Key Takeaways:

-

Compliant agentic collections require deterministic rules to approve every contact attempt and account action.

-

Compliance engine, orchestration layer, RAG knowledge base, predictive models, and human escalation are core requirements.

-

CRM and servicing integrations, payment tools, and audit logs ensure production-grade collections platform governance.

-

Controlled pilots cost $70,000 to $110,000 while enterprise deployments reach $210,000 to $300,000.

-

How Intellivon builds agentic collections platforms by separating probabilistic AI from deterministic compliance enforcement controls.

Every automated message a collections agent sends is a potential FDCPA or TCPA violation. Compliant agentic collections start with the compliance guardrail layer before any contact strategy is built. That layer enforces FDCPA rules, TCPA consent requirements, and CFPB Regulation F contact limits automatically. From there, agents contact debtors by phone, email, and text, with every communication pre-checked for compliance.

The compliance guardrail layer is the most important build decision in agentic collections, not the AI model. Moreover, one unauthorized contact can trigger FDCPA class action liability and CFPB enforcement simultaneously. The CFPB received 207,800 debt collection complaints in 2024, nearly double the prior year. Consequently, the regulatory pressure makes compliance architecture the only acceptable starting point for this build.

Intellivon builds compliant agentic collections platforms for lenders, servicers, and debt buyers. The approach therefore always starts with FDCPA, TCPA, and Regulation F guardrails before anything else. Accordingly, this blog walks through guardrail design, omnichannel orchestration, right-party verification, and propensity scoring. By the end, compliance and build decisions are clear enough to commission this platform.

What Compliant Agentic Collections Mean in Production

An agentic collections system is a bounded framework of specialized software models designed to manage debt recovery within strict regulatory limits. Therefore, agentic does not mean unrestricted autonomy in a live production environment. Instead, these systems evaluate account context, plan approved sequences, use authorized tools, and communicate through permitted channels.

Consequently, they update core ledgers and immediately escalate exceptions to human supervisors.

1. Rules, Predictive Models, Copilots, and Agents Are Different

Enterprise technology leaders often confuse basic automation with autonomous systems. For that reason, understanding the distinct operational boundaries between these technologies is critical for risk management.

| Capability | Primary Function | Can Act Independently? | Compliance Role |

| Rules engine | Determines permitted actions | Yes, deterministically | Final control |

| Predictive model | Scores likelihood or risk | No | Advisory |

| GenAI copilot | Drafts and summarizes | No | Human-reviewed |

| AI agent | Executes approved workflows | Within limits | Evidence-producing |

| Human supervisor | Handles exceptions | Yes | Final authority |

2. Use Four Levels of Collections Autonomy

Deploying an autonomous system requires a structured framework for delegating operational authority safely. Thus, financial institutions use four distinct levels of collections autonomy to mitigate compliance risks.

- Level 0 (Recommendation): The system scores risk and suggests the next action to a human collector.

- Level 1 (Drafting): The AI drafts a communication that a human must review before sending.

- Level 2 (Low-Risk Execution): The system executes basic inbound balance inquiries autonomously.

- Level 3 (Bounded Workflows): The agent completes end-to-end outbound workflows with automated exception escalation.

However, certain high-risk scenarios must always remain under human control. For instance, legal escalation, litigation recommendations, material settlements, bankruptcy, deceased consumers, attorney representation, and vulnerable-customer cases require human empathy and final authority.

3. Compliance Must Operate Before the Agent Acts

Compliance guardrails must function as a strict preventative filter rather than a post-action review. As a result, the system processes every account event through a rigid execution order.

This sequence ensures that the AI collection agent cannot initiate contact without verifying active consent. Finally, every single action generates an immutable evidence log for regulatory auditing.

The core distinction of a production-ready system is structural authority and not conversational quality. Once the autonomy boundary is clear, the platform can safely generate significant operational value.

Where Agentic Collections Create Measurable Business Value

The strongest business case for an agentic collections architecture does not stem from replacing every human collector. Instead, value is generated by consistently working eligible accounts, selecting appropriate channels, preparing compliant payment options, and processing routine responses.

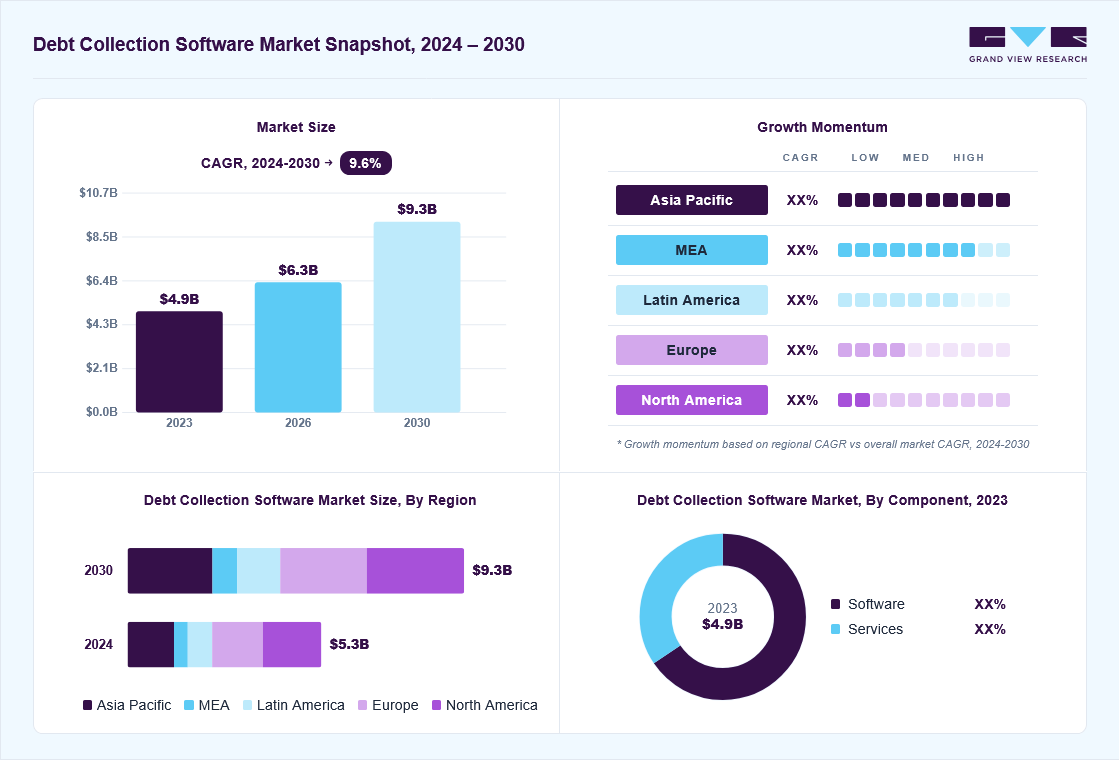

For context, the broader debt collection software market is projected to expand from $6.3 billion in 2026 to $9.3 billion by 2030. However, this growth highlights an infrastructure reality: success depends on directing human attention away from routine tasks and toward complex disputes, hardship cases, consumer vulnerability, and high-value exceptions.

1. Work the Eligible Portfolio, Not Merely the Largest Balances

Traditional collection operations focus exclusively on high-balance accounts because human agent hours are limited and expensive. Consequently, a vast portion of the low-balance, long-tail portfolio remains unaddressed, which accelerates write-offs.

- Long-Tail Account Coverage: Autonomous agents consistently contact low-balance accounts that would otherwise be financially unviable to pursue manually.

- Early-Stage Delinquency: Engaging consumers within the first 1 to 15 days of delinquency prevents accounts from rolling into deeper, harder-to-recover buckets.

- Event-Triggered Outreach: Systems instantly initiate a compliant contact sequence the moment an automated core banking trigger occurs, such as a missed payment.

- Self-Service Account Resolution: Consumers can resolve their outstanding balances entirely on their own terms through intuitive digital portals.

- After-Hours Inbound Assistance: The platform resolves inbound inquiries during evenings and weekends, removing historical staffing constraints.

This transition ensures that no account sits idle due to staff shortages.

2. Improve Kept Arrangements, Not Just Promises to Pay

Measuring success solely by a verbal promise to pay creates inaccurate liquidation forecasts and high broken-promise rates. Therefore, enterprise leaders must evaluate deeper behavioral milestones to ensure real financial recovery.

- Promise-to-Pay Rate: The percentage of consumer interactions in which the individual verbally or digitally agrees to a specific future payment.

- Payment-Plan Acceptance: The rate at which consumers select structured, multi-month repayment options rather than unrealistic lump-sum commitments.

- First-Payment Success: A critical operational milestone checks whether the initial scheduled payment successfully processes without an ACH or card failure.

- 30-, 60-, and 90-Day Kept Rate: The ultimate structural health metric that tracks long-term consumer adherence to the agreed-upon plan.

- Broken-Promise Recovery: The speed and automated efficiency with which the platform re-engages a consumer immediately following a missed payment.

Consequently, the AI agent dynamically proposes optimized payment plans tailored to verified consumer constraints. This systematic design shifts the focus from short-term promises to long-term cash flow predictability.

3. Treat Consumer Protection Metrics as Business KPIs

Regulatory compliance and revenue generation are often viewed as opposing goals, yet consumer protection failures directly destroy profit margins. For that reason, modern enterprise systems treat consumer risk variables as core performance indicators.

- Complaints per 1,000 Accounts: Tracking consumer dissatisfaction indicators filed through the CFPB portal or internal channels.

- Wrong-Party Contacts: Measuring and eliminating instances where an agent discusses a debt with an unrelated third party due to outdated skip-tracing data.

- Opt-Out Processing Time: The speed at which the system registers a “stop” or “do not call” request across all communication channels.

- Dispute Acknowledgement Time: The interval between a consumer disputing a balance and the system freezing automated outreach while generating an automated validation notice.

- Vulnerable-Customer Escalation Rate: The frequency with which the NLP engine accurately detects emotional distress or cognitive impairment and transfers the consumer to a specialized human team.

- Unauthorized Offer Attempts: Audit logs verify that the AI agent never offered a settlement percentage outside pre-approved corporate mandates.

- Suppressed-Contact Failures: Tracking and blocking any system attempt to message a consumer during restricted structural windows or active bankruptcy stays.

This protection infrastructure protects the enterprise from class-action exposure and costly regulatory remediation.

Ultimately, recovery volume alone cannot prove that an autonomous platform is safe and effective for production. The system must improve net financial outcomes while producing fewer uncontrolled actions and stronger compliance evidence. Now that the commercial advantages are clear, we will map out the architectural blueprints required to build this technology securely.

Turn FDCPA, TCPA, and Regulation F Into System Rules

Compliance requirements must become machine-readable conditions, prohibitions, timers, counters, templates, and escalation events. Regulation F explicitly covers communications, harassment, deceptive representations, unfair practices, time-barred debt, validation information, disputes, disclosures, record retention, and state law relationships.

Therefore, engineering teams must build a dynamic compliance layer that screens every action before execution. This approach converts legal prose into strict, deterministic system constraints.

1. Encode Regulation F Communication Controls

Managing communication compliance requires tracking call frequencies, time windows, and consumer preferences in real time. For that reason, the platform translates regulatory parameters into automated operational boundaries.

- Time-Zone-Aware Windows: Outbound attempts occur strictly between 8:00 AM and 9:00 PM local time based on the consumer’s zip code.

- Inconvenient Places: The system dynamically flags and blocks contact during consumer-specified inconvenient hours or employment settings.

- Frequency Presumptions: The platform tracks the seven-call threshold to maintain a legal presumption of compliance under CFPB guidelines.

- Cease-Communication Requests: Verbal or written “stop” requests trigger an immediate, permanent block on all outbound activity.

- Work Email Bans: The system purges employer-provided email domains to prevent unauthorized third-party debt disclosures.

Time-sensitive database triggers calculate local consumer time before any communication gateway opens. For a deeper breakdown of compliant interaction models, see our guide on [compliant agentic agents for collections development]. This ensures the system remains compliant even across multiple changing time zones.

2. Automate Disclosures and Validation Notices Carefully

Automating consumer notices requires precise data mapping and exact language delivery to maintain regulatory safe harbors. Consequently, the platform controls the exact format and timing of every required disclosure.

- Initial Mini-Miranda: The NLP engine enforces mandatory legal disclosures during the very first consumer interaction.

- Model Validation Letters: The system generates physical or digital validation notices that exactly match the CFPB layout.

- Multi-Language Options: The platform dynamically delivers Spanish-language versions based on documented consumer preferences or regional mandates.

- Itemization Tracking: Every notice accurately populates the exact itemization date, principal balance, fees, and payments.

- Dispute Window Management: The system automatically tracks the 30-day dispute window, freezing collections if a consumer objects.

Immutable document templating engines prevent any manual or AI-generated modification to approved legal language. Thus, the system eliminates text hallucinations during critical disclosure steps. This structural enforcement protects the enterprise from technical disclosure violations.

3. Build TCPA Consent and Channel Controls

Telephone Consumer Protection Act compliance requires strict verification of consumer consent and phone number ownership. As a result, the architecture connects directly to consumer consent databases prior to launching any digital outreach.

- Consent Scope Verification: The system verifies that the historical consent record covers the specific outbound channel utilized.

- Number Portability Checks: Regular database queries verify that the phone number has not been reassigned to a different individual.

- Autodialer Rules: The dialing infrastructure shifts execution strategies based on whether the line is a cell phone or a landline.

- SMS Opt-Out Processing: Incoming keywords like “QUIT” or “UNSUBSCRIBE” instantly terminate the SMS gateway link for that account.

- State-Level Overlays: The platform applies stricter state-specific quiet hours, such as Florida’s tighter telemarketing windows.

Real-time phone verification APIs integrate directly into the pre-flight routing microservice. Therefore, the system automatically drops call attempts if number ownership cannot be verified. This layer mitigates the risk of high-cost TCPA statutory fines.

4. Add State-Law and Licensing Versioning

Because debt collection regulations vary significantly by state, a centralized compliance engine must dynamically adapt to the consumer’s location. Thus, the platform utilizes a real-time jurisdiction matrix to enforce localized rules.

| Rule Event | Machine Condition | Blocked Action | Required Evidence |

| Cease request | Active cease flag | Further collection contact | Request transcript and timestamp |

| Open dispute | Dispute status active | Unsupported collection progression | Dispute case and source records |

| No verified party | Identity confidence low | Debt disclosure | Authentication result |

| Offer outside authority | The offer exceeds the matrix | Settlement communication | Offer-policy version |

| Missing consent | Channel permission absent | Automated call or message | Consent record |

This structural matrix updates automatically via API whenever state collection laws change. Consequently, the platform protects multi-state organizations from localized compliance oversights. This granular control ensures seamless adherence to regional variations like the California Rosenthal Act.

5. Add FCRA, Privacy, and Medical-Debt Overlays

When managing specialized asset classes like healthcare accounts receivable, the system must layer additional privacy protections over standard collection rules. For that reason, data isolation and strict access controls are mandatory.

- FCRA Dispute Isolation: The system halts active credit bureau reporting the moment a consumer disputes a balance accuracy status.

- Metro 2 Precision: The platform formats all credit data updates into the exact Metro 2 standard to ensure data reporting accuracy.

- HIPAA Data Safeguards: The system encrypts and masks all Protected Health Information, exposing only the minimum necessary financial data.

- Charity-Care Verification: The AI screens medical debt against hospital financial assistance guidelines before initiating any recovery workflows.

Secure, zero-trust data pipelines isolate clinical data from financial interaction logs. Thus, the autonomous agents operate effectively without ever exposing sensitive consumer medical histories. This design satisfies both strict healthcare privacy laws and financial reporting mandates.

This structured compliance architecture is the exact layer that market competitors typically discuss only in broad, non-technical terms. Once all legal requirements become executable code rules, the platform enforces them with absolute consistency. Next, we will examine the actual multi-agent system architecture required to run these rules in production.

Design the Architecture for Compliant Agentic Collections

An agentic collections platform relies on a layered architecture to maintain strict enterprise controls. At the same time, data, policy, agent reasoning, tools, and audit evidence must remain completely separable so teams can instantly identify why an action occurred and which control authorized it.

This decoupling ensures that raw probabilistic LLM outputs never directly touch consumers or live databases without passing through rigid, deterministic filters.

The Seven Operational System Layers

To manage autonomous recovery safely, engineering teams must organize platform capabilities into distinct functional zones. The table below outlines how these layers map from data storage to final execution.

| Layer | Component Focus | Production Responsibility |

| Layer 1 | Data & Account State | Tracks balances, delinquency stages, bankruptcy statuses, and channel consent records. |

| Layer 2 | Identity & RPC Verification | Manages knowledge-based authentication, one-time passcodes, and third-party disclosure suppression. |

| Layer 3 | Compliance Policy Engine | Enforces policy-as-code, contact counters, state-law matrices, and decision reason codes. |

| Layer 4 | Orchestration & Memory | Directs specialized-agent routing, idempotency checks, and human-in-the-loop interrupts. |

| Layer 5 | AI Models & Regulatory RAG | Runs intent classifiers, propensity models, sentiment tracking, and compliance knowledge bases. |

| Layer 6 | Controlled Tool Gateway | Validates outbound messages, arrangement creations, payment processing, and core servicing updates. |

| Layer 7 | Audit & Observability | Generates immutable event IDs, model version logs, policy versions, and transcripts. |

For a deeper breakdown of coordinating specialized agents across these layers, see our guide on [Enterprise AI Agent Orchestration Platform Development]. The control plane enforces strict data boundaries between these steps to prevent security failures.

The policy engine strictly dictates what is legally permitted to happen, while the orchestrator determines which specialized agent should perform the work. By separating policy from reasoning, the architecture delivers absolute compliance alongside autonomous efficiency.

Choose the First Agents in a Multi-Agent Collections System

Deploying a single, general-purpose debt collection agent in production introduces severe compliance risks. Instead, enterprise technology leaders should start with five to seven bounded agents working within a multi-agent framework.

Each specific agent operates with its own restricted data access, permitted tools, strict output schemas, assigned risk levels, and automated human escalation rules. This structural segregation prevents a single model failure from compromising the entire recovery pipeline.

The Specialized Multi-Agent Framework

To maintain absolute control over autonomous workflows, engineering teams deploy isolated agents with narrow functional mandates. The following components represent the foundational building blocks of a compliant agentic collections system.

- Account Eligibility Agent: This system component validates account ownership, balance freshness, active dispute statuses, recall positions, bankruptcy filings, deceased statuses, legal representation, and statute limitations. Crucially, it never initiates contact with the consumer.

- Contact Strategy Agent: This model recommends the optimal channel, contact timing, language, message objective, and contact cadence based on historical data. However, the centralized policy engine must explicitly approve every recommendation before execution.

- Right-Party Verification and Disclosure Agent: This agent handles identity challenges, knowledge-based authentication, and one-time passcodes before displaying or discussing any sensitive debt information.

- Payment Arrangement Agent: It presents only financial options returned by a deterministic corporate offer service. While it can explain terms, it cannot invent settlement percentages, interest waivers, payment dates, fee concessions, or hardship parameters.

- Dispute and Consumer-Request Agent: This tool instantly detects and processes validation requests, cease requests, wrong-party claims, fraud claims, and bankruptcy assertions to halt automated sequences.

- Payment and Reconciliation Agent: This functional model generates secure payment links, confirms transactions, records promise-to-pay events, and reconciles statuses with the core servicing platform.

- Compliance Supervisor Agent: Operating as an internal auditor, this agent reviews transcripts and proposed text actions against historical templates but cannot override deterministic platform prohibitions.

These independent agents create an auditable, structural division of operational responsibility across the entire lifecycle of an account. By enforcing these specialized boundaries, the architecture ensures that every decision remains completely trackable.

The next section will demonstrate exactly how these components cooperate safely during a live collection journey.

Map the End-to-End Autonomous Collections Workflow

A production-ready agentic collections workflow does not begin with an outbound message. Instead, it starts by evaluating whether any recovery action is legally permitted for a given account asset. This multi-step process routes every transaction through explicit validation checks before a consumer ever receives a notification.

By establishing this sequence, the framework guarantees that compliance constraints completely dictate the operational lifecycle of the account.

The 7-Step Operational Lifecycle

To guarantee absolute compliance, every delinquent account must progress through a sequence of strict architectural checkpoints. The system executes this structured workflow sequentially to prevent unauthorized outreach.

1. Receive and Validate the Account Event

The platform ingests account data from the core system of record. It instantly validates balance freshness, creditor ownership, structural data completeness, account status, and duplicate placements before initiating any logic.

2. Determine Eligibility and Jurisdiction

The system maps the specific debt type, consumer location, governing state rules, collector license status, and time-barred status. Consequently, it suppresses the account if any localized regulatory barrier exists.

3. Select an Approved Contact Strategy

Predictive models recommend the optimal channel and contact timing based on historical consumer patterns. Next, deterministic business rules explicitly review and either approve or reject the recommended contact strategy.

4. Verify the Right Party

The communication gateway opens but completely suppresses creditor, balance, or debt details. Therefore, the agent must successfully complete required identity controls before disclosing any private account information.

5. Complete the Permitted Conversation

Once authenticated, the conversational agent can explain the account, answer approved questions, and present authorized payment arrangements. It can also capture hardship details or send a link to a secure self-service portal.

6. Process Exceptions Immediately

The system constantly monitors input strings for high-risk triggers. It immediately halts the automated workflow if the consumer mentions disputes, fraud, bankruptcy, legal representation, illness, wrong numbers, or death.

7. Update Systems and Produce Evidence

Finally, the platform writes the transaction outcome to the loan servicing software, CRM, and payment processors. Every entry uses a shared, immutable event ID to construct an unalterable compliance audit trail.

This runtime execution path ensures that no autonomous agent can operate outside your established corporate parameters. Once this operational cycle is mapped out, engineering teams can focus on the specific technical steps required to build these capabilities. Next, we will break down the precise development methodologies and engineering requirements needed to assemble this system.

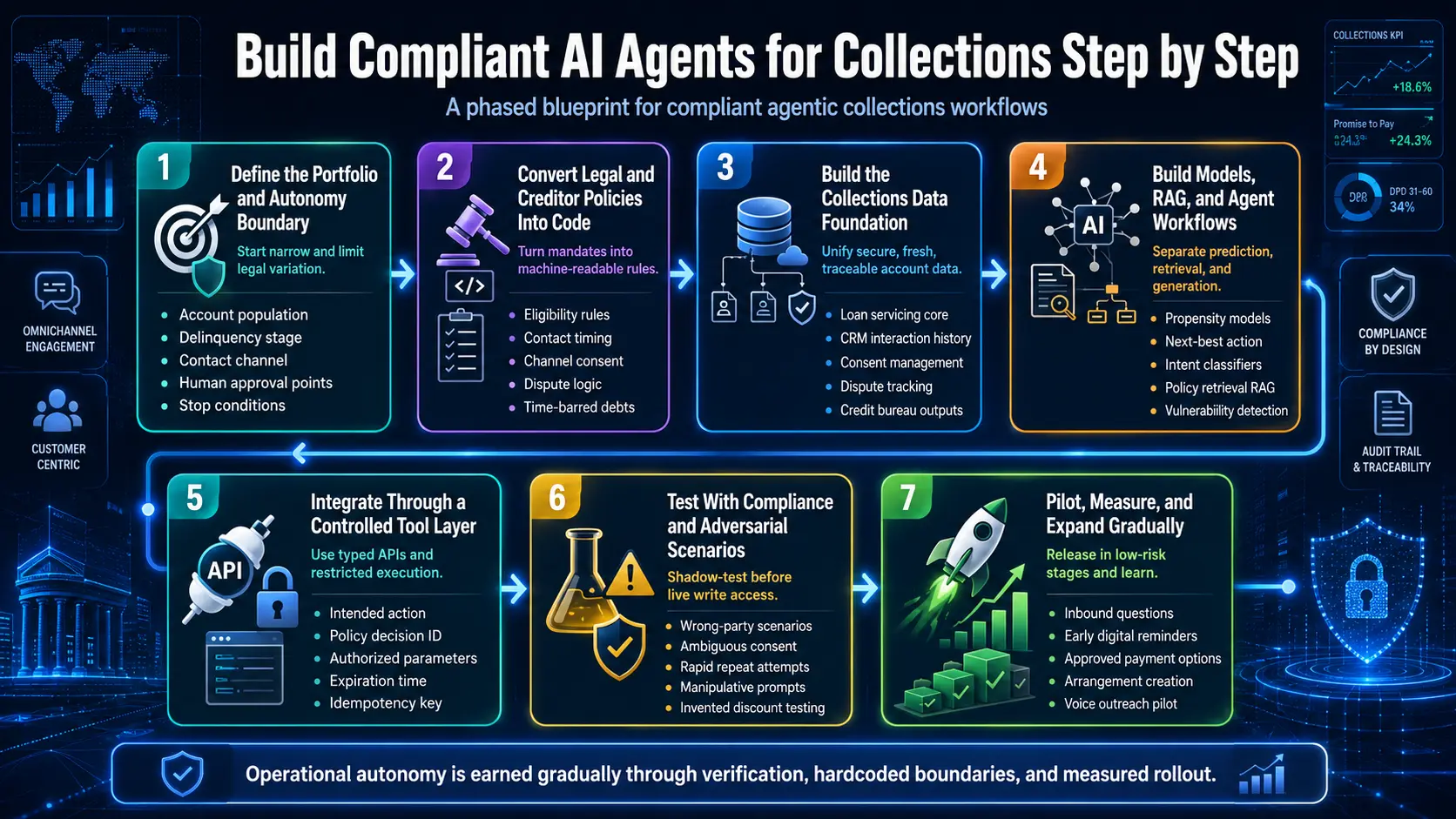

Build Compliant AI Agents for Collections Step by Step

Building a custom production platform requires moving systematically from isolation to full orchestration. Engineering teams must avoid launching a single, general-purpose LLM wrapper across all accounts.

Instead, companies construct compliant agentic collections workflows by establishing clear operational boundaries, normalizing data, and hardcoding strict verification gates.

Step 1 — Define the Portfolio and Autonomy Boundary

Begin by targeting one specific portfolio, delinquency stage, jurisdiction group, and communication channel. At the same time, a broad launch across every single debt type creates too many legal variations for a controlled first release.

- Account Population: Define the exact group of borrowers entering the autonomous workflow.

- Debt Ownership: Map whether the debt belongs to the original creditor or a third-party buyer.

- Delinquency Stage: Restrict the initial phase strictly to early-stage balances, such as 1 to 30 days past due.

- Contact Channels: Limit the initial outbound delivery to a single channel, like SMS or email.

- Available Remedies: Lock down the permitted payment structures and authorized discount parameters.

- Excluded States: Automatically filter out complex account states like active bankruptcies or legal representation.

- Human Approval Points: Pinpoint the exact moments where an agent must pause for human review.

- Success Metrics: Track the right-party contact rate, fulfillment percentage, and net liquidation.

- Stop Conditions: Code immediately shuts down if the platform detects any system latency anomalies.

Step 2 — Convert Legal and Creditor Policies Into Code

Translate qualitative regulatory mandates into explicit, machine-readable validation logic. Therefore, do not place raw legal PDFs directly into an LLM context window and ask the model to determine compliance.

- Eligibility Rules: Code automated queries to check active collection licenses before analyzing an account.

- Contact Timing: Set server-side clocks to block outbound channel gateways outside permitted state hours.

- Contact Frequency: Implement real-time tracking arrays to count all outbound attempts across all communication channels.

- Channel Consent: Establish an explicit consent check that blocks routing if an opt-out marker is present.

- Disclosure Enforcers: Bind mandatory legal text, like the Mini-Miranda, directly to the messaging template payload.

- Dispute Logic: Program the system to freeze automated outreach the millisecond a dispute trigger word matches.

- Opt-Out Handling: Map structural processing pipelines to apply “STOP” requests immediately across the entire database.

- Offer Boundaries: Hardcode strict mathematical limits for settlements into a secure business rules management system.

- Fee Constraints: Enforce deterministic logic that blocks the addition of unauthorized convenience fees.

- Time-Barred Debts: Flag out-of-statute accounts to prevent automated payment demands or credit reporting threats.

Step 3 — Build the Collections Data Foundation

Normalize disparate structural records from across the enterprise into a unified, secure data layer. Additionally, add data freshness, clear provenance, and confidence indicators to every single material field.

- Loan Servicing Core: Ingest the active principal balance, contract parameters, and original delinquency date.

- Core Banking Systems: Link real-time checking account statuses to verify funds before processing scheduled transactions.

- CRM Interaction History: Surface all historical collector notes, call attempts, and past promises to pay.

- Payment Processor Links: Connect directly to ACH and card networks to track settlement statuses instantly.

- Dialer Call Records: Monitor all prior outbound dial logs to maintain precise communication frequency counters.

- Consent Management System: Store time-stamped opt-in records along with the specific authorized channels.

- Dispute Tracking Repositories: Centralize documented customer objections, validation demands, and internal research files.

- Credit Bureau Outputs: Maintain copies of active Metro 2 reporting files to ensure credit alignment.

Step 4 — Build Models, RAG, and Agent Workflows

Deploy separate, specialized machine learning components rather than relying on an all-in-one conversational model. At the same time, keep payment calculations, eligibility criteria, and write permissions completely outside the core LLM boundary.

- Propensity Models: Run machine learning algorithms to score a consumer’s underlying statistical likelihood to resolve a balance.

- Next-Best Action: Use predictive models to select the most effective, compliant channel for outreach.

- Intent Classifiers: Deploy narrow natural language processing models to identify consumer objections and requests accurately.

- Language Generation: Use bounded generative models restricted to pre-approved corporate phrasing libraries.

- Policy Retrieval RAG: Connect an orchestration layer to index internal credit policies and specific state regulations.

- Conversation Summarization: Program automated models to extract clear, structured interaction notes after each conversation ends.

- Vulnerability Detection: Utilize specialized sentiment analysis models to capture markers of cognitive or financial hardship.

Step 5 — Integrate Through a Controlled Tool Layer

Create strongly typed, secure APIs for every individual system action. Consequently, autonomous agents must never have direct write access to databases, payment systems, or communication gateways.

- Account ID: Pass the unique, system-generated internal identifier for the target customer record.

- Intended Action: Specify the exact function requested, such as sending a message or updating a status.

- Policy Decision ID: Require a verified confirmation token from the compliance engine before execution.

- Authorized Parameters: Enforce strict data schemas that limit variables like maximum settlement discount percentages.

- Model Version: Log the precise LLM version and prompt configuration hash that generated the request.

- Requester Identity: Tag the specific specialized agent microservice initiating the API transaction call.

- Expiration Time: Apply short time-to-live timestamps to prevent the execution of stale automated actions.

- Idempotency Key: Attach unique tracking hashes to eliminate the risk of duplicate payments or repeat messages.

Step 6 — Test With Compliance and Adversarial Scenarios

Run the entire platform in a strict shadow execution mode before enabling any live production write capabilities. At the same time, engineering teams frequently use shadow testing and unalterable action history logs to confirm system safety during regulatory readiness reviews.

- Wrong-Party Scenarios: Verify that the platform terminates communication if the target identity cannot be verified.

- Ambiguous Consent: Test how the NLP engine processes confusing consumer statements like “stop calling me at work.”

- Rapid Repeat Attempts: Force the simulation layer to attempt rapid-fire messages to verify that frequency caps hold.

- Reopened Balance Disputes: Confirm that entering a new dispute instantly freezes active automated collection sequences.

- Partial Payment Rules: Check that the ledger updates correctly without generating an incorrect broken-promise flag.

- Changed Phone Numbers: Verify that third-party data changes trigger an immediate reset of active consent markers.

- Manipulative Prompts: Attempt to inject adversarial prompts designed to trick the agent into waiving a balance.

- Invented Discount Testing: Ensure the system blocks any agent’s attempt to offer an unapproved settlement percentage.

Step 7 — Pilot, Measure, and Expand Gradually

Transition capabilities into production using a conservative, multi-phased release schedule. For a deeper breakdown of separating deterministic rules from probabilistic financial AI, see our guide on [How to Build AI Agents for Banking Compliance and AML].

- Inbound Questions: Launch the pilot by resolving routine consumer balance checks and payment portal navigation requests.

- Early Digital Reminders: Introduce automated, low-risk digital notifications for accounts that are under five days past due.

- Approved Payment Options: Allow the system to present standard, pre-calculated installment plans via digital interfaces.

- Routine Arrangement Creation: Enable the agent to log structured promises to pay directly into the servicing platform.

- Voice Outreach Pilot: Transition into active outbound voice interactions within strict, single-state jurisdiction boundaries.

A compliant recovery platform earns operational autonomy gradually through continuous verification and hardcoded structural boundaries. Once these baseline technical steps are established, engineering teams must evaluate the total capital required to construct and support this architecture.

Next, we will break down the complete financial investment and development timelines necessary to launch a production-ready system.

Integrate Agents With Servicing, CRM, Payments, and Dialers

Integration quality directly controls account accuracy within an agentic collections infrastructure. For that reason, a fluent conversational agent connected to stale balances, incomplete disputes, or delayed payments creates far greater regulatory risk than a basic automated workflow linked to reliable systems.

Consequently, engineering teams must build bidirectional, low-latency API wrappers around every core system. This integration architecture ensures that the autonomous agent constantly evaluates real-time data before executing any outbound consumer interaction.

The Enterprise Core Integration:

To maintain an accurate account state, the platform orchestrator must coordinate data flows across several distinct enterprise software environments. Therefore, the system balances these connections to prevent broken consumer promises and misreported balances.

- Systems of Record: The platform links directly to core banking databases, loan servicing platforms, patient accounting architectures, and enterprise resource planning (ERP) ledgers. This includes synchronizing financial data across platforms like FIS, Fiserv, Jack Henry, ICE Mortgage Technology, Sagent, Epic, Oracle, SAP, and Microsoft Dynamics.

- Customer Engagement Systems: The system routes communication payloads through Salesforce, Dynamics, Five9, Genesys, and NICE interfaces. It manages automated IVR scripts, SMS gateways, email providers, and digital customer self-service portals.

- Payments and Reconciliation: The framework orchestrates tokenized card processing, ACH networks, secure payment links, and recurring plan authorizations. It also handles returned payments, chargebacks, real-time payment rails, and ledger updates.

- Credit Reporting and Dispute Systems: The platform formats data into the Metro 2 standard for bureau furnishing. It syncs dispute statuses, logs account corrections, routes files through e-OSCAR systems, and generates compliance evidence packages.

For a deeper breakdown of connecting agents with older enterprise platforms, see our technical guide on [Build AI Agents for Legacy ERP Systems]. Therefore, building these secure pipelines protects the institution from executing outreach on recently cleared balances.

Reliable, transactional integrations keep the agent’s internal view of the portfolio current and accurate. Furthermore, robust governance frameworks prove that every resulting action remained entirely within approved corporate boundaries.

Agentic Collections Development Cost: $70K–$300K

An agentic collections platform development usually costs $70,000 to $300,000, depending on agent scope, communication channels, jurisdictions, integrations, model requirements, payment workflows, security controls, and compliance-validation depth. These capital projections represent Intellivon planning estimates for custom engineering rather than fixed, universal vendor pricing packages.

For that reason, total capital deployment varies based on whether an enterprise requires an early-stage validation pilot or a multi-tenant SaaS infrastructure layer.

1. Controlled Compliance Pilot — $70,000 to $110,000

This baseline investment tier targets institutions seeking to validate core automation within a restricted, low-risk environment. Consequently, it establishes a predictable proof of concept before expanding deep architectural system permissions.

- Portfolio Scope: Limited strictly to one specific consumer asset class, such as early-stage credit card debt.

- Delinquency Range: Focuses exclusively on early-stage accounts ranging from 1 to 30 days past due.

- Channel Routing: Restricts outbound interaction methods to one or two low-risk digital channels, specifically email and text messaging.

- Agent Architecture: deploys three to four highly bounded agents managed by a centralized orchestration engine.

- System Connections: Integrates with a single core system of record, mapping data fields out of a loan servicing core database.

- Payment Boundaries: Provides pre-approved payment matching options, requiring immediate human collector approval for any material settlement adjustments.

- Delivery Timeline: Standard engineering deployment ranges from 12 to 16 weeks from initial technical discovery.

2. Production Collections Platform — $120,000 to $200,000

This mid-tier implementation delivers an end-to-end autonomous collection environment optimized for live, active mid-market recovery portfolios. Thus, it features deep operational integrations alongside a dynamic, real-time compliance matrix.

- Portfolio Scope: Manages diverse portfolios across multiple advancing delinquency stages simultaneously.

- Channel Routing: Executes coordinated omnichannel outreach using automated voice, SMS gateways, emails, and customer self-service portals.

- Agent Architecture: Operates five to seven independent, specialized agents handling verification, arrangement creation, and exception routing.

- System Connections: Hooks directly into multiple enterprise banking systems, customer relationship managers, and payment processors.

- Compliance Logic: Enforces a versioned, machine-readable state rule matrix to block outreach during restricted hours dynamically.

- Feature Extensions: Processes real-time digital payment plan executions and provides structured dispute intake flows.

- Delivery Timeline: Assembling and validating this production-grade architecture requires five to eight months of development.

3. Enterprise or White-Label Platform — $210,000 to $300,000

This elite engineering tier is designed specifically for high-volume third-party collection agencies, multinational banks, and large healthcare hospital networks. Therefore, the architecture supports extensive multi-tenancy and advanced security isolation protocols.

- Portfolio Scope: Orchestrates complex multi-state recovery operations across thousands of unique concurrent creditor portfolios.

- Channel Routing: Integrates high-volume conversational voice agents capable of managing inbound and outbound phone calls at scale.

- System Connections: Connects seamlessly across legacy mainframes, modern cloud ERP architectures, and localized loan servicing software interfaces.

- Compliance Logic: Embeds custom financial offer computation engines alongside advanced, audit-ready AI model governance platforms.

- Feature Extensions: Deploys white-label management dashboards, multi-tenant database partitions, and isolated private cloud infrastructure setups.

- Delivery Timeline: Implementing this comprehensive enterprise infrastructure layer requires eight to eleven months of active development.

4. Development Phase Cost Breakdown

To assist technology leaders with capital allocation, engineering tasks are divided into explicit financial phases. The table below highlights the estimated investment ranges associated with each milestone.

| Phase | Estimated Cost Range |

| Discovery & Compliance Mapping | $8,000 – $18,000 |

| Data & Platform Architecture | $12,000 – $30,000 |

| Agents & Policy Engine Code | $25,000 – $70,000 |

| Enterprise Core Integrations | $15,000 – $60,000 |

| Testing, Security & Validation | $8,000 – $32,000 |

| Deployment & Observability Setup | $5,000 – $25,000 |

| Enterprise SaaS Extensions | $20,000 – $65,000 |

These phase ranges are not strictly additive across every individual customer engagement. For example, a specialized mid-market business may completely bypass enterprise white-label extensions, keeping total costs within the initial production tier.

5. Managing Ongoing Infrastructure Costs

Operating a live platform requires planning for continuous maintenance beyond the initial engineering expense. For that reason, organizations must budget 15% to 25% of the initial development cost annually to support ongoing operations:

Specifically, these funds support continuous model monitoring, state-level regulatory code updates, policy alterations, core integration maintenance, annual security vulnerability testing, prompt performance evaluations, cloud infrastructure optimization, and immediate incident response coordination.

6. Primary Drivers of Development Costs

Understanding the underlying variables that shift engineering complexity helps teams manage their technical roadmap. The following factors directly influence where a project lands within our budgeting tiers:

- Jurisdiction Count: Expanding from a single-state portfolio to a nationwide, multi-state operation dramatically increases compliance rule complexity.

- Channel Complexity: Implementing real-time, conversational voice agents requires more engineering effort than digital-only text setups.

- Integration Density: Connecting to five legacy banking platforms creates higher integration costs than linking to a single database.

- Data Quality: Stale, fragmented data requires extensive custom data normalization pipelines before the engine can operate safely.

- Payment Customization: Processing complex real-time ACH transactions increases validation logic compared to sending simple external checkout links.

Instead, sustainable cost efficiency comes from limiting the first production release to a tightly bound portfolio, a single channel set, and a strict autonomy boundary. Once these core compliance boundaries are running safely, the platform can scale its operational reach without introducing legal risks. Next, we will address the most common technical questions enterprise technology leaders raise during infrastructure design.

Build Compliant Agentic Collections With Intellivon

Intellivon operates as a specialized enterprise development partner for organizations requiring more than basic AI voice wrappers or standard reminder bots. Our engineering team builds end-to-end production infrastructure.

Consequently, the work comprehensively covers policy architecture, multi-agent orchestration, data integration, model development, payments, security, compliance evidence, testing, deployment, and MLOps.

- Compliance Architecture: The platform converts counsel-approved FDCPA, Regulation F, TCPA, state, privacy, dispute, and creditor requirements into versioned, executable code controls.

- Bounded Multi-Agent Workflows: The architecture strictly separates core operational responsibilities, dividing task loads between independent account eligibility, contact strategy, verification, negotiation, dispute, payment, and compliance-review agents.

- Enterprise Integrations: We securely connect autonomous orchestrators directly into legacy loan servicing platforms, CRM environments, contact centers, third-party payment gateways, identity validation services, and credit reporting systems.

- Controlled AI Infrastructure: The framework isolates probabilistic large language models and prediction systems completely from deterministic legal boundaries, absolute offer thresholds, and real-time tool-authorization decisions.

- Production Governance Pipelines: Systems deploy with strict shadow execution capabilities, generating immutable audit evidence packages alongside human collector override mechanisms, continuous telemetry monitoring, and rapid safety rollbacks.

- Flexible Deployment Options: Engineering workflows support private cloud partitioning, hybrid network configurations, highly isolated multi-tenant SaaS environments, and comprehensive corporate white-label platform management.

Discuss a custom agentic collections platform architecture with Intellivon’s fintech AI engineering team today to securely modernize your portfolio workflows.

Conclusion

Building an operational agentic collections architecture requires moving completely past unconstrained chat models. Instead, enterprise technology teams must implement strict, multi-agent frameworks that isolate probabilistic language generation behind hardcoded compliance validation filters.

Consequently, this engineering approach helps financial institutions safely maximize portfolio liquidation rates while generating unalterable regulatory evidence trails. Ultimately, managing debt recovery with bounded autonomous systems transforms modern collection operations into a highly predictable, compliant financial infrastructure layer.

FAQs

Q1. Is an Agentic AI Collections Platform Legal Under the FDCPA?

Legality depends on the collector, debt type, communication channel, conduct, disclosures, jurisdiction, and implementation. Deploying autonomous technology does not create a regulatory exemption. Therefore, the platform must enforce applicable FDCPA and Regulation F requirements before executing any collection action.

Q2. Can a TCPA-Compliant Agentic Collection Agent Call or Text Consumers?

A2. Yes, but the platform requires channel-specific consent records, rapid revocation processing, number validation, do-not-call controls, and strict time restrictions. The FCC classifies AI voices as artificial speech under the TCPA. Consequently, legal counsel must define the exact consent standard required for each communication workflow.

Q3. Can an AI Agent Negotiate Settlements Without Human Approval?

A3. The agent may present specific options generated by a deterministic offer engine when all amounts, dates, concessions, and eligibility conditions fall within pre-approved limits. However, material exceptions, legal claims, consumer hardship cases, and offers outside the corporate matrix instantly require human collector approval.

Q4. What Happens When the AI Contacts the Wrong Person?

A4. The platform immediately stops debt disclosures, captures the wrong-party status, and suppresses the phone number. It flags identity data, prevents cross-channel contact, investigates the source record, and retains strict audit evidence. Crucially, the system avoids asking the unverified recipient to authenticate a debt that is not theirs.

Q5. Does the Platform Need a Special Collections LLM?

A5. A general enterprise LLM successfully supports language tasks when grounded through RAG and controlled tools. However, the architecture still requires dedicated intent classifiers, predictive propensity models, deterministic business rules, strict data validation pipelines, output checking frameworks, and task-specific evaluation metrics.

To Sum It Up

- An AI collection agent should never decide whether contact is lawful. It should receive that decision from a versioned compliance engine.

- A promise-to-pay rate can rise while actual portfolio performance falls. Measure 30-, 60-, and 90-day kept arrangements.

- The most dangerous hallucination is not an awkward sentence. It is an unauthorized message, settlement, payment, disclosure, or account update.

- A $70,000 pilot should prove one bounded workflow. Trying to cover every debt type, state, and channel turns the pilot into an uncontrolled enterprise build.