Key Takeaways

-

Payment failure signals like processor latency, BIN decline rates, and gateway errors appear before failures occur, but sit across systems too slow to act on manually.

-

Gradient boosting, time-series analysis, anomaly detection, and ensemble models predict decline risk before submission and identify optimal retry windows based on issuer behavior.

-

Smart retry logic based on decline code classification recovers 50 to 70% of failed payments versus 25 to 35% with fixed schedules.

-

Build costs range from $20,000 for an MVP to $250,000 and above for enterprise payment intelligence with predictive routing and compliance-ready audit infrastructure.

-

How Intellivon builds predictive payment failure systems your enterprise fully owns, with real-time scoring, smart retry orchestration, and revenue recovery dashboards from day one.

Every payment that goes through cleanly is the result of dozens of conditions aligning at once, which includes the right processor, the right issuer response, and the right routing path, all holding up under real traffic. When those conditions start shifting, however, the window to act is narrow, and most teams only find out after customers already have.

The signals that precede a failure are almost always present beforehand. Processor response times start slipping, decline rates on specific BINs tick upward, and a gateway that handled traffic fine yesterday starts throwing soft errors on a particular corridor. Individually, none of them trips an alarm. Collectively, though, it is a failure in progress. The challenge is that these signals typically sit across separate systems, and connecting them manually is simply not fast enough to matter.

That is precisely where predictive analytics changes the dynamic. At Intellivon, we build systems that read those patterns in real time, model the conditions that tend to precede a failure, and give payment teams enough lead time to reroute traffic, trigger fallback logic, or escalate before customers feel it. The result is a fundamentally more resilient payment operation. This blog covers how we build that system from the ground up.

Why Do Enterprises Need Payment Failure Prediction?

That rate of investment reflects something straightforward: the cost of not solving this problem has become too significant to absorb.

1. Failed Payments Create Hidden Revenue Leakage

Silent declines from insufficient funds or expired cards quietly erode 5-8% of recurring revenue, often going unnoticed until a quarterly audit surfaces the gap. Predictive models address this by analyzing over 200 signals to flag risk before a charge is attempted.

The result is up to 30% of would-be failures recovered through better-timed retries and smarter charge sequencing.

2. Failed Payments Increase Customer Churn

Over 60% of customers do not return after a single failed payment, and involuntary churn in SaaS and fintech climbs 20-25% as a direct consequence.

Predictive systems respond by enabling proactive retries and surfacing alternative payment methods before the customer even notices an issue, cutting churn by up to 15% and protecting lifetime value without introducing unnecessary friction.

3. Static Retry Rules Miss Recovery Opportunities

Fixed retry schedules succeed only 25-35% of the time because they ignore bank-specific behaviors, fraud flags, and account-level patterns.

Machine learning changes this by adjusting retry logic dynamically based on what has worked across billions of similar transactions, pushing recovery rates into the 50-70% range consistently.

4. Payment Failures Hurt Authorization Rates

Authorization rates typically sit between 92-95%, but during peak traffic periods, failures pull them below 90% and inflate processing costs in the process.

Real-time failure prediction addresses this by optimizing routing across processors before a transaction is submitted, lifting approval rates by 3-5 percentage points without adding latency.

Payment failure prediction has moved from a technical capability to a commercial priority, with 70% of fintechs placing it on their 2026 roadmap. Done well, it secures customer trust, reduces churn, and raises authorization rates, making it one of the higher-return infrastructure investments a payment enterprise can make right now.

What Is Payment Failure Predictive Analytics?

Payment failure predictive analytics is a machine learning system that analyzes historical and real-time transaction data to identify conditions that typically precede a payment failure.

Rather than waiting for a decline to occur, it reads signals across processors, issuers, and payment methods to surface risk before a charge is attempted. The result is a system that gives payment teams enough lead time to reroute, retry, or intervene before the customer is affected.

1. How It Predicts Failed Transactions

The software identifies subtle patterns that human analysts might easily overlook. It looks at the time of day and specific gateway performance to score every attempt.

Machine learning models are trained on millions of successful and failed historical records. Consequently, the software learns which combinations of factors lead to a decline. When a new transaction matches a failure profile, the system flags it for action.

For example, if a specific bank shows high latency, the engine might predict a timeout failure. You can then use this insight to adjust your routing logic dynamically. This technical depth ensures your platform remains resilient under varying market conditions.

2. How It Differs From Basic Payment Reports

Standard reports tell you what went wrong in the past. Predictive analytics tells you what might go wrong in the future so you can fix it.

Predictive analytics focuses on the probability of future events rather than historical summaries. It provides a probability score for every transaction in your pipeline. This allows you to treat different risk levels with unique business logic.

Basic reporting is often siloed within a single payment processor. In contrast, predictive systems aggregate data across multiple providers to give you a global view. This broader perspective is vital for scaling international operations.

3. Where AI Fits Into Payment Success Optimization

AI acts as a brain that manages all your payment rules automatically. It learns from every transaction to make the next one more likely to succeed.

AI provides the processing power needed to analyze complex data sets at scale. It handles the orchestration required to switch between different models based on the payment method. This level of sophistication is impossible to achieve with static rules.

Deep learning can detect evolving fraud patterns that traditional filters might miss. As the market changes, the AI adapts its predictions without needing new code. This continuous learning cycle keeps your platform ahead of industry shifts.

By using these smart systems, your business stays ahead of technical failures and keeps revenue flowing.

What Causes Payment Failures in Digital Payments?

Most payment errors stem from technical glitches or banking rules that block the money. Understanding these triggers is the first step toward protecting your revenue.

Payment failures happen due to insufficient funds, expired cards, issuer declines, gateway downtime, fraud rules, network errors, and routing problems. Using machine learning to classify these codes in real-time allows for automated recovery.

1. Insufficient Funds and Soft Declines

Soft declines occur when a customer has a temporary lack of funds. The system predicts the best time to retry, such as on a common payday, to capture the revenue without bothering the user.

2. Expired Cards and Outdated Details

Expired cards cause unnecessary churn. Predictive models flag cards nearing their end and trigger account updaters to refresh details automatically before the next billing cycle.

3. Issuer Declines and Bank-Level Rules

Banks often block valid payments based on rigid internal filters. By analyzing issuer behavior, your platform can adjust transaction timing to bypass these invisible hurdles.

4. Gateway Downtime and Processor Errors

Technical outages at the processor level can kill your conversion rates. Real-time analytics detect these spikes and switch to a backup gateway to keep your business online.

5. Fraud Filters Blocking Valid Payments

Overly strict fraud rules often turn away honest customers. Predictive models distinguish between real theft and unusual but safe buying habits to approve more sales.

6. Authentication and 3DS Friction

Security steps like 3DS can cause checkout abandonment. The system predicts which transactions are safe enough to bypass extra verification, keeping the user journey fast and frictionless.

7. Cross-Border and Currency Failures

International payments often fail due to local banking restrictions. Smart routing identifies the best local processor for each region to ensure global transactions succeed.

| Failure Type | Common Cause | Predictive Opportunity |

| Soft decline | Bank issue | Retry at a better time |

| Gateway error | Network issue | Route to backup |

| Fraud decline | Rule rejection | Review false positives |

Effective failure management turns lost transactions into captured revenue. These insights keep your investment secure and your growth on track.

How Does Predictive Analytics Reduce Failures?

Predictive tools move your payment strategy from guessing to knowing. This shift prevents errors before they impact your balance sheet.

Predictive analytics reduces payment failures by forecasting decline risk, selecting better retry windows, routing payments intelligently, and triggering customer recovery actions. Modern systems use Random Forest models to determine the statistical probability of success for every transaction attempt.

1. Predicting Decline Risk Before Submission

Most systems wait for a failure to happen before they react. Predictive analytics evaluates the risk of a decline before the transaction ever reaches the processor.

By analyzing merchant category codes and historical bank behavior, the system can pause a high-risk attempt. This allows you to request an alternative payment method or fix data errors upfront.

2. Choosing the Best Time to Retry Payments

If a payment fails, the timing of the next attempt is everything. Tools like Stripe’s Smart Retries use machine learning to pick the specific hour when a bank is most likely to approve a charge.

Instead of retrying at random intervals, the model uses billions of data points to find the ideal window for success.

3. Routing Transactions to Better Providers

Not all payment gateways are equal for every transaction type. Predictive routing identifies which provider has the highest authorization rate for a specific geography or currency.

If a primary gateway shows signs of latency, the system automatically shifts traffic to a secondary provider. This ensures your platform stays resilient and maintains a high success rate.

4. Flagging Customers Likely to Churn

Payment failures are the biggest driver of involuntary churn in subscription models. The analytics engine identifies customers whose payment behavior suggests they might leave soon.

For instance, repeated soft declines are a major red flag. Identifying these users early allows your success team to intervene before the account is canceled.

5. Triggering Payment Method Updates Early

Waiting for a card to expire is a reactive strategy that costs you money. Predictive models look at the lifecycle of a card and predict when it will become invalid.

You can then trigger automated workflows that ask the user to update their details. This proactive approach keeps the service active without any interruption for the user.

6. Improving Authorization Strategy Over Time

Data models get smarter with every transaction your platform processes. Platforms like Recurly train models to predict which specific retry attempt in a sequence is most likely to win.

This continuous learning helps you refine your rules and reduce the cost of processing failed attempts. Over time, this creates a compounding effect on your total revenue.

Successful prediction turns a potential loss into a guaranteed sale. Using these insights ensures your payment infrastructure grows alongside your business.

What AI Models Predict Payment Failures Best?

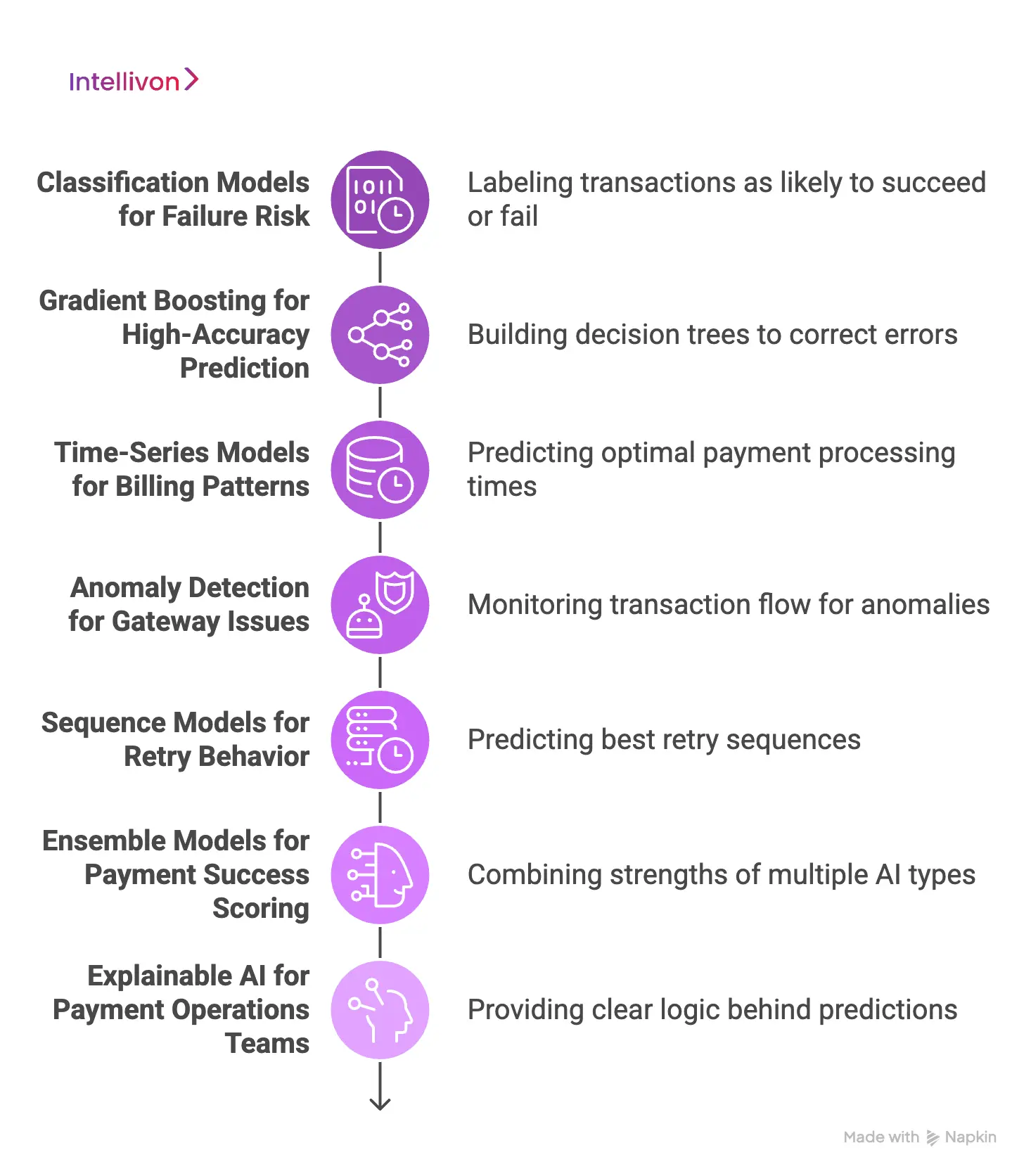

Choosing the right mathematical model is the key to turning raw data into profit. Different types of math solve different parts of the payment puzzle. Payment failure prediction uses classification models, gradient boosting, and time-series analysis to improve accuracy.

Advanced systems often deploy Random Forest or XGBoost to evaluate transaction risk, while LSTM models help predict the best retry sequences for subscription billing.

1. Classification Models for Failure Risk

Classification is the foundation of payment prediction. It works by labeling every incoming transaction as likely to succeed or likely to fail. These models look at simple binary outcomes based on historical data.

By assigning a risk score to every attempt, you can stop high-risk payments before they cost you a processing fee.

2. Gradient Boosting for High-Accuracy Prediction

Models like XGBoost are the industry standard for high-performance prediction. They work by building many small decision trees that correct the errors of the previous ones.

Airwallex and other leaders use this to learn from complex issuer behaviors and shifting market trends. This approach is highly effective at catching subtle reasons for declines that simpler models miss.

3. Time-Series Models for Billing Patterns

Time-series math looks at how data changes over a calendar month or year. It is perfect for predicting when a customer is most likely to have funds in their account.

By mapping out when salaries are deposited across different regions, the AI can pinpoint the exact day a recurring payment should be processed. This timing minimizes “insufficient funds” errors significantly.

4. Anomaly Detection for Gateway Issues

Anomaly detection is like a security guard for your payment pipes. It monitors the “normal” flow of transactions and sounds an alarm if things look strange.

If a gateway that usually has a 90% success rate suddenly drops to 60%, the AI detects this outlier instantly. This allows the system to reroute traffic before a minor glitch becomes a major outage.

5. Sequence Models for Retry Behavior

Long Short-Term Memory (LSTM) models are great at understanding a series of events. In payments, this means looking at the history of previous retry attempts to predict the next best move.

If three attempts failed on a Tuesday, the model might learn that a Friday attempt has a higher success rate. This creates a personalized recovery path for every single customer.

6. Ensemble Models for Payment Success Scoring

An ensemble model combines the strengths of several different AI types into one master score. Instead of relying on one point of view, it takes a “vote” from multiple models to reach a conclusion.

This reduces bias and makes your predictions much more stable. It is the most robust way to handle the massive, messy data sets found in global enterprise payments.

7. Explainable AI for Payment Operations Teams

Decision-makers need to know why a model made a specific choice. Explainable AI provides a “clear box” view into the logic behind a predicted failure.

If the AI blocks a transaction, your team can see if it was due to the bank, the location, or the card type. This transparency builds trust and helps you refine your broader business strategy.

The right model transforms your payment data into a strategic asset. Investing in these technical foundations ensures your platform remains efficient as you scale.

What Architecture Supports Failure Prediction?

A robust technical foundation is required to turn data into real-time payment decisions. This architecture ensures every transaction is analyzed and optimized in milliseconds.

Payment failure prediction requires real-time data ingestion, feature engineering, and model serving layers. Modern fintech stacks use Kafka for event streaming and Feast as a feature store to provide low-latency signals for ML-driven retry orchestration and smart routing.

1. Payment Event Streaming Layer

This layer acts as the central nervous system for your payment data. It captures every swipe, click, and decline signal as it happens across your global network.

This real-time stream provides the raw material needed for immediate prediction and routing adjustments.

- Apache Kafka: For high-throughput, fault-tolerant messaging.

- Amazon Kinesis: For managed real-time data streaming.

- Google Pub/Sub: For asynchronous event delivery.

2. Data Processing and Enrichment Layer

Raw payment data is often messy and needs to be cleaned before it is useful. This layer adds context, such as identifying the issuing bank from a BIN number. Enriched data allows the AI to see the full picture behind every potential failure.

- Apache Spark: For large-scale distributed data processing.

- Apache Flink: For low-latency stream processing.

- dbt (data build tool): For transforming data within your warehouse.

3. Feature Store for Payment Signals

A feature store is a specialized library that holds the variables used by your AI models. It stores attributes like a customer’s average spend or a gateway’s recent success rate for instant access. This ensures the model has the most current information to make an accurate prediction.

- Feast: The leading open-source feature store for machine learning.

- Tecton: For enterprise-grade feature management and serving.

- Redis: For ultra-low latency feature retrieval during live transactions.

4. Model Training and Serving Layer

This is where the actual intelligence lives, hosting the math that forecasts transaction outcomes. The serving layer then delivers these predictions to your payment gateway via high-speed APIs. It bridges the gap between complex data science and live business operations.

- Python (Scikit-learn, XGBoost): For building high-performance models.

- TensorFlow Serving: For deploying deep learning models in production.

- MLflow: For managing the machine learning lifecycle and versioning.

5. Retry and Routing Decision Engine

The decision engine takes the AI’s prediction and turns it into a concrete action. It decides whether to try a different gateway or wait several days before attempting a retry. This layer combines custom ML logic with your specific business rules to maximize authorization rates.

- Go or Rust: For high-performance, low-latency decision logic.

- Amazon Step Functions: For coordinating distributed workflow steps.

- Drools: For managing complex business rule sets.

6. Customer Recovery Workflow Layer

When a failure is predicted as permanent, this layer triggers the human side of the recovery process. It connects to your communication tools to send personalized emails or SMS alerts to the customer. This keeps the user experience helpful rather than frustrating during a decline.

- Node.js or Python: For building flexible API integrations.

- SendGrid or Twilio: For automated customer notifications.

- Braze: For sophisticated customer engagement and lifecycle marketing.

7. Monitoring and Analytics Dashboard

You cannot improve what you do not measure, making this layer vital for long-term success. Dashboards track failure trends and model accuracy in real-time to alert the team of issues. This visibility allows executives to see the direct ROI of their predictive investments.

- Grafana: For real-time observability and technical metrics.

- Tableau or Looker: For business intelligence and revenue reporting.

- Prometheus: For monitoring system health and alerting.

A well-structured architecture transforms fragmented payment data into a powerful engine for growth. Building these layers correctly ensures your platform remains scalable, secure, and highly profitable.

How To Develop Payment Failure Prediction Step by Step?

Building a predictive system requires a structured approach to turn raw transaction logs into actionable financial intelligence. At Intellivon, we follow a rigorous engineering roadmap to ensure every payment has the best possible chance of approval.

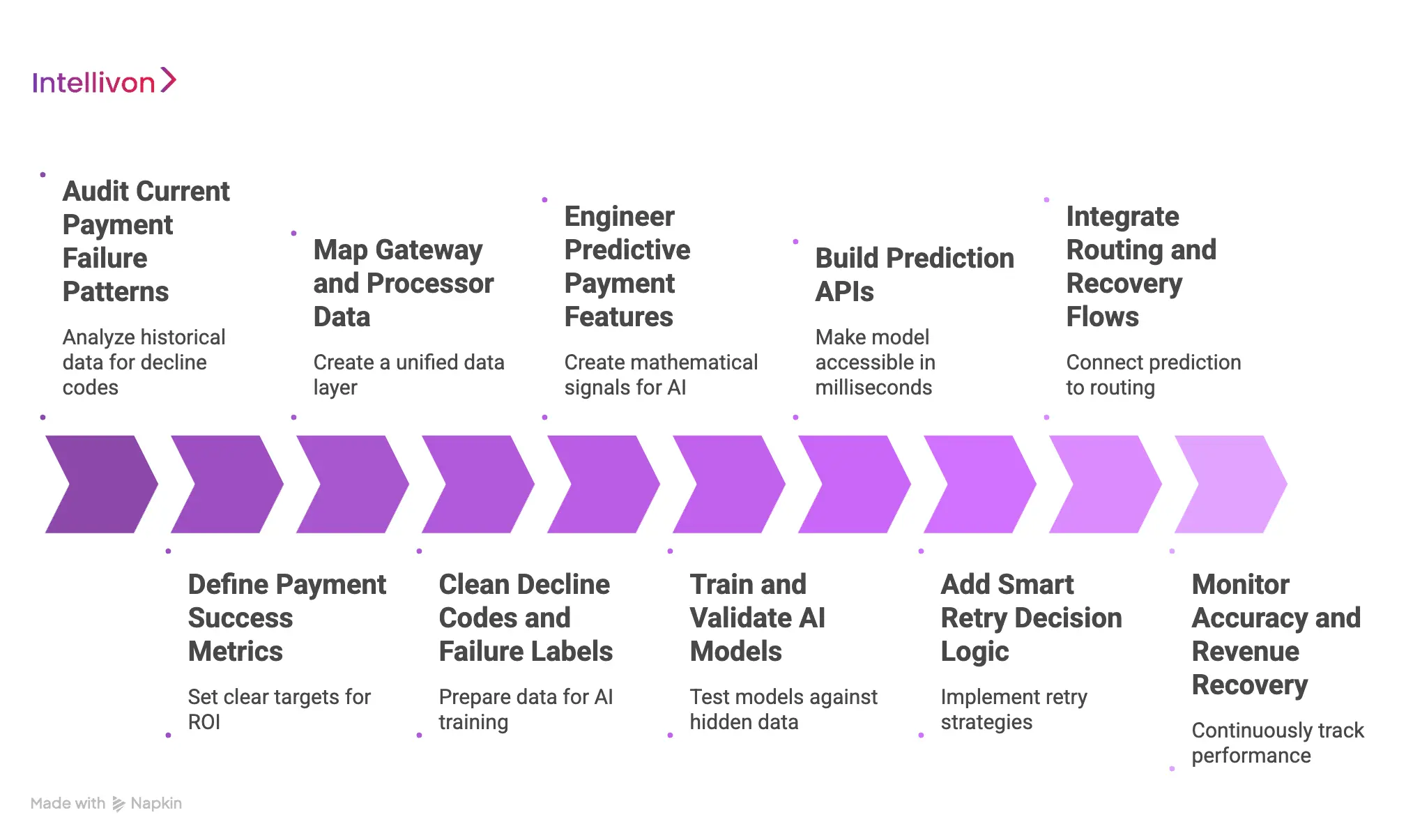

Development starts with failure analysis, data mapping, model training, prediction APIs, retry logic, routing intelligence, dashboards, and continuous optimization. High-performing teams utilize an iterative lifecycle to refine feature engineering and model weights based on live processor feedback.

Step 1: Audit Current Payment Failure Patterns

Before writing any code, you must understand exactly how your money is currently being lost. We analyze your historical data to find the biggest leaks in your payment funnel.

- Identify major decline codes: Categorize errors by bank, geography, and card type.

- Segment by customer value: Determine which failures impact your highest-revenue users.

- Analyze time-based trends: Look for patterns in when failures peak during the day or month.

Step 2: Define Payment Success Metrics

You need clear targets to measure the ROI of your predictive investment. We help you move beyond simple “pass/fail” stats to more sophisticated business KPIs.

- Authorization Rate: The percentage of transactions successfully approved.

- Involuntary Churn Rate: The number of customers lost due to failed recurring payments.

- Recovery Efficiency: How much lost revenue is captured through smart retries.

Step 3: Map Gateway and Processor Data

Every payment provider uses different names and formats for their data. We build a unified mapping layer so your AI sees a consistent picture across all partners.

- Normalize decline strings: Map varied processor messages to a standard internal taxonomy.

- Identify metadata gaps: Check if you are missing key signals like 3DS version or IP geolocation.

- Consolidate multi-processor logs: Ensure data from Stripe, Adyen, or Braintree speaks the same language.

Step 4: Clean Decline Codes and Failure Labels

AI is only as good as the data used to train it. We scrub your records to separate “hard” failures from “soft” failures that can actually be saved.

- Labeling: Tag transactions clearly as “Stolen Card” (permanent) versus “Insufficient Funds” (temporary).

- Deduplication: Remove noise caused by multiple rapid-fire attempts by the same user.

- Anomaly Removal: Filter out data from rare gateway outages that might confuse the model.

Step 5: Engineer Predictive Payment Features

This is where we turn raw data into “features” that the AI can understand. This process creates the mathematical signals that hint at a future decline.

| Feature Category | Description | Why It Matters |

| Temporal | Time of day, day of week | Matches bank processing cycles |

| Behavioral | Last 5 transaction outcomes | Detects patterns of card trouble |

| Technical | Device type, OS, IP risk | Identifies potential security friction |

| Geopolitical | Issuer country vs. Merchant | Flags cross-border routing risks |

Step 6: Train and Validate AI Models

We use the cleaned data to train models that can predict the probability of success. We test these models against “hidden” data to ensure they work in the real world.

- Model Selection: We often start with XGBoost for its balance of speed and accuracy.

- Backtesting: We run the model against last year’s data to see if it would have correctly predicted the failures.

- Calibration: We adjust the model so it is neither too aggressive nor too passive.

Step 7: Build Prediction APIs

Once the model is ready, it needs to be accessible in milliseconds during the checkout process. We build high-speed APIs that serve a “success score” for every transaction.

- Low Latency: The API must respond in under 50ms to avoid slowing down the user.

- High Availability: The service must be online 24/7 to support global sales.

- Scalability: The infrastructure must handle sudden spikes during Black Friday or major launches.

Step 8: Add Smart Retry Decision Logic

Prediction is useless without action. We build a logic layer that takes the AI score and decides the next best move for a failing payment.

- Dynamic Windows: Pick a specific hour and day for the next attempt based on the score.

- Cost Awareness: Decide if a retry is worth the processing fee based on the transaction value.

- Limit Controls: Stop retrying once the probability of success drops below a certain threshold.

Step 9: Integrate Routing and Recovery Flows

For the highest success rates, we connect the prediction engine directly to your routing and messaging tools.

- Intelligent Routing: Send the payment to the gateway with the highest predicted success for that specific card.

- User Intervention: Trigger an SMS to the customer if the AI predicts a manual card update is required.

- Backup Cascading: Automatically try a secondary processor if the primary one is predicted to fail.

Step 10: Monitor Accuracy and Revenue Recovery

The payment landscape changes every day, so we never stop watching the numbers. We build dashboards that show exactly how much revenue the system has saved.

- Drift Detection: Alert the team if the AI starts becoming less accurate as banks change their rules.

- A/B Testing: Compare the AI’s performance against your old static rules to prove the ROI.

- Continuous Learning: Feed new results back into the model to keep it sharp and effective.

Developing a custom prediction engine is the most effective way to protect your margins. Following this roadmap ensures you build a system that delivers measurable financial growth.

How Do Smart Retries Recover Failed Payments?

Smart retries transform the recovery process from a blind gamble into a precise financial operation. This shift ensures you capture revenue that would otherwise be lost to technical timing errors.

Smart retries use predictive models to choose the best retry time, retry method, and recovery sequence based on payment context and past outcomes. By moving beyond static schedules, systems can increase recovery rates by up to 30% through ML-driven timing optimization.

1. Why Fixed Retry Schedules Underperform

Most legacy systems use a rigid “retry every 24 hours” rule regardless of the failure reason. This approach ignores the reality of banking cycles and customer behavior patterns.

Consequently, many attempts fail simply because the retry happens at the same unfavorable time as the original decline.

2. How AI Finds Better Retry Windows

Machine learning analyzes billions of successful transactions to pinpoint when specific banks are most likely to approve a charge.

It considers factors like time zones, local paydays, and bank maintenance windows to schedule the next attempt. This precision ensures you hit the “sweet spot” when liquidity and system uptime are at their peak.

3. How Decline Codes Shape Retry Logic

Not all declines should be treated equally by your recovery engine. A “soft” decline for insufficient funds deserves a different retry strategy than a “technical” error from a gateway timeout.

By reading these codes, the AI adapts the frequency and timing of attempts to match the specific problem it is trying to solve.

4. How Retry Attempts Affect Customer Experience

Too many failed attempts can trigger bank alerts or cause a customer to view your brand as intrusive. Smart retries balance the need for revenue recovery with the importance of maintaining a positive user relationship.

The system stops automatically before it creates “notification fatigue” or risks the card being permanently blocked by the issuer.

5. How To Measure Retry Recovery Rate

Success is measured by the “Recovery Rate,” which tracks how much failed revenue was eventually captured.

You should also monitor the “Cost of Recovery” to ensure that gateway fees for retries do not eat too deeply into your margins. Comparing these metrics against a control group of static retries reveals the true ROI of your AI investment.

Effective retry logic turns a technical failure into a successful long-term subscription. These strategies ensure your business remains resilient in a complex global payment landscape.

How To Predict Payment Failures Before Checkout?

Stopping a payment failure before it happens is the ultimate way to protect your conversion rates. This proactive approach ensures a smooth experience for your highest-value customers.

Enterprises can predict payment failure risk before checkout by analyzing customer history, payment method health, issuer patterns, and transaction context. Using pre-authorization scoring allows platforms to suggest alternate payment methods dynamically, reducing the likelihood of a hard decline.

1. Pre-Authorization Risk Scoring

Every session carries data points that hint at the eventual success of a transaction. By analyzing the user’s device, location, and past behavior in real-time, we assign a “confidence score” before they hit the pay button. If the score is low, you can adjust the checkout flow to mitigate risk immediately.

2. Payment Method Health Checks

Not all saved cards are ready for a successful charge at any given moment. Systems can perform silent health checks by looking at the age of the card and its previous success rate on your platform. This allows you to flag potentially problematic accounts before the user even begins the checkout process.

3. Issuer and BIN-Level Failure Patterns

Banks often experience localized technical issues that affect specific card types. By monitoring global BIN (Bank Identification Number) performance, the AI can predict if a specific issuer is currently having a high decline rate. This insight lets you steer the user toward a more reliable payment method in real-time.

4. Check out Friction and Authentication Risk

High-security requirements like 3DS often lead to failures if the user is on an unstable connection or an old device. The system predicts the likelihood of authentication friction based on the transaction’s technical metadata. You can then choose to simplify the verification process for low-risk users to ensure the sale goes through.

5. Alternate Payment Method Recommendations

If a credit card failure is predicted, the best move is to offer an alternative like a digital wallet or bank transfer. The AI identifies which backup method the specific user is most likely to use and highlights it at checkout. This strategic pivot keeps the customer in the buying loop and prevents a total loss of the sale.

Predicting risk early allows you to control the narrative of the transaction. This foresight turns a potential technical hurdle into a seamless moment of customer service.

What Are Enterprise Use Cases for Payment Prediction?

Predictive analytics is a vital tool across diverse industries. From global fintechs to insurance giants, these models protect revenue and ensure operational stability.

1. Fintech Apps Improving Transaction Success

Fintech platforms rely on high-speed approvals to maintain user trust and wallet utility. Predictive scoring identifies potential card declines before they happen, allowing the app to prompt the user for a top-up or an alternative card.

Real-World Example: Revolut utilizes sophisticated fraud and failure prediction models to ensure that valid cross-border transactions pass through without unnecessary friction.

2. PSPs Reducing Merchant Payment Failures

Payment Service Providers (PSPs) use analytics to protect their merchants from sudden spikes in decline rates. By monitoring issuer health in real-time, they can shift traffic between gateways to maintain high authorization standards across their entire network.

Real-World Example: Adyen offers “RevenueProtect,” which uses machine learning to predict and prevent failures while distinguishing between actual fraud and legitimate technical errors.

3. Digital Banks Predicting Transfer Failures

Digital banks process millions of internal and external transfers where timing is critical. Predictive models analyze recipient bank uptime and historical routing success to ensure that money moves without getting stuck in a “pending” failure state.

Real-World Example: Chime leverages predictive insights to manage real-time deposits and transfers, ensuring users have immediate access to funds by anticipating bank-side delays.

4. Marketplaces Preventing Payout Failures

Marketplaces face the unique challenge of “reverse” payments, or payouts to sellers and vendors. Predicting payout failures before they are initiated prevents expensive reconciliation tasks and keeps your supply side satisfied.

Real-World Example: Uber applies predictive logic to its driver payout systems to ensure that weekly earnings are transferred successfully across thousands of different banking institutions globally.

5. Subscription Platforms Reducing Churn

For subscription models, a failed payment often means a lost customer. Predictive analytics identifies which users are at risk of “involuntary churn” and optimizes the retry schedule to capture the subscription fee on the first attempt.

Real-World Example: Dropbox famously applied machine learning to its payment handling infrastructure, significantly improving its ability to keep subscribers active by predicting the best time to process recurring charges.

6. Lenders Improving Repayment Success

Lending platforms need to ensure that loan repayments are processed successfully to avoid late fees for the borrower. Predicting the best window for a repayment pull based on historical cash flow patterns increases the success rate of every collection attempt.

Real-World Example: Affirm uses data-driven insights to manage repayment schedules, helping consumers stay on track by optimizing when and how payments are requested.

7. Insurers Reducing Policy Payment Lapses

In the insurance world, a failed payment can lead to a dangerous lapse in coverage. Predictive models flag high-risk renewals early, allowing insurers to reach out to policyholders before their protection expires due to a simple card error.

Real-World Example: Metromile (now part of Lemonade) utilizes predictive analytics to monitor pay-per-mile billing, ensuring that intermittent payment cycles remain consistent and successful.

| Enterprise Type | Payment Failure Problem | Predictive Use Case |

| Fintech App | Wallet failures | Pre-payment scoring |

| Digital Bank | Failed transfers | Real-time prediction |

| Marketplace | Seller payout delays | Payout risk scoring |

| Subscription | Involuntary churn | Smart retry optimization |

| Insurance | Policy lapses | Renewal payment alerts |

Applying these use cases correctly transforms payment operations into a strategic advantage. These industry-specific applications ensure your platform remains a leader in the digital economy.

Should You Build or Buy Payment Analytics Software?

The choice between building and buying depends on your technical maturity and long-term goals. Each path offers distinct advantages for protecting your transaction revenue.

Enterprises should buy payment recovery tools for speed, but build custom analytics when they need data control and custom workflows. Choosing to build allows for deeper integration with specific backend services and proprietary customer data points.

1. When Buying Payment Recovery Tools Makes Sense

Purchasing a ready-made solution is the fastest way to reduce current failure rates. These tools are designed for quick integration and offer immediate access to industry-wide data sets.

Consequently, you can start seeing a return on investment within weeks rather than months. This is ideal for teams that need to stop revenue leakage without hiring a specialized data science department.

2. When Building Custom Analytics Makes Sense

Building your own system provides total control over the predictive logic and data security. You can train models on your specific customer behaviors, which often leads to higher accuracy than generic tools.

In addition, a custom build allows you to integrate complex business rules that a third-party vendor might not support. This path is preferred by enterprises with unique payment flows or highly sensitive data.

3. Why Enterprises Often Choose Hybrid Systems

Many organizations combine the speed of purchased tools with the precision of custom models. They might use a third-party gateway for basic retries while building a custom routing engine.

This hybrid approach allows you to scale quickly while still maintaining a competitive advantage through proprietary AI. It offers a balanced way to manage development costs while achieving high performance.

4. Build vs Buy Cost and Control Comparison

Buying typically involves lower upfront costs but requires ongoing subscription fees that scale with your volume. Conversely, building requires a significant initial investment in engineering talent and infrastructure.

However, the long-term cost per transaction is often lower with a self-hosted system. You must weigh the immediate need for speed against the strategic value of owning your core payment intelligence.

| Factor | Buy Payment Tool | Build Custom System |

| Launch speed | Faster | Slower |

| Data ownership | Lower | Higher |

| Model control | Limited | Strong |

| Strategic advantage | Limited | Strong |

How Custom Models Improve With Your Data

A custom model becomes more effective as it processes more of your specific transactions. It learns the nuances of your customer base and the specific banks they use.

This creates a feedback loop where your system constantly adapts to new failure patterns. Over time, this leads to a level of authorization success that off-the-shelf software simply cannot match.

Choosing the right approach ensures your payment infrastructure remains a source of strength. Balancing speed and control is the key to a sustainable financial strategy.

How Much Does It Cost To Build?

Predictive analytics for payment failures typically costs between $20,000 and $250,000+, depending on the platform scope, payment volume, data readiness, model complexity, gateway integrations, smart retry logic, and enterprise reporting needs.

For fintech companies, PSPs, subscription platforms, marketplaces, lenders, insurers, and digital banks, this investment is not just about identifying why payments fail. It is about improving authorization rates, recovering lost revenue, reducing involuntary churn, and strengthening payment operations.

Cost Breakdown by Platform Scope

| Predictive Analytics Scope | Estimated Timeline | Estimated Cost |

| MVP payment failure scoring system | 8–12 weeks | $20,000–$40,000 |

| Smart retry and recovery engine | 3–5 months | $40,000–$85,000 |

| Predictive routing and analytics platform | 5–8 months | $85,000–$160,000 |

| Enterprise payment intelligence system | 8–12+ months | $160,000–$250,000+ |

1. MVP Payment Failure Scoring System: $20,000–$40,000

An MVP is suitable for fintech platforms, SaaS businesses, or subscription companies that want to understand failure patterns and predict high-risk transactions before building a full payment intelligence layer.

This version usually includes basic data ingestion, failure classification, risk scoring, and a dashboard for tracking failed payments. It helps teams identify recurring decline patterns, gateway issues, customer-level risks, and early revenue leakage.

Key components may include:

- Payment failure data ingestion

- Decline code mapping and cleanup

- Basic failure risk scoring

- Failure trend dashboard

- Customer and transaction-level failure insights

- Simple reporting for failed, retried, and recovered payments

This build works well when the goal is to validate predictive analytics before investing in smart retries, routing intelligence, and automated recovery workflows.

2. Smart Retry and Recovery Engine: $40,000–$85,000

A mid-scale system adds retry intelligence and recovery automation. Instead of retrying failed payments on a fixed schedule, the platform predicts when a payment is more likely to succeed and triggers the right recovery action.

This version is useful for subscription platforms, lenders, insurers, marketplaces, and fintech apps that lose revenue because of soft declines, expired cards, insufficient funds, authentication failures, or processor-level issues.

Key components may include:

- AI-based retry timing recommendations

- Decline-code-based retry logic

- Customer recovery workflow automation

- Payment method update triggers

- Recovery dashboards for revenue teams

- Integration with billing, CRM, or payment systems

- Alerts for repeated payment failures

This system helps reduce involuntary churn and improve payment recovery without overwhelming customers with repeated failed attempts.

3. Predictive Routing and Analytics Platform: $85,000–$160,000

A predictive routing and analytics platform is built for businesses that process payments across multiple gateways, processors, regions, issuers, or payment methods.

At this level, the system not only predicts whether a payment might fail. It also recommends the best gateway, processor, payment rail, or retry path based on approval probability, issuer behavior, region, cost, and transaction context.

Key components may include:

- Gateway and processor performance analytics

- Issuer and BIN-level success rate tracking

- Predictive routing recommendations

- Real-time payment failure scoring APIs

- Smart retry orchestration

- Processor failover logic

- Revenue recovery dashboards

- Payment operations reporting

This build is valuable for PSPs, marketplaces, fintech platforms, and digital commerce businesses that want to improve authorization rates and reduce dependency on one payment provider.

4. Enterprise Payment Intelligence System: $160,000–$250,000+

An enterprise-grade payment intelligence system combines predictive analytics, smart retries, routing intelligence, recovery automation, and payment performance monitoring into one scalable infrastructure.

This version is best suited for digital banks, large fintech platforms, global marketplaces, insurers, lenders, and enterprises operating across multiple markets or payment rails.

Key components may include:

- Real-time payment event streaming

- Feature store for payment signals

- Advanced machine learning models

- Multi-gateway and multi-rail orchestration

- Customer recovery workflow engine

- Churn and revenue recovery analytics

- Model monitoring and drift detection

- Compliance-ready reporting and audit logs

- Multi-region infrastructure and access controls

This build helps enterprises move from reactive payment failure reporting to proactive payment performance optimization.

Main Factors That Affect Development Cost

The final cost depends on how deeply the predictive analytics system must connect with your payment ecosystem.

The biggest cost drivers include:

- Data quality: Messy decline codes, missing failure reasons, and fragmented gateway logs increase cleanup work.

- Payment volume: Higher transaction volumes require stronger infrastructure and faster data processing.

- Gateway integrations: More gateways, processors, billing systems, and payment rails increase integration effort.

- Model complexity: Basic classification models cost less than routing models, churn models, or sequence-based retry models.

- Retry logic: Smart retry engines require rules, timing models, recovery workflows, and performance testing.

- Routing intelligence: Predictive routing adds issuer, processor, region, cost, and success-rate analysis.

- Dashboard needs: Revenue, operations, finance, and product teams often need different analytics views.

- Compliance requirements: Audit logs, access controls, and regional data handling can increase scope.

- Deployment scale: Multi-region systems cost more than single-market analytics platforms.

How Intellivon Optimizes Build Cost

At Intellivon, we develop predictive payment failure systems in phases, so enterprises can start with the highest-impact use cases before expanding into full payment intelligence infrastructure.

Our approach usually includes:

- Starting with the payment failure data you already have

- Cleaning and standardizing decline codes early

- Building an MVP around the highest-loss failure patterns

- Adding smart retry logic before advanced routing when needed

- Designing APIs that fit into existing payment workflows

- Creating dashboards for payment, finance, and revenue teams

- Expanding into routing intelligence once enough data is available

- Monitoring model performance after launch

This phased approach helps enterprises control development cost while still building toward a scalable payment intelligence system.

If your enterprise is dealing with recurring failed payments, low authorization rates, involuntary churn, or fragmented payment reporting, Intellivon can help you build a predictive analytics system that improves recovery, strengthens payment performance, and scales with your transaction ecosystem.

Conclusion

Implementing predictive analytics for payment failures is a vital move for any growing enterprise. This technology transforms unpredictable technical hurdles into a manageable and strategic asset. By anticipating declines before they happen, you protect your revenue and build lasting customer trust.

Investing in these advanced systems ensures your platform remains resilient and profitable in a competitive global market. Start optimizing your payment success today to enable sustainable long-term growth.

Build Payment Failure Analytics With Intellivon

Building predictive analytics for payment failures requires more than a reporting dashboard. It needs a connected payment intelligence system where transaction data, decline codes, issuer behavior, retry outcomes, gateway performance, and recovery workflows work together in real time.

At Intellivon, we develop enterprise payment failure analytics systems where AI is embedded directly into the payment performance layer. This helps fintech platforms, PSPs, digital banks, marketplaces, subscription businesses, lenders, and insurers predict failed payments, recover revenue faster, improve authorization rates, and reduce involuntary churn at scale.

A. Designing Payment Failure Prediction Systems

Payment failures often happen before teams can respond. We design prediction systems that identify high-risk transactions, payment methods, issuers, customers, and gateways before revenue is lost.

- Real-time failure scoring: We build scoring APIs that predict payment failure risk before authorization, retry, renewal, or payout.

- Decline-code intelligence: The system standardizes issuer, gateway, and processor decline codes to identify patterns accurately.

- Issuer-level prediction models: We analyze BIN, bank, region, card type, and network behavior to forecast approval probability.

- Payment context analysis: Transaction amount, currency, customer history, location, device, and payment method signals feed the prediction layer.

This gives payment teams early visibility into likely failures, instead of waiting for declined transactions to appear in reports.

B. Building Smart Retry and Recovery Engines

Fixed retry schedules often waste recovery opportunities and create customer friction. We build smart retry engines that use predictive analytics to decide when, how, and whether a failed payment should be retried.

- AI-based retry timing: Models recommend retry windows based on issuer behavior, customer history, decline reason, and past recovery outcomes.

- Retry orchestration logic: The system controls retry frequency, retry spacing, payment method selection, and customer notification triggers.

- Soft decline recovery flows: Temporary failures, insufficient funds, network errors, and authentication issues are routed into targeted recovery paths.

- Payment method update triggers: The platform prompts customers to update expired, invalid, or high-risk payment methods before repeated failures occur.

This improves recovery rates while reducing unnecessary retries, support tickets, and customer frustration.

C. Integrating Analytics Into Payment Workflows

Payment failure analytics only create value when it works inside the actual payment stack. We design integration layers that connect prediction intelligence with gateways, processors, billing systems, wallets, banking rails, and internal operations tools.

- Payment gateway integrations: We connect analytics systems with gateways and processors to capture live transaction and failure data.

- Real-time decision APIs: Prediction outputs can trigger retry, route, alert, payment update, or customer recovery actions instantly.

- Billing and subscription integration: The system connects with recurring billing workflows to reduce failed renewals and involuntary churn.

- Routing and failover logic: Payments can be redirected to stronger providers when gateway, issuer, or regional failure patterns emerge.

This ensures payment intelligence becomes part of the transaction lifecycle, not a separate dashboard that teams check after revenue loss happens.

D. Creating Dashboards for Revenue Recovery

Enterprise teams need visibility into why payments fail, how much revenue is at risk, and which recovery actions are working. We build dashboards that turn payment failure data into clear operational and financial decisions.

- Revenue recovery dashboards: Teams can track recovered revenue, failed payment value, retry performance, and churn impact.

- Gateway performance analytics: Operations teams can compare approval rates, failure reasons, latency, and processor-level reliability.

- Customer and segment insights: Product and revenue teams can identify high-risk customer groups, subscription cohorts, regions, and payment methods.

- Failure trend reporting: Dashboards highlight recurring decline patterns, issuer issues, authentication friction, and gateway outages.

This helps payment, finance, product, and revenue teams act on failure patterns before they become larger business losses.

Whether you need an MVP failure scoring system, a smart retry engine, predictive routing intelligence, or a full enterprise payment analytics platform, Intellivon can help you design the architecture, build the models, integrate the workflows, and estimate a development roadmap aligned with your payment ecosystem.

FAQs

Q1. What is payment failure predictive analytics?

A1. This technology uses machine learning to forecast if a transaction will be declined before it is processed. It analyzes historical patterns and real-time signals to identify risk. By predicting outcomes early, businesses can reroute or adjust payments to ensure success and protect their revenue streams.

Q2. How does AI predict payment failures?

A2. AI evaluates thousands of data points, including issuer behavior, transaction timing, and hardware metadata, to find failure signatures. It compares live attempts against millions of past records to calculate a probability score. This allows the system to automate decisions that prevent declines and optimize authorization rates in milliseconds.

Q3. What data is needed to predict failed payments?

A3. High-quality prediction requires transaction metadata like BIN numbers, currency types, and merchant category codes. It also uses behavioral signals such as past customer success and gateway latency. Clean data from multiple processors ensures the model understands the full context behind every payment attempt for better accuracy.

Q4. Can predictive analytics reduce failed payments?

A4. Yes, it significantly lowers failure rates by selecting better retry windows and routing transactions to more reliable processors. It also triggers proactive customer updates for expiring cards to stop involuntary churn. These combined actions transform technical errors into successful sales while improving the overall health of your business.