Key Takeaways:

-

AI merchant risk monitoring replaces periodic manual reviews with continuous behavioral scoring across onboarding, underwriting, transaction monitoring, dispute prediction, and offboarding.

-

Effective tools detect transaction laundering, MCC mismatches, synthetic merchant accounts, and volume spikes by combining graph AI, NLP, anomaly detection, and supervised models in one stack.

-

Chargeback prediction identifies dispute signals weeks before filing, allowing processors to adjust reserves or processing limits before card network thresholds are breached.

-

Build costs range from $10,000 for a rule-based MVP to $80,000 and above for a real-time enterprise system with AI scoring, compliance layers, and full case management workflows.

-

How Intellivon builds AI merchant risk monitoring tools your enterprise fully owns, with real-time pipelines, multi-model architectures, and compliance-ready audit trails from day one.

Merchant risk is always changing. In acquiring banks, payment service providers, embedded finance platforms, and high-volume marketplaces, fraud tactics evolve, chargeback patterns change, and compliance requirements become stricter, often all at the same time. Traditional monitoring systems rely on fixed rules and periodic reviews, which cannot handle this level of pressure. As a result, gaps form, allowing fraudulent merchants to slip through unnoticed.

This is why AI-based merchant risk monitoring is now a key investment for serious payment systems. Instead of waiting until problems occur, machine learning models continuously assess merchant behavior, create dynamic risk scores, and identify unusual activities before chargebacks or compliance issues arise. This shifts risk management from merely limiting damage to a strategic function integrated into the platform.

Intellivon has created adaptive AI systems for financial institutions. These systems combine regulatory intelligence, detect suspicious activities in real time, and learn continuously as new risk patterns develop. This blog uses that practical knowledge to outline the architecture, data needs, risk modeling methods, and operational setup required to create effective merchant risk monitoring tools that can scale for enterprise use.

Why Is AI Merchant Risk Monitoring Adoption Rising?

AI-powered merchant risk monitoring is growing fast. Payment systems are becoming more complex, fraud is more advanced, and regulations are stricter. As a result, legacy systems can’t keep up. At the same time, banks, processors, and platforms are now adopting AI tools to manage risk more effectively at scale.

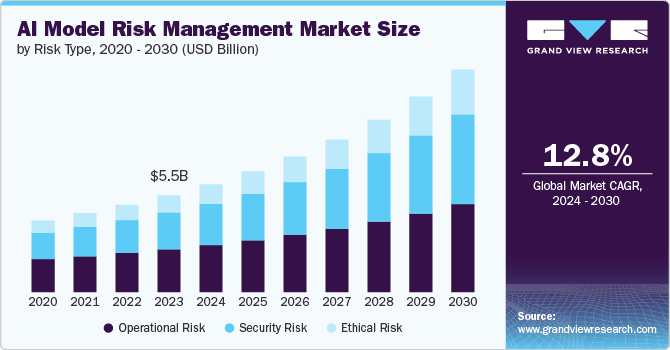

The global AI model risk management market was valued at USD 5.47 billion in 2023. It is expected to reach USD 12.57 billion by 2030. This reflects steady growth, with a CAGR of 12.8% between 2024 and 2030.

1. Rising Chargeback And Fraud Pressure On Processors

Payment processors and acquirers face increasing chargeback thresholds and fraud exposure. Even small spikes can trigger network penalties, reserve requirements, or merchant shutdowns, forcing platforms to adopt proactive monitoring systems.

2. Growth Of High-Risk And Digital-Only Merchants

Digital-first businesses scale rapidly and often operate across geographies, making manual monitoring ineffective. Platforms must track behavior changes continuously as merchant risk evolves after onboarding.

3. Transaction Laundering And Hidden Merchant Activity

Transaction laundering has become harder to detect with rule-based systems. Enterprises are adopting AI to identify mismatches between approved merchant profiles and actual transaction behavior.

4. Real-Time Payments Require Real-Time Risk Decisions

With faster payment rails, risk decisions must happen instantly. Delayed detection increases financial exposure, pushing platforms to adopt real-time AI monitoring.

This shift shows that traditional risk systems are no longer enough to manage modern payment ecosystems. As complexity grows, AI-driven monitoring is becoming essential for enterprises to stay secure, compliant, and scalable.

What Is AI-Based Merchant Risk Monitoring?

AI-based merchant risk monitoring is the use of machine learning models and real-time data analysis to evaluate, score, and manage risk across a merchant portfolio. It continuously tracks transaction behavior, chargeback patterns, compliance signals, and fraud indicators at the merchant level.

Therefore, instead of waiting for thresholds to breach, the system detects risk early and flags it automatically, giving payment processors and acquiring banks proactive control over portfolio-wide exposure.

Who Needs Merchant Risk Monitoring Software?

Identifying risk early is the difference between sustainable growth and sudden regulatory fines. For any organization handling massive transaction volumes, manual oversight is no longer a viable strategy.

1. Acquiring Banks And Merchant Acquirers

Banks sit at the top of the payment chain and carry the ultimate financial liability. They require automated tools to scan thousands of merchant accounts for unusual spikes or suspicious activity.

This protection ensures they maintain their licenses and avoid heavy penalties from central regulators.

2. Enterprise Payment Processors

Processors act as the technical engine for global commerce and must ensure every transaction is legitimate. They use AI to detect high chargeback rates or fraudulent patterns across various industries simultaneously.

This allows them to protect their reputation while maintaining high uptime for honest merchants.

3. Large PSPs And Payment Gateways

Payment Service Providers often work with smaller businesses that lack their own security teams. By implementing risk software, these gateways can offer a safer environment for their clients.

It helps them filter out bad actors before they can cause damage to the broader ecosystem.

4. Embedded Finance And BaaS Platforms

Banking as a Service (BaaS) providers allow non-financial brands to offer digital wallets or lending. Since these brands often lack deep fintech expertise, the underlying platform must provide robust risk monitoring.

This automation prevents financial crimes like money laundering from slipping through the cracks.

5. High-Volume Marketplaces And Platforms

Marketplaces manage a diverse range of third-party sellers with different risk profiles. AI tools help track seller behavior and product listings to ensure compliance with global trade laws.

This scale of oversight is impossible to achieve without sophisticated machine learning models.

Investing in these tools creates a shield that protects your capital and your brand reputation. Strategic risk management is the foundation upon which global payment leaders build their long-term success.

Why Enterprises Need AI For Merchant Risk

AI for merchant risk monitoring replaces manual reviews with real-time behavioral analysis and automated risk scoring. This technology enables payment enterprises to scale rapidly while reducing exposure to sophisticated digital fraud.

Traditional safety nets often fail because they rely on historical data rather than current behavior. Modern enterprises require a proactive approach to stay ahead of increasingly clever financial threats.

1. Rising Fraud Across Digital Payment Systems

Criminals now use automation to launch sophisticated attacks against payment networks at incredible speeds. Static rules cannot keep up with these evolving methods because they are too predictable.

AI systems learn from every transaction and identify new fraud patterns before they become widespread problems.

2. Faster Merchant Growth And Higher Exposure

Rapidly expanding a merchant portfolio increases the surface area for potential financial loss. Every new partner brings a unique set of risks that could impact your bottom line.

Machine learning allows you to onboard thousands of users while maintaining a strict security posture.

3. Manual Reviews Cannot Scale With Portfolios

Human analysts are excellent at deep investigation, but they cannot process millions of data points every second. Relying only on manual checks creates massive bottlenecks that frustrate legitimate business partners.

AI-powered automation handles the heavy lifting so your experts can focus on the most complex cases.

4. Risk Teams Need Real-Time Decision Support

Decision makers need instant insights to block suspicious transfers without stopping the flow of valid commerce. Advanced algorithms provide a clear risk score for every event in a fraction of a second. This support ensures your team makes informed choices based on data rather than gut feelings.

Shifting to an intelligent risk model turns a defensive cost center into a strategic advantage. It provides the speed and accuracy necessary to dominate the modern financial landscape.

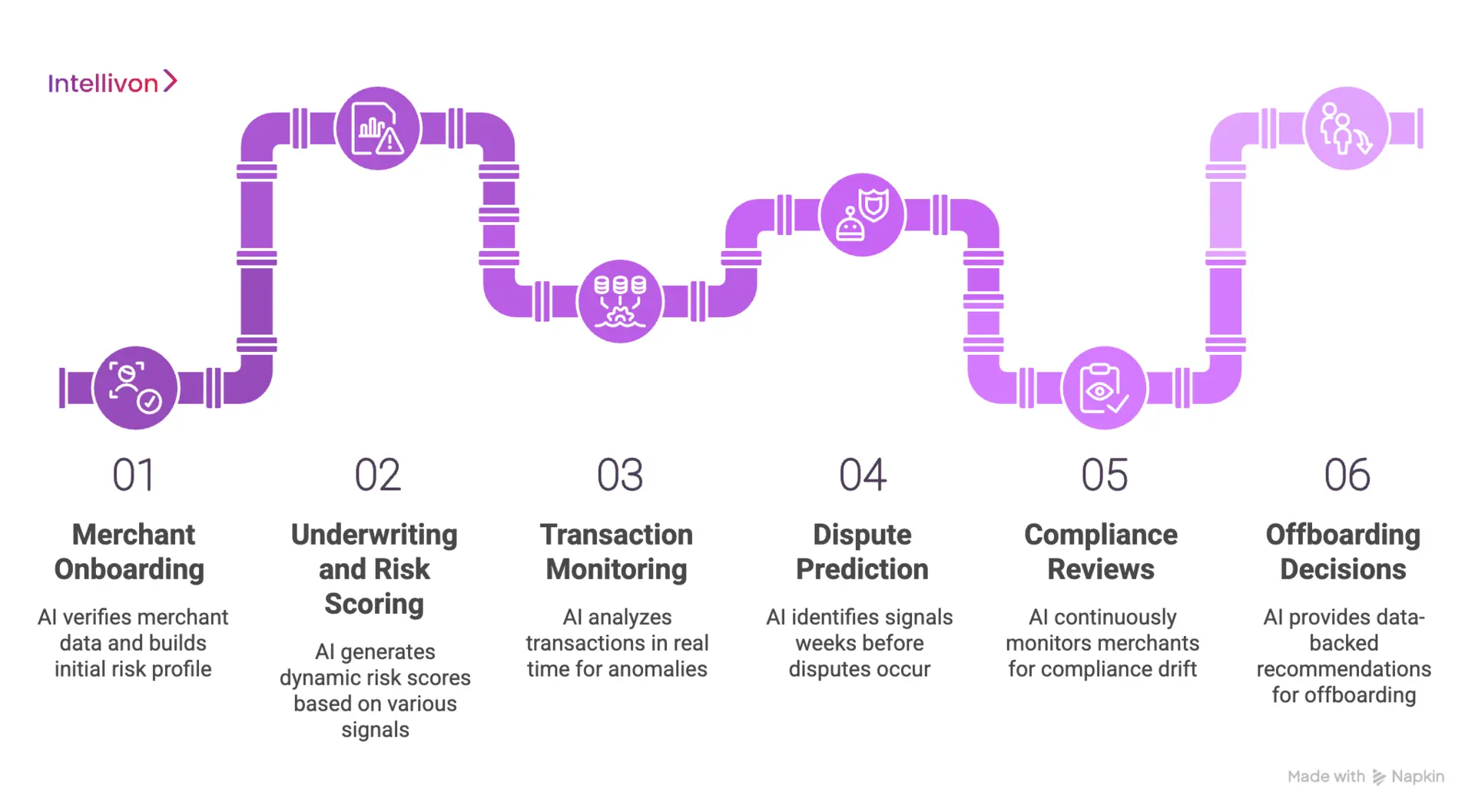

Where Does AI Fit In The Merchant Lifecycle?

AI fits into the merchant lifecycle at every stage, including onboarding, underwriting, transaction monitoring, dispute prediction, compliance reviews, and offboarding.

This gives payment processors and acquiring banks continuous, real-time merchant risk monitoring across the entire portfolio rather than isolated point-in-time checks.

1. AI In Merchant Onboarding And KYB

Onboarding is where risk either gets caught early or gets missed entirely. AI accelerates Know Your Business verification by automatically cross-referencing merchant data against sanctions lists, business registries, adverse media, and ownership structures simultaneously. Traditional KYB processes take days. AI-powered onboarding compresses that to minutes.

More importantly, it builds an initial risk profile based on business category, geography, processing history, and ownership patterns. Therefore, underwriters receive a merchant that has already been pre-scored before any human review begins.

2. AI In Underwriting And Risk Scoring

Underwriting determines what processing limits, reserve requirements, and risk controls apply to each merchant. AI improves this by moving beyond static application data. It pulls in behavioral signals, industry benchmarks, and real-time financial indicators to generate a dynamic risk score.

Consequently, merchants with strong signals get approved faster. High-risk merchants get flagged with specific reasons, not just a blanket decline. This makes underwriting both more accurate and more defensible from a compliance standpoint.

3. AI In Transaction Monitoring

Transaction monitoring is where merchant risk monitoring operates at its highest frequency. AI models analyze every transaction in real time, looking for behavioral anomalies, velocity spikes, unusual refund patterns, and category mismatches. However, the real advantage is pattern recognition across the entire portfolio.

A single merchant’s transaction data tells one story. When AI compares it against thousands of similar merchants simultaneously, it identifies coordinated fraud rings, bust-out patterns, and collusion signals that no manual review process would catch in time.

4. AI In Dispute And Chargeback Prediction

Chargebacks rarely appear without warning signals. AI identifies those signals weeks before a dispute is filed. It monitors refund ratios, customer complaint patterns, delivery failure rates, and processing behavior to generate a chargeback probability score at the merchant level.

Therefore, acquiring banks and PSPs can intervene early, whether through reserve adjustments, processing limits, or direct merchant outreach, before the chargeback ratio breaches card network thresholds. Prevention is always cheaper than remediation.

5. AI In Ongoing Compliance Reviews

Merchant compliance doesn’t end at onboarding. Business models shift, ownership changes, and regulatory requirements evolve. AI continuously monitors merchants for compliance drift by tracking changes in transaction categories, geographic expansion, and processing behavior against the original approved profile.

In addition, it flags PEP exposure updates, sanctions list changes, and AML red flags automatically. This means compliance teams spend their time on genuine exceptions rather than routine portfolio sweeps.

6. AI In Merchant Offboarding Decisions

Offboarding a merchant is a high-stakes decision. Exiting too early damages a legitimate business relationship. Exiting too late creates liability. AI removes much of that ambiguity by providing a clear, data-backed risk trajectory for each merchant.

When behavioral signals consistently deteriorate across fraud indicators, compliance flags, and chargeback trends, the system generates an offboarding recommendation with a full audit trail. Therefore, the decision is documented, defensible, and separated from manual judgment.

Merchant risk monitoring is evolving rapidly, and therefore, platforms that rely on static rules will continue falling behind.

What Risks Should The Tool Detect?

A robust monitoring system must look beyond simple credit scores to understand operational behavior. Effective tools identify hidden patterns that indicate a merchant is no longer acting in good faith.

1. Transaction Laundering

This occurs when a legitimate merchant account is used to process payments for an unrelated or illegal business.

AI identifies this by spotting discrepancies between reported sales and actual digital footprints. It helps prevent your platform from becoming a conduit for unauthorized trade.

2. Chargeback And Dispute Risk

High dispute rates can damage your relationship with card networks and lead to heavy fines.

Predictive models analyze historical patterns to forecast which merchants are likely to see a surge in claims. This foresight allows you to adjust collateral requirements or reserve funds before losses occur.

3. Synthetic Merchant Accounts

Fraudsters often create fake businesses using a mix of real and fabricated data to bypass initial checks. Advanced verification tools cross-reference multiple databases to ensure the entity and its owners actually exist. This layer of defense stops professional criminals from entering your ecosystem.

4. MCC And Business Model Mismatch

A business might register as a clothing store but actually sell high-risk electronics or software. Monitoring tools track Merchant Category Code consistency to ensure the business stays within its approved risk profile. This prevents unexpected exposure to industries that carry higher regulatory scrutiny.

5. Suspicious Volume And Velocity Spikes

Sudden bursts in transaction activity often signal a “bust-out” fraud attempt or a compromised system. AI-powered alerts trigger when a merchant exceeds their typical processing limits in a short timeframe. You can then pause payouts while your team verifies the legitimacy of the new volume.

6. Refund, Payout, And Settlement Risk

Irregularities in how money leaves a merchant account can indicate internal theft or liquidity issues. Automated systems track the ratio of refunds to sales to spot potential money-draining schemes. This ensures that the funds moving through your pipes remain stable and accounted for.

7. Website And Product Category Drift

Merchants may start with compliant goods but slowly transition into selling restricted or prohibited items. Web crawling agents periodically scan merchant sites to detect changes in inventory or terms of service. This constant check keeps your portfolio aligned with your internal risk appetite.

Comprehensive detection is the only way to build a resilient and trustworthy payment network. Identifying these diverse threats ensures your capital remains safe while your legitimate partners thrive.

How Can AI Detect Transaction Laundering?

AI detects transaction laundering through automated web crawling, graph-based network analysis, and behavioral pattern matching. These tools identify hidden storefronts and suspicious payment routing to prevent illegal merchants from accessing legitimate payment rails.

Transaction laundering is a sophisticated shell game where illegal sales hide behind a legitimate storefront. AI provides the deep visibility needed to track these obscured money trails across global networks.

1. Hidden Merchant Pattern Detection

Sophisticated algorithms scan for anomalies in transaction data that do not match the declared business model. For example, a small bakery processing large round-dollar amounts at midnight triggers an immediate investigation.

Machine learning identifies these behavioral outliers by comparing them against millions of similar, honest businesses.

2. Website And Domain Monitoring

Automated crawlers frequently visit merchant websites to ensure the products sold match the processed payments. AI can detect if a site is merely a “front” with no real checkout activity or if it redirects to a hidden store.

This persistent digital surveillance ensures that the merchant remains compliant long after the initial onboarding.

3. Payment Descriptor Mismatch Checks

The text that appears on a customer’s bank statement must accurately reflect the business they visited. AI monitors these descriptors to find discrepancies between the merchant of record and the entity charging the card.

Identifying these mismatches helps stop unauthorized businesses from piggybacking on a clean account.

4. Linked Merchant Network Analysis

Fraudsters often operate networks of multiple accounts to spread their risk and avoid detection. Graph technology maps connections between disparate merchants based on shared bank accounts, IP addresses, or physical locations.

This bird’s-eye view reveals hidden clusters of high-risk activity that individual checks would miss.

5. Suspicious Routing And Processing Flows

Illicit actors often use complex routing to hide the final destination of their funds. AI tracks the flow of money in real time to spot unusual hops or international transfers that lack a clear business purpose.

This transparency ensures that every dollar moving through your platform has a verified and legal origin.

Unmasking these hidden actors is vital for maintaining the integrity of your financial ecosystem. Modern detection ensures your infrastructure remains a safe harbor for legitimate global commerce.

What Features Should The Tool Include?

Building a world-class risk platform requires a balance between automated intelligence and human control. The most effective tools provide a centralized command center where complex data becomes a clear, actionable strategy.

1. Merchant Risk Scoring Dashboard

A high-level dashboard serves as the nerve center for your entire portfolio health. It should aggregate data from multiple sources to assign a dynamic risk score to every merchant.

This allows your leadership team to see at a glance which segments of the business are thriving and which require immediate intervention.

2. Real-Time Transaction Monitoring

The ability to analyze payments as they happen is the cornerstone of modern fraud prevention. Your tool must process thousands of transactions per second, checking each against historical behavior and global threat intelligence.

This ensures that high-risk events are paused before the money leaves the ecosystem.

3. AI-Based Alert Prioritization

Not all flags deserve the same level of attention from your staff. Machine learning models can rank alerts based on their probability of being actual fraud versus a simple false positive.

By prioritizing the most dangerous threats, your team avoids alert fatigue and focuses its energy where it matters most.

4. Merchant Case Management

When a suspicious pattern emerges, your analysts need a structured way to investigate. Integrated case management allows users to attach evidence, record communication with the merchant, and track the progress of an inquiry.

This creates a permanent paper trail that is vital for legal protection and internal accountability.

5. Rule Builder For Risk Policies

While AI handles the unknown, your team needs the flexibility to set hard boundaries. A “no-code” rule builder allows non-technical managers to implement new restrictions instantly based on geography, industry, or transaction size.

This agility is crucial when responding to sudden market shifts or new regulatory mandates.

6. Chargeback Prediction Module

Predicting a dispute before it happens allows you to take preemptive action to protect your margins. This module analyzes merchant history and customer data to identify transactions with a high likelihood of being contested.

You can then choose to hold funds in reserve or request additional verification from the seller.

7. Compliance And Audit Reporting

Regulatory bodies require detailed proof that you are monitoring your network effectively. Your tool should generate automated reports for Anti-Money Laundering (AML) and Know Your Business (KYB) standards.

Having these documents ready for download saves hundreds of hours during annual audits and state examinations.

8. Analyst Feedback And Model Learning

The system must get smarter with every decision your team makes. When an analyst marks an alert as “confirmed fraud” or “false alarm,” the AI should incorporate that feedback into its future logic.

This continuous learning loop ensures the software adapts to your specific business environment and risk tolerance.

These features transform risk management from a manual burden into a scalable asset. A well-equipped platform provides the technical foundation needed to support the most ambitious growth targets in the fintech space.

What Data Is Needed For Merchant Risk AI?

AI-based merchant risk monitoring requires a combination of KYB data, transaction logs, and external watchlist signals. By integrating device fingerprints and historical case data, enterprises can build a 360-degree view of merchant behavior and portfolio health.

Data is the fuel that powers any intelligent monitoring system. High-quality inputs from diverse sources allow the engine to distinguish between a legitimate business surge and a criminal attack.

1. Merchant Onboarding And KYB Data

The foundation of risk assessment begins with a deep understanding of who the merchant is. This includes verified corporate registration, tax identities, and the personal details of ultimate beneficial owners.

Collecting this data during the initial application creates a baseline for all future behavioral comparisons.

2. Transaction And Authorization Data

Every payment carries a wealth of information, including amount, currency, and terminal identification. Real-time authorization logs reveal how a merchant interacts with various card networks and banks.

This stream of data allows the AI to spot unusual spending patterns or suspicious card testing attempts instantly.

3. Refund, Dispute, And Chargeback Data

Historical performance in handling customer complaints is a primary indicator of future stability. Monitoring the frequency and reasons for chargebacks helps identify merchants with poor quality control or deceptive practices.

This data is essential for calculating the financial reserves you must hold to cover potential losses.

4. Device, IP, And Location Signals

Digital footprints provide a layer of security that traditional paperwork cannot offer. By tracking the hardware and network locations used for transactions, the system can detect account takeovers or offshore fraud rings.

These technical signals act as a silent alarm when a merchant suddenly logs in from an unexpected country.

5. Website, Domain, And Content Signals

A merchant website is a living document that reflects the merchant’s current business activities. Automated tools scrape site content to look for prohibited products or changes in the terms of service.

Analyzing domain age and hosting reputation adds another layer of validation to ensure the business is legitimate.

6. External Risk And Watchlist Data

No enterprise operates in a vacuum, so it is vital to check global databases. Integrating feeds from sanctions lists, politically exposed persons (PEP) registries, and industry blacklists is a non-negotiable requirement.

This external context ensures you never accidentally facilitate business for a high-risk entity.

7. Analyst Review And Case History Data

Your own internal expertise is a goldmine for training machine learning models. Every time an investigator closes a case, they provide a valuable label that tells the AI what “good” or “bad” looks like.

Storing this history allows the system to replicate human intuition at a much larger scale.

Access to diverse data sets ensures your risk models remain sharp and effective. This information architecture is the bedrock of a secure and compliant payment enterprise.

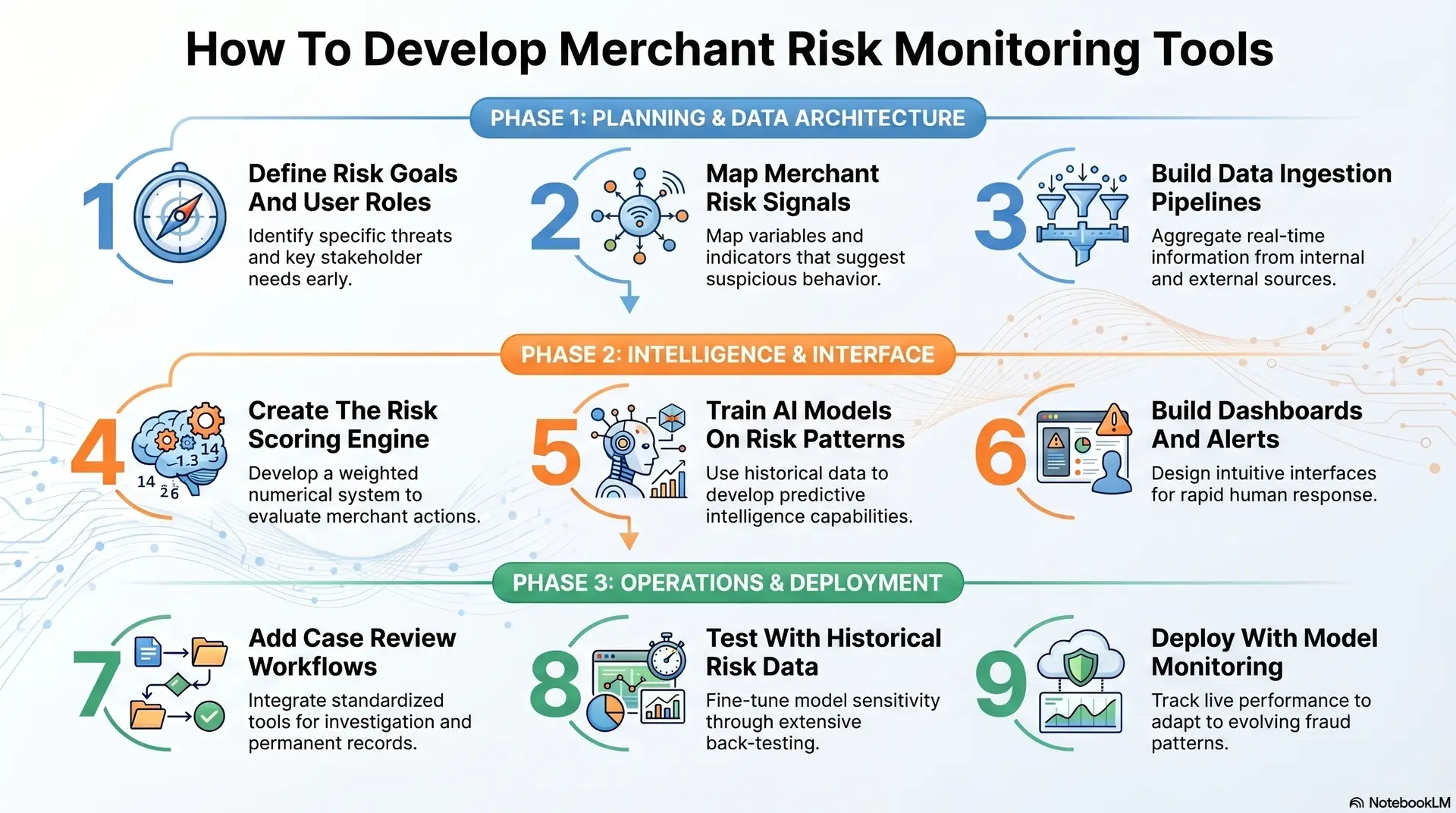

How To Develop Merchant Risk Monitoring Tools

Building an enterprise-grade risk engine requires a disciplined architectural approach. We follow a rigorous methodology to ensure the final product is both legally compliant and technically superior.

This phase-by-phase roadmap outlines the necessary journey from raw data to proactive intelligence.

Step 1: Define Risk Goals And User Roles

Every successful development project begins with a clear understanding of the specific threats you intend to stop. We start by identifying the key stakeholders who will interact with the system daily. Compliance officers need detailed audit trails while executive leadership requires high-level portfolio health summaries.

Defining these personas early ensures the software serves the actual needs of your organization rather than just checking a technical box.

Step 2: Map Merchant Risk Signals

Once the goals are set, we identify the specific indicators that suggest a merchant is moving outside of acceptable boundaries. This involves mapping out hundreds of variables such as average transaction value, geographic concentration, and refund ratios. We look for the subtle “digital breadcrumbs” that fraudsters leave behind.

By creating a comprehensive library of risk signals, we provide the AI with the specific vocabulary it needs to describe suspicious behavior.

Step 3: Build Data Ingestion Pipelines

A risk tool is only as good as the data it consumes in real time. We construct high-speed pipelines that aggregate information from internal payment gateways, external KYB databases, and third-party threat feeds.

These pipelines must be resilient enough to handle millions of events per hour without latency. Ensuring data remains clean and standardized during this process is vital for the accuracy of the downstream machine learning models.

Step 4: Create The Risk Scoring Engine

The scoring engine is the brain of the operation, where all ingested data is evaluated against your business logic. We develop a weighted system that assigns a numerical value to every action a merchant takes.

A sudden change in IP address might add ten points to a score, while a transaction from a sanctioned country might add one hundred. This creates a dynamic environment where risk is constantly recalculated as new information arrives.

Step 5: Train AI Models On Risk Patterns

At this stage, we move beyond static rules and into predictive intelligence. We use historical data to teach machine learning models how to recognize the complex signatures of transaction laundering and account takeovers.

These models learn to identify relationships between data points that a human analyst might never notice. This training phase is a continuous loop where the AI becomes increasingly accurate as it sees more examples of both honest and fraudulent behavior.

Step 6: Build Dashboards And Alerts

The insights generated by the AI must be presented in a way that allows for rapid human response. We design intuitive interfaces that highlight the most critical threats through visual cues and priority queues.

Rather than burying your team in a mountain of data, we focus on surfacing the “why” behind every alert. This transparency builds trust in the system and ensures that your staff knows exactly where to look when an anomaly occurs.

Step 7: Add Case Review Workflows

When a high-risk event is detected, the system must guide your team through a standardized investigation process. We build integrated case management tools that allow analysts to freeze payouts, request documents, or clear a merchant with a single click.

These workflows ensure that no alert is ever forgotten and that every decision is backed by a permanent record. This structure is essential for maintaining high operational standards and passing regulatory audits.

Step 8: Test With Historical Risk Data

Before the system goes live, we run it through extensive “back-testing” using your previous year of transaction history. We check to see if the AI would have caught past fraud cases and how many false alarms it would have generated.

This stress test allows us to fine-tune the sensitivity of the models. By adjusting the parameters in a safe environment, we ensure the tool is ready to protect your capital from day one.

Step 9: Deploy With Model Monitoring

The launch is just the beginning of the journey because fraud patterns never stop evolving. We implement real-time monitoring to track the performance of the AI models in the live environment.

If the software begins to miss new types of attacks, we can quickly retrain the engine with fresh data. This constant vigilance ensures your risk posture remains ironclad even as the global payment landscape shifts around you.

What Architecture Does The Platform Need?

Building a reliable risk platform requires a modular architecture that separates data collection from intelligent decisioning. Each layer must operate independently to ensure that a failure in one area does not bring down your entire security apparatus.

1. Merchant Data Ingestion Layer

The first layer acts as the entry point for all incoming information from disparate sources. It must handle structured data like KYB forms and unstructured data such as website content or social media signals.

We design this layer to be “agnostic” so it can easily connect with new payment gateways or third-party identity providers. This flexibility ensures your platform can grow alongside the evolving fintech ecosystem without needing a total rebuild.

2. Real-Time Event Processing Layer

Once data enters the system, it must be processed within milliseconds to be effective during live transactions. This layer uses stream processing technologies to evaluate every payment against historical merchant behavior.

It acts as a high-speed filter that identifies immediate threats like velocity spikes or known fraudulent cards. Handling the heavy lifting of data sorting in real time, it allows the more complex AI models to focus on deep pattern analysis.

3. AI And Machine Learning Layer

This is the intellectual core where sophisticated models analyze the relationships between millions of data points. We deploy various algorithms here, ranging from supervised learning for known fraud types to unsupervised learning for detecting “black swan” events.

This layer does not just look for single red flags but identifies complex clusters of behavior that suggest organized crime. It provides the deep context necessary to separate a legitimate high-growth business from a dangerous actor.

4. Risk Decisioning Layer

The decisioning layer translates the complex outputs of the AI into specific business actions. It applies your internal risk policies to determine if a transaction should be approved, flagged for review, or blocked entirely.

This layer is highly configurable, allowing your team to adjust sensitivity levels based on current market conditions. It ensures that your risk appetite is consistently applied across every single interaction on your platform.

5. Alert And Case Workflow Layer

When the system identifies a high-risk event, this layer manages the human intervention process. It generates detailed alerts that explain exactly why a merchant was flagged, providing analysts with the evidence they need for a quick decision.

We built this as a collaborative workspace where team members can share notes and track the status of investigations. This structured approach reduces the time it takes to resolve cases and prevents critical threats from slipping through the cracks.

6. Compliance Reporting Layer

Regulatory oversight is a constant reality for any enterprise handling payments at scale. This layer automatically compiles all monitoring activity into standardized reports for AML and SAR filings.

It maintains a comprehensive audit trail of every automated decision and human action taken within the system. Having this data readily available ensures you can respond to regulatory inquiries with confidence and precision.

7. Security And Access Control Layer

Because this platform handles sensitive financial and personal data, the highest levels of security are non-negotiable. This layer manages who can view specific datasets and who has the authority to change risk policies.

We implement strict encryption and multi-factor authentication to protect the integrity of the entire system. This final layer of defense ensures that your internal risk tools do not become a vulnerability themselves.

A well-designed architecture provides the stability needed to support massive transaction volumes while remaining agile enough to face new threats. Investing in this technical foundation is the only way to build a truly scalable and secure financial enterprise.

What AI Models Power Merchant Risk Tools?

Modern risk engines do not rely on a single algorithm to protect your assets. Instead, they deploy a sophisticated stack of diverse models that work together to identify threats from multiple angles.

1. Supervised Models For Known Fraud Patterns

These models are trained on vast datasets of past transactions where the outcome is already known. They excel at recognizing the specific digital fingerprints of established fraud types.

- Binary Classification: These systems categorize every event as either safe or suspicious based on historical labels.

- Feature Importance: The AI identifies which specific variables—such as country of origin or time of day—are the strongest indicators of risk.

- High Precision: Because they learn from confirmed cases, these models have a low rate of false alarms for common attack vectors.

2. Anomaly Models For Unusual Behavior

Anomaly detection focuses on finding the “unknown unknowns” by establishing a baseline for normal activity. These models flag anything that deviates significantly from a merchant’s typical behavior.

- Unsupervised Learning: These models simply look for outliers in the flow of information.

- Behavioral Baselining: The system learns the unique “pulse” of a business, such as its typical daily volume and peak hours.

- Early Warning: This is the first line of defense against new, never-before-seen fraud tactics that supervised models might miss.

3. Graph AI For Connected Merchant Risk

Graph technology visualizes the complex relationships between different entities in your payment network. It is designed to expose professional fraud rings that operate multiple accounts simultaneously.

- Link Analysis: This identifies merchants who share the same phone numbers, bank accounts, or digital device IDs.

- Community Detection: The AI spots clusters of accounts that interact in ways that suggest a coordinated money-laundering scheme.

- Structural Risk: Even if an individual merchant looks clean, the system may flag them if they are too closely connected to known bad actors.

4. NLP Models For Website And Complaint Data

Natural Language Processing allows the platform to “read” and understand text-based information. This provides a layer of context that numerical data alone cannot provide.

- Sentiment Analysis: The AI monitors customer reviews and social media to detect a sudden surge in dissatisfaction or scam allegations.

- Content Auditing: Automated crawlers scan merchant websites to ensure they are not selling prohibited items or using deceptive marketing.

- Document Parsing: These models extract key details from business licenses and identity documents to speed up the verification process.

5. Ensemble Models For Better Risk Accuracy

An ensemble approach combines the predictions of several different models to reach a final decision. This “wisdom of the crowd” strategy significantly improves the reliability of your risk scores.

- Voting Systems: If three different models flag a transaction but two others say it is safe, the ensemble calculates the most likely reality.

- Reduced Bias: By blending different mathematical approaches, the system compensates for the weaknesses of any single algorithm.

- Higher Throughput: These models can handle massive scale without losing the nuance required for high-stakes financial decisions.

Agentic AI For Risk Investigation

The newest frontier in risk management involves autonomous agents that can perform complex research tasks. These AI agents act as digital assistants for your human analysts.

- Autonomous Research: An agent can independently search external databases and public records to verify a merchant’s identity.

- Reasoning Chains: Unlike basic bots, agentic AI can follow a logical series of steps to investigate a suspicious transaction from start to finish.

- Report Generation: These agents can summarize a three-day investigation into a concise, actionable brief for your compliance team.

Deploying a multi-layered model strategy is the only way to stay ahead of sophisticated financial criminals. This technological depth ensures your platform remains a secure environment for legitimate business growth.

What Integrations Does The Tool Need?

A risk monitoring platform must function as a central nervous system that connects to every part of the payment lifecycle. These integrations ensure that data flows seamlessly between your internal infrastructure and the external world.

1. Payment Gateway And Processor APIs

Direct connections to your transaction engines provide the raw material for real-time monitoring.

- Stream Integration: These APIs deliver a constant feed of authorization and settlement events as they occur.

- Low Latency: High-speed connections ensure that risk checks happen in milliseconds without slowing down the customer checkout experience.

- Status Syncing: The system can automatically trigger transaction voids or reversals through the gateway when fraud is detected.

2. Acquiring And Core Banking Systems

Interfacing with the underlying banking rails is essential for tracking the actual movement of funds.

- Ledger Visibility: Integration with core banking software allows the tool to monitor merchant balances and payout schedules.

- Settlement Reconciliation: The system matches processed transactions against final bank settlements to identify discrepancies or missing funds.

- Reserve Management: You can automate the holding or releasing of merchant reserves based on current risk levels directly within the banking system.

3. KYB, KYC, And AML Providers

External identity and compliance feeds add a layer of legal certainty to your internal data.

- Identity Orchestration: These integrations pull data from global sources like Alloy or Onfido to verify business owners and legal entities.

- Sanctions Screening: Automated checks against PEP and OFAC lists ensure you remain compliant with international anti-money laundering laws.

- Continuous Monitoring: The tool receives updates if a merchant’s status changes on a government watchlist long after they have been onboarded.

4. Chargeback And Dispute Platforms

Managing disputes requires a tight link between the risk engine and the card networks.

- Dispute Ingestion: APIs from platforms like Verifi or Ethoca feed chargeback notifications directly into your risk dashboard.

- Evidence Automation: The system can pull transaction logs and digital signatures to help your team represent and win disputes more effectively.

- Predictive Analysis: Historical dispute data from these platforms is used to train your AI models on which merchants are becoming a liability.

5. CRM And Merchant Management Systems

Risk management is more effective when it includes a 360-degree view of the merchant relationship.

- Profile Enrichment: Syncing with tools like Salesforce or HubSpot provides context on merchant size, industry, and previous support interactions.

- Communication Logs: Analysts can see if a merchant has a history of policy violations or unusual account changes documented by the sales team.

- Automated Offboarding: If a merchant is terminated for fraud, the CRM is updated instantly to prevent future outreach or reactivation.

6. BI, Data Warehouse, And Reporting Tools

Long-term strategy depends on moving data into specialized environments for deep analysis.

- Data Lake Export: Large volumes of historical risk data are pushed to warehouses like Snowflake or BigQuery for longitudinal studies.

- Executive Dashboards: Integration with BI tools like Tableau or Power BI allows leadership to track key performance indicators and portfolio health.

- Audit Readiness: Having a centralized repository of all risk decisions makes it easier to generate comprehensive reports for annual regulatory examinations.

Robust integrations turn a standalone software product into an indispensable part of your business operations. This connected approach ensures your risk strategy is always informed by the most accurate and up-to-date data available.

What Tech Stack Is Best For Development?

The success of a risk platform depends on its ability to process millions of events without a single second of downtime. Choosing the right combination of tools ensures your system is fast enough to stop fraud while remaining flexible enough to evolve.

1. Backend Technologies

The backend serves as the heavy-duty engine that powers all your internal logic and database interactions.

- Java or Go: These languages are the industry standards for high-concurrency financial systems because they offer superior memory management.

- Microservices Architecture: Dividing the platform into small, independent services allows you to update specific risk models without taking the entire system offline.

- Rust: We increasingly use Rust for performance-critical components because it provides memory safety without the overhead of a garbage collector.

2. AI And Machine Learning Frameworks

AI and ML are the heart of the platform, requiring frameworks that can handle both research and production-scale inference.

- PyTorch: This is our preferred choice for rapid experimentation and building complex neural networks for fraud detection.

- Scikit-learn: We use this for traditional machine learning tasks like random forests and logistic regression, which remain highly effective for structured financial data.

- TensorFlow Serving: This tool allows us to deploy trained models as scalable APIs that can handle thousands of requests per second.

3. Data Engineering And Streaming Tools

A risk engine is only as good as its ability to see data the moment it is generated.

- Apache Kafka: This serves as the central nervous system for event streaming, ensuring that transaction data is distributed to every part of the stack instantly.

- Apache Flink: We use Flink for stateful stream processing, which allows the system to remember past events while analyzing new ones in real time.

- Apache Iceberg: This table format provides a reliable way to manage massive amounts of historical data in a data lake for future model training.

4. Cloud Infrastructure

Enterprise platforms require a global footprint with a focus on high availability and regional data compliance.

- AWS or Google Cloud: These providers offer the specialized hardware and managed services needed to run massive AI workloads.

- Kubernetes: We use container orchestration to ensure the platform can scale up instantly during holiday shopping peaks or sudden traffic surges.

- Serverless Functions: For smaller, periodic tasks like weekly reporting or batch cleanup, serverless architecture reduces operational costs.

5. Frontend And Dashboard Technologies

The user interface must be responsive and capable of displaying complex, real-time data visualizations.

- React.js: This framework allows us to build dynamic dashboards where risk scores and alerts update instantly without a page refresh.

- Tailwind CSS: We use this for building clean, professional interfaces that are easy for your analysts to navigate during high-pressure investigations.

- Next.js: This meta-framework improves performance through server-side rendering, ensuring your internal tools are fast and SEO-friendly for public-facing portals.

6. Security And Compliance Tools

Security is not an afterthought but is baked into every layer of the development process.

- HashiCorp Vault: This tool manages sensitive secrets like API keys and database credentials to ensure they are never exposed in your source code.

- Wiz or Prisma Cloud: We use these for continuous cloud security posture management to identify vulnerabilities before they can be exploited.

- eBPF-based Monitoring: This advanced technology provides deep visibility into your system performance and security without impacting the speed of your transactions.

Selecting a modern and resilient stack ensures your investment is protected against technical debt. This architectural foresight allows you to focus on growing your business while the technology handles the burden of security.

How Much Does It Cost To Build?

Building AI-based merchant risk monitoring tools depends on the level of intelligence, real-time capabilities, and compliance depth required. However, most enterprise builds fall into three tiers.

Total Cost By Build Scope

| Build Scope | Key Capabilities | Timeline | Estimated Cost |

| MVP Risk Monitoring Tool | Rule-based alerts, basic dashboards, and limited integrations | 6–10 weeks | $10,000 – $25,000 |

| Mid-Level AI Risk Platform | AI scoring, real-time alerts, case management, integrations | 10–16 weeks | $25,000 – $60,000 |

| Enterprise AI Risk System | Real-time pipelines, advanced AI models, compliance layers | 16–28 weeks | $60,000 – $80,000+ |

Cost Breakdown By System Component

| Component | % of Total Cost | What Drives Cost |

| Data pipelines and ingestion | 20–25% | Number of data sources and integrations |

| AI model development | 15–20% | Model complexity and training effort |

| Backend and APIs | 15–20% | System logic and scalability requirements |

| Dashboards and workflows | 10–15% | UI complexity and analyst tools |

| Real-time infrastructure | 10–15% | Streaming systems and latency needs |

| Compliance and security | 10–15% | Audit logs, access control, and regulations |

Key Factors That Affect Cost

Several factors can increase or decrease the final investment:

- Number of merchants and transaction volume

- Real-time vs batch processing requirements

- Depth of AI models (basic vs predictive vs graph AI)

- Integration complexity (payment systems, KYB, CRM, etc.)

- Compliance requirements (PCI DSS, auditability, explainability)

- Multi-region and multi-entity support

Cost Of Scaling And Maintenance

Beyond development, ongoing costs include:

- AI model monitoring and retraining

- Cloud infrastructure and data storage

- Compliance updates and audits

- Feature upgrades and integrations

Most enterprises allocate 15–25% of the initial build cost annually for maintenance and optimization.

The investment depends on how advanced the system needs to be. As merchant risk grows more complex, AI-driven monitoring becomes essential for scaling securely and staying compliant.

Conclusion

Building a sophisticated AI risk monitoring system is the smartest move for any growing fintech enterprise. It secures your capital while providing a seamless experience for your honest merchants. This strategic investment turns regulatory compliance into a competitive advantage for your brand.

Deploying elite AI infrastructure is the only way to protect your global payment operations today. Modern business leaders prioritize custom tools that provide deep visibility and empower teams to lead with confidence. Invest in the technology that ensures a secure and scalable future for your digital platform

Build AI Merchant Risk Tools With Intellivon

Developing an enterprise-grade merchant risk monitoring system requires more than simple software deployment. It demands a sophisticated architecture where data ingestion, behavioral analysis, and automated decisioning function as a single unit.

At Intellivon, we build high authority risk infrastructure where machine learning is embedded directly into the payment flow. This approach enables faster merchant onboarding, lower financial exposure, and scalable protection across global ecosystems.

Our systems are designed to handle massive transaction volumes and evolving criminal tactics without impacting your operational performance.

A. Designing Real-Time Risk Decision Architectures

Merchant monitoring is a real-time challenge that requires immediate intervention. We design systems that score every merchant action instantly within the processing lifecycle.

- Low-latency scoring pipelines: These are built for sub-second risk detection to ensure legitimate business continues without interruption.

- Event-driven architecture: High-speed streaming systems process millions of risk signals in real time across your entire portfolio.

- Unified decision engines: Identity, transaction, and behavioral signals converge into a single logic layer for total visibility.

- Inline risk mitigation: Automated actions such as payout holds or step-up verification happen before financial loss occurs.

B. Building Multi-Layered ML Risk Detection Systems

Effective protection requires a diverse combination of analytical strategies. We design layered systems that ensure your platform identifies threats from every possible angle.

- Hybrid model architectures: Supervised, unsupervised, and graph-based models work together to spot hidden laundering rings.

- Feature-rich data pipelines: Behavioral, device, and website signals drive superior model accuracy and reduce false positives.

- Adaptive learning systems: Models continuously evolve by learning from new merchant patterns and historical case data.

- Decision orchestration layers: Complex rules and advanced ML models operate together for surgical precision and control.

C. Embedding Explainability and Compliance Into the Core

Risk systems must be transparent and ready for regulatory scrutiny from day one. We build compliance into the technical architecture rather than treating it as a final step.

- Transaction-level explainability: Every automated risk score is backed by interpretable outputs that your analysts can trust.

- Continuous audit trails: All system actions and human reviews are logged for regulatory reporting and dispute handling.

- Global standards alignment: Systems are designed to meet PCI DSS, GDPR, and regional financial licensing requirements.

- Access governance: Strict role-based controls ensure the secure handling of sensitive merchant and financial data.

D. Integrating Risk Intelligence Across Your Ecosystem

Merchant monitoring only works when it connects across your entire platform. We design integration layers that unify your risk stack into a centralized intelligence source.

- API first architecture: This enables seamless connections with payment gateways, KYB providers, and internal CRM systems.

- Gateway level connectivity: Direct integration with processors and financial systems ensures data is captured at the source.

- Unified risk intelligence: Your leadership team gains a centralized view of merchant signals across all channels and regions.

- Phased system evolution: You can upgrade your risk stack in stages without disrupting your existing payment operations.

At Intellivon, we help you translate complex merchant risks and transaction flows into a clear machine learning architecture and execution roadmap. Talk to our team to design a merchant risk monitoring system tailored to your enterprise and get a detailed project estimate.

FAQs

Q1. Why Are Chargebacks A Major Risk For Payment Processors?

A1. Chargebacks create financial, operational, and compliance exposure for processors, acquirers, PSPs, and PayFacs. High chargeback rates can trigger network penalties, reserve pressure, settlement losses, and fraud investigations. AI-based monitoring helps detect dispute patterns early before they become expensive portfolio-level risks.

Q2. How Can AI Detect Risky Merchants Before Losses Grow?

A2. AI detects risky merchants by analyzing transaction spikes, refund behavior, chargebacks, payout patterns, KYB data, geolocation, device signals, and website changes. It identifies unusual behavior before fixed rules trigger, helping risk teams review merchants earlier and prevent fraud, money laundering, or dispute losses.

Q3. What Risk Signals Should Merchant Monitoring Tools Track?

A3. Merchant risk tools should track transaction volume, velocity, average order value, refunds, disputes, chargebacks, payout behavior, MCC changes, device signals, IP locations, customer complaints, and website content shifts. Together, these signals help detect fraud, category drift, transaction laundering, and operational risk.

Q4. How Do Payment Platforms Monitor Sub-Merchant Risk?

A4. Payment platforms monitor sub-merchant risk by combining KYB data, transaction behavior, chargeback activity, refund trends, payout patterns, and compliance signals. AI can score each sub-merchant continuously, prioritize alerts, and help platforms detect risky accounts before they affect the broader merchant portfolio.

Q5. Can AI Detect Transaction Laundering In Merchant Portfolios?

A5. Yes. AI can detect transaction laundering by comparing merchant profiles, websites, payment descriptors, transaction patterns, customer behavior, and linked accounts. It flags mismatches between approved business activity and actual processing behavior, helping acquirers and PSPs identify hidden merchants or prohibited activity.