Building a white-label fintech platform is a key move in today’s financial industry. For fintech companies, the chance lies in closing the gap between outdated banking systems and the need for flexible, digital-first financial services. However, getting a platform ready for market can often be confusing due to technical terms and unclear direction.

Succeeding in this area needs a solid structure that can manage high transaction volumes while staying compliant with global banking rules. As a result, many investors have difficulty balancing quick market entry with long-term technical growth.

This blog provides a clear guide for creating a high-quality white-label solution. We will cover the key elements of a banking-grade platform, from core ledger integration to the details of multi-tenant security. You will understand the development process and the strategic decisions that can make a platform profitable or turn it into a technical burden.

At Intellivon, we have designed and built advanced financial technologies where precision, security, and scalability are the main priorities. Our experience in creating enterprise-grade AI and platform solutions for global markets shapes the depth of this blog.

Why White-Label Platforms Are Revolutionizing The Banking Sector

White-label fintech platforms help banks launch branded digital services faster. They remove the need to build infrastructure from scratch, reducing costs and speeding up innovation.

As a result, adoption is rising quickly. At the same time, traditional banks are digitizing, while non-banks are entering finance through embedded models.

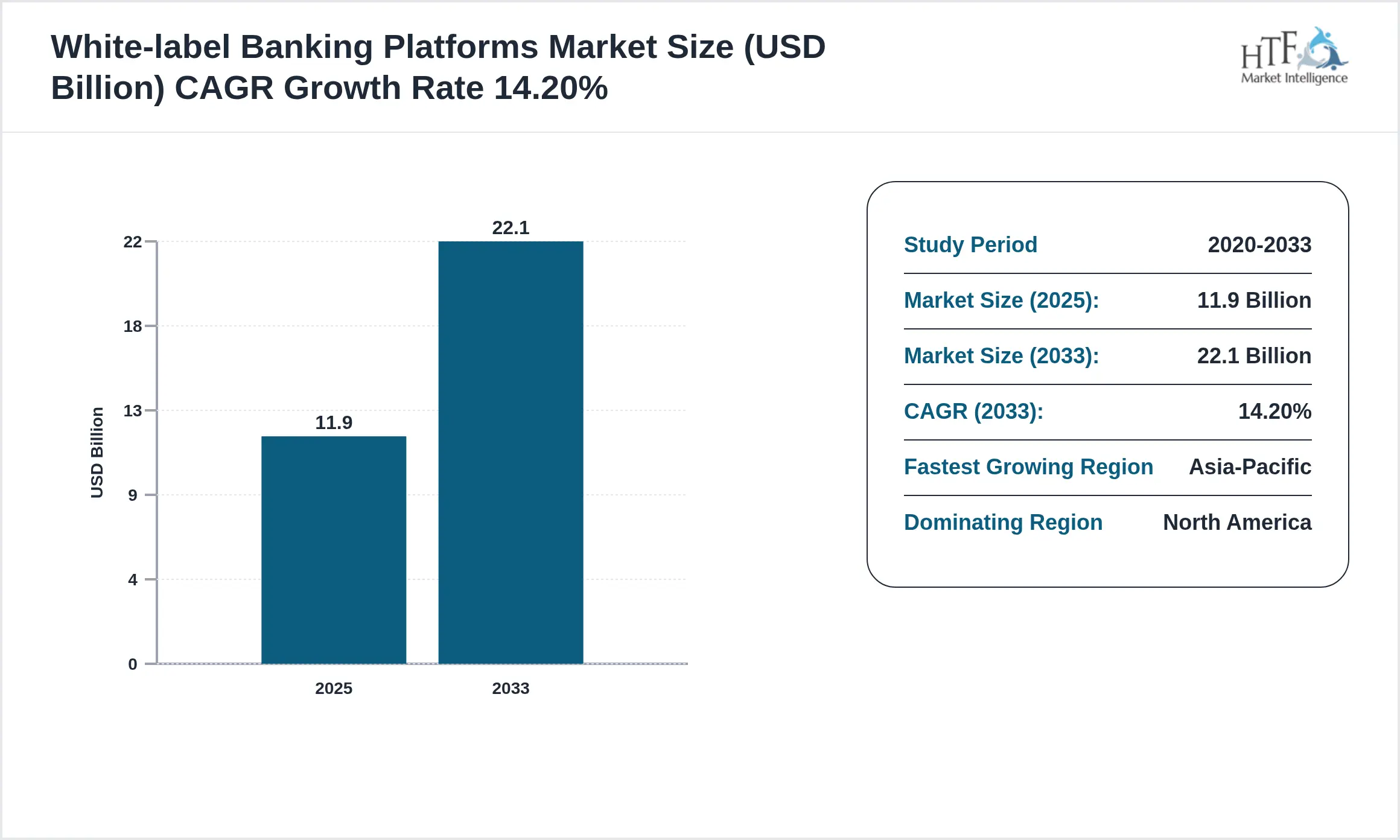

The white-label banking platform market is growing rapidly. In North America alone, it is valued at around $11.9 billion in 2025. Globally, the market is expected to expand at a 14.2% CAGR through 2033, driven by rising demand for faster digital banking launches.

Providers like Solaris offer modular BaaS platforms with payments and lending. Narvi enables businesses to launch IBAN accounts and onboarding in just a few weeks.

For example, Nicheclear used a paytech platform to expand into Europe within a year. It gained market share quickly by offering compliant IBAN services.

These examples show clear results where businesses see 30–40% efficiency gains and faster ROI. This shift also aligns with the rise of agentic AI in banking, where systems can operate more autonomously.

The shift toward modular fintech architecture represents a fundamental pivot in how financial services are delivered and scaled. For investors, this model offers a high-velocity entry point into a sector previously defined by high capital moats and technical inertia.

1. Rapid Market Entry and Capital Efficiency

White-label solutions eliminate the multi-year development cycles traditionally associated with banking software. Entrepreneurs can deploy pre-validated stacks that have already cleared performance benchmarks.

Consequently, this lowers the risk of deployment and allows for rapid iteration based on live market feedback.

2. Bridging the Legacy Technology Gap

Traditional banks often struggle with monolithic systems that lack API compatibility. A white-label layer acts as a sophisticated digital wrapper, providing a modern user experience without requiring a total overhaul of the core ledger.

Therefore, it enables legacy institutions to offer competitive features like instant lending or real-time treasury management almost overnight.

3. Scalable Regulatory Compliance

Compliance remains the most significant hurdle in the financial industry. Leading white-label platforms integrate automated KYC, AML, and SOC2 protocols directly into the system architecture.

By utilizing a platform that is “compliant by design,” investors mitigate legal risks while ensuring the product remains attractive to risk-averse institutional partners.

This transition from rigid infrastructure to modular agility is redefining the economics of the digital banking landscape. It transforms financial innovation from a heavy capital expenditure into a flexible, scalable strategic asset.

What Is A White-Label Fintech Platform for Banks?

A white-label fintech platform is a ready-to-use digital banking system developed by a specialized technology company. Banks or entrepreneurs purchase this software and apply their own branding to it.

Think of it as a pre-built engine where you only need to design the car’s exterior. This allows you to offer professional financial services like mobile payments or lending without writing a single line of code.

This plug-and-play approach transforms complex infrastructure into a simple, customizable business asset. It enables you to launch a fully functional financial brand with minimal technical overhead and maximum speed.

What Banks Actually Get in a White-Label Platform

A white-label platform provides a sophisticated balance between foundational stability and outward-facing uniqueness.

It allows institutions to secure high-tier infrastructure while maintaining the flexibility to tailor the experience for their specific demographic.

1. What is pre-built vs custom-built in the system

The platform arrives with a battle-tested core, but leaving room for customization is vital for market differentiation. Therefore, banks focus their resources on unique features rather than reinventing basic transaction logic.

| Feature Category | Pre-built Foundation | Custom-built Layer |

| Infrastructure | Core Ledger, Database, Security Protocols | Third-party API Integrations |

| Operations | KYC Workflows, Transaction Engines | Unique Credit Scoring Models |

| Interface | Standard Dashboard Templates | Proprietary UI/UX Design & Branding |

2. What banks control vs what partners manage

Success depends on a clear division of labor between the financial institution and the technology provider.

This partnership ensures that the bank remains the authority on customer relationships while the partner handles the technical heavy lifting.

| Operational Area | Bank Control | Partner Management |

| Compliance | Final Approval, Regulatory Licensing | AML Monitoring, Technical Audits |

| Data | Customer Relationship Management | Encryption, Hosting, Backups |

| Support | Tier 1 Customer Interaction | Technical Troubleshooting, Maintenance |

3. How branding and ownership work in practice

Ownership in a white-label context usually refers to the “right to use” and the ownership of customer data. While the provider owns the underlying code, the bank retains full control over the brand identity and the user base.

This ensures that the institution builds its own equity without the burden of maintaining a massive internal dev team.

4. Why is this not SaaS or a ready-made product

Unlike standard SaaS, white-label fintech is highly extensible and often deployed in isolated environments.

It offers deep integration capabilities that generic software cannot match, making it a strategic asset rather than a simple subscription. Consequently, it provides the “feel” of a bespoke build with the reliability of a proven product.

This structural approach allows banks to innovate at the speed of a startup while maintaining institutional-grade security. It represents a strategic compromise that maximizes both speed-to-market and long-term control.

Who Should Build a White-Label Platform

Deciding to build a white-label platform is a big step for any growing business. It is a smart move for companies that want professional tools without the long wait of building them from scratch.

1. Mid-size banks scaling digital offerings

Smaller banks often have loyal customers but struggle with old technology. Therefore, a white-label system helps them launch modern apps and fast loans in a few months. It bridges the gap between old-school trust and the new digital world.

2. NBFCs launching new financial products

Finance companies can use these platforms to make their loan process fully digital. Instead of using paper and manual checks, they can use automated systems to approve customers faster. Consequently, this saves money and helps them grow their business much quicker.

3. Fintech firms targeting B2B banking models

New tech startups use these pre-built systems to offer banking tools to other businesses. By using a ready-made backend, they can spend their time solving specific customer problems. It turns their business into a high-profit tech company instead of a slow service provider.

4. Enterprises entering embedded finance

Large companies like online stores are now adding banking features to their own apps. Whether it is “buy now, pay later” or digital wallets, white-label tech makes it easy and legal. This allows brands to make more money from their current customers without becoming a real bank.

This technology is a powerful tool for any leader who wants to grow through financial services. It removes the high risk of starting from zero by providing a system that already works.

What a Bank-Ready Platform Must Support

A banking platform is only as good as the trust it builds with its users. To compete in today’s market, the system must manage the entire financial journey.

Therefore, investors should look for a foundation that is both strong and flexible.

1. End-to-end onboarding with KYC and AML

The first impression starts with how a user joins the platform. A bank-ready system must make this process smooth but incredibly secure to meet legal rules.

- Identity Checks: Real-time scanning of IDs and face-matching technology.

- Risk Screening: Instant checks against global watchlists to block bad actors.

- Digital Signatures: Secure ways for customers to sign documents on their phones.

2. Payments, cards, and wallet infrastructure

Money movement is the heartbeat of any fintech app. The platform must connect with global payment networks so users can move their funds without delays.

- Virtual & Physical Cards: The ability to issue branded debit or credit cards instantly.

- Digital Wallets: Safe storage for money that supports quick transfers and QR payments.

- Bank Transfers: Easy connections to standard systems like ACH, SEPA, or SWIFT.

3. Lending, underwriting, and risk systems

Lending is where most financial platforms find their profit. However, doing this safely requires smart tools that can predict who will pay back their loans.

- Automated Scoring: Using data to decide on loan approvals in seconds.

- Risk Management: Tools that monitor the total health of the loan portfolio.

- Collections: Systems that send reminders and manage repayments automatically.

4. Compliance, audit, and reporting layers

Banks operate under heavy supervision, so the software must keep a perfect record of everything that happens. This makes it easy to pass audits and keep regulators happy.

- Audit Trails: A permanent log of every click and transaction made on the platform.

- Tax Reporting: Automated tools that generate documents for users and the government.

- Data Security: Using high-level encryption to ensure that sensitive info never leaks.

5. Multi-tenant and multi-brand capabilities

A true white-label platform must allow you to run different “stores” from one single engine. This is vital for companies that want to launch several different brands or serve many partners at once.

- Separate Databases: Keeping customer data for different brands completely apart.

- Custom Branding: Changing logos and colors for each partner without touching the code.

- Central Control: Managing all different brands from one master dashboard.

Investing in these core features ensures your platform is ready for the big leagues. Consequently, you spend less time fixing bugs and more time growing your user base.

White-Label vs Custom vs SaaS Platform

Choosing the right path for your fintech project is a major decision. You must balance the need for speed with the desire for total control.

While some choose to build everything from scratch, others prefer ready-made tools. Therefore, understanding these three models is the first step toward a successful launch.

Key differences in cost, speed, and control

Each model offers a different trade-off between how much you spend and how much you own:

- A custom build gives you total freedom but takes years to finish.

- On the other hand, SaaS is fast but often lacks the deep features a bank truly needs.

- White-label platforms sit in the middle, offering a pre-built engine that you can still customize.

| Feature | Custom-Built | SaaS Product | White-Label Platform |

| Time to launch | 18–24 Months | 1–2 Months | 3–6 Months |

| Cost of development | Very High ($$$) | Low (Monthly Fee) | Moderate ($$) |

| Customization depth | Unlimited | Very Limited | High (Modular) |

| Compliance readiness | Build from scratch | Shared/Generic | Built-in (Bank-grade) |

| Long-term scalability | High (Hard to manage) | Limited by the provider | High (Flexible) |

Selecting the right model depends on your specific business goals. If you want to own your brand and scale quickly without the massive headache of a custom build, white-label is often the best path.

This is because it gives you the “look and feel” of a custom product with the speed of a ready-made one.

This comparison shows that white-label works best when built right. It provides a solid foundation that allows you to focus on your customers rather than fixing code. Consequently, you can enter the market with confidence and a professional edge.

Architecture of a White-Label Fintech Platform

The architecture of a professional fintech platform is like the foundation of a skyscraper. It must be strong enough to hold massive weight but flexible enough to change as the market grows.

The goal is to build a system where every part talks to the others without friction.

1. API-First Integration with Core Banking Systems

Modern platforms do not try to do everything inside one single piece of software. Instead, they use an “API-first” approach. This means the platform acts as a bridge that connects to old bank records or new payment networks easily.

- Easy Connections: You can plug in new services like crypto trading or international wires in days.

- System Agnostic: The software works with almost any existing bank database.

- Future Proof: As technology changes, you only need to update the connection, not the whole system.

2. Multi-Tenant Product and Branding Engine

A great white-label platform must support “multi-tenancy.” This is a technical way of saying one engine can power many different brands at the same time.

Therefore, you can sell your platform to five different banks, and each one will look and feel unique.

- Branding Isolation: Each partner gets their own colors, logos, and user flows.

- Resource Sharing: You save money by running everyone on the same core code while keeping their data separate.

- Scalability: Adding a new brand to your platform becomes as simple as clicking a button.

3. Data Pipelines and Real-Time Processing Layers

In finance, speed is everything. If a customer swipes a card, the data needs to move instantly.

The platform uses “data pipelines” to make sure information flows from the point of sale to the bank ledger in milliseconds.

- Live Updates: Customers see their balance change the second they spend money.

- Fraud Detection: The system looks for patterns in data while the transaction is still happening.

- Error Handling: If a connection drops, the system holds the data and tries again automatically.

4. Security, Compliance, and Governance Systems

Security is the most important part of the build. Because you are handling other people’s money, the architecture must include “compliance by design.” This means the rules are baked into the code.

- Encryption: Every piece of data is locked, so only authorized people can see it.

- Access Control: You can set strict rules on who within a bank can view sensitive customer info.

- Automated Audits: The system creates a paper trail for every action, making it easy to show regulators you are following the law.

5. AI-Driven Automation and Decision Engines

The best platforms today use AI to handle the boring and repetitive tasks. This reduces the need for a large staff and makes the platform much smarter over time.

- Smart Lending: AI looks at a user’s history and decides if they qualify for a loan in seconds.

- Customer Support: Bots handle the most common questions, so humans only step in for big issues.

- Predictive Analysis: The system can warn a bank if it looks like many people might miss their loan payments next month.

Building this kind of architecture ensures your platform stays relevant for a long time. Consequently, you create a digital asset that grows in value as more partners and users join.

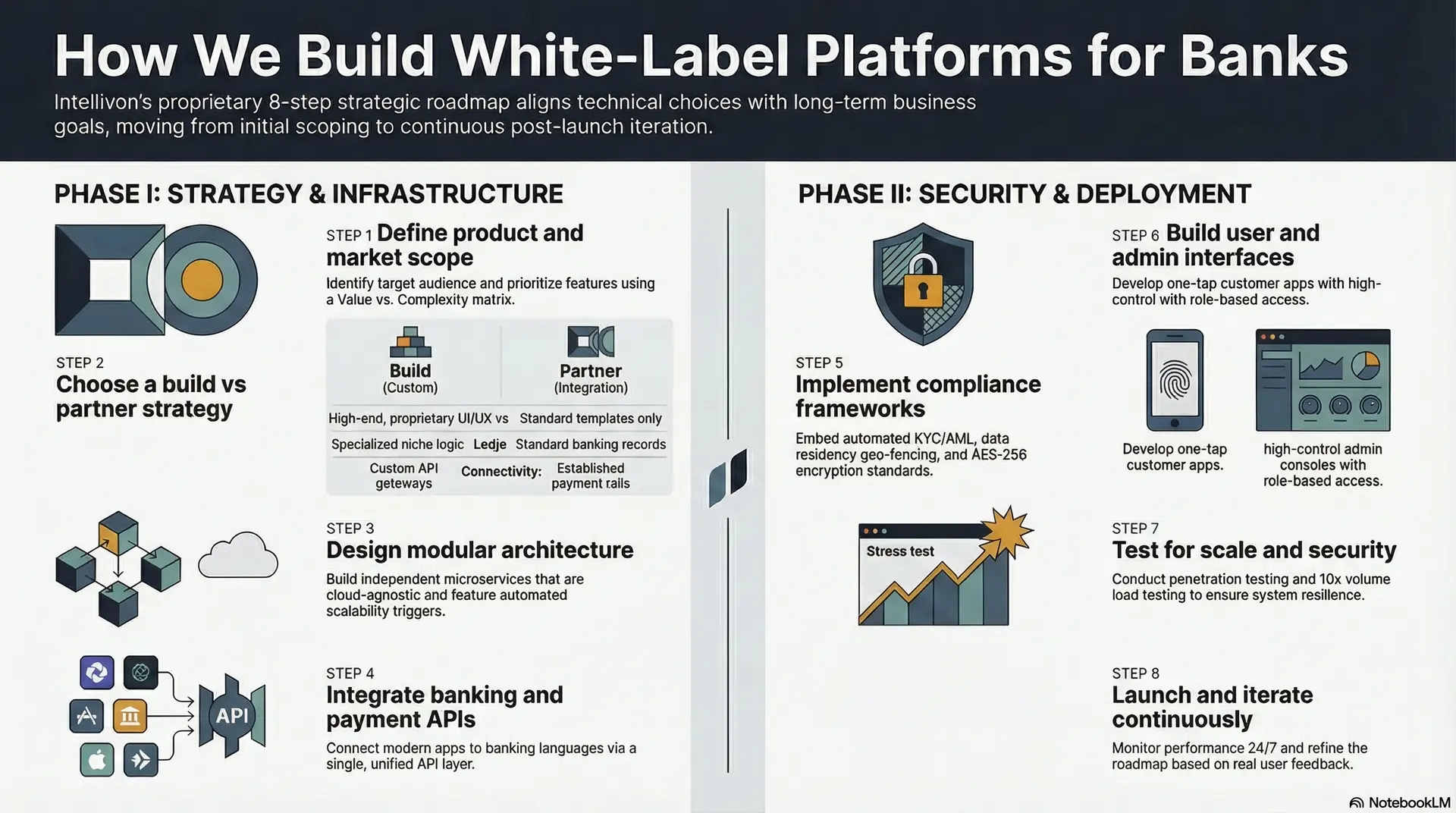

How We Build White-Label Platforms for Banks

Building a professional platform requires a disciplined, phase-by-step approach. At Intellivon, we use a proven roadmap to move from a blank page to a live, secure banking environment.

Therefore, we ensure that every technical choice aligns with your long-term business goals.

Step 1: Define product and market scope

First, we identify exactly who the platform is for and what problems it solves. We help you decide if you are building a simple payment app or a full-scale digital bank.

- Strategic Mapping: We look at your target audience, whether they are retail users, SMEs, or corporate clients.

- Feature Prioritization: We use a “Value vs. Complexity” matrix to decide which features go live in Version 1.

- Market Alignment: We ensure your platform meets the specific regional needs of the banks you plan to serve.

Our team pressure-tests the business model behind the software. We analyze the unit economics of each proposed feature. This ensures the platform is designed to be profitable from the day you launch, rather than just being a technical expense.

Step 2: Choose a build vs partner strategy

We analyze which parts of the system should be custom-made and which should use existing technology. This balance is what makes a project both fast and unique.

| Component Type | Build (Custom) | Partner (Integration) |

| User Experience | High-end, proprietary UI/UX | N/A (Standard templates only) |

| Core Ledger | Specialized niche logic | Standard banking records |

| Connectivity | Custom API gateways | Established payment rails |

We maintain an extensive library of pre-vetted partners. Instead of you spending months interviewing vendors, we bring a curated list of the best-in-class providers for ledgers, cards, and KYC. This significantly reduces your research time and technical risk.

Step 3: Design modular architecture

Our engineers create a “modular” system where different parts of the software can be updated without breaking the whole thing.

- Microservices Approach: We break the platform into independent services like “Payments,” “User Profile,” and “Loans.”

- Cloud Agnostic: We build so you can host on AWS, Azure, or Google Cloud without being “locked in.”

- Scalability Triggers: The system automatically adds more power during high-traffic times, like paydays.

We specialize in building event-driven systems. This ensures that when a transaction happens, every other part of the platform, like balance updates and fraud checks, reacts instantly without any lag.

Step 4: Integrate banking and payment APIs

This step turns the software into a real financial tool. We handle the complex connections so money moves safely across borders and networks.

- Protocol Translation: We make modern apps talk to old-school banking languages (like ISO 20022).

- Unified API Layer: We build a single doorway that connects to multiple payment networks at once.

- Webhook Management: We set up real-time alerts for instant payment success notifications.

Our deep experience with Open Banking standards ensures your platform is ready to plug into the wider financial ecosystem. This allows for advanced features like account aggregation that give you a competitive edge.

Step 5: Implement compliance frameworks

Safety is baked into the code from day one. We install tools that protect you from bad actors and legal trouble.

- Automated KYC/AML: We use AI to verify identities and scan for money laundering risks in seconds.

- Data Residency: We ensure customer data stays in the country required by law using geo-fencing.

- Encryption Standards: All data is protected with AES-256 encryption, the gold standard for banks.

We follow a “Compliance-as-Code” philosophy. Instead of checking for rules at the end of the project, our system is programmed to prevent non-compliant actions from happening in the first place. This proactive approach saves you from heavy fines later on.

Step 6: Build user and admin interfaces

We design two versions of the app: one for your customers and one for your staff.

- The Customer App: Focused on speed, ease of use, and one-tap actions.

- The Admin Console: A powerful cockpit for your team to monitor the health of the entire platform.

- Role-Based Access: We ensure your employees only see the data they absolutely need.

We use a “Design System” approach for our white-label builds. This means your partners or sub-brands can change the entire look and feel of their version of the app in minutes without writing new code. This flexibility makes your platform highly attractive to a wide range of institutional buyers.

Step 7: Test for scale and security

Before going live, we put the platform through rigorous stress tests.

- Penetration Testing: We simulate “ethical hacks” to find and fix any weak spots.

- Load Testing: We push the system to handle 10x your expected volume to ensure it never crashes.

- Regression Testing: We automatically test all old features every time we add something new.

We utilize principles of chaos engineering to ensure the platform is resilient. This means we intentionally test how the system handles failures in a controlled way. It proves that the platform can recover itself automatically without human help.

Step 8: Launch and iterate continuously

The launch is just the beginning of the journey. Once the platform is live, we use real-world data to see how people use it.

- A/B Testing: We test different feature versions to see which ones your customers like best.

- Performance Monitoring: We watch the system 24/7 to catch and fix issues early.

- Roadmap Planning: We help you decide what to build next based on real user feedback.

We act as your long-term technical partner, helping you manage your product roadmap based on real user feedback. Our goal is to ensure your technology stays future-proof as the global fintech landscape changes.

This approach allows enterprises to launch secure, scalable financial platforms in 3-6 months while maintaining full control over brand identity and customer data.

Cost to Build a White-Label Fintech Platform

Building a white-label fintech platform is not a fixed-cost project. The total investment depends on how deeply the system integrates with banking infrastructure, compliance frameworks, and multi-product financial workflows.

Unlike plug-and-play solutions, enterprise-grade platforms require modular architecture, real-time data systems, and regulatory readiness from day one. As a result, costs are driven more by system complexity, integrations, and scalability needs than just feature count.

1. Cost Breakdown by Modules and Complexity

| Component | Scope | Estimated Cost |

| Onboarding & KYC Layer | User onboarding, identity verification, AML checks | $8,000 – $20,000 |

| Payments & Wallet System | Transfers, wallets, payment processing | $15,000 – $40,000 |

| Cards & Transaction Engine | Card issuing, transaction handling, and settlements | $10,000 – $30,000 |

| Lending & Risk Engine | Credit scoring, underwriting, and loan workflows | $15,000 – $35,000 |

| Compliance & Reporting | Audit logs, regulatory reporting, and monitoring | $10,000 – $25,000 |

| Multi-Tenant & Branding Layer | White-label controls, UI customization | $8,000 – $20,000 |

| Admin & Analytics Dashboard | Insights, controls, operational dashboards | $8,000 – $18,000 |

Estimated Total Development Cost:

$70,000 – $180,000+, depending on complexity and integrations

2. Key Factors That Influence Cost

A. Integration Depth

Connecting with core banking systems, payment gateways, KYC providers, and card networks significantly increases complexity and cost.

B. Compliance Requirements

Multi-region compliance (GDPR, PCI-DSS, AML) adds layers of validation, monitoring, and reporting infrastructure.

C. Customization Level

The more tailored the workflows (lending, onboarding, risk), the higher the development effort.

D. Scalability Needs

Platforms designed for multi-country expansion and high transaction volumes require stronger infrastructure from the start.

3. Infrastructure and Operational Costs

Building the platform is only part of the investment. Running it at scale requires:

- Cloud infrastructure (AWS, Azure, GCP)

- Data storage and processing pipelines

- Security and monitoring systems

- API management and uptime infrastructure

Estimated Monthly Cost:

$2,000 – $10,000+ depending on scale and usage

4. Timeline vs Cost Trade-Off

Faster launches require larger teams and parallel development, which increases cost. However, this reduces long-term opportunity loss and accelerates ROI.

Standard Timelines:

- MVP Platform: 3–5 months

- Full-Scale Platform: 6–12 months

The cost of building a white-label fintech platform is shaped by how deeply it integrates, how scalable it is, and how compliant it needs to be.

Enterprises that invest in the right architecture early avoid costly rebuilds later. As a result, the focus should not be on the lowest cost, but on building a platform that can scale, adapt, and operate reliably in regulated environments.

Want an exact cost breakdown for your platform? Speak with our experts today.

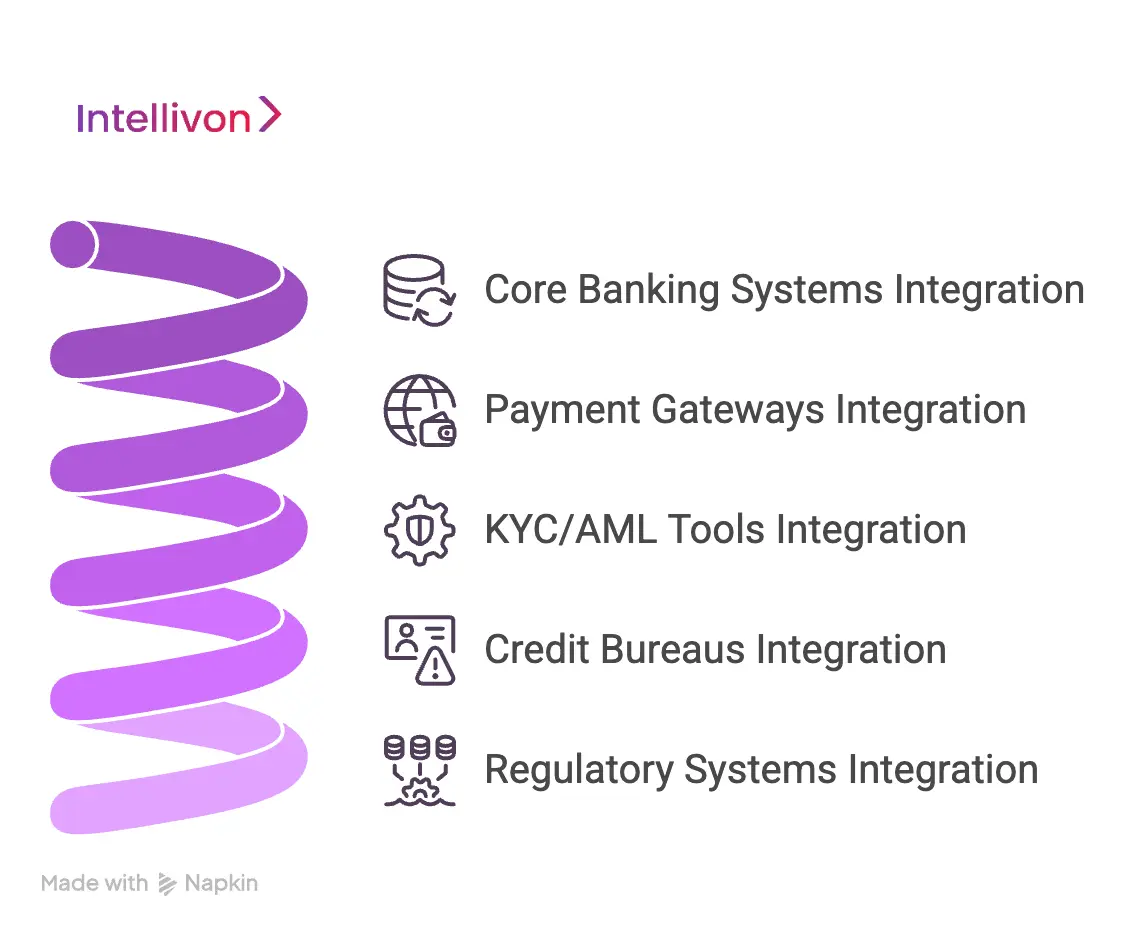

Key Integrations Required for Success

A white-label platform is only as powerful as the ecosystem it connects to. For a bank-ready system, the true value lies in how it communicates with the global financial grid.

Therefore, choosing the right integrations is a vital business strategy.

1. Core banking systems and ledger integrations

The core banking system (CBS) is the “brain” of the bank where all account balances and transaction histories live. A successful platform must sync perfectly with these legacy systems without slowing down.

- Bi-directional Sync: Ensuring the app and the bank’s main database always show the same balance.

- Standard Protocols: Using languages like ISO 20022 to talk to global banking networks.

- Legacy Wrappers: Building a modern layer over old systems so they can finally support mobile features.

Our approach focuses on “core-agnostic” connectivity. This means the platform can plug into almost any existing bank database, whether it’s a modern cloud ledger or a 30-year-old physical server, ensuring a smooth flow of data.

2. Payment gateways and card networks

To be useful, your platform must allow users to move money in and out easily. This requires deep connections to the world’s biggest payment rails.

- Card Issuance: Integrating with processors like Marqeta or Galileo to issue virtual and physical debit cards.

- Global Rails: Connecting to networks like Visa and Mastercard, as well as local systems like ACH or SEPA.

- Real-time Settlement: Ensuring that when a customer pays, the merchant gets the money instantly.

We build unified payment gateways that manage multiple providers at once. This redundancy ensures that if one payment network goes down, the system automatically switches to another, keeping your services live 24/7.

3. KYC, AML, and identity verification tools

Identity checks are the “gatekeepers” of your platform. They must be fast enough to keep customers happy but tough enough to block criminals.

- Biometric Verification: Using face-matching and liveness checks to prove the user is real.

- Sanctions Screening: Automatically checking new users against global watchlists in real-time.

- Document Scanning: Using AI to verify passports and IDs from over 200 different countries.

By integrating top-tier tools like Onfido or Sumsub, we automate the heavy lifting of compliance. This allows you to onboard thousands of users daily without needing a massive team to check every ID manually.

4. Credit bureaus and risk data providers

If your platform offers loans or credit cards, you need accurate data to decide who to trust. Connecting to credit bureaus provides the “financial resume” of your users.

- Traditional Scoring: Pulling data from giants like Experian or TransUnion for official credit scores.

- Alternative Data: Using “open banking” to see a user’s actual spending habits and utility payment history.

- Dynamic Underwriting: Updating a user’s credit limit automatically based on their recent financial behavior.

We help you build “hybrid” risk models. By combining traditional bureau data with real-time cash flow analysis, your platform can safely lend to “thin-file” customers that traditional banks often ignore.

5. Regulatory and reporting systems

Banks are required by law to send frequent reports to the government. A professional platform automates this process so you never miss a deadline.

- Automated Filing: Generating tax and transaction reports in the exact format regulators require.

- Audit Logs: Keeping a permanent, unchangeable record of every single action taken on the platform.

- Suspicious Activity Reports (SARs): Automatically flagging unusual transactions for your compliance officer to review.

We implement “RegTech” (Regulatory Technology) that stays updated with changing laws. This ensures that as banking rules evolve, your platform updates itself automatically, keeping your business safe and compliant.

Integrating these systems correctly transforms a simple app into a high-performance financial engine. Consequently, you create a platform that banks can trust with their most sensitive operations.

Compliance Challenges in Platform Development

Navigating the regulatory landscape is the most significant hurdle in fintech. For investors, a single compliance failure can result in massive fines or a total shutdown of the platform.

Therefore, understanding these risks and how to neutralize them is the difference between a successful venture and a legal liability.

1. Managing multi-region regulatory requirements

The Challenge: Banking laws change the moment you cross a border. What is legal in the UK may not meet requirements in the US. Keeping up with these shifting rules manually is nearly impossible for a growing company.

How We Fix It: We build “regulatory flexibility” into the software architecture. Our system uses a modular compliance engine that can be toggled based on the user’s location. This means the platform automatically applies the correct legal rules, such as GDPR in Europe or CCPA in California, without needing to rewrite the core code.

2. Data privacy and security compliance needs

The Challenge: Banks handle the most sensitive data on earth. A data leak destroys trust forever. Regulators demand that this data is not only encrypted but also stored and accessed according to very strict standards like SOC2 and ISO 27001.

How We Fix It: We implement a “Zero Trust” security model. This means that every person and device trying to access the platform must be verified at every step. We use high-level AES-256 encryption for data at rest and in transit, ensuring that even if data is intercepted, it remains unreadable to hackers.

3. Real-time monitoring and audit readiness

The Challenge: Regulators now expect you to be “audit-ready” at all times. If you cannot produce a clear record of every transaction and system change within minutes, you risk losing your license.

How We Fix It: We install an automated “Always-On” audit trail. Every single action taken by a user or an admin is recorded in a permanent, tamper-proof log. We also provide a dedicated “Regulator Dashboard” that allows authorized officials to see the reports they need without having to ask your team for help.

4. Third-party risk and vendor dependencies

The Challenge: Most white-label platforms rely on third parties for things like KYC or cloud hosting. If one of these partners has a security breach or goes out of business, your entire platform could go down with them.

How We Fix It: We use a “Multi-Vendor Strategy” to remove single points of failure. Our platform is designed to switch between different service providers instantly. If your primary KYC provider has an outage, the system automatically redirects to a backup, ensuring your bank partners never experience a second of downtime.

Facing these challenges alone is the primary reason most fintech projects fail before they even launch. By solving for compliance at the code level, we turn a major business risk into a powerful competitive advantage.

Conclusion

Building a white-label fintech platform rests on control, compliance, and long-term scalability. Banks that invest in the right architecture avoid costly rebuilds and fragmented systems later. The real advantage lies in launching faster while staying fully aligned with regulatory and operational needs.

With the right partner, enterprises can move from idea to a fully functional, bank-ready platform without unnecessary complexity or risk.

Why Banks Choose Intellivon To Build A White-Label Platform

At Intellivon, white-label fintech platforms are built as enterprise financial infrastructure, and not as standalone products. The goal is to unify payments, lending, onboarding, and compliance into one scalable system.

Each platform is tailored to your operations and integrates with core banking, KYC/AML, and payment systems without disrupting workflows. This enables faster launches and better control.

Our approach combines modular architecture, API-first design, and cloud-native systems to ensure scalability, flexibility, and long-term performance.

Why Build With Intellivon

- Infrastructure-First Architecture: Built to replace fragmented systems, not layer over them

- Deep Banking Workflow Alignment: Designed for real lending, payments, and compliance flows

- Faster Time-to-Market: Launch fintech platforms 40–60% faster

- API-First Integration: Seamless connectivity with banking and fintech ecosystems

- Multi-Tenant & White-Label Ready: Full control over branding and product configurations

- Compliance by Design: Supports AML, KYC, GDPR, and regulatory reporting from day one

- Scalable Cloud Infrastructure: Built to handle growth across regions and products

- Real-Time Data & Decision Systems: Enables faster processing and smarter operations

- Dedicated Engineering Support: Continuous optimization, scaling, and system evolution

Build a Bank-Ready White-Label Platform With Intellivon

You’ve seen how complexity, compliance, and integrations shape platform success. The difference lies in building it right from day one.

Build your white-label fintech platform with confidence. Book a strategy call to get a tailored cost estimate and roadmap.

FAQs

Q1. What is a white-label fintech platform?

A1. A white-label fintech platform is a customizable financial system that enterprises can brand as their own. It is built on pre-developed infrastructure but tailored to specific workflows, integrations, and compliance needs. Unlike SaaS tools, it gives banks full control over features, user experience, and operations while accelerating time-to-market.

Q2. How long does development take?

A2. Development timelines depend on complexity and integrations. A basic platform can take 3–5 months, while a full-scale, enterprise-grade system typically takes 6–12 months. Timelines also vary based on compliance requirements, customization depth, and the number of financial products being deployed.

Q3. What integrations are required?

A3. A white-label fintech platform integrates with multiple systems, including core banking platforms, payment gateways, card networks, KYC/AML providers, and credit bureaus. It may also connect with regulatory reporting tools and third-party APIs to support lending, onboarding, and transaction processing workflows.

Q4. Is it compliant across regions?

A4. Yes, but compliance depends on how the platform is built. Enterprise-grade platforms are designed to support regulations like GDPR, PCI-DSS, and AML/KYC frameworks. Multi-region compliance requires additional configurations for local regulatory requirements, reporting standards, and data handling policies.

Q5. How much does it cost to build?

A5. The cost typically ranges from $70,000 to $180,000+, depending on features, integrations, and scalability requirements. Platforms with advanced compliance, multi-product capabilities, and deep integrations require higher investment but reduce long-term operational and rebuild costs.