Key Takeaways:

-

AI AML monitoring reduces false positives when combining validated alert scoring, behavior-based risk signals, and explainable reason codes.

-

HSBC benchmarks show over 60% fewer false positives and two to four times more confirmed suspicious activity.

-

Rule thresholds, ML scoring, copilot summaries, and auto-closure require separate controls under FFIEC expectations.

-

Custom alert-optimization builds cost $60,000 to $250,000 with 18 to 25% annual maintenance costs.

-

How Intellivon maps compliance controls, SR 26-2 guidance, and production workflows before any deployment rollout begins.

Yes, AI copilots can reduce false positives in AML monitoring. They do it by scoring each incoming alert against a behavioral baseline, so investigators see a ranked risk queue instead of raw alert volume. That shift moves a compliance team from chasing noise to investigating genuinely suspicious activity.

Without continuous retraining on fresh investigator feedback and behavioral signals, a copilot cannot sustain that reduction. The model freezes at its starting calibration, and alert quality decays back toward the original false positive rate within months. But adaptive models fed with fresh feedback and live risk signals have cut false positives by 45% and sustained that number over time.

Intellivon has spent over ten years building AI AML monitoring systems for financial institutions, neobanks, and payment platforms. Every build starts with the behavioral baseline model and retraining pipeline first, so the copilot explains every alert score to investigators and examiners. This post draws from our experience and covers how we develop such a platform from the ground up.

What are False Positives in an AML Monitoring System?

An AML false positive is an incorrect system alert that incorrectly classifies a legitimate financial transaction as a financial crime risk. It is a piece of data or software output that mistakes normal customer behavior for money laundering or fraud.

An AML false positive occurs when transaction monitoring software flags a harmless financial transaction as suspicious. This mistake forces human compliance teams to manually review safe, legitimate customer activities, which slows down operations and spikes compliance costs.

Why False Positives Happen

- Static Thresholds: Legacy systems trigger alerts on fixed rules, such as any wire transfer exceeding $10,000, without looking at historical customer habits.

- Lack of Context: Software often fails to recognize regular business operations, like a retail store depositing cash every Monday morning.

- Data Silos: Systems rarely connect external customer profiles with real-time transaction data, missing the full picture of a user’s normal behavior.

The Real-World Impact

When 90% to 95% of generated alerts are false alarms, investigator teams experience severe burnout. Furthermore, financial institutions waste millions of dollars annually reviewing safe transactions rather than catching actual financial crime.

What False Positives Cost an AML Operations Team Before AI

An AML false positive is an incorrect system alert that improperly flags a legitimate financial transaction as a financial crime risk. These system errors create severe capital drains through manual analyst fatigue, delayed high-risk queues, and heavy audit trails.

Consequently, the global compliance software market will reach $68.93 billion in 2026, according to Business Research Insights’ Compliance Software Report, as firms look to fix plummeting compliance officer productivity.

1. Plunging Compliance Officer Productivity

Legacy rule-based transaction monitoring software forces your team to review thousands of junk alerts every single month. Because these static rules completely lack behavioral context, senior compliance officers spend most of their workday performing repetitive data entry:

- The Manual Loop: Investigators waste hours checking basic account details across separate dashboards.

- Operational Bottlenecks: This slow workflow causes massive case backlogs, which prevents teams from meeting strict internal deadlines.

2. High False Positive Cost Per Alert

Every mistaken flag carries a fully loaded payroll and software infrastructure cost that scales linearly with your overall transaction monitoring alert volume. Therefore, failing to optimize your core rule parameters directly inflates your daily compliance overhead:

- Wasted Capital: Processing high alert volumes costs institutions between $20 and $50 per false alarm.

- Budget Exhaustion: As highlighted by KBV Research’s Global AML Industry Outlook, these small, repetitive costs quickly accumulate into millions of dollars of annual operational waste.

3. Skyrocketing Transaction Monitoring Alert Volume

As digital payments and real-time transfers expand, legacy systems generate a higher frequency of false alarms. Consequently, your operational burden multiplies because the old software cannot differentiate between a legitimate payment velocity spike and a true structuring threat:

- False Alarms: Up to 95% of all system-generated flags are completely harmless.

- Data Overwhelm: Compliance infrastructure faces severe strain from the constant influx of raw, unfiltered risk signals.

4. Delayed Review of Critical Risks

When analysts are buried under harmless alerts, genuinely dangerous transactions remain unreviewed for days. Furthermore, this delay creates a massive regulatory vulnerability that exposes your platform to severe financial penalties and structural security compliance failures:

- Hidden Threats: True financial crime hidden within the noise is often missed entirely.

- Regulatory Exposure: Delayed filings directly breach FinCEN expectations, inviting costly federal enforcement actions.

In short, traditional transaction monitoring engines create a compounding financial and operational drain that actively undermines your compliance mission. When 95% of your alert output yields zero actionable intelligence, your team is simply managing software noise rather than stopping financial crime.

Therefore, maintaining this infrastructure directly harms your bottom line while increasing your vulnerability to regulatory penalties.

Can AI AML Monitoring Software Reduce False Positives Safely?

Yes. An AI AML monitoring software system can safely reduce false positives when it helps score, group, prioritize, and explain alerts while the institution separately validates detection quality, human decision authority, and audit evidence.

The core goal is not fewer alerts alone. Instead, the true goal is fewer low-value reviews without losing suspicious activity visibility across your network.

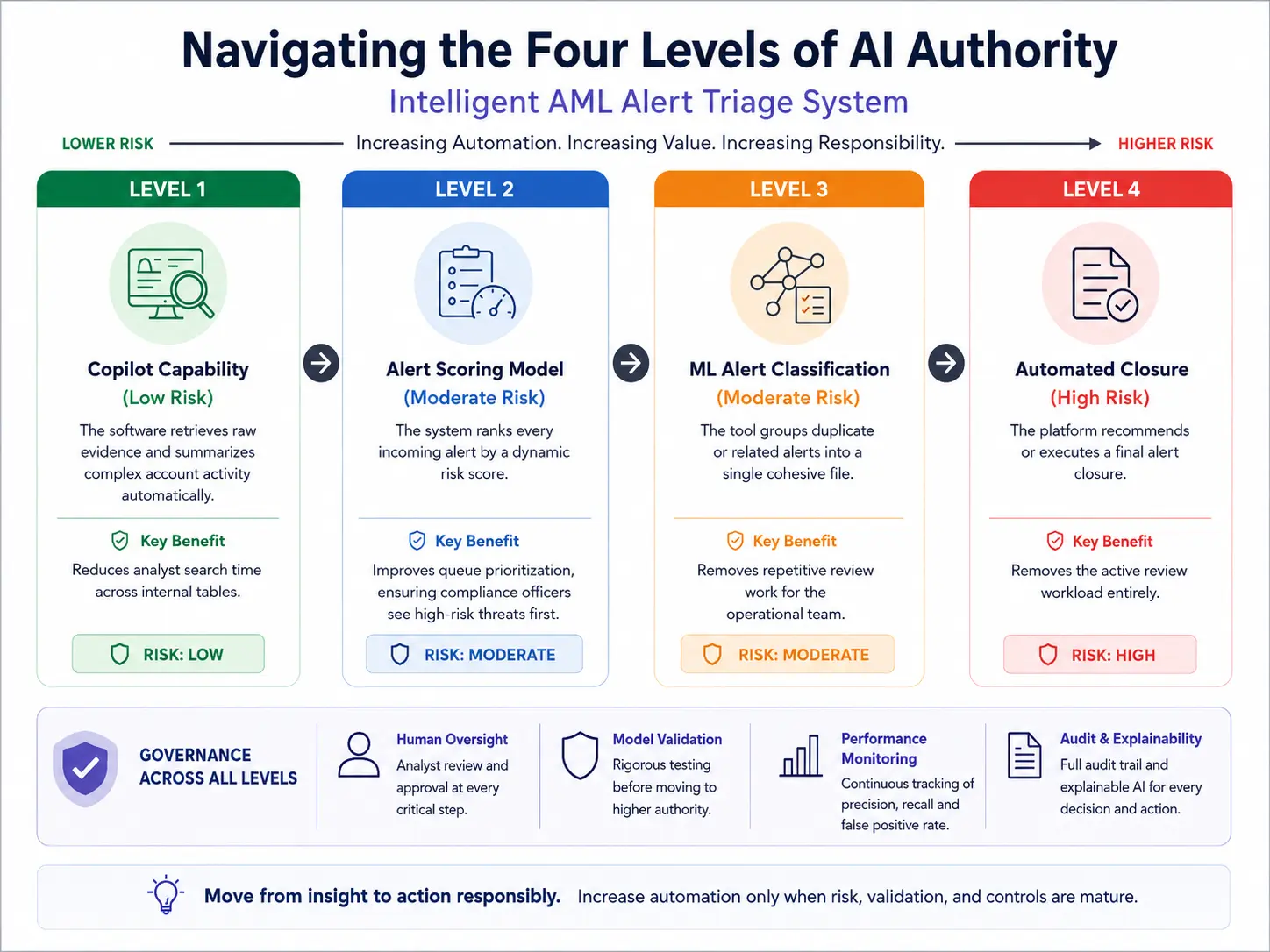

1. Navigating the Four Levels of AI Authority

When deploying an intelligent AML alert triage system, your engineering team must define clear limits for the software. Therefore, mapping out the precise operational value and decision risk across different automation levels prevents compliance drift:

- Level 1: Copilot Capability (Low Risk): The software retrieves raw evidence and summarizes complex account activity automatically. Consequently, this step reduces analyst search time across internal tables.

- Level 2: Alert Scoring Model (Moderate Risk): The system ranks every incoming alert by a dynamic risk score. This data ranking improves queue prioritization, ensuring compliance officers see high-risk threats first.

- Level 3: ML Alert Classification (Moderate Risk): The tool groups duplicate or related alerts into a single cohesive file. As a result, it removes boring, repetitive review work for your operational team.

- Level 4: Automated Closure (High Risk): The platform recommends or executes a final alert closure. While this removes the active review workload entirely, it requires strict model validation before deployment.

2. Analyzing Real-World Production Benchmarks

Looking at real industry cases helps establish a realistic expectation for this technology. For instance, according to the Google Cloud AML AI Case Study, HSBC used a bespoke machine learning model to enhance its customer monitoring framework. This production deployment yielded remarkable operational metrics:

- Fewer False Alarms: The bank achieved more than 60% fewer false positives compared to its legacy rules.

- Better Signal Catching: The team detected two to four times more confirmed suspicious activity.

However, you should view this as a single published production example rather than a universal guarantee. Every financial platform features unique transaction velocities and risk profiles that affect performance.

3. Establishing Safe Technical Guardrails

To reduce AML alert false positives with AI without raising your regulatory risk, you must implement strong infrastructure guardrails. Consequently, safe optimization requires balancing model precision with strict federal audit expectations:

- Recall Testing: You must run typology-level recall testing to ensure the AI does not drop true money laundering patterns.

- Human-in-the-Loop Review: Human compliance officers must maintain final AI copilot AML alert management authority over high-risk flags.

- Audit Trails: The system must generate clear, timestamped audit trail alert decisions for every automated scoring change to satisfy regulators.

- Model Validation: Engineers must build a continuous false negative risk management framework to detect underlying data drift.

In conclusion, an AI copilot should always begin with recommendation and prioritization authority rather than unrestricted closure authority. Giving the software full permission to close alerts too early introduces heavy compliance risks that examiners will penalize.

Therefore, letting human experts verify the model’s logic builds the trust needed for deeper automation.

How Many AML Alerts Can You Safely Retire Without Missing Risk?

You can safely retire between 30% and 50% of your current transaction monitoring alerts by using an alert retirement budget. This exact number is the total volume of low-risk, repetitive false alarms your system can remove while keeping your true criminal tracking rate at 100%.

Consequently, this data-backed strategy ensures you lower your daily overhead without dropping critical risk visibility.

The Alert Retirement Budget Framework

An alert retirement budget is the maximum reduction an institution can approve while its detection, escalation, and audit controls remain within documented limits. Therefore, your engineering and product teams must validate the following parameters to secure regulatory sign-off:

| Approval Metric | Baseline Required | Go-Live Evidence Required |

| Alert reduction rate | Current false-positive volume by scenario | Reduction results by scenario and risk tier |

| Recall by typology | Known suspicious outcomes for structuring, layering, mule behavior, velocity patterns | Challenger-model results and sampled reviews |

| Alert-to-SAR conversion | Existing escalation and filing pathway | Conversion quality after tuning |

| Analyst overrides | Current disposition patterns | Override reason analysis |

| Auto-closure quality | Current closure categories | QA sampling and exception review |

| Drift exposure | Customer, payment, and product changes | Monitoring thresholds and retraining trigger architecture |

Mandatory Operational Guardrails

To implement this framework safely, you must follow strict, risk-based operational guardrails during development and rollout:

- No Universal Assumptions: Do not invent a universal safe alert-reduction percentage, as your budget must rely solely on institution-approved tolerances.

- Pilot Phase Dual Control: Require 100% human review for high-risk alert categories during your initial pilot deployment.

- Rigorous Backtesting: Require documented QA sampling and deep backtesting of transaction monitoring rules for any proposed automated closure path.

- Immediate System Freezes: Stop deployment expansion immediately if model validation false positive tests show that recall or typology coverage has deteriorated beyond approved limits.

In short, a lower alert count is not a valid operational outcome until the institution proves exactly what transactions remained detectable across the network. Simply clearing out data queues to lower your operational burn rate will cause catastrophic failures during an audit.

Therefore, you must prove that your alert-to-SAR conversion rate improvement matches your false negative risk management limits before retiring rules.

Where an AI Copilot Fits in the Alert Disposition Workflow

An AML copilot should initially sit directly between alert generation and analyst disposition. It can retrieve background evidence, group related customer activity, score risk priority, and draft a reasoned investigation recommendation.

However, the system must not silently change transaction monitoring thresholds, approve final SAR decisions, or close high-risk alerts until the institution has validated that software authority separately through rigorous audit testing.

AI Copilot Role Within Workflows

| Workflow Layer | What It Does | Copilot Role |

| Transaction ingestion | Collects payment, account, customer, and counterparty data | No decision authority |

| Rules and scenarios | Detects typology-linked patterns | Receives triggered alert context |

| ML alert scoring | Estimates risk priority | Explains score drivers |

| Entity resolution | Groups related accounts and duplicate signals | Reduces repeat review work |

| Evidence retrieval | Pulls KYC, activity history, prior cases, and records | Summarizes findings |

| Disposition workflow | Records final investigation outcome | Recommends; analyst approves |

| Audit and SAR pathway | Retains traceability and escalation history | Logs evidence and reasoning |

Maintaining this strict separation of powers ensures your platform abides by standard banking governance expectations. Therefore, deploying this multi-layered framework allows analysts to accelerate daily case resolutions while creating a bulletproof audit trail alert decisions ledger for federal examiners to review.

For a deeper breakdown of full copilot workflows, see our guide on How Can Banks Develop an AI AML Compliance Copilot Platform?.

In short, an AI copilot functions best as an intelligent data aggregator rather than a standalone compliance judge. By positioning the software as an alert triage automation assistant, you instantly eliminate the tedious research phase that slows down your active investigator operations.

Which AI Models Reduce AML Alert False Positives?

Achieving effective machine learning AML false positive reduction requires a layered model stack rather than a standalone language model. Traditional deterministic rules preserve your known criminal typologies while supervised models rank incoming risk based on historical data.

Concurrently, behavioral analytics and graph networks detect hidden entity relationships and unusual network transfers.

Finally, an LLM copilot explains the aggregated evidence to support the final alert classification, while human analysts retain complete control over all material decision-making.

Consequently, each specialized software component plays a distinct role in filtering out systemic noise without creating dangerous visibility gaps across your payment networks.

AI Model Table

| Model or Component | Works On | Role in False-Positive Reduction | Evidence Required |

| Deterministic AML rules | Defined thresholds and typologies | Preserves known regulatory scenarios | Rule versions, approvals, backtesting |

| Gradient boosted trees / XGBoost | Labelled alert outcomes and customer features | Scores alert priority efficiently | Precision, recall, SHAP values, segment testing |

| Random forest challenger | Same labelled dataset | Provides benchmark comparison | Challenger results and variance checks |

| Behavioral analytics | Customer behavioral baseline and peer group analysis | Identifies deviations from normal activity | Feature definitions and review sampling |

| Anomaly detection | Unusual payment patterns or velocity shifts | Surfaces new or rare behavior | False-negative review and investigator feedback |

| Graph analytics / GNNs | Linked customers, counterparties, devices, accounts | Detects layering and connected activity | Explainable subgraph evidence |

| Entity resolution and clustering | Duplicate or related alerts | Groups repeat signals for combined review | Matching rules and QA review |

| LLM copilot with grounded retrieval | Case files, transaction evidence, KYC documents | Drafts summaries and disposition reasoning | Source citations, access controls, analyst approval |

Engineering and compliance teams must realize that deep learning transaction analysis should only enter the system design when transaction volumes, complex sequencing problems, and high volumes of labelled evidence actively justify its heavy validation burden.

For simpler transaction types, lightweight algorithms function perfectly and cost significantly less to audit. For a deeper breakdown of monitoring infrastructure, see our guide on How To Build an AI-Powered Transaction Monitoring System?.

In short, an efficient automated triage engine relies on a carefully tuned combination of traditional math, advanced network graphs, and clear language models. Relying on an isolated artificial intelligence framework will either miss hidden fraud patterns or create a rigid system that fails basic regulatory model risk checks.

How an AI-Powered AML Alert Tuning Platform Tunes Rules Without Hiding Risk

Yes, an AI-powered AML alert tuning platform can safely fix broken tracking rules by acting as a smart testing lab instead of making quiet changes on its own. The software simply scans your historical data to find bad settings, drafts a list of safer rule adjustments, and presents the evidence to a human compliance manager for final approval.

Consequently, the system never silently deletes safety controls or turns off alerts without a human officer signing off on the change first.

1. Scenario Tuning AML Monitoring

Scenario tuning AML monitoring ensures that your tracking boundaries adapt to real customer trends instead of fixed assumptions.

Consequently, this step involves parsing rule tuning AML transaction monitoring parameters across highly specific criminal patterns like structuring, layering, unusual transaction velocity, and peer-group deviation:

- Typology Analysis: The platform reviews individual scenario performance by product, geography, and risk tier to see where boundaries are too wide.

- Smart Adjustments: Instead of generic filters, the software alters specific code logic to match real-world user activity profiles.

2. Threshold Optimization and Suppression Logic

Executing threshold optimization AML rules allows your engineering team to clear out predictable system noise safely without dropping your defense guardrails.

Through automated alert suppression logic, the software groups duplicate data points and applies related-alert clustering across interconnected accounts:

- Duplicate Detection: The tool bundles thousands of identical payment alerts into a single case file to stop repeat work.

- Exception Protection: High-risk profiles and watch-list entries automatically bypass the suppression filters to ensure they always get a manual review.

3. Champion-Challenger Testing Before Release

You should never push new alert boundaries live without running thorough champion-challenger model testing. Consequently, implementation setups should run parallel A/B testing AML models in controlled test environments using real, historical ledger data before updating any live system rules:

- Backtesting Logic: The software runs your new rules against past case datasets to check the exact precision-versus-recall metrics.

- Human Verification: Human compliance officers check a random sample of the alerts that the new system wants to close to verify the logic is sound.

In short, system tuning is safe only when every reduced alert category remains completely traceable, reversible, and measurable. Attempting to change software rules based on unbacked algorithmic suggestions will instantly break model validation rules during a regulatory examination.

How We Build an AI AML Alert Optimization System

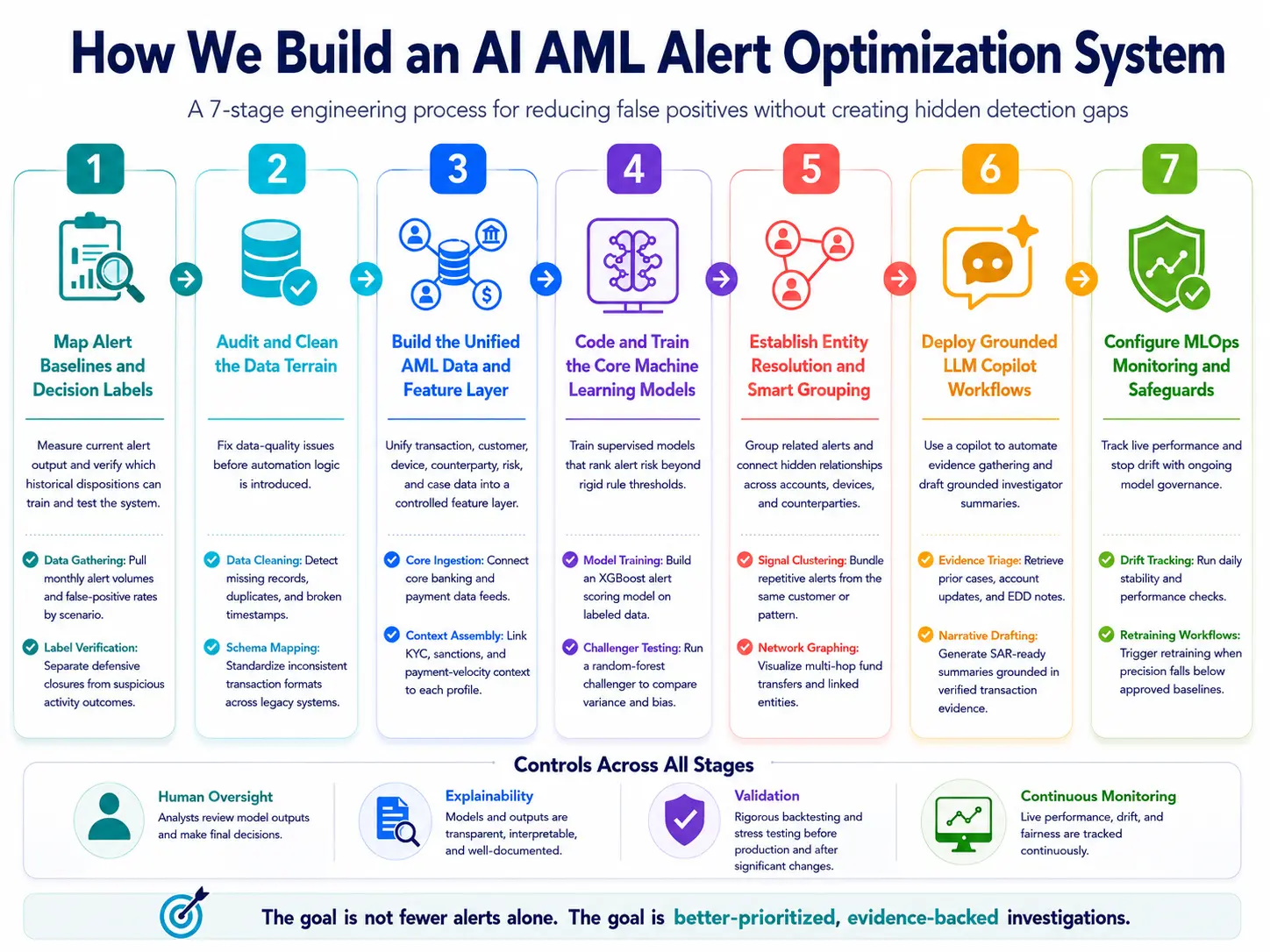

Building an AI AML alert optimization system requires a controlled, seven-stage engineering process. Our teams baseline the institution’s current alert economics, clean the data terrain, construct a unified feature layer, program the core machine learning models, group related signals, deploy grounded large language models, and establish automated model monitoring.

Each stage must prove that a reduced review workload does not create hidden detection gaps across your payment network.

Consequently, this step-by-step framework transforms your transaction tracking from a rigid, rule-based grid into a flexible, compliant fortress.

1. Map Alert Baselines and Decision Labels

The first step is to measure your current alert output and determine which historical dispositions can train or test the system. Without dependable closure labels, SAR review outcomes, escalation reasons, and analyst effort data, your institution cannot prove that a lower alert rate represents improvement:

- Data Gathering: We pull your historical monthly alert volumes and false-positive rates by scenario to locate your biggest operational bottlenecks.

- Label Verification: Our engineers review past case files to separate clean, defensive rule closures from actual suspicious activity reports.

At Intellivon, we begin by converting your raw alert histories, case management files, and historical analyst actions into an empirical, mathematical baseline. This structured data foundation serves as the benchmark that all our future machine learning model updates must outperform to prove their real-world value.

Consequently, once these historical labels are verified, the engineering focus shifts directly to your primary live transaction feeds.

2. Audit and Clean the Data Terrain

The second step requires auditing your active system databases to fix data quality gaps before introducing any automation logic. If your underlying records contain duplicate fields, missing country codes, or broken timestamps, your machine learning models will produce inaccurate risk priority calculations:

- Data Cleaning: The system runs automated validation checks to find missing customer records and patch fragmented ledger entries.

- Schema Mapping: We align inconsistent transaction formats from disparate legacy software tools into a single, standardized data format.

Our development teams establish a clear build-versus-buy boundary during this phase by constructing custom data cleaning scripts tailored precisely to your specific banking infrastructure. This custom engineering prevents your pipeline from processing corrupted data, which eliminates the root cause of many systemic false alarms.

Therefore, cleaning your active data channels ensures your primary infrastructure can support deep behavioral tracking.

3. Build the Unified AML Data and Feature Layer

The third step is to unify transaction, customer, device, counterparty, risk, and case data into a controlled feature layer. This structured data environment allows your models to evaluate long-term financial behavior over time rather than relying only on isolated transaction amounts:

- Core Ingestion: We set up a secure core banking system integration alongside a real-time payment processor integration to capture live fund shifts.

- Context Assembly: The platform automatically links incoming KYC records, sanctions screening files, and payment velocity monitoring feeds to each active profile.

Intellivon designs this underlying data layer with completely traceable feature definitions, strict role-based access controls, and versioned ingestion pipelines. This rigorous architecture ensures that every single feature calculation can be fully reconstructed later during an official regulatory audit.

As a result, building this unified context allows your software to execute complex peer group analysis without experiencing lag.

4. Code and Train the Core Machine Learning Models

The fourth step involves programming the supervised machine learning models that calculate your actual alert risk priority scores. Instead of relying on rigid thresholds, this layer uses advanced statistical mathematics to separate true criminal threats from everyday consumer spending habits:

- Model Training: We build and train an optimized XGBoost transaction monitoring model using your historical, labeled transaction datasets.

- Challenger Testing: The infrastructure runs a parallel random forest alert classification model to check for variance and prevent algorithmic bias.

Our practitioner approach focuses on training these models strictly within your platform’s approved risk tolerances to maintain absolute precision. We optimize the system to identify complex financial crime indicators, such as structuring detection accuracy and layering detection precision, across all asset classes.

Consequently, maximizing model accuracy ensures that your downstream compliance teams can focus their energy on truly dangerous alerts.

5. Establish Entity Resolution and Smart Grouping

The fifth step implements entity resolution alert deduplication to group related alerts and duplicate signals into a single case file. This layer scans your network to connect hidden relationships between different account holders, shared devices, and cross-border counterparties:

- Signal Clustering: The tracking engine automatically bundles repetitive alerts triggered by the same customer within a short window.

- Network Graphing: We deploy advanced graph neural networks AML alerts to visualize complex, multi-hop fund transfers across public and private networks.

We assemble these grouping mechanisms as a non-disruptive triage layer that sits directly on top of your existing core database. This setup allows your compliance department to review a single, comprehensive network anomaly detection profile rather than opening ten identical alerts.

Therefore, removing these redundant tracking files drastically increases your daily compliance officer productivity.

6. Deploy Grounded LLM Copilot Workflows

The sixth step introduces an AI copilot AML alert management workspace to automate your manual evidence-gathering tasks. The language model reads the structured data from your core models, pulls relevant files, and writes clear summaries for human investigators:

- Evidence Automated Triage: The system scans your historical files to find prior cases, account updates, and linked enhanced due diligence notes.

- Narrative Drafting: The copilot generates legal-grade SAR narrative drafts and case summaries based solely on verified transaction records.

Intellivon explicitly separates your quantitative model scoring logic from your qualitative copilot language generation engines. This strict separation ensures that human reviewers can instantly see the exact mathematical drivers behind every score, ensuring total SHAP values alert explainability.

As a result, grounding the text output in raw transaction evidence protects your platform from dangerous algorithmic hallucinations.

7. Configure MLOps Monitoring and Safeguards

The final step deploys continuous MLOps alert model monitoring pipelines to track live system performance and stop algorithmic drift. Because consumer transaction patterns change constantly, your machine learning models require automated guardrails to remain accurate over time:

- Drift Tracking: The platform runs automated model drift detection AML checks every day to ensure the scoring logic remains stable.

- Retraining Workflows: We build an automated retraining trigger architecture that flags engineers the moment model precision drops below your approved baseline.

Our implementation teams structure this final layer around versioned model tracking databases, secure code rollback paths, and rigorous zero-trust architecture. This disciplined setup ensures your technical leads can comfortably push continuous model improvement AML updates without disrupting your live production lines.

What SR 26-2 Changes for AI AML Monitoring Software in 2026

The Federal Reserve’s SR 26-2 guidance changes how financial institutions must classify and govern AI used in AML monitoring. Quantitative alert-scoring engines and machine learning tracking algorithms fall squarely within this updated, risk-based model risk management framework.

However, generative AI summaries and agentic copilots fall outside that specific definition, yet regulators still require you to maintain verified data controls, rigid test logs, security limits, and clear human oversight over their final text outputs.

Consequently, mapping out your structural compliance obligations ensures that your modern software passes strict federal inspections.

Changes By SR 26-2

| AML System Component | Governance Question | Evidence the Institution Should Retain |

| Deterministic rules and thresholds | Are filtering criteria reasonable and independently verified? | Rule inventory, approvals, version history, testing, backtesting results |

| XGBoost or statistical alert score | Is the model valid for its intended AML use? | Development record, data lineage, validation report, performance monitoring, outcome analysis |

| Behavioral or network model | Does it identify relevant patterns without creating unexplained bias or missed risk? | Feature definitions, segment results, typology tests, drift monitoring |

| Generative AI copilot summary | Does it present grounded evidence without independently making a regulated decision? | Source retrieval logs, prompts, response controls, analyst approval records |

| Agentic closure workflow | What authority has the institution allowed, and under which controls? | Approval policy, exception routing, sampled QA, access logs, rollback control |

| Third-party vendor platform | Can the institution validate outcomes even if full internal methodology is unavailable? | Vendor documentation, limitations, customizations, ongoing monitoring, outcome analysis |

A critical structural shift under the new guidance changes how institutions must look at their core infrastructure:

- Rule Classification: Simple deterministic rules are not automatically treated as formal models under the updated SR 26-2 framework.

- Basic Expectations: Standard FFIEC monitoring expectations still require you to maintain reasonable filtering criteria and independently verified programming logic across all legacy screens.

- The AI Boundary: While generative and agentic AI tools sit completely outside the formal model risk management AML scope, they are never exempt from core corporate governance responsibility.

In short, an AI copilot tool cannot inherit an automatic compliance approval merely because your underlying transaction scoring model successfully passed its validation check. Each layer of your software stack introduces unique security risks that require separate, documented testing logs to satisfy federal examiners.

Can an AI Copilot Auto-Close AML Alerts, or Only Prioritize Them?

No, an AI copilot cannot automatically close alerts on its own when you first deploy it. Initially, the software only has the power to prioritize your data queues and gather transaction evidence for human analysts to review.

Consequently, giving a computer engine the immediate authority to auto-close alerts without human oversight creates a massive regulatory vulnerability that federal examiners will penalize during an audit.

Consequently, treating data collection and final decision-making as two entirely separate functions allows your platform to scale safely without violating federal guidelines.

AI Copilot Work

| Level of Authority | What the Copilot Can Do | Initial Production Position |

| Evidence support | Retrieve relevant transactions, KYC data, and case history | Appropriate early use |

| Prioritization | Rank alerts for analyst attention | Appropriate after score validation |

| Grouping | Combine duplicates or linked activity for review | Appropriate with QA testing |

| Closure recommendation | Draft reason and evidence for analyst approval | Appropriate with human sign-off |

| Automatic closure | Close narrowly defined low-risk alerts | Only after controlled validation |

| SAR decision / high-risk | Make regulated escalation decision | Keep human-controlled |

Therefore, software teams should deploy the system as a supportive assistant to reduce AML investigation workload AI while keeping final disposition control in human hands.

How Much Does AI AML Monitoring Optimization Software Cost?

Custom AI AML monitoring optimization software typically costs $60,000–$250,000, with scope driven by data integrations, scoring-model depth, copilot workflow authority, validation rigor, real-time processing requirements, security controls, and audit evidence needs.

Therefore, your upfront budget depends heavily on how much operational authority you plan to give the algorithms.

Understanding these pricing bands allows engineering and product leads to plan their rollout without over-purchasing unnecessary modules. Each stage of the platform build carries distinct development costs that scale based on the complexity of your core banking network.

Development Cost Breakdown

| Development Phase | What It Covers | Estimated Cost |

| Discovery and Scope Mapping | Alert baselines, disposition review, risk tiers, governance boundaries | $8,000–$15,000 |

| Data Engineering & Integration | Core banking, payment, KYC, case systems, APIs, data normalization | $12,000–$40,000 |

| Rule Tuning & Data Prep | Scenario mapping, threshold analysis, closure labels, test datasets | $10,000–$30,000 |

| ML Alert Scoring Engine | XGBoost, behavioral features, clustering, graph or network signals | $18,000–$55,000 |

| Copilot Workflow Assembly | Retrieval, summaries, disposition support, analyst interfaces | $15,000–$45,000 |

| Explainability & Shadow Testing | SHAP evidence, challenger tests, QA sampling, approval reports | $12,000–$35,000 |

| Production Release & MLOps | Monitoring, model versioning, drift controls, RBAC, logging | $15,000–$40,000 |

Solution Scope Bands

- Focused MVP ($60,000–$100,000): Targets one alert family, handles prioritization and evidence retrieval, and requires manual analyst approval.

- Integrated AML Optimization System ($120,000–$180,000): Covers multiple scenarios, features active ML scoring, links with your case management system, and builds governance reporting dashboards.

- Production-Grade Copilot ($180,000–$250,000): Includes multi-system integrations, deep validation testing, automated MLOps tracking, and advanced authority controls.

Ongoing Maintenance Cost

Annual maintenance generally requires 18–25% of the initial build cost for model monitoring, drift review, rule recalibration, retraining, audit updates, security testing, and workflow improvement. Failing to budget for this upkeep will cause your machine learning models to drop in accuracy as consumer payment habits naturally change.

For a deeper breakdown of wider AML copilot budgeting, see our guide on What Does It Cost to Build an AI AML Compliance Copilot?.

Build an AML Alert Optimization Roadmap With Intellivon

Intellivon helps financial institutions build AI AML monitoring software around explainable alert scoring, controlled copilot assistance, secure financial-data integrations, validation evidence, and production monitoring.

1. Enterprise AI Capability Built for Regulated Fintech Workflows

Intellivon combines enterprise AI engineering, machine learning, MLOps, data engineering, secure integrations, and fintech compliance-monitoring capability within one delivery environment.

Verified Intellivon Proof Points:

- 500+ successful AI-driven projects.

- 11+ years of experience delivering AI solutions.

- 200+ dedicated AI experts.

- Fintech AI capability across compliance monitoring, fraud analytics, and risk intelligence.

- Experience shaping AI systems around enterprise security, governance, and production performance.

2. We Understand That Fewer Alerts Are Not the Final Goal

Banks and fintech companies do not need an AI system that simply suppresses alerts. They need a platform that reduces low-value review work while preserving visibility into activity that deserves investigation.

Intellivon designs AML alert optimization around the outcomes compliance leaders actually need to measure:

- False-positive reduction by alert scenario and customer risk tier.

- Investigator time saved without reducing review quality.

- Alert-to-case and alert-to-SAR conversion performance.

- Human overrides, escalation patterns, and closure evidence.

- Typology-level monitoring for structuring, layering, velocity, and network risk.

This matters because a system that reduces noise without proving detection quality creates a new compliance problem instead of solving one.

3. We Build Intelligence That Explains Why an Alert Matters

AML investigators cannot act on an unexplained risk score. They need to see what triggered the alert, which customer or transaction behavior changed, what related entities appeared, and why the system recommended review or closure.

Intellivon can design the platform around the intelligence layers required for meaningful alert decisions:

- Machine learning alert scoring for risk-based prioritization.

- Behavioral baselines that identify unusual customer activity.

- Entity resolution to connect related accounts and transactions.

- Alert clustering to reduce duplicate investigation work.

- Explainable reason codes and evidence-backed copilot summaries.

- Investigator-facing workflows for review, override, and escalation.

The result is not an AI black box. It is an investigation-support system where compliance teams can inspect the evidence behind every recommendation.

4. We Know Where AI Assistance Should Stop

An AML copilot can retrieve evidence, summarize activity, group related alerts, prioritize cases, and recommend next steps. However, it should not receive unrestricted authority over sensitive closure or escalation decisions from the beginning.

Intellivon helps institutions define the correct control boundary for each use case:

- Evidence retrieval and alert summarization for faster reviews.

- Risk-ranked queues for overloaded investigation teams.

- Analyst-approved disposition recommendations for controlled adoption.

- High-risk escalation pathways that remain human-controlled.

- Automatic closure considered only for narrowly defined, validated low-risk categories.

- Audit logs that record the evidence, score, model version, reviewer action, and final outcome.

This approach allows AML teams to gain efficiency while retaining clear ownership of regulated decisions.

5. We Connect AI to the Systems That AML Teams Already Use

An alert optimization platform is only valuable when it can access the data investigators need. Transaction data alone does not provide enough context for a credible AML decision.

Intellivon can engineer secure connections across the institution’s existing compliance environment, including:

- Transaction monitoring engines and existing rule libraries.

- Core banking systems and payment-processing platforms.

- KYC, CDD, customer-risk, and onboarding records.

- Case management and investigator workflow systems.

- Prior alert dispositions and escalation histories.

- Audit, reporting, and compliance review dashboards.

This connected foundation helps the copilot present a complete evidence trail rather than a fragmented transaction summary.

6. We Build Governance Into the Platform, Not Around It Later

AI used in AML monitoring must remain reviewable after deployment. Compliance teams need to know which model version produced an alert score, what evidence supported a recommendation, how thresholds changed, and whether model performance is drifting over time.

Intellivon builds the controls required for accountable production use:

- Explainable model outputs and traceable risk drivers.

- Version-controlled rules, thresholds, models, and prompts.

- Champion-challenger testing before expanding automation authority.

- Model drift monitoring and retraining triggers.

- Role-based access controls and secure audit logs.

- Validation records that support internal governance and examination review.

- Separate controls for statistical scoring models and copilot-generated recommendations.

This is especially important as institutions assess AI AML systems under evolving model-risk and governance expectations.

Build an AML Platform That Reduces Noise Without Reducing Control

Your compliance team should not have to choose between operational efficiency and accountable AML oversight. Intellivon helps you build an AI alert optimization platform that prioritizes meaningful risk, supports investigators with explainable evidence, fits existing financial workflows, and gives governance teams the controls required for production use.

Conclusion

Yes, AI AML monitoring software can successfully reduce false positives, but only when alert reduction remains tightly bound to clear detection evidence, accountable human choices, and constant model validation. To deploy this technology safely, you must always map your internal alert baselines, use a layered model stack over standalone language tools, and give the copilot recommendation authority before granting automatic closure permission.

Furthermore, you must apply the new SR 26-2 rules to your quantitative scoring models while governing generative text and agentic workflows under separate security controls. Ultimately, you should approve your software investment against both measurable operational cost savings and strict, long-term tracking safeguards.

By keeping human investigators in the loop and maintaining clean model audit logs, your firm can confidently achieve a massive compliance cost reduction without compromising your structural security or failing federal regulatory examinations

Things To Know About AI AML Monitoring Software

Q1. Does SR 26-2 Require Validation for an AI Copilot AML Alert Management Workflow?

A1. Yes, but the requirements are split. Quantitative scoring engines require strict model validation under the updated SR 26-2 rules. Generative text engines and agentic tools sit outside this formal model scope. However, banks must still provide documented testing, access limits, human oversight, and audit evidence before letting any copilot tool influence live compliance queues.

Q2. Can Compliance Teams Reduce AML Alert False Positives With AI Without Auto-Closing Cases?

A2. Yes. The software handles risk scoring, duplicate grouping, evidence retrieval, and queue prioritization while human analysts retain final closure authority. Consequently, this safe setup lets you eliminate manual research and lower investigator fatigue without giving up control. It also allows you to measure system recall and analyst overrides before deploying automated closure pathways.

Q3. Should a Bank Buy a Platform or Build an AML False Positive Reduction Platform?

A3. Buy a platform if your workflows are basic and you need speed. Build a custom system if your transaction volume is massive, your core data is trapped in separate legacy banking systems, or you require absolute ownership of your scoring code and underlying evidence logs to pass strict federal model audits.

Q4. Can an AI Copilot Automatically Close False-Positive AML Alerts?

A4. Yes, but only for verified, low-risk cases. The system can auto-close basic alarms after you establish strict authority limits, QA sampling, exception routing, and rollback controls. However, it should never close high-risk profiles, suspicious payment velocity spikes, or complex transaction anomalies without human investigator sign-off.