Key Takeaways:

-

A scalable banking backend requires a microservices architecture, event-driven infrastructure, API-first design, and cloud-native elasticity.

-

Real-time banking infrastructure depends on event streaming, reliable message brokers, and AI-powered fraud detection.

-

Security and cross-border compliance must be embedded at the design stage, covering Zero Trust enforcement, jurisdiction-aware data routing, and PCI DSS, SOC 2, and AML controls.

-

Building, buying, or partnering each carries distinct tradeoffs in cost, ownership, and long-term scalability that directly determine how much control an enterprise retains over its infrastructure.

-

How Intellivon builds scalable enterprise-grade backend tech stacks for your banking platform.

The backend infrastructure of an enterprise-grade banking platform has become the factor that decides how quickly the business can operate and generate ROI. In given scenarios where transaction volumes double, a new payment system needs to launch, and the backend infrastructure needs to be resilient to withstand modernization. For large financial institutions, this pressure arises more often than one would expect.

The remedy lies in building a scalable banking backend that manages real-time transaction processing, compliance across multiple jurisdictions, third-party API integrations, and unexpected traffic spikes without requiring extraordinary efforts each time the business expands. This combination results from intentional design choices made before any service goes live.

At Intellivon, we build banking backends that perform at that standard. Our goal is to construct a backend infrastructure that makes every downstream initiative, from AI deployment to open banking, structurally possible. This blog draws from that experience and breaks down exactly how we do it.

Why Do Enterprises Need Scalable Banking Backends?

Modern digital value chains now rely on embedded financial rails to manage massive transaction volumes and regulatory shifts.

Building a scalable banking backend ensures your infrastructure handles these spikes without performance loss or over-provisioning costs.

In 2026, this architecture serves as a strategic engine for high-revenue models like BaaS and real-time payments.

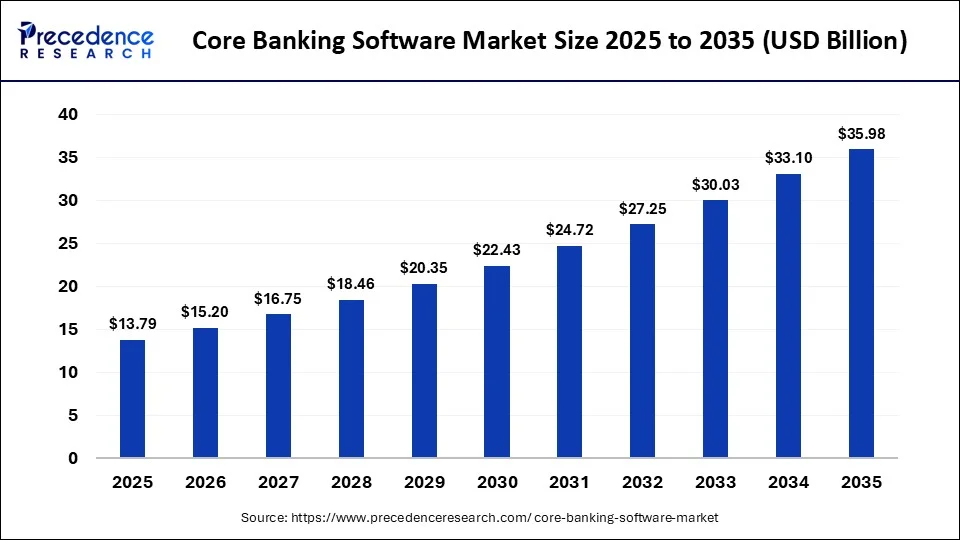

The global core banking software market reached $13.79 billion in 2025 and is projected to hit $15.20 billion this year. Experts forecast this sector will expand to nearly $35.98 billion by 2035, maintaining a steady 10.07% annual growth rate. These figures highlight the massive capital currently flowing into modernizing legacy financial infrastructure.

Key Market Drivers:

- SaaS-based core systems are growing at over 20% annually as institutions ditch legacy hardware for cloud-native elasticity.

- Banking-as-a-Service adoption is set to quadruple by 2034, forcing enterprises to expose APIs at a global scale. Building resilient infrastructure is now essential to support these external financial integrations.

- Consumers now demand instant payments and seamless onboarding across all digital channels. Microservices allow you to scale individual components like fraud detection or KYC independently to meet these expectations.

What “Scalable Banking Backends” Really Means

A scalable banking backend serves as a resilient architecture designed for the growth of banking platforms, resulting in higher ROI. It moves beyond simple server upgrades to embrace a modular, flexible framework. In practice, this means:

- Independent Scaling: You can scale specific components like the core ledger or KYC services individually via microservices.

- Elastic Provisioning: Your system operates in cloud-native environments that adjust capacity based on real-time demand.

- Operational Reliability: High-performance rails prevent failed payments and slow onboarding during peak traffic.

For enterprises launching card-issuing platforms or Banking-as-a-Service (BaaS) models, the backend acts as your primary revenue engine.

However, poor scaling activities lead directly to reputational damage and lost market share. Consequently, investing in a flexible architecture is the only way to support complex, high-volume financial workflows.

Revenue Benefits Of Backend Scalability

Building a scalable banking backend actively protects your profit margins. These systems allow you to manage risk and costs more effectively as your customer base expands.

By modernizing your infrastructure, you ensure your business remains stable even during unexpected market shifts.

- Smart Spending on Technology: Cloud-based systems let you pay only for the computer power you actually use. This prevents you from wasting money on expensive servers that sit idle during slow hours.

- Preventing System Crashes: A modular setup spreads the workload across different areas. If one small part of the system has an issue, the rest of your banking services keep running smoothly.

- Easier Regulatory Compliance: Modern backends automatically track every transaction and change. This built-in record-keeping makes it much simpler to prove you are following financial laws as you grow.

For business leaders, scalability is about more than speed; it is about building a disciplined, reliable company. Investing in this technology creates a resilient foundation that satisfies both your board and your regulators.

Therefore, a flexible backend is a vital tool for long-term operational health.

What Does a Scalable Banking Backend Require?

Building a modern financial engine requires a shift from rigid hardware toward a flexible, software-driven architecture. This transition ensures that each part of the banking ecosystem can expand or contract based on real-world business needs.

1. Service independence through microservices

Traditional systems handle all tasks in one large block, which makes them difficult to change or grow. By breaking the backend into smaller, independent services, you can scale specific functions like “Payments” or “Account Management” without touching the rest of the system.

This modularity allows your technology to stay fast and efficient even as your user base grows into the millions.

2. Event-driven systems for speed

Modern banking happens in the blink of an eye, requiring a backend that reacts to data as it arrives. Event-driven systems use a messaging framework to notify different parts of the platform when a transaction occurs.

This setup eliminates the need for slow, scheduled updates, ensuring that balances and fraud alerts remain accurate in real-time.

3. API-first platform design

A scalable backend should act as a central hub that easily connects to other fintech tools and services. An API-first approach treats every internal function as a bridge that can be safely accessed by external partners.

This design choice is essential for businesses looking to launch Banking-as-a-Service (BaaS) models or integrated financial products.

4. Distributed data management

Relying on a single data center creates a massive risk for both performance and reliability. Modern backends distribute data across multiple geographic regions to ensure that users always connect to the nearest possible server.

This strategy reduces the time it takes to process a request and provides a vital safety net if one region experiences a technical failure.

5. Cloud-native elastic infrastructure

Cloud-native technology allows your system to behave like a living organism that grows when busy and shrinks when quiet. This elasticity is achieved through automated tools that manage your computing resources without manual intervention.

For an enterprise, this means maintaining high performance during peak shopping holidays while keeping costs low during off-peak hours.

6. Decoupled fault isolation

In a well-designed system, a problem in the loyalty points module should never prevent a customer from using their debit card. Decoupling ensures that different services are isolated from one another so that failures are contained.

This structure significantly improves the overall uptime of the platform and protects the core banking experience from minor technical glitches.

7. Complete system observability

Managing a complex, scalable backend requires clear visibility into every moving part. Observability tools allow your team to monitor the health of the system through three main pillars:

- Metrics: Tracking transaction speeds and resource usage to spot trends early.

- Logs: Maintaining a detailed record of events to help troubleshoot specific issues.

- Tracing: Following a single transaction as it moves through various services to find bottlenecks.

Integrating these core requirements transforms a standard banking tool into a high-performance platform capable of global scale. Prioritizing these architectural pillars ensures your business can handle the complexities of modern digital finance with absolute confidence.

How Is Real-Time Banking Infrastructure Actually Built?

Transitioning to real-time operations requires moving away from scheduled updates toward a system that processes data the moment it moves.

This shift ensures that every financial decision is based on the most current information available across the entire enterprise.

1. Event streaming over batch cycles

Older systems often collect transactions in large groups and process them once a day, creating a delay in visibility. Event streaming replaces this by treating every transaction as a continuous “event” that flows through the system instantly.

This allows your business to see live balances and updated ledgers without waiting for a nightly data dump.

2. Reliable message brokers

In a complex system, different services need a guaranteed way to talk to each other without losing data.

Message brokers act as secure couriers, ensuring that if one part of the system is temporarily busy, the transaction data is stored safely and delivered as soon as the millisecond capacity returns.

This infrastructure prevents missing payments and keeps the entire platform synchronized.

3. Flexible asynchronous communication

Real-time backends use asynchronous communication to keep things moving quickly. Instead of every service waiting for the others to finish a task, they send notifications and move on to the next request immediately.

This “non-blocking” approach is what allows a banking app to remain snappy and responsive even during peak usage hours.

4. Preventing duplicate transactions

One of the biggest risks in digital banking is a customer accidentally being charged twice due to a network glitch. Idempotency is a technical safeguard that ensures the system recognizes a repeated request and only processes it once.

Implementing this logic is essential for maintaining customer trust and accurate financial records.

5. Instant settlement and reconciliation

Traditional reconciliation, which means matching internal records with bank statements, can take days. In this situation, modern real-time models automate this process, matching and validating transactions as they happen.

This immediate oversight allows finance teams to spot discrepancies or cash flow issues in minutes rather than weeks.

6. Streaming fraud detection

Security must move as fast as the transactions it protects. Streaming data allows AI-driven fraud tools to analyze patterns, like unusual locations or spending speeds, while the transaction is still being authorized.

By catching suspicious activity in real-time, you can block fraudulent charges before the money even leaves the account.

7. Synchronized data consistency

When data is spread across different servers, keeping everything accurate is a major challenge. Distributed systems use specialized protocols to ensure that a balance shown on a mobile app matches the one in the core ledger.

Strong data consistency ensures that your enterprise operates on a single version of the truth at all times.

Building for real-time speed requires a fundamental rethink of how data moves between your banking services. By prioritizing streaming and immediate verification, you create a backend that is not only faster but also significantly more secure and transparent.

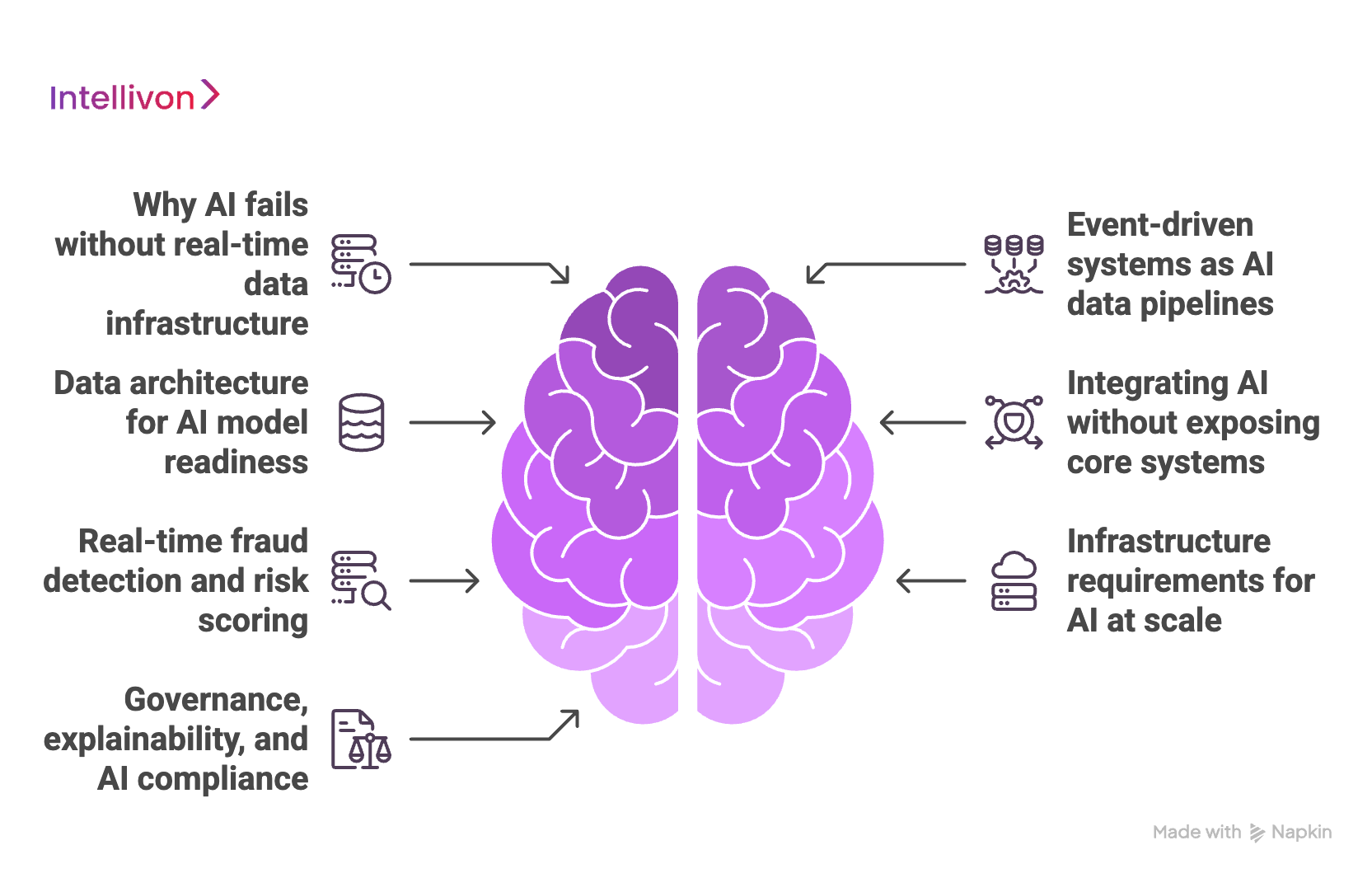

Determining the AI-Rediness of Your Banking Backend Infrastructure

Many enterprises discover that their AI ambitions are limited by the quality and speed of their underlying data.

A scalable banking backend acts as the essential nervous system that provides the live information these intelligent models need to function effectively.

1. Why AI fails without real-time data infrastructure

AI systems are only as smart as the data they consume. If your backend relies on batch processing, your AI is essentially making decisions based on old data, which leads to inaccurate risk assessments and missed opportunities.

- Live Data Dependency: Intelligent models require immediate access to current balances and recent behaviors to provide relevant insights.

- Legacy Core Limitations: Most traditional banking cores are not designed to export data quickly enough to fuel high-performance AI.

- Stalled Initiatives: Without a modern data flow, expensive AI projects often fail to move past the testing phase because they cannot perform in a live environment.

2. Event-driven systems as AI data pipelines

An event-driven architecture transforms your banking backend into a continuous stream of information. This allows your AI models to note every transaction and update their logic as events happen.

- Continuous Learning: By using streaming tools like Kafka, your models can learn from new data patterns without needing manual updates.

- Reactive Intelligence: This setup ensures that your AI can react to a market change or a customer action in milliseconds rather than hours.

- Streamlined Integration: Event pipelines simplify the process of connecting new AI features to your existing financial services.

3. Data architecture for AI model readiness

Preparing your backend for AI requires a clean and organized data layer that is easy for machines to read. Modern architectures separate the data used for day-to-day transactions from the data used for complex analysis.

This separation prevents heavy AI processing from slowing down the actual banking app. Furthermore, building dedicated “feature pipelines” helps the AI quickly identify the specific data points it needs to make a prediction.

4. Integrating AI without exposing core systems

Protecting the stability of your core banking logic is a top priority when adding new technology. By using an API layer, you can position your AI as an external intelligence layer that doesn’t interfere with the main transaction engine.

This “sidecar” approach allows you to experiment with AI tools while keeping your sensitive financial data secure and isolated.

5. Real-time fraud detection and risk scoring

One of the most immediate benefits of an AI-ready backend is the ability to stop fraud before it happens. AI models running on streaming data can spot unusual spending patterns or suspicious logins instantly.

- Immediate Detection: Automated systems can flag anomalies while a transaction is still in the “pending” state.

- Risk Reduction: Faster detection lowers the financial loss from fraud and ensures your enterprise stays compliant with safety regulations.

- Dynamic Scoring: AI can adjust a user’s risk score in real-time based on their most recent actions, providing better protection for the bank and the customer.

6. Infrastructure requirements for AI at scale

Running AI across millions of transactions requires significant computing power and high-speed data paths. Your backend must be capable of moving massive amounts of information without creating bottlenecks.

Low-latency systems ensure that the AI’s “thinking time” does not add any noticeable delay to the user’s experience.

Consequently, a scalable cloud infrastructure is necessary to provide the compute power needed for complex model execution on demand.

7. Governance, explainability, and AI compliance

Financial regulators require that every AI-driven decision, such as a loan denial, must be explainable and fair. Modern backends include “Explainable AI” (XAI) tools that provide an audit trail for every automated choice.

This transparency is vital for meeting legal requirements and maintaining public trust. Additionally, keeping a “human-in-the-loop” allows your expert staff to review and override AI decisions when necessary, ensuring a balance between automation and human judgment.

Preparing your banking backend for AI readiness requires building a data-rich environment where intelligence can thrive. This foundation ensures your enterprise can scale its AI capabilities safely while meeting the strict demands of the financial industry.

How Do Banks Build Security Into the Backend?

In the modern financial landscape, security is no longer a perimeter wall but a core feature woven into every line of code. A scalable banking backend must protect sensitive data at every touchpoint without compromising the speed of the transaction.

1. Zero trust across all services

The traditional “castle-and-moat” security model is no longer sufficient for complex, cloud-based systems. Zero-trust architecture operates on the principle of “never trust, always verify,” meaning every service must prove its identity before it can talk to another.

This approach ensures that even if one part of the system is compromised, the attacker cannot move freely to other areas of the bank.

2. Strict identity and access controls

Managing who can see and move data is a fundamental pillar of banking security. Identity and Access Management (IAM) tools ensure that both human employees and automated services have the minimum level of access required to do their jobs.

By enforcing these strict controls, enterprises can significantly reduce the risk of internal data leaks or unauthorized system changes.

3. End-to-end data encryption

Protecting information as it travels between users, apps, and databases is essential for maintaining privacy. End-to-end encryption ensures that financial data is scrambled at the source and only unscrambled when it reaches its intended destination.

This safeguard makes intercepted data useless to hackers, protecting everything from account balances to personal identification numbers.

4. API security and gateways

APIs are the primary entry points for modern banking services, making them a top target for cyberattacks. A secure API gateway acts as a digital bouncer, checking every incoming request for valid credentials and signs of malicious intent.

This layer also prevents “brute force” attacks by limiting how many requests a single user or bot can make in a short period.

5. Threat and anomaly monitoring

Waiting for a security breach to happen is a high-risk strategy; instead, banks use automated tools to spot trouble early. Anomaly monitoring systems use patterns to identify unusual behavior, such as a sudden surge in login attempts from a foreign country.

By detecting these threats in real-time, the system can automatically trigger security protocols to block suspicious activity before any damage is done.

6. Secure management of keys and secrets

Every secure system relies on digital keys and passwords (secrets) to unlock encrypted data. Rather than storing these in the code itself, banks use specialized “vault” systems to manage and rotate these credentials automatically.

This practice ensures that even if a developer’s computer is compromised, the master keys to the banking backend remain safely locked away.

7. Continuous security validation

Security is not a one-time setup but a continuous process of testing and improvement. Automated validation pipelines scan new code for vulnerabilities every time a change is made to the system.

This “shift-left” approach catches security flaws during the building phase, ensuring that every update to the platform meets the highest standards of safety before it ever reaches a customer.

Integrating these security layers ensures that your banking infrastructure is resilient against both current and emerging threats.

Prioritizing a secure-by-design approach allows your enterprise to build deep trust with customers while satisfying the strict requirements of global financial regulators.

How Do Banks Handle Cross-Border Data Compliance?

Expanding a banking platform globally introduces a complex web of laws regarding where data is stored and how it is moved.

Navigating these requirements requires a sophisticated architecture that balances local legal mandates with the need for a unified global business operation.

1. Data residency laws across multiple jurisdictions

Governments worldwide are increasingly protective of their citizens’ financial information, creating strict “data residency” rules. Regulations like the GDPR in Europe require that sensitive data must remain within national borders.

Relying on a single global database is now a significant risk; a breach or a legal dispute in one country could lead to massive fines or even the total suspension of your operating license.

2. Region-specific data storage architecture

To comply with these laws, enterprises use geo-fencing at the infrastructure level to ensure that data stays exactly where it belongs.

- In-Region Storage: European customer data is pinned to servers in Frankfurt or Dublin.

- Cloud Mapping: Modern cloud providers offer specific regions that align with these jurisdictions, making it easier to host your backend in the correct physical location.

- Automated Routing: The system automatically identifies a user’s location and directs their data to the legally compliant storage bucket without any manual input.

3. Multi-region cloud and hybrid deployments

A robust cross-border strategy often involves a mix of public cloud and private infrastructure. Many enterprises use a multi-region strategy on AWS or Azure to maintain high availability while respecting local laws.

In some cases, highly sensitive financial ledgers may be kept on private, on-premise servers (a hybrid setup) to satisfy regulators who are not yet comfortable with 100% public cloud reliance for core banking functions.

4. Data sovereignty without duplicating systems

The challenge is to follow local laws without having to build and manage a completely different software system for every country.

- Logical Separation: Instead of physical duplication, banks use a “shared services” model where the core logic is global, but the data layers are strictly localized.

- Unified Management: This prevents system fragmentation, allowing your team to push updates to the whole platform at once while the data remains safely separated.

- Efficiency: This approach keeps operational costs low by sharing the most expensive parts of the infrastructure across all regions.

5. Cross-border transaction data flow control

When money moves between countries, some information must travel with it, but other data must stay behind. Enterprises use tokenization and data masking to protect a customer’s identity during an international transfer.

This ensures that while the transaction is settled according to global banking standards, the person’s full private profile is never exposed to a jurisdiction where it does not belong.

6. Auditability across jurisdictions

Regulators in different countries have different requirements for what an audit trail should look like. A scalable backend must maintain separate, localized logs that are “regulator-ready” for each specific market.

This ensures that if an official in the US or the EU requests a report, the system can generate a document that meets their specific legal format without exposing data from other regions.

7. Designing for regulatory change across regions

Laws can change overnight, and your backend must be modular enough to adapt without a total system rebuild. By using “compliance layers,” you can update the rules for one specific region, such as a new reporting requirement in Brazil, without affecting your operations in the rest of the world.

This flexibility allows your enterprise to enter new markets faster and stay ahead of evolving global standards.

Managing cross-border data is a high-stakes balancing act between global efficiency and local legality. Implementing a geo-aware architecture ensures your enterprise can grow into new territories with the confidence that your data practices are both safe and fully compliant.

Should You Build, Buy, or Partner for Backend Infrastructure?

Choosing how to source your banking infrastructure is a high-stakes decision that dictates your enterprise’s agility for the next decade.

Leaders must weigh the immediate need for market entry against the long-term necessity of owning a flexible, high-performance asset.

1. Cost and complexity of in-house development

Building a banking backend from scratch offers total control, but the true cost often exceeds initial budgets. The reasoning lies in the specialized talent required, which is that you are not just hiring web developers, but experts in distributed systems, cryptography, and financial regulations.

- The Talent Gap: Finding and retaining senior engineers who understand both high-scale cloud architecture and complex banking laws is difficult and expensive.

- Hidden Timelines: Building from zero often takes years, meaning your competitors may launch and capture the market while your team is still testing basic ledger functions.

- Infrastructure Overhead: You are responsible for every server, security patch, and maintenance task, which can distract your team from building features that actually make you money.

2. Tradeoffs of buying banking platforms

Buying a prebuilt “bank-in-a-box” solution seems like the fastest way to launch, yet it often creates a “ceiling” for growth. These platforms are designed for the average user, meaning they lack the specialized features needed for a unique enterprise value proposition.

- The “Black Box” Problem: Since you do not own the source code, you cannot easily modify the system to handle unique transaction types or integrate specific AI models.

- Shared Performance: Many SaaS platforms host multiple clients on the same infrastructure, meaning another company’s traffic spike could potentially slow down your services.

- Feature Lag: You are at the mercy of the vendor’s roadmap; if you need a new payment integration, you must wait for them to decide it is a priority for their entire customer base.

3. Vendor lock-in and long-term risk

When you buy a closed-source platform, you are essentially outsourcing your company’s destiny to a third party. If the vendor raises their prices or suffers from technical instability, your entire business is at risk.

- Strategic Dependency: Your most important asset(your financial ledger) is controlled by an entity whose priorities may not always align with yours.

- High Exit Barriers: Moving data and workflows out of a proprietary system is notoriously difficult, often requiring a total system rebuild to escape.

- Product Sunset Risk: If the vendor decides to discontinue the product or gets acquired, you may be forced into an emergency migration that halts your business growth.

4. Customization limits in prebuilt systems

Standardized platforms often force your business processes to fit their software, rather than the other way around. This prevents you from building the “secret sauce” that sets an enterprise leader apart.

- Rigid Frameworks: Most prebuilt systems use templates that are hard to change, making it difficult to launch truly innovative or “first-of-its-kind” financial products.

- Integration Friction: Connecting your existing CRM or specialized fraud tools to a closed vendor system often requires clunky, fragile workarounds.

- Generic User Experience: Because the backend logic is standard, it is hard to create a customer experience that feels truly distinct from your competitors.

5. Benefits of specialized development partners

Engaging a specialized development partner offers a “middle path” that combines the speed of buying with the control of building. A partner brings battle-tested blueprints and senior expertise, allowing you to avoid the common architectural traps of in-house builds.

- Accelerated Launch: Partners use proven frameworks to jumpstart the build, saving months of time while still delivering a custom solution.

- Expert Guidance: You benefit from a team that has already solved scaling and security challenges for other global enterprises.

- Focus on Strategy: While the partner handles the heavy technical lifting, your leadership team can stay focused on customer acquisition and business growth.

6. Ownership of architecture and codebase

The primary reason to work with a development partner is the eventual ownership of the intellectual property.

Unlike a subscription-based vendor, a partner builds a system that you own, giving you the freedom to modify or scale it without asking for permission.

- Capital Asset: An owned codebase is an asset on your balance sheet that increases the valuation of your company.

- Strategic Independence: You have the right to host the system anywhere and change the code whenever you want, ensuring you are never trapped by a vendor.

- Knowledge Transfer: A good partner trains your internal team as they build, ensuring you have the skills to maintain the platform long after the initial project is finished.

7. Aligning backend strategy with business goals

Your technology choice must reflect your ultimate business objective, which is either to be a market leader or just a market participant. A development partner helps align the technical architecture with your specific revenue goals.

- Bespoke Scalability: The system is built specifically for your expected transaction volumes and geographic footprint.

- AI and Innovation Ready: A custom build ensures your data layers are structured specifically to fuel the AI tools your business needs to stay competitive.

- Long-Term ROI: While the upfront cost is higher than a subscription, the lack of per-transaction fees and the value of owning your tech lead to much higher returns over time.

Strategic Comparison: Build vs. Buy vs. Partner

| Feature | In-House Build | Prebuilt Vendor (SaaS) | Development Partner |

| Speed to Market | Very Slow | Fastest | Moderate/Fast |

| Total Control | Maximum | Minimum | High |

| Upfront Cost | Very High | Low/Moderate | Moderate |

| IP Ownership | Fully Owned | None (Licensed) | Fully Owned |

| Scalability | Variable | Capped by Vendor | Enterprise-Grade |

| Maintenance | Internal Team | Vendor Managed | Collaborative/Transferable |

While building alone is daunting and buying limits your potential, partnering with experts provides the optimal balance of speed, cost, and customization. This collaborative approach ensures your banking backend is a bespoke, owned asset that fuels your growth rather than restricting it.

Can You Modernize Systems Without Replacing Everything?

Enterprises often fear that upgrading their technology requires a huge replacement that risks total system failure.

However, a strategic approach allows you to introduce high-performance, scalable components while keeping your existing core operations running safely and your existing data protected.

1. Sidecar architecture for gradual transition

A sidecar architecture allows you to attach new, modern features to your legacy system without actually modifying the old code.

This creates a bridge between the past and the future, allowing you to test new logic in a real-world environment.

- Non-Invasive Growth: You can add AI tools or real-time payment modules alongside your legacy core.

- Isolated Testing: Errors in the new sidecar service do not crash the primary banking functions.

- Strategic Offloading: Gradually move heavy processing tasks away from the old system to the more efficient sidecar.

2. Running legacy and modern systems together

Maintaining two systems simultaneously(often called a “strangler pattern”) allows you to slowly shift traffic from the old infrastructure to the new one. This ensures that the transition is invisible to the customer while providing a safety net for the business.

- Dual Routing: Transactions are sent to both systems to verify that the new backend produces the exact same results as the old one.

- Zero Downtime: You never have to “turn off” the bank; you simply dial up the volume on the modern system as your confidence grows.

- Risk Mitigation: If the new system hits a snag, you can instantly revert traffic back to the legacy core.

3. Reducing risk in backend modernization

The greatest risk in financial technology is a loss of data integrity or system availability during an update. By breaking the modernization into small, manageable pieces, you ensure that no single mistake can derail the entire project.

- Continuous Validation: Every new component is subjected to rigorous automated testing before it touches live data.

- Rollback Capabilities: Modern deployment tools allow you to undo any change in seconds if performance metrics drop.

- Data Synchronization: Real-time data bridges ensure that both old and new databases remain perfectly in sync during the transition.

4. Migrating services in controlled phases

A phased migration treats the modernization as a series of small wins rather than one massive gamble. This reasoning allows the team to learn from each phase and apply those lessons to more complex services later.

- Prioritizing Low-Risk Tasks: Start by migrating non-essential services, such as loyalty points or reporting, before touching the core ledger.

- Revenue Protection: By keeping the payment gateway on the stable legacy system until the very end, you protect your primary cash flow.

- Team Scaling: A phased approach allows your internal team to slowly get used to the new technology without being overwhelmed.

5. Avoiding disruption to live operations

For a global enterprise, there is no such thing as a “maintenance window” that fits every time zone. Your modernization must happen while millions of people are actively using their accounts.

- Blue-Green Deployments: Run two identical environments and switch users between them only when the new one is fully verified.

- Canary Releases: Roll out new features to only 1% of users first to catch edge-case bugs before a full-scale launch.

- Traffic Shaping: Use intelligent load balancers to slowly migrate user groups based on their risk profile or geographic location.

6. Lessons from tier-1 banking transformations

The world’s largest banks have proven that a modular approach is the only way to modernize without causing a national financial crisis. These transformations show that success depends on architectural flexibility rather than brute-force replacement.

A. JPMorgan Chase (USA)

The firm invests over $15 billion annually in technology to move away from rigid legacy structures. By building “Fusion,” a cloud-native data platform, and utilizing reusable APIs, they have achieved a 99.9% success rate for system changes even as their volume of updates increased by 60%.

B. Lloyds Banking Group (UK)

As one of the UK’s oldest institutions, Lloyds transitioned from a brick-and-mortar traditional model to a digital-first organization. They established a dedicated GenAI office and a cloud-native foundation that allows them to scale new services independently of their massive core ledger.

C. Royal Bank of Canada (Canada)

RBC utilizes AI-driven “blueprint” tools to map out dependencies within its decades-old core applications. This allows their developers to refactor specific parts of the system safely, reducing the “idea-to-code” cycle and ensuring that 19 million clients experience zero disruption during backend upgrades.

D. Goldman Sachs (USA)

When launching “Marcus,” Goldman Sachs didn’t try to force consumer banking into their existing investment banking core. Instead, they built a completely new, cloud-native platform on AWS that operates as a high-speed, independent engine, allowing them to manage billions in deposits with 24/7 availability.

Modernizing your banking backend is a journey of evolution, not a single event of destruction. By adopting a modular strategy, you can secure the benefits of a scalable, AI-ready system while maintaining the absolute stability your enterprise requires.

Intellivon provides the architectural foresight and strategic execution needed to navigate these complex transitions, ensuring your legacy systems evolve into future-ready assets.

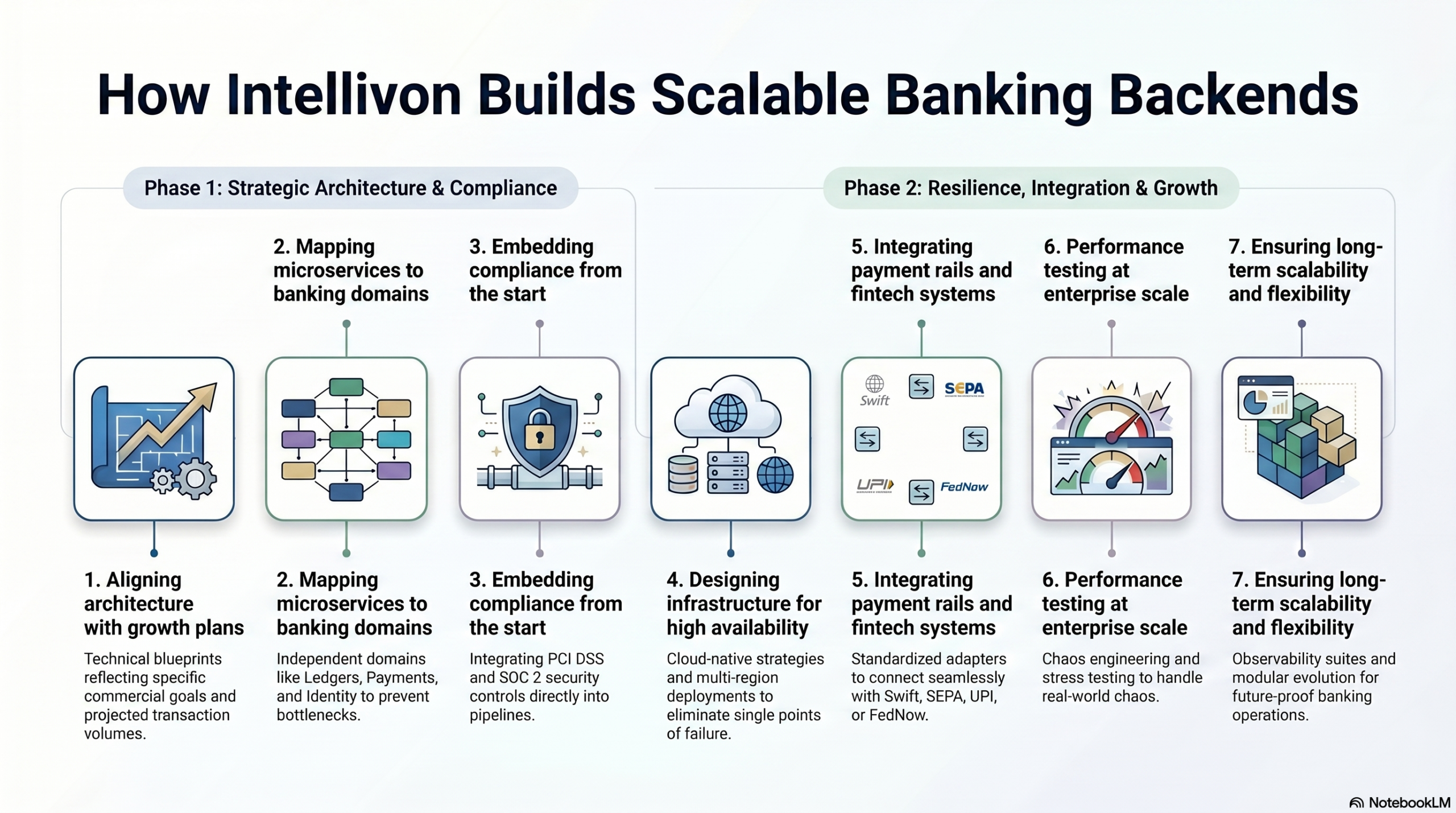

How Intellivon Builds Scalable Banking Backends

Building a banking backend requires a delicate balance between extreme technical precision and long-term business strategy.

Our approach moves beyond simple coding; we construct a resilient financial engine designed to handle the rigorous demands of global enterprise operations while remaining flexible enough to pivot with the market.

1. Aligning architecture with growth plans

We begin by ensuring the technical blueprint reflects your specific commercial goals, whether that is launching a neobank or expanding into embedded finance.

- Strategic Mapping: We evaluate your projected transaction volumes and geographic expansion targets to determine the necessary level of server redundancy and data residency.

- Technology Selection: Our teams select a stack (often utilizing Go or Java Spring Boot) that offers the best performance-to-cost ratio for your specific use case.

- Future-Proofing: We design the system with modular “plug-and-play” capabilities, ensuring you can add new currencies or payment methods without a total rebuild.

2. Mapping microservices to banking domains

We break down the complex world of banking into manageable, independent “domains” such as Ledgers, Payments, and Identity.

- Domain-Driven Design (DDD): Each service is isolated, meaning a high volume of traffic in the “Rewards” module will never slow down the “Core Transaction” engine.

- Communication Protocols: We use gRPC for ultra-fast internal communication and REST/GraphQL for external integrations, ensuring the system remains snappy.

- Data Sovereignty: Each microservice manages its own database, preventing the “giant database” bottleneck that plagues older banking systems.

3. Embedding compliance from the start

Compliance is treated as a core architectural feature rather than a checkbox at the end of the project.

- Automated Guardrails: We integrate PCI DSS and SOC 2 security controls directly into the deployment pipelines, so every update is automatically checked for safety.

- KYC/AML Integration: Our backends connect seamlessly to global identity providers through secure API layers, enabling real-time risk scoring and onboarding.

- Audit Transparency: We implement immutable logging using tools like Elasticsearch, providing a permanent and unchangeable record of every financial movement for regulators.

4. Designing infrastructure for high availability

We build systems that are “always on,” utilizing cloud-native strategies to eliminate any single point of failure.

- Multi-Region Active-Active: Your backend is deployed across multiple AWS or Azure regions simultaneously; if one goes down, the others take over in milliseconds.

- Kubernetes Orchestration: We use Kubernetes to manage your server containers, allowing the system to automatically “heal” itself if a service crashes.

- Global Load Balancing: Traffic is intelligently routed to the nearest healthy server, reducing latency for your global customer base.

5. Integrating payment rails and fintech systems

A banking backend is only as useful as its connections to the wider financial world.

- Universal API Layer: We build a standardized “adapter” layer that allows you to connect to Swift, SEPA, UPI, or FedNow without changing your core logic.

- Webhooks and Event Streams: Using Apache Kafka, we ensure that when a payment is received, every relevant system—from notifications to accounting—is updated instantly.

- Third-Party Orchestration: We manage the complex “handshakes” between your backend and external fintech tools like Plaid or Stripe, ensuring data flows securely and reliably.

6. Performance testing at enterprise scale

Before a single customer logs in, we push the system to its breaking point to ensure it can handle real-world chaos.

- Chaos Engineering: We intentionally trigger server failures and network delays in a controlled environment to prove the system can recover without losing data.

- Load and Stress Testing: Using tools like JMeter, we simulate millions of concurrent users to identify and fix bottlenecks before they affect your business.

- Latency Optimization: We fine-tune database queries and caching layers to ensure that even during peak traffic, response times remain under 200 milliseconds.

7. Ensuring long-term scalability and flexibility

Our partnership doesn’t end at launch; we build the system so your internal team can manage and grow it for years to come.

- Comprehensive Documentation: We provide clear, strategic architectural maps and “clean code” that is easy for future developers to understand and maintain.

- Observability Suites: We install advanced monitoring tools like Prometheus and Grafana, giving your leadership team a “cockpit view” of system health and transaction trends.

- Modular Evolution: Because the system is decoupled, you can upgrade your AI models or switch cloud providers in the future without disrupting your live banking operations.

At Intellivon, we engineer the high-performance foundations that allow your enterprise to lead the financial industry. Our experience-driven approach ensures your banking backend is not just a technical requirement, but a strategic asset that powers your long-term growth and innovation.

Conclusion

Building a scalable banking backend is the definitive pivot from managing technical debt to driving market expansion. By prioritizing modularity, real-time data flows, and automated compliance, enterprises secure a resilient foundation for innovation.

This strategic investment ensures your infrastructure remains a high-performance engine capable of supporting tomorrow’s global financial demands.

Build A Scalable And Compliant Backend For Your Platform With Intellivon

Building an enterprise banking system requires creating a platform that can operate within strict regulatory expectations, satisfy bank partners, support audits, and scale without exposing the business to avoidable compliance risk.

At Intellivon, we build enterprise banking platforms with compliance embedded into the architecture from the start. Our approach focuses on turning regulatory complexity into clear system design, so your platform is easier to launch, easier to defend, and easier to scale.

A. Embedding Compliance Into Core Platform Architecture

Compliance becomes expensive when it is added on after the system is built. That’s why we design banking systems where auditability, access control, monitoring, and recordkeeping are built into the platform foundation from day one.

- Audit Readiness: Audit trails are designed for reviews, investigations, and control validation.

- Granular Security: Role-based access controls with approval and segregation logic are baked into the core.

- Deep Visibility: Event logging covers every action across onboarding, payments, and account activity.

- Strategic Data Design: Data structures support long-term retention, reporting, and traceability. This proactive design helps you avoid costly rework later and creates a stronger base for growth.

B. Building AML, KYC, and Monitoring Workflows Into Operations

Banking compliance depends on how operational workflows actually function. We build systems that support identity checks, business verification, screening, transaction monitoring, and review workflows in a way that fits real enterprise operations.

- Verified Onboarding: KYC and KYB workflows are aligned strictly with onboarding requirements.

- Proactive Screening: Seamless sanctions, PEP, and watchlist screening integrations protect your rails.

- Automated Vigilance: Transaction monitoring logic includes built-in alerts and case flows.

- Operational Oversight: Review queues and escalation paths are designed for compliance teams. This allows your team to manage compliance through the product, not outside of it.

C. Preparing Platforms for Bank and Enterprise Due Diligence

Strong compliance posture matters long before regulators get involved. Enterprise buyers, sponsor banks, and financial partners all want proof that the platform has been designed with control maturity in mind. We help build systems that stand up to that scrutiny.

- Control Maturity: Architecture is aligned with the security and control expectations of tier-1 institutions.

- Due Diligence Support: Our designs support vendor reviews and deep-dive due diligence discussions.

- Evidence-Based Accountability: We provide clear evidence trails for approvals, changes, and incidents.

- Partner Credibility: Platform logic is built for accountability across teams and partners. This makes your platform more credible in high-stakes sales and partnership conversations.

D. Supporting Privacy, Security, and Resilience by Design

Modern banking platforms must do more than process transactions. They must protect data, handle incidents properly, and operate reliably under pressure. We design systems that support privacy requirements, security controls, and resilience planning without fragmenting the experience.

- Layered Protection: Encryption, access control, and data protection layers are standard.

- Policy Alignment: Retention and deletion logic are aligned with specific global policy needs.

- Response Readiness: Incident response support and evidence preservation are integrated features.

- Operational Resilience: We plan for recovery, failover, and operational resilience at scale. This helps you build a banking platform that is dependable in both day-to-day operations and high-risk situations.

E. Scaling Compliance Across Products, Partners, and Regions

Compliance complexity grows quickly as platforms expand. Whether you are adding new workflows, entering new markets, or working with more partners, the platform needs a structure that can support change without breaking control integrity.

- Modular Growth: Modular compliance logic supports rapid product and feature expansion.

- Shared Frameworks: We implement shared control frameworks across all teams and workflows.

- Global Readiness: The architecture is designed to support cross-border regulatory requirements.

- Oversight at Scale: Your infrastructure scales without weakening critical oversight. This gives you a more practical path to scale while maintaining total control.

Enterprise banking platforms succeed when compliance is treated as part of the system, not a layer added later. Intellivon helps organizations build banking infrastructure that supports regulatory readiness, operational clarity, and long-term growth.

Planning a compliance-ready banking platform? Connect with Intellivon today to discuss your requirements and get a tailored project estimate.

FAQs

Q1. How do banks handle sudden 10x transaction spikes without going down?

A1. Cloud infrastructure with auto-scaling detects traffic surges and immediately spins up additional compute capacity. Because the architecture separates services independently, only the strained component scales.

And as a result, everything else continues normally. Meanwhile, load balancers distribute incoming requests across the expanded capacity in real time. The system flexes without friction. Users feel nothing.

Q2. Should we build a custom banking backend or use a platform like Mambu or Thought Machine?

A2. Tier-1 banks typically run both. They adopt modern platforms for specific products while keeping existing infrastructure operational elsewhere. In practice, custom builds deliver full architectural control, whereas platforms accelerate time to market.

Ultimately, the deciding factor is always the same: how differentiated does your product need to be, and how much vendor dependency can your risk appetite absorb?

Q3. If we modernize our core banking infrastructure, how do we make sure we’re still PCI DSS, SOC 2, and AML compliant the whole way through?

A3. Start by embedding compliance into the architecture before development begins rather than auditing it afterwards. In practice, every data flow, access control, and audit log gets designed against its corresponding regulatory requirement from day one.

Beyond that, a parallel compliance environment runs alongside the build throughout, so nothing reaches production without first clearing the same checks regulators will apply.

Q4. How does backend architecture handle cross-border transactions without becoming a legal liability?

Through jurisdiction-aware data routing built directly into the infrastructure layer. In practice, the backend identifies where data originated and automatically applies the corresponding residency rules, keeping each country’s data within its designated regional environment.

Critically, this works cleanly only when designed in from the start. Enterprises that instead try to retrofit it onto existing systems consistently create the legal exposure they were originally trying to avoid.

Q5. How do you build a banking system where one component failure doesn’t cascade into a total outage?

A5. By isolating failure at the service boundary before it spreads. Each microservice runs independently with its own data store, so a failure in one does not automatically affect another.

As a result, circuit breakers detect the problem and cut propagation immediately. Furthermore, fallback logic keeps critical paths running even when a dependent service goes down. One failure stays contained, and the rest of the system carries on.