The banking sector is racing toward AI transformation, but legacy systems remain its heaviest anchor. Mainframes designed in the 1970s and 1980s still run mission-critical operations in most global banks. Data shows that 37% of systems built on legacy technologies have below-average architecture ratings. This poor architecture slows change velocity, with weaker systems delivering updates 40% slower than those built on robust frameworks.

The solution is not tearing down legacy cores but intelligently integrating AI into existing infrastructure. This approach allows banks to modernize fraud detection, risk scoring, compliance automation, and customer engagement, all without disrupting the systems that already power global finance.

At Intellivon, we’ve delivered AI integrations that make legacy cores future-ready through secure APIs, data pipelines, and modular microservices. In this blog, we will explore how enterprises can bridge the old and the new by covering compliance frameworks, the costs, and the processes of integrating AI into legacy banking systems.

Legacy Banking’s $400T Annual Flows Need AI Integration

Legacy banking systems process more than $400 trillion annually, anchoring global finance. Their reliability is proven, but digital pressures are exposing cracks. With 94% of modernization projects facing delays or overruns, banks can’t afford full replacements.

The smarter path is AI integration, which is an adaptive layer that enhances efficiency and security while lowering the total cost of ownership by up to 52%.

Where the $400T Infrastructure Is Most at Risk

1. Middleware and API Integration

Legacy cores create bottlenecks during real-time data flows. IBM’s 2025 study shows middleware retrofits cost $3–6 million, but deliver 42% efficiency gains when optimized with AI.

2. Data Migration and Quality

Moving petabytes of data carries risks of loss and compliance breaches. Deloitte notes migration adds $1.2–2 million in overhead, while AI orchestration cuts errors by 73%.

3. Compliance and Security

Manual audits drain budgets. Gartner finds AI governance costs $400k–$800k annually, but reduces breaches by 37% and speeds reporting by 60%.

4. Talent and Scalability

Shortages of COBOL talent drive labor costs higher. McKinsey values technical debt at $14 per line of code. AI automation offsets this, improving throughput by 48%.

Key Takeaways of AI Trends in Banking

AI’s Impact on Banking

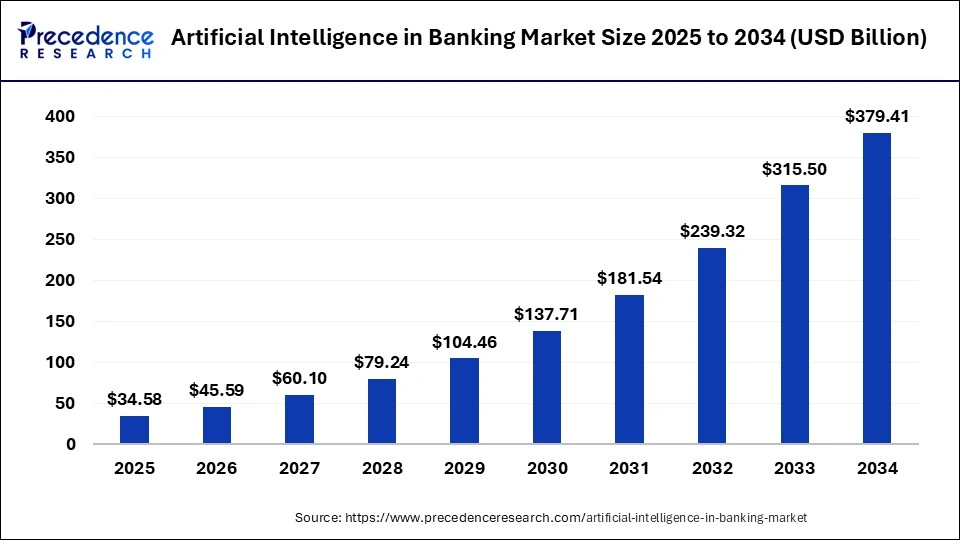

- AI is projected to create US$140 billion of annual value in banking by 2025 through process automation and decision augmentation.

- Generative AI in financial services alone is forecast to reach USD 15.69 billion by 2034, growing at a 26.29% CAGR, fueled by advancements in risk modeling, personalization, and fraud prevention.

- The emerging AI Agents in Financial Services market, covering autonomous compliance and risk management agents, is expected to grow 45.4% annually from 2025 to 2030.

- By 2030, AI-enabled banking systems will manage over 60% of personal financial operations worldwide, automating savings, loans, and risk workflows.

- Banking AI deployments have already cut operational costs by up to 25%, reduced manual errors by 40–45%, and increased retention through personalized service delivery.

- Banks deploying AI for modernization and automation have achieved an average ROI of 3.5× within 18 months, driven by process optimization and efficiency gains.

- AI integration has improved risk detection and liquidity forecasting accuracy by up to 99.3%, outperforming traditional systems significantly.

- By the end of 2025, 75% of large banks (assets > $100 billion) are expected to achieve full AI integration, accelerating modernization cycles.

Performance Gains Through AI Integration

- Banks modernizing legacy systems with AI have reported 45% fewer operational errors and 25% faster loan processing times, along with a 13% reduction in operational costs.

- AI-driven compliance automation has reduced audit preparation time by 35% and manual document processing by 90% in mid-tier banks.

- Predictive AI models have improved credit approval accuracy by 34% and cut false positives in fraud detection by up to 80%.

AI Integration Trends

- Integrating AI with cloud-native frameworks helps reduce technical debt, which is rising sharply as banks modernize legacy codebases.

- Recent surveys reveal that 54% of bank leaders cite data silos as a critical barrier to AI integration, emphasizing the need for data consolidation and API-driven strategies.

Why Legacy Systems Hold Banks Back

Legacy banking systems were never built for today’s AI-driven financial world. Most cores still run on mainframes from the 1970s and 1980s, powered by COBOL and batch processing. As of 2025, 70% of banks globally still depend on legacy core banking systems, while 43% continue to operate on mainframes.

These systems are reliable for transaction handling, but they have become roadblocks to transformation.

1. High Costs, Low Agility

Banks are spending a staggering 70% of their budgets on maintaining outdated legacy systems, with many using an expensive ‘patch and upgrade’ approach. That leaves little room for AI integration or digital innovation. The result is slower modernization cycles and a limited ability to respond to fintech competitors.

2. Data Silos and Fragmentation

Legacy cores operate in silos, leading to customer, payment, and risk data residing in separate systems with minimal connectivity.

This fragmentation makes it hard to implement AI-powered banking solutions, as machine learning models require unified, high-quality data pipelines to function effectively. Without integration layers, banks cannot unlock the full value of AI.

Although core banking modernization remains a top priority, fewer than 50% of CIOs say their projects have delivered expected ROI, highlighting the importance of AI for efficiency and agility.

3. Compliance and Risk Exposure

Legacy technology complicates compliance with frameworks like Basel III, GDPR, and PCI DSS. Audit trails are incomplete, and manual reporting is time-consuming.

In contrast, AI-enabled banking systems can automate reporting, detect anomalies instantly, and improve regulatory readiness. Banks that remain on outdated cores face higher compliance penalties and reputational risks.

4. Slow Customer Experience Delivery

Challenger banks and fintechs launch AI-powered digital services in months, while traditional banks struggle for years. Outdated architecture makes it difficult to deploy new APIs, chatbots, or personalization engines.

This gap directly impacts customer loyalty, with younger users preferring agile, AI-first competitors.

5. Security Vulnerabilities

Mainframes running decades-old code expose banks to cybersecurity risks. Patching is costly, and new threats emerge faster than updates can be deployed.

AI-driven fraud detection requires modern integration points, which legacy cores simply cannot support without middleware or cloud-native extensions.

Legacy systems are not going away overnight. But integrating AI into core banking systems allows institutions to modernize without complete replacement. For instance, McKinsey estimates that AI could increase banks’ revenues by as much as 30% and cut costs by 25% or more.

The next section explores how AI integration unlocks new value in fraud prevention, risk management, and customer experience.

Role of AI in Legacy Banking Systems

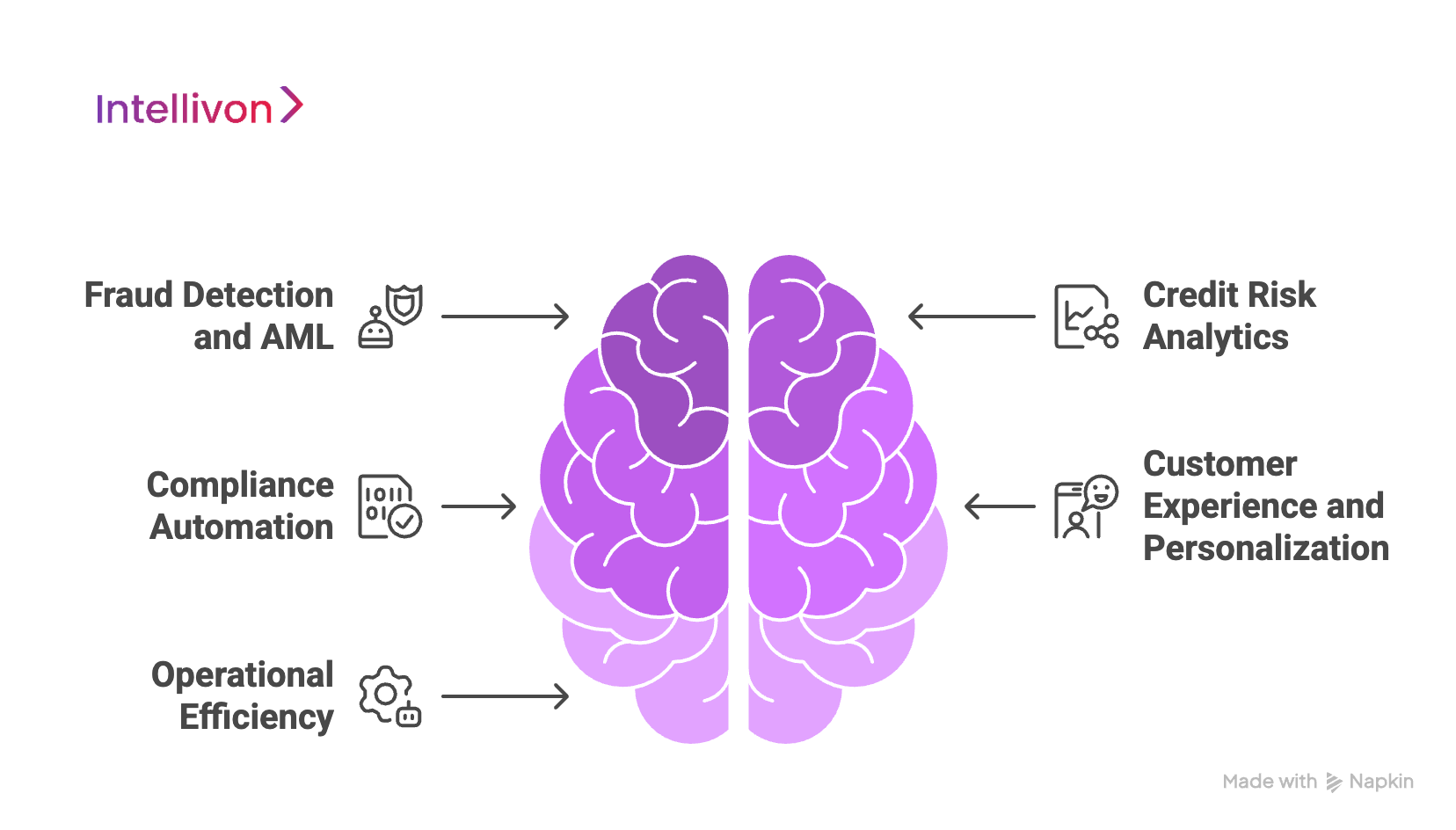

AI is here to strengthen legacy banking systems rather than replace them. Instead of a risky “rip and replace,” banks can layer AI capabilities on top of their existing systems. This approach lets them modernize where it matters most, which is fraud prevention, compliance, risk management, efficiency, and customer engagement.

1. Fraud Detection and AML

Legacy systems weren’t built for real-time monitoring. They rely on batch processing, which leaves gaps for fraud to slip through. AI models close that gap by scanning thousands of transactions instantly, spotting patterns no human team could see.

Studies show AI-driven fraud detection cuts false positives by 40–60%, easing compliance burdens and freeing up investigators for high-value cases.

2. Credit Risk Analytics

Traditional credit scoring is rigid because it leans too heavily on bureau data and outdated models. AI goes further and pulls in behavioral, transactional, and even market data to give a fuller picture of risk. That means faster, more accurate decisions, and the ability to extend credit responsibly to customers who would otherwise be overlooked.

3. Compliance Automation

Ask any compliance team, and they’ll tell you that legacy cores make audits a nightmare. Manual reporting, inconsistent data, and endless document reviews slow everything down.

AI changes that by automating document checks, flags anomalies, and generates reports that are regulator-ready. The result is faster audits, fewer errors, and compliance teams focused on strategy instead of paperwork.

4. Customer Experience and Personalization

Customers expect banks to know them, but legacy systems treat everyone the same. AI bridges that gap. It powers conversational interfaces, personalized product recommendations, and real-time financial advice.

For banks, that means stronger retention in a world where fintech challengers win customers with personalization.

5. Operational Efficiency

The biggest drain of all is cost. Many banks spend 60–70% of their IT budgets just to keep legacy systems running. That’s money tied up in maintenance instead of innovation. With AI layered on top, banks can cut waste, streamline operations, and redirect spending toward growth.

Key AI Use Cases for Legacy Banking Systems

AI becomes most valuable in banking when it is applied with purpose. For institutions still running on legacy cores, the question is not whether to modernize, but where AI can make the biggest difference without destabilizing critical systems. When done thoughtfully, the impact is immediate and tangible.

1. Fraud Detection and AML

Legacy systems were never designed to track fraud in real time. They flag suspicious transactions in batches, often after the damage is done.

AI turns this on its head by instantly spotting unusual patterns, enabling banks to respond before fraud escalates. The result is fewer false alarms, faster investigations, and stronger protection for both the bank and its customers.

2. Credit Risk Analytics

Credit scoring has always been one of banking’s weak spots. Relying on outdated bureau data alone leaves gaps and slows decision-making.

AI fills those gaps by analyzing transaction history, spending behavior, and even broader market signals. For banks, this means approvals that are not only quicker but also more accurate and fair, something legacy systems alone could never deliver.

3. Compliance Automation

Compliance is where many banks feel the weight of their legacy infrastructure most heavily. Endless spreadsheets, manual checks, and reactive reporting consume entire teams.

AI lifts that weight by automating document reviews, generating audit-ready reports, and flagging risks in real time. This allows compliance teams to work proactively instead of constantly playing catch-up.

4. Customer Engagement and Personalization

Customers today expect banking that feels as personal as their favorite app. Legacy cores, rigid by design, can’t keep up with that demand.

Here, AI bridges the gap by powering conversational interfaces, personalized offers, and real-time financial advice. For customers, it feels like banking finally understands them. For banks, it strengthens loyalty in an increasingly competitive landscape.

5. Operational Efficiency

Running a legacy system is like keeping an old car on the road, which is costly, time-consuming, and prone to breakdowns.

AI helps lighten that load by automating repetitive back-office tasks, speeding up processes like loan approvals, and even predicting when core systems might fail. This frees up IT teams to focus on innovation instead of endless maintenance.

These use cases show how AI can breathe new life into legacy systems without tearing them apart. But integrating AI into decades-old infrastructure doesn’t happen without obstacles. The next section unpacks the biggest challenges banks face, and how they can be addressed strategically.

Challenges in Integrating AI with Legacy Banking Systems

Bringing AI into legacy banking systems is rarely a smooth process. These platforms were designed decades ago for stability and scale, not for real-time analytics, compliance automation, or AI-driven personalization. Below are the most pressing challenges—and how our team helps institutions turn them into opportunities for modernization.

1. Data Silos That Limit Intelligence

Most banks still run customer, payments, and risk data across multiple disconnected systems. One database holds account information, another manages loan history, while compliance reports exist on an entirely separate platform. This fragmentation leads to inconsistencies and makes cross-functional visibility nearly impossible.

Why It Blocks AI Integration:

AI thrives on consolidated, high-quality datasets. When information is siloed, models underperform because they cannot “see” the whole picture. Fraud detection engines miss hidden anomalies, and credit scoring tools cannot factor in behavioral data locked away in another system. Without addressing data silos, AI integration in banking becomes a costly experiment with limited impact.

How We Solve It:

Our experts design secure data pipelines and integration frameworks that break down silos without disrupting the core.

By building unified data layers and AI-ready architectures, we give banks a single, trusted view of their customers and operations. This ensures every AI model, from fraud detection to compliance automation, is powered by complete, accurate data.

2. System Rigidity and Technical Debt

Legacy cores, often written in COBOL, are extremely rigid. They process millions of transactions reliably, but cannot easily adapt to new requirements. Over the decades, patchwork upgrades have created “technical debt,” which is outdated code that slows development cycles and increases the cost of every change. For many banks, even simple system enhancements take months to deliver.

Why It Blocks AI Integration:

AI integration in banking requires agility, and fraud models need to be deployed and retrained quickly. Customer personalization engines must adapt to real-time behaviors. Technical debt makes this impossible. Banks find themselves trapped, unable to innovate at the speed demanded by regulators, customers, and markets.

How We Solve It:

We specialize in layering API-driven microservices on top of rigid legacy cores. This creates a flexible integration layer where AI applications can run independently.

Our team reduces reliance on outdated code, enabling banks to experiment, deploy, and scale AI solutions without destabilizing mission-critical systems.

3. Compliance Complexity

Banking is one of the most tightly regulated industries in the world. Legacy cores were not built with today’s compliance demands in mind. Generating reports for regulators still requires manual data pulls, reconciliations, and endless spreadsheets.

This creates delays and increases the risk of human error, both of which can trigger costly penalties.

Why It Blocks AI Integration:

When compliance teams lack confidence in new technology, adoption stalls, and AI models that are not explainable or audit-ready can alarm regulators and cause leadership pushback. Without embedding governance and transparency from the start, AI banking solutions will always face internal resistance.

How We Solve It:

Our approach is compliance-first by design. We build AI systems aligned with frameworks like Basel III, GDPR, and PCI DSS from day one. Every model is explainable, auditable, and regulator-ready. Our team works directly with compliance officers to ensure they trust the outputs, turning AI into an ally rather than a risk.

4. Security and Risk Exposure

Legacy systems rely on outdated security protocols, making them vulnerable to modern cyberattacks. As banks digitize, their risk exposure grows, particularly when sensitive financial data is spread across multiple, unsecured environments. Introducing AI without upgrading the security perimeter only magnifies these vulnerabilities.

Why It Blocks AI Integration:

AI integration in banking involves connecting models to sensitive, real-time transaction flows. Without modern security frameworks, these integrations become potential entry points for hackers. For CIOs and CISOs, the risk of a breach often outweighs the promise of AI innovation.

How We Solve It:

Our team embeds AI-driven cybersecurity alongside every banking solution we deploy. From anomaly detection that flags suspicious activity in real time to layered encryption and DevSecOps practices, we make sure AI deployments are as secure as the systems they enhance. The result is modernization without compromising trust or stability.

These challenges are real, but they are not insurmountable. With the right architectural strategies and cultural alignment, AI can be integrated into legacy systems without risking stability or compliance. Next, we’ll explore the architectural approaches that make this possible.

Architectural Approaches to AI Integration into Legacy Banking Systems

Banks cannot afford to rip out legacy cores overnight. The smarter approach is to extend existing infrastructure with modern AI-ready layers. Below are the core architectural strategies that make integration sustainable, secure, and scalable.

1. API-Driven Integration Layers

APIs act as bridges between legacy cores and modern AI applications. Instead of modifying the core directly, banks can use secure API gateways to connect fraud detection engines, credit risk models, and customer personalization tools. This approach lowers risk while enabling fast experimentation with AI-powered banking solutions.

2. Data Lakes and AI Pipelines

Legacy cores scatter information across multiple silos. A data lake unifies this data into a single repository, where it can be cleaned, normalized, and prepared for AI models. AI pipelines then feed this data into fraud detection, compliance automation, or liquidity forecasting engines. For banks, this architecture unlocks insights without destabilizing the core system.

3. Microservices Architecture

Unlike monolithic cores, microservices break down functionality into smaller, independent services. Fraud detection, compliance reporting, and credit risk assessment can all be built as modular microservices. These services plug into legacy cores via APIs, enabling banks to modernize one function at a time instead of attempting risky full replacements.

4. Hybrid Cloud Deployment

Some banking functions can run securely on the cloud, while others must remain on-premises for compliance. A hybrid cloud architecture allows AI models to operate flexibly across both environments. For example, sensitive compliance workloads can stay on-prem, while customer-facing personalization engines run on the cloud for scalability.

5. Security and Governance by Design

Every architectural choice must be underpinned by strong security and governance. That means embedding DevSecOps practices, encryption protocols, and AI model governance frameworks from the start. With these controls in place, banks can innovate without sacrificing compliance or customer trust.

These architectural approaches provide a roadmap for integrating AI into legacy banking systems without triggering costly overhauls. The next step is understanding the features of an AI-ready legacy system and how to ensure it can support both innovation and compliance at scale.

Features of an AI-Integrated Legacy Banking System

Modernizing a legacy core with AI is about preparing the system to support intelligence at scale. An AI-ready banking system has distinct features that allow it to integrate seamlessly with advanced models while staying compliant and secure.

1. Real-Time Monitoring and Insights

Legacy systems operate in batch cycles, which delays decision-making. An AI-ready system enables real-time monitoring across payments, risk, and customer transactions. This allows banks to detect fraud, adjust liquidity positions, and serve customers instantly, which is something traditional cores cannot achieve alone.

2. Explainable and Transparent AI

For banking, “black box” models are a non-starter. Regulators demand clarity on how AI reaches decisions. An AI-ready legacy system integrates explainability tools that make model outputs auditable and transparent. This builds trust with compliance teams, regulators, and executives.

3. Model Governance and Auditability

Governance is the backbone of responsible AI in banking. An AI-ready core ensures that every model is documented, monitored, and retrained when performance drifts. Audit trails are embedded by design, allowing banks to meet regulatory requirements without manual intervention.

4. Scalable Microservices and Modularity

AI-ready systems are flexible. They run fraud detection, compliance automation, or customer personalization as modular services. Each microservice plugs into the legacy core via APIs, meaning banks can modernize one function at a time instead of attempting a disruptive “big bang” overhaul.

5. Secure API Connectivity

Connectivity defines agility. Secure APIs allow banks to integrate AI tools with legacy cores without exposing vulnerabilities. They also make it easier to collaborate with fintech partners, cloud providers, or external data sources, thereby unlocking innovation while safeguarding sensitive data.

The shift from legacy to AI-ready systems is about layering intelligence onto what already works. Banks that achieve this balance unlock faster fraud detection, smarter compliance, and more personalized customer engagement. But success requires an architecture designed for scale, transparency, and security.

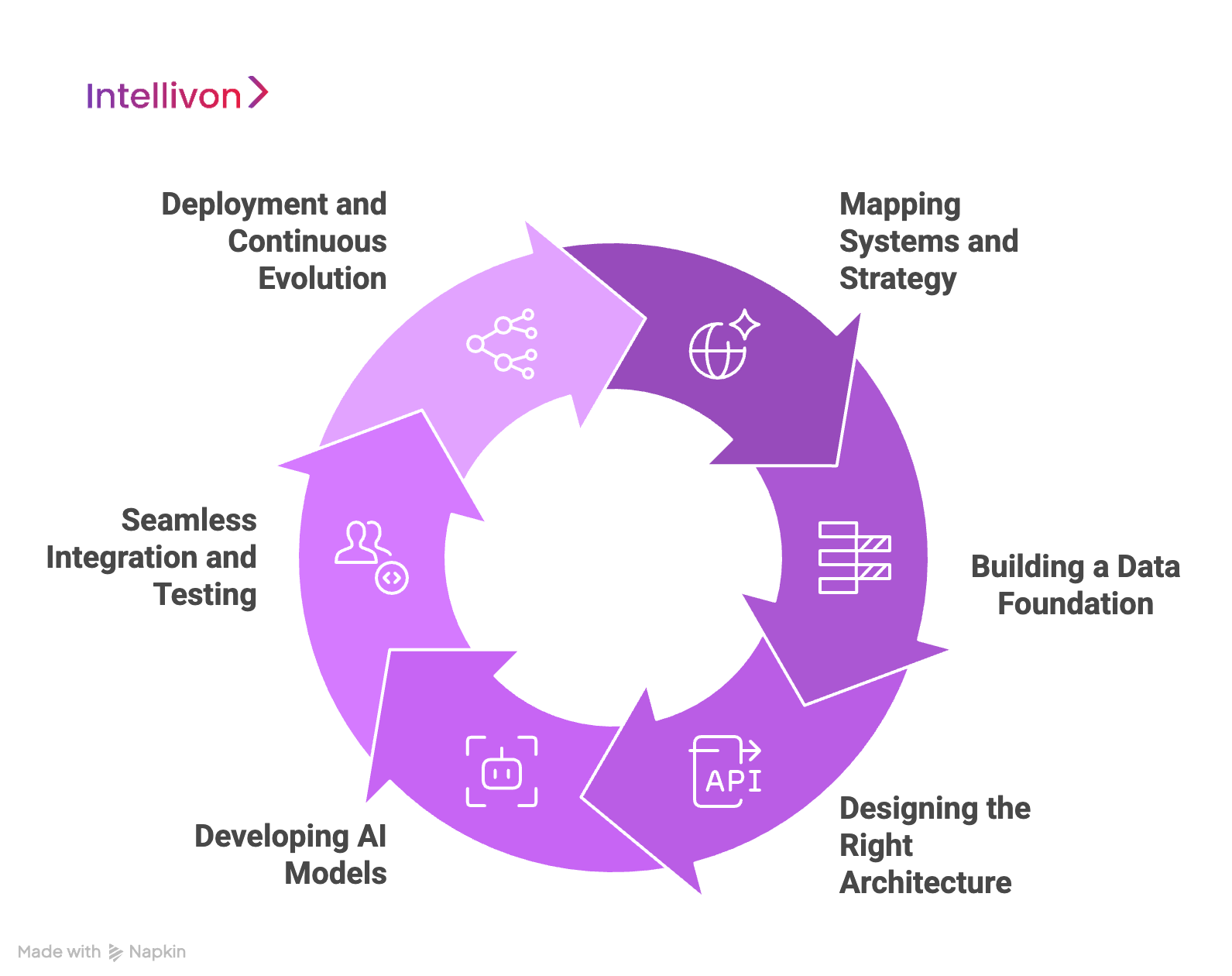

How We Integrate AI Into Legacy Banking Systems

Integrating AI into a bank’s legacy systems is rooted in building a bridge between stability and intelligence. At Intellivon, we guide this process carefully, ensuring every step adds value without disrupting what already works.

Step 1: Mapping Systems and Strategy

We begin by understanding the bank’s existing systems, their bottlenecks, and the objectives leadership wants AI to achieve.

Fraud prevention, compliance automation, credit risk analytics, or customer personalization all require different approaches. By aligning AI adoption with business goals from the start, we make sure every effort leads to measurable outcomes.

Step 2: Building a Data Foundation

Legacy systems scatter information across silos, which blocks AI from reaching its full potential. Our team builds secure data pipelines and integration layers that unify fragmented records into a single AI-ready foundation. Governance is embedded here too, ensuring data is consistent, secure, and audit-ready. This gives banks the confidence that their AI models are working with trusted, regulator-approved data.

Step 3: Designing the Right Architecture

Once the data layer is in place, we design an architecture that allows AI to run seamlessly alongside legacy cores.

That means deploying API gateways, adding modular microservices, and setting up hybrid cloud environments where sensitive workloads remain on-prem while customer-facing models can scale in the cloud. This balance keeps compliance intact while unlocking flexibility.

Step 4: Developing AI Models

With infrastructure ready, we begin building the AI applications themselves. Fraud detection engines, risk scoring tools, compliance automation platforms, or personalization engines are developed in close collaboration with banking teams. Every model we design is explainable, regulator-friendly, and tuned to the bank’s unique risk appetite and customer landscape.

Step 5: Seamless Integration and Testing

AI models must integrate with the legacy systems that drive daily banking operations. We create sandbox environments where integrations are tested, security is validated, and compliance teams can review outputs in advance. This minimizes risk while ensuring that once live, the AI augments the core instead of disrupting it.

Step 6: Deployment and Continuous Evolution

Once validated, AI systems are deployed gradually and monitored in real time. Our team sets up dashboards that track performance, bias, compliance alignment, and business impact.

When conditions change, whether regulatory, market, or customer-driven, we retrain and fine-tune models. This makes AI not just a one-time upgrade, but a living, evolving capability that grows with the institution.

Our integration process embeds layering intelligence on top of legacy systems without tearing them down. By combining strategy, data unification, modern architectures, and ongoing monitoring, we help banks move from static legacy environments to agile, AI-ready ecosystems.

At Intellivon, this is our specialty. We’ve built frameworks that let banks embrace AI confidently, protecting compliance, safeguarding trust, and ensuring every step of modernization is aligned with business outcomes.

Compliance & Security Frameworks for AI in Banking

For banks, adopting AI is about doing so within the strict boundaries of compliance and security. Legacy systems already struggle with regulatory reporting and outdated protocols. Adding AI without the right governance can introduce more risk than reward. That’s why every AI integration must be designed with compliance and security at its core.

1. Regulatory Alignment from Day One

Banking operates under some of the most complex regulatory frameworks in the world. Basel III requires rigorous stress testing and risk modeling. GDPR and PCI DSS demand strong data privacy controls. The EU AI Act adds expectations for transparency and accountability in algorithmic decisions. We ensure every AI solution is aligned with these frameworks before it goes live, so banks never face unpleasant surprises in audits or inspections.

2. Explainability and Model Governance

AI in banking cannot function as a black box. Regulators, compliance officers, and even customers need to understand how decisions are made. We embed explainability features that make model outputs transparent, traceable, and auditable. Governance frameworks are layered on top, ensuring every model is documented, monitored, and retrained when performance drifts. This protects banks from both regulatory pushback and reputational damage.

3. Security by Design

Legacy cores are attractive targets for cybercriminals, and connecting them with AI models introduces new entry points if not handled correctly. Our security-first design closes these gaps. We integrate AI-driven threat detection, real-time anomaly monitoring, multi-layered encryption, and DevSecOps practices into every deployment. Security is woven into the architecture from the beginning.

4. Continuous Monitoring and Audit Readiness

Compliance isn’t static; it evolves with new regulations and threats. We build continuous monitoring systems that track AI performance, bias, and compliance alignment in real time. Automated audit trails are generated as part of daily operations, ensuring that when regulators ask for documentation, banks are already prepared.

In banking, compliance and security are non-negotiable. AI must not only enhance operations but also strengthen resilience against risk. At Intellivon, our frameworks combine explainable AI, governance, and security-first design, giving banks the confidence to scale AI adoption without fear of regulatory or security failures. With us, compliance becomes a competitive advantage.

Conclusion

Integrating AI into legacy banking systems is no longer a question of if but how. Banks that continue to rely on outdated cores risk slower innovation, higher compliance costs, and reduced competitiveness against digital-first challengers.

AI offers a way forward. By layering intelligence onto existing infrastructure, banks unlock real-time fraud detection, smarter credit decisions, compliance automation, and personalized customer experiences.

The path forward requires a structured framework. Building secure architectures and embedding governance at every step allows banks to modernize without destabilizing mission-critical operations.

The result is a financial ecosystem that balances trust and agility. Legacy systems evolve into future-ready platforms capable of supporting the next era of banking.

Integrate AI Into Your Legacy Banking Systems With Us

At Intellivon, our mission is to help enterprises modernize their legacy banking systems with AI, without costly rip-and-replace overhauls. We design integration frameworks that balance stability with intelligence, enabling banks to innovate while maintaining compliance and customer trust.

Why Partner With Intellivon?

- Tailored Integration Strategies: Every roadmap is designed around your existing systems, regulatory environment, and modernization priorities.

- Compliance-First Approach: AI integrations align with Basel III, GDPR, PCI DSS, and other global standards, ensuring regulator-ready adoption from day one.

- Proven Enterprise Expertise: With 500+ AI projects delivered, we’ve guided global banks through successful AI integrations that improve efficiency, compliance, and resilience.

- Future-Ready Architecture: API-first, cloud-native, and modular microservices ensure your systems can scale as workloads and customer expectations grow.

- End-to-End Partnership: From assessment to deployment and continuous monitoring, our experts stay with you through the entire integration journey.

Book a strategy call today to explore how we can help transform your legacy systems into AI-ready platforms that reduce costs, accelerate modernization, and secure long-term competitiveness.

FAQs

Q1. Can AI work with legacy banking systems, or do banks need full replacement?

A1. Banks do not need to rip out their legacy cores to adopt AI. Instead, AI can be layered on top of existing systems through APIs, microservices, and data pipelines. This approach reduces cost and risk while allowing banks to modernize step by step.

Q2. What are the biggest challenges of integrating AI into legacy cores?

A2. The most common challenges include siloed data, outdated programming languages, compliance complexity, cybersecurity gaps, and organizational resistance. These hurdles make integration slower but not impossible. With the right architecture and governance, banks can overcome them and achieve measurable results.

Q3. How does AI improve compliance in legacy banking environments?

A3. AI automates key compliance tasks such as document review, anomaly detection, and audit trail generation. Models designed with explainability and transparency ensure regulators can see how decisions are made, reducing the risk of penalties and making compliance more proactive than reactive.

Q4. What features make a legacy system AI-ready?

A4. An AI-ready legacy system supports real-time monitoring, explainable models, embedded governance, modular microservices, and secure APIs. These features allow banks to integrate fraud detection, credit risk analytics, and personalized banking services without destabilizing the core.

Q5. How long does it take to integrate AI into a legacy banking system?

A5. Timelines vary based on complexity, but banks typically see functional integrations within 6–12 months. Using modular microservices and hybrid cloud environments allows phased adoption, ensuring business continuity while AI systems are tested, deployed, and scaled safely.