Key Takeaways:

-

Legacy banking systems batch-process and go offline. A 24/7 enterprise platform never does, and that gap directly affects revenue, retention, and global competitiveness

-

Always-on infrastructure is not an IT decision. It sits at the intersection of product strategy, compliance architecture, and customer experience

-

The difference between a platform that scales and one that breaks is decided during the architecture phase, not after launch

-

Outages in financial services cost between $1.8M and $2.2M per hour, making infrastructure resilience a direct line item on the P&L

-

Building this right requires event-driven architecture, real-time data synchronization, global compliance automation, and multi-region failover, each layer engineered to work as a single resilient system

The banking infrastructure running most enterprise operations today has a tolerance issue, which is a long-standing willingness to accept downtime, settlement delays, and outdated systems as the unavoidable cost of operating at scale.

That tolerance is getting expensive. Enterprise clients now work across time zones, currencies, and regulatory environments at the same time. Their banking infrastructure needs to keep up, without downtime or manual work.

The change goes beyond understanding emerging tech, where finance teams at large organizations expect real-time visibility across all the tools they use. When their banking platform needs a 24-hour settlement cycle or goes offline for maintenance, this gap creates operational friction that can grow quickly at scale. A 24/7 enterprise banking platform is now a must-have for keeping up with the changing fintech environment. Organizations that see it as a future goal are already lagging behind those that adopted it two years ago.

At Intellivon, we create these platforms for enterprises that can’t afford to operate any other way. What we cover in this blog comes directly from our experience, which includes architecture, compliance, scalability, and go-live strategy, and how we build these platforms from the ground up.

Why Do Banks Need 24/7 Functioning Platforms Today?

Customer expectations have fundamentally shifted. A 2024 Forrester report found that 65% of U.S. banking customers want to complete any financial task through a mobile app. For tens of millions of users, that app is now the primary banking channel.

Therefore, any unplanned downtime or after-hours unavailability erodes trust, accelerates churn, and hands a competitive edge to institutions that stay online.

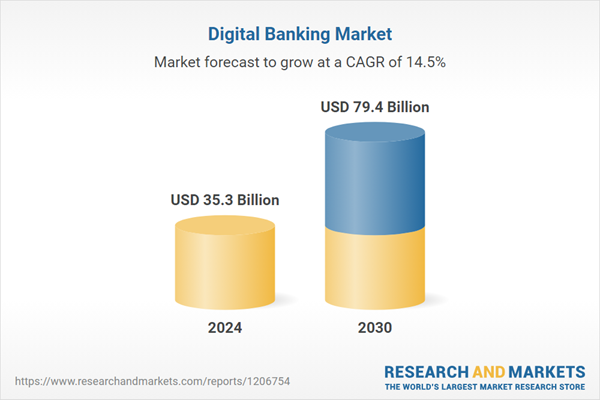

The market itself confirms the urgency. The global digital banking market is projected to grow from USD 35.3 billion in 2024 to USD 79.4 billion by 2030, at a 14.5% CAGR. That trajectory doesn’t reward those organizations whose systems are already built for scale.

1. Market Demand Is Always-On

Banking behavior has shifted to digital-first and self-serve. Customers now expect to open accounts, move money, and resolve issues on their own schedule.

They no longer compare their banking experience against other banks. Instead, they compare it against the best digital experience they’ve had anywhere. That bar keeps rising, and it shows no sign of leveling off.

2. Downtime Is Expensive

Given that baseline expectation, any service interruption carries immediate consequences. Financial services carry some of the highest penalty rates for outages across any industry.

According to New Relic, high-impact outages in financial services cost approximately $1.8 million per hour on average.

A separate 2025 report placed the median even higher, at $2.2 million per hour. Those losses go beyond technical disruption. They hit revenue, productivity, and customer confidence simultaneously.

3. Availability Drives Retention

However, the cost of unavailability isn’t always measured in outage hours. A 24/7 platform is also a retention strategy. Recent banking studies show customers are increasingly willing to move funds or switch providers after a single poor experience.

Silent switching is becoming more common, where customers quietly spread balances across institutions without ever formally leaving. Therefore, service gaps on weekends, overnight, or during outages directly weaken wallet share over time.

4. Competitive Pressure Is Now Structural

In addition to retention risk, there is a structural competitive shift underway. Neobanks and digital-native competitors have permanently reset the baseline for speed and availability. Seamless self-service and always-on access are no longer differentiators.

They are entry requirements. As a result, 24/7 infrastructure has moved out of the IT department’s remit and into the product experience itself.

Building a 24/7 enterprise banking platform is therefore not a technology upgrade. Instead, it is a strategic decision that directly determines how well an organization competes, retains customers, and weathers operational disruption.

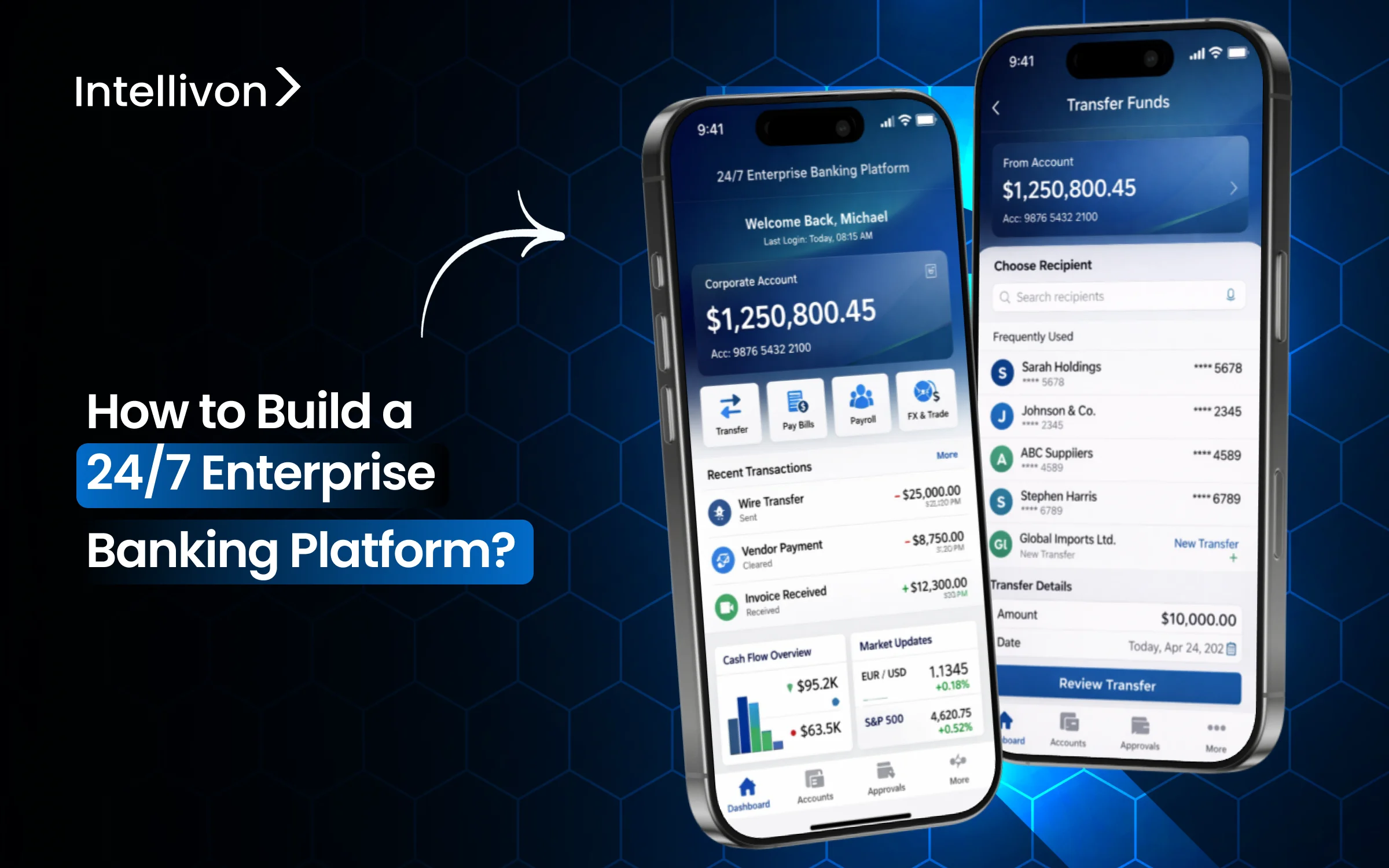

What Is a 24/7 Enterprise Banking Platform?

A 24/7 enterprise banking platform is a continuously operational financial infrastructure that processes transactions, manages accounts, and delivers banking services without downtime or business-hour restrictions.

It combines core banking engines, API-driven integrations, real-time payment rails, compliance automation, and multi-entity support into a single unified system.

Built for scale, it serves large organizations across multiple geographies, currencies, and regulatory environments, while maintaining security, availability, and performance at all times.

Difference From Core Banking Platforms

Traditional banking infrastructure was never designed for the modern “always-on” economy. Most legacy systems operate on batch-processing cycles, which essentially means they “sleep” at night to reconcile accounts. For an enterprise handling global trade, this downtime is a significant strategic bottleneck.

A 24/7 enterprise banking platform, however, utilizes a cloud-native, event-driven architecture. This shift allows for real-time transaction processing without the need for end-of-day pauses.

Consequently, businesses can maintain liquidity and operational momentum across every time zone simultaneously.

| Feature | Legacy Core Banking | 24/7 Enterprise Platform |

| Processing Logic | Batch-based (Delayed) | Event-driven (Real-time) |

| System Availability | Scheduled Downtime | High Availability (99.99%+) |

| Data Flow | Periodic Synchronization | Continuous Streaming |

| Scalability | Vertical (Limited) | Horizontal (Elastic) |

| Integration | Monolithic/Hard-coded | API-first/Microservices |

The fundamental distinction lies in how data moves through the organization. Legacy systems often create information silos, where the CFO might see a different cash position than the regional manager due to sync delays. In contrast, a modern platform provides a “single source of truth” that updates with every micro-transaction.

Therefore, leadership gains the ability to make high-stakes decisions based on live data rather than yesterday’s reports. This transition from reactive to proactive financial management is the primary driver for institutional migration.

Can You Build 24/7 Banking on Legacy Systems?

The short answer is yes, but it requires significant technical compromise. Legacy systems mostly rely on 40-year-old foundations designed for a world that closed at 5 PM.

To achieve 24/7 uptime, enterprises often implement complex middleware wrappers to mimic real-time responsiveness. However, these layers frequently struggle with data consistency during nightly reconciliation windows.

Consequently, while you can force an old system to stay awake, the resulting technical debt often outweighs the temporary convenience.

1. Limits of Traditional Core Banking Systems

Legacy infrastructures are fundamentally constrained by linear, batch-processing logic. These systems require a mainframe maintenance window to lock the ledger and calculate interest.

For a global enterprise, this creates a dangerous shadow period where transactions are authorized but not reflected in live balances. This lack of transparency leads to liquidity mismanagement in high-frequency environments.

Furthermore, traditional systems lack the elasticity required for modern digital demands. This is because they are often hosted on-premise, making horizontal scaling nearly impossible during peak periods.

In addition, rigid data schemas make it difficult to integrate third-party APIs or AI tools. Therefore, the enterprise stays trapped in a cycle of maintaining hardware rather than innovating.

2. Extending vs. Replacing Legacy Infrastructure

Deciding whether to patch an existing system or migrate is a critical financial crossroads. Extending via middleware allows for faster market entry but leaves a fragile core intact.

Conversely, a full replacement offers cloud-native capabilities but carries higher initial migration risks.

| Strategic Factor | Extending | Replacing |

| Time to Value | Fast (3–6 months) | Slow (18–36 months) |

| Capital Expenditure | Moderate | Very High |

| Systemic Risk | Low (Incremental) | High (Migration complexity) |

| Long-term Agility | Limited by the old core | Unlimited/Cloud-native |

| Maintenance Cost | Increasing | Decreasing (Automation) |

3. Hybrid Approaches Used by Enterprises

Many successful organizations utilize a coexistence strategy to mitigate total overhaul risks. This involves hollowing out the legacy core over time.

By shifting high-demand functions, like real-time payments, to a modern cloud layer, the enterprise functions 24/7 while the old core handles back-office accounting.

- Sidecar Core Implementation: Running a digital-native ledger alongside the legacy system for real-time traffic.

- Event-Driven Synchronization: Using tools like Kafka to stream data to a real-time reporting layer.

- Shadow Ledgers: Maintaining a 24/7 mirror of balances that handles authorizations when the main core is offline.

- API Gateway Abstraction: Shielding old system complexity behind a modern, developer-friendly interface.

In conclusion, while building 24/7 capabilities on legacy foundations is possible, it is rarely a permanent growth solution.

The hybrid approach serves as a necessary bridge toward native resilience. Ultimately, this transition ensures your financial infrastructure catalyzes global expansion rather than tethering you to the past.

What Architecture Is Needed for a 24/7 Banking Platform?

Building a platform that never sleeps requires a complete departure from traditional server setups. You cannot rely on a single central database that needs to pause for backups or updates.

Instead, the architecture must be distributed and modular, allowing individual components to fail or upgrade without stopping the entire system.

1. API-First Infrastructure Design

An API-first approach treats every banking function as a reusable service. Instead of building a closed box, you create a flexible ecosystem where internal and external tools connect seamlessly.

- Rapid Deployment: Launch new financial products in weeks rather than years.

- Global Connectivity: Connect easily with international payment networks or fintech partners.

2. Event-Driven Microservices Architecture

Traditional software waits for commands, but event-driven systems react to changes in real-time. In this model, every transaction is an event that triggers automated actions across small, independent services.

This separation of concerns is the secret to maintaining 100% uptime even if one component fails.

3. Real-Time Data Streaming Pipelines

Data must move like a river rather than being stored in stagnant ponds. Real-time streaming ensures information is processed the millisecond it is generated.

Furthermore, these pipelines feed live data into AI engines to detect suspicious patterns instantly.

4. Failover and Multi-Region Resilience

True 24/7 banking requires a footprint spanning multiple geographic regions. If a data center in London goes offline, the system instantly shifts traffic to Singapore or New York.

Therefore, the platform remains resilient against natural disasters or localized internet failures.

5. Distributed Ledgers and Cloud-Native Security

Modern platforms use distributed technology to handle high volumes of complex transactions while maintaining absolute transparency.

Additionally, a zero-trust architecture assumes no user is safe by default, requiring constant verification for every request.

In summary, the right architecture balances flexibility with extreme reliability. By utilizing distributed, intelligent services, you build a foundation that scales with your growth and drives global revenue.

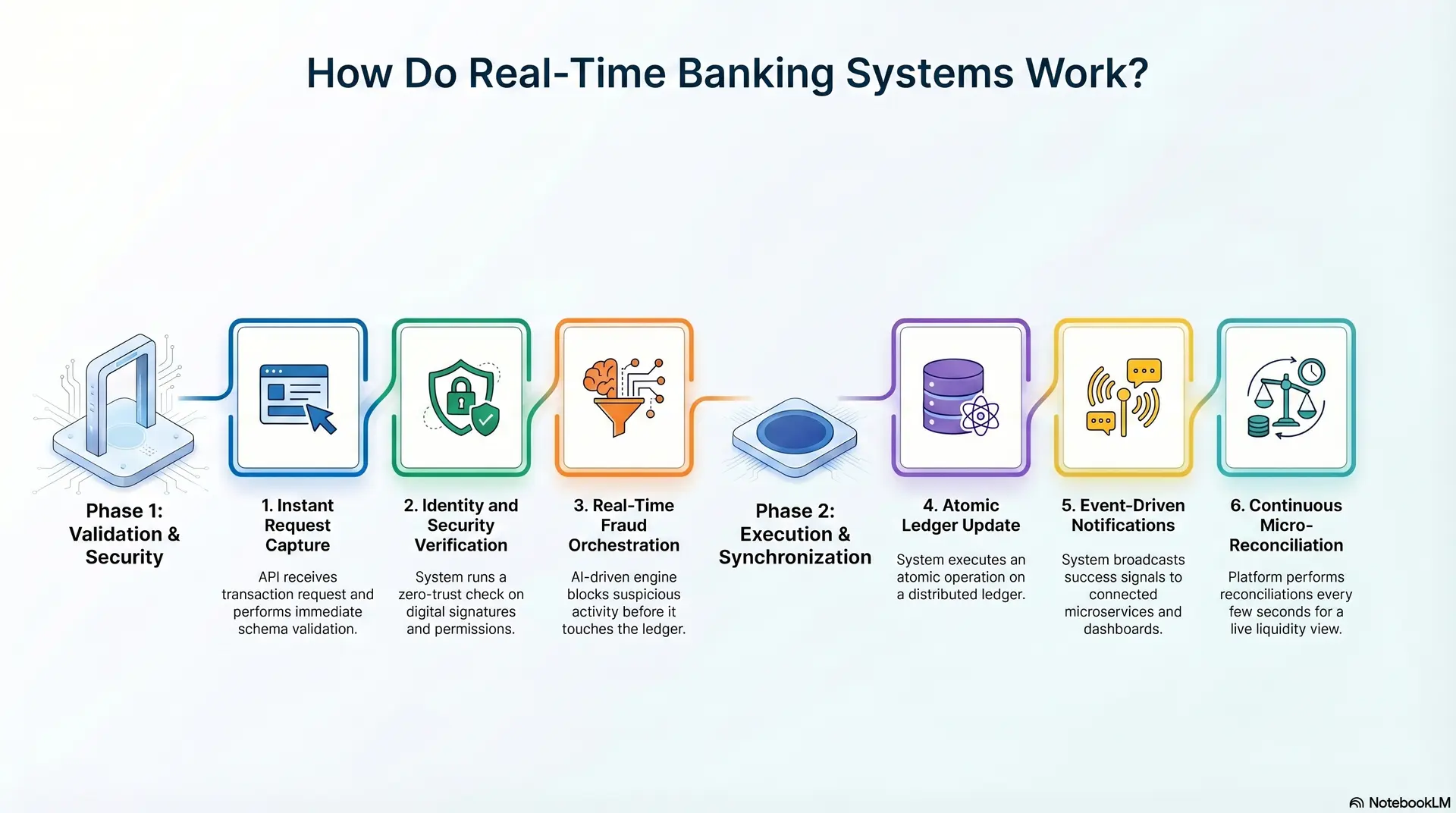

How Do Real-Time Banking Systems Work?

Real-time banking systems operate through a continuous loop of data validation, execution, and synchronization. Unlike legacy systems that group transactions for later processing, these platforms handle every request as an individual, high-priority event.

This architecture ensures that funds move and accounts update the exact millisecond a trigger occurs. Consequently, the enterprise maintains an accurate financial position at all times, regardless of global volume.

1. Instant Request Capture

The process begins when an API receives a transaction request from a client or internal system. This entry point performs immediate schema validation to ensure the data is complete and correctly formatted.

By filtering out malformed requests at the edge, the system preserves core processing power for legitimate traffic.

2. Identity and Security Verification

Before any money moves, the system runs a zero-trust check on the requester. It verifies digital signatures, checks for multi-factor authentication, and ensures the user has the necessary permissions.

This step happens in parallel with other checks to keep latency under ten milliseconds.

3. Real-Time Fraud Orchestration

The transaction data streams through an AI-driven fraud engine. This engine compares the current event against historical patterns and global blacklists instantly.

Therefore, suspicious activity is blocked before it ever touches the ledger, protecting the enterprise from significant capital loss.

4. Atomic Ledger Update

Once cleared, the system executes an atomic operation on a distributed ledger. This means the transaction either succeeds completely or fails entirely, preventing partial updates that could cause data corruption.

This integrity is vital for maintaining trust in high-volume, 24/7 environments.

5. Event-Driven Notifications

After the ledger updates, the system broadcasts a success signal to all connected microservices. This triggers secondary actions like sending push notifications, generating digital receipts, and updating treasury dashboards.

In addition, it allows downstream systems to react without waiting for a manual refresh.

6. Continuous Micro-Reconciliation

Instead of waiting for the end of the day, the platform performs reconciliations every few seconds.

This ensures that internal records always match external gateway balances across all currencies. Consequently, there is a live view of global liquidity without the traditional morning-after surprises.

In summary, this workflow transforms banking from a series of delayed entries into a live, breathing infrastructure. By automating every layer of the transaction lifecycle, enterprises can operate with total confidence in their global liquidity.

What Features Should a 24/7 Platform Include?

A 24/7 enterprise banking platform must serve as a comprehensive financial control center that operates with zero human intervention for routine tasks.

Therefore, the platform should prioritize automation, deep integration, and intelligent oversight to remain competitive. These features ensure that the infrastructure supports global growth rather than acting as a bottleneck.

1. Multi-Currency Liquidity Management

Enterprises operating across borders cannot wait for traditional settlement windows to see their cash position. This feature provides a consolidated, live view of all accounts across various currencies and jurisdictions.

In addition, it allows for automated sweeps to optimize interest or meet local funding requirements. Consequently, the treasury department can move funds instantly to where they are needed most.

2. AI-Driven Predictive Fraud Detection

Static rules are no longer sufficient to stop sophisticated modern cyber-attacks. An enterprise platform must include machine learning models that analyze transaction behavior in real-time.

These models identify anomalies, such as unusual velocity or geographical shifts, and block them before the ledger is updated. Therefore, the system protects the organization’s assets without slowing down legitimate business traffic.

3. Autonomous Regulatory Compliance

Managing KYC, AML, and tax reporting manually is impossible in an always-on environment. This feature automates the screening of every transaction against global sanction lists and local regulations. Furthermore, it generates real-time audit trails and regulatory reports that are ready for submission at any moment.

This automation reduces the risk of heavy fines and simplifies the work for legal teams.

4. Programmable Money and Smart Contracts

Modern platforms allow businesses to bake logic directly into their financial transactions. By using smart contracts, payments are only released when specific conditions, such as a delivery confirmation, are met.

This reduces the need for escrow services and minimizes counterparty risk. In addition, it streamlines complex supply chain financing and automated royalty distributions.

5. Seamless API Orchestration and Open Banking

A 24/7 platform must act as a hub that connects easily to the wider financial ecosystem. This involves offering a robust set of APIs that allow ERP systems, payroll providers, and fintech tools to communicate directly.

Seamless orchestration ensures that data flows freely between the bank and the enterprise’s core business applications. Consequently, manual data entry is eliminated, and operational errors are significantly reduced.

6. Virtual Account Management (VAM)

Large organizations often struggle with hundreds of physical bank accounts that are difficult to reconcile. Virtual Account Management allows the enterprise to create thousands of sub-accounts under a single physical header.

Each sub-account can be assigned to a specific client, project, or department for instant reconciliation. This feature simplifies the cash management structure while providing granular visibility into every revenue stream.

7. High-Availability Multi-Cloud Deployment

To guarantee 100% uptime, the platform should not be tethered to a single cloud provider. A multi-cloud strategy ensures that if one provider experiences a major outage, the banking operations immediately shift to another.

This level of redundancy is a non-negotiable requirement for enterprise leaders who cannot afford even a minute of downtime. It provides the ultimate peace of mind for mission-critical financial infrastructure.

In summary, these features transform a simple banking tool into a strategic asset. By focusing on automation and real-time intelligence, you build a platform that thrives in the complexity of global finance. This feature set ensures that your investment is future-proof and ready to scale.

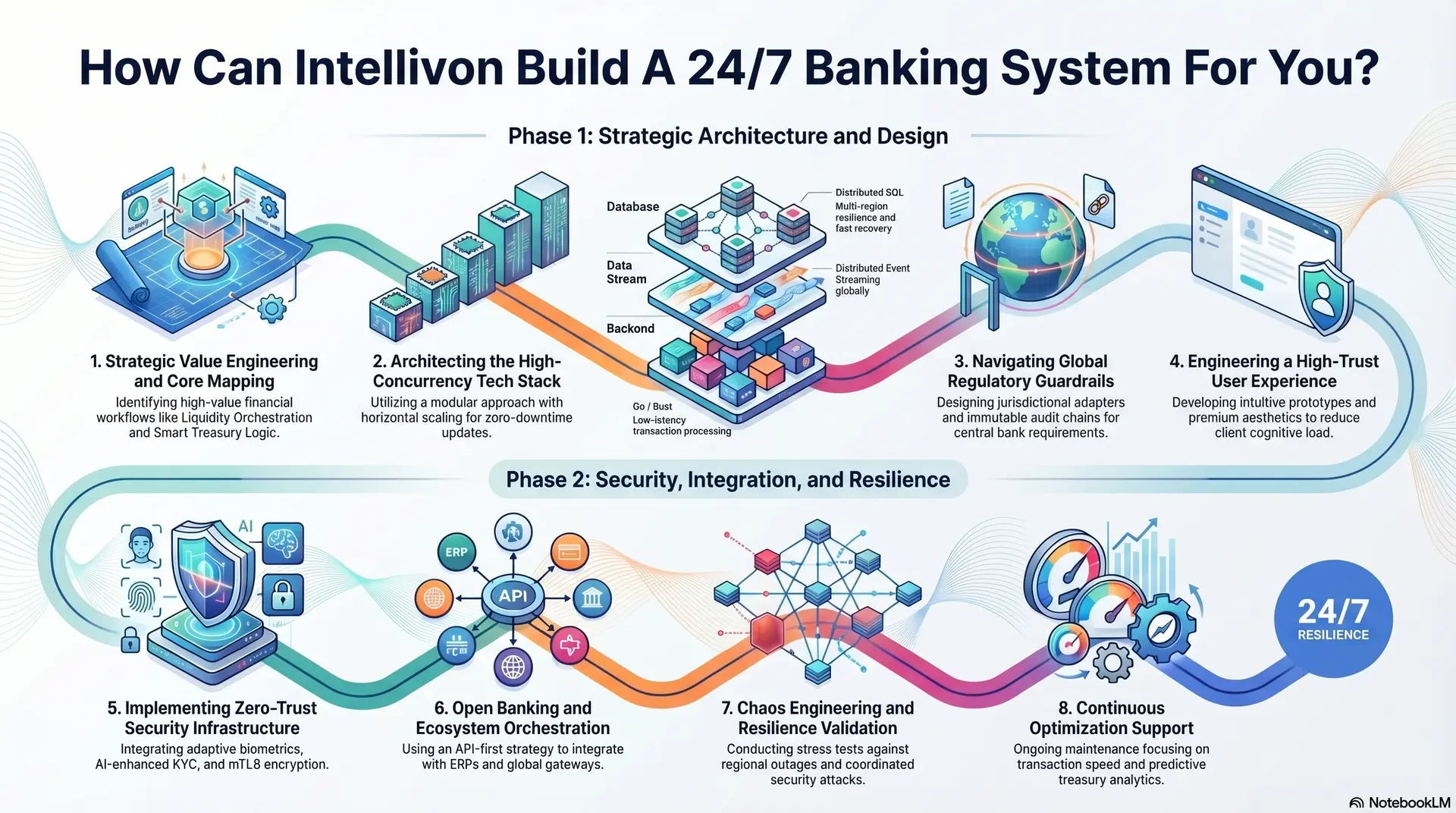

How Can Intellivon Build A 24/7 Banking System For You?

Building a platform that never sleeps requires an architectural overhaul of traditional financial logic. At Intellivon, we treat your platform as mission-critical infrastructure that must remain resilient under extreme load and regulatory scrutiny.

Our process focuses on eliminating single points of failure while maximizing the throughput of every transaction. Consequently, we move beyond generic development to create a bespoke technical moat for your enterprise.

Step 1. Strategic Value Engineering and Core Mapping

We begin by identifying the specific financial workflows that will drive your business model. While standard features are a given, we focus on high-value differentiators that attract institutional capital and ensure long-term market dominance.

- Liquidity Orchestration: We map real-time visibility across global sub-accounts and multiple currencies.

- Smart Treasury Logic: Our team designs automated cash sweeping and yield optimization protocols.

- Feature Moats: We identify unique functionalities, such as instant cross-border settlement rails, that make your platform indispensable.

Step 2. Architecting the High-Concurrency Tech Stack

A 24/7 platform requires a stack that supports horizontal scaling and zero-downtime updates.

We utilize a modular approach to ensure the frontend remains snappy while the backend handles heavy asynchronous processing.

| Layer | Strategic Technology Focus | Enterprise Benefit |

| Frontend | Micro-frontend Architecture | Independent updates without site-wide downtime |

| Backend | High-Performance Go / Rust | Type-safe, low-latency transaction processing |

| Data Stream | Distributed Event Streaming | 100% data consistency across global nodes |

| Database | Distributed SQL (ACID Compliant) | Native multi-region resilience and fast recovery |

Step 3. Navigating Global Regulatory Guardrails

Compliance is not a hurdle; it is a structural requirement. We design the system to meet the specific licensing needs of your target markets, whether you are pursuing a full banking license or a specialized e-money permit.

- Jurisdictional Adapters: We build logic specifically for the UAE, Singapore, or EU-specific financial mandates.

- Immutable Audit Chains: Every system change is recorded in a tamper-proof log to satisfy central bank requirements.

Step 4. Engineering a High-Trust User Experience

Design in banking is about building confidence through extreme clarity. We develop intuitive prototypes that allow stakeholders to visualize complex financial workflows before any code is written.

Therefore, the final interface reduces cognitive load for your clients while maintaining a premium, enterprise-grade aesthetic.

Step 5. Implementing Zero-Trust Security Infrastructure

We protect your assets by assuming every request is a potential threat until proven otherwise. Our security layer is integrated into the transaction flow rather than sitting on top of it as an afterthought.

- Adaptive Biometrics: Multi-factor authentication tailored for high-value corporate transfers.

- AI-Enhanced KYC/KYB: Real-time identity verification to prevent money laundering and fraud.

- mTLS Encryption: Secure, encrypted communication between every microservice within the platform.

Step 6. Open Banking and Ecosystem Orchestration

Your platform should not exist in a vacuum. We use an API-first strategy to integrate your system with the broader financial world, including ERPs, payroll providers, and global payment gateways.

This connectivity ensures your platform becomes the central hub for your customers’ financial lives.

Step 7. Chaos Engineering and Resilience Validation

Before going live, we subject the platform to rigorous stress tests. We simulate regional outages, massive traffic spikes, and coordinated security attacks.

This ensures that when the system launches, it is already battle-tested against the volatile realities of the global market.

Step 8. Continuous Optimization Support

The financial landscape shifts daily, and your platform must adapt. We provide ongoing maintenance that focuses on optimizing transaction speeds and lowering operational costs.

Furthermore, we help you integrate emerging technologies like predictive treasury analytics as your enterprise scales.

In conclusion, partnering with Intellivon means moving from a vision to a high-performance reality. We provide the technical depth and strategic foresight needed to lead the next generation of finance. Your infrastructure should be a growth engine, not a liability.

What Integrations Are Required for 24/7 Banking Platforms?

A modern banking platform serves as a central hub that must communicate with dozens of external financial services. For an enterprise, the quality of these integrations determines the overall speed and reliability of the global business.

Therefore, your architecture must support seamless connectivity that remains stable even when external partners face downtime.

1. Core Banking and Legacy Integrations

Many enterprises still rely on older systems for their primary ledger and accounting records. To achieve 24/7 functionality, your new platform acts as a high-speed layer that sits on top of these legacy cores.

- Bi-directional Sync: Ensures data moves between the cloud and the mainframe without errors.

- Shadow Ledgers: Maintains a live mirror of balances to handle requests when the core is offline.

2. Payment Networks and Card Processors

To facilitate global trade, your platform must connect directly to international payment rails and local clearing houses. This includes integrations with networks like SWIFT for cross-border wires and local systems for domestic transfers.

- Network Redundancy: Prevents a failure in one network from freezing your entire payment flow.

- Real-Time Settlement: Connects to instant domestic clearing systems for immediate fund movement.

3. KYC, AML, and Compliance Systems

Regulatory safety is a non-negotiable requirement for any serious financial investment.

Your platform must integrate with specialized identity services that check users against global watchlists in real-time.

| Integration Type | Business Value | Critical Feature |

| Identity Verification | Reduces manual onboarding | Biometric and document OCR |

| AML Monitoring | Prevents legal liabilities | AI-driven behavioral flagging |

| Sanction Screening | Ensures global compliance | Real-time database cross-referencing |

4. Third-Party APIs and Ecosystems

The most successful banking platforms function as ecosystems that allow for easy expansion. By integrating with third-party APIs, you can offer additional services like payroll management or tax calculation tools.

Consequently, this open banking approach increases the value of your platform and creates new revenue streams for the enterprise.

In summary, the strength of your platform depends on the quality of its deep technical connections. By building a highly integrated environment, you ensure your financial infrastructure is versatile enough to adapt to any market demand.

How Do Banks Keep Systems in Sync in Real Time?

Maintaining a unified record of truth across a global network requires a move away from traditional database locks. Systems must ensure that a balance update in one region is instantly reflected across all other nodes to prevent financial discrepancies.

Therefore, banks utilize distributed coordination techniques to keep every ledger entry perfectly aligned without slowing down the user experience.

1. Data Consistency Across Systems

In a 24/7 environment, the platform must achieve what architects call strong consistency. This means that once a transaction is confirmed, every subsequent request sees the updated balance immediately.

- Atomic Operations: Transactions are processed as single units that either succeed fully or fail completely.

- Distributed Locking: The system uses sophisticated protocols to manage access to the same account across different servers.

- Validation Loops: Continuous checks ensure that the front-facing ledger always matches the underlying core records.

2. Event Streaming and Messaging Layers

Modern platforms move data as a series of immutable events rather than static updates. By using high-speed messaging layers like Kafka, the system broadcasts every transaction to all relevant services simultaneously.

- Decoupled Services: One service can update the ledger while another triggers a fraud alert using the same data stream.

- Order Preservation: The messaging layer ensures that transactions are processed in the exact sequence they occurred.

- Buffer Management: High-volume traffic spikes are managed by queuing events, preventing system crashes during peak hours.

3. Handling Failures and Data Conflicts

When a network connection drops, the system must decide how to handle pending updates without corrupting the data. Resilience is built in by allowing nodes to work independently and then reconcile once connectivity is restored.

| Failure Type | Impact | Resolution Strategy |

| Network Partition | Nodes cannot communicate | Majority-rule consensus protocols |

| Database Latency | Delayed balance updates | Optimistic concurrency control |

| Service Crash | Interrupted transaction | Automated state recovery from event logs |

4. Distributed Consensus and Voting

To prevent errors in a decentralized setup, multiple servers must agree on the state of a transaction before it is finalized. This voting process happens in milliseconds and ensures that no single faulty node can authorize an invalid payment.

Consequently, the platform maintains institutional-grade integrity even if part of the infrastructure fails.

5. Idempotency and Duplicate Prevention

In high-speed systems, a network glitch might cause a request to be sent twice. To prevent double-charging, every transaction is assigned a unique fingerprint that the system recognizes instantly.

Therefore, if the same request arrives again, the platform identifies it as a duplicate and ignores the second attempt while returning the original success message.

In summary, keeping systems in sync is a balance of speed and mathematical precision. By implementing these advanced coordination layers, you ensure your enterprise platform remains a reliable and trustworthy financial backbone.

How Do You Secure a 24/7 Banking Platform?

Securing a platform that never closes requires a shift from static perimeter defense to a dynamic, multi-layered security model. You must protect every transaction and data point without introducing friction that slows down the global movement of capital.

Therefore, the goal is to build a self-healing security architecture that detects and neutralizes threats as they appear.

1. Identity and Access Management

Identity is the new perimeter in modern financial systems. We implement a zero-trust framework where every user and device must be continuously verified before accessing sensitive data.

- Biometric Authentication: Uses unique physical markers like fingerprints or facial recognition to ensure true identity.

- Just-in-Time Permissions: Grants temporary access to specific functions only when needed, reducing the window for potential abuse.

- Behavioral Fingerprinting: Tracks how a user interacts with the system to identify hijacked accounts through unusual navigation patterns.

2. Encryption and Data Protection

Data must be unreadable to unauthorized parties, whether it is moving across the internet or sitting in a database. Consequently, we utilize advanced cryptographic standards to shield your enterprise assets from interception or theft.

- End-to-End Encryption: Protects the data tunnel between the user app and the backend server.

- Hardware Security Modules: Stores cryptographic keys in dedicated physical devices that are tamper-proof.

- Tokenization: Replaces sensitive card numbers with random strings, ensuring that actual account data is never stored on the platform.

3. Real-Time Fraud Detection Systems

Static rules are insufficient for stopping modern cyber-attacks that evolve in seconds. Our approach utilizes machine learning models that analyze thousands of data points across every transaction to find hidden risks.

| Security Layer | Function | Technical Approach |

| Velocity Checks | Prevents rapid-fire withdrawals | Real-time transaction counters |

| Geo-Fencing | Blocks logins from high-risk areas | IP and GPS coordinate tracking |

| Anomaly Detection | Flags unusual spending habits | Unsupervised neural network models |

4. Regulatory Compliance Requirements

Operating a 24/7 bank means adhering to a complex web of global mandates like GDPR, PCI-DSS, and local banking laws. The system must automate the collection of evidence and the filing of reports to remain in good standing with central banks.

Therefore, compliance is treated as a continuous automated process rather than an annual manual check. This ensures that the platform is always audit-ready without interrupting daily operations.

In summary, security is the foundation upon which trust and investment are built. By implementing these rigorous protection layers, you ensure your platform remains a safe harbor for enterprise capital in a volatile digital world.

What Challenges Come With 24/7 Banking Systems?

Transitioning to an always-on model introduces technical and operational hurdles that legacy institutions rarely face. You must manage complex data synchronization while ensuring the system remains impenetrable to evolving cyber threats.

Therefore, understanding these obstacles is the first step toward building a resilient financial infrastructure. These challenges require a shift from traditional maintenance mindsets to a culture of continuous engineering and proactive monitoring.

1. Navigating Global Regulatory Fluidity

Challenge: Operating across different time zones means adhering to a patchwork of financial laws like GDPR, AML, and local residency mandates. These rules change without notice and require immediate system adjustments to avoid heavy fines.

Solution: We implement automated compliance engines that act as jurisdictional adapters. These tools update internal logic instantly based on the latest central bank directives. Consequently, your enterprise remains audit-ready in every market without manual intervention.

2. Managing Asynchronous Data Consistency

Challenge: Maintaining a single version of truth across global data centers is a massive technical hurdle. If a user withdraws funds in London, the system must reflect that change in Singapore instantly to prevent double-spending.

Solution: Our architecture utilizes distributed consensus protocols and atomic ledger updates. This ensures that every node in the network agrees on the account state before the transaction finalizes. Therefore, you maintain 100% data integrity even during peak global traffic.

3. Eliminating Maintenance Windows for Updates

Challenge: Traditional banks close at night to perform system patches and data backups. In a 24/7 environment, you lose this luxury and must implement updates while millions of transactions are in flight.

Solution: We utilize blue-green deployment strategies to switch traffic between different versions of the platform without a single second of lag. This allows for continuous improvement and security patching without interrupting the user experience.

4. Infrastructure Scalability and Peak Management

Challenge: Financial platforms must handle massive fluctuations in demand during holidays or market volatility. A sudden spike can crash a traditional server, leading to lost revenue and damaged reputation.

Solution: By using cloud-native microservices, the platform scales elastically in response to real-time load.

| Component | Scaling Strategy | Benefit |

| Transaction Engine | Horizontal Pod Autoscaling | Handles unlimited concurrent payments |

| Data Stream | Partitioned Messaging Queues | Prevents bottlenecks during spikes |

| API Gateway | Global Edge Distribution | Reduces latency for international users |

5. Balancing Security Rigor With User Friction

Challenge: Overly aggressive security checks can drive users away by slowing down simple transactions. The challenge lies in creating a frictionless experience that still blocks sophisticated fraud in under 50 milliseconds.

Solution: We focus on invisible security layers like behavioral analysis and device fingerprinting. This approach allows legitimate users to move quickly while creating an impenetrable wall for malicious actors.

Integration With Rigid Legacy Systems

Challenge: Many new platforms must still talk to old, slow-moving mainframes that were not designed for the digital age. This creates significant architectural friction and data migration risks.

Solution: We build sophisticated middleware and API abstraction layers to bridge the gap between old and new technologies. This allows for a gradual modernization of your legacy core without risking system stability.

6. Reliance on Third-Party Ecosystems

Challenge: Digital banks often rely on external partners for KYC, card issuing, or cloud hosting. If a partner experiences an outage, it can take your entire platform down with it.

Solution: We implement circuit-breaker patterns and multi-vendor redundancy. If one provider fails, the system automatically reroutes traffic to a backup partner. Consequently, your platform remains operational regardless of external failures.

In summary, these challenges are the barrier to entry that protects your market position once overcome. By solving these complex problems, you build a technical moat that competitors cannot easily replicate.

Conclusion

Investing in a 24/7 enterprise banking platform is a strategic move to secure your financial future. It transforms rigid infrastructure into a dynamic growth engine that operates across every time zone. Therefore, modernizing your core system is essential for maintaining a global competitive advantage.

Our team provides the cutting-edge AI and fintech expertise needed to build this resilient foundation. Contact us today to develop a secure, always-on platform.

Why Enterprises Choose Intellivon To Build 24/7 Banking Platforms

Building a 24/7 banking platform is not merely a development task. It is the creation of a high-trust digital economy that must remain resilient under immense regulatory and transactional pressure. While many firms can write code, Intellivon specializes in engineering the sophisticated AI-driven infrastructure required to turn complex financial visions into market-leading realities.

A. Deep Fintech and AI Orchestration Expertise

Apart from building enterprise-grade fintech apps, we design intelligent financial ecosystems that operate with surgical precision. Our deep understanding of the global fintech stack ensures your platform is both technologically superior and future-proof.

- AI-Driven Core Logic: We implement autonomous layers for real-time fraud detection and predictive liquidity management.

- Immutable Ledger Systems: Our architectures prioritize data integrity, ensuring every transaction is traceable and error-free.

- Intelligent Automation: We utilize AI to streamline complex back-office workflows, reducing operational overhead from day one.

B. Mastery of Global Regulatory Frameworks

The biggest barrier to entry in global banking is compliance. We treat regulatory alignment as a core feature of the build, ensuring your platform is ready for international scrutiny.

- Automated Compliance Engines: We build integrated KYC, AML, and KYB workflows that adapt to shifting regional laws instantly.

- Audit-Ready Architecture: Every system includes automated reporting hooks designed for central bank transparency and ease of oversight.

- Data Sovereignty Management: We design infrastructure that respects local data residency laws while maintaining seamless global connectivity.

C. Strategic Execution with Accelerated Timelines

In the financial sector, a delayed launch is a lost opportunity. Intellivon utilizes a disciplined, sprint-based methodology to move you from architectural blueprint to live production without compromising on security.

- Phased MVP Delivery: We help you launch the most critical features first to capture early market share.

- Zero-Debt Engineering: Our developers write clean, modular code that prevents expensive refactoring as your user base grows.

- Seamless Connectivity: We provide pre-verified integrations for global payment rails like SWIFT, SEPA, and local clearinghouses.

D. Architected for Infinite Scalability

Most banking platforms face performance bottlenecks when user concurrency spikes. We anticipate this growth during the design phase, building a system that remains stable regardless of the load.

| Capability | Strategic Approach | Business Impact |

| System Uptime | Multi-region failover clusters | Guaranteed 24/7/365 availability |

| Transaction Load | Elastic microservices scaling | Zero latency during peak market spikes |

| Resource Cost | AI-optimized cloud utilization | Reduced infrastructure waste and overhead |

By combining technical depth with strategic foresight, we ensure your investment becomes a dominant force in the global economy. Ready to architect your financial future?

Contact Intellivon today to discuss how our AI-driven approach can bring your 24/7 banking platform to life with precision, security, and speed.

FAQs

Q1. Can you build a 24/7 banking platform on top of legacy infrastructure?

A1. You can, but it requires complex middleware layers that accumulate technical debt fast. Most enterprises use a hybrid approach, modernizing in phases while running a parallel cloud-native layer for real-time traffic.

Q2. What architecture does a 24/7 banking platform require?

A2. It requires cloud-native, event-driven microservices with multi-region failover, distributed ledgers, API-first design, and real-time data streaming. No single point of failure. Every component must fail independently without taking the entire system offline.

Q3. What are the biggest challenges in building an always-on banking infrastructure?

A3. Global compliance fluidity, data consistency across regions, zero-downtime deployments, and legacy integration are the core challenges. Each requires purpose-built engineering solutions, not workarounds. Most cost overruns trace back to underestimating exactly these four areas.

Q4. Is it better to build or buy a core banking system?

A4. Building gives you full control and competitive differentiation. Buying via BaaS reduces upfront cost but limits flexibility long-term. Most enterprises use a hybrid, proprietary logic built on pre-certified infrastructure. The right answer depends entirely on your growth trajectory.