed rule, and not final, but banks still need defensible, evidence-backed controls today for exams.

Therefore, banks are increasingly evaluating AI AML copilots now because rising alert volumes meet regulator demands for demonstrable effectiveness, with proven ROI through 33–50% false positive reduction and 25–40% compliance cost savings.

[For a deeper breakdown of the regulatory foundation behind bank AI systems, see our guide on AI in Financial Risk Management: Custom Tools for Enterprise.]

Which AML Decision Should AI Assist First?

Banks should start AI AML compliance copilot development with workflows that collect and organize evidence before they automate workflows that influence regulatory filing decisions. Therefore, the best first release usually supports case summarization, alert context assembly, and reviewer prioritization, because these tasks reduce analyst effort while keeping filing authority with qualified compliance officers.

In order to pick your entry point safely, you can use the Evidence-Yield Prioritization Model. Consequently, this framework helps teams evaluate where an AI AML compliance copilot delivers the highest operational yield with the lowest compliance risk.

1. The Evidence-Yield Prioritization Model

Specifically, the table below outlines how a bank measures each core automation candidate across five critical decision factors before writing any code.

| Decision Factor | What the Bank Measures |

| Evidence availability | Can the platform retrieve reliable source documents and transactions? |

| Regulatory consequence | What happens if the AI output is incomplete or wrong? |

| Human review clarity | Can an analyst easily approve, reject, or correct the output? |

| Operational time saved | Does the workflow consume significant analyst hours today? |

| Measurable outcome | Can the bank track review time, escalation quality, or false-positive reduction? |

Furthermore, evaluating workflows this way prevents teams from building complex systems that regulators might reject during an examination. Instead, it forces a clear focus on immediate compliance officer productivity gains.

2. Recommended Automation Order

By applying these factors systematically, you can establish a clear roadmap for deployment, moving from low-risk assistance to high-complexity automation.

| Workflow | MVP Priority | Why |

| Case evidence gathering and summarization | Very High | High analyst burden; low autonomy risk when sources remain visible |

| Alert prioritization and disposition assistance | High | Improves queues while retaining human closure decisions |

| KYC/CDD questionnaire and document review | High | Speeds onboarding and review with clear source documents |

| SAR narrative drafting | Medium–High | Valuable, but every narrative needs evidence validation and analyst sign-off |

| Transaction monitoring model replacement | Later Phase | Requires validation, back-testing, threshold governance, and monitoring |

| Autonomous filing or automatic case closure | Exclude from MVP | Creates unacceptable accountability and examination exposure |

3. Our Decision Approach

To achieve this outcome, Intellivon maps your actual investigation time, data availability, alert disposition workflow, and regulatory exposure before choosing the first module. For example, we design the initial release to serve as a supportive tool that proves its accuracy before expanding into deeper transaction systems.

Ultimately, a bank does not need its first copilot release to make filing decisions. Rather, it needs that release to shorten the distance between an alert and a defensible human decision. Once the entry workflow is chosen, the platform must connect the complete AML investigation chain.

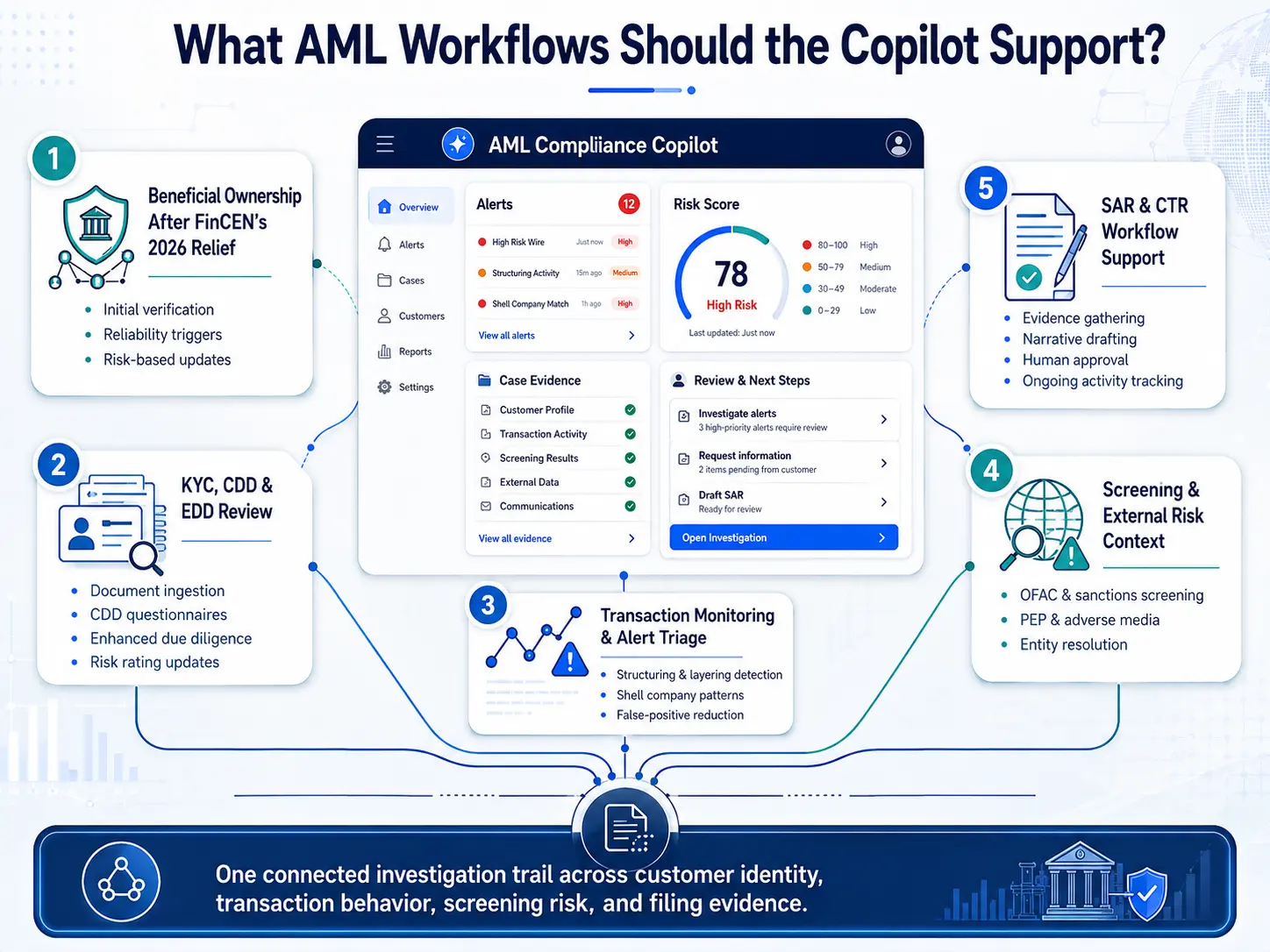

What AML Workflows Should the Copilot Support?

An enterprise AML copilot should support the full investigation path: customer onboarding review, customer risk scoring, transaction monitoring, screening, alert triage, case investigation, SAR preparation, regulatory filing support, and audit evidence retrieval.

The platform should connect these workflows rather than force analysts to investigate each risk signal in separate systems. Implementing an intelligent AML compliance software development approach guarantees that all background data points flow into a single, cohesive user interface.

1. Handle Beneficial Ownership After FinCEN’s 2026 Relief

The government recently changed the rules for tracking who owns a business. Banks no longer need to verify company owners every single time that a business opens a new bank account.

Therefore, your digital platform must adapt to a modern, trigger-based verification framework instead of running duplicative workflows.

- Initial Verification: The platform executes full identification and verification only when a legal entity customer opens their very first account.

- Reliability Triggers: The copilot flags cases automatically if an analyst uncovers new signatories, altered public registry data, or conflicting documentation.

- Risk-Based Updates: System workflows allow existing customers to confirm their status verbally or in writing during routine customer due diligence reviews.

This means your software can stop repeating the same paperwork over and over again. This official shift moves the focus from checking account-opening forms to maintaining dynamic, risk-based procedures, as detailed in the FinCEN 2026 Exceptive Relief Order.

2. KYC, CDD, and EDD Review

Building an AI KYC compliance copilot development module requires automating data ingestion from multiple unstructured files. The software reviews corporate registry filings, processes complex Customer Due Diligence questionnaires, and handles initial identity checks.

Furthermore, when a high-risk entity triggers Enhanced Due Diligence parameters, the copilot collects deep tax and corporate documents without manual intervention. It updates customer risk ratings across systems instantly based on the discovered risk profile.

3. Transaction Monitoring and Alert Triage

Deploying an AI-powered AML transaction monitoring platform allows banks to spot structural anomalies that traditional threshold rules miss. The system parses multi-layered transactions to uncover suspicious patterns like structuring, layering, and classic shell company activities.

Consequently, the alert triage module analyzes past investigator patterns to dismiss standard false positives automatically. This specific feature significantly drops the alert burden on human compliance teams.

4. Screening and External Risk Context

Sanctions screening automation must run continuously across dynamic global watchlists to ensure real-time security. The system integrates directly with Office of Foreign Assets Control datasets, Politically Exposed Persons registers, and global adverse media APIs.

Additionally, the software uses advanced entity resolution to match spelling variations and aliases to a singular legal identity. This ensures all external citations are linked directly into the permanent case record for audit purposes.

5. SAR and CTR Workflow Support

An AI SAR filing automation platform development focus streamlines the most text-heavy part of a compliance officer’s day. The system automatically gathers all transactional evidence and drafts a complete, narrative summary of the suspicious activity.

However, the human investigator retains absolute control to review, edit, and approve the narrative before electronic submission. The copilot also tracks continuous suspicious patterns to simplify mandatory 90-day updates, which aligns perfectly with standard filing protocols found in the FFIEC BSA/AML Examination Manual.

The copilot should connect customer identity, transaction behavior, screening risk, and filing evidence in one investigation trail. That trail becomes the design basis for architecture and integrations. Therefore, connecting these data structures properly remains the next critical milestone for technical teams.

Can an AI AML Copilot Process SAR Data Without Disclosure Risk?

Yes, an AI AML copilot can process SAR data without disclosure risk, but only if the bank hosts the AI model within its own secure network and completely blocks outside vendors from accessing the data. To prevent illegal leaks, the platform must use strict data walls, private model hosting, and zero-retention logging.

Consequently, protecting this confidentiality must shape your software setup before the AI ever writes a single sentence.

1. Separate Investigation Clues From Final Government Reports

To keep your files safe, the software must build a digital wall between your daily research data and the final reports you send to the government. At the same time, Investigators need to look at facts, but they should not mix raw data with official filings.

- Daily Research Clues: This includes account files, transaction logs, and notes about weird money patterns.

- Official Drafts and Filings: This includes the actual summaries written for the government and the final submission confirmations.

By keeping these files in separate digital folders, you can control exactly who gets to see them. For example, a regular clerk might see transaction logs, but only a senior officer should see the actual government report.

2. Keep Your Data Out of Public AI Systems

You should never let your data leave your own secure bank computers. If you use a public AI system, your private customer information could accidentally be leaked or used to train public models.

Therefore, your system should be built inside a private cloud environment that only your bank controls. Setting strict rules that stop the AI from saving or learning from your private text prompts is important. Additionally, the software should automatically scratch out Social Security numbers and names before sending text to the AI engine.

3. Track Employee Actions Safely for Bank Inspectors

Bank inspectors will eventually want to know exactly how your AI system works, but you cannot just hand them confidential government reports.

Therefore, the copilot must track the math and the steps your team took without exposing secret text.

The software keeps a clean diary of every action, showing who started a case, what evidence the AI used, and who approved the final text. This clear history proves to inspectors that you are following the rules in the FFIEC BSA/AML Examination Manual without breaking privacy laws.

What Evidence Must an AML Copilot Produce Before Human Review?

An AML copilot should never present a risk label or SAR draft without a reviewable evidence packet. Before an analyst accepts the recommendation, the platform should show the alert trigger, transaction timeline, customer context, related entities, detected typology, regulatory basis, cited source records, model confidence, and the reasons supporting escalation or closure. Therefore, providing this information clearly helps compliance workers make safe, fast choices.

Consequently, building a complete data summary helps banks avoid errors during manual investigations. The system arranges the background facts into clear blocks before any human review takes place.

A. The Automated Evidence Components

Specifically, the table below lists the exact pieces of information that the software needs to assemble for the compliance team automatically:

| Evidence Packet Component | What the Copilot Must Display |

| Alert trigger | Scenario, threshold, anomaly, or network event that created the alert |

| Customer context | Expected account activity, risk rating, KYC/CDD status, business purpose |

| Transaction timeline | Dates, amounts, channels, counterparties, geography, linked events |

| Entity relationships | Shared owners, aliases, beneficiaries, connected accounts, shell-company indicators |

| Typology explanation | Structuring, layering, mule activity, sanctions exposure, unusual wire behavior |

| Source evidence | Transaction records, KYC documents, screening hits, policy references |

| Recommendation basis | Why the case should be closed, escalated, reviewed further, or prepared for SAR decision |

| Human action required | Reviewer decision, correction, escalation, or filing approval |

| Audit record | Model version, retrieved documents, generated output, analyst edits, and sign-off |

Furthermore, presenting these components together ensures that human investigators do not have to hunt for documents across multiple old databases. Instead, they can verify the AI’s logic instantly on a single screen.

B. Verifying Source Records for Safety

To maintain high data accuracy, the software must connect every single text claim directly to an original transaction log or ID scan. For example, if the AI claims that a customer moved money to a high-risk country, it must highlight the exact wire transfer record.

Ultimately, this step prevents the software from making up facts or confusing different bank accounts. It also guarantees that the bank can back up its choices if a government examiner asks questions later.

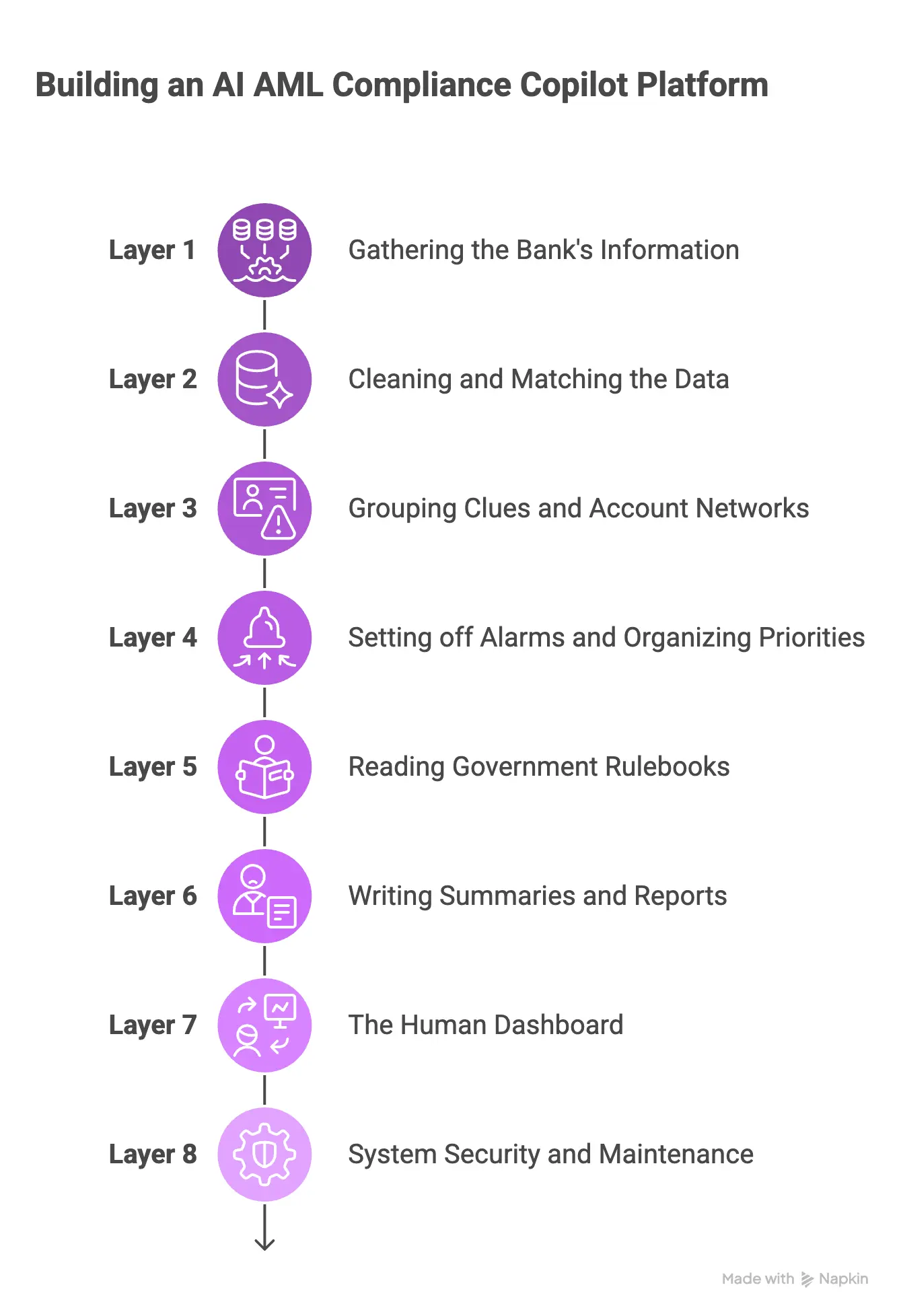

Architecture for an AI AML Compliance Copilot Platform

To build an AI AML compliance copilot platform, banks need a layered architecture that separates source data, detection models, regulatory knowledge, LLM assistance, human approvals, and audit records. This separation prevents a generative model from becoming an uncontrolled decision engine while allowing investigators to work faster with better evidence. Therefore, organizing your software into distinct parts keeps data safe and ensures regulatory compliance.

Consequently, each part of the platform handles a specific task without interfering with the rest of the network. This modular setup allows engineering teams to upgrade individual pieces without breaking the entire compliance pipeline.

Layer 1 — Gathering the Bank’s Information

The bottom layer of the system focuses entirely on pulling data from different parts of the bank safely. It hooks directly into core banking databases to grab traditional account activity and balances in real time.

Furthermore, it connects to external payment processors to track quick movements across ACH networks and wire transfers.

- Main banking files: Grabs current account balances, name changes, and past account history from the bank’s main computers.

- Card and wire transfers: Tracks quick electronic payments and cash movements as they happen.

- International money feeds: Checks big global wire transfers for weird or suspicious behavior.

- Customer signup forms: Collect original ID pictures, sign-up papers, and business profiles.

- Global watchlists: Downloads fresh government lists of blocked people and bad news stories every day.

- Old case files: Links the new incoming money info directly to old notes your workers already wrote.

Layer 2 — Cleaning and Matching the Data

Once the raw information enters the system, the platform must clean it up and make it look uniform. It moves all incoming files into a common customer and transaction schema so that different computer programs can read them. For example, it converts messy text strings into standard formats for names, dates, and account numbers.

- One standard file style: Changes different types of computer files into one layout so they are easy to read.

- Typo fixer: Cleans up spelling mistakes and name variations across different bank files automatically.

- Real owner finder: Figures out who actually owns and pockets the cash from a business account.

- Nickname linker: Connects fake names, shortened names, or nicknames to the user’s real profile.

- Business map builder: Draws a clear picture of how separate companies are secretly tied to each other.

- Data tracking diary: Records exactly where every piece of information came from so inspectors can check it.

Layer 3 — Grouping Clues and Account Networks

This layer studies how customers behave over time to spot weird changes in their spending habits. It calculates behavioral features, like how often a person visits a branch or moves money online. Consequently, the system updates customer risk scoring numbers automatically based on real-world actions rather than static forms.

- Regular habit tracker: Measures everyday spending to understand what a normal day looks like for a customer.

- Live safety scores: Updates a customer’s active danger rating based on their real-world actions.

- Sudden change spotter: Flags instances when an account suddenly gets a huge burst of cash or rapid wire transfers.

- Account network tracer: Looks at how different accounts send money back and forth across the bank.

- Crime ring mapper: Uncovers groups of bad actors who are using multiple accounts to hide their tracks.

- Shared link detector: Groups accounts that share the same phone numbers, addresses, or computer logins.

Layer 4 — Setting off Alarms and Organizing Priorities

This zone combines classic bank rules with smart pattern-spotting models to clean up the alert queue. First, a standard rules engine checks for obvious legal limits, like cash deposits over ten thousand dollars. Second, anomaly detection models look for strange deviations from a customer’s typical monthly spending baseline.

- Basic rule checker: Catches simple law breaks, like cash deposits that go over strict government limits.

- Strange action detector: Flags actions that completely clash with how a customer spent money in the past.

- Trick spotter: Recognizes known criminal tricks, like breaking up big cash bundles into tiny deposits.

- Urgency ranker: Sorts incoming alarms by danger level so workers fix the biggest problems first.

- Report helper: Studies that alarms actually turn into official government reports over time.

- False alarm clearer: Identifies and deletes harmless mix-ups to keep the worker’s screen clean.

Layer 5 — Reading Government Rulebooks

To help the AI write legal arguments correctly, this layer stores real government rulebooks inside a private database. It uses a Retrieval-Augmented Generation(RAG)pipeline to pull relevant text from official FinCEN regulations on command.

Instead of guessing, the AI reads exact paragraphs from the FFIEC examination guidelines before suggesting an action.

- Rulebook searcher: Looks through private legal libraries to find the exact compliance rule your team needs.

- Official government laws: Connects report drafting directly to official federal anti-money laundering rules.

- Inspector guides: Matches investigation steps to the rules that government inspectors use to grade banks.

- National bank updates: Keeps the system updated with the latest rules for big banking groups.

- The bank’s own rules: Mixes your bank’s specific choices and safety limits into the AI’s daily logic.

- Legal proof logs: Attaches real, dated legal paragraphs to every single case summary automatically.

Moreover, for a deeper breakdown of the supporting engineering stack, see our guide on What Tech Stack is Used in AI-Powered Fintech Platforms?

Layer 6 — Writing Summaries and Reports

This is where the natural-language helper reads the compiled data and drafts easy-to-read summaries for your human staff. The system handles compliance case summarization by turning thousands of transaction rows into a short, three-paragraph story.

It handles SAR narrative drafting by assembling the facts into the exact text format that government agencies require.

- Quick story builder: Turns hundreds of messy transfer lines into short, simple text paragraphs.

- Government report drafter: Writes official summaries of bad activity following strict government templates.

- Fact lifter: Pulls exact transaction numbers, dates, and account names directly into the report body.

- Simple text questions: Let workers type plain questions like “Where did this cash go?” to get an answer.

- Clean layouts: Delivers neat information packages that match your main database layouts perfectly.

- Truth lockers: Stop the AI from making up facts or adding imaginary information to the file.

Layer 7 — The Human Dashboard

The AI never makes final legal choices on its own; instead, it passes everything to a human dashboard. The software organizes cases into review queues based on urgency and risk scores.

To maintain high safety standards, it enforces a four-eyes approval system, meaning a second senior worker must sign off on every major decision.

- To-do lists: Organize waiting cases by priority so workers know exactly what to click next.

- Double-check rule: Requires a second senior worker to agree on big choices before any final submission.

- Smart hand-offs: Automatically sends complicated international files to top legal experts.

- Note saver: Records every comment, note, and correction made by employees during an investigation.

- Fix-it tools: Allow human workers to type over or delete any text written by the AI.

- Final send button: Gives an approved human the final power to lock the file and send it to the state.

Layer 8 — System Security and Maintenance

The final layer keeps the platform safe from hackers, system bugs, and legal audit failures. It secures the system using audit trail immutability, which means no one can delete or alter the history of a case.

Role-based access control ensures that workers only see the specific customer files required for their daily jobs.

- Locked history logs: Freezes the case diary forever so no one can secretly change old records.

- Passkey limits: Locks files up so workers only see information that matches their exact job.

- Data scramblers: Protect private customer facts while they sit in storage or move across networks.

- Constant identity checks: Demands security check-ins from every computer and user on the bank’s network.

- Accuracy tracker: Watches the AI over time to make sure its advice does not get sloppy or outdated.

- Question logs: Saves a secure history of what workers asked the AI and what the AI answered.

- Health monitor: Tracks system speed and computer power to stop crashes before they happen.

The architecture should let AI retrieve, classify, summarize, and recommend. It should not allow an unverified generated output to become a regulatory filing or a silent case closure. Therefore, keeping these distinct layers separated guarantees that your human team keeps absolute control over your bank’s legal safety.

Which AI Models Power an AML Compliance Copilot?

An AML copilot requires several model types because no single model can detect suspicious behavior, understand ownership networks, retrieve regulatory guidance, and draft compliant narratives safely. Banks typically need rules, machine learning, graph analytics, NLP, retrieval-augmented generation, and controlled LLM outputs working together under human review. Therefore, combining these different mathematical tools ensures that your compliance platform catches bad actors without making up false stories.

Consequently, each specific mathematical engine handles one part of the investigation pipeline. To achieve a successful LLM AML compliance platform build, engineering teams must integrate these separate tools into a unified scoring network.

1. Supervised Risk Scoring Models

These models look at your bank’s past history to guess which new alerts are actually dangerous. They study old case decisions to see what features caused your human team to file real government reports in the past.

- Learning from history: The software analyzes past alert outcomes to find patterns in true criminal behavior.

- Customer safety grades: The model updates active user risk ratings whenever new transaction files appear.

- Filing predictions: It calculates a baseline alert-to-SAR conversion rate to see if an alert matches older reports.

- Smart priority lists: The model ranks alerts from highest to lowest risk instead of automatically filing documents.

- Clear reasoning: The system provides explainable features so a human worker can see exactly why a score is high.

2. Unsupervised Anomaly Detection

This software does not need past examples to find dangerous behavior. Instead, it measures everyday habits to spot sudden, weird changes that deviate from a normal routine.

- Spike detection: The engine flags unusual transaction patterns that do not fit a user’s normal baseline.

- Group comparison: It measures peer-group deviation to see if a customer spends money like similar businesses.

- New trick finding: The system spots novel typologies that old rulebooks have never seen before.

- Wire transfer monitoring: It watches cross-border wire transfer anomalies for unexpected jumps in cash volume.

- Discovery tools: The math uncovers new behaviors, so your team can write new rules before crimes happen.

3. Graph Analytics and Network Detection

Money launderers rarely use just one bank account to hide cash. Therefore, this tool builds a visual map of how different accounts, people, and businesses are secretly tied together.

- Connection tracking: The software uncovers entity links like shared phone numbers, addresses, or computer IDs.

- Hidden boss finder: It tracks shared beneficial owners across multiple separate corporate accounts.

- Mule network mapping: The system spots groups of people moving small amounts of cash to the same spot.

- Fake company detection: It highlights shell company detection signs, like multiple businesses using one tiny mailbox.

- Layering pattern tracers: The tool follows complex loops where cash bounces between accounts to confuse workers.

Furthermore, banks can scale up to graph neural networks AML modules as an advanced option later, rather than requiring them as a basic default during your initial launch phase.

4. NLP for Customer and Compliance Documents

Most bank information sits inside messy text files rather than clean spreadsheets. Natural Language Processing acts like an automated speed-reader that extracts facts from typed pages.

- Name lifters: The code uses named entity recognition financial documents tools to pull out names, dates, and locations.

- ID document scanning: It pulls text out of KYC document extraction scans, like passports and business licenses.

- Questionnaire processing: The software reads through long corporate CDD questionnaires to find risky answers.

- News summaries: It condenses global adverse media reports into three short sentences for quick reading.

- Note parsing: The engine reads old investigator notes to find past warnings written by your staff.

5. RAG and Controlled Generative AI

This is the writing engine that talks to your team and drafts your reports. To prevent the system from lying, it uses a strict lookup process to fetch real evidence before typing anything.

- Workflow helper: The system configures the main LLM for compliance workflows to handle heavy text sorting.

- Rulebook checking: It uses retrieval-augmented generation compliance steps to find real government laws first.

- Legal citations: The system appends official regulatory source citations to every document draft automatically.

- Report drafting: It uses generative AI SAR drafting code to turn raw numbers into readable text.

- Strict templates: The platform uses template-constrained output rules so the AI never writes outside the lines.

- Evidence links: It builds evidence-linked statements so every typed sentence links to a real transaction row.

Ultimately, your platform must require explicit human approval before any of this text is finalized or sent away.

However, while these global numbers look impressive, your custom copilot build must validate its results against your bank’s unique transaction mix and distinct risk profile before deployment.

The model stack should improve investigator focus, not hide how a result was reached. Therefore, the next section must establish the compliance controls surrounding every model output.

What BSA/AML and AI Governance Controls Must Be Built In?

A bank AML copilot must operate inside the bank’s BSA/AML program, not beside it. The platform needs controls for SAR timelines, CTR reporting, customer due diligence, screening, decision documentation, access security, audit history, model testing, and human approval so that AI assistance strengthens rather than obscures compliance accountability.

Therefore, installing rigid checkpoints throughout your software architecture ensures that your digital helper never creates legal liabilities for your board.

Consequently, automated tools must serve as assistive text drafters rather than independent decision makers. This baseline keeps tracking duties perfectly aligned with existing federal safety expectations.

1. BSA/AML Program and FinCEN Reporting Controls

The platform must track strict federal filing windows automatically to ensure complete Bank Secrecy Act compliance. It monitors specific calendars to guarantee that the team files suspicious activity reports exactly on time without human counting errors.

- Thirty-day SAR filing period: Alarms sound immediately if an asset file sits near its thirty-day window from the initial date of suspect identification.

- Sixty-day extension tracking: The software logs a maximum sixty-day filing period if initial database reviews fail to uncover a specific suspect name.

- Continuing activity alarms: The platform tracks historical suspect logs to surface recurring suspicious patterns every ninety days automatically.

- Currency Transaction Report automation: The system creates automatic filing packages for cash transactions exceeding the applicable reporting threshold, which matches standard requirements found in the FFIEC BSA/AML Examination Manual.

2. Customer and Screening Controls

Background check features must look for hidden client risks during onboarding and throughout daily transaction cycles. The platform updates customer profiles by parsing public files on its own.

- Onboarding identity checks: The copilot handles basic KYC automation to verify new user identities against official state papers.

- Risk updates: The software executes Customer Due Diligence automation to catch shifting company habits before they trigger a violation.

- Deep legal tracking: The system escalates high-risk profiles to Enhanced Due Diligence queues while running beneficial ownership verification checks.

- Sanctions checks: The software runs continuous sweeps across Office of Foreign Assets Control data for absolute OFAC compliance.

- Risk profiles: It matches accounts against Politically Exposed Persons screening databases and live adverse media screening networks.

3. Explainability and Human-in-the-Loop Controls

The software must explain its math clearly so your human staff can audit its logic in seconds. It must never give an output without detailing its exact search steps.

- Clear reasoning logs: To maintain explainable AI compliance, the system shows the exact text rules that triggered an alarm.

- Visible evidence links: The dashboard displays real transaction rows and customer source profiles next to every single summary paragraph.

- Filing locks: The platform requires explicit reviewer approval for SAR narrative generation before any external transfer happens.

- No-file notes: If an analyst decides to close an alarm safely, the software forces them to save a documented decision not to file.

- Override diaries: The system saves a permanent record whenever an analyst edits, deletes, or completely rewrites an AI suggestion.

4. Model Risk and 2026 Regulatory Accuracy

Bank supervisors updated their model safety definitions through the revised interagency guidance released in April 2026. Therefore, software testing plans must reflect these new principles while acknowledging where the limits of the rulebook sit today.

The 2026 Model Scope Rule: The April 2026 revised interagency guidance explicitly states that generative AI and agentic AI models are completely outside its active scope, as these tools are too novel and rapidly evolving

Consequently, this update proves that the government has not yet created settled, generative AI-specific compliance requirements for banks. Instead, your internal teams must design prudent internal governance controls to test, validate, and monitor model outputs on their own.

5. Proposed FinCEN Reform Direction

Regulators also published a massive modernization proposal in April 2026 that focuses on evaluating real-world program effectiveness rather than simple check-the-box documentation rules. This update provides critical strategic context for long-term software design.

The public comment deadline for this proposed AML/CFT program rule sits on June 9, 2026, meaning the text is a future direction rather than an active compliance obligation.

Therefore, an experienced bank AML AI platform development company should map every model output to a reviewer action, an evidence record, a policy control, and an audit export before production release.

Compliance-readiness is not an appendix to the platform. It determines what the copilot can read, recommend, draft, store, and never submit without human authority. Therefore, engineering teams must weigh these control points directly against the phase-by-phase costs of building the system.

What Systems Must the AML Copilot Integrate With?

AI AML copilots for banks must be connected to the platform to transaction, customer, screening, filing, and case-management systems. Without these integrations, the copilot produces summaries without complete evidence and forces analysts to verify information manually across the same fragmented tools they were trying to simplify. Therefore, mapping these data connections early prevents development delays and budget overruns.

Consequently, establishing secure data pipelines allows information to flow right onto the investigator’s screen. The software links your historical records together so that humans can spot suspicious activity trends.

1. Required Integration Groups

Specifically, the table below maps out the eight core integration zones that an automated copilot platform must connect with safely.

| Integration Group | Systems and Data to Cover |

| Core banking | Customer accounts, deposits, withdrawals, profile history |

| Payments | ACH, domestic wires, international wires, cards, real-time payments |

| Messaging networks | SWIFT transaction monitoring and correspondent-payment data |

| Customer compliance | KYC, CIP, CDD, EDD, beneficial ownership records |

| Screening | OFAC, sanctions, PEP, adverse media, internal watchlists |

| AML operations | Existing transaction monitoring, alert queues, case management |

| Regulatory filing | SAR preparation records, CTR workflows, BSA E-Filing support records |

| Security and governance | IAM, RBAC, SIEM, DLP, audit logs, encryption keys |

Furthermore, linking these databases creates an audit trail that shows inspectors exactly how the AI pulled its conclusions.

2. Integration Boundary for Safe Submissions

However, technical teams must build a strict gate around government submission systems. The copilot may compile research files and draft narrative text, but it should never connect directly to public filing portals for automated submission.

Instead, the bank should preserve controlled approval and submission workflows that keep a qualified compliance officer in charge. This human gatekeeper reads the text, checks the data links, and clicks the final submit button manually.

The integration map determines whether the copilot becomes a useful investigation workspace or merely another interface that analysts must double-check. Once the data path is clear, banks can define a practical development roadmap.

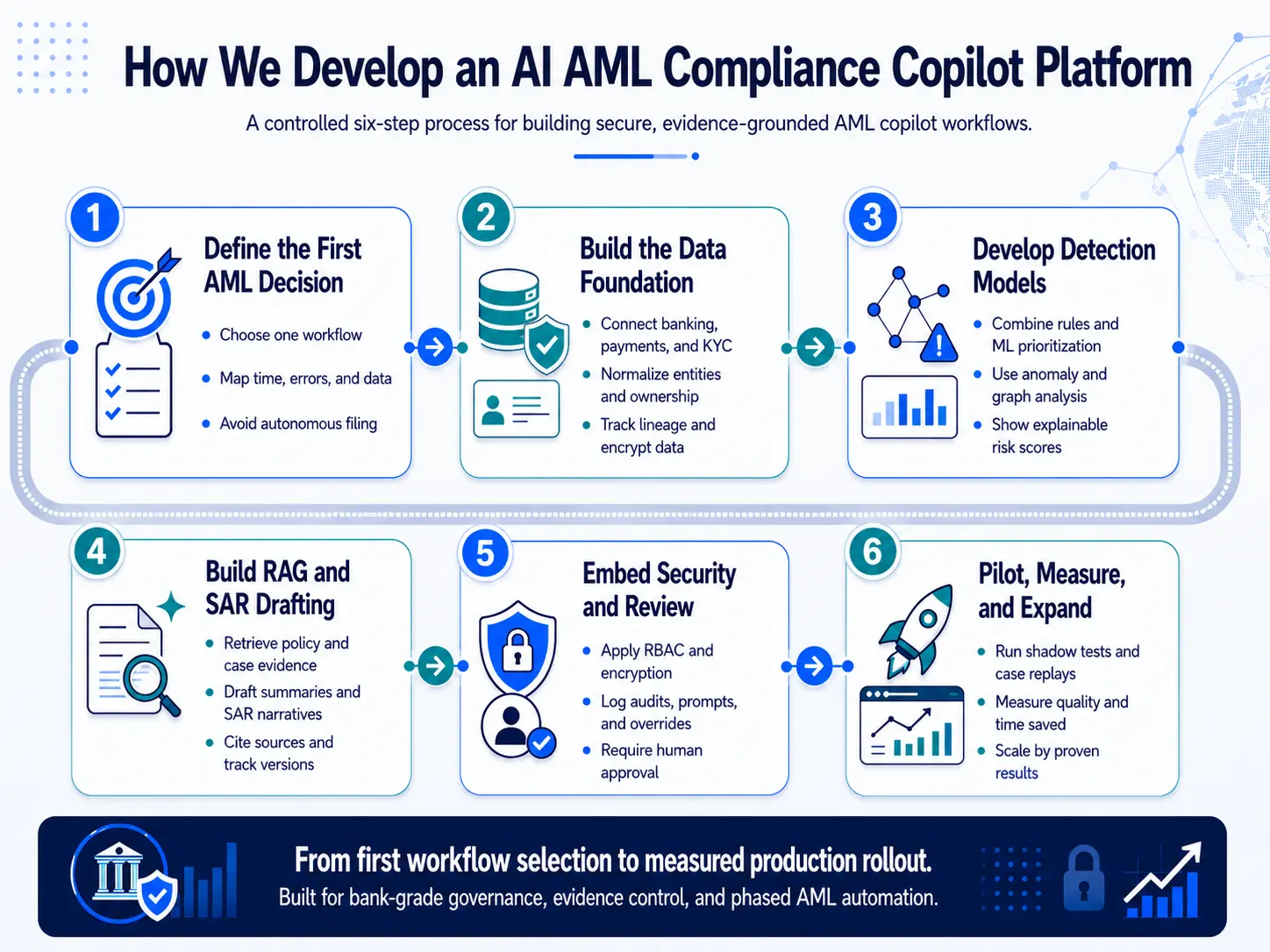

How We Develop an AI AML Compliance Copilot Platform

A custom AI AML compliance platform build should begin with workflow risk, data access, regulatory obligations, and measurable outcomes before model development starts. Intellivon’s development approach would define the first safe automation target, connect required evidence sources, design controlled models, embed human approvals, and pilot the platform against real AML review metrics. Therefore, mapping out these core steps carefully ensures absolute project safety.

Consequently, setting a predictable pathway helps bank executives track progress from initial data connection to final deployment. This step-by-step framework keeps your engineering delivery fully accountable to bank risk committees.

Step 1 — Define the First AML Decision the Copilot Will Assist

Begin with one measurable AML workflow, such as evidence gathering, case summarization, alert prioritization, KYC/CDD review, or SAR narrative drafting. Do not begin with autonomous filing or silent alert closure.

A controlled first workflow creates measurable productivity improvements while leaving regulatory accountability with trained compliance professionals.

- Process mapping: The team charts your current alert and investigation flows to find hidden bottlenecks.

- Time benchmarks: Engineers record the average handling time for each type of case file.

- Pathway tracking: The software maps how alerts move from initial flags to final escalation choices.

- Error logging: Developers analyze your active false positive baseline to understand common system triggers.

- Data availability checks: Workers audit your databases to ensure the AI has clean information to read.

Intellivon uses our Evidence-Yield Prioritization Model during this step to pinpoint high-effort analyst tasks. We focus on areas with clean source data and manageable compliance risks rather than sweeping entire core workflows on day one. Once the first workflow is selected, the bank needs a usable and traceable data foundation.

Step 2 — Build the AML Data and Entity Foundation

The copilot becomes dependable only when it receives normalized customer, account, transaction, ownership, screening, and case data. This stage creates the shared schema, lineage records, entity links, and quality checks needed for risk models and LLM summaries to reference the same verified evidence.

- Core banking pipes: Connects the software directly to the main account records and transaction systems.

- Payment processor links: Tracks quick electronic movements across ACH networks and wire transfers.

- Document ingestion scanners: Read scanned paperwork, application forms, and customer questionnaires automatically.

- Name cleaning tools: Runs identity matching scripts to fix typos and variations across separate bank records.

- History logging diaries: Saves a time-stamped lineage record for every single piece of customer data.

- Data lockboxes: Deploys file encryption to keep private client records hidden from outside networks.

Intellivon designs an auditable data layer that keeps the original source files completely visible beside every single summary. We build secure storage environments with full data encryption to keep private client files safe from outside networks during the extraction process.

After the data foundation exists, detection and prioritization models can be designed against bank-specific risk patterns.

Step 3 — Develop Detection, Prioritization, and Graph Models

The AI model layer should rank suspicious activity and reveal connected risk patterns without replacing the bank’s approved monitoring controls prematurely.

A practical first release combines existing scenarios with machine learning prioritization, anomaly detection, network analysis, and explainable risk factors that analysts can review directly.

- Rule framework setup: Maps your bank’s approved security rules directly into the new digital database.

- Customer segmentation groupings: Clusters similar business accounts together so the AI knows what normal behavior looks like.

- Anomalous pattern spotters: Employs machine learning to catch strange deviations from everyday spending habits.

- Link analysis mapping: Uses basic graph analytics to draw lines between connected customer accounts.

- Urgency ranking logs: Builds priority scores so workers tackle the most dangerous alerts first.

- Reasoning score tags: Generates clear, text-based math explanations for every single model prediction.

Intellivon benchmarks model recommendations against your bank’s historical review outcomes before exposing any scores to active employees. This process measures false positive reduction rates and tests alert-to-SAR conversion capabilities under tight guardrails.

Detection tells analysts what deserves attention, and the copilot layer must explain why and prepare usable evidence.

Step 4 — Build RAG and Controlled SAR Drafting Workflows

An LLM AML compliance platform build should ground every response in approved regulatory documents, bank policy, case evidence, and structured transaction facts. RAG should retrieve source material first, while the LLM formats summaries or SAR narrative drafts that analysts can verify, edit, approve, or reject.

The engineering team builds a private Retrieval-Augmented Generation pipeline to scan local compliance libraries safely. This pipeline holds digital copies of internal BSA/AML policies alongside official FinCEN rulebooks and FFIEC guide text. The system locks down text generation by forcing the model to follow restricted output schemas and pre-approved report templates.

- Private legal lookup pipes: Builds a secure search engine that scans official government compliance books.

- Local policy archives: Indexes your bank’s custom rulebooks so the AI can reference internal limits.

- Evidence citation tags: Forces the writing engine to paste real transaction links next to its claims.

- Report template blocks: Restricts the AI to pre-approved government form structures and text layouts.

- Truth lock systems: Deploy strict prompt controls that stop the AI from making up imaginary data.

- Draft version trackers: Saves a clean history log of every single text change made by your human team.

Our software automatically flags any unsupported text claims and logs a detailed version history of every edited draft. The platform can now assist investigations, but it still needs security, governance, and operational monitoring before deployment.

Step 5 — Embed Security and Human Review Controls

Banks need role-based access, encrypted data movement, immutable audit history, reviewer approvals, model monitoring, prompt logging, override tracking, and clear escalation rules before compliance officers rely on AI-generated recommendations.

Building this framework requires setting up enterprise-grade security protocols that align with SOC 2 readiness standards. Developers deploy a zero-trust network layout that encrypts files while they move across backend networks and while they sit in database storage.

The code locks down your review queues through strict role-based access compliance systems.

- Security readiness blueprints: Configures software settings to align with official SOC 2 security parameters.

- Active network scramblers: Encrypt private customer data while files travel across internal bank computers.

- Passkey access filters: Enforce role-based access rules so workers only see files required for their jobs.

- Frozen history trails: Locks the system log permanently so no one can secretly edit old case notes.

- Model drifting trackers: Watches the AI’s predictions daily to catch any slips in accuracy.

- Override diary recorders: Saves a permanent note whenever a human deletes or changes an AI text suggestion.

Intellivon designs AML compliance copilot software development permissions around specific job roles, file sensitivity, and reviewer authority rather than giving every user identical copilot buttons.

We build permanent log files to watch for model drift while installing human-in-the-loop compliance windows for final reviewer sign-off. The final step tests whether the platform creates measurable compliance productivity without weakening review quality.

Step 6 — Pilot, Measure, and Expand by Proven Outcome

Banks should pilot the Copilot on a controlled workflow and a defined analyst group before expanding it across transaction monitoring or filing operations.

The pilot should measure investigation time, evidence completeness, reviewer correction rates, false-positive handling, SAR draft quality, user adoption, and audit traceability.

- Small testing cohorts: Introduces the software to a tiny group of investigators before launch.

- Old case replays: Tests the AI by feeding it old historical bank files to check its accuracy.

- Shadow mode runs: Operates the software quietly in the background without affecting live customer accounts.

- Feedback dashboard dials: Collects direct change logs and speed notes from your daily users.

- System rollback brakes: Installs emergency controls so engineers can shut off features if a bug appears.

- Quality grade checks: Measures how often senior review workers have to correct the AI’s typed drafts.

Intellivon uses this pilot evidence to decide exactly when the bank should scale into deeper automated features. We analyze the worker metrics to prove the business case before expanding into alternative business departments or foreign jurisdictions.

A bank-grade AML copilot should be released in measured stages. Therefore, measuring real operational value ensures that your investment delivers a clear return.

How The Top 5 Fintech Platforms Use AI in AML Workflows

Banks and fintech platforms are already using AI in targeted anti-money laundering and financial crime workflows, including transaction monitoring, correspondent banking analysis, name screening, alert disposition, and cross-border payment surveillance.

These implementations do not all represent full AML copilots, but they show which compliance workloads can benefit from controlled AI support in production environments.

Therefore, analyzing these real-world projects helps teams see what a unified platform needs to combine.

1. HSBC (Improve Transaction Monitoring Precision)

HSBC provides the clearest public benchmark for AI-powered AML transaction monitoring.

Using Google Cloud AML AI within its Dynamic Risk Assessment approach, the bank applies machine learning to large-scale transaction monitoring and risk detection rather than relying only on manually maintained rule scenarios and high-volume alert generation.

- Massive data sweeps: The network reviews more than 1.2 billion transactions each month for hidden financial-crime risk.

- Fewer false alarms: The bank reported a massive sixty percent drop in false-positive alerts across its monitoring systems.

- Better crime catching: The deployment successfully uncovered two to four times more confirmed suspicious activity.

- Smart workforce focus: The machine learning engine prioritizes high-risk files so analysts do not waste time on safe profiles.

This example supports the business case for combining transaction monitoring, customer risk signals, network behavior, explainable scoring, and investigation prioritization inside an AI AML compliance platform, as proven by the Google Cloud AML AI Platform data layers.

2. Banco Santander (Correspondent Banking Risk)

Banco Santander illustrates how AI can support AML monitoring across correspondent banking, where transaction routes, institutional counterparties, international payment traffic, and customer context create complex investigation demands.

Santander selected ThetaRay’s AML solution to analyze SWIFT traffic, Know Your Customer data, and risk indicators for suspicious patterns.

- Cross-border monitoring: The system scans multi-bank transfer paths to spot illegal patterns moving through complex financial systems.

- Diverse data linking: The platform reads SWIFT traffic logs, regional KYC data, and internal risk metrics simultaneously.

- Network risk discovery: The software uncovers complex anomalies linked to money laundering schemes across separate global branches.

A custom AML copilot for commercial or correspondent banking should connect payment-message data, customer risk records, related-party context, and anomaly detection in one investigator-ready evidence trail. You can trace this layout on the official ThetaRay AML Solutions infrastructure charts.

3. Standard Chartered (Transaction Screening)

Standard Chartered shows that AI in financial crime compliance extends beyond transaction monitoring.

The bank has publicly described the use of AI and machine learning for name and transaction screening, while its Silent Eight partnership focused on improving screening decisions where customer or related-party names match watchlists.

- Continuous list sweeping: The system runs real-time matching checks across massive global sanctions lists and internal lookups.

- Fuzzy name matching: The text engine uses natural language processing to connect spelling variations and alternative names to one entity.

- Consistent choices: The machine learning algorithms reduce manual intervention rates by resolving obvious false alarms automatically.

An AML copilot architecture should not combine every financial-crime control into one opaque model. Instead, it should connect AML investigations, sanctions screening, PEP review, and watchlist evidence while preserving separate control logic and reviewer accountability, in line with corporate benchmarks tracked by Standard Chartered Financial Crime Compliance.

4. Emirates NBD (Automates Screening Investigation)

Emirates NBD provides a practical example of AI supporting the investigation stage of compliance operations.

The bank partnered with Silent Eight after a proof-of-value engagement demonstrated that AI could automate alert-screening investigation processes while improving operational efficiency, accuracy, and auditability within its financial-crime control environment.

- Adjudication help: The platform assists investigators by preparing data arguments for immediate alert disposition choices.

- Accuracy guarantees: The system replicates human reasoning paths to make case reviews precise and fully defendable.

- Clean history trails: The software records every data retrieval step to ensure total auditability for government inspections.

This example is closest to the investigation-support role of an AML copilot. It supports an Intellivon architecture built around evidence display, analyst review, decision logging, audit exports, and permission-controlled AI assistance, which mirrors the goals of the Emirates NBD Compliance Operations program.

5. Payoneer (Monitor Cross-Border Digital Payments)

Payoneer demonstrates how AI-powered AML monitoring applies to fintech payment platforms as well as traditional banks.

The company selected ThetaRay’s cloud-based SONAR system to monitor global cross-border payment transactions and identify suspicious activity across digital payment services operating in fast-moving, international commerce environments.

- Fast-moving commerce loops: The engine checks rapid web payments without slowing down legitimate trade growth.

- Unknown pattern catching: The math uncovers hidden transfer anomalies that traditional rules miss completely.

- Scalable data handling: The cloud layout grows automatically alongside transaction spikes and new cross-border corridors.

For digital banks and payments businesses, an AI AML copilot should combine payment monitoring, customer context, case evidence, risk scoring, and investigator workflows without blocking legitimate transaction growth. This digital layout keeps operations flexible, as seen in the Payoneer Global Payment Infrastructure.

Comparison Table: What Each Implementation Proves

The table below outlines the core workflows and primary compliance lessons from each major production implementation.

| Company | AI-Enabled Workflow | Data or System Focus | Core Buyer Lesson |

| HSBC | AML transaction monitoring | Transaction and customer risk data | AI can reduce review waste while improving suspicious-activity detection |

| Banco Santander | Correspondent banking AML | SWIFT, KYC, risk indicators | AI helps investigate complex international payment networks |

| Standard Chartered | Name and transaction screening | Watchlists, parties, payment screening | AI can improve screening consistency while preserving workflow separation |

| Emirates NBD | Alert-screening investigations | Transaction alerts and investigator decisions | AI can improve case efficiency and auditability |

| Payoneer | Cross-border digital payments AML | Global payment flows | Fintech platforms need scalable risk monitoring across payment corridors |

These examples show that AI adoption in AML is already happening at specific points in the compliance workflow. However, none of these examples removes the need for defensible evidence, clear reviewer authority, audit records, and controlled regulatory decision-making.

The strategic question for a bank is not whether AI belongs in AML, but which decision it should assist first and what evidence it must show before compliance officers trust it. Once the entry workflow is chosen, the platform must connect the complete AML investigation chain.

Build Your AI AML Compliance Copilot Platform With Intellivon

Intellivon works with banks, credit unions, digital banks, and fintech platforms to design AI AML compliance copilots around real investigation workflows. The focus is on helping compliance teams assemble evidence, prioritise alerts, review KYC/CDD risk, prepare SAR narratives, and document decisions within controlled BSA/AML processes.

Every platform roadmap accounts for secure data access, reviewer authority, model governance, SAR confidentiality, and measurable analyst outcomes.

- Identify the safest first AML workflow to assist. Map alert triage, KYC/CDD review, case summarisation, transaction monitoring, or SAR drafting against evidence availability, analyst effort, and regulatory consequence.

- Design architecture around a complete investigation of evidence. Connect transaction records, customer profiles, beneficial ownership data, sanctions, PEP screening results, case histories, and regulatory guidance within one controlled review environment.

- Build AI models and RAG workflows that compliance teams can verify. Use explainable risk scoring, entity resolution, regulatory retrieval, and evidence-backed SAR narrative drafting without removing human filing authority.

- Pilot the copilot against measurable compliance outcomes. Track investigation time, false-positive handling, reviewer corrections, audit traceability, alert-to-SAR conversion quality, and secure human approvals before wider rollout.

If your bank is evaluating an AI AML copilot for alert triage, KYC/CDD review, transaction monitoring, or SAR workflow support, Intellivon can help you map the right first release before development begins.

Conclusion

Banks need better investigation infrastructure rather than completely ungoverned automation. A defensible copilot must connect your transaction monitoring, KYC/CDD, screening, case evidence, SAR drafting, and review history on one secure screen.

Therefore, the safest first build starts with evidence-heavy, measurable workflows where human review remains central for final SAR decisions and absolute regulatory accountability.

Consequently, any bank considering AI AML compliance copilot development should carefully assess its workflow scope, data readiness, integration requirements, governance boundaries, total cost, and pilot metrics before committing to a full production release.

Things To Know About AI AML Compliance Copilots

Q1. How much does AML compliance copilot software development cost for a bank?

A1. A controlled bank-grade copilot typically costs between $60,000 and $250,000 or more. Furthermore, a lower-scope release supports evidence retrieval, case summaries, and SAR drafting assistance. However, costs increase when adding transaction monitoring models, graph analytics, core banking integrations, screening, KYC/CDD automation, multi-entity controls, and strict production governance layers. Therefore, banks must scope features carefully.

Q2. How long does it take to build an AI AML compliance copilot platform?

A2. A focused MVP usually takes 5 to 7 months to construct safely. Consequently, a production deployment with core integrations, human reviews, audit controls, security testing, and active monitoring typically takes six to nine months. Furthermore, full bank-wide expansion may require 9 to 15 months when complex data mapping or legacy payment systems require extra work.

Q3. Can AI draft SAR narratives without making the final filing decision?

A3. Yes, a copilot can collect transaction evidence, identify entities, retrieve internal policies, and produce a structured draft. To remain safe, AI SAR filing automation platform development systems must still require a qualified human reviewer to verify the facts. Ultimately, the human employee must edit the narrative, decide whether to file, and authorize the submission.

Q4. How should banks measure whether AI reduces false positives without hiding genuine risk?

A4. Banks must track more than simple alert reduction metrics. For example, your teams should monitor true-positive identification, alert-to-SAR conversion rates, override rates, and missed-risk back-testing data.

Therefore, running an AI-powered AML transaction monitoring platform is only effective when your risk detection accuracy, typology coverage, and examination-ready evidence packs remain completely defensible during audits.

Q5. What compliance controls are required for an AI anti-money laundering development?

A bank must map the platform directly to its BSA/AML program, SAR workflows, CTR reporting, and KYC/CDD obligations. Furthermore, the current 2026 U.S. regulatory guidance must be managed carefully. While the April 2026 FinCEN program reform remains a proposal, the revised interagency model-risk guidance explicitly excludes generative and agentic tools from its active scope.