Key Takeaways

-

AvenuesAI proves enterprises can replace fragmented PSP stacks with a single AI orchestration layer that manages fraud, routing, compliance, and settlement simultaneously.

-

Multi-rail architecture connects cards, UPI, RTP, SWIFT, and blockchain into one layer, with AI selecting the optimal path per transaction.

-

Legacy integration requires middleware abstraction and phased migration to modernize infrastructure without disrupting live operations.

-

Build costs range from $50,000 for an MVP to $150,000 and above, depending on AI complexity, compliance scope, and rail depth.

-

How Intellivon builds AvenuesAI-like platforms your enterprise fully owns, controls, and scales without vendor dependency.

AI is quickly changing how payment platforms are built and is rewriting the way enterprises that adopt it can generate twice the ROI they are currently stuck with. Financial enterprises that recognize this early are creating systems that think through transaction processes instead of mundanely generating them.

AvenuesAI is a helpful example because it shows a specific design philosophy. Here, AI is the decision engine at its core, managing fraud scoring, compliance checks, routing logic, and settlement sequencing simultaneously, in real time, and at scale, instead of being a hype addition.

This difference is very important when evaluating what it actually takes to create something in this field. Companies operating in multiple markets need platforms where smart automation can manage complexity that humans cannot keep up with, without increasing regulatory risks. Building at this level needs a clear design strategy, compliance engineering that can withstand regulatory review, and a true understanding of where AI provides real operational benefits.

At Intellivon, we develop these systems following the train of thought used to build AvenuesAI. This blog explains what that process looks like, from essential infrastructure decisions to the compliance and AI layers, and demonstrates how we can build you such a platform from the ground up.

Why Are Enterprises Building Platforms Like AvenuesAI Today?

Building an AI-powered payment platform like AvenuesAI is no longer about moving money. Instead, it rests on creating a sovereign financial operating system. Enterprises are abandoning traditional gateways because they lack the intelligence to handle fragmented global markets and rising transaction costs.

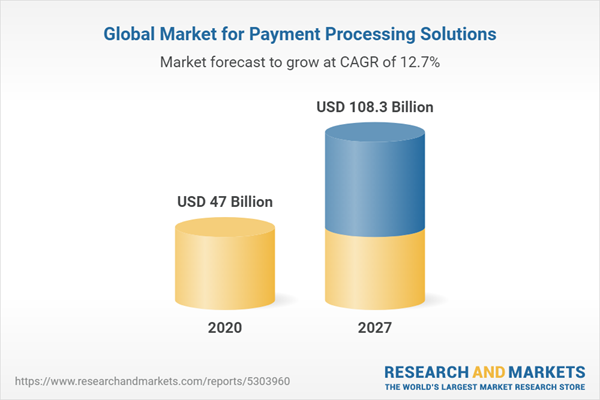

The global market for payment processing solutions is expanding rapidly. Valued at roughly USD 58.5 billion in 2022, this sector is on track to reach USD 161.9 billion by 2030. This growth represents a compound annual growth rate (CAGR) of 13.6%. While this steady climb is significant, it is being outpaced by the explosive rise of AI-integrated systems.

By building a dedicated orchestration layer, you replace rigid “pipes” with an adaptive system that centralizes data, risk management, and vendor governance.

A unified platform like AvenuesAI consolidates these vendors into one layer, eliminating the friction of manual reconciliation and multiple contracts. This shift allows leaders to treat payments as a strategic asset.

1. Limits of PSPs like Stripe and Adyen

While major providers offer convenience, they often function with rigid fee structures. At the same time, high-volume enterprises eventually outgrow these models because they cannot customize the underlying logic or negotiate aggressive interchange pass-throughs. Relying on a single provider also creates a systemic risk, which is that if their service lags, your entire revenue stream halts.

2. Rising fraud complexity and cost pressure

Legacy fraud detection relies on static rules that fail against modern, AI-driven social engineering and botnets. These attacks drive up chargeback costs and insurance premiums.

A custom platform utilizes machine learning to identify anomalous patterns in real-time, protecting margins without blocking legitimate transactions.

3. Need for real-time payment decision control

Enterprises require the autonomy to toggle processors based on instant performance data. Consequently, if a specific gateway in Europe sees a dip in approval rates, an intelligent system reroutes traffic to a healthy alternative immediately. This level of granular control ensures that no transaction is left to chance.

4. Ownership of payment data and intelligence

Data is the primary currency of the digital age. By building a proprietary layer, companies retain full ownership of their customer transaction history. This data is then used to train internal models for better credit scoring, churn prediction, and personalized loyalty programs.

5. Strategic advantage of AI-powered infrastructure

An AI-led approach transforms payments from a utility into a competitive moat. It allows for rapid experimentation with new business models like subscription-based micro-payments or cross-border settlement using stablecoins.

This technical agility ensures the business remains ahead of regulatory and market shifts.

6. Intelligent routing and risk

Static routing leads to failed transactions and lost revenue. An AI-powered platform uses real-time decisioning to send transactions through the path of least resistance, maximizing approval rates.

It simultaneously evaluates fraud signals to block sophisticated attacks while reducing false positives.

7. Unified cost-and-compliance control

A central layer standardizes global regulations and scheme fees into a single workflow. This visibility allows treasury teams to optimize FX rates and avoid unnecessary international fees. At the same time, automation ensures the business stays compliant across jurisdictions without increasing headcount.

8. Speed to market

Pre-built primitives for dispute prediction and cash-flow forecasting allow product teams to launch new features like BNPL instantly. This modular approach reduces technical debt and accelerates the deployment of embedded finance solutions.

Controlling your payment logic creates a durable competitive advantage. It transforms transaction data into a proprietary asset that scales without operational risks.

Why Is AvenuesAI a Real-World Benchmark for AI Payments?

This specific platform serves as a blueprint because it successfully transitions from simple transaction processing to complex financial orchestration.

It demonstrates how machine learning solves high-stakes problems like global routing and real-time liquidity management.

1. Evolution from gateway to AI-powered payment platform

The transition of this infrastructure highlights a fundamental shift from simple data transfer to active financial orchestration. Modern systems now operate as an intelligent transaction infrastructure that makes autonomous decisions to improve outcomes.

This evolution allows the platform to handle the complex needs of modern enterprises by automating tasks that previously required human intervention.

2. How AvenuesAI applies AI in live payment systems

AI functions as the core brain of the system, managing everything from routing to risk assessment in real-time. Specialized agents monitor the health of various banking networks to ensure that every payment follows the most reliable path.

These AI layers work simultaneously to increase successful sales while keeping operational costs low.

3. Why enterprises benchmark against this model

Decision-makers study this model because it combines high technical performance with measurable business results. It proves that a single, unified environment can replace a fragmented collection of legacy tools.

Furthermore, observing this framework helps founders understand how to build a scalable system that grows without increasing complexity.

4. Role in modern fintech infrastructure

This platform acts as a foundational pillar for the next generation of digital financial services. It provides the essential connectivity needed to link different banking systems, mobile wallets, and local payment methods globally.

As a result, businesses can focus on their core product while the infrastructure handles the heavy lifting.

5. What makes it commercially and technically relevant

The commercial relevance of this system stems from its ability to turn payment data into a compounding asset. Technically, the platform is built to handle massive scales without sacrificing speed or security.

It represents a shift toward a more efficient, automated, and data-rich future for global commerce.

The success of this model illustrates that the future of finance lies in moving beyond basic processing toward total orchestration. Following this benchmark ensures that an enterprise build is prepared for the demands of an increasingly digital world.

What Is an AI Payment Platform Like AvenuesAI?

AvenuesAI functions as a sophisticated intelligence layer that sits between an enterprise and the global financial network. It replaces static rules with dynamic, data-driven logic to ensure every transaction is processed at the lowest cost and highest success rate.

1. Core definition in enterprise payment ecosystems

- Centralized AvenuesAI Intelligence: The platform acts as a brain that oversees all incoming and outgoing financial flows across multiple regions.

- Autonomous Operations: AvenuesAI utilizes machine learning to handle routine tasks like reconciliation and bank switching without manual input.

- Unified Connectivity: By providing a single integration point, AvenuesAI links various payment methods, currencies, and banking partners into one dashboard.

- Sovereign Infrastructure: This model allows enterprises to own their financial logic rather than being locked into a single provider’s ecosystem.

2. AI-native vs traditional payment architectures

Traditional systems are built on rigid code that follows “if-then” logic, which often fails in complex, changing markets.

In contrast, AvenuesAI is an AI-native architecture designed to learn from every transaction, making it more resilient and adaptive over time.

| Feature | Traditional Architecture | AvenuesAI (AI-Native) |

| Decision Logic | Hard-coded, static rules | Dynamic machine learning models |

| Routing | Fixed paths (e.g., Bank A first) | Real-time path optimization |

| Scalability | Requires manual updates for new markets | Automatically adapts to new data patterns |

| Data Usage | Records data for reporting only | Uses data to improve future performance |

| Integration | Heavy, siloed technical debt | Modular, API-first orchestration |

3. Role of AI in decision-making across payments

- AvenuesAI Predictive Routing: The system forecasts which bank is most likely to approve a transaction based on current network health.

- Dynamic Retries: If a payment fails due to a technical error, AvenuesAI determines the best time and route to try again to capture the sale.

- Smart Throttling: AvenuesAI manages high-volume traffic during peak times to prevent system overloads and transaction timeouts.

- Treasury Optimization: The platform’s AI analyzes liquidity across different accounts to recommend the best movement of funds.

4. System boundaries: payments, fraud, analytics

- Integrated Payments: The core AvenuesAI layer handles the actual movement of money across gateways and acquiring banks globally.

- Adaptive Fraud Layer: Instead of a separate tool, AvenuesAI bakes fraud detection into the payment flow to block threats with millisecond precision.

- Predictive Analytics: This boundary moves beyond simple reporting to provide “what-if” scenarios and growth forecasting based on payment trends.

- Unified Governance: AvenuesAI manages all three areas under one compliance framework, ensuring data privacy and security standards are met.

5. Why orchestration is central to modern platforms

- Vendor Agility: AvenuesAI orchestration allows a business to add or remove payment providers instantly without rebuilding its technical stack.

- Cost Efficiency: By shifting volume between providers in real-time, AvenuesAI automatically pursues the lowest available processing fees.

- Global Reach: AvenuesAI provides a standardized way to enter new countries by simply “plugging in” local payment methods to the orchestrator.

- Operational Resilience: If one gateway goes down, the AvenuesAI orchestrator shifts all traffic to a healthy alternative, preventing any revenue downtime.

The structural change provided by AvenuesAI ensures that enterprises remain agile, profitable, and technologically independent. This shift allows leaders to focus on growth while the infrastructure handles the complexities of global finance.

How Do Platforms Like AvenuesAI Differ from PSPs?

Choosing between a standard Payment Service Provider (PSP) and an orchestration platform like AvenuesAI is a decision between using a service and owning an asset.

This distinction defines whether an enterprise is a passive participant in the financial network or an active architect of its own transaction logic.

1. Static rules vs AI-driven decision systems

Traditional gateways operate on rigid, pre-defined logic that requires manual updates to handle new market conditions.

AvenuesAI utilizes machine learning to evaluate transaction data dynamically, allowing the system to adjust its behavior in real-time without human intervention.

| Feature | Traditional PSP Rules | AvenuesAI Decisioning |

| Logic Type | Hard-coded “If-Then” statements | Adaptive Machine Learning models |

| Adaptability | Requires manual coding for changes | Self-corrects based on new data |

| Precision | Broad filters often block good sales | Granular analysis reduces false positives |

| Maintenance | High operational overhead | Automated model retraining |

2. Fixed routing vs intelligent orchestration

A standard PSP typically locks your traffic into its own proprietary network, offering no fallback if its performance dips.

AvenuesAI provides an orchestration layer that views every global bank and rail as a potential path, selecting the best one for every unique payment.

| Aspect | Fixed PSP Routing | AvenuesAI Orchestration |

| Provider Access | Single-vendor lock-in | Multi-vendor agility |

| Path Selection | Static and non-negotiable | Dynamic based on success rates |

| Redundancy | Total downtime if the vendor fails | Instant failover to healthy routes |

| Cost Control | Fixed merchant discount rates | Real-time pursuit of the lowest fees |

3. Reactive fraud vs predictive fraud prevention

Most service providers react to fraud only after a breach has occurred or a signature is matched.

AvenuesAI employs a predictive stance, identifying sophisticated anomalies and behavioral shifts before the transaction is finalized to stop losses before they happen.

| Fraud Component | Reactive PSP Approach | AvenuesAI Predictive Layer |

| Detection Timing | Post-transaction or simple blacklists | Real-time behavioral scanning |

| Threat Intelligence | Limited to the vendor’s database | Global, cross-network pattern recognition |

| Friction Level | High (triggers 3DS frequently) | Low (identifies “safe” users accurately) |

| Risk Evolution | Struggles with “Day Zero” attacks | Predicts and blocks novel attack vectors |

4. Vendor dependency vs infrastructure ownership

Relying on a PSP means your business logic is hosted and controlled by a third party.

Building or embedding a platform like AvenuesAI allows the enterprise to own the underlying infrastructure, providing the freedom to pivot strategies without asking for permission.

| Factor | Vendor Dependency (PSP) | Infrastructure Ownership (AvenuesAI) |

| Strategic Control | Determined by the vendor roadmap | Controlled by the enterprise |

| Data Sovereignty | Data is often siloed with the vendor | Full ownership of transaction assets |

| Switching Costs | Extremely high (requires rebuilding) | Low (modular provider management) |

| Brand Experience | Often generic or vendor-branded | Fully white-labeled and embedded |

5. Limited data vs full payment intelligence control

Standard processors provide basic reports that satisfy accounting needs but fail to offer deep strategic value.

AvenuesAI turns every transaction into a rich data point, fueling advanced analytics that can predict churn and optimize corporate treasury.

| Data Capability | Standard PSP Reporting | AvenuesAI Intelligence |

| Visibility | Surface-level (Success/Fail) | Deep-dive (Sub-code & latency analysis) |

| Predictive Insights | None | Forecasts CLV and revenue leakage |

| Integration | Limited to basic exports | Direct sync with ERP and AI models |

| Customization | Standardized templates | Fully customizable data schemas |

The shift from a service-based model to an ownership-based model ensures that an enterprise can scale without being held back by vendor limitations. By prioritizing intelligence and autonomy, leaders transform their payment stack into a powerful engine for long-term growth.

Architecture Supporting Payment Platforms Like AvenuesAI?

The foundation of an AI-powered payment platform like AvenuesAI is a sophisticated, multi-layered architecture designed for extreme speed and modularity.

This structural design ensures the system can process millions of decisions per second without sacrificing security or operational stability.

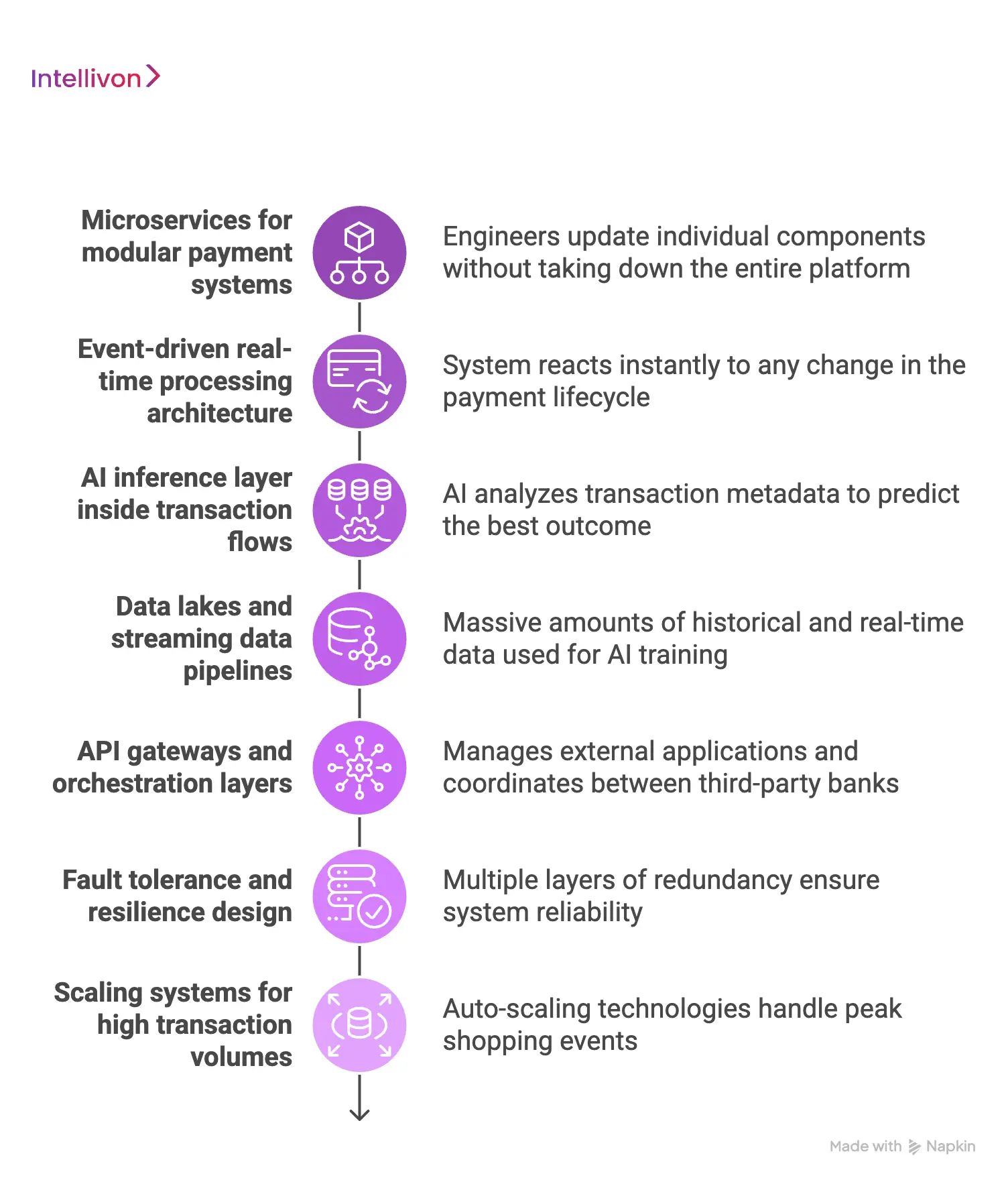

1. Microservices for modular payment systems

Large financial systems are often broken down into smaller, independent services that handle specific tasks like currency conversion or tax calculation. This modular approach allows engineers to update individual components without taking down the entire platform.

Consequently, the business can innovate faster by deploying new features to a single service rather than rebuilding the whole system.

This architecture ensures that the platform remains agile and easy to maintain as it grows in complexity.

2. Event-driven real-time processing architecture

Modern systems use an event-driven design to react instantly to any change in the payment lifecycle.

When a user clicks “pay,” the system triggers a chain reaction of events across different services, such as fraud checks and ledger updates.

- Reduced Latency: Decisions happen in parallel rather than waiting in a slow, linear queue.

- Instant Reconciliation: Every event is logged as it happens, ensuring financial records are always up-to-date.

- Enhanced Performance: The system can handle sudden spikes in traffic by distributing the workload across various event handlers.

3. AI inference layer inside transaction flows

The AI inference layer acts as the “brain” embedded directly within the data pipeline to make split-second decisions. Unlike traditional software that simply follows a path, this layer analyzes transaction metadata to predict the best outcome before the money moves.

This placement is critical because even a few milliseconds of delay can lead to a timed-out transaction. Therefore, the architecture is optimized to keep the AI model close to the core transaction flow for maximum efficiency.

4. Data lakes and streaming data pipelines

AI-powered payment platforms like AvenuesAI rely on massive amounts of historical and real-time data to remain effective.

Data lakes store every transaction detail for long-term model training, while streaming pipelines feed current events into the AI in real-time.

- Continuous Training: The models get smarter by constantly “reading” new data from the lake.

- Real-time Insights: Streaming pipelines allow dashboards to show live performance metrics without delay.

- Security Auditing: Centralized data storage makes it easier to perform deep security forensic checks if an anomaly is detected.

5. API gateways and orchestration layers

The API gateway serves as the front door, managing how external applications talk to the internal payment logic.

The orchestration layer then takes over, coordinating between multiple third-party banks and internal AI services to find the optimal result.

This layer abstracts away the complexity of dealing with different banking languages, providing a clean interface for the enterprise. It ensures that no matter how many banks you add, the integration remains simple and unified.

6. Fault tolerance and resilience design

Reliability is the most important metric for any financial system, which is why the architecture includes multiple layers of redundancy.

If one server or data center fails, the system automatically shifts traffic to a backup without the user ever noticing.

- Automatic Failover: Traffic is rerouted instantly if a primary banking partner goes offline.

- Database Mirroring: Transaction records are stored in multiple locations simultaneously to prevent data loss.

- Self-Healing Logic: The AI can detect a failing service and restart it or route around it automatically.

7. Scaling systems for high transaction volumes

As a business grows, the architecture must be able to handle an increasing number of payments per second.

AI-powered payment platforms like AvenuesAI use “auto-scaling” technologies that automatically add more processing power during peak shopping events. This elasticity ensures that the system stays fast and responsive regardless of the load.

By planning for scale at the architectural level, founders avoid the expensive “bottlenecks” that often plague legacy payment gateways.

The underlying architecture of these platforms turns a complex technical challenge into a seamless business advantage. By combining modularity with real-time intelligence, enterprises create a foundation that is both resilient and infinitely scalable.

How to Integrate AI Payment Platforms with Legacy Systems?

Modernizing financial infrastructure does not require a complete “rip and replace” of existing core banking or ERP systems.

AI-powered payment platforms like AvenuesAI are designed to sit on top of legacy layers, acting as a sophisticated bridge that adds intelligence without disrupting established workflows.

1. Middleware abstraction for legacy cores

Middleware acts as a translation layer that allows modern AI logic to communicate with older, rigid banking cores.

This abstraction ensures that the legacy system remains untouched while the AI-powered payment platform handles the complex decision-making and routing. By using this buffer, enterprises can enjoy the benefits of advanced orchestration without the risk of breaking their stable back-end records.

2. API-first integration strategies

An API-first approach ensures that the new payment layer can be plugged into any part of the enterprise ecosystem with minimal friction. AvenuesAI provides clean, standardized endpoints that allow developers to connect legacy databases to modern AI modules instantly.

- Simplified Connectivity: Standardized APIs replace custom, fragile code pathways.

- Modular Rollouts: Specific features like fraud detection can be integrated before moving the entire payment flow.

- Future-Proofing: New banking partners can be added via the API without modifying the legacy core.

3. Data synchronization across systems

Maintaining a single source of truth is vital when running a modern platform alongside an older ledger.

AI-powered payment platforms like AvenuesAI use real-time sync engines to ensure that every transaction is mirrored across both the new and old systems.

- Bi-Directional Sync: Changes in the legacy system are reflected in the AI dashboard and vice versa.

- Conflict Resolution: The AI automatically identifies and fixes discrepancies between different data versions.

- Latency Management: Synchronization happens in the background to ensure checkout speed is never impacted.

4. Phased migration without downtime

Moving to a new platform is best handled in stages to prevent any interruption in revenue or customer service. AvenuesAI allows for a “canary deployment” where a small percentage of traffic is moved to the AI layer while the rest stays on the old system.

- Risk Mitigation: Any issues are identified on a small scale before a full transition.

- Performance Comparison: Leaders can see the immediate lift in approval rates on the new system.

- Seamless Cutover: Once the new path is proven, the remaining traffic is shifted over gradually.

5. Handling inconsistent legacy data formats

Legacy systems often store data in outdated or non-standard formats that are difficult for modern models to read. AvenuesAI includes automated data normalization tools that clean and reformat this information as it passes through the platform.

This ensures that the AI has high-quality, consistent data to make accurate routing and risk decisions. By solving the “garbage in, garbage out” problem, the platform ensures that even the oldest systems can benefit from modern intelligence.

6. Avoiding tight coupling and failures

Building a “loose” connection between the AI platform and the legacy core prevents a failure in one from taking down the other. If the legacy database experiences a delay, the AI-powered payment platform, like AvenuesAI, can continue to process and queue transactions independently.

This resilience is essential for maintaining 24/7 operations in a global market. It ensures that the enterprise stays functional even during maintenance windows or technical glitches in older infrastructure.

This integration strategy allows a business to evolve at its own pace while immediately capturing the value of AI. By bridging the gap between old and new, enterprises create a hybrid environment that is both stable and highly innovative.

How Do Multi-Rail Systems Like AvenuesAI Work?

A multi-rail system like AvenuesAI functions as a high-speed traffic controller for the global financial network. It ensures that money moves through the most efficient path available, whether that is a traditional card network or a modern instant-payment rail.

1. Routing across cards, RTP, and bank rails

AvenuesAI connects to a diverse array of financial “rails” to give enterprises maximum flexibility in how they collect and send funds. By supporting everything from standard credit cards to global Real-Time Payment (RTP) networks, the platform allows businesses to meet customers wherever they are.

This multi-rail approach means that if one network is slow or expensive, the system can instantly pivot to a more suitable alternative. It removes the limitations of being tied to a single payment method.

2. AI-based cost and success optimization

The platform uses intelligent algorithms to weigh the cost of a transaction against its likelihood of being approved. Platforms like AvenuesAI analyze historical data and real-time performance metrics to determine which rail offers the best balance for a specific payment.

- Margin Protection: The system automatically prioritizes lower-cost rails like bank transfers when the risk profile allows.

- Approval Maximization: High-priority payments are routed through the most reliable rails to ensure a successful checkout.

- Dynamic Fee Management: The AI accounts for shifting interchange and scheme fees to protect the enterprise’s bottom line.

3. Failover logic across payment networks

Reliability is built into the core of AvenuesAI through automated failover logic that prevents transaction drops. If a specific banking partner or card network experiences a technical glitch, the system detects the failure in milliseconds and reroutes the traffic.

This ensures that the customer experience remains uninterrupted, even during large-scale network outages. By having multiple “backup” paths ready at all times, the platform provides the 24/7 uptime that modern digital commerce demands.

4. Cross-border payment intelligence

International transactions are often plagued by high fees and slow settlement times, but AvenuesAI uses localized intelligence to solve these issues. The platform identifies the best regional partners and local rails to use for cross-border flows, often avoiding expensive intermediary bank fees.

- Local Acquiring: Routing payments through banks in the customer’s home country to boost approval rates.

- Compliance Orchestration: The AI ensures that every international transfer meets the specific regulatory requirements of both the sender and receiver.

- Transparency: Real-time tracking provides clear visibility into where funds are at every stage of the global journey.

5. Currency conversion and settlement handling

AvenuesAI simplifies the complexity of dealing with multiple currencies by automating the conversion and settlement process. The system looks for the best available FX rates in real-time to minimize the cost of converting international revenue back into the enterprise’s home currency.

- Smart Settlement: AI-powered payment platforms like AvenuesAI can hold funds in multiple currencies to avoid unnecessary conversion fees.

- Automated Payouts: Funds are settled into corporate accounts according to pre-set logic that optimizes for liquidity and tax efficiency.

- Rate Locking: The platform can hedge against currency volatility by locking in favorable rates for large-scale settlements.

6. Extending rails to include blockchain networks

The architecture of platforms like AvenuesAI is designed to bridge traditional finance with the emerging world of digital assets. By treating blockchain networks as just another “rail,” the platform allows enterprises to settle transactions using stablecoins or other tokenized assets.

This addition provides a new level of speed and 24/7 availability that traditional banking hours cannot match. It prepares businesses for a future where programmable money becomes a standard part of global trade.

7. AI deciding between fiat and on-chain settlement

The most advanced feature of the AvenuesAI orchestration layer is its ability to choose the best settlement medium, which is traditional fiat or blockchain-based stablecoins. The AI evaluates the current gas fees on the blockchain against the wire fees of the banking system.

- Liquidity Optimization: The system chooses the fastest route to get usable capital into the company’s treasury.

- Counterparty Risk: AI assesses the stability of the settlement rail to ensure funds arrive safely.

- Programmable Settlement: The platform can trigger payouts automatically based on smart contract conditions, merging the best of both financial worlds.

The sophisticated multi-rail logic of AvenuesAI ensures that an enterprise is never limited by the friction of old-fashioned banking. By using AI to navigate the world’s financial paths, businesses can move money at the speed of the internet.

What Is the Revenue Model of Platforms Like AvenuesAI?

The commercial structure of an AI-powered payment platform like AvenuesAI is designed to scale alongside the growth of the enterprise it serves.

This model ensures that the interests of the platform and the business are aligned by focusing on performance, volume, and long-term value creation.

1. Transaction-based revenue streams

The primary engine of growth for these platforms is a small fee applied to every successful transaction processed through the orchestration layer.

This approach ensures that the platform only generates significant revenue when the enterprise is successfully moving money and completing sales.

| Fee Type | Description | Strategic Benefit |

| Volume Rebates | Lower fees for higher transaction counts | Encourages enterprise-wide adoption |

| Per-Transaction Fee | A fixed cent-based or percentage fee | Predictable costs for budgeting |

| Success-Only Billing | Fees applied only to approved payments | Aligns the platform with performance goals |

2. SaaS and subscription pricing layers

In addition to transaction fees, platforms like AvenuesAI often charge a recurring subscription fee for access to the core infrastructure. This “platform fee” covers the ongoing maintenance, security updates, and cloud hosting costs required to keep the system running 24/7.

It provides the enterprise with a stable, predictable cost for maintaining its sovereign financial environment. Consequently, the business can plan its technical budget with high accuracy while enjoying the benefits of a managed, high-performance ecosystem.

3. Monetization of fraud and analytics tools

Specialized AI modules, such as advanced fraud detection and predictive analytics, are often offered as high-value add-ons. Enterprises can choose to pay for these features based on the level of protection or depth of insight they require.

- Risk-Based Pricing: Fees tied to the number of fraud checks performed or the volume of disputes prevented.

- Premium Insights: Access to deep-dive AI reporting and churn prediction dashboards.

- Optimization Incentives: Some models offer a “gain-share” where the platform takes a percentage of the savings generated by its AI routing.

4. Integration and onboarding fees

Building a custom or embedded platform requires an initial investment in setup and technical integration. These one-time fees cover the cost of connecting the AI-powered payment platform, like AvenuesAI, to the enterprise’s existing legacy cores and third-party banks.

This phase ensures that the system is perfectly tuned to the specific needs and data formats of the organization. It represents an investment in creating a durable, long-term asset that will serve the company for years to come.

5. Enterprise licensing and customization

Large-scale organizations often require unique features or specific security configurations that go beyond standard offerings.

In these cases, the revenue model includes licensing fees for custom development and dedicated support teams.

- White-Label Licensing: Fees for rebranding the platform as a proprietary internal tool.

- Dedicated Support: Premium tiers for 24/7 technical assistance and strategic consulting.

- Custom AI Training: Specialized fees for training the models on the enterprise’s unique historical data sets.

6. Recurring vs usage-based revenue mix

The most successful platforms like AvenuesAI utilize a hybrid model that combines stable recurring revenue with flexible usage-based growth.

This mix provides the platform with the capital needed for constant innovation while giving the enterprise the flexibility to pay only for what they use.

- Stable Foundation: Subscription fees ensure the infrastructure is always modern and secure.

- Growth Elasticity: Usage fees allow the cost to scale naturally as the business expands into new markets.

- Predictive Budgeting: The hybrid approach allows CFOs to forecast costs while maintaining the ability to handle seasonal spikes in volume.

This diversified revenue model ensures that platforms like AvenuesAI remain financially robust while providing maximum value to their clients. By linking profit to performance and growth, these platforms foster a true partnership with the enterprises they power.

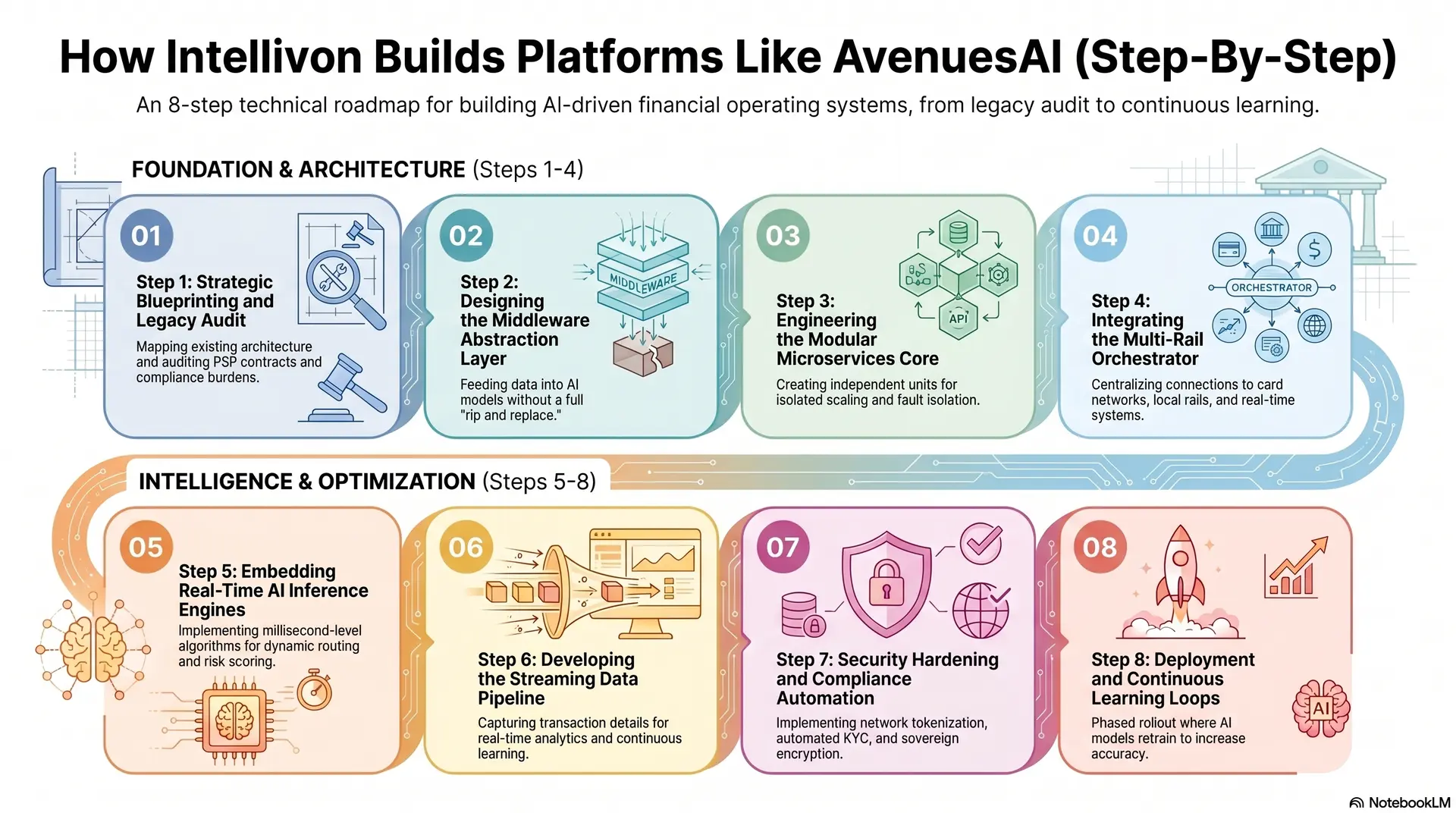

How Intellivon Builds Platforms Like AvenuesAI (Step-By-Step)

At Intellivon, we approach the construction of an AI-powered payment platform as the development of a mission-critical financial operating system.

Our methodology ensures that we build a foundation that is not only resilient and secure but also capable of autonomous growth through deep machine learning integration.

Step 1: Strategic Blueprinting and Legacy Audit

We begin by mapping your existing financial architecture and identifying specific areas where “dumb” pipes are causing margin erosion.

This phase involves a deep audit of your current payment service provider (PSP) contracts, approval rates, and regional compliance burdens.

- Stakeholder Alignment: Establishing clear KPIs such as target approval rates and processing cost reductions.

- Technical Auditing: Reviewing existing legacy systems to design the optimal middleware abstraction layer.

- Infrastructure Design: Choosing the right cloud or hybrid environment to support high-volume transaction loads.

Step 2: Designing the Middleware Abstraction Layer

To avoid disrupting your core business, we build an abstraction layer that sits between your legacy systems and the new orchestration engine.

This layer allows us to feed data into our AI models without requiring a full “rip and replace” of your existing ERP or banking cores.

| Component | Function | Enterprise Benefit |

| Data Adapter | Converts legacy formats to JSON/modern APIs | No need to rewrite old database logic |

| State Manager | Tracks transaction status across systems | Maintains a single source of truth |

| Security Proxy | Encrypts data before it leaves the core | Ensures local data remains private |

Step 3: Engineering the Modular Microservices Core

We construct the platform using a microservices architecture, where every function operates as an independent unit.

This modularity is essential because it allows us to update or scale specific parts of the platform without impacting the entire system.

- Isolated Scaling: Add power to the “fraud service” during peak sales without affecting the “ledger service.”

- Rapid Deployment: Test and launch new features in days rather than months.

- Fault Isolation: If one service experiences a delay, the rest of the platform remains functional.

Step 4: Integrating the Multi-Rail Orchestrator

Our team connects your platform to a diverse array of global financial rails. We centralize these connections into a single, unified orchestration layer that acts as the primary traffic controller for your money movement.

- Card Networks: Direct connections to Visa, Mastercard, and Amex.

- Local Rails: Integration with regional systems like UPI, SEPA, or Pix.

- Real-Time Rails: Support for RTP (Real-Time Payments) and FedNow for instant settlement.

Step 5: Embedding Real-Time AI Inference Engines

This is where we inject the “brain” into the platform by placing AI models directly into the live transaction stream. We implement specialized algorithms that perform millisecond-level inference to decide on the best routing path and risk score.

| AI Model Type | Specific Application | Outcome |

| Random Forest | Real-time fraud scoring | Blocks theft while allowing good sales |

| Multi-Armed Bandit | Dynamic routing optimization | Finds the bank most likely to say “Yes” |

| XGBoost | Decline analysis and smart retries | Recovers revenue from technical failures |

Step 6: Developing the Streaming Data Pipeline

We build high-speed data pipelines that capture every transaction detail and feed it into a central data lake. This streaming architecture allows your platform to perform real-time analytics and provides the raw material for continuous machine learning.

- Real-time Visibility: Dashboards that update every millisecond with success/fail data.

- Model Feed: Outcome data is sent back to the AI to help it learn from every transaction.

- Audit Readiness: Every single event is timestamped and logged for regulatory transparency.

Step 7: Security Hardening and Compliance Automation

We embed global security standards directly into the code, ensuring the platform is natively compliant with PCI-DSS, GDPR, and regional fintech regulations. This step involves implementing advanced network tokenization and vaulting techniques.

- Network Tokenization: Replaces card numbers with secure tokens that only work for your merchant ID.

- Automated KYC/KYB: Built-in identity verification flows for rapid merchant or user onboarding.

- Sovereign Encryption: You hold the keys to your data, ensuring total privacy from third-party vendors.

Step 8: Deployment and Continuous Learning Loops

The final step is a phased rollout where we gradually shift traffic to the new platform while monitoring performance through a feedback loop.

As the system processes real transactions, the AI models retrain themselves to become more accurate.

| Phase | Action | Purpose |

| Canary Release | Route 1-5% of traffic to the AI layer | Verify stability on a small scale |

| Optimization | AI adjusts weights based on live bank responses | Maximize approval rates in real-time |

| Full Cutover | Shift 100% of volume to the new ecosystem | Achieve total technical and financial sovereignty |

This structured approach allows us to deliver a sovereign financial platform that scales with your ambition. By partnering with Intellivon, you gain a dedicated engineering ally focused on turning your payment infrastructure into a durable competitive advantage.

What Does It Cost to Build Like AvenuesAI?

Building an AI-powered payment platform like AvenuesAI is not a fixed-cost project.

It’s a multi-layer infrastructure investment that depends on AI depth, integrations, compliance, and scale.

However, based on real fintech benchmarks, you can break it down into three practical investment tiers:

Total Investment Range by Platform Scope

| Build Scope | Timeline | Investment Range |

| MVP (Core payments + basic AI fraud) | 4–6 months | $70,000 – $150,000 |

| Mid-Scale Platform (AI routing + multi-rail) | 6–10 months | $150,000 – $300,000 |

| Enterprise Platform (AvenuesAI-like system) | 10–18 months | $300,000 – $600,000+ |

Why these ranges:

- AI-powered fintech platforms typically start around $70K–$150K for MVPs and scale beyond $300K+ for advanced systems

- Full-featured fintech ecosystems can exceed $400K+, depending on modules and compliance

Cost Breakdown by Core System Layers

| System Layer | % of Total Cost | What You’re Paying For |

| Payment Infrastructure | 20–25% | Transaction processing, APIs, orchestration |

| AI & Decision Systems | 20–30% | Fraud models, routing engines, training pipelines |

| Compliance & Security | 15–25% | PCI DSS, AML/KYC, encryption, audits |

| Integrations (Banks, Rails, APIs) | 15–20% | UPI, cards, wallets, third-party systems |

| Frontend & Dashboards | 10–15% | Merchant dashboards, admin panels |

| DevOps & Cloud Infrastructure | 10–15% | Hosting, scaling, and monitoring systems |

Key insight:

AI alone can increase cost by 20–40% due to model training and real-time processing complexity

What Drives Cost in AvenuesAI-Like Platforms?

These are the real cost drivers enterprise buyers care about:

- AI complexity → Fraud detection vs full decision engine

- Number of payment rails → UPI, cards, RTP, SWIFT, crypto

- Compliance scope → Single country vs multi-region

- Integration depth → Banks, gateways, KYC, risk systems

- Transaction volume requirements → Scaling infra cost

- Real-time decision latency requirements → High-performance systems

Hidden Costs Most Enterprises Miss

This is where budgets usually break.

- Compliance audits and certifications (PCI, GDPR)

- Ongoing cloud and infrastructure costs

- Model retraining and data pipeline maintenance

- Payment network and API usage fees

- Security upgrades and incident response systems

Maintenance alone typically adds 15–20% annually to the initial build cost

Despite the investment, companies choose to build because:

- Reduce fraud losses by millions annually

- Improve payment success rates by 5–15%

- Cut routing costs through intelligent optimization

- Gain full control over payment data and margins

Get a Cost Estimate for Your AI Payment Platform

If you’re evaluating whether to build a platform like AvenuesAI, the fastest way to get clarity is to map your requirements to a realistic cost range.

At Intellivon, we help enterprises break this down based on:

- Your target transaction volume and scale

- Required payment rails and integrations

- AI capabilities across fraud, routing, and decisioning

- Compliance requirements across regions

Instead of generic estimates, you get a clear cost structure, timeline, and system blueprint aligned to your business goals.

Share your requirements, and we’ll give you a practical estimate of what it takes to build your platform.

Conclusion

Implementing an AI-powered payment platform like AvenuesAI transforms financial infrastructure into a strategic asset. By prioritizing orchestration and AI, enterprises achieve superior approval rates and total technical sovereignty.

Partnering with Intellivon ensures your system is built for scale, security, and the future of autonomous, data-driven global commerce.

Build A Scalable And AI-Ready Backend For Your Platform With Intellivon

Building an enterprise platform like AvenuesAI requires more than just moving money; it requires a backend that can think. At Intellivon, we build infrastructure where high-speed AI inference and strict regulatory compliance coexist.

Our approach ensures your platform satisfies bank partners and auditors while scaling through autonomous, data-driven intelligence.

A. Embedding AI and Compliance Into Core Architecture

Compliance and intelligence are most effective when they are designed into the platform foundation from day one. We build banking systems where auditability and AI-driven decisioning are part of the core code, not expensive add-ons.

- Audit-Ready AI: Every decision made by the AI routing or fraud engine is logged with a clear evidence trail for investigations.

- Granular Security: Role-based access controls with approval logic are baked into the core to protect your AI models.

- Intelligent Visibility: Event logging covers every action across onboarding, AI-driven payments, and account activity.

- Strategic Data Design: Data structures are optimized to feed your machine learning models while supporting long-term retention and traceability.

B. Building AI-Native AML, KYC, and Monitoring Workflows

Banking compliance depends on how your operational workflows actually function. We build systems that support identity checks and transaction monitoring using the same AI-native approach used for payment orchestration.

| Workflow Component | AI-Native Implementation | Operational Benefit |

| Verified Onboarding | AI-assisted KYC/KYB document verification | Faster, friction-free user acquisition |

| Proactive Screening | Real-time sanctions and PEP watchlist integration | Instant protection for your payment rails |

| Automated Vigilance | Machine learning pattern detection for AML | Lower false positives in fraud alerts |

| Operational Oversight | Intelligent review queues for compliance teams | Efficient management of high-risk cases |

C. Preparing AI Platforms for Bank and Enterprise Due Diligence

A strong compliance posture is critical when convincing tier-1 institutions to partner with your AI platform. We help you build systems that stand up to the deepest scrutiny, proving that your AI logic is transparent, accountable, and secure.

- Control Maturity: Your architecture is aligned with the security and control expectations of global financial institutions.

- Evidence-Based Logic: We provide clear logs explaining why the AI chose a specific route or flagged a specific transaction.

- Partner Credibility: Platform logic is built for accountability, making your AI more credible in high-stakes partnership conversations.

Planning an AI-powered payment or banking platform? Connect with Intellivon today to discuss your technical requirements and get a tailored project estimate.

FAQs

Q1. What’s the real difference between an AI-powered payment platform and a traditional one with some ML fraud detection bolted on?

A1. A bolted-on model reacts. At the same time, a native AI platform reasons. The difference is architectural, where AI-native systems make routing, compliance, and fraud decisions in a unified inference layer, in real time, before settlement. Additionally, traditional platforms with ML overlays introduce latency, blind spots, and decision conflicts that compound at enterprise transaction volumes.

Q2. What’s a realistic development cost range for an AI-powered payment platform at enterprise scale?

A2. Scope determines cost more than ambition does. At the same time, a production-ready AI payment platform with compliance infrastructure, fraud models, and multi-rail support typically ranges from $400K to $600K+, depending on jurisdictions, integration complexity, and regulatory requirements. Additionally, the more important question is what the cost of not building it correctly the first time looks like.

Q3. How do we build an AI payment platform that stays compliant with different AML/KYC rules per jurisdiction?

A3. Through a modular compliance architecture. Each jurisdiction requires its own rule engine, not a one-size-fits-all policy layer. AI models can be trained to flag jurisdiction-specific risk signals, while a centralized compliance orchestration layer enforces the right AML/KYC framework per transaction origin, dynamically, without manual switching or operational overhead.

Q4. With AI agents starting to make autonomous purchase decisions on behalf of consumers, how do we future-proof our payment stack for agent-to-agent transactions?

A3. Design for programmable money movement from day one. Agent-to-agent commerce requires credentialed identity verification between non-human actors, consent frameworks, spending limit governance, and real-time settlement rails that don’t depend on human approval loops. Platforms built on rigid, user-centric assumptions will require fundamental rearchitecting. Building AI-native from the start avoids that entirely.