Key Takeaways:

-

AI transaction monitoring combines real-time ingestion, ML alert scoring, behavioral baselines, and graph analytics.

-

Real-time and batch processing, ISO 20022/SWIFT integration, and payment-rail connectivity are core requirements.

-

FinCEN SAR workflows, FFIEC-ready evidence, and human review ensure regulatory compliance and audit readiness.

-

Focused overlays start at $60,000 to $120,000 while bank-grade platforms reach $250,000.

-

How Intellivon builds governed financial-crime infrastructure where explainable AI supports analysts, and not replaces them.

When alert volumes outpace an analyst team, adding more detection rules doesn’t solve it, but building a smarter system does. An AI transaction monitoring platform replaces static thresholds with ML models that learn from your actual transaction behavior. As patterns shift, detection adapts, false positives drop, and your team focuses on cases that genuinely warrant investigation.

What separates a long-term platform from one that eventually degrades is the retraining architecture you design first. Without it, ML models drift as transaction patterns evolve, and false positive rates return to legacy levels within 14 months. Banks that build continuous retraining pipelines from day one maintain 60% false positive reduction and recover investigation ROI within 12 months.

Intellivon has spent over a decade building custom AI transaction monitoring systems for banks and fintech platforms. What we have experienced during the development process is that every build that can withstand the OCC model risk examination starts with the retraining loop. This blog post maps ML model selection, real-time processing, core banking integration, compliance controls, and the cost of building these platforms from the ground up.

What Is an AI Transaction Monitoring Platform?

An AI transaction monitoring platform is a smart software system that banks use to spot digital bank robbers, money launderers, and scammers. Instead of just looking at numbers, this system studies how a person normally spends money and who they send it to.

Consequently, it combines simple, strict rules with smart machine learning and a real human-in-the-loop alert review to catch fraudsters without blocking normal accounts by mistake.

1. Transaction Monitoring vs Fraud Prevention vs Sanctions Screening vs Investigation Support

Banks use different security tools to stop diverse financial crimes. While fraud prevention blocks an immediate theft, transaction monitoring looks for patterns of illegal money moving over time. Similarly, sanctions screening blocks banned people from using the bank, and investigation support helps humans build a legal case against criminals.

| Tool | Core Goal | Timing |

| Fraud Prevention | Stops immediate theft (e.g., stolen card). | Instant (Pre-auth) |

| Transaction Monitoring | Catches long-term patterns like money laundering. | Real-time or Batch |

| Sanctions Screening | Blocks banned individuals or countries. | At onboarding & transfer |

| Investigation Support | Helps humans check alerts and write reports. | Post-alert |

Thus, understanding these specific differences helps engineering teams build better defenses. Next, we must examine how banks actually catch these patterns using rules versus AI.

2. Rule-Based Transaction Monitoring vs ML-Powered Alert Scoring

Legacy rule-based transaction monitoring flags any account that crosses a rigid, pre-set limit. However, these basic rules create thousands of false alarms for normal human behavior.

In contrast, ML-powered alert scoring uses math to look at hundreds of clues at once, which ranks alerts by actual risk so humans only check the dangerous ones.

| Feature | Rule-Based System | ML-Powered Scoring |

| Logic | Simple “If-Then” limits (e.g., spend > $10k). | Multi-variable math patterns |

| False Alarms | Very high (often over 95%). | Drastically lower |

| Setup | Easy to write but easy for thieves to trick. | Needs data training but adapts |

Therefore, switching to machine learning stops compliance teams from wasting time on safe accounts. This data processing choice then leads directly to how fast the system needs to run.

3. Real-Time Transaction Monitoring vs Batch Transaction Monitoring

Real-time transaction monitoring checks money movements instantly as they happen to catch fast-moving scams. On the other hand, batch transaction monitoring groups millions of old history records together to run checks later that night.

Consequently, real-time tools cost more to operate but stop instant digital wallet theft, while batch tools are cheaper and great for slow tracking.

| Metric | Real-Time Monitoring | Batch Monitoring |

| Speed | Under one second | Hours or days later |

| Main Use | Instant wires, crypto, and digital wallets | Standard check deposits and ACH |

| Tech Cost | Higher (requires constant cloud power) | Lower (runs during off-peak hours) |

Because instant payment systems are growing globally, real-time setups are becoming mandatory for new fintechs (Source: [Wolfsberg Group, 2024]). Once a system processes this data, it must decide what to do with a suspicious match.

4. Alert Generation vs SAR Filing Decision

An alert generation happens automatically when the software spots a weird transaction pattern. However, a computer cannot legally declare someone a criminal or file a government report.

Instead, the system hands the alert to a human-in-the-loop alert review, where a compliance officer makes the final SAR filing decision based on federal law.

| Action | Alert Generation | SAR Filing Decision |

| Who Does It? | The AI software | A qualified human officer |

| Legal Weight | Internal flag only | Official report sent to FinCEN |

| Result | Triggers an internal review | Can trigger a federal investigation |

Ultimately, keeping a human in charge ensures the bank stays compliant without trusting automated code blindly. This balance is exactly how modern financial institutions protect their networks today.

Why Banks Need Real-Time Monitoring for Instant Payments

Banks are actively upgrading their security systems because rapid payment speeds and rich message standards require an immediate defense. Consequently, compliance teams must deploy a real-time transaction monitoring platform development strategy to score financial activity before stolen money leaves the building.

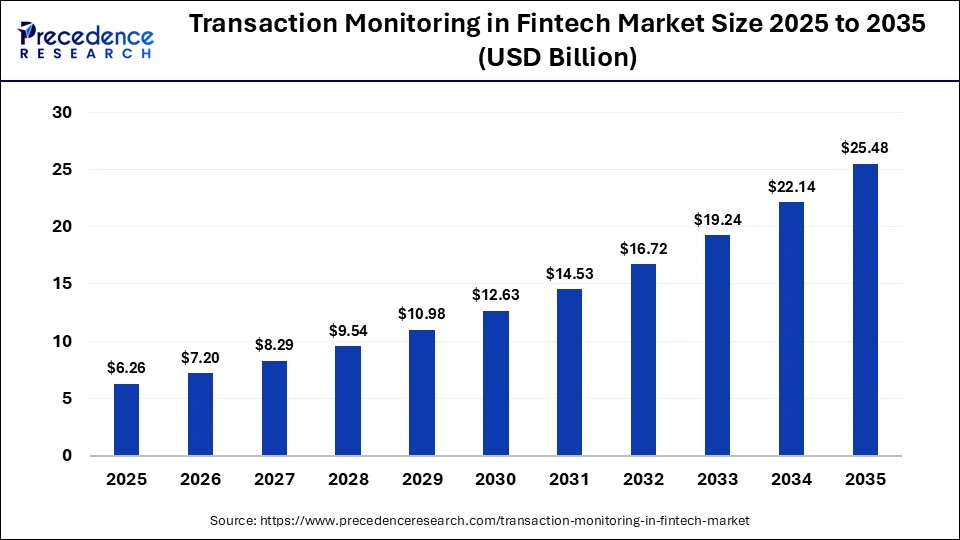

This structural shift is happening fast because the global transaction monitoring software market size is growing at an incredible rate. For instance, reputable research indicates that the overall fintech transaction monitoring software sector will expand at a 15.07% CAGR through 2035 to reach $25.48 billion.

Therefore, engineering teams face heavy pressure to build systems that analyze these massive, high-speed money flows instantly.

1. FedNow Operates 24/7 Without Pauses

Traditional bank security lines shut down over weekends, but modern criminal threats do not take breaks. Because the FedNow infrastructure operates continuously every single day, malicious actors can transfer illicit funds anytime.

Thus, checking transaction records the next morning fails to protect account security. This round-the-clock nature requires an automated, scalable monitoring infrastructure that handles peak volumes without human oversight.

2. ISO 20022 Unlocks Much Richer Data

The financial sector recently upgraded its underlying messaging formats, which unlocked deep data for compliance software. Because the Fedwire ISO 20022 implementation provides structured fields, systems can access clean details regarding ultimate beneficiaries.

Consequently, this clean data makes feature engineering transaction data much easier for developers. It also lets engineering teams run advanced pattern recognition without handling messy text strings.

3. Manual Review Takes Too Long

When money moves in under 60 seconds, human compliance officers cannot spend hours evaluating a flag. Because legacy verification queues take too much time, traditional review setups create massive bottlenecks.

Therefore, banks must build automated logic that can make instant routing decisions while a transaction is live.

4. Real-Time Alerts Stop Active Theft

If an algorithm flags a theft late, the bank loses its ability to recover those funds. Therefore, modern software engineering requires low-latency alert generation that scores transactions in under two hundred milliseconds.

By pairing this speed with strict intervention rules, a machine learning transaction monitoring system build can freeze transfers.

5. Batch Sweeps Catch Hidden Patterns

Even though instant detection is vital, real-time code often misses complex criminal rings that move money slowly. For example, batch transaction monitoring allows systems to group weeks of records to spot deep multi-account anomalies.

These anomalies include structuring detection, smurfing detection, and round-tripping detection.

For a deeper breakdown of compliance architecture for regulated fintech products, see our guide on How to Use Agentic AI for Compliance Automation in Finance.

Ultimately, rapid transfer rails do not eliminate the need for classic batch data processing methods. Instead, they divide your core compliance application into two highly distinct workloads: immediate intervention and pattern detection.

What Transactions and Typologies Should the Platform Cover?

An AI transaction monitoring platform must cover five core financial domains: retail banking, commercial banking, card networks, international wires, and digital crypto assets. Rather than using one generic rule for every transfer, the system deploys a targeted coverage map.

This map instantly matches each payment type, rail, and criminal method to the exact data pipeline, scoring speed, and review workflow required to mitigate that specific risk.

1. Transactions and Typologies Coverage Table

| Monitoring Domain | Payment or Entity Coverage | Typologies to Detect | Required Processing Mode |

| Retail Banking | ACH, wires, cash deposits | Structuring, smurfing, rapid fund movement | Real-time plus daily aggregation |

| Commercial Banking | Business accounts, trade payments | Layering, round-tripping, high-risk locations | Real-time plus network review |

| Card & Wallet Activity | Card payments, wallet transfers | Money mules, velocity spikes, merchant scams | Low-latency scoring |

| Cross-Border Flows | SWIFT, ISO 20022 messages | Bad routing, sanctions evasion, layering | Real-time data enrichment |

| Digital Assets | Crypto transfers, blockchain wallets | Chain-hopping, dark-web wallet exposure | Blockchain analytics integration |

2. Retail and Commercial Banking Coverage

Traditional banking infrastructure requires highly specialized tracking speeds to expose hidden criminal patterns.

- ACH Transaction Monitoring: The system tracks automated bank transfers to catch structuring detection and smurfing detection, where bad actors split large illicit funds into tiny, unassuming deposits.

- Wire Transfer Monitoring: The software runs instant checks to execute rapid fund movement detection before international transfers move completely out of domestic legal reach.

- Commercial Tracking: The platform maps business accounts to reveal round-tripping detection, which stops rings from sending money in giant circles just to make dirty cash look clean.

3. Card, Wallet, and Crypto Coverage

High-speed digital payment networks require instant, low-latency analysis to freeze malicious activities before settlement.

- Card Payment Monitoring: The software analyzes store and online card swipes to identify stolen accounts and active money mules instantly.

- Digital Wallet Monitoring: The engine tracks peer-to-peer mobile app transfers to stop rapid velocity anomalies and coordinated merchant scams.

- Crypto Transaction Monitoring: The system integrates with specialized public ledgers to spot chain-hopping across different tokens and prevent high-risk jurisdiction monitoring failures (Source: [Wolfsberg Group, 2024]).

4. Beyond Simple Transaction Screening

The platform must not assume that a single unusual transfer means a customer is a criminal. Instead, software engineers must build pipelines that blend basic payment data with customer behavioral baseline modeling.

The engine continuously calculates peer group analysis, transactions, network connections, and past alert histories together. Consequently, this complete contextual history gives the machine learning model the necessary foundation to score threats accurately.

Ultimately, the specific types of crime you need to catch will dictate your core software design.

What Architecture Supports Real-Time and Batch Monitoring?

Successful real-time transaction monitoring platform development requires building two distinct but connected data processing paths. Specifically, the system needs a streaming path for instant payment scoring and a separate batch path to uncover slow-moving criminal networks across time and channels.

Consequently, both pipelines must feed into a single unified case system to generate consistent audit logs, model versions, and investigator review histories.

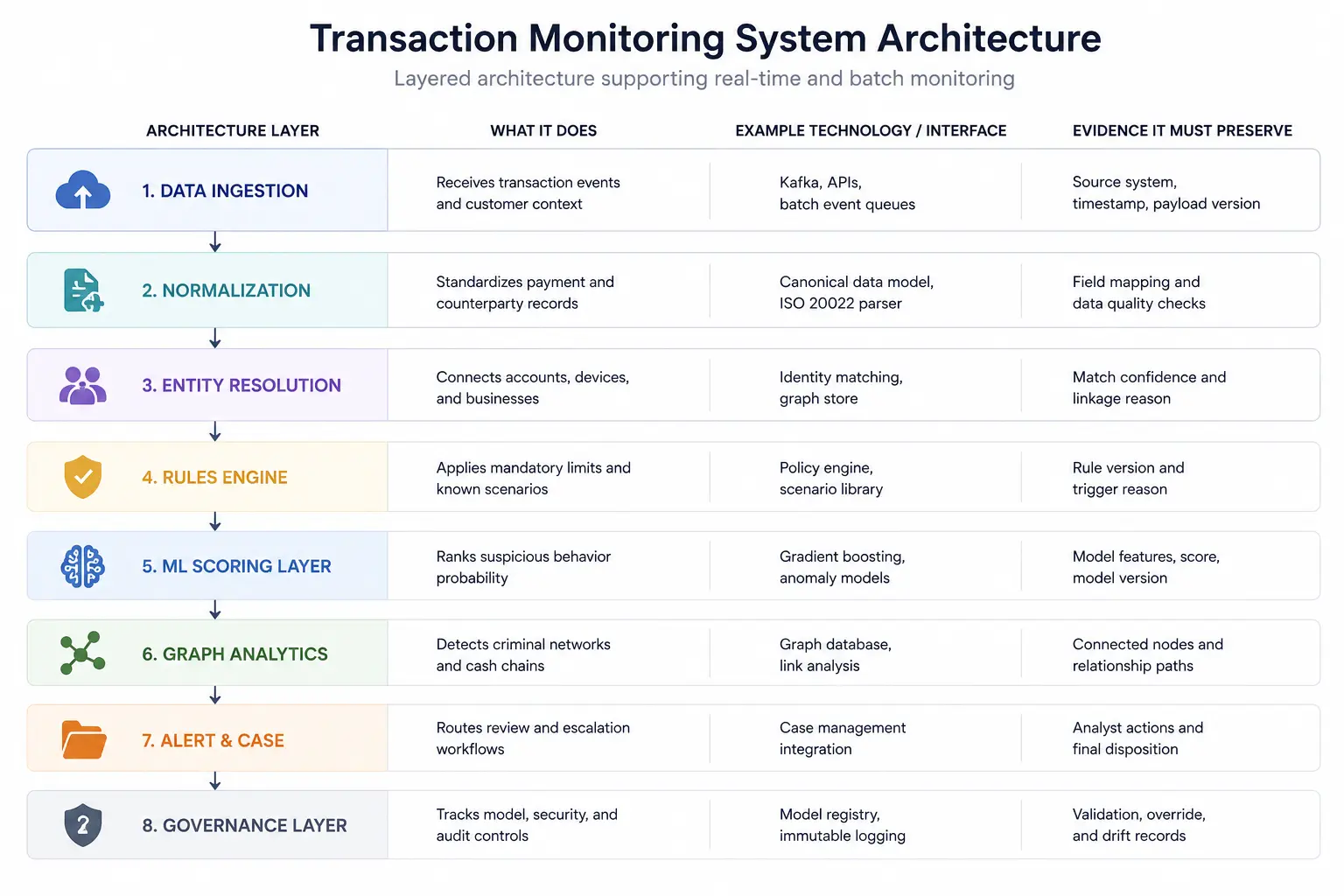

1. Architecture Layers

| Architecture Layer | What It Does | Example Technology or Interface | Evidence It Must Preserve |

| Data Ingestion | Receives transaction events and customer context | Kafka, APIs, batch event queues | Source system, timestamp, payload version |

| Normalization | Standardizes payment and counterparty records | Canonical data model, ISO 20022 parser | Field mapping and data quality checks |

| Entity Resolution | Connects accounts, devices, and businesses | Identity matching, graph store | Match confidence and linkage reason |

| Rules Engine | Applies mandatory limits and known scenarios | Policy engine, scenario library | Rule version and trigger reason |

| ML Scoring Layer | Ranks suspicious behavior probability | Gradient boosting, anomaly models | Model features, score, model version |

| Graph Analytics | Detects criminal networks and cash chains | Graph database, link analysis | Connected nodes and relationship paths |

| Alert & Case | Routes review and escalation workflows | Case management integration | Analyst actions and final disposition |

| Governance Layer | Tracks model, security, and audit controls | Model registry, immutable logging | Validation, override, and drift records |

2. Core Infrastructure Components

Building a resilient transaction monitoring system architecture requires a decoupled, cloud-native microservices transaction monitoring setup.

- The Ingestion Pipeline: An event-driven monitoring architecture uses Kafka transaction streaming to pull financial messages from the core banking system integration layer instantly.

- Data Normalization: The data ingestion pipeline AML layer instantly routes messy payloads into a standard format using a specialized ISO 20022 transaction data parser.

- Entity Resolution: The platform runs entity resolution transaction monitoring routines via an API-based monitoring architecture to merge separate accounts into single human profiles.

3. The Scoring and Review Engine

Once data moves through the ingestion layers, it enters the parallel processing engines for risk grading.

- Dual-Path Processing: The streaming engine evaluates threshold-based alert generation rules in milliseconds, while the graph engine performs deep link analysis and financial crime sweeps in the background.

- Machine Learning Scoring: The ML layer runs gradient boosting models to evaluate behavioral analytics transaction monitoring features, instantly filtering out safe customer anomalies.

- Defensible Auditing: The platform routes high-risk alerts into the case management integration panel while ensuring complete audit trail immutability across the entire pipeline.

Ultimately, this dual-path architecture is only defensible to bank examiners when each detection method has a clearly defined job.

This foundational data layout means we must now look at the specific mathematical models and machine learning frameworks that sit inside the scoring layer.

Which Decisions Belong to Rules and Reviewers?

An AI-powered transaction monitoring platform should never use a single machine learning model to make every compliance decision. Instead, a defensible architecture uses deterministic rules to enforce strict regulatory limits while applying machine learning to analyze complex behavior.

Consequently, this multi-layered approach isolates graph analytics for tracking hidden networks and reserves the final legal judgments entirely for human compliance officers.

1. Decision Allocation Framework

| Decision Type | Best Control | Why It Fits | Example Output |

| Known Limits | Deterministic rule | Explicit, testable, and repeatable | Threshold alert with reason code |

| Unusual Transfers | Supervised ML | Compares data against learned patterns | Transaction risk score |

| Customer Changes | Behavioral baseline model | Evaluates deviation over time | Baseline variance flag |

| Peer Abnormalities | Peer-group analysis | Compares similar customer cohorts | Outlier cohort score |

| Mule Networks | Graph analytics | Surfaces linked entities and paths | Connected-risk graph |

| Alert Explanation | Explainability layer | Makes model output reviewable | SHAP values and feature drivers |

| Case Disposition | Trained analyst | Requires judgment and accountability | Close, escalate, or investigate |

| SAR Filing Decision | Authorized compliance officer | Regulatory decisions must be defensible | Documented SAR decision |

2. Allocating the Analytical Workloads

Building a dependable bank AI transaction monitoring platform requires assigning clear responsibilities to each software component.

- Rules Engine: Simple policies handle fixed mandates, such as flagging any single cash transfer that crosses a specific regulatory threshold.

- Machine Learning Engine: Advanced anomaly detection financial transactions models handle variable patterns, such as tracking when a retail account suddenly switches to high-volume commercial behavior.

- Graph Analytics Engine: The system uses network graph analysis to map transactions across multiple institutions, which helps uncover hidden mule accounts and complex layering rings.

3. Empowering the Human Investigators

Engineers must prioritize explainable AI transaction monitoring features to ensure human reviewers can defend their choices during federal audits.

- Model Explainability: The scoring pipeline calculates SHAP values and alert explainability data to provide explicit, clear text reasons for every automated flag.

- The Role of LLMs: Do not position a large language model as your primary transaction pattern recognition engine. Instead, use LLMs strictly to write automated case summaries, draft suspicious activity reports, or search internal policy databases.

For a deeper breakdown of investigation-stage AI assistance, see our guide on How Do Fintech Companies Build AI AML Investigation Systems?.

Ultimately, model selection is incomplete without strict governance controls that govern validation, performance monitoring, and reviewer accountability. This balance ensures your software platform remains entirely defensible during annual regulatory reviews.

What Should Banks Check Against the 2026 Model Risk Update?

U.S. bank buyers must evaluate AI transaction monitoring models against the current interagency model-risk framework rather than relying only on older historical rules. Specifically, the 2026 updated regulatory guidance completely changes how financial institutions must test, document, and manage automated risk scoring systems.

Consequently, your platform design should explicitly separate your quantitative data models from generative AI tools because regulators now require entirely different governance reasoning for these two distinct technologies.

1. The Overhaul of Federal Model Rules

Federal regulators recently launched a major update to banking safety rules that directly impacts automated compliance software. In April 2026, the Federal Reserve, OCC, and FDIC jointly issued a brand-new model risk management framework.

- Replacing Outdated Standards: This directive officially replaces the older SR 11-7 rules and the 2021 BSA/AML model statements.

- Regulatory Shift: Banks cannot build modern platforms using obsolete governance checklists without facing serious audit issues during examinations.

- Modernized Supervision: The updated rules force institutions to grade mathematical algorithms based on their actual real-world materiality.

2. Quantitative Models Need Strict Validation

Any math tool that creates a specific risk number or probability score counts as a formal model under the 2026 rules. Therefore, your ML-powered alert scoring, behavior tracking, and graph-risk algorithms require a complete mathematical review.

- Core Mandates: This means developers must run deep outcomes testing, independent validations, and regular backtesting against real fraud data.

- Inventory Control: Furthermore, your engineering team must maintain a live, structured model inventory that tracks every active mathematical version in production.

- Effective Challenge: Validators must have the organizational standing to challenge model assumptions and record those debates in a clean audit trail.

3. Copilots Require Separate Control Boundaries

Generative AI and agentic software are explicitly excluded from the strict scope of the April 2026 quantitative guidelines. Because these tools are novel and rapidly evolving, regulators expect banks to govern them through separate risk boundaries.

- No Blind Trust: Thus, a compliance platform must ensure that an AI assistant cannot autonomously close alerts or submit suspicious activity reports.

- Human-in-the-Loop: A qualified human compliance officer must review every piece of text generated by an LLM copilot before approval.

- Immutable Logs: Every prompt, user action, and grounded document reference must be logged permanently to protect data integrity.

4. Vendors Cannot Absorb Your Compliance Risk

Many bank leaders mistakenly believe that buying a third-party software platform transfers their legal model risk to the vendor. However, current regulatory standards state that the purchasing bank holds final accountability for any algorithmic mistakes.

- In-House Responsibility: Even if you use an outside vendor, your internal compliance teams must still fully validate the system’s conceptual soundness.

- Continuous Testing: Your engineers must track ongoing performance monitoring metrics to catch processing errors before they impact real accounts.

5. Small Institutions Must Follow Similar Discipline

The new 2026 guidance is primarily directed at banking organizations that manage over $30 billion in total assets. However, smaller community banks and growing fintech startups are not completely off the hook if they use advanced software.

- Risk Exposure Rules: If a small institution deploys a complex machine learning setup to score payments, examiners will still review the system closely.

- Proportional Scaling: Oversight rigor must match the complexity and total dollar exposure of the transactions passing through your platform.

- Defensible Systems: Consequently, maintaining clear documentation is necessary for any company using mathematical algorithms to handle public funds.

Ultimately, regulatory model governance becomes practical only when your software records exactly what federal examiners need to reconstruct a compliance decision.

This strict documentation requirement means engineering teams must purposefully design an evidence architecture that captures data states at the exact microsecond of a transaction.

What Evidence Must Each Alert Preserve for FFIEC Review?

An alert is only ready for an official FFIEC examination when the platform preserves the complete transaction data, customer context, rules triggered, model reasoning, analyst research, escalation paths, and final outcomes needed to explain why the activity was investigated, closed, or reported.

It is never enough to simply show a high risk score. Consequently, the platform must lock down this complete digital trail to prove your

1. Required Evidence Specification Table

| Evidence Object | What the Platform Stores | Why the Buyer Needs It |

| Transaction Evidence | Original payload, rail types, exact amounts, timestamps, counterparties | Proves what specific financial activity was evaluated by the engine |

| Customer Context | Live CIP, CDD, EDD risk levels, and historical expected behavior | Proves the alert was scored within the customer’s normal baseline |

| Detection Evidence | Triggered rules, specific model features, scores, and network graph links | Explains the explicit logic that caused the software to fire an alert |

| Investigation Evidence | Analyst notes, uploaded files, query trails, and research workflows | Reconstructs the exact steps the human took during the case review |

| Decision Evidence | Final closure codes, escalation logs, SAR files, and reviewer identities | Supports internal corporate governance and individual accountability |

| Model Evidence | Production model versions, threshold versions, validation statuses | Supports model-risk reviews and defends system integrity during audits |

| Access Evidence | Role-based permissions, override histories, assumption-change logs | Proves compliance controls are secure from internal tampering |

2. Designing for Traceability and Staffing Reality

Building an immutable data ledger allows your compliance team to easily withstand intense regulatory scrutiny.

- End-to-End Mapping: Current FFIEC examination procedures dictate that field auditors must be able to select any random alert and completely trace it through the entire monitoring, research, and reporting lifecycle.

- Alert Volumetrics: Your system’s alert generation parameters must be configured strictly around actual institutional risk profiles. Therefore, you cannot tune alert thresholds down merely to match available staffing levels or reduce human queue sizes.

- Alert Management Integrity: The underlying alert management system must automatically enforce these capture requirements across every live financial channel. Consequently, your platform remains protected against data loss during unexpected transaction volume spikes.

3. Formalizing Case and Dismissal Documentation

Every downstream decision must be supported by permanent, unalterable proof within your central compliance database.

- Defensible Dismissals: When an investigator clears a flag without filing a report, the platform must mandate clear, documented reasoning explaining the “No-SAR” decision. This rule is vital because federal guidelines require explicit facts to prove why an unusual pattern did not cross the suspicion threshold.

- Deep Case Management Integration: Your platform must retain all raw investigation evidence directly inside its own data store instead of merely pushing out a shallow notification to an external ticketing tool.

- Seamless SAR Filing Workflow: If a case escalates, the system must automatically package the compiled evidence ledger to drive an electronic FinCEN SAR submission without losing the underlying model metadata.

Ultimately, your core evidence architecture determines your technical integration requirements. This structural dependency means engineering teams must precisely design the system connections that supply incoming data streams and receive outbound monitoring outcomes.

Which Systems Must the Platform Integrate With?

A successful custom transaction monitoring software development project works only when your automated risk scanning engine sits directly inside the bank’s live operational data flows. Consequently, the platform cannot run as a standalone database silo.

It must actively ingest payment events, customer risk context, sanctions screenings, and historical ledger files from your core systems, then instantly return formatted alerts, case files, and reporting records back to your existing compliance dashboards.

1. Unified Compliance Integration Matrix

| Integration Target | Data Received or Sent | Processing Needed | Monitoring Value |

| Core Banking System | Accounts, balances, customer profiles, transfers | Batch and live event feeds | Provides deep relationship context |

| Payment Processor | Card swipes, mobile wallets, ACH, payout events | Real-time API streaming | Powers low-latency risk scoring |

| ISO 20022 / SWIFT | Structured transfer and remittance data text | Parsing and data normalization | Enables counterparty network analysis |

| KYC / KYB Platforms | Identity verification, corporate ownership data | Scheduled cron-job refreshes | Updates the customer risk rating |

| Sanctions & OFAC | Watchlist match hits and screening logs | Synchronous API lookups | Delivers strict regulatory evidence |

| PEP & Adverse Media | Politically exposed person alerts, media logs | Background data enrichment | Prioritizes risky investigator queues |

| Case Management | Shared alerts, legal notes, analyst files | Bidirectional syncing | Guarantees complete record retention |

| SAR / CTR Workflow | Regulatory-ready suspicious activity documents | Controlled reviewer handoffs | Speeds up final government filings |

| Blockchain Analytics | Crypto wallet addresses and token movement tracking | Public ledger API enrichment | Tracks dangerous web3 fund links |

2. Core Ledger and Processing Integrations

Connecting to your primary deposit books and processor links keeps ingestion lines running at sub-second speeds.

- Core Ledger Systems: The ingestion engine hooks directly into your primary database files to pull fresh balance data and primary identity profiles without lagging behind ledger updates.

- Processor Pipes: The platform links directly into card networks and regional clearinghouses via a low-latency API-based monitoring architecture to evaluate point-of-sale swipes immediately.

- Rich Messaging Rails: Building native support for ISO 20022 translation code allows your platform to read deep transaction data fields, helping developers execute precise feature engineering transaction data workflows.

3. Risk Context and Watchlist Integrations

Blending background data with external threat registries gives your scoring algorithms the context needed to reduce false alarms.

- Identity Networks: Connecting to your KYC and KYB engines updates customer behavioral baseline modeling systems whenever a business adds new corporate signatories.

- Sanctions Automation: The platform deploys strict OFAC screening automation to block dirty transactions before they enter settlement queues.

- Media Tracking: Real-time PEP screening and continuous adverse media monitoring updates customer risk context variables in your machine learning models automatically.

4. Downstream Investigation Integrations

Your internal automation must securely bridge its analytical findings into your daily human compliance workspaces.

- Case Dashboards: Bidirectional case management integration ensures that when a human closes an alert, the system logs the outcome in its central model retraining database.

- Web3 Security Intelligence: For modern platforms tracking digital assets, deploying a native Chainalysis API integration or a TRM Labs integration provides vital crypto transaction monitoring safety shields.

- Investigation Assistance: For a deeper breakdown of analyst assistance after alerts are raised, see our guide on How Can Banks Develop an AI AML Compliance Copilot?.

Ultimately, a tight integration design makes your software build real, but your technical rollout sequence determines whether the platform reaches the production floor safely. This engineering dependency means your leadership team must follow a strict, milestone-driven development process to successfully deploy your new compliance layers.

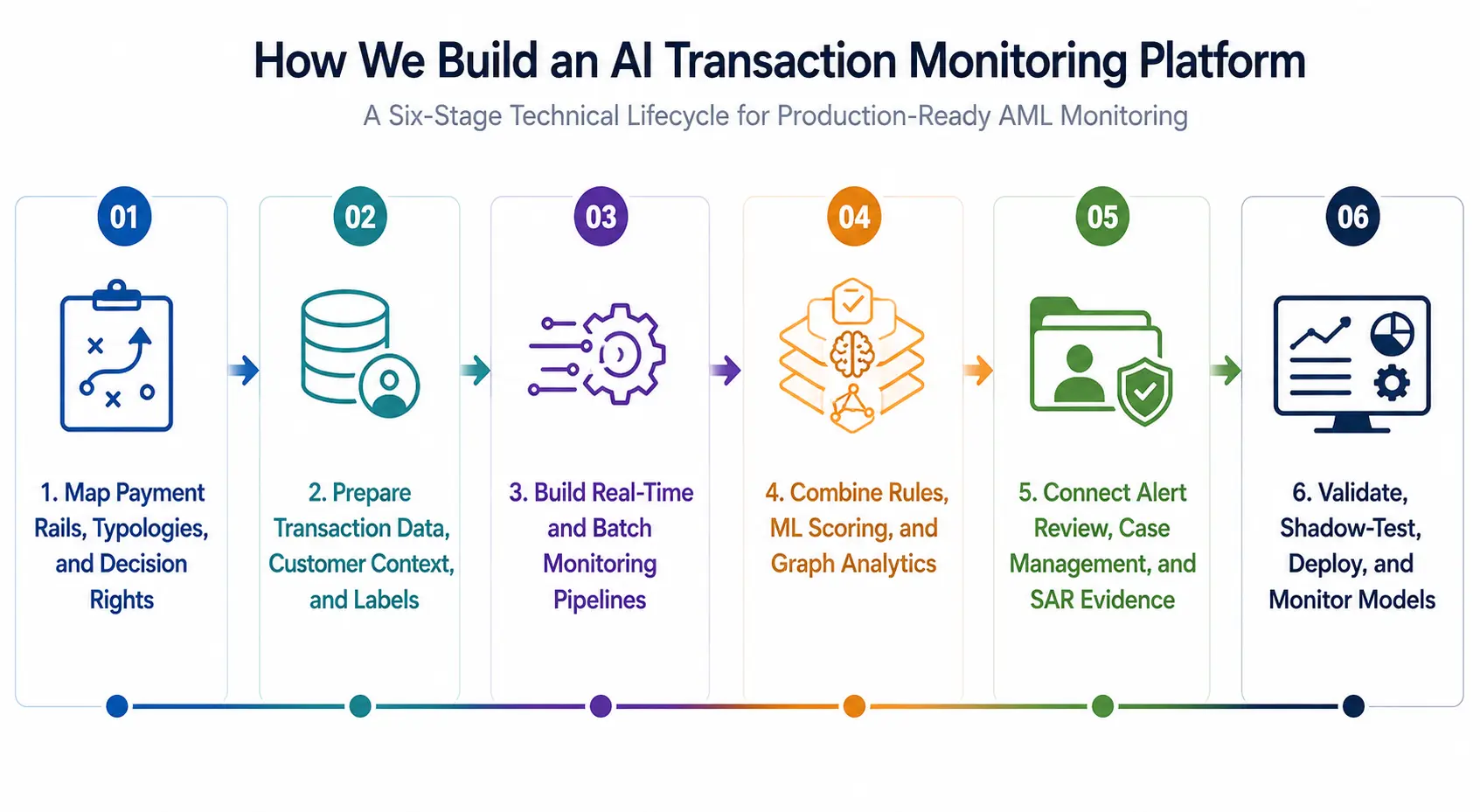

How We Build an AI Transaction Monitoring Platform

Building a production-ready AI transaction monitoring platform requires an engineered, six-stage technical lifecycle. Consequently, teams must systematically map coverage, clean historical data labels, deploy streaming pipelines, and configure hybrid detection layers before validating the final software code.

Each development phase must actively prove that it improves risk detection or reduces manual review workloads without ever weakening your institutional regulatory defense.

1. Map Payment Rails, Typologies, and Decision Rights

The first stage defines what the platform will monitor, which risks require real-time intervention, which patterns need longer-horizon analysis, and which decisions remain with compliance reviewers.

Without this map, teams often build alert features without proving that they cover the institution’s real products, customers, geographies, and reporting obligations.

- Asset Ingestion Mapping: Establish distinct intake definitions for domestic wires, ACH files, card processing events, digital mobile wallets, and correspondent banking networks.

- Typology Matrix Tuning: Prioritize the exact code criteria needed to flag retail structuring detection, commercial layering detection, money mule clusters, and high-risk jurisdiction monitoring failures.

- Control Boundary Placement: Pinpoint the precise system lines separating pre-settlement blocks, immediate post-posting alerts, and long-horizon background batch investigation scans.

- Authority Assignment Rules: Define clear technical ownership profiles for automated alert triaging, human-in-the-loop alert review escalations, and official regulatory reporting handoffs.

At Intellivon, our architecture teams begin with comprehensive transaction-flow mapping, strict regulatory obligation audits, and current alert economic reviews long before selecting machine learning frameworks.

This foundation ensures that the software directly fixes operational bottlenecks while satisfying federal exam guidelines from the very first day. Once risk coverage is precisely defined, the build needs reliable transaction and decision data.

2. Prepare Transaction Data, Customer Context, and Labels

The platform needs normalized payment events, customer-risk profiles, counterparty links, and historical alert outcomes before it can train or test detection models.

Labels must distinguish suspicious outcomes, defensive closures, operational errors, and incomplete reviews, because poor disposition data teaches the model to reproduce yesterday’s review noise.

- Canonical Format Design: Build a single unified data schema that standardizes all incoming payment payloads into identical processing objects.

- Message Field Harmonization: Normalize varied legacy core banking values, payment gateway strings, and rich ISO 20022 message blocks into matching data types.

- Entity Resolution Triggers: Resolve identity fragments across multiple accounts, devices, business filings, and counterparties to create isolated unique profiles.

- Label Verification Sweeps: Clean past training labels by separating verified FinCEN SAR submissions from defensive false alarms and careless analyst dismissals.

- Dataset Splitting Rules: Structure isolated historical data segments to feed your training, validation, and champion-challenger backtesting model pipelines.

Our engineering team manually configures automated data-quality rules, explicit lineage tracking maps, entity-resolution confidence parameters, and manual label audit checks before enabling automated scoring code.

Consequently, this deep cleaning prevents your machine learning algorithms from magnifying old human review errors. Once data is usable, the platform can process immediate risks and longer patterns through separate monitoring paths.

3. Build Real-Time and Batch Monitoring Pipelines

A production monitoring platform needs a streaming path for transactions that require immediate scoring and a batch or graph path for suspicious patterns that emerge across days, accounts, and relationships.

The two paths should use consistent data definitions, model versions, alert identifiers, and evidence logging so investigations remain coherent.

- Event-Driven Intake Setup: Deploy a scalable Kafka transaction streaming engine to pull ledger movements straight from core banking webhooks.

- Low-Latency API Construction: Build high-speed scoring endpoints that evaluate live financial transfers in under two hundred milliseconds to support immediate intervention.

- Daily Aggregation Framing: Configure background cron routines to run continuous velocity analysis and multi-account structuring detection rules every night.

- Graph Database Configuration: Integrate specialized graph neural networks transaction monitoring stores to scan for hidden link analysis financial crime connections.

- Immutable Storage Layout: Save all processing events, active rule thresholds, algorithm scores, and analyst notes inside an unalterable database ledger.

Intellivon structures the core network architecture entirely around operational latency: what must be scored before payment release, what can be reviewed after posting, and what requires relationship-level detection.

This tiered strategy prevents heavy analytical graph processing from slowing down your instant checkout rails. With the data pipeline operating, the platform can assign the right detection method to each risk type.

4. Combine Rules, ML Scoring, and Graph Analytics

We focus on deploying sophisticated mathematical models only where they actively improve signal quality or prioritize high-risk investigator queues. Consequently, we deliberately preserve classic deterministic rules wherever audit clarity and exact statutory execution matter most to federal examiners.

- Scenario Rule Implementation: Deploy simple, rigid scenario-based detection rules to handle absolute mandates, such as specific country bans and flat regulatory limits.

- Supervised Alert Ranking: Train gradient-boosted classification algorithms to rank incoming alarms based on clear historical compliance case outcomes.

- Unsupervised Anomaly Checks: Run isolation forests to spot customer behavioral baseline modeling deviations that fall far outside standard spending curves.

- Network Topology Scans: Execute graph network scans to trace complex round-tripping detection circles and coordinated multi-branch money mule rings.

- Explainability Feature Calculations: Force the scoring layer to calculate explicit SHAP values alert explainability metrics to output clear text alert reason codes.

Better alerts create value only when investigators can act on them through an evidence-rich workflow.

5. Connect Alert Review, Case Management, and SAR Evidence

The platform must move from a model score to an investigator-ready case without losing evidence. Every alert should include transaction context, triggered scenarios, model reasoning, connected entities, customer-risk information, and prior decisions, then record reviewer actions, escalations, reporting decisions, and supporting documents in one controlled workflow.

- Intelligent Routing Logic: Segment new flags into specialized human investigator lines based on calculated risk scores, specific typologies, and institutional SLAs.

- Workspace Dashboard Integration: Connect the scoring pipeline directly into an interactive case management integration interface to display complete customer profiles.

- Audit Registry Preservation: Permanently lock down the exact model versions, raw statistical features, and manual override reasoning codes for every alert.

- Controlled Narrative Assistance: Use secure, internal language models to help human compliance officers draft standard suspicious activity summary texts.

- Repeat Activity Monitoring: Link closed cases to automated tracking flags to highlight recurring suspicious patterns if the same entity triggers rules later.

Intellivon intentionally designs case management workflows around the specific evidence a compliance officer, internal auditor, or federal bank examiner must later use to reconstruct a decision.

For a deeper breakdown of alert-review and narrative support, see our guide on Can AI Copilots Reduce False Positives in AML Monitoring?. Once the workflow is connected, the system must prove that its models and thresholds remain effective after deployment.

6. Validate, Shadow-Test, Deploy, and Monitor Models

A monitoring platform should enter production only after historical backtesting, shadow-mode comparison, validation of model behavior, threshold review, and documented human oversight.

After launch, teams must monitor drift, alert quality, typology coverage, analyst outcomes, model versions, and retraining triggers instead of assuming performance remains stable.

- Historical Program Backtesting: Run your new machine learning algorithms against past ledger records to verify that they accurately catch known historical threats.

- Champion-Challenger Evaluations: Route small fractions of live production traffic to parallel testing models to evaluate performance before updating your core logic.

- Shadow-Mode Execution Runs: Operate the entire automated platform in a hidden background environment alongside your legacy system to compare raw alert outputs safely.

- Conversion Rate Analytics: Track key performance indicators including overall false positive rates and the specific alert-to-SAR conversion rate during testing.

- Drift and Registry Tracking: Set up automated MLOps transaction monitoring pipeline parameters to log data variance, version changes, and manual parameter overrides instantly.

Our development teams construct strict deployment gates, unified model registries, and immutable logging monitors directly into your tech stack. This ensures that any performance decay or shifts in transactional data properties trigger immediate engineering warnings before they can impact your legal compliance standing.

The remaining commercial question is the investment required for each delivery stage.

How Much Does AI Transaction Monitoring Platform Development Cost?

A custom AI transaction monitoring platform typically requires a $60,000 to $220,000 build budget. While a simple validation overlay sits at the lower end of this spectrum, a multi-rail platform with real-time scoring capabilities, model governance layers, and complete SAR evidence tracking moves closer to the $220,000 limit.

Ultimately, your definitive transaction monitoring platform development cost depends directly on transaction volume, structural system complexity, and specific regulatory obligations.

1. Cost Breakdown by Platform Scope

| Platform Scope | Estimated Build Range | Suitable For | Included Capability |

| Focused Monitoring Overlay | $60,000–$100,000 | Fintechs optimizing old rule frameworks | Simple data ingestion, rules, alert scoring, basic analyst dashboard |

| Integrated Transaction Platform | $100,000–$160,000 | Wallets, PSPs, and growing neobanks | Real-time scoring, behavioral models, screening links, secure workflows |

| Production-Ready Enterprise Platform | $160,000–$220,000 | High-volume banks and fintech networks | Multi-rail pipelines, graph tools, model validation, advanced audit trails |

2. Phase-Wise Development Cost Breakdown

Building a defensible system requires dividing your financial resources across eight distinct implementation steps. Consequently, organizing your budget by clear technical milestones helps your engineering team stay aligned with regulatory requirements while keeping development transparent.

| Development Phase | Cost Range | What Is Included |

| Risk Scoping & Compliance Mapping | $8,000–$15,000 | Defines your payment-rail maps, coverage gaps, and individual review ownership levels. |

| Data Ingestion & Normalization | $15,000–$35,000 | Connects your core banking feeds, processor APIs, and detailed ISO 20022 mapping scripts. |

| Rules & Alert Engine | $10,000–$25,000 | Deploys your static scenario libraries, strict alert thresholds, and logical routing tables. |

| ML Scoring & Behavioral Analytics | $15,000–$45,000 | Funds your supervised training runs, historical baselines, and SHAP explainability variables. |

| Graph & Entity-Resolution Layer | $12,000–$35,000 | Covers identity matching, counterparties, and advanced layering detection algorithms. |

| Case, SAR, & Reporting Integration | $10,000–$30,000 | Builds out your investigator dashboard queues, evidence bundles, and FinCEN formatting scripts. |

| Security, Validation, & Governance | $10,000–$35,000 | Establishes role-based access rules, immutable audit logs, backtesting, and model validation logs. |

| Deployment & Monitoring | $5,000–$22,000 | Handles your production deployment pipeline, drift trackers, and live operational support. |

Planning a custom monitoring build? Get an AI Transaction Monitoring Cost Quote covering architecture, model scope, integration requirements, governance controls, and phased budget planning.

3. Ongoing Maintenance and Operation Costs

Running a bank AI transaction monitoring platform build requires continuous engineering support. Therefore, annual maintenance, platform monitoring, model refreshing, and compliance updates should be budgeted at 18%–25% of your initial development cost.

Furthermore, these ongoing expenses will rise with additional payment rails, expanded regional jurisdictions, new machine learning families, external data providers, and examiner-driven change requirements.

Build vs Buy: When Should a Bank Own Monitoring Intelligence?

Choosing a build vs buy transaction monitoring platform strategy requires separating your standard checklist requirements from your unique institutional risks. Specifically, institutions should buy commodity tools when simple standardization matters, but they must build custom monitoring intelligence when their distinct product structures, payment networks, or user segments create unique behavior patterns.

Consequently, this engineering choice ensures your core risk strategy remains flexible enough to block advanced modern threats.

1. Strategic Decision Matrix

| Requirement | Buy or Configure Vendor | Build or Customize |

| Standard Watchlist Screening | Suitable to buy | Customize only for API links |

| Common Case Workflow Workspaces | Often suitable to buy | Customize for deep evidence captures |

| Proprietary Behavioral Scoring | Limited fit from vendor | Strong custom-build case |

| Unique Payment-Rail Patterns | Requires heavy configuration | Strong custom-build case |

| Bank-Owned Typology Analytics | High vendor opacity risk | Custom models or software overlays |

| Rapid Launch (Small Team) | Practical buy-first path | Avoid full custom builds initially |

| Model-Governance Accountability | Vendor still needs audit oversight | Build when full ownership adds value |

2. Core Evaluation Questions for Engineering Leaders

Before committing capital to an outside vendor contract, your technical and compliance leadership teams must answer four fundamental engineering questions:

- Logic Validation: Can your internal data scientists validate the underlying mathematical detection logic completely independently during an official federal audit?

- Feature Transparency: Will the third-party software provider openly expose all feature reasoning, training data properties, model versions, and threshold histories to regulatory examiners?

- Hybrid Architecture: Can your team successfully build an intelligent transaction monitoring system development overlay to keep your own behavior models while purchasing standard case wrappers?

- Value Extraction: Does a modular scoring overlay create immediate, measurable business value without requiring you to replace your entire legacy core system?

Ultimately, deploying your platform inside a secure private deployment AML setup or using a cloud-native AML platform allows your bank to maintain strict control over sensitive customer information. Custom software development makes sense when owning your risk intelligence creates superior data defensibility or reduces annual compliance operation costs.

This long-term strategic value means we must now evaluate the scenarios where custom software might face practical operational limitations.

What is the ROI of A Transaction Monitoring Platform?

An AI transaction monitoring platform earns its budget only when it improves detection quality, investigator capacity, and audit evidence together. Consequently, a lower overall alert volume alone is not proof of software engineering success. Buyers must track whether the system identifies meaningful financial risks much earlier, supports faster human-in-the-loop alert review steps, and preserves comprehensive digital files for regulatory reviews.

Recent banking data highlights that more than 90% of traditional rule-based alerts are false positives, consuming approximately 42% of all internal compliance resources. Therefore, replacing legacy setups with custom machine learning pipelines delivers concrete financial returns across key performance metrics.

1. Measurable AML Outcomes KPI Matrix

| KPI Target | What It Measures | Why It Matters | Real-World Target Benchmark |

| False-Positive Rate Reduction | Decrease in total alerts closed without escalation | Proves massive analyst-noise reduction | 40% to 60% drop against old rules |

| Alert-to-SAR Conversion Rate | Proportion of alerts resulting in formal reports | Confirms superior model signal quality | 2x to 4x increase in real threats caught |

| Time to Alert Disposition | Review effort required from alert to final decision | Quantifies daily operational efficiency | 115 minutes saved per analyst per shift |

| Fraud Prevention Lift | Tested detection across priority risk patterns | Prevents narrow algorithmic optimization | 49% improvement in overall rail security |

| Audit Preparation Speed | Drop in time needed to collect regulator files | Supports end-to-end FFIEC readiness | 40% reduction in manual document pulling |

| Compliance Cost Reduction | Total drop in software management overhead | Lowers institutional administrative costs | 35% savings via cloud-native AML setups |

2. Balancing Precision and Absolute Detection

When evaluating your monitoring platform ROI, your technical teams must not optimize the software to reduce alerts at the expense of safety. A sound KPI framework balances a lower daily workload with improved threat detection.

- Regulatory Penalty Avoidance: Global tracking reports indicate that institutions implementing advanced models cut compliance gaps by 37% and avoid an average of $8.5 million in annual regulatory penalties.

- Significant Noise Reduction: Prominent financial institutions like HSBC have proven that deploying machine learning reduces false positives by 60% across hundreds of millions of monthly transfers.

- Increased Catch Rates: This same algorithmic optimization simultaneously catches 2x to 4x more genuine suspicious activity than legacy systems.

- Blind Spot Prevention: Balancing these metrics ensures that your engineering team safely increases accuracy without creating dangerous processing gaps in your network rails.

Ultimately, your tracking metrics should validate that the system successfully lowers the cost per investigated alert while stabilizing your model drift detection TMS parameters.

Build a Defensible AI Transaction Monitoring Platform With Intellivon

Intellivon builds custom AI transaction monitoring infrastructure for banks, fintech platforms, payment processors, digital wallets, and regulated financial products. The platform is designed around transparent detection decisions, production-ready integrations, controlled compliance workflows, and the evidence teams need to review alerts with confidence.

With Intellivon, your team can:

- Design real-time and batch monitoring architecture around ACH, wires, card payments, wallets, instant payments, and cross-border flows.

- Build hybrid detection using scenario rules, behavioral scoring, anomaly detection, and graph analytics.

- Integrate core banking, payment processors, screening tools, case-management systems, and SAR-support workflows.

- Implement explainability, model versioning, validation support, audit trails, and reviewer controls.

- Plan a phased development budget around transaction volume, payment risk, integration complexity, and governance scope.

Plan an AI transaction monitoring platform roadmap with Intellivon, built around your payment flows, monitoring evidence, model-governance obligations, and deployment budget.

Conclusion

An AI transaction monitoring platform is a complex financial-crime control system, not just an alert dashboard with a model attached. Building a bank-grade solution requires integrating full payment rail coverage, a dual real-time streaming and batch architecture, hybrid detection scoring, and deep case evidence logging.

Furthermore, U.S. financial buyers must rigorously evaluate their core infrastructure design against current FinCEN mandates, FFIEC examination guidelines, and the newly revised 2026 interagency model-risk management framework. Ultimately, investing in custom development becomes fully justified when a regulated financial institution requires complete, transparent ownership of its monitoring intelligence to confidently govern its sensitive transaction data, machine learning models, and human compliance choices.

Things to Know About AI Transaction Monitoring Platform Development

Q1. How Much Does AI Transaction Monitoring Platform Development Cost?

A1. Development ranges from $60,000 to $100,000 for an overlay, $100,000 to $160,000 for an integrated platform, and $160,000 to $220,000 for a production-ready enterprise build. Annual maintenance requires budgeting an additional 18% to 25% of initial costs.

Q2. How Long Does It Take to Build an AI Transaction Monitoring System?

A2. To build an AI transaction monitoring system, it takes 10 to 14 weeks for a basic overlay, 4 to 7 months for a production fintech system, and 7 to 12 months for enterprise banking platforms. At the same time, data access speed dictates timelines.

Q3. Should Transaction Monitoring Stay Rule-Based or Become AI-Driven?

A3. The ideal system uses a hybrid model. Deterministic rules manage strict thresholds and sanctions, machine learning ranks behavioral risk anomalies, and graph analytics track hidden networks. At the same time, human compliance reviewers make all final escalation and legal filing decisions.

Q4. Can AI Automatically Close False-Positive AML Alerts?

A4. Automated alert closure should never be the default setup. Platforms must begin with automated prioritization and human verification. At the same time, tightly defined low-risk closures can occur only after independent mathematical validation, strict audit logging, and formal compliance approval.