Key Takeaways

-

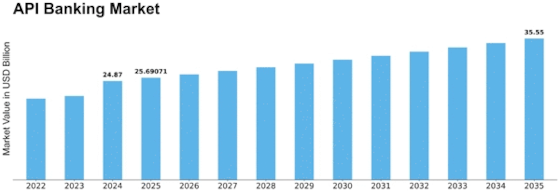

The API banking market is growing from $24.87 billion in 2024 to $35.55 billion by 2035. Enterprises building API-first infrastructure now are positioning for that growth directly.

-

Every service in an API-first banking system functions as a composable building block, enabling real-time data flow, programmable money movement, and third-party integration without rebuilding the core.

-

A ledger-accurate system is the foundation on which everything else is built. Real-time balances, double-entry design, and immutable audit trails determine whether the platform earns institutional trust.

-

Compliance embedded at the infrastructure level, KYC, AML, data consent, and audit logs, reduces regulatory risk and accelerates entry into new markets without costly redesigns.

-

How Intellivon builds a compliance-ready API-first banking infrastructure for your banking platform.

Banking infrastructure is facing an identity crisis. Many companies rely on old core systems that are insufficient to meet the speed, flexibility, or partnership needs of today’s finance. At the same time, financial systems now demand real-time data, programmable money movement, and smooth third-party integration from the start.

An API-first architecture changes how digital banking systems are being built. Instead of connecting features after launching the product, every service and workflow is created as a composable building block from the beginning. This leads to infrastructure that grows with product demand instead of against it.

For entrepreneurs and business builders looking into this area, the opportunity is clear. Institutions that have embraced API-first principles can launch new products in weeks instead of years, opening revenue channels that outdated systems simply can’t support.

Intellivon has partnered with large fintech companies to create AI-powered financial systems that meet both product speed and regulatory requirements. This blog draws from that experience and outlines the key principles, architectural choices, compliance layers, and development strategies for building a scalable system.

Why Is API-First Banking Adoption Growing In Enterprises?

Enterprises are adopting API-first banking because legacy core systems cannot keep pace with modern product demands. Speed, flexibility, and cross-platform interoperability are no longer optional. They are baseline expectations.

As open banking regulations expand across markets, financial institutions need infrastructure that connects, shares, and processes data without friction.

Therefore, APIs are no longer a technical layer sitting beneath the product. They have become the operating model itself. The numbers confirm this shift. According to Market Research Future, the API banking market was valued at $24.87 billion in 2024. It is projected to reach $35.55 billion by 2035, growing at a CAGR of 3.3%.

1. Faster Time to Market

Speed is one of the strongest drivers behind rising adoption. API-first banking lets enterprises plug into financial capabilities without rebuilding entire systems.

As a result, development cycles shrink considerably. Product launches, whether payment features, treasury tools, or customer finance workflows, move from months to weeks.

2. Easier System Integration

Most enterprises run a mix of legacy platforms, cloud applications, and third-party tools. However, getting these systems to communicate has historically been expensive and slow. API-first banking solves this through standardized interfaces that reduce integration complexity.

Consequently, financial data becomes easier to share across departments, and banking functions slot directly into existing operational workflows without disruption.

3. Stronger Embedded Finance Use Cases

Beyond integration, enterprises increasingly want financial services built into their products rather than bolted on separately. Instant payouts, digital wallets, lending, and automated reconciliation are all achievable through APIs.

This turns banking into a native product capability. The result is a stronger user experience and measurable new revenue streams.

4. Better Scalability and Control

As enterprises grow, their financial infrastructure must grow alongside them. API-first systems allow companies to add services, partners, or new geographies without overhauling their core stack.

Furthermore, they gain tighter control over how services are accessed, monitored, and secured, which directly strengthens compliance and risk management.

5. Cost and Efficiency Gains

Growth aside, the operational savings are equally significant. API-first models cut manual processes and eliminate the overhead of maintaining disconnected systems.

Automation across payments, reconciliation, reporting, and onboarding improves both speed and accuracy. Over time, the cost case becomes as compelling as the strategic one.

Enterprises are adopting API-first banking because it aligns with the way modern businesses operate: fast, connected, and digital-first. It helps them modernize financial services without replacing everything at once, while also supporting embedded finance, automation, and long-term scalability.

What Is API-First Banking Infrastructure and Why Does It Matter?

Developing an API banking platform requires a shift in how we perceive core financial services. In this model, the interface is the product itself. For organizations seeking to scale, this architecture provides the necessary modularity to adapt to shifting market demands without overhauling the entire backend. It moves banking from a closed loop into an open, programmable ecosystem.

What API-First Means in Banking Infrastructure

API-first design means building the communication layer before the user interface or internal logic. In financial systems, every function exists as a discrete, accessible service.

This strategy ensures that third-party developers or internal teams can interact with the core bank ledger instantly. Consequently, the infrastructure becomes a set of Lego-like blocks that drive rapid product innovation.

API-First Banking vs API-Wrapped Legacy Systems

Choosing between a native API architecture and a legacy system is a pivotal decision for any enterprise looking to modernize. While wrappers offer a quick fix, native systems provide the structural integrity required for long-term digital dominance.

| Feature | API-Wrapped Legacy System | API-First Native Infrastructure |

| Data Processing | Batch-based (updates happen in cycles) | Real-time (instant transaction updates) |

| Scalability | Limited by the original monolith’s capacity | Highly scalable via cloud-native microservices |

| Maintenance | High; fixing one part risks breaking the whole | Low; services are independent and modular |

| Deployment | Monthly or quarterly update cycles | Continuous delivery (updates in minutes) |

| System Latency | High due to the translation “wrapper” layer | Low; direct communication between services |

Ultimately, a native infrastructure is the only logical choice for building a future-proof API banking platform. It eliminates technical debt and provides the agility needed to compete with agile fintech giants.

Where API-first architecture creates business value

API-first banking creates enterprise value by enabling modular financial services and reducing time-to-market.

It allows businesses to integrate banking capabilities directly into non-financial workflows, driving customer retention and opening new revenue streams through embedded finance.

- Faster Launch Times: Launching new financial features takes weeks instead of years. You can test new ideas quickly without rebuilding your entire system.

- New Revenue Streams: You can let other companies use your banking tools for a fee. This turns your internal infrastructure into a profitable product.

- Lower Costs: Cloud-based APIs remove the need for expensive physical servers. You only pay for what you actually use, which keeps your overhead predictable.

- Better Data: All your financial information is updated in real-time. This makes it easier to track your cash flow and stay compliant with regulations.

Ultimately, this architecture ensures your business remains agile and ready for future trends. It is a strategic move that balances high-level security with the speed of a modern startup.

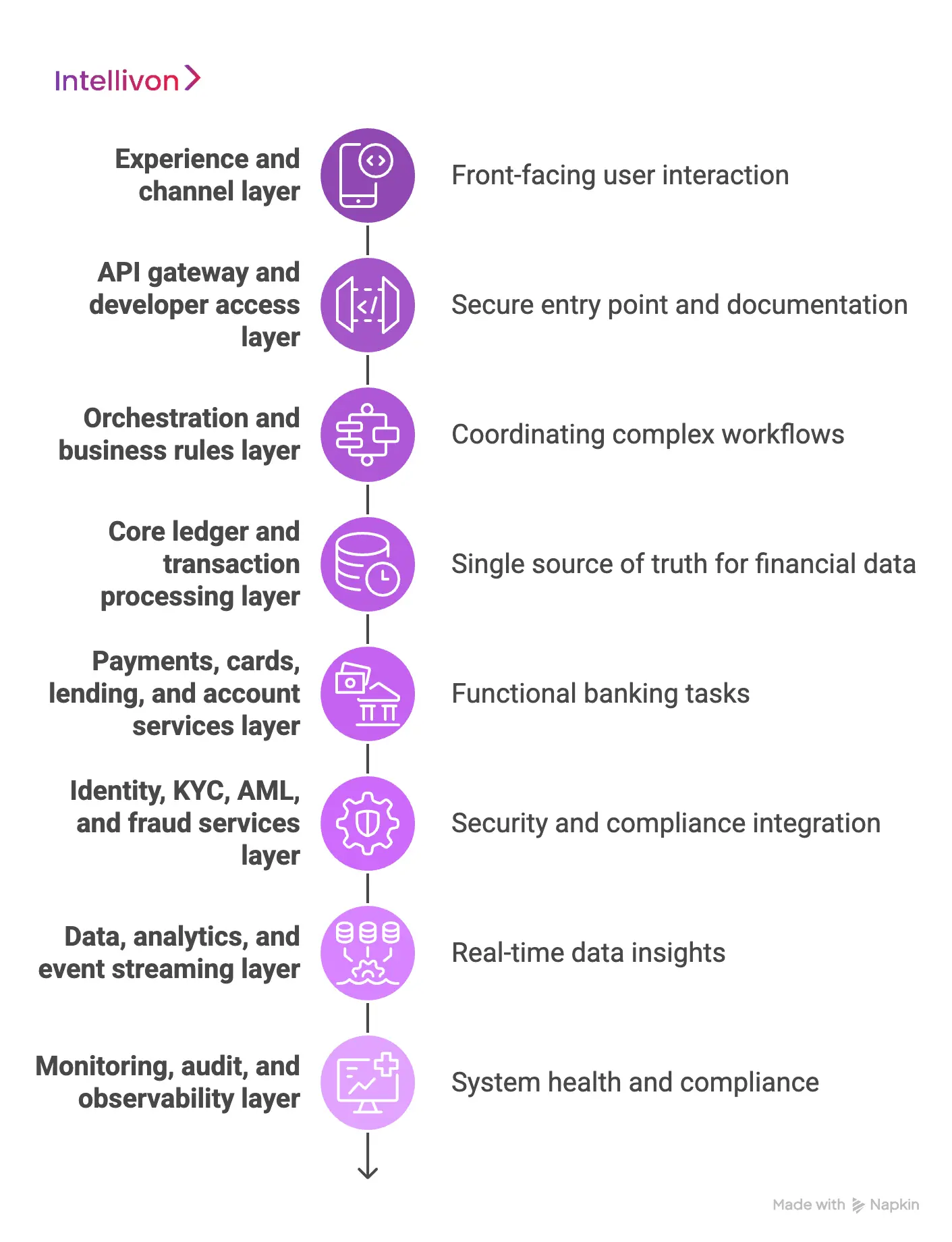

Core Layers of an API-First Banking Infrastructure System

Building a modern API banking platform requires a structured, multi-tiered approach. Instead of a single code, the system is organized into distinct layers that communicate through standardized protocols.

This separation allows for granular control, where an update to the payment engine does not disrupt the identity verification process.

1. Experience and channel layer

This is the front-facing part of the infrastructure where users interact with financial services. It manages the delivery of data to mobile apps, web portals, or even voice assistants.

Because the backend is decoupled, you can build a consistent experience across all platforms without duplicating logic.

2. API gateway and developer access layer

The gateway acts as the secure entry point for all internal and external requests. It handles critical tasks like rate limiting to prevent system overloads and authentication to ensure only authorized users gain access.

A well-designed gateway also includes a developer portal, providing clear documentation that allows partners to integrate your services in record time.

3. Orchestration and business rules layer

This layer functions as the brain of the system, coordinating complex workflows between different services.

For example, when a loan is requested, the orchestration layer triggers the credit check, risk assessment, and approval logic in a specific sequence. It ensures that business rules are followed consistently across every transaction.

4. Core ledger and transaction processing layer

The core ledger is the “single source of truth” for all financial positions and movements. It records every debit and credit with absolute precision and provides the foundation for balance management.

In an API-first world, this ledger must be capable of high-throughput, real-time processing to handle modern digital demands.

5. Payments, cards, lending, and account services layer

These are the functional engines that perform specific banking tasks. Each service operates independently:

- Payments: Connects to global rails like Swift, ACH, or blockchain networks.

- Cards: Manages the lifecycle of physical and virtual cards, including freezing and limit settings.

- Lending: Handles the calculation of interest, repayment schedules, and collateral management.

- Account Services: Manages the creation and configuration of various account types.

6. Identity, KYC, AML, and fraud services layer

Security and compliance are integrated directly into the infrastructure rather than being an afterthought. This layer automates “Know Your Customer” (KYC) and “Anti-Money Laundering” (AML) checks during onboarding.

It also uses real-time monitoring to detect and block fraudulent activities before they impact the bottom line.

7. Data, analytics, and event streaming layer

Modern banking generates massive amounts of data that must be captured and analyzed instantly. Event streaming allows the system to react to changes as they happen, such as sending a notification the moment a large purchase is made.

This layer provides the deep insights needed for personalized marketing and strategic financial planning.

8. Monitoring, audit, and observability layer

To maintain trust, an enterprise must have total visibility into its system’s health. This layer tracks every API call and system change, creating an immutable audit trail for regulators.

It also provides real-time alerts for technical issues, allowing your team to resolve problems before they affect the end user.

By organizing your infrastructure into these specific layers, you create a system that is both resilient and remarkably easy to upgrade. This modularity is what separates a world-class banking platform from a fragile legacy setup.

How Do You Design the Architecture of an API-First Banking Platform?

Designing a financial system requires balancing extreme reliability with the agility to innovate. A well-architected API banking platform acts as a resilient backbone that can support millions of concurrent transactions without sacrificing performance.

Strategic architectural choices made at the start will determine whether the platform scales effortlessly or becomes a bottleneck.

1. Choosing Your Architectural Starting Point

Most enterprises must choose between a modular monolith and microservices. While a monolith is easier to manage early on, microservices offer the independence needed for massive global scale.

| Architecture | Best For | Pros | Cons |

| Modular Monolith | Early-stage platforms | Faster development; simpler deployment | Harder to scale individual parts |

| Microservices | Large-scale enterprises | Independent scaling; fault isolation | Complex networking and overhead |

2. Decoupling Records from Experience Layers

Separating the core ledger from the user-facing layer prevents front-end changes from affecting financial stability. This approach ensures you can update your mobile app daily without touching the sensitive code that manages balances.

- System of Record: Focuses on data integrity, audit trails, and regulatory compliance.

- Experience Layer: Focuses on speed, user interface customization, and third-party integrations.

3. REST, Webhooks, and Event-Driven Patterns

Modern systems use different communication styles depending on the urgency and nature of the data being moved.

- REST APIs: Used for immediate actions, like a user requesting their current account balance.

- Webhooks: Used to “push” data to partners, such as notifying a budgeting app that a purchase occurred.

- Event-Driven: Uses a message broker (like Kafka) to let multiple systems react to a single event simultaneously.

4. Idempotency and Async Financial Flows

In banking, processing the same request twice is a critical failure. Idempotency ensures that even if a network glitch sends a “pay” command three times, the money only moves once.

- Idempotency Keys: Unique identifiers that prevent duplicate transaction processing.

- Async Processing: Handles heavy calculations in the background so the app remains fast for the user.

5. Resilience Across Third-Party Dependencies

Your platform will rely on external providers for KYC or credit scoring. Designing for resilience means building “circuit breakers” to prevent a partner’s downtime from crashing your entire system.

| Resilience Strategy | Function | Business Impact |

| Circuit Breaker | Stops requests to a failing provider | Prevents system-wide hang-ups |

| Retries with Backoff | Gradually retries failed connections | Fixes temporary network blips |

| Failover | Switches to a secondary provider | Ensures 100% service uptime |

6. Versioning Without Downstream Breakage

API versioning must be handled through clear paths to ensure backward compatibility. This allows you to launch new features for modern apps while keeping older integrations functional for existing corporate clients.

At the same time, it prevents the “forced upgrade” cycle that frustrates enterprise partners.

7. Defining a Future-Ready Service Mesh

A service mesh provides a dedicated infrastructure layer for service-to-service communication. It handles encryption, load balancing, and deep observability across all your microservices automatically.

This ensures that as your platform complexity grows, your team can still monitor and secure every single data packet.

Architecting with these principles ensures that your financial infrastructure is built on a foundation of trust by design. It creates a system that is powerful today and easily adaptable to the technologies of tomorrow.

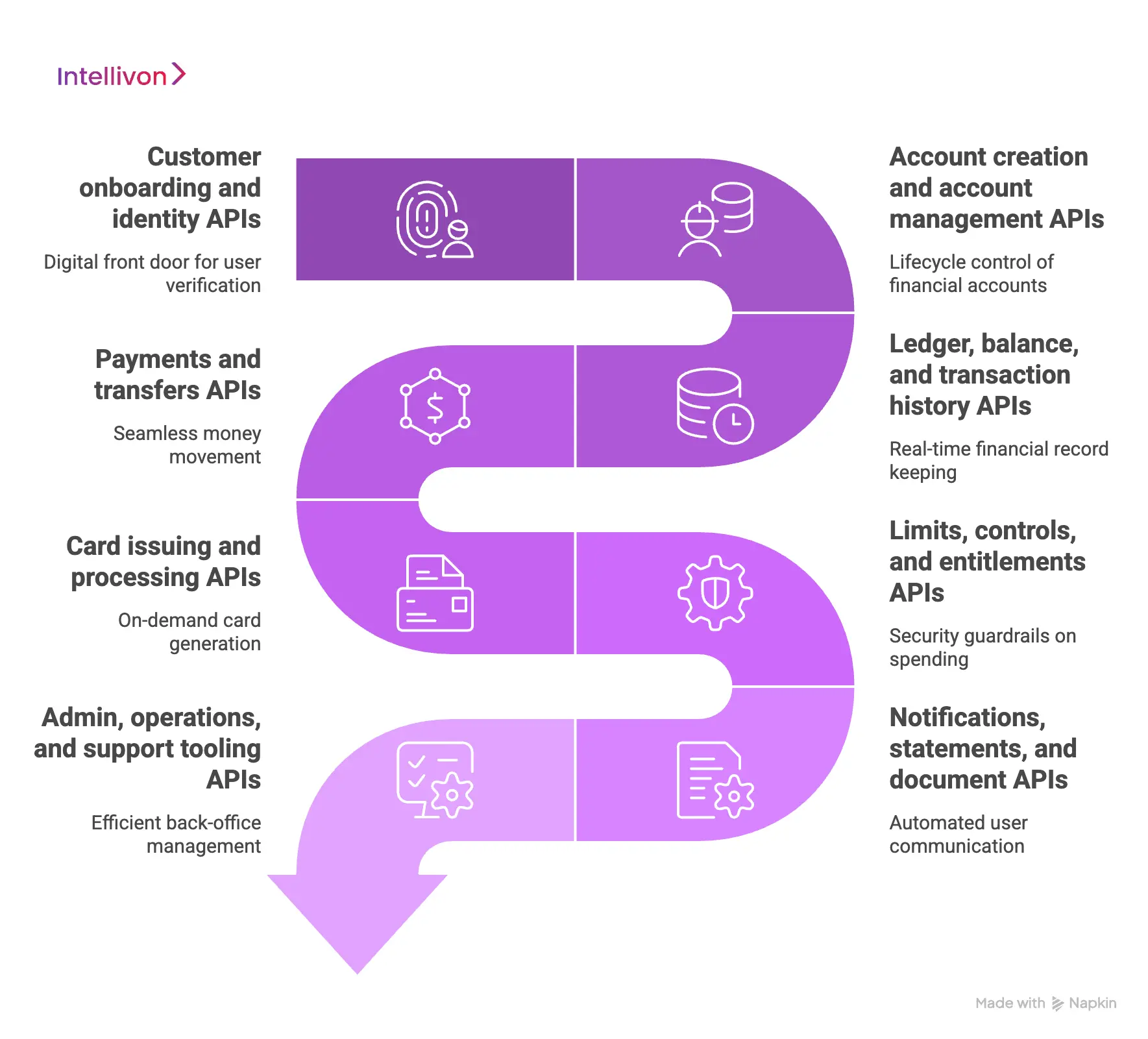

Which APIs Should You Build First in an API-First Banking Infrastructure?

Choosing the right development sequence prevents integration bottlenecks and accelerates the return on investment. A strategic roadmap focuses on the core ledger and identity layers before moving to consumer-facing features.

1. Customer onboarding and identity APIs

Onboarding APIs serve as the digital front door for every user. These tools handle the complex process of verifying identities and conducting background checks automatically.

By integrating with global databases, the platform ensures that every account holder is legitimate and safe to serve.

- Biometric Verification: Uses facial recognition or fingerprint data to confirm a user’s physical presence.

- Document Scanning: Automatically extracts and validates information from government-issued identification.

- Sanction Screening: Cross-references names against global watchlists to ensure regulatory compliance.

2. Account creation and account management APIs

Once an identity is verified, the system needs the ability to generate various account types. These APIs control the lifecycle of a financial account from opening to eventual closure.

In addition, they allow for the customization of account features based on specific user needs.

- Virtual Accounts: Enables the creation of partitioned funds for budgeting or sub-ledgering.

- Multi-Currency Support: Allows accounts to hold and manage different global currencies.

- Interest Logic: Automates the calculation and distribution of interest payments to the user.

3. Ledger, balance, and transaction history APIs

The core ledger is the heartbeat of any API banking platform. These APIs provide a real-time record of all funds and an immutable history of every movement.

Therefore, the business always has a single source of truth for financial reporting and auditing purposes.

- Real-Time Balances: Provides the exact amount of available funds at any given millisecond.

- Immutable Logs: Ensures that transaction records cannot be altered or deleted after the fact.

- Categorization: Tags transactions automatically to help users track their spending habits.

4. Payments and transfers APIs

Money movement is the primary utility that drives user engagement. These APIs connect the internal ledger to external payment rails such as ACH, SWIFT, or instant payment networks.

Consequently, the platform can facilitate seamless transfers between different institutions and individuals.

| Transfer Type | Speed | Use Case |

| Internal (P2P) | Instant | Moving money between users on the same platform. |

| ACH / SEPA | 1-3 Days | Standard payroll or bill payment cycles. |

| Real-Time (RTP) | Seconds | Urgent business payments or instant p2p cashouts. |

5. Card issuing and processing APIs

Cards remain the most common way for users to spend their funds at the point of sale. These APIs allow for the on-demand generation of both physical and virtual payment cards.

Furthermore, they give the platform the power to approve or decline transactions based on available balances.

6. Limits, controls, and entitlements APIs

Security in a digital system requires strict rules on how money is used. These APIs allow administrators or users to set specific guardrails on spending behavior.

As a result, the risk of large-scale fraud is significantly reduced.

- Merchant Blocking: Restricts spending at specific types of businesses, such as gambling or tobacco.

- Daily Caps: Limits the total amount of money that can leave an account in 24 hours.

- Geofencing: Prevents transactions from occurring outside of approved geographic regions.

7. Notifications, statements, and document APIs

Engagement depends on keeping the user informed about their financial status. These APIs trigger automated alerts for every account event and generate legal documents like monthly statements.

Therefore, the enterprise meets its transparency obligations without manual work.

8. Admin, operations, and support tooling APIs

A scalable system must be manageable by internal support teams. These APIs provide the necessary interface for staff to investigate issues and resolve customer disputes. They ensure that the back-office remains as efficient as the front-end experience.

Prioritizing these core services creates a functional infrastructure that supports immediate growth. This modular approach ensures each piece of the system is reliable and ready for future expansion.

Build Ledger-Accurate API-First Banking System

A ledger-accurate system is the only way to ensure institutional trust and regulatory safety. Failing to prioritize the core record-keeping layer often leads to irreversible financial discrepancies and loss of investor confidence.

1. Centrality of the Core Ledger

The ledger must function as the primary engine of the platform rather than a secondary database. It serves as the definitive source of truth for every cent moving through the ecosystem. Consequently, all other services must report to this central hub to maintain system-wide integrity.

- Single Source of Truth: Every transaction originates and ends within the ledger to prevent data silos.

- Service Independence: The ledger remains isolated so that front-end glitches cannot corrupt financial records.

- Operational Priority: Building the ledger first ensures that all subsequent features are built on a solid foundation.

2. Real-Time vs. Available Balances

Managing the difference between a total balance and what a user can actually spend is critical. Real-time calculations must account for pending holds, uncleared checks, and active disputes instantly. Therefore, the system prevents overdrafts and reduces the risk of liquidity shortfalls.

3. Double-Entry Design Principles

Modern banking relies on the ancient but effective rule of double-entry bookkeeping. Every movement of money must involve at least two accounts where one is debited, and another is credited. This ensures that the total sum of the system always equals zero, making errors easy to spot.

- Error Detection: Discrepancies become immediately obvious if the books do not balance.

- Transparency: Auditors can trace the exact path of every dollar from origin to destination.

- Integrity: It prevents the “creation” of money through software bugs or entry errors.

4. Multi-Party Reconciliation

Financial systems rarely work in isolation and must constantly talk to external processors and banks. Reconciliation is the process of ensuring your internal records match the actual money sitting in partner accounts. In addition, this process must happen daily to catch errors before they compound.

| Reconciliation Type | Frequency | Goal |

| Internal | Instant | Matches API requests to ledger entries. |

| Processor | Hourly | Ensures card swipes match pending ledger holds. |

| Bank/Network | Daily | Matches internal ledgers to actual cash in the bank. |

5. Managing Exceptions and Reversals

Not every transaction goes as planned, and the system must handle failures gracefully. Settlement delays, payment reversals, and customer disputes require specific logic to prevent the ledger from becoming inaccurate. As a result, the platform remains resilient even when external partners fail.

6. Audit Trails and Immutability

Every entry in a banking system must be permanent and time-stamped with absolute precision. An immutable history means that no record can be deleted or changed once it is written. Therefore, regulators can verify the state of the system at any point in the past with total confidence.

7. Lessons from Industry Failures

The 2024 Synapse Financial bankruptcy serves as a warning about the risks of inaccurate middleware recordkeeping. This collapse resulted in a massive reconciliation shortfall where ledger totals did not match the actual cash held in bank accounts.

- Fund Visibility: Relying on third-party data layers can lead to a total loss of visibility into which user owns which dollar.

- Reconciliation Gaps: Discrepancies between middleware and bank ledgers can freeze millions in deposits during a crisis.

- Systemic Risk: The failure of one recordkeeping layer can paralyze multiple partner institutions and thousands of end users.

The Synapse collapse proved that an enterprise must maintain its own native ledger to ensure absolute fund safety. This architectural choice prevents the accounting chaos that occurs when external systems fail to synchronize with reality.

By focusing on these core principles, an enterprise builds a system that is not just functional but fundamentally trustworthy. This level of accuracy is what separates a long-term financial institution from a short-lived tech experiment.

Build Compliance Into API-First Banking Infrastructure From Day One

Embedding regulatory requirements directly into the code ensures that compliance is a feature rather than a friction point. This approach reduces the risk of costly enforcement actions and builds a foundation of institutional trust.

1. Defining Compliance Ownership Models

Clear ownership of regulatory duties prevents gaps that often lead to legal trouble. In a Banking-as-a-Service (BaaS) setup, the responsibility is typically shared between the infrastructure provider and the banking partner. Consequently, every participant must know exactly where their liability starts and ends.

- Bank Partner: Usually handles the ultimate regulatory license and oversight.

- Tech Platform: Manages the automated monitoring and data collection tools.

- Accountability: Direct API integrations ensure that compliance data flows to all parties in real-time.

2. Embedded KYC, KYB, and AML Workflows

Compliance checks should be an invisible part of the user experience. By embedding “Know Your Customer” (KYC) and “Anti-Money Laundering” (AML) tools directly into the onboarding APIs, the system can verify users in seconds.

This automation removes the need for manual review for the vast majority of new accounts.

3. Data Consent and Permission Controls

Modern users demand transparency in how their financial data is shared and used. Designing for granular permissions allows customers to grant or revoke access to their information through a simple dashboard.

Therefore, the enterprise stays ahead of strict privacy laws like GDPR or CCPA.

4. Regulatory Audit Logs and Evidence

Regulators expect to see a clear and immutable trail of every action taken within the system. An audit log must record who accessed what data, when they did it, and what changed as a result.

In addition, these logs must be protected from alteration to serve as valid evidence during an official examination.

| Evidence Type | Regulator Expectation | Technical Implementation |

| Identity Proof | Validated ID and biometric match | Encrypted storage of KYC results |

| Money Trail | Origin and destination of funds | Immutable ledger transaction IDs |

| System Access | Who modified a user’s limit? | Detailed administrative action logs |

5. Modular Policy Update Support

Financial regulations change frequently, and your software must be able to keep up. Using a modular policy engine allows leadership to update compliance rules, like increasing a daily transfer limit, without changing the core code.

As a result, the business stays agile and compliant without needing constant developer intervention.

6. Third-Party Vendor Due Diligence

No banking system is an island, and every external partner introduces a potential point of failure. The infrastructure must be designed to monitor the health and security of third-party vendors constantly.

This ensures that a breach at a partner does not compromise your primary enterprise data.

7. Global Open Banking Infrastructure

New laws in the U.S. and EU are forcing banks to share data more freely with third parties. Planning for these developments now means building APIs that are compatible with standards like FDX or Berlin Group.

Therefore, your platform becomes a hub for innovation rather than a siloed legacy system.

Integrating these compliance layers from the start protects the long-term value of the investment. It ensures the platform can scale across borders while maintaining a clean record with global financial authorities.

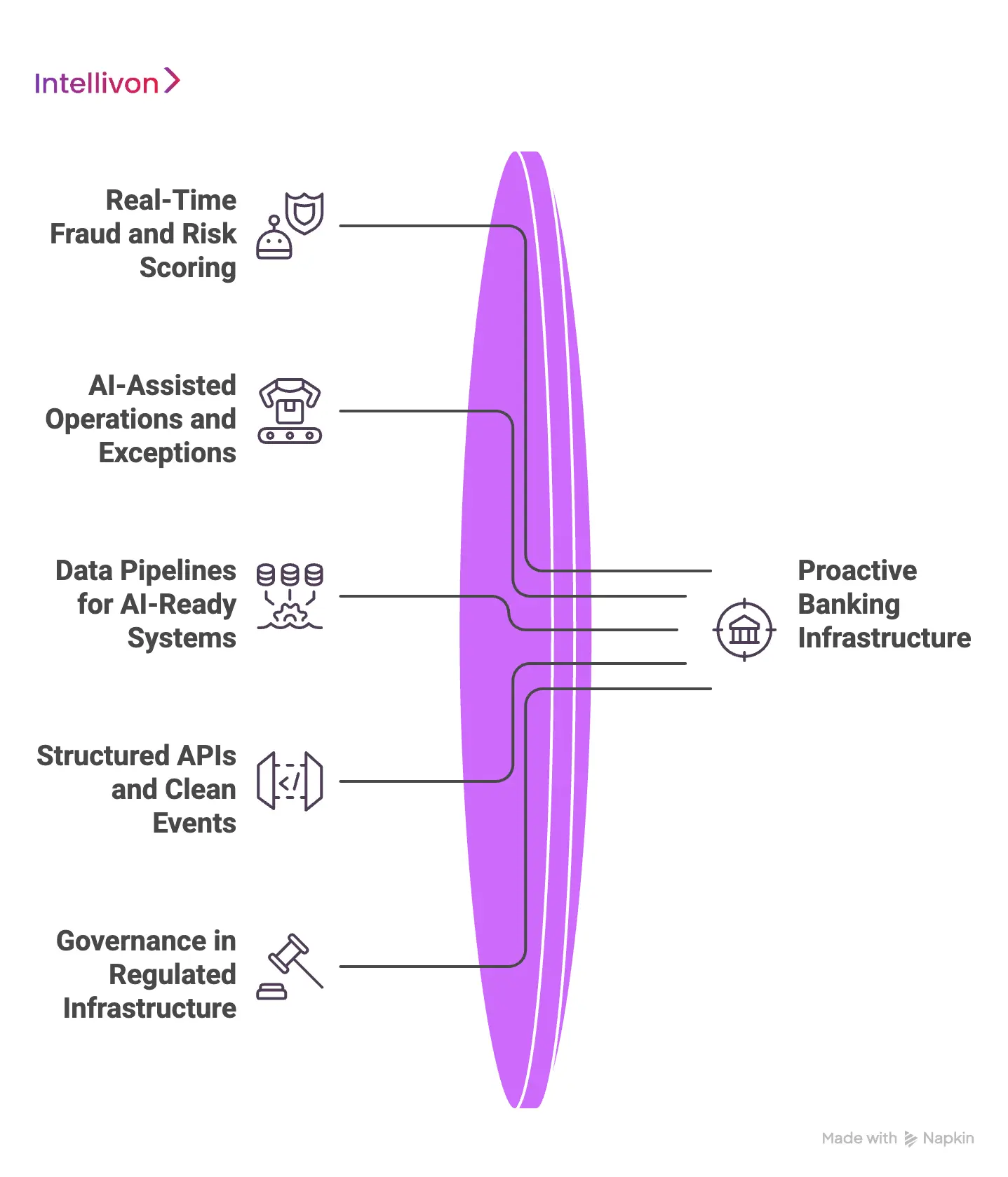

How Is AI Changing API-First Banking Infrastructure?

AI is transforming banking infrastructure from a passive ledger into an active, predictive system. Key shifts include real-time fraud detection layers, AI-assisted exception handling, and structured data pipelines.

Successful implementation requires risk-based governance that aligns with the latest 2026 OCC model risk management guidance for safe and sound banking operations.

1. Real-Time Fraud and Risk Scoring

Legacy fraud systems often rely on rigid rules that are easy for criminals to bypass. AI-driven layers can analyze thousands of data points, such as location, device health, and typing speed, to assign a risk score to every transaction instantly.

Consequently, a bank can stop a fraudulent payment before the money ever leaves the account.

- Behavioral Biometrics: Identifies users based on how they interact with their devices.

- Pattern Recognition: Detects unusual spending cycles that suggest a compromised account.

- Instant Decisioning: Approves or blocks transactions in milliseconds without manual review.

2. AI-Assisted Operations and Exceptions

Managing financial errors and customer disputes is traditionally a labor-intensive process. AI can now handle these exceptions by automatically gathering relevant data and suggesting a resolution.

In addition, this reduces the time it takes to resolve a customer issue from days to minutes.

3. Data Pipelines for AI-Ready Systems

An AI model is only as good as the data it consumes. Building a modern platform requires specialized data pipelines that can stream information from the ledger to the AI engine without delay.

This ensures that the intelligence is always based on the most current financial facts.

| Data Requirement | Why It Matters | Enterprise Impact |

| High Freshness | Models need the latest transactions. | Prevents fraud based on old data. |

| Clean Lineage | Tracks where every data point originated. | Simplifies regulatory audits. |

| Standardized Schema | Ensures all APIs speak the same language. | Reduces time to build new AI features. |

4. Structured APIs and Clean Events

AI readiness begins with how you organize your data at the source. Using structured APIs ensures that every piece of information follows a consistent format that a machine can understand.

Furthermore, clean event streaming allows the AI to “listen” to every system change as it happens, creating a truly responsive financial ecosystem.

5. Governance in Regulated Infrastructure

The Office of the Comptroller of the Currency (OCC) issued updated 2026 guidance emphasizing a risk-based approach to model management. Leadership must ensure that AI models are transparent, explainable, and free from bias.

Therefore, the infrastructure must include tools to monitor model performance and flag any decisions that deviate from established safety standards.

By embedding AI into the foundational layer, a business moves from reactive management to proactive strategy. This architectural shift creates a platform that is not only faster but fundamentally smarter and more secure.

Modernize Legacy Banking Systems Into an API-First Model

Transitioning from a monolithic legacy system to a modern architecture is often the most complex challenge an enterprise faces.

While the goal is a flexible API banking platform, the path requires a tactical balance between maintaining current operations and building for the future.

1. Strategic Alternatives to Full Replacement

Attempting to replace an entire banking core in one move is extremely risky and often ends in failure. These legacy systems are deeply embedded in every business workflow and contain decades of critical data logic.

Therefore, smart leadership focuses on incremental changes that deliver value without threatening the stability of the institution.

2. The Strangler Pattern for Banking Workflows

The Strangler Pattern involves building new API-based services around the edges of the old system. Over time, these new services handle more of the workload until the legacy core is eventually phased out.

Consequently, the business modernizes at its own pace while customers experience zero downtime during the transition.

3. Building Middleware Around Legacy Cores

Middleware acts as a sophisticated translation layer between modern apps and old mainframes. It allows newer technologies to request data in a standard format, even if the underlying system uses outdated protocols.

In addition, this layer can cache data to improve performance and reduce the load on the aging core.

- Protocol Translation: Converts modern JSON requests into legacy formats like COBOL or SOAP.

- Traffic Routing: Directs requests to either the old system or the new API based on the service maturity.

- Security Shielding: Provides modern encryption and authentication for systems that were never designed for the internet.

4. Wrapping Services Without Architectural Traps

“Wrapping” a legacy service provides a quick API entry point, but it can accidentally lock a business into a bad design. To avoid this, developers should ensure the wrapper follows modern standards rather than simply mirroring the flaws of the old code.

Therefore, the wrapper should be a temporary bridge, not a permanent part of the long-term plan.

5. Prioritizing Capability Exposure

Not every banking function needs to be an API on day one. High-demand services that drive the most customer value or operational cost savings should be moved first.

This targeted approach allows the enterprise to see a return on its modernization investment much earlier.

| Priority | Feature | Business Reasoning |

| High | Balance Inquiries | High volume and easy to decouple from the core. |

| Medium | New Account Opening | Low volume but high impact for growth. |

| Low | Historical Tax Exports | Complex data retrieval with low daily usage. |

6. Migration Sequencing for Lower Risk

A successful migration follows a logical order that minimizes potential points of failure. It usually begins with read-only data, such as transaction history, before moving to “write” actions like moving money.

This sequence allows the team to test the new infrastructure under real-world conditions with minimal danger to the ledger.

7. Coexistence and Rollback Strategies

During the modernization journey, the old and new systems must work together in total harmony. A robust coexistence strategy ensures that data is synchronized across both platforms in real-time.

Furthermore, every new API must have a “kill switch” or rollback plan that allows traffic to move back to the legacy system if an error occurs.

By following this measured approach, an institution can shed its technical debt without the chaos of a full system shutdown. This path ensures the enterprise remains competitive while protecting the integrity of its most valuable financial assets.

Build API-First Banking Systems for Cross-Border Use Cases

Expanding financial services across borders requires an architecture that can handle radical shifts in law, currency, and technical standards. A global API banking platform must be flexible enough to feel local in every market while maintaining a centralized core for the enterprise.

1. Architecture Choices for Global Growth

Founders must decide between a single global instance or separate regional deployments early in the design phase. While a single global core is easier to manage, it often struggles with local latency and strict regional regulations.

Consequently, many enterprises choose a “hub-and-spoke” model to balance control with local performance.

- Single Core: Best for startups with a narrow geographic focus and lower complexity.

- Regional Pods: Necessary for global enterprises that must isolate data by country.

- Hybrid Model: Centralized identity and ledger with localized payment gateways.

2. Data Residency and Sovereignty

Many countries now require that financial data about their citizens remain within their physical borders. This means the infrastructure must be able to store sensitive records in local data centers rather than a single global cloud bucket.

Therefore, the API layer must intelligently route data to the correct geographic storage point based on the user’s location.

3. Regional Rail and Settlement Complexity

Every region has its own unique way of moving money, from the US ACH system to Europe’s SEPA and Brazil’s Pix.

An API-first system uses “adapters” to speak to these different networks through a single internal command. In addition, the system must handle the complex math of real-time currency conversion and international settlement times.

| Region | Primary Rail | Typical Settlement | Key Requirement |

| USA | FedNow / ACH | Instant to 3 Days | Strict AML/BSA tracking |

| Europe | SEPA Instant | Seconds | GDPR and PSD3 compliance |

| India | UPI | Instant | High-volume mobile throughput |

4. Compliance Across Multiple Jurisdictions

What is legal in one country may be a regulatory violation in another, especially regarding privacy and reporting. A modular compliance engine allows the platform to toggle specific rules on or off depending on where the transaction occurs.

As a result, the business can enter new markets without rebuilding its entire security stack.

5. The Role of Global Orchestration

As a platform expands into more regions, the “brain” or orchestration layer becomes the most critical component.

It determines which regional bank partner to use, which currency to settle in, and which local tax laws to apply. This centralized intelligence ensures that complex cross-border flows remain fast and predictable for the end user.

6. Consistency Across Fragmented Infrastructure

Despite the mess of different local banks and rails, the user experience must remain seamless and uniform. High-quality APIs act as an “abstraction layer” that hides this backend complexity from the front-end developer.

Therefore, an app built for the UK can look and feel exactly like an app built for Singapore, even if the underlying pipes are completely different.

Building for a global audience ensures that the infrastructure remains a scalable asset rather than a regional liability. This foresight allows an enterprise to capture international market share with minimal technical friction.

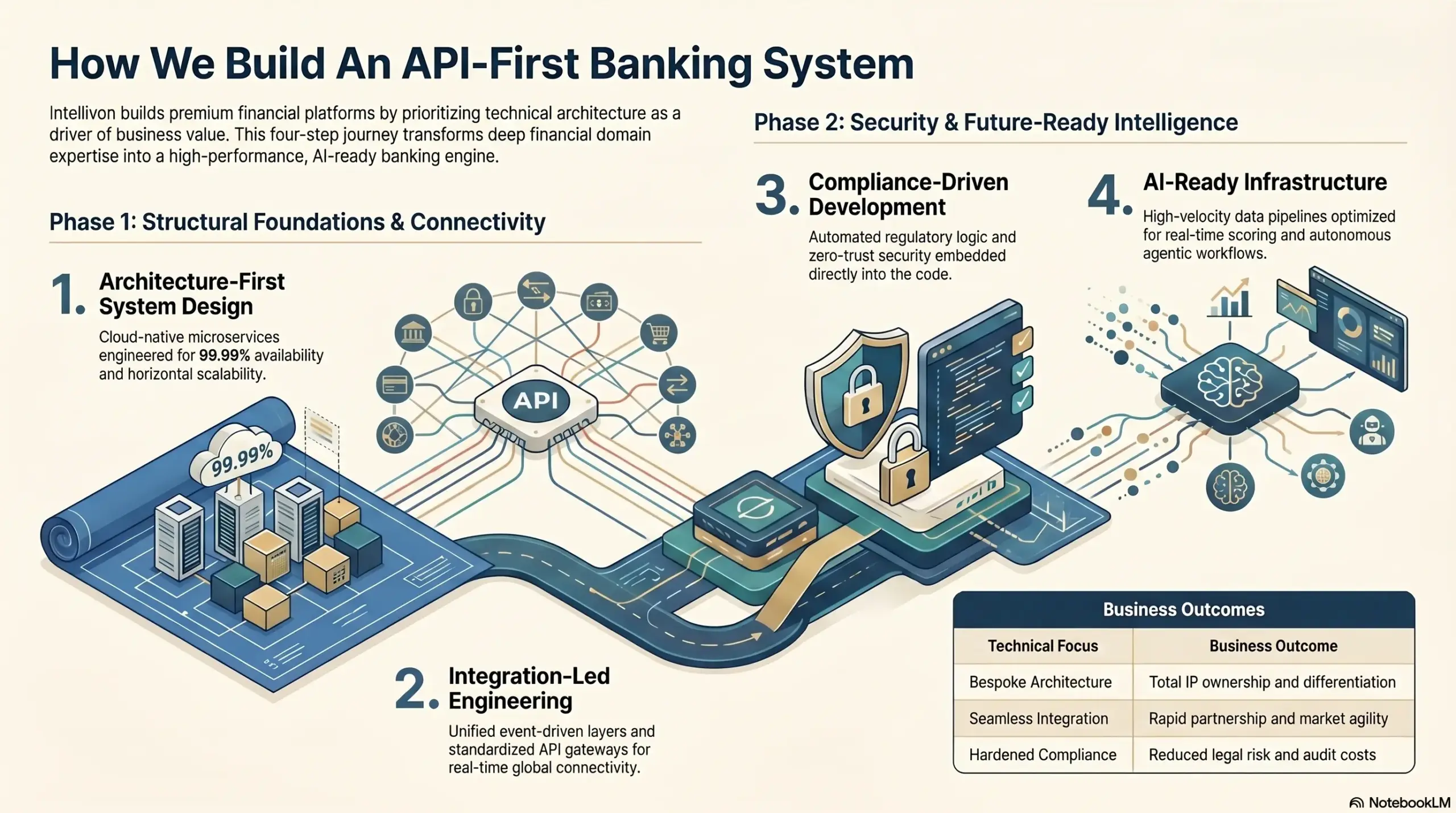

How We Build An API-First Banking System

Constructing a world-class financial platform requires a disciplined, phase-based approach that balances speed with institutional safety. We ensure that every technical decision aligns with the long-term business goals and regulatory obligations of the enterprise.

1. Discovery and capability mapping

Our process begins by identifying exactly which financial superpowers the platform must possess.

We conduct a deep dive into the specific workflows, user journeys, and revenue models intended for support. Consequently, we avoid building unnecessary features that add cost without adding value.

- Gap Analysis: We compare current capabilities against the desired future state.

- Feature Prioritization: We determine which APIs are essential for the initial launch.

- Regulatory Scoping: Our team identifies the specific licenses and jurisdictions required for operation.

2. Architecture design and vendor evaluation

Once the roadmap is clear, we shift the focus to selecting the right technology stack and partners. This is a critical juncture where we choose between cloud providers, ledger engines, and payment processors.

Therefore, we design the architecture to be vendor-agnostic to prevent being locked into a single provider’s ecosystem.

| Selection Factor | Business Impact | Strategic Goal |

| Scalability | Handles growth without crashes. | Support millions of users. |

| Interoperability | Works with existing systems. | Prevent data silos. |

| Vendor Stability | Reduces long-term risk. | Ensure service continuity. |

3. Compliance and control design

We believe compliance must be the foundation of the build. We design the automated guardrails that govern every transaction within the platform.

By building these controls into the infrastructure from day one, we significantly reduce the risk of manual error or regulatory fines.

4. API design and domain modeling

A successful platform depends on how easily other developers can use its tools. We focus on creating intuitive, well-documented APIs that follow global standards.

In addition, our domain modeling ensures that the data structure in the code matches how the business thinks about its financial products.

5. Core build and integration phase

This is where we handle the actual construction, connecting the various layers of the system. We integrate each module, from the ledger to the payment gateway, using secure, high-speed connections.

Furthermore, we ensure that the system is resilient enough to handle third-party downtime without affecting the core ledger.

- Microservices Development: We build independent blocks for specific tasks.

- Security Hardening: Our team implements encryption and advanced authentication at every layer.

- Third-Party Handshakes: We establish secure pipes to banks and processors.

6. Testing, certification, and operational readiness

Before a single real dollar moves, we put the system through rigorous stress testing. We simulate thousands of transactions to ensure the ledger remains accurate and the system remains fast.

Consequently, the enterprise gains the certification needed to prove to regulators and partners that the platform is safe for public use.

7. Launch, monitoring, and phased expansion

Our final phase is a controlled release, often starting with a small group of users to monitor performance. We use real-time dashboards to track every API call and system event, allowing us to spot and fix minor issues before they scale.

As a result, the platform expands with confidence, adding new features and regions only when the foundation is proven stable.

Following this rigorous methodology transforms a complex technical challenge into a predictable business success. This structured path ensures the final product is a secure, high-performance asset that drives growth for years to come.

Mistakes To Avoid When Developing API-First Banking Infrastructure?

Building a financial stack is an exercise in risk management as much as it is in engineering. Avoiding common architectural pitfalls early in the journey prevents the kind of technical debt that can paralyze a growing institution.

1. Treating the API gateway as the architecture

A gateway is merely an entry point, not the system itself. Many leaders focus too much on how the API looks to the outside world while ignoring the complex logic required behind it. Therefore, the platform may look modern on the surface but remain fragile and unscalable at its core.

2. Ignoring ledger design until later

The ledger is the most difficult part of the system to change once money starts moving. Delaying its design often results in a “database” that cannot handle the strict requirements of double-entry accounting. Consequently, the business may face unsolvable balance discrepancies that destroy user trust.

3. Over-customizing around one provider

Building too deeply into the specific features of a single bank or cloud provider creates “vendor lock-in.” If that partner changes their terms or suffers a failure, the enterprise is trapped. In addition, migrating to a new provider becomes a multi-year nightmare rather than a strategic shift.

- Hard-Coded Integrations: Avoid writing code that only works with one partner’s specific data format.

- Lack of Abstraction: Use a middle layer to ensure your core logic is independent of external APIs.

- Single-Point Failure: Ensure the architecture supports switching to a backup provider quickly.

4. Underestimating reconciliation complexity

Reconciliation is often treated as a simple “end-of-day” task, but in reality, it is a massive data challenge. Failing to automate the matching of internal records to external bank statements leads to “phantom” balances.

Therefore, the system must be designed to handle reconciliation as a continuous, real-time process.

5. Designing without compliance stakeholders

Engineers often build for speed, while compliance officers build for safety. If these two groups do not collaborate from day one, the final product may be technically brilliant but legally unusable.

As a result, the project faces expensive redesigns just weeks before a planned launch.

6. Launching without auditability and observability

Knowing that a transaction failed is not enough. Instead, the leadership must know exactly why and where it failed.

A lack of deep monitoring tools makes it impossible to troubleshoot issues in a complex, multi-service environment. Furthermore, without a clear audit trail, a regulator may deem the platform unsafe for public operation.

| Oversight | Immediate Consequence | Long-Term Risk |

| No Audit Logs | Hard to fix user errors. | Massive regulatory fines. |

| Poor Monitoring | Slow system performance. | System-wide outages go unnoticed. |

| Lack of Alerts | Issues discovered by users first. | Rapid loss of brand reputation. |

7. Optimizing for speed but not migration flexibility

The financial world moves fast, and the partners you use today may not be the ones you need tomorrow. Designing a rigid system that cannot easily migrate to new rails or processors is a major strategic error. Consequently, the enterprise loses its competitive edge because it is too technically “heavy” to pivot.

By recognizing these common errors, an organization can build a more resilient and adaptable financial future. This foresight ensures the infrastructure remains an asset that supports growth rather than a liability that creates risk.

Conclusion

Developing a robust API banking platform is a strategic investment in long-term enterprise growth. By prioritizing a ledger-accurate architecture, you ensure stability, security, and market agility. Consequently, your organization remains positioned to lead the future of digital finance with confidence.

Choosing the right partner is essential to turn these complex technical requirements into a scalable business asset. A dedicated focus on high-performance infrastructure ensures your platform remains compliant and ready for global expansion. Start building your financial future today to secure a lasting competitive advantage.

Why Banks Choose Intellivon For API-First Banking Development

Building API-first banking infrastructure is not just about exposing services through APIs. It requires designing a system that can support real-time transactions, complex integrations, compliance controls, and future product expansion without creating operational risk.

At Intellivon, we build banking infrastructure with a long-term architecture mindset. Our focus is on helping banks, fintechs, and financial platforms create modular, integration-ready systems that are easier to scale, govern, and evolve.

A. Engineering API-First Banking Systems That Scale From Day One

API-first banking platforms need more than clean endpoints. They need a solid foundation that supports transaction integrity, service orchestration, and consistent performance as usage grows.

We build banking systems with scalable architecture at the core, so your platform is designed for real-world load from the beginning.

- Modular API-first architecture for faster product expansion

- Banking workflows built for reliability, speed, and control

- Scalable service design that supports long-term platform growth

B. Solving Integration Complexity at the Core

Banking infrastructure depends on multiple systems working together without friction. Core platforms, payment rails, KYC tools, fraud engines, reporting systems, and third-party services all need to operate as one connected environment.

We build the integration layer that brings these systems together in a structured and dependable way.

- API-first architecture for seamless system connectivity

- Middleware and orchestration layers for complex banking workflows

- Reliable integrations across payments, KYC, fraud, and financial systems

C. Building Compliance Into the Architecture

In banking, compliance cannot be treated as an add-on. It has to be embedded into the way the platform is designed, integrated, and monitored from the start.

We help teams reduce rework and operational risk by making compliance part of the core system architecture.

- PCI DSS, GDPR, and SOC 2-aligned system design

- Built-in audit trails, logging, and reporting workflows

- Secure data handling across services, APIs, and integrations

D. Designing Banking Infrastructure for Resilience and Control

API-first banking systems often rely on multiple internal and external dependencies. Without the right architecture, small failures can ripple across the platform and affect customer experience, operations, and compliance.

We design infrastructure with resilience in mind, so your platform can remain stable even as complexity increases.

- Fault-tolerant architecture for critical transaction flows

- Monitoring and observability across services and integrations

- Controlled service interactions to reduce operational risk

E. Creating AI-Ready Banking Platforms Without Compromising Governance

Modern banking systems increasingly depend on real-time intelligence for fraud detection, risk analysis, customer insights, and operational efficiency. However, those capabilities only work when the underlying infrastructure is structured, secure, and compliant.

We build platforms that can support advanced analytics and AI use cases without weakening system integrity.

- Real-time data pipelines for AI and analytics use cases

- Infrastructure for fraud detection and risk scoring models

- Controlled AI enablement with oversight, explainability, and governance

F. Supporting Growth From Focused MVPs to Enterprise-Scale Systems

Some banking products begin with a narrow use case. Others launch with wider infrastructure goals from the start. In both cases, the architecture must support growth without forcing a major rebuild later.

We align the system design with your current priorities while keeping expansion paths clear.

- Lean architecture for focused MVP launches

- Scalable foundations for enterprise-grade growth

- Clear upgrade paths from early product to full infrastructure platform

Talk to Intellivon About Your API-First Banking Platform

If you are planning to build, modernize, or expand an API-first banking platform, the right architecture decisions early on can prevent major cost and complexity later.

Connect with Intellivon’s experts to discuss your platform goals, evaluate your infrastructure needs, and define a practical path forward.

FAQs

Q1. How is API-first banking different from open banking?

A1. API-first banking is an architectural choice where the system is built using modular, programmable interfaces from the start. Open banking is a regulatory requirement or business practice that allows third-party providers to access financial data. While API-first is the “how” of the build, open banking is the “what” it enables.

Q2. How long does it take to build API-first banking infrastructure?

A2. A production-ready system typically takes nine to eighteen months to develop and certify. The timeline depends on the complexity of the ledger and the number of regional payment integrations required. Starting with a modular framework allows for a minimum viable product (MVP) launch within six months.

Q3. How much does it cost to develop API-first banking infrastructure systems?

A3. Initial development for an enterprise-grade platform generally ranges from $80,000 to $130,000. These costs include core ledger engineering, security hardening, and regulatory licensing fees. Ongoing maintenance and compliance monitoring should be factored in as a percentage of the total operating budget.

Q4. Can banks modernize legacy systems without replacing the core?

A4. Yes, institutions can use the Strangler Pattern to migrate services incrementally. By building an API layer around the legacy core, banks can launch modern features while slowly decommissioning old code. Therefore, the organization achieves modernization without the high risk of a total system shutdown.

Q5. What compliance controls should be embedded into banking APIs?

A5. Infrastructure must include automated KYC, AML screening, and real-time transaction monitoring. In addition, granular data consent and immutable audit logs are essential for regulatory examinations. These controls ensure that every API call is verified, authorized, and recorded for long-term safety.