Key Takeaways:

-

Building an AI fintech platform ranges from $50,000 for a specialized MVP to $200,000 for a full enterprise solution.

-

Platform type drives cost significantly, from $20,000 for wallet and payment apps to $300,000 for neo-banking infrastructure.

-

Hidden costs, including model retraining, are where most budgets exceed projections, adding 15 to 20 percent annually on top of the initial build.

-

AI-native builds outperform retrofitted systems at scale, but a phased hybrid approach allows established institutions to modernize critical modules.

-

How Intellivon builds AI fintech platforms that your enterprise fully owns and cost structures are mapped to your specific use case and growth stage.

What if the biggest risk in building an AI fintech platform is not the budget but creating the wrong product at the right time? Fintech leaders are no longer wondering whether to use AI. They are focused on how to implement it in a way that meets regulations, works across markets, and doesn’t need a complete overhaul in eighteen months.

The cost to build an AI fintech platform usually ranges from $50,000 to $150,000. This depends on your use case’s complexity, compliance needs, and the design choices made early on. At Intellivon, we have observed how those early choices can either reduce costs or quietly increase them.

The financial platforms built five years ago focused on manual workflows, single-market rules, and human-reviewed decisions. That approach cannot handle real-time credit scoring, automated KYC, or cross-border fraud detection at the speed the market requires today.

The builders are designing systems that increase in value as data grows and regulations change. This blog covers what it costs to build an AI fintech platform and will also cover how we built this platform from scratch.

Why Is AI Fintech Costing More Than Expected?

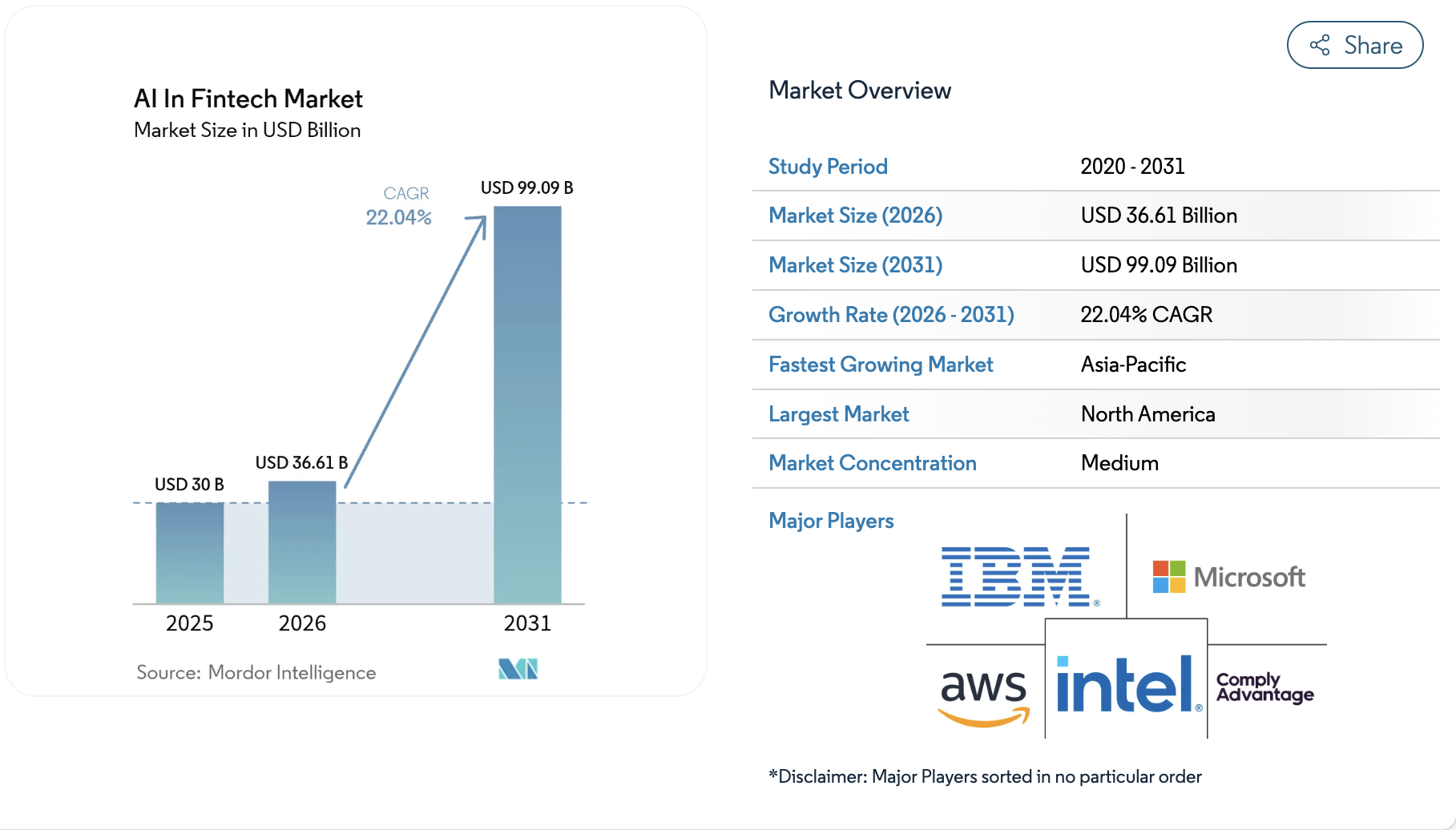

Building advanced financial systems is a high-stakes investment. Most leaders expect efficiency, yet many face stinging budget overruns. Data indicates the sector will hit $99 billion by 2031. However, 85% of these projects exceed their original financial blueprints.

1. Talent Shortages Driving Premium Costs

Finding the right people is the biggest hurdle in 2026. General AI developers are common, but fintech requires a rare hybrid skill set. You need experts who understand both machine learning and complex banking regulations. This scarcity creates a massive talent gap in the BFSI sector.

Consequently, salaries for specialized engineers have reached record highs. A single bad hire can cost three times their annual salary in lost time. Many firms face months of delays simply waiting for the right architect. Therefore, talent acquisition remains a primary driver of rising development budgets.

2. Data Readiness and Infrastructure Overheads

Data is the fuel for any risk scoring system. Unfortunately, most enterprise data is messy and fragmented. Leaders often underestimate the cost of cleaning and standardizing these datasets. Poor data quality costs companies millions annually through rework and model errors.

In addition, hardware costs are highly volatile. GPU availability fluctuates, causing sudden spikes in infrastructure bills. Multi-agent systems can generate massive monthly cloud expenses without warning. Managing these variable compute costs requires strict architectural oversight from the start.

3. Regulatory Compliance and Security Burdens

Finance is a heavily regulated industry. You cannot simply deploy a “black box” model and hope for the best. Regulators demand explainability, which requires expensive diagnostic tools. Bias audits and governance frameworks add significant layers to your initial budget.

Security also demands a massive financial commitment. Protecting fraud-prone systems involves advanced encryption and constant real-time monitoring. These aren’t optional extras; they are fundamental requirements for credit scoring. Fragmented global regulations further complicate the scaling process for international platforms.

4. Implementation and Scaling Surprises

Custom builds offer more power than basic APIs. However, they also come with a much higher price tag. Developing unique fraud detection features can easily cost over $500,000. Many projects fail because leaders overlook the cost of ongoing maintenance and MLOps.

Success requires looking beyond the initial launch. Scaling an AI platform involves constant process redesign and governance updates. While the upfront spend is high, long-term ROI only appears after the system stabilizes. Smart investors prioritize phased rollouts to manage these financial pressures effectively.

Building a world-class risk system requires balancing innovation with fiscal discipline.

Real Cost to Build An AI Fintech Platform in 2026?

Investing in an AI fintech platform requires a clear understanding of capital allocation. In 2026, the market has moved beyond experimental prototypes toward high-performance systems that require strategic funding. While costs fluctuate based on complexity, most successful deployments fall within a predictable range.

| Development Stage | Estimated Cost | Typical Timeline | Core Deliverable |

| Specialized MVP | $50,000 – $80,000 | 3 – 4 Months | Core AI Logic & UI |

| Mid-Scale Platform | $80,000 – $140,000 | 5 – 7 Months | API Suite & Analytics |

| Enterprise Solution | $140,000 – $200,000 | 8 – 12 Months | Full Compliance & AI Agents |

In addition, your choice of development partner significantly impacts these figures. A team with deep domain expertise can navigate regulatory hurdles faster, saving months of potential delays. Understanding these milestones helps you plan your capital infusions with confidence and precision.

Successfully launching an AI fintech platform depends on matching your budget to your strategic goals. Intellivon provides the elite engineering and strategic oversight needed to transform $50,000 – $200,000 investments into industry-leading financial assets. Contact us to architect your next breakthrough.

What Is the Step-by-Step AI Fintech Build Process?

Executing a fintech project requires a disciplined, phase-based approach to ensure capital efficiency. Moving from a concept to a live environment involves specific technical milestones that dictate your total expenditure.

By following a structured roadmap, you can mitigate risks and avoid the common financial pitfalls of unorganized development.

| Development Phase | Cost Range | Key Activity | Strategic Why |

| 1. Strategy & Planning | $3,000 – $8,000 | MVP Scoping & Feasibility | Prevents feature creep and wasted R&D. |

| 2. UX & User Flows | $5,000 – $12,000 | Wireframing & AI Interaction | Reduces churn and high rebuild costs. |

| 3. Core Architecture | $10,000 – $30,000 | Microservices & Payment Rails | Ensures the platform scales with volume. |

| 4. AI Integration | $8,000 – $25,000 | Model Training & Selection | Drives the actual ROI and risk accuracy. |

| 5. Compliance & Security | $7,000 – $20,000 | KYC/AML & Audit Trails | Protects the business from legal failure. |

| 6. QA & Validation | $4,000 – $10,000 | Stress Testing & Bias Audits | Prevents catastrophic post-launch errors. |

| 7. Cloud Deployment | $3,000 – $10,000 | Infrastructure & Monitoring | Guarantees system uptime and speed. |

| 8. Maintenance | $2,000 – $8,000* | Retraining & Optimization | Stops AI model degradation over time |

Step 1: Product Strategy and Cost Planning

Every successful platform begins with a rigorous strategic blueprint. You must define your core business model and identify the specific AI use cases that will drive revenue.

- What happens: This phase includes deep market research, competitor benchmarking, and MVP scoping. Teams assess AI feasibility and data availability to ensure the project is technically sound.

- Cost Range: $3,000 – $8,000.

- Why it matters: This stage is vital because it prevents overspending on unnecessary features that users may not actually need.

Step 2: UX Design and User Flow Mapping

Design in fintech rests in building trust. You must map out exactly how users will interact with financial workflows and AI-driven insights.

- What happens: Designers create wireframes, user journeys, and UI for dashboards. Specialized focus is placed on AI interaction design, such as how recommendations are presented to the user.

- Cost Range: $5,000 – $12,000.

- Why it matters: Poorly designed interfaces lead to high user drop-off rates and expensive rebuilds after the launch.

Step 3: Backend and Core Architecture Setup

The backend serves as the engine of your entire financial operation. This phase involves building the microservices and API architecture that handle transactions and logic.

- What happens: Engineers set up the API architecture, microservices, and database design. They also integrate payment rails and essential third-party financial services.

- Cost Range: $10,000 – $30,000.

- Why it matters: Most scalability issues originate here; a robust core is non-negotiable for future growth.

Step 4: AI Model Development and Integration

Integrating AI into your workflows is where the platform gains its competitive edge. You must select the right models for fraud detection, credit assessment, or personalized recommendations.

- What happens: This involves model selection and training using behavioral and financial data. Once trained, the AI is integrated into real-time decision-making systems.

- Cost Range: $8,000 – $25,000.

- Why it matters: AI quality directly impacts your ROI and determines the overall risk profile of your lending or fraud systems.

Step 5: Compliance, Security, and Data Governance

Operating in the financial sector requires strict adherence to global regulatory standards. You must integrate automated workflows to verify user identities instantly.

- What happens: Developers implement KYC/AML workflows, data encryption, and access controls. They also build the audit trails and explainability layers required by regulators.

- Cost Range: $7,000 – $20,000.

- Why it matters: Compliance failures can become existential risks and lead to heavy legal penalties.

Step 6: Testing, QA, and Risk Validation

You cannot launch a fintech product without exhaustive validation. This phase involves rigorous testing to ensure payment flows work perfectly every time.

- What happens: Specialists conduct functional and regression testing. They also perform accuracy and bias testing on AI models to ensure fair decision-making.

- Cost Range: $4,000 – $10,000.

- Why it matters: Thorough validation prevents costly post-launch failures and system crashes while live users are active.

Step 7: Deployment and Cloud Infrastructure Setup

Launching into a live production environment requires a secure and scalable cloud setup. Whether you use AWS, GCP, or Azure, you need pipelines to manage code updates without downtime.

- What happens: Teams manage cloud deployment and set up CI/CD pipelines. They also implement load balancing and failover systems to ensure 100% uptime.

- Cost Range: $3,000 – $10,000.

- Why it matters: Poor deployment setups increase downtime costs and degrade user trust during peak usage.

Step 8: Post-Launch Maintenance and AI Optimization

A fintech platform requires constant refinement to stay relevant. You must continuously retrain your AI models as market conditions and user behaviors change.

- What happens: This involves model retraining, performance tuning, and compliance updates. Teams also expand features based on real-world user behavior.

- Monthly Cost: $2,000 – $8,000.

- Why it matters: AI systems naturally degrade without continuous updates and optimization.

Total Estimated Cost Across All Steps

- MVP Build: $25,000 – $60,000

- Mid-Scale Platform: $60,000 – $120,000

- Advanced AI Fintech Platform: $120,000+

These ranges align with real-world app benchmarks and cost drivers like AI complexity, integrations, and compliance scope.

What Drives AI Fintech Development Costs?

Allocating capital for a fintech platform requires understanding specific technical levers. Cost is rarely a flat fee. It is a variable influenced by operational weight and logic precision.

Recognizing these drivers early allows you to build a system that is both high-performing and sustainable.

1. Product complexity and transaction volume

The scale of your operations determines the fundamental engineering requirements of your system.

- Engineering depth: Complexity dictates the specific requirements of your backend. A platform handling thousands of micro-transactions per second requires specialized, low-latency architecture.

- Scalability needs: Therefore, high-volume environments demand robust load balancing and sophisticated caching layers. Investing in these early prevents a total architectural overhaul as your user base expands.

2. AI model type and decision criticality

The financial impact of each AI decision determines the level of investment needed for model safety.

- Model precision: The type of intelligence you integrate serves as a major cost center. Predictive models for high-stakes credit scoring are significantly more expensive to build and verify than basic chatbots.

- Validation requirements: However, this investment ensures the AI logic remains sound and defensible under market stress. High decision criticality requires rigorous edge-case testing to maintain financial accuracy.

3. Data pipelines and infrastructure needs

Modern AI platforms rely on continuous streams of high-quality data to function effectively.

- Data orchestration: AI is only as effective as the data it consumes. Building real-time pipelines to aggregate information from fragmented sources is a complex and vital engineering feat.

- Compute strategies: Consequently, managing these compute costs requires a strategic choice between local and cloud processing. This prevents unexpected monthly bills from volatile GPU usage.

4. Compliance across multiple jurisdictions

Regulatory requirements vary by region and add significant layers of technical complexity to your build.

- Regulatory flexibility: Operating across borders introduces massive legal complexity. Each jurisdiction has unique rules regarding data residency, KYC, and AML that your platform must satisfy.

- Explainability layers: Therefore, your system must include transparent audit trails to justify AI-driven decisions to regulators. Building these “explainable” layers is a foundational requirement for modern fintech.

5. Security and cloud architecture choices

Ensuring the safety of financial assets is the most critical factor for maintaining user trust.

- Zero-trust protocols: Security is the cornerstone of user trust in finance. Your architecture must defend against sophisticated threats while ensuring rapid, secure access for legitimate users.

- Reputation protection: Implementing high-level encryption adds initial build hours but protects your long-term reputation. A secure cloud environment ensures your platform remains resilient and ready for institutional-grade partnerships.

Strategic cost management separates successful platforms from failed prototypes. Intellivon specializes in optimizing these drivers to ensure your $50,000 to $200,000 investment delivers maximum value.

How Much Does Each Fintech Module Cost?

Granular cost management requires breaking down the platform into its functional components. Each module serves a specific purpose, and the price reflects the complexity of the underlying logic and third-party integrations.

By understanding these individual costs, you can prioritize features that offer the highest immediate ROI while staying within your budget.

Module Pricing Comparison Table

The following estimates reflect the development and integration costs for essential modules in an enterprise-grade system.

| Fintech Module | Estimated Cost | Core Technical Requirement |

| KYC & Identity | $7,000 – $15,000 | Biometric & Document Verification |

| Payment & Ledger | $15,000 – $35,000 | Double-Entry & Multi-Rail Support |

| AI Risk & Fraud | $12,000 – $30,000 | Predictive Model & Real-Time Scoring |

| Admin & Audit | $6,000 – $12,000 | Role-Based Access & Logs |

| Analytics & Monitoring | $5,000 – $10,000 | Drift Detection & Performance Viz |

1. KYC, onboarding, and identity systems

The onboarding process is your first point of contact with a user and must be frictionless yet secure.

- Verification Logic: This module handles the automated checking of government IDs and biometric liveness. It usually integrates with third-party providers like Onfido or Jumio to ensure global compliance.

- Cost Efficiency: Therefore, a well-built system reduces manual review time by over 80%. This allows your team to focus on high-risk cases rather than routine approvals.

2. Payments, ledgers, and transaction flows

Managing the movement of money requires a backend that is both immutable and highly available.

- Architecture Integrity: You must build a system that supports multiple payment rails, such as ACH, Swift, or stablecoin networks. The ledger must follow double-entry accounting principles to prevent data corruption.

- Security Standards: In addition, this module requires high-level encryption to protect sensitive transaction data. This is often the most expensive component because it serves as the financial backbone of your platform.

3. AI risk scoring and fraud detection

This is the “brain” of your platform, where data is converted into actionable financial decisions.

- Model Training: We develop custom algorithms that analyze behavioral patterns to detect anomalies in real-time. This helps in identifying fraudulent transactions before they are settled.

- Decision Speed: Consequently, your system can approve or deny credit in milliseconds. This speed provides a major competitive advantage in high-velocity markets like micro-lending or retail trading.

4. Admin dashboards and audit controls

Internal tools are essential for managing operations and satisfying regulatory reporting requirements.

- Granular Control: The admin panel allows your staff to manage users, view transaction histories, and override AI decisions when necessary. It must include role-based access to ensure sensitive data remains restricted.

- Transparency: Furthermore, the audit trail captures every action taken within the system. This provides the “explainability” required during government audits or internal reviews.

5. Analytics and model monitoring systems

To maintain long-term accuracy, your AI models must be continuously monitored for performance shifts.

- Performance Tracking: This module visualizes key metrics such as model accuracy, precision, and “drift.” Drift occurs when the AI’s performance degrades as real-world market conditions change.

- Early Warning: Therefore, monitoring systems act as an early warning signal for your engineering team. They ensure the platform remains profitable and safe even as user behaviors evolve.

Investing in these modules ensures your fintech platform is built on a foundation of technical excellence.

What Does It Cost by Fintech Platform Type?

Budgetary requirements fluctuate significantly based on the specific niche and the complexity of the underlying financial instruments. A platform’s category determines the depth of the ledger, the frequency of transactions, and the intensity of the regulatory oversight required.

Aligning your capital with the right platform type ensures you don’t over-engineer simple tools or under-fund complex engines.

| Platform Type | Cost Range | Primary Cost Driver |

| Banking (Neo-banks) | $30,000 – $300,000 | CBS Integration & Security |

| Lending & BNPL | $25,000 – $160,000 | AI Scoring & Collections |

| Investment & Trading | $35,000 – $250,000 | Low-Latency Data & APIs |

| Wallets & Payments | $20,000 – $100,000 | UX & Local Rail Integration |

| Crypto & Blockchain | $40,000 – $280,000 | Smart Contract Audits |

1. Banking: $30,000 – $300,000

Digital banking requires the highest level of stability and multi-layered security.

- Core Systems: Building a neo-bank involves creating complex deposit engines and integrating with core banking systems (CBS). You must handle thousands of concurrent users without any data loss.

- Regulatory Depth: Therefore, a significant portion of the budget goes toward multi-factor authentication and real-time transaction monitoring. These features are essential for maintaining a high-trust environment.

2. Lending and BNPL: $25,000 – $160,000

Lending platforms prioritize credit decisioning speed and risk mitigation.

- Credit Logic: The primary cost driver here is the AI-driven scoring engine that evaluates borrower risk in seconds. You also need automated loan disbursement and repayment tracking modules.

- Collection Tools: In addition, these platforms require robust notification and collection systems to manage defaults. A well-built lending app pays for itself by lowering the cost of bad debt through better prediction.

3. Investment and Trading: $35,000 – $250,000

Trading applications are defined by their need for extreme speed and real-time data accuracy.

- Market Data: You must pay for high-fidelity market data feeds and build a backend capable of sub-second order execution. Any lag in data presentation can lead to significant financial loss for users.

- Compliance Layers: Furthermore, these apps need complex “Know Your Business” (KYB) and anti-money laundering tools to verify high-volume traders. Consequently, the engineering effort is focused on latency reduction and security.

4. Wallets and Payment Apps: $20,000 – $100,000

Wallet applications focus on ease of use and rapid integration with local payment rails.

- User Experience: The budget is typically directed toward a frictionless mobile interface and QR-code-based transaction logic. You need seamless integration with various banks and card networks.

- Transaction Velocity: Therefore, these platforms are designed to handle frequent, low-value transactions with minimal processing fees. This makes them highly scalable for mass-market retail adoption.

5. Crypto and Blockchain: $40,000 – $280,000

Blockchain-based platforms require specialized expertise in decentralized ledger technologies.

- Smart Contracts: Developing secure, audited smart contracts is the most critical and expensive part of the build. One logic error can result in a total loss of funds with no way to reverse the transaction.

- Security Audits: In addition, you must account for third-party security audits to verify the integrity of the protocol. These audits are non-negotiable for any platform looking to attract institutional or retail liquidity.

Understanding the specific cost drivers for your platform type is the first step toward a successful launch.

Real AI Fintech Apps and Their Build Costs

Analyzing the market leaders provides a realistic benchmark for your own capital allocation. Established platforms often started as targeted solutions before expanding into comprehensive financial ecosystems.

By examining these benchmarks, you can understand how a $50,000 to $200,000 budget translates into functional, market-ready technology in today’s landscape.

Market Leader Cost Benchmark Table

The following figures represent the estimated capital required to build a production-ready version of these successful platform types.

| Application Type | Market Equivalent | Estimated Build Cost | Core AI Focus |

| Personal Finance | Cleo / Oportun | $50,000 – $100,000 | Conversational AI & Budgeting |

| AI Lending | Upstart | $80,000 – $150,000 | Non-Traditional Credit Scoring |

| Multi-Service | SoFi | $150,000 – $200,000 | Cross-Platform Data Sync |

| Active Trading | Webull | $150,000 – $200,000 | Low-Latency Execution |

| Digital Wallet | Cash App | $60,000 – $130,000 | P2P Logic & Stock/Crypto Buy |

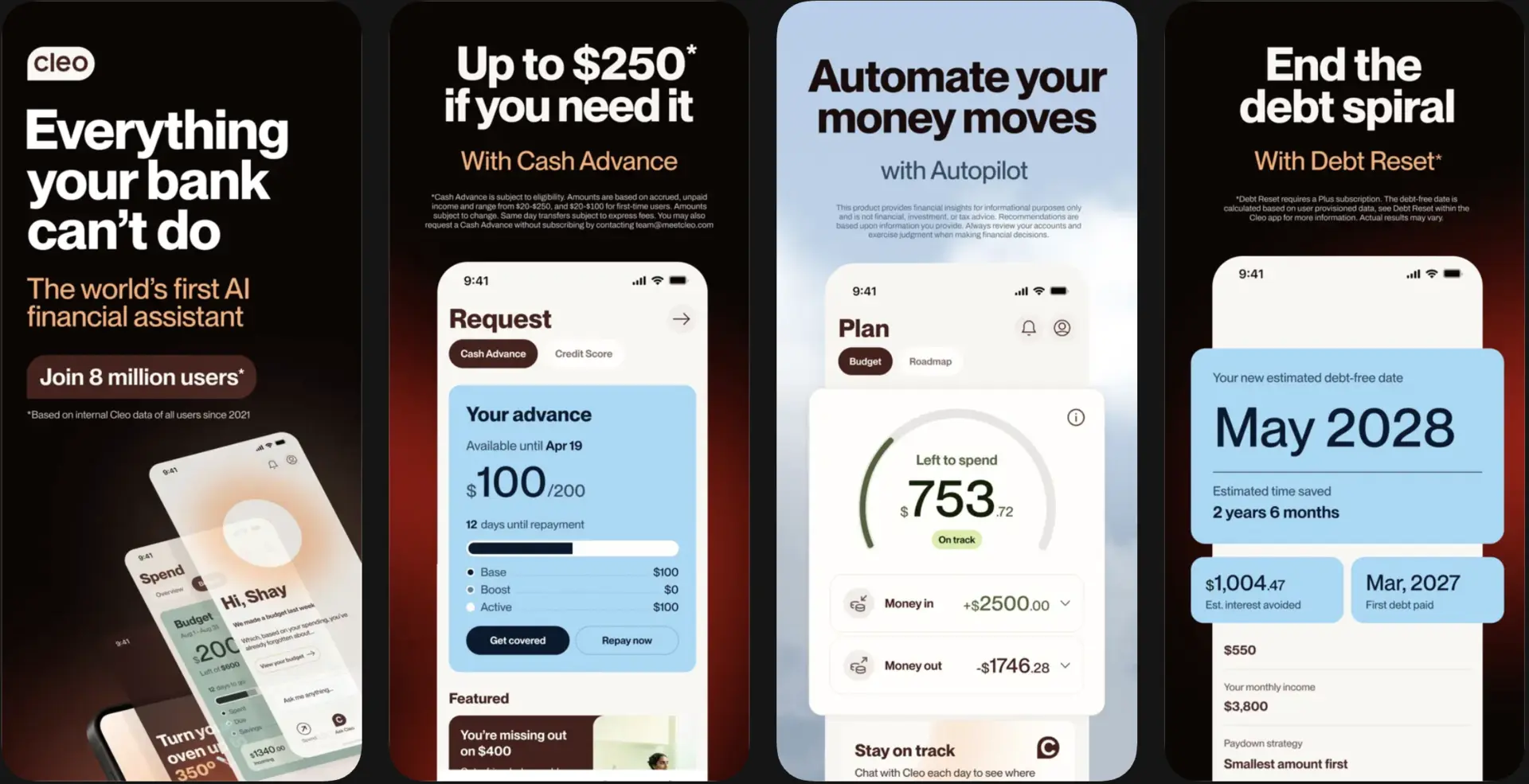

1. Cleo

Cleo focuses on conversational banking and automated financial health for the retail consumer.

- Logic Requirements: Building a similar app involves developing an NLP-driven chatbot that analyzes user spending habits. You need secure read-only access to bank APIs via services like Plaid.

- Capital Efficiency: Therefore, these apps are relatively cost-effective because they focus on data visualization rather than complex lending or high-frequency trading.

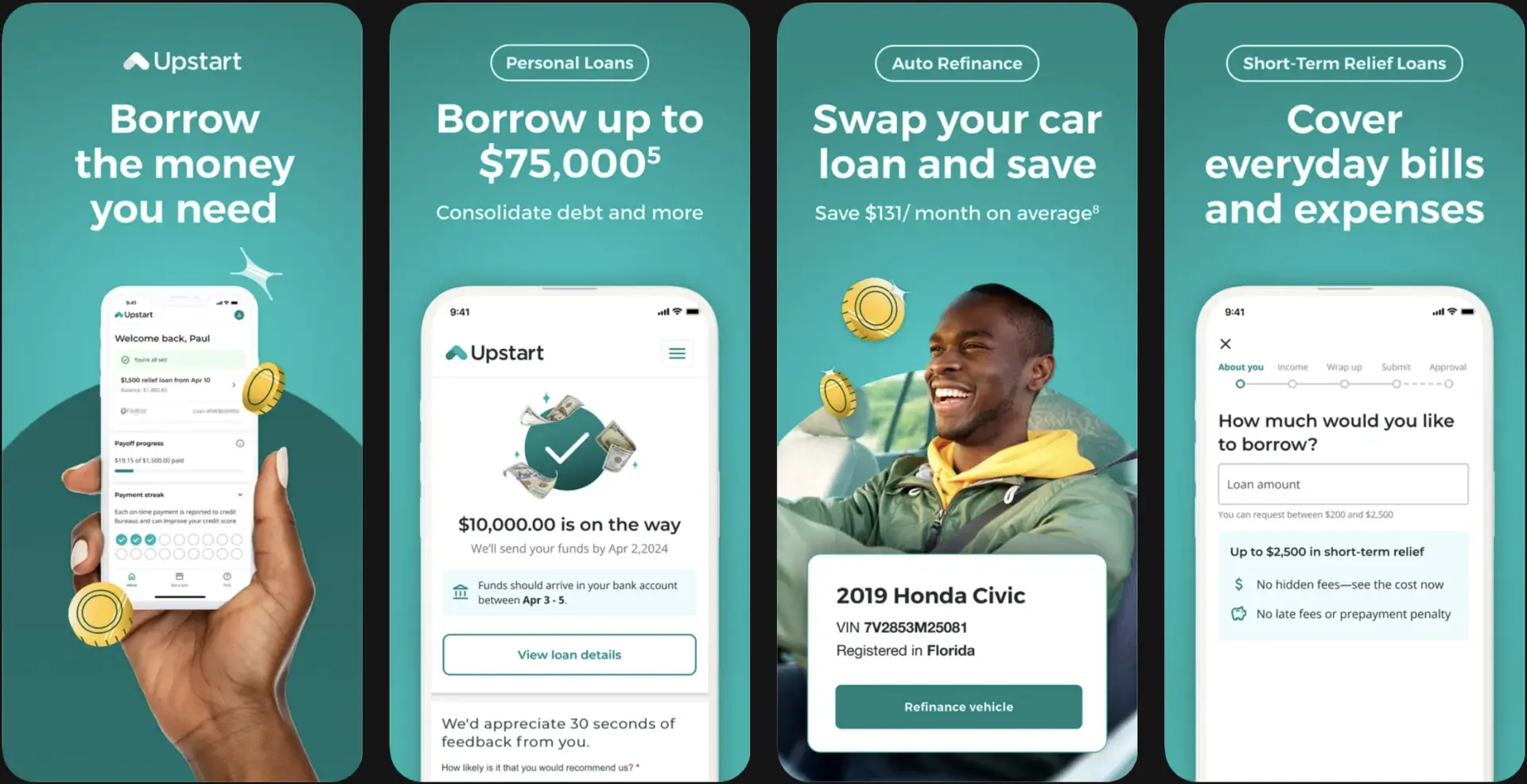

2. Upstart

Upstart changed the market by moving beyond traditional FICO scores to evaluate borrower risk.

- Modeling Depth: Replicating this requires an investment in advanced machine learning models that process thousands of non-conventional variables. You must also build automated loan approval and disbursement workflows.

- Risk Management: Consequently, the budget reflects the intensive testing required to ensure the AI’s predictive accuracy is superior to standard credit models.

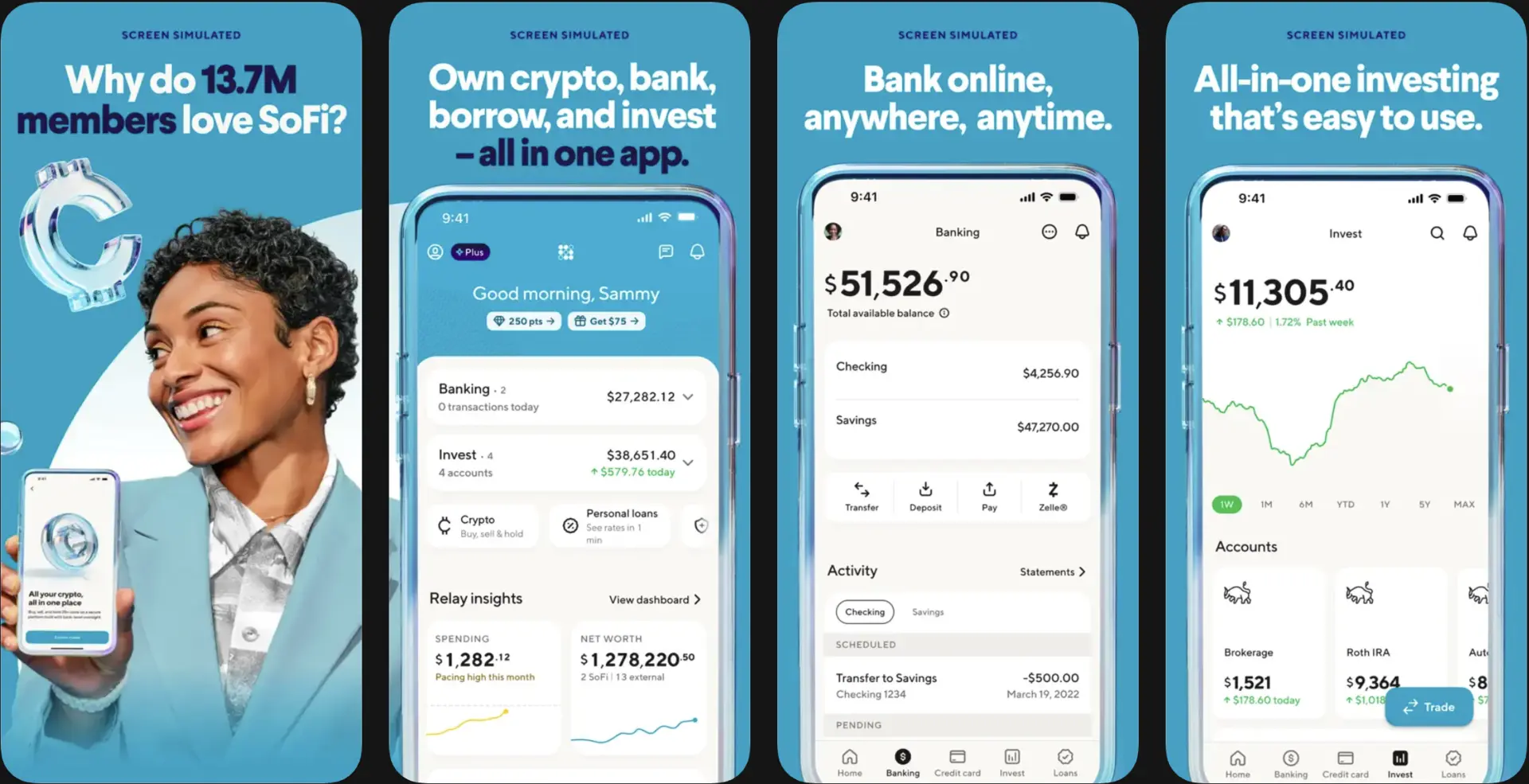

3. SoFi

SoFi represents the “Super App” model where lending, banking, and investing live in a single ecosystem.

- Architecture Complexity: This is the most expensive build type because it requires a unified user identity across multiple distinct financial products. The backend must handle diverse transaction types from mortgage applications to stock trades.

- Data Integration: In addition, the system requires a sophisticated data layer to offer personalized product recommendations based on the user’s total financial picture.

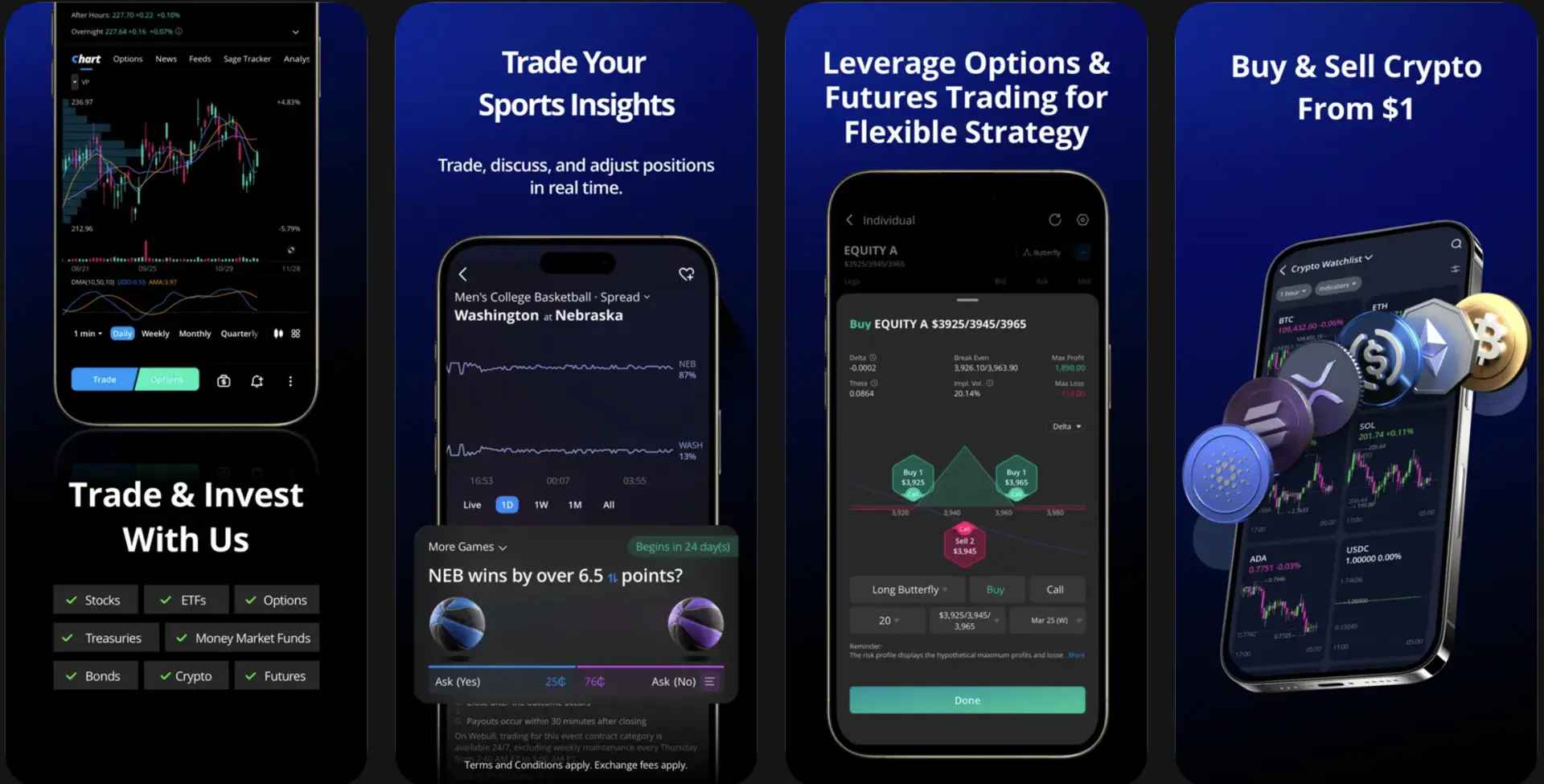

4. Webull

Trading apps require institutional-grade speed and a high-performance frontend for technical analysis.

- Infrastructure Speed: You must invest in a low-latency environment to support real-time price updates and instant order execution. The system must remain stable even during periods of extreme market volatility.

- Analytics Tools: Therefore, a significant portion of the budget goes toward building complex charting libraries and integrating with multiple market data providers.

5. Cash App

Cash App succeeded by making P2P payments, stock buying, and Bitcoin access simple and social.

- Feature Breadth: Building a similar platform involves creating a robust P2P ledger and integrating with various brokerage and crypto APIs. You need a highly secure, yet simple, onboarding process to drive mass adoption.

- Compliance Focus: Furthermore, these apps require heavy investment in real-time fraud monitoring to prevent illicit money transfers. This ensures the platform remains compliant while handling high volumes of retail transactions.

Each of these benchmarks demonstrates how strategic engineering can turn a specific budget into a high-value financial asset. Selecting the right starting point allows you to build a foundation that can eventually scale into a multi-service giant.

What Hidden Costs Do Most Teams Miss?

A successful launch is only the beginning of your financial commitment to an AI platform. Many founders focus heavily on initial development but overlook the “technical debt” and operational overhead that follow.

Recognizing these hidden expenses early prevents your project from becoming a drain on resources and ensures a sustainable path to profitability.

1. Model retraining and drift management

AI models are not “set and forget” tools; they naturally degrade as real-world market conditions change.

- Drift Detection: This cost covers the continuous monitoring of your AI’s accuracy. If consumer spending patterns shift or inflation spikes, your risk models may start making incorrect predictions.

- Retraining Cycles: Therefore, you must budget for regular retraining phases to keep the logic sharp. Without this, your platform’s decision-making value will drop, leading to higher default rates or missed fraud.

2. Compliance updates after launch

Regulatory landscapes in 2026 are highly fragmented and evolve faster than traditional software cycles.

- Regulatory Tracking: You will face ongoing costs for legal audits and technical updates to comply with new privacy laws or AI acts. These changes often require structural adjustments to how your platform stores and processes user data.

- Audit Readiness: In addition, maintaining “audit-ready” status involves recurring fees for third-party security certifications. Neglecting these updates can result in massive fines that far exceed the cost of the updates themselves.

3. Vendor pricing that scales with usage

Many teams rely on third-party APIs for KYC, document verification, or specialized financial data.

- Inference Costs: As your user base grows, your monthly “per-call” fees for these services can skyrocket. What seemed like a cheap integration during the MVP phase can become a major line item as you scale.

- Volume Forecasting: Consequently, you must negotiate volume-based pricing early to avoid being trapped by expensive vendor lock-ins. Strategic founders build their infrastructure to be “vendor-agnostic” to maintain leverage during contract renewals.

4. Explainability and audit layer costs

Regulators now demand that AI systems “explain” their reasoning, especially in high-stakes areas like lending.

- XAI Infrastructure: Building an “Explainable AI” (XAI) layer involves extra logging and diagnostic tools that justify every denial or approval. These layers ensure your platform is transparent and defensible during a government inquiry.

- Diagnostic Maintenance: Furthermore, these tools require their own maintenance to ensure they accurately reflect the model’s current logic. This is no longer an optional feature; it is a foundational cost of doing business in 2026.

5. Legacy system integration overhead

If your platform needs to communicate with older banking cores, the integration process is rarely straightforward.

- Middleware Development: Most legacy systems were not built for real-time AI interaction. You will likely need to build custom middleware to translate data between your modern stack and the bank’s older protocols.

- Maintenance Drag: Therefore, you must account for the specialized developer hours needed to maintain these fragile connections. High-level engineers who understand both COBOL and Python are rare and command premium rates.

Understanding these hidden levers allows you to build a more resilient financial model from day one. By planning for these recurring costs within your $50,000 to $200,000 budget, you ensure your platform remains a high-performance asset.

Should You Add AI or Build AI-Native?

Deciding whether to layer intelligence onto an existing system or build from the ground up is a pivotal financial choice.

In 2026, the architectural foundation of your platform dictates not just your initial spend, but your long-term operational efficiency. Understanding the cost trade-offs between retrofitting and native development helps you avoid expensive technical debt as you scale.

1. Cost of adding AI to existing platforms

Integrating AI features into a pre-existing fintech stack usually requires a smaller initial investment of $15,000 – $45,000.

- Integration Logic: This budget focuses on building API connectors that feed legacy data into third-party AI models. You aren’t rebuilding the core, but rather creating a “bridge” between your current database and the intelligence layer.

- Speed to Value: Therefore, this is the preferred route for established firms looking for quick wins like customer service automation or basic fraud alerts. It allows you to test AI utility without a total system overhaul.

2. Cost of building AI-native fintech apps

Building an AI-native platform from scratch requires a more significant commitment of $60,000 – $180,000.

- Foundation Design: Every part of the system is designed specifically to support machine learning workflows. This includes specialized data pipelines that allow the AI to “learn” in real-time.

- Proprietary Edge: Consequently, you own a highly optimized asset that is far more efficient at handling complex tasks like predictive credit scoring. This higher upfront cost buys you a significant competitive advantage in decision-making speed and accuracy.

3. When retrofitting becomes expensive

Retrofitting seems cheaper initially, but it can quickly become a financial burden if the underlying data is poor.

- Data Friction: If your legacy system was not built for high-speed data flow, the AI will struggle to get the information it needs. You may find yourself spending more on “data cleaning” and middleware than you would have on a fresh build.

- Performance Caps: In addition, retrofitted systems often hit a performance ceiling where they simply cannot handle high transaction volumes. Therefore, if you anticipate rapid growth, the “cheap” fix often becomes a multi-million dollar bottleneck.

4. Choosing the right architecture early

Selecting your path depends on your existing infrastructure and your long-term market goals.

- Strategic Alignment: If you are a startup with no legacy baggage, building AI-native is almost always the better investment for your $200,000 budget. It ensures your platform is future-proof and ready for 2027’s regulatory and technical shifts.

- Hybrid Approaches: However, for established players, a phased “hybrid” approach can manage costs. You can build new, native modules for critical AI decisions while leaving non-essential tasks on the legacy system. This allows you to migrate slowly without disrupting active revenue streams.

Balancing immediate costs with future scalability is the hallmark of a savvy fintech investor.

By choosing the right architecture now, you protect your capital and ensure your platform remains a lean, high-performance engine.

How Do AI Fintech Platforms Make Money?

In 2026, the most resilient fintech monetization strategies are “Hybrid.” Successful platforms combine flat-rate subscriptions for predictability with usage-based “credits” for AI-intensive tasks like deep-risk scoring or instant credit checks.

Platform Monetization Benchmarks

The following table outlines the primary revenue streams for modern AI fintech platforms, reflecting typical market rates and performance expectations.

| Revenue Model | Estimated Earning Potential | Key Performance Metric |

| Subscriptions | $5 – $20 per month/user | Churn Rate & LTV |

| Transaction Fees | 0.5% – 2.0% per transaction | Total Volume (GTV) |

| Data Insights | $5,000 – $30,000 per month | Data Quality & Accuracy |

| White-Labeling | $10,000 – $75,000 per year | License Seat Utilization |

| AI Upgrades | $10 – $50 per “premium” logic | Attach Rate for Power Users |

1. Subscription and freemium models

The subscription model provides a steady, predictable foundation for your recurring revenue.

- Tiered Access: Most platforms offer a basic free tier to drive user acquisition and then upsell to “Pro” or “Enterprise” plans ranging from $5 to $20 per month. These plans often unlock higher transaction limits or priority processing.

- Retention Strategy: Therefore, focusing on high-value features for premium tiers ensures a stable cash flow that covers your baseline operational and cloud costs.

2. Transaction fee-based revenue models

Charging a small percentage on every dollar moved is the most traditional way fintechs scale with their users.

- Volume Alignment: Whether you are processing a P2P transfer or a merchant payment, taking a 0.5% to 2.0% cut aligns your revenue directly with platform usage. This is particularly effective for wallet and payment applications.

- Instant Transfer Fees: In addition, many platforms charge a premium for “instant” settlement versus standard 3-day clearing. Consequently, as your total volume grows, this becomes your most powerful engine for exponential growth.

3. Premium AI features and upgrades

You can monetize the specific “intelligence” of your platform by charging for high-fidelity AI tasks.

- Advanced Logic: Users may pay a one-time fee or an add-on subscription to access “Deep Risk Analysis” or “Automated Tax Optimization.” These features provide tangible financial value that justifies a higher price point.

- Credit Economy: Therefore, implementing a “token” or “credit” system for these tasks allows power users to pay more for heavy usage while keeping the entry point accessible for others.

4. Data monetization and insights sales

The anonymized, aggregated data your platform collects is a highly valuable asset for external partners.

- Market Trends: Institutional investors and retailers pay $5,000 to $30,000 per month for high-level reports on consumer spending habits or credit trends. This data must be properly anonymized to ensure total privacy compliance.

- Anonymized Benchmarking: In addition, you can offer specialized benchmarks to other fintech firms. This allows them to compare their performance against industry averages without ever seeing individual user data.

5. Partnerships and white-label revenue

Licensing your technology to other institutions allows you to monetize your engineering efforts multiple times.

- B2B Licensing: Many regional banks or retail giants prefer to pay $10,000 to $75,000 per year to use your proven infrastructure under their own brand. This “white-label” approach provides high-margin, stable income.

- API Monetization: Furthermore, charging other developers to access your risk scoring or KYC engines via API creates a secondary revenue stream. This transforms your platform from a standalone app into a core piece of financial infrastructure.

Maximizing your ROI requires a strategic mix of these models to capture value from every user segment. By aligning your pricing with the real-world value your AI provides, you transform your development spend into a self-sustaining profit engine.

How to Reduce AI Fintech Build Costs Smartly

Smart cost reduction in fintech centers on “Reusability.” Leveraging pre-vetted security modules and standardized AI APIs can shave months off a development timeline, allowing capital to be diverted toward proprietary model tuning and market acquisition.

Strategic Savings Comparison Table

The following estimates represent the typical percentage of the total budget you can save by adopting these specific optimization strategies.

| Strategy | Potential Savings | Impact on Time-to-Market |

| Pre-built APIs | 15% – 25% | Reduces build by 4–8 weeks |

| Focused MVP | 20% – 40% | Enables launch in 90 days |

| Strategic Outsourcing | 30% – 60% | Rapid access to expert talent |

| Open-Source Tools | 10% – 20% | Lowers licensing overhead |

| Automated QA | 5% – 15% | Prevents expensive rework |

Using pre-built AI models and APIs

Instead of building foundational logic from scratch, you can integrate proven third-party engines for common tasks.

- API Integration: Using established APIs for document verification or basic sentiment analysis can save you 15% to 25% on development costs. You pay only for what you use, which keeps your initial R&D spend low.

- Integration Speed: Therefore, your team can focus on the “last mile” of customization that makes your platform unique. This approach allows you to launch faster while maintaining institutional-grade accuracy.

Leveraging open-source frameworks

Modern fintech relies on a massive ecosystem of open-source libraries that handle everything from encryption to data processing.

- Framework Selection: Utilizing frameworks like Apache Flink for real-time processing or TensorFlow for model training reduces your reliance on expensive proprietary software. These tools are maintained by global communities, ensuring they stay up to date with the latest security standards.

- Community Support: In addition, using widely adopted tools makes it easier to find and hire developers. Consequently, you avoid the high costs associated with training staff on obscure or custom-built internal languages.

Starting with a focused MVP

A Minimum Viable Product should solve one core problem exceptionally well rather than several problems poorly.

- Scope Discipline: Narrowing your focus to a single high-impact feature, such as AI-driven credit scoring for a specific demographic, can reduce costs by 20% to 40%. You avoid the “feature creep” that often causes budgets to spiral out of control.

- Market Validation: Therefore, you can use the initial $50,000 investment to prove your business model and generate revenue. This early success makes it significantly easier to secure the capital needed for later-stage expansions.

Outsourcing to cost-efficient teams

Accessing global talent pools allows you to hire elite engineers at a fraction of the cost of a local in-house team.

- Expert Access: Strategic outsourcing can reduce your total labor costs by 30% to 60%. You gain immediate access to specialists who have already built and scaled similar fintech platforms.

- Reduced Overhead: In addition, you save on the massive costs of recruitment, office space, and employee benefits. This allows you to put more of your capital directly into the code and the AI models that drive your platform’s value.

Automating testing and QA

Manual testing is slow, prone to human error, and expensive over the long term.

- CI/CD Pipelines: Implementing automated testing ensures that every code change is instantly checked for errors or security vulnerabilities. This prevents “regression” where new features accidentally break old ones.

- Long-Term ROI: Therefore, while there is a small upfront cost to set up these scripts, the long-term savings are substantial. You avoid the catastrophic costs of a system failure or a data breach in a live production environment.

Building a world-class fintech platform is a marathon, not a sprint. By applying these cost-reduction strategies, you ensure your capital lasts until the platform becomes self-sustaining.

Conclusion

Investing in an AI-powered fintech system is a move toward long-term growth and operational precision. By understanding the true cost drivers, you can deploy your capital with confidence. In 2026, the most successful leaders prioritize lean, AI-native frameworks that scale without the burden of technical debt.

The journey from a $50,000 MVP to a $200,000 enterprise-grade platform is paved with specific technical milestones and strategic choices. Now is the time to transition from observation to execution. Partner with a team that understands the intersection of finance and intelligence to ensure your platform sets the industry standard for the next decade.

Build Your AI Fintech Platform With Intellivon

Building an AI-native payment infrastructure rests on designing a system where every payment decision is made in real time, across fraud, routing, settlement, and compliance. At

Intellivon builds payment infrastructure where AI is embedded into the core decisioning layer, enabling faster transactions, lower risk, and seamless scalability across modern payment rails.

Our approach ensures your platform can operate in real-world conditions, handling high transaction volumes, evolving fraud patterns, and complex regulatory requirements without performance trade-offs.

A. Designing Real-Time Payment Decision Architectures

Payment infrastructure today operates in milliseconds. We design systems where every transaction is evaluated, routed, and executed instantly without latency.

- Low-latency decision pipelines: Our engineering focus ensures sub-second transaction processing to maintain a smooth user experience.

- Event-driven systems: We utilize streaming frameworks like Kafka to handle massive data volumes with zero bottlenecking.

- Unified decision engines: This architecture combines fraud, routing, and compliance into a single logic layer for higher accuracy.

- Orchestration across rails: The system manages card, ACH, RTP, and cross-border rails seamlessly within one environment. This ensures every payment decision happens within the transaction flow, not after it.

B. Enabling Agent-Ready Payment Architectures

As agentic commerce evolves, payment systems must support AI-initiated transactions safely and reliably.

- Layer Separation: We maintain a strict separation between the decisioning and execution layers to prevent unauthorized activity.

- Secure Tokenization: Credential handling is managed through advanced tokenization to protect user data during automated trades.

- Delegation Frameworks: Our systems include controlled payment authority, allowing for delegated spending within strict parameters.

- Protocol Compatibility: We ensure your platform remains compatible with emerging agentic standards to future-proof your investment. This ensures your infrastructure is ready for AI agents without compromising control or security.

C. Embedding Explainability and Compliance Into the Core

AI in payments must be transparent and compliant by design. We build systems that meet regulatory requirements without slowing operations.

- Transaction-level Explainability: Every AI-driven decision is backed by a clear, human-readable justification for regulatory defense.

- Continuous Audit Trails: The architecture captures a permanent record of all system actions to ensure total operational transparency.

- Standards Alignment: Our builds are strictly aligned with PCI DSS and GDPR requirements from the very first line of code.

- Governance Controls: We implement role-based access to ensure sensitive financial data remains accessible only to authorized personnel. This ensures your system remains auditable, compliant, and regulator-ready at all times.

D. Integrating AI Across the Payment Ecosystem

AI-native infrastructure only works when it connects seamlessly across systems. We design integration layers that unify your payment stack.

- API-First Architecture: Our modular design allows for rapid connectivity with external fintech tools and services.

- Gateway Integration: We ensure the system communicates flawlessly with existing processors, gateways, and core banking systems.

- Unified Intelligence: The platform provides a single view of data across card, ACH, and cross-border payment flows.

- Phased Modernization: Therefore, you can upgrade your infrastructure incrementally without the risk of a total system shutdown. This allows you to evolve your infrastructure without replacing everything at once.

At Intellivon, we help you map your transaction volume, system complexity, and business goals into a clear AI-native architecture and roadmap. Talk to our team to get a tailored payment infrastructure strategy and project estimate.

FAQs

Q1. What is the cost to build an AI fintech platform?

A1. Building a production-ready AI fintech platform in 2026 typically requires an investment between $50,000 and $200,000. This range covers everything from a focused $50,000 MVP to a sophisticated $200,000 enterprise-grade system. Key cost drivers include the complexity of your risk scoring models, data pipeline depth, and required regulatory integrations.

Q2. Why is AI fintech more expensive than SaaS?

A2. Unlike standard SaaS, AI fintech requires expensive real-time data orchestration and high-stakes model validation. You are processing sensitive financial decisions that demand extreme precision. These platforms require specialized talent, massive compute power for model inference, and continuous retraining to prevent performance degradation over time.

Q3. Can I add AI to an existing fintech app?

A3. Yes, you can retrofit AI onto existing stacks for approximately $15,000 to $45,000. This process involves building API connectors to bridge your legacy database with modern intelligence layers. However, while cheaper initially, retrofitting may eventually face performance bottlenecks if your original architecture cannot handle high-speed, AI-driven data flows.

Q4. How much does compliance increase cost?

A4. Compliance and security protocols can increase your total development budget by 20% to 30%. In finance, you must invest in automated KYC/AML workflows, data encryption, and “Explainable AI” layers to satisfy regulators. Neglecting these areas is a massive risk; the cost of a single regulatory fine often dwarfs the initial investment.

Q5. Should I build or buy AI fintech solutions?

A5. Buying is faster for generic needs, but building ensures you own the intellectual property and unique AI logic. If your business model relies on proprietary risk scoring or a unique user experience, building is the superior long-term investment. Most leaders choose a hybrid approach: buying infrastructure while building custom AI modules.