Key Takeaways

-

AI fintech platforms must satisfy AML, KYC, sanctions, data privacy, AI governance, and PCI DSS across multiple jurisdictions from day one.

-

The EU AI Act classifies most fintech AI as high-risk, requiring explainability, model inventories, and human oversight before deployment.

-

Compliance embedded at the architecture level through policy-as-code costs far less than retrofitting it after regulatory scrutiny.

-

AI transforms KYC, AML, fraud, and credit scoring from static rule checks into continuous, self-improving risk layers.

-

How Intellivon builds compliance-first AI fintech infrastructure connecting AML, sanctions, fraud models, and audit trails into one real-time system your enterprise fully owns.

AI fintech infrastructure faces more regulatory pressure than most technology categories. This is because financial services regulators, data protection authorities, and AI governance bodies are all pushing their requirements forward at the same time, across various regions, each with different enforcement focuses. The compliance landscape evolves as platforms grow, new markets emerge, and regulators clarify their expectations for how AI systems handle financial decisions.

This is why compliance architecture has become essential for AI fintech platforms to integrate. Integrating the right frameworks from the beginning, including AML obligations, data protection laws, AI model governance, and licensing requirements, enables platforms to expand into new markets without expensive rebuilds. At the same time, viewing compliance as infrastructure, instead of a legal check at the end, distinguishes platforms designed for long-term growth from those that falter before achieving enterprise scale.

Intellivon has designed and delivered AI fintech platforms for businesses operating in regulated markets worldwide, incorporating compliance directly into the infrastructure from the initial design through deployment. This blog draws on that experience to outline the key compliance areas relevant to AI fintech infrastructure, helping founders and investors make informed decisions before starting their projects.

Why Compliance Can Make or Break AI Fintech Platforms

Modern AI fintech compliance utilizes “Compliance-as-Code” to integrate regulatory checks directly into the CI/CD pipeline, ensuring every model update is pre-validated for bias and transparency before deployment.

Compliance is the foundation on which every serious AI fintech platform is built, and the firms that treat it that way from the start are the ones that scale with confidence, earn regulatory trust, and attract the calibre of investors and partners that accelerate long-term growth.

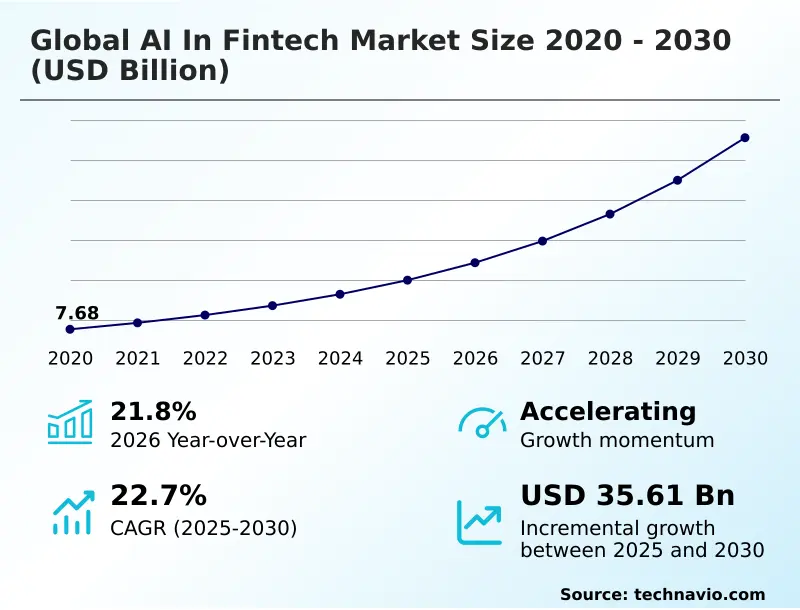

The AI in the fintech market is projected to grow by USD 35.61 billion at a CAGR of 22.7% between 2025 and 2030, which is a trajectory that reflects how decisively capital and enterprise adoption are moving toward AI-powered financial infrastructure.

1. AI decisions now carry regulatory liability

AI actively approves loans and flags trades now instead of just being a passive tool. Consequently, every automated decision becomes a permanent, auditable record that regulators scrutinize.

At the same time, entities like the Securities and Exchange Commission now demand full traceability, meaning “the black box said so” is no longer a legal defense.

2. Non-compliance creates immediate financial risk

Regulatory friction translates directly to drained capital through heavy fines or frozen banking licenses. Furthermore, partners often sever ties instantly if they detect compliance gaps, leading to halted operations.

Consequently, this operational paralysis destroys market reputation and scares away future institutional investors.

3. AI introduces new compliance challenges

Machine learning models often evolve beyond their original programming, creating “black-box” scenarios that lack explainability. If an adaptive model develops bias in credit scoring, it violates fair lending laws.

Additionally, adhering to NIST AI risk guidance is now essential to ensure these systems remain predictable and fair.

4. Legacy compliance models cannot support AI systems

Static, rule-based audits fail because they cannot track the fluid nature of neural networks. Manual reviews are simply too slow for platforms processing thousands of instant transactions.

At the same time, relying on disconnected legacy systems creates visibility gaps that leave your infrastructure vulnerable to undetected systemic errors.

5. Global regulations are tightening around AI fintech

The EU AI Act and similar global frameworks are setting strict boundaries for financial algorithms. Regulators are increasing scrutiny, requiring platforms to adapt their codebases to meet cross-border standards.

Hence, continuous adaptation is the only way to maintain a competitive, global fintech presence.

AI fintech compliance is no longer a checklist handled after deployment. It defines how the system is designed, how decisions are made, and how platforms scale under regulatory scrutiny.

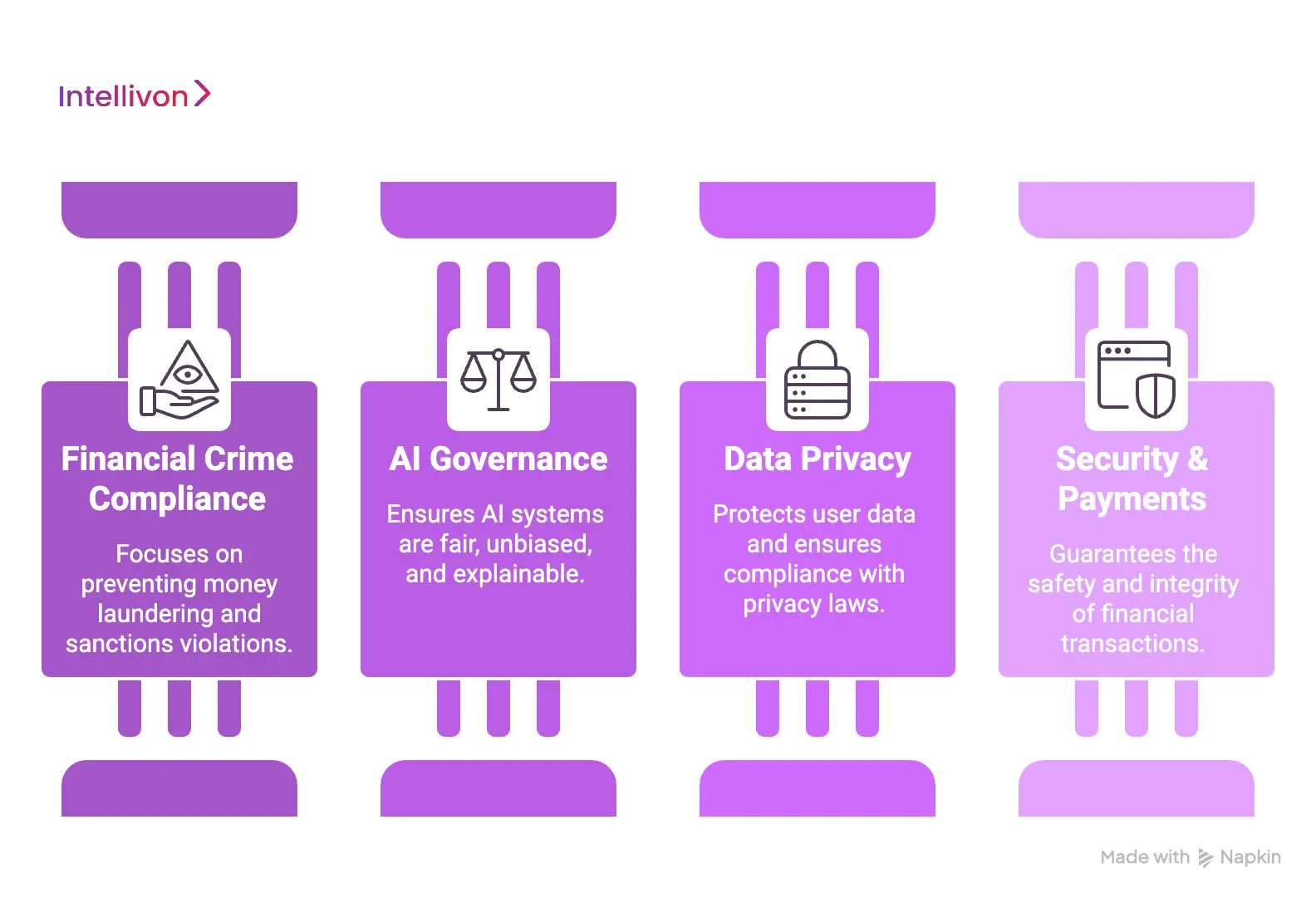

What Compliance Applies to AI Fintech Systems?

Building an enterprise-grade AI fintech platform requires balancing multiple regulatory layers simultaneously. Consequently, stakeholders must view compliance as a multidimensional matrix rather than a simple checklist.

The following table provides a high-level overview of the primary domains you must navigate to ensure platform viability.

| Compliance Domain | Primary Focus | Key Regulators/Frameworks |

| Financial Crime | AML, KYC, and Sanctions | FATF, OFAC, FinCEN |

| AI Governance | Bias, Fairness, and Explainability | EU AI Act, NIST AI RMF |

| Data Privacy | User Rights and Data Locality | GDPR, CCPA, Digital Personal Data Protection |

| Security & Payments | Transaction Safety and Data Integrity | PCI DSS, SOC 2, ISO 27001 |

1. Financial crime compliance: AML, KYC, and CTF

Anti-Money Laundering (AML) and Know Your Customer (KYC) protocols form the bedrock of financial integrity. Furthermore, the Financial Action Task Force (FATF) sets global standards that every platform must mirror.

- Customer Due Diligence: You must implement robust identity verification to ensure users are who they claim to be.

- Transaction Monitoring: AI must flag suspicious patterns in real time to prevent money laundering or terrorist financing (CTF).

- Risk Profiling: Systems should continuously assess user behavior to update risk scores dynamically.

2. Sanctions screening and watchlist checks

Global platforms must prevent prohibited entities from accessing financial rails. Therefore, your infrastructure must integrate real-time screening against international databases.

- Watchlist Integration: Automatically screen every participant against OFAC, UN, EU, and UK sanctions lists.

- PEP Identification: Identify Politically Exposed Persons (PEPs) who require enhanced due diligence.

- Risk Intelligence: Use adverse media checks to spot reputational risks before they enter your ecosystem.

3. Consumer protection and fair use regulations

Regulators are increasingly focused on how AI affects the end consumer. Consequently, your algorithms must be transparent and non-discriminatory to avoid legal repercussions.

- Fair Lending: You must ensure that credit models do not discriminate based on race, gender, or age.

- Adverse Action Notices: If an AI rejects a user, you are often legally required to provide a clear reason.

- Bias Mitigation: Regular audits are necessary to prove that your underwriting logic remains neutral.

4. AI model risk and governance requirements

Managing an AI model is different from managing traditional software. Specifically, the “black box” nature of deep learning requires specialized oversight.

- Model Validation: You must test models for performance and drift before they go live.

- Documentation: Maintain detailed logs of model logic to satisfy auditors during a review.

- Retraining Controls: Ensure that as models learn from new data, they do not deviate from safety parameters.

5. AI governance under global regulatory frameworks

The regulatory landscape is shifting from general finance laws to AI-specific mandates. For instance, the EU AI Act classifies many fintech applications as “high-risk.”

- Risk-Based Controls: Implement stricter oversight for systems that impact a user’s financial livelihood.

- Explainability: You must be able to explain how an automated system reached a specific conclusion.

- Human Oversight: Maintain “human-in-the-loop” protocols for high-stakes financial decisions.

6. Data privacy, consent, and user rights

Data is the fuel for AI, but it is also a massive liability. Therefore, strict adherence to the General Data Protection Regulation (GDPR) is mandatory for global operations.

- Data Minimization: Only collect the specific data points required for the transaction.

- Consent Management: Users must have clear, granular control over how their data is used for AI training.

- Localization: Some jurisdictions require that financial data stay within national borders.

7. Payment compliance and transaction controls

If your platform moves money, you must enforce compliance at the point of execution. However, this must happen without adding friction to the user experience.

- Onboarding Enforcement: Block access immediately if KYC requirements are not met during signup.

- Live AML Checks: Run screening protocols within the milliseconds it takes to authorize a payment.

- Multi-Rail Safety: Ensure consistent checks across card networks, ACH, and Real-Time Payments (RTP).

8. PCI DSS and payment data security standards

Handling credit card information requires strict physical and digital security. Consequently, the Payment Card Industry Data Security Standard (PCI DSS) is non-negotiable.

- Tokenization: Replace sensitive card data with unique identifiers to reduce your attack surface.

- Encryption: Secure data both at rest and during transit using enterprise-grade protocols.

- Access Logging: Maintain strict records of every employee or system that interacts with payment data.

9. Open banking and strong auth requirements

Open banking allows for better AI insights but introduces new security risks. Therefore, you must implement Strong Customer Authentication (SCA) under frameworks like PSD2.

- API Security: Use secure, encrypted gateways for third-party data sharing.

- Consent Frameworks: Ensure users explicitly authorize every instance of data retrieval.

- Multi-Factor Auth: Require at least two forms of verification for high-value transactions.

10. Cybersecurity, SOC 2, and ISO standards

General security certifications build trust with institutional partners and investors. Moreover, they prove that your internal processes are mature and reliable.

- SOC 2 Type II: This demonstrates that you maintain high standards for security, availability, and privacy over time.

- ISO 27001: Adopting this international standard ensures a systematic approach to managing sensitive company information.

- Incident Response: You must have a pre-defined plan to detect and neutralize threats instantly.

11. Third-party and vendor risk management

Modern fintechs rely on an ecosystem of APIs and vendors. However, you remain legally responsible for their failures.

- Vendor Audits: Regularly review the compliance certifications of your KYC or fraud partners.

- Dependency Mapping: Know exactly which external systems your AI relies on to avoid single points of failure.

- Performance Monitoring: Track if vendor latency is impacting your real-time compliance checks.

AI fintech compliance is not a single framework or regulation. It spans financial crime, data protection, AI governance, infrastructure security, and operational resilience. The real challenge is designing systems where all these requirements work together in real time.

What AI Rules Matter Most for Fintech Infrastructure?

Navigating the intersection of finance and AI requires a deep understanding of emerging regulatory standards. Consequently, infrastructure must be designed to withstand scrutiny from both traditional financial auditors and new AI-specific oversight bodies.

Therefore, success depends on moving beyond general software testing toward a rigorous, model-centric governance framework.

1. Classifying AI models by financial risk level

Not all algorithms carry the same weight under regulatory scrutiny. For instance, a recommendation engine for UI themes is low-risk, while an automated mortgage approval system is high-risk.

Therefore, your first step is to categorize every model based on its potential to cause financial harm or systemic instability.

2. Mapping EU AI Act duties to fintech use cases

The EU AI Act is the gold standard for global algorithmic accountability. Specifically, many fintech applications are now classified as “high-risk,” requiring mandatory third-party assessments and strict data quality controls.

Furthermore, you must ensure your architecture supports these standards to avoid massive turnover in European markets.

3. Applying NIST govern, map, measure, and manage

The NIST AI Risk Management Framework (RMF) provides a non-prescriptive yet rigorous methodology for handling model uncertainty.

- Govern: Build a culture where compliance is integrated into the development lifecycle.

- Map: Identify specific risks and dependencies before a single line of code goes live.

- Measure: Use quantitative metrics to track bias, accuracy, and safety vulnerabilities.

- Manage: Prioritize and mitigate risks based on their potential business impact.

4. Building model inventories for every AI system

Regulators now expect a comprehensive “Asset Register” for your algorithms. This inventory must track every model version, its intended use, and its current performance status.

Moreover, having this centralized view allows your compliance team to react instantly to new legislative updates.

5. Validating credit, fraud, AML, and routing models

Validation is a continuous obligation, not a one-time event at launch. You must stress-test your models against diverse datasets to ensure they remain robust under shifting market conditions.

For example, a fraud model must be proven effective against new types of synthetic identity theft.

6. Logging training data, features, and model versions

Reproducibility is a core requirement for any serious regulatory audit. You must be able to prove exactly what data influenced a specific model version at any given time.

Consequently, your infrastructure should automatically log every feature and hyperparameter to create a transparent “paper trail” for examiners.

7. Creating human review paths for high-risk decisions

Total autonomy is a significant regulatory liability in high-stakes finance. Therefore, your system must include “circuit breakers” that escalate questionable or high-value outcomes to a human professional.

This hybrid approach ensures that the efficiency of AI is balanced by expert human judgment.

Robust AI governance ensures your platform remains compliant as international regulations evolve. This structured approach transforms compliance from a cost center into a significant competitive advantage.

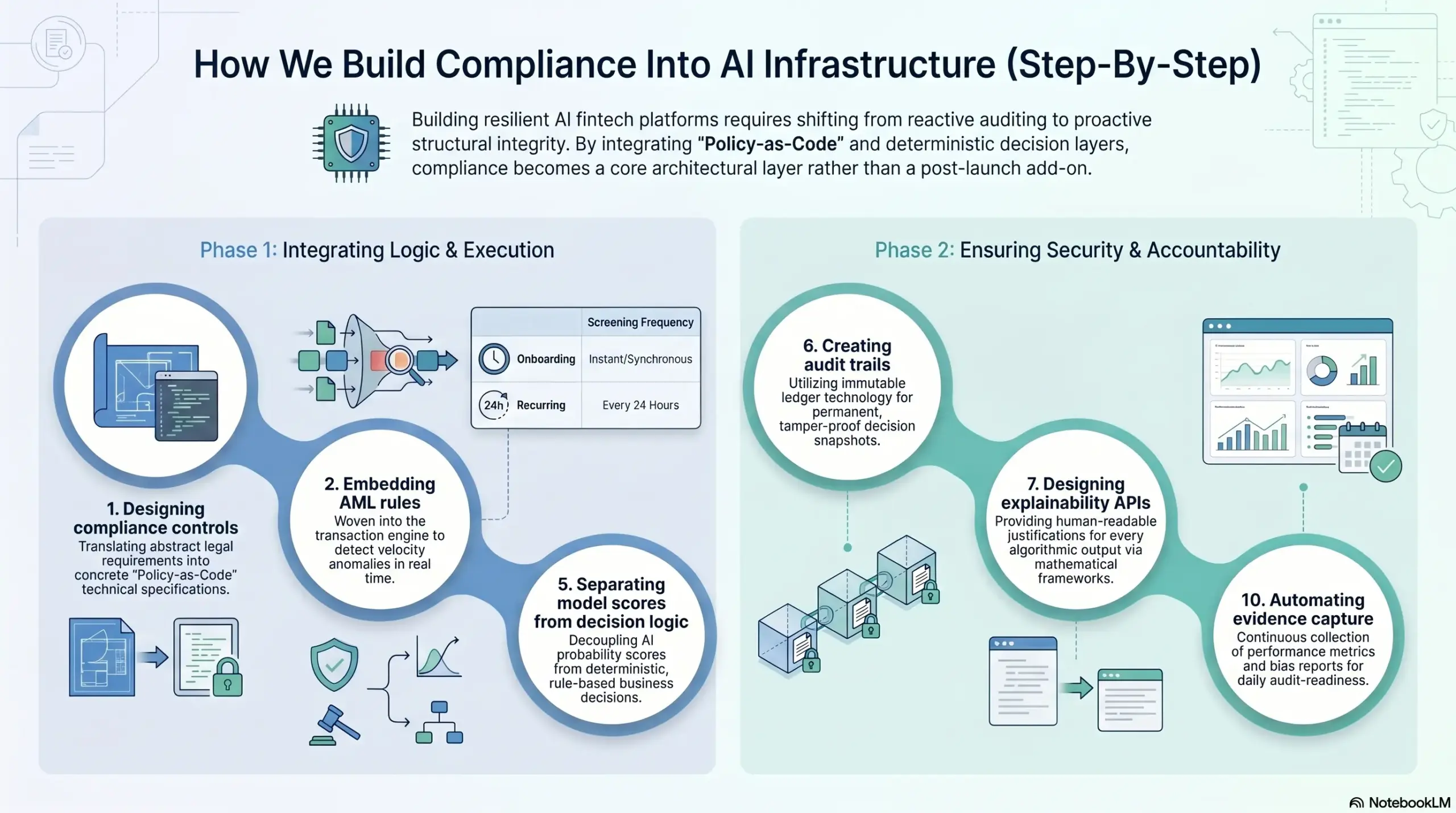

How We Build Compliance Into AI Infrastructure (Step-By-Step)

Building a resilient AI fintech platform requires shifting from reactive auditing to proactive, structural integrity. Consequently, we integrate regulatory requirements directly into the engineering lifecycle. This approach ensures that every transaction is pre-validated against global standards before execution.

1. Designing compliance controls

We begin by translating abstract legal requirements into concrete technical specifications. Therefore, our team utilizes “Policy-as-Code” to ensure that compliance rules are version-controlled and testable.

- Requirement Mapping: We map specific jurisdictional mandates to automated gatekeepers within your CI/CD pipeline.

- Threshold Management: Specifically, we define clear risk appetites that trigger “circuit breakers” during high-volatility events.

| Control Aspect | Implementation Method |

| Logic Storage | Git-based versioning |

| Enforcement | Automated API Gateways |

2. Embedding AML rules

Anti-Money Laundering (AML) protocols must be woven into the fabric of the transaction engine. However, we ensure these rules adapt to emerging patterns of synthetic identity fraud and layering.

- Pattern Recognition: We deploy AI models that detect velocity anomalies and structuring attempts in real time.

- FATF Standards: Furthermore, our systems align with Financial Action Task Force recommendations for cross-border monitoring.

3. Running sanctions checks

Global infrastructure must verify every participant against international watchlists. Consequently, we implement low-latency screening APIs that run during the initial handshake of a transaction.

- Watchlist Syncing: We maintain live connections to OFAC, UN, and EU lists to ensure no prohibited entity gains access.

- PEP Identification: Our logic identifies Politically Exposed Persons (PEPs) to trigger enhanced due diligence workflows automatically.

| Screening Type | Frequency |

| Onboarding | Instant/Synchronous |

| Recurring | Every 24 Hours |

4. Adding policy engines

A centralized policy engine acts as the “brain” for regulatory decision-making. Therefore, we ensure that every business rule is centralized rather than scattered across different microservices.

- Granular Logic: We enable you to update compliance rules across different regions without redeploying the entire codebase.

- Conflict Resolution: Specifically, the engine manages overlapping regulations when transactions cross multiple borders.

5. Separating model scores from decision logic

To avoid “black box” liabilities, we strictly decouple the AI’s probability score from the final business decision. Consequently, the AI predicts risk, but a transparent, rule-based layer determines the outcome.

- Inference vs. Execution: The AI provides a risk score; however, a deterministic policy layer enforces the actual “Approve” or “Deny” action.

- Bias Mitigation: This separation allows us to override model outputs that show signs of demographic drift or unfair underwriting.

6. Creating audit trails

Every automated action must leave a permanent, tamper-proof footprint. Therefore, we utilize immutable ledger technology to store transaction metadata and decision snapshots.

- Event Sourcing: We capture the exact state of the system, including model versions and input data, at the moment a decision occurred.

- Regulator-Ready Exports: Specifically, these logs are designed to be exported directly into formats required by financial examiners.

| Trail Element | Technology |

| Storage | WORM (Write Once Read Many) |

| Integrity | Cryptographic Hashing |

7. Designing explainability APIs

Transparency is a core requirement under the EU AI Act. Consequently, we build dedicated APIs that provide human-readable justifications for every algorithmic output.

- SHAP/LIME Integration: We use advanced mathematical frameworks to pinpoint which specific features led to a rejection.

- Adverse Action Notices: Furthermore, our systems automatically generate the legal notices required when a consumer’s request is denied.

8. Encrypting sensitive data

Protecting cardholder and personal data is a non-negotiable security pillar. Therefore, we implement end-to-end encryption and tokenization to minimize the impact of any potential breach.

- PCI DSS Compliance: We ensure that sensitive credit card data is never stored in plain text within your AI environment.

- Data Masking: Specifically, we use anonymization techniques so that AI models can learn from data without exposing PII.

9. Building role-based access

Security is maintained through the principle of least privilege. Consequently, we design infrastructure where access to sensitive compliance controls is strictly monitored and limited.

- Granular Permissions: We distinguish between the data scientists who train models and the compliance officers who set the rules.

- MFA Integration: Furthermore, every high-level system change requires multi-factor authentication and a secondary “peer review” approval.

10. Automating evidence capture

Manual data gathering for audits is a significant operational drain. Therefore, we automate the collection of compliance evidence, ensuring you are “audit-ready” every day.

- Real-time Snapshots: We capture performance metrics, bias reports, and security logs as they happen.

- Continuous Compliance: Specifically, this shifts your posture from an annual panic to a sustained state of regulatory readiness.

| Evidence Type | Capture Trigger |

| Bias Report | Weekly/Monthly |

| Model Drift | Real-time Alert |

At Intellivon, we treat compliance as a core architectural layer rather than a post-launch add-on. This systematic integration allows your platform to scale globally while maintaining the highest standards of financial integrity.

How AI Changes Core Fintech Compliance Workflows

AI transforms compliance from a static verification step into a dynamic, learning process. Consequently, these optimized workflows allow platforms to handle massive transaction volumes while simultaneously reducing false positives and manual intervention.

Therefore, modernizing these core functions is essential for any enterprise looking to maintain high-speed financial operations.

1. KYC systems with risk-based identity verification

Traditional identity verification often relies on rigid, manual checks that create user friction.

However, AI-driven Know Your Customer (KYC) systems utilize risk-based scoring to determine the depth of verification required for each user.

- Dynamic Friction: Low-risk users enjoy a seamless onboarding experience, while high-risk profiles trigger automated requests for additional documentation.

- Liveness Detection: Specifically, we integrate biometric AI to detect deepfakes or spoofing attempts during the selfie verification stage.

| Workflow Component | AI Enhancement |

| Document Verification | OCR and forgery detection |

| User Risk Level | Probabilistic scoring models |

2. AML systems with behavioral transaction scoring

Static rules often fail to catch sophisticated money laundering techniques like “structuring” or “smurfing.”

Consequently, AI-based Anti-Money Laundering (AML) systems shift the focus toward long-term behavioral patterns rather than isolated events.

- Anomaly Detection: Our models identify deviations from a user’s “normal” spending habits, flagging suspicious velocity changes instantly.

- Network Analysis: Furthermore, AI can visualize complex relationships between accounts to spot laundering rings that manual audits would miss.

3. Fraud engines with real-time risk orchestration

Fraud detection must be fast enough to block a transaction before it clears. Therefore, we implement real-time orchestration layers that combine internal data with external threat intelligence.

- Feature Engineering: We track thousands of data points, such as IP reputation and device fingerprinting, to calculate a fraud score in milliseconds.

- Adaptive Learning: Specifically, the engine learns from every successful and blocked attempt to harden your platform’s defenses against new attack vectors.

4. Credit models with explainable approval logic

Underwriting in the AI era requires a balance between predictive power and transparency. Consequently, we move beyond simple FICO scores to incorporate alternative data while maintaining strict adherence to fair lending laws.

- Feature Transparency: We utilize explainability frameworks to ensure that credit decisions are based on legally permissible variables.

- Bias Auditing: Therefore, we run continuous simulations to ensure that the scoring logic does not inadvertently discriminate against protected groups.

| Credit Feature | Compliance Safeguard |

| Alternative Data | Strict purpose limitation |

| Decision Output | Automated Adverse Action Notices |

5. Payment routing with compliance-aware rail selection

Routing capital across different rails, such as ACH, SWIFT, or RTP, requires navigating diverse regulatory landscapes. Consequently, building “compliance-aware” routing logic selects the optimal path based on regional laws and risk profiles.

- Sanctions Interception: The system automatically diverts or blocks payments destined for jurisdictions under heavy regulatory scrutiny.

- Cost vs. Risk: Specifically, we balance transaction speed with the necessary compliance overhead required for each specific payment rail.

6. Merchant risk systems with continuous monitoring

For B2B platforms, risk management does not end at onboarding. Therefore, implementing continuous monitoring systems tracks merchant health and transaction patterns to prevent high-volume fraud.

- Sentiment Analysis: We can monitor adverse media and public filings to flag merchants facing financial or legal distress.

- Threshold Alerts: Furthermore, automated alerts trigger if a merchant’s chargeback ratio exceeds industry-standard safety limits.

7. Wallet and ledger controls for regulated balances

Managing digital wallets requires precise accounting of “commingled” and “segregated” funds. Consequently, embedding compliance logic into the ledger itself ensures that balances are handled according to money transmitter laws.

- Immutable Tracking: Every balance movement is recorded in a tamper-proof ledger, ensuring an accurate audit trail for financial examiners.

- Automated Reconciliation: Specifically, we use AI to match ledger entries against bank statements, identifying discrepancies before they become liabilities.

8. Dispute and chargeback workflows with audit trails

Handling disputes effectively is a core requirement for maintaining card network compliance. Therefore, we automate the collection of evidence to ensure that every chargeback response is backed by robust data.

- Evidence Aggregation: The system automatically pulls transaction logs, IP addresses, and shipping confirmations to build a defensible case.

- Workflow Tracking: Furthermore, we maintain a complete history of every communication and decision, ensuring you are prepared for any regulatory review or network audit.

| Dispute Phase | Automation Strategy |

| Intake | Natural Language Processing (NLP) |

| Resolution | Automated evidence submission |

By modernizing these workflows, your platform gains the ability to scale into new markets with minimal manual overhead. This transformation ensures that compliance becomes an enabler of speed rather than a barrier to growth.

Examples of Leading Compliance-First AI Fintech Companies

Examining market leaders reveals that the most successful AI fintech platforms do not treat compliance as a secondary feature. Instead, they leverage regulatory rigor as a core value proposition to win enterprise contracts and secure banking partnerships.

Consequently, these companies serve as benchmarks for how to scale sophisticated AI models within strictly regulated environments.

1. Stripe: The gold standard in global risk orchestration

Stripe has built a multi-billion-dollar ecosystem by abstracting the complexity of global financial regulations. Therefore, they allow businesses to scale internationally without worrying about local licensing or tax compliance.

- Stripe Radar: This AI-powered fraud engine processes trillions of data points across the entire Stripe network to block fraud in real time.

- Global Identity: Furthermore, their identity verification systems adapt dynamically to the local KYC requirements of over 30 countries.

2. Adyen: Single-platform compliance for global merchants

Adyen’s success stems from its “single platform” approach, which eliminates the need for fragmented third-party compliance tools. Consequently, they provide end-to-end visibility across the entire payment lifecycle.

- RevenueProtect: This system uses machine learning to balance fraud prevention with high conversion rates, ensuring legitimate transactions are never blocked.

- Automated KYC: Specifically, Adyen automates the complex merchant onboarding process while remaining fully compliant with regional AML directives.

3. Revolut: Scaling AI compliance for retail and business

As a neobank operating in dozens of countries, Revolut relies heavily on AI to manage its vast regulatory obligations. Therefore, they have pioneered the use of automated systems to monitor millions of transactions daily.

- AI-Driven AML: Their algorithms identify suspicious patterns far more accurately than traditional rule-based systems, reducing manual review times.

- Real-time Sanctions: Specifically, Revolut integrates instant screening for all cross-border transfers to ensure compliance with shifting global watchlists.

4. Affirm: Explainable AI in consumer lending

Affirm has disrupted the “Buy Now, Pay Later” space by prioritizing transparency and fair lending. Consequently, their AI models are designed to be fully explainable to both consumers and regulators.

- Fair Underwriting: They use machine learning to assess creditworthiness without relying on biased traditional metrics.

- Regulatory Transparency: Furthermore, Affirm provides clear, automated disclosures to users, satisfying consumer protection laws regarding loan terms.

These industry leaders demonstrate that an “AI-first, compliance-first” mentality is the only sustainable path forward.

How to Future-Proof Compliant AI-Fintech Systems

Regulatory landscapes shift rapidly, and failing to anticipate these changes can result in costly infrastructure overhauls. Consequently, entrepreneurs must build with modularity and foresight to ensure their platforms remain resilient.

Therefore, the goal is to create a compliance layer that evolves as quickly as the AI it governs.

1. Designing for changing AI regulations from day one

You must assume that the laws governing your platform today will be obsolete within twenty-four months. However, by adopting a “Compliance-by-Design” philosophy, you ensure that every architectural decision accounts for future oversight.

- Modular Frameworks: We build systems where regulatory modules can be swapped or updated without touching the core payment logic.

- Agile Governance: Specifically, we implement flexible data schemas that can accommodate new reporting requirements as they emerge.

| Future-Proofing Strategy | Operational Benefit |

| Modular Architecture | Zero-downtime compliance updates |

| Schema Flexibility | Rapid adaptation to new data laws |

2. Updating rules without rebuilding core systems

Infrastructure rigidity is the primary enemy of scalability. Therefore, we utilize headless compliance engines that allow your legal team to modify business logic via a dashboard rather than through code deployments.

- Versioned Rules: Every update to your compliance logic is version-controlled, allowing for instant rollbacks if a new rule causes unexpected friction.

- Shadow Testing: Furthermore, we allow you to run new compliance rules in “shadow mode” against live data to test their impact before full enforcement.

3. Preparing for stricter AI model accountability

The shift toward “white-box” AI is inevitable as regulators demand deeper insights into algorithmic decisions. Consequently, you must invest in infrastructure that supports comprehensive model lineage and metadata tracking.

- Automated Lineage: We track exactly which datasets and weights were used in every model iteration to satisfy future audit requirements.

- External Auditing Hooks: Specifically, we provide secure access points for third-party auditors to verify model fairness without exposing your intellectual property.

4. Supporting stablecoins and tokenized settlement rails

As the industry moves toward blockchain-based settlement, your compliance stack must bridge the gap between fiat and digital assets. Therefore, we integrate on-chain monitoring tools directly into your traditional AML workflows.

- Multi-Asset Compliance: Our systems handle both traditional ACH/SWIFT rails and tokenized assets within a single unified interface.

- Liquidity Monitoring: Furthermore, we implement real-time tracking of digital asset reserves to ensure your platform meets emerging stablecoin regulations.

5. Managing on-chain and off-chain compliance together

Hybrid systems introduce unique risks where traditional identity data meets pseudonymous blockchain transactions. Consequently, we create a unified identity layer that links off-chain KYC data with on-chain wallet behavior.

- Cross-Chain Intelligence: We utilize AI to analyze wallet clusters and identify high-risk on-chain activity before it touches your platform.

- Unified Reporting: Specifically, we consolidate these disparate data streams into a single, regulator-ready report.

| Data Source | Compliance Treatment |

| Off-Chain (KYC) | Standard PII protection |

| On-Chain (Wallet) | Behavioral risk scoring |

6. Building controls for agent-led payment decisions

The rise of autonomous AI agents requires a new set of “delegated authority” controls. Therefore, we implement strict spending limits and intent-verification layers for agent-initiated transactions.

- Dynamic Permissions: We allow users to set granular permissions for what an AI agent can and cannot purchase on their behalf.

- Human-in-the-Loop Triggers: Specifically, high-value or high-risk agent decisions are automatically escalated for human approval.

7. Scaling governance across new markets and products

Expanding into a new country should not mean starting your compliance journey from scratch. Consequently, we build “localization templates” that allow you to replicate your governance structure while tweaking only the necessary local variables.

- Regional Templates: Quickly adapt your core fraud and AML logic to meet the specific requirements of the MAS, FCA, or RBI.

- Product Portability: Furthermore, your existing compliance data can be leveraged to launch new products, such as lending or insurance, with minimal delay.

8. Keeping audit evidence ready as systems evolve

Auditors want to see your history. Therefore, we automate the archival of every compliance state, ensuring you can “time travel” back to any specific day for an audit.

- Immutable Snapshots: We take regular, cryptographic snapshots of your entire compliance posture and store them in a tamper-proof environment.

- Self-Service Portals: Specifically, we provide a secure portal for regulators to access historical evidence, reducing the manual burden on your engineering team.

By focusing on these future-proofing strategies, you transform compliance from a reactive burden into a scalable asset. This approach ensures that your platform remains a leader in the next generation of AI-driven financial services.

Conclusion

Strategic compliance is the ultimate bridge between innovative AI and sustainable financial growth. By embedding regulatory controls directly into your core infrastructure, you transform legal necessity into a powerful competitive moat.

This proactive approach secures institutional trust and simplifies global expansion. Ultimately, the future belongs to platforms that treat algorithmic accountability not as a final hurdle, but as the foundational architecture for long-term enterprise success.

Build AI-Powered Fintech Systems With Intellivon

Building an AI-powered transaction monitoring system needs a connected financial crime intelligence layer where transaction data, AML rules, sanctions signals, fraud patterns, AI models, case workflows, and audit trails work together in real time.

At Intellivon, we build transaction monitoring systems for fintech platforms, PSPs, digital banks, wallets, lenders, marketplaces, BaaS providers, and embedded finance companies. Our systems help teams detect suspicious activity earlier, reduce false positives, speed up investigations, and stay audit-ready as they scale.

A. Designing Real-Time Monitoring Architecture

Transaction monitoring must happen while activity is still actionable. We design systems that screen transactions, users, merchants, accounts, wallets, and counterparties before risk turns into regulatory exposure.

- Real-time transaction ingestion: Payment, wallet, card, transfer, merchant, and ledger activity enters the system instantly.

- Unified risk data layer: KYC, KYB, sanctions, fraud, device, location, and transaction history feed into one risk view.

- Low-latency monitoring APIs: Risk checks can run before payment approval, settlement, withdrawal, payout, or account action.

This ensures suspicious activity is detected during the transaction lifecycle, not after delayed reporting.

B. Building AI Risk Scoring Models

Rule-based monitoring can miss hidden patterns and create too many false positives. We build AI risk scoring systems that combine explainable rules with machine learning models.

- Dynamic risk scoring: Each transaction is scored using customer behavior, transaction context, geography, velocity, and counterparty risk.

- Anomaly detection models: AI identifies unusual spikes, new counterparties, changed device behavior, and abnormal activity patterns.

- Graph-based detection: The system maps linked users, accounts, merchants, and wallets to detect mule networks and layering patterns.

This helps compliance teams focus on meaningful risk instead of reviewing repetitive low-value alerts.

C. Connecting AML, Fraud, KYC, and Sanctions

Transaction monitoring works best when it connects the full compliance ecosystem. We build systems where AML checks, fraud signals, sanctions screening, and customer risk profiles work together.

- KYC and KYB integrations: Identity, business verification, ownership, and onboarding risk feed into monitoring logic.

- Sanctions and watchlist checks: Users, merchants, counterparties, wallets, and transactions are screened against sanctions, PEP, and adverse media data.

- Risk-based escalation: Low-risk activity can clear automatically, while higher-risk events move into review, hold, block, or escalation workflows.

This turns fragmented compliance checks into one connected financial crime monitoring system.

D. Creating Case and SAR Workflows

Alerts only create value when they lead to structured investigations. We build case workflows that help compliance teams review, document, escalate, and resolve suspicious activity.

- Investigation-ready queues: Related alerts are grouped by customer, merchant, account, typology, counterparty, or transaction pattern.

- Evidence capture: Each case stores triggered rules, model scores, transaction history, customer data, analyst notes, and review actions.

- SAR support: Case evidence and investigation notes can support suspicious activity reporting and regulatory reviews.

This gives teams a clear path from detection to investigation, decision, reporting, and audit review.

Whether you need an MVP monitoring layer, an AI risk scoring engine, AML workflow automation, a case management system, SAR support, or a full financial crime monitoring infrastructure, Intellivon can help you design, build, integrate, and scale it. Talk to our experts today and book your free strategy call.

FAQs

Q1. When does fintech compliance become an infrastructure problem?

A1. Fintech compliance becomes infrastructure when the platform must enforce controls automatically. This happens in workflows like payments, KYC, lending, refunds, AI decisions, and account changes, where audit logs, access control, human review, and evidence trails must exist inside the system.

Q2. What evidence is needed before launching AI in fintech?

A2. Before launching AI, fintech teams need evidence showing what data the AI accessed, what action it attempted, whether it touched PII or regulated workflows, and whether humans reviewed high-risk actions. The system must also produce audit trails after deployment.

Q3. How should enterprises manage AI fintech compliance at scale?

A3. Enterprises need compliance built into the architecture, not handled through manual reviews alone. This means automated controls for AML, sanctions, privacy, access, model governance, audit trails, escalation workflows, and regulator-ready reporting across every product, region, and transaction flow.

Q4. Why do AI fintech systems need explainability?

A4. AI fintech systems need explainability because teams must prove why decisions were made. For lending, fraud, KYC, and transaction monitoring, the platform should show inputs, rules, model scores, final actions, human overrides, and model versions.