Key Takeaways

-

The global digital banking platform market is projected to grow from $30.4 billion in 2023 to $168.3 billion by 2032, making platform investment a strategic priority, not an optional upgrade

-

Enterprise digital banking platforms are fundamentally different from online banking portals. They re-engineer entire operations through automation, microservices architecture, and real-time data intelligence

-

Core features like multi-account management, real-time settlement, embedded compliance, and API-first architecture are non-negotiable for platforms built to operate at scale

-

AI capabilities including fraud detection, autonomous decisioning, predictive forecasting, and intelligent process automation are baseline expectations for enterprise-grade builds

-

The most successful platforms in market, from Revolut to Solaris, win not by building everything, but by making deliberate architectural choices early that compound into structural competitive advantages over time

When a banking platform fails on a large scale, it usually occurs because the wrong features were prioritized at the wrong time during development. Enterprise digital banking platforms are assessed differently from consumer fintech products.

An enterprise-grade digital banking platform is defined by a specific mix of capabilities that work well under pressure, across different regions, at a high volume, and within tightly regulated environments. Organizations that invest in or create these platforms need to understand which features are essential, which set them apart, and which are just standard offerings dressed up in marketing terms. This distinction impacts build costs, compliance status, time to scale, and long-term infrastructure issues.

Intellivon specializes in building these kinds of platforms. Our engineering and compliance teams have been involved in the key decisions that determine whether a platform can scale or if it will falter. This blog draws on that experience to detail the features that make up enterprise digital banking platforms and should be considered before starting the build.

Why Are Enterprises Investing in Digital Banking Platforms Now

Enterprises are accelerating digital banking investments as customer expectations shift, fintech competition intensifies, and real-time services become the norm.

Instead of layering features onto legacy systems, banks are adopting platform-based models to reduce operational costs, streamline workflows, and deliver more personalized, data-driven experiences at scale.

The global digital banking platform market is valued at $30.4 billion in 2023 and is projected to reach $168.3 billion by 2032, growing at a CAGR of 20.9%. This rapid expansion reflects how banks are shifting toward platform-led infrastructure to support real-time services, scale operations, and stay competitive in a digital-first financial ecosystem.

1. Meet Changed Customer Expectations

Customer patience for slow banking is gone. Users expect instant onboarding and real-time decisions as a baseline. Digital platforms allow enterprises to redesign journeys, moving from generic products to contextual, mobile-first offers.

2. Break Free from Legacy Systems

Siloed systems slow launches and drive up costs. Modern platforms provide a flexible orchestration layer alongside the core. This reduces time-to-market and enables faster experimentation without risky replacements.

3. Compete with Fintechs and Big Tech

Challengers reset expectations with slick, AI-driven experiences. Enterprises invest in digital platforms to close this gap. By using APIs, they can power embedded finance and unlock new revenue streams.

4. Unlock Cost Efficiency and Hyper-Automation

Digital workflows replace manual processes, cutting turnaround times. Hyper-automation combines AI and RPA to help banks scale without increasing headcount. This shift improves margins and enables competitive pricing.

5. Use Data and AI as Strategic Assets

Legacy stacks hide valuable data. Digital platforms create unified layers for real-time insights. This foundation enables AI-powered personalization, smarter risk modeling, and proactive customer interventions.

6. Strengthen Compliance, Security, and Digital Identity

Manual compliance cannot track intensifying regulations. Digital platforms embed security into workflows, ensuring consistent policy enforcement. Advanced authentication protects trust while maintaining low-friction user experiences.

7. Prepare for the Future of Embedded and Open Banking

Banking is moving toward integrated, third-party ecosystems. API-first architectures allow banks to provide regulated services anywhere. This ensures they capture new flows rather than facing disintermediation.

Enterprises are investing in digital banking platforms now because the stakes have shifted from “nice‑to‑have apps” to core survival and growth. Those that modernize can deliver the experiences customers expect, operate with fintech‑level agility, and plug into the emerging open‑finance economy.

What Is an Enterprise Digital Banking Platform?

An enterprise digital banking platform is a comprehensive orchestration layer that integrates legacy core systems with modern digital front-ends. It enables financial institutions to deliver scalable, API-driven services and personalized user experiences while maintaining rigorous security and compliance standards.

How Enterprises Use These Platforms in Practice

Enterprises use these platforms to unify fragmented services into a single, cohesive ecosystem. Instead of managing separate tools for lending, payments, and wealth management, leaders integrate them into one orchestration layer. This allows for seamless data flow across the entire organization.

Consequently, teams can launch new financial products in weeks rather than years. In practice, this means a bank can offer a personalized mortgage rate instantly by pulling real-time data from a customer’s existing accounts.

By shifting complex logic to the digital platform, the enterprise reduces the burden on its legacy core. This strategic move ensures the business remains agile and ready for market shifts.

- Retail Banking: Automating loan approvals to provide decisions in seconds rather than days.

- Corporate Banking: Providing real-time cash management tools for CFOs to monitor global liquidity.

- Embedded Finance: Allowing non-bank partners to offer branded credit cards or payment terms via APIs.

Digital Banking vs Online Banking: Key Differences

While online banking digitizes the interface, digital banking re-engineers the entire institution through a comprehensive, automated ecosystem.

Understanding this distinction is critical for leaders choosing between a surface-level update and a true structural transformation.

| Feature | Online Banking | Digital Banking |

| Operational Depth | Web-based wrapper for manual branch tasks. | End-to-end automation of the full banking lifecycle. |

| Architecture | Monolithic and tied to physical core limitations. | Microservices-based and cloud-agnostic. |

| Data Utilization | Historical data views with limited analysis. | Real-time big data ingestion and predictive AI. |

| Deployment Model | On-premise, requiring heavy maintenance. | SaaS or Private Cloud with elastic scalability. |

| Service Agility | Months to launch a basic new product. | Days to deploy features via modular components. |

| Security Framework | Perimeters based on logins and passwords. | Zero-trust architecture with biometric identity. |

| Customer Journey | Linear, static, and often reactive. | Contextual, hyper-personalized, and proactive. |

| API Connectivity | Limited or non-existent external links. | API-first design for Open Banking integration. |

The transition from online to digital banking moves your enterprise from maintaining a portal to owning a high-speed, programmable financial engine. Investing in a true digital platform ensures your infrastructure can pivot as fast as the market demands.

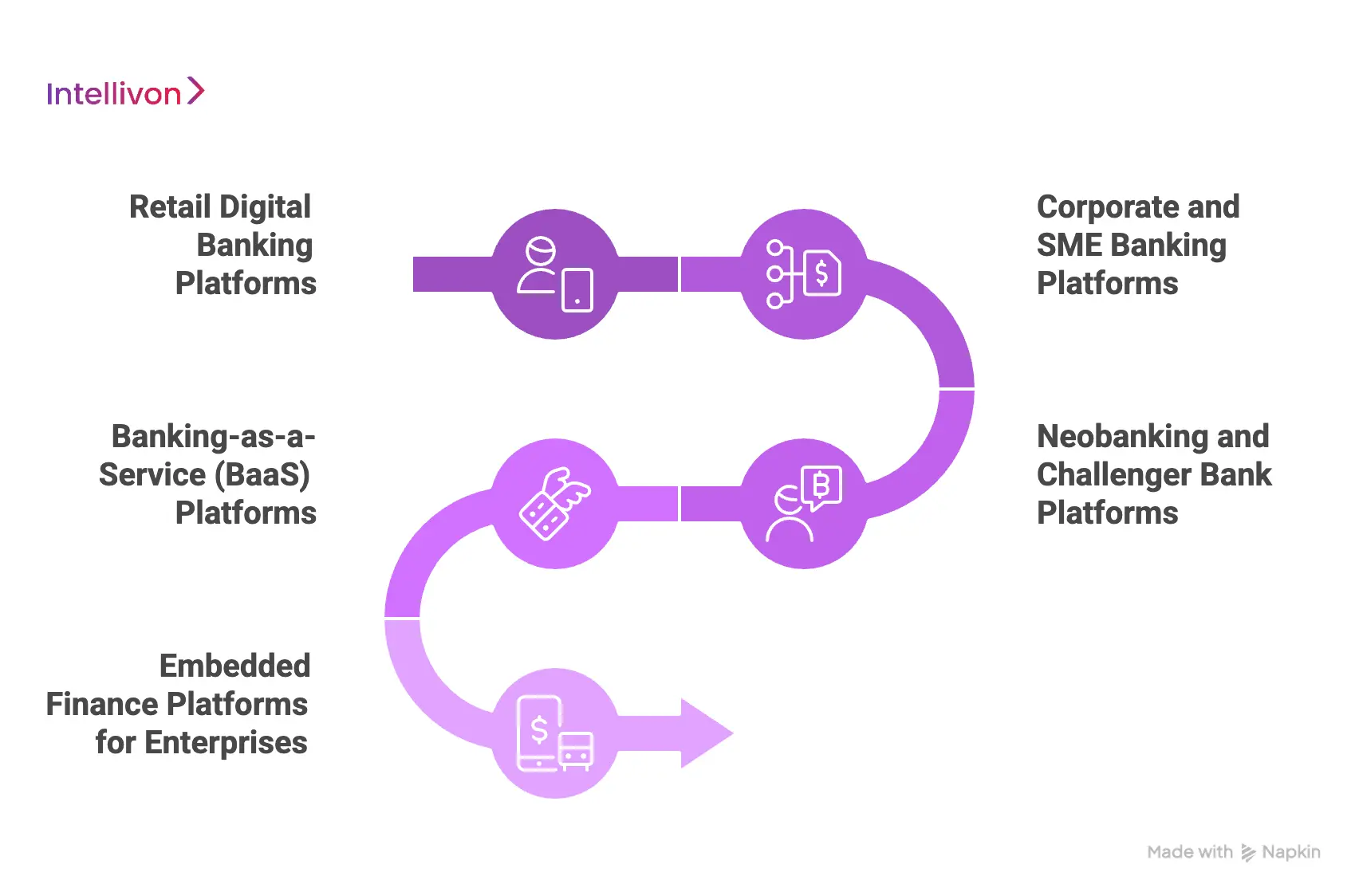

Types of Digital Banking Platforms in the Market

Selecting a platform depends on the target audience and specific business goals. These categories represent the different ways financial services are structured and delivered today.

1. Retail Digital Banking Platforms

Retail platforms prioritize high-volume, user-friendly experiences for individual consumers. They focus on making daily banking tasks as fast and simple as possible.

- Focus: High-speed transactions and mobile-first accessibility.

- Key Features: Automated KYC, instant account opening, and personal budget tracking.

- Example: A user opening a savings account in under three minutes via a smartphone app.

2. Corporate and SME Banking Platforms

Corporate platforms manage complex financial needs for businesses rather than individual users. They emphasize control, security, and integration with existing business software.

- Focus: Deep integration with accounting tools and bulk transaction handling.

- Key Features: Multi-user approval workflows, payroll automation, and real-time liquidity management.

- Example: A CFO managing international payments across multiple currency accounts from one dashboard.

3. Neobanking and Challenger Bank Platforms

These platforms are built from scratch on modern cloud technology without any legacy hardware. They offer extreme agility and lower costs compared to traditional institutions.

- Focus: Rapid deployment of niche features and superior user interfaces.

- Key Features: Modular architecture, real-time data processing, and highly automated back-office tasks.

- Example: A tech-first bank launching a new crypto-trading feature in just a few weeks.

4. Banking-as-a-Service (BaaS) Platforms

BaaS platforms allow licensed banks to rent out their infrastructure to other companies. This enables non-banks to offer financial products under the bank’s regulatory umbrella.

- Focus: Turning banking-regulated functions into a programmable service for partners.

- Key Features: Secure API middleware, automated compliance reporting, and ledger management.

- Example: A fintech startup using a bank’s license to offer branded debit cards to its users.

5. Embedded Finance Platforms for Enterprises

Embedded finance integrates banking directly into non-financial apps like retail or delivery platforms. This makes the financial transaction a seamless part of the buying process.

- Focus: Providing “invisible” banking at the exact point of a sale or service.

- Key Features: Flexible API integration, point-of-sale lending, and embedded insurance options.

- Example: A ride-sharing app allowing drivers to receive instant pay through an integrated digital wallet.

Understanding these categories ensures the chosen technology matches the intended market strategy. Matching the right platform type to your business model prevents costly integration hurdles later.

Core Features Every Enterprise Platform Must Have

Building a high-performance banking ecosystem requires a specific set of foundational tools to ensure stability and growth. These features form the technical bedrock that allows an enterprise to operate at scale while maintaining total control.

1. Multi-Account and Entity Management

Managing complex organizational structures requires more than simple database entries. Enterprise platforms must handle intricate account hierarchies that mirror real-world business departments and subsidiaries.

- Account Hierarchies: Create and manage thousands of sub-accounts under a single master entity for better capital allocation.

- Role-Based Financial Control: Assign specific permissions to different users, ensuring that only authorized personnel can approve large transactions.

- Visibility: Real-time monitoring of liquidity across all levels of the organization from a single glass pane.

2. Real-Time Payments and Settlement

Speed is the primary currency of the digital economy. Platforms must support instant payment rails to move funds without the traditional multi-day waiting periods.

- Instant Rails: Integration with global networks like SEPA Instant, FedNow, or UPI for immediate fund transfers.

- Cross-Border Payments: Automated currency conversion and routing to ensure international transfers are both fast and cost-effective.

- Settlement Orchestration: Intelligent logic that decides the best path for a payment based on cost, speed, and regulatory requirements.

3. Security and Fraud Detection Systems

As transaction volumes grow, manual monitoring becomes impossible. Modern platforms use sophisticated defense layers to protect assets and sensitive user data from evolving cyber threats.

- AI Fraud Detection: Machine learning algorithms that analyze behavior patterns to flag and block suspicious activity in milliseconds.

- Zero-Trust Layers: A security model where every request is verified, regardless of where it originates, minimizing internal and external risks.

- Encryption: End-to-end data protection that ensures information remains unreadable even if a breach occurs.

4. Compliance and Audit Readiness

Regulatory requirements are non-negotiable and constantly changing. The platform must automate the heavy lifting of compliance to prevent human error and legal penalties.

- KYC and AML: Automated identity verification and anti-money laundering checks integrated directly into the onboarding flow.

- Global Standards: Built-in frameworks to meet GDPR for data privacy and PCI-DSS for payment security.

- Audit Trails: Immutable logs of every action taken within the system, making regulatory reporting simple and transparent.

5. API-First and Open Banking

A closed system is a stagnant system. An API-first approach ensures the platform can communicate with the outside world, from fintech partners to accounting software.

- Third-Party Integrations: Easily connect with external tools like CRM systems, ERPs, or specialized insurance providers.

- BaaS Enablement: The ability to expose core banking functions as programmable services for other businesses to use.

- Scalability: Modular hooks that allow for adding new features without rebuilding the entire platform from scratch.

Modernization is now a requirement for staying relevant in a digital-first economy. Transitioning to an enterprise digital banking platform turns your financial infrastructure into a proactive growth driver rather than a reactive cost center

Capabilities That Define Digital Banking Platforms

True enterprise platforms are distinguished by their ability to handle massive scale and complex logic without sacrificing speed. These underlying capabilities ensure the system remains resilient, adaptable, and ready for future technological shifts.

1. Cloud-Native Microservices Architecture

Traditional banking software often functions as one giant, rigid block that is difficult to update. A microservices approach breaks the platform into smaller, independent pieces that communicate with each other seamlessly.

- Scalability: Automatically add more computing power during peak times, such as major shopping holidays or tax deadlines.

- Resilience: If one small service fails, the rest of the platform continues to run, preventing total system downtime.

- Rapid Updates: Deploy new features or security patches to specific areas without needing to take the entire bank offline.

2. Real-Time Data and Analytics Systems

Legacy systems often rely on “batch processing,” which means data is only updated once a day. Modern platforms process information as it happens, providing an instant view of the financial landscape.

- Instant Insights: Track liquidity, risk levels, and customer behavior in the exact moment a transaction occurs.

- Predictive Modeling: Use historical data to forecast future trends, helping to prevent cash flow issues before they arise.

- Hyper-Personalization: Deliver specific financial advice or product offers based on a user’s current spending habits.

3. Embedded Finance and White-Label Features

Enterprises can now extend their banking capabilities to other brands through white-labeling. This allows a non-bank partner to offer financial services that look and feel like their own.

- Brand Integration: Allow partners to use your regulated infrastructure while maintaining their own unique look and feel.

- Market Expansion: Reach new customer segments by embedding your payment or lending tools into popular retail apps.

- Revenue Sharing: Create new business models where you earn fees from the transactions processed by your white-label partners.

4. Cross-Channel Experience (Web, Mobile, API)

A platform must provide a consistent experience regardless of how a user chooses to interact with it. Whether through a smartphone, a desktop, or a direct software link, the data must remain synchronized.

- Unified Interface: Ensure that a transaction started on a mobile phone can be seamlessly finished on a laptop.

- API Access: Provide developers with the tools to build their own custom interfaces on top of your secure core.

- Omni-channel Sync: Real-time updates ensure that balances and transaction histories are identical across all touchpoints.

5. Multi-Currency and Cross-Border Support

In a global economy, being restricted to a single currency or region is a significant limitation. Digital platforms must handle the complexities of international finance automatically.

- Virtual IBANs: Issue local bank account numbers in multiple countries to simplify international collections.

- Real-Time FX: Access live exchange rates to ensure currency conversions are fair and transparent for the user.

- Global Compliance: Automatically adjust to the specific tax and reporting rules of different geographical regions.

These advanced capabilities move a platform beyond simple transactions and into the realm of strategic infrastructure. By mastering these areas, an enterprise ensures it can support any business model, anywhere in the world.

Advanced Capabilities for Enterprise Banking

High-scale financial operations require more than just a user interface; they demand a sophisticated engine capable of managing complex logic and massive data flows. These advanced modules provide the granular control necessary to run a global financial institution with precision.

1. Ledger and Accounting Engine

A robust financial platform must maintain an indisputable record of every movement of value. This engine serves as the single source of truth for the entire organization.

- Double-Entry Ledger: Every transaction is recorded in at least two accounts to ensure the books always balance and errors are easily spotted.

- Real-Time Reconciliation: The system automatically matches internal records with external bank statements, identifying discrepancies instantly rather than at the end of the month.

- Scalable Architecture: Capable of processing thousands of ledger entries per second without performance degradation.

2. Workflow and Approval Orchestration

In an enterprise environment, significant financial actions rarely happen in a vacuum. Logic-driven workflows ensure that every sensitive move follows established corporate policies.

- Multi-Level Approvals: Set up complex chains where a transaction requires sign-off from multiple departments or seniority levels.

- Rule-Based Controls: Automatically trigger or block actions based on specific criteria, such as transaction size, destination, or time of day.

- Custom Routing: Direct tasks to the right person based on their current workload or area of expertise.

3. Transaction Monitoring and Exceptions

Managing millions of flows requires a system that can spot the “needle in the haystack.” This capability ensures that errors or suspicious patterns are caught before they cause financial damage.

- Real-Time Tracking: Monitor the status of every payment from initiation to final settlement across global networks.

- Dispute and Reversal Handling: Built-in tools to manage chargebacks or payment errors systematically, keeping a clear audit trail of the resolution.

- Exception Management: Automatically flag transactions that fall outside of normal parameters for human review.

4. Treasury and Liquidity Management

Effective capital management depends on having a clear view of available funds at all times. This module helps organizations optimize their cash flow across different regions and currencies.

- Cash Positioning: Get a real-time snapshot of exactly how much liquidity is held in every account and currency globally.

- Liquidity Forecasting: Use historical data and scheduled payments to predict future cash needs, preventing shortfalls.

- Sweep Automation: Automatically move funds between accounts to maximize interest or ensure specific balances are maintained.

5. Card Issuing and Payment Controls

Modern platforms allow enterprises to become their own card issuers, providing tools for staff or customers to spend safely.

- Virtual/Physical Cards: Issue digital cards instantly for online use or physical cards for in-person transactions.

- Spend Controls: Set granular limits on where, when, and how much can be spent on a specific card, right down to the merchant category.

- Real-Time Freezing: Instantly disable a card via the API if it is lost or stolen, minimizing the window for fraud.

6. Identity and Access Management (IAM)

Security starts with knowing exactly who is accessing the system and what they are allowed to do. IAM provides a rigorous framework for protecting sensitive financial data.

- Role-Based Permissions: Grant access based on specific job functions, ensuring employees only see the data they need to perform their roles.

- Secure Authentication: Support for multi-factor authentication (MFA) and biometric logins to verify identities beyond just passwords.

- Session Monitoring: Track active users in real-time and automatically terminate sessions that show suspicious behavior.

7. Data Governance and Audit Systems

In a regulated environment, you must not only have the data but also prove where it came from and how it has been handled.

- Data Lineage: Maintain a visual map of how data moves through the system, from the moment it is collected to where it is stored.

- Compliance Reporting: Automatically generate the complex reports required by financial regulators, saving hundreds of hours of manual work.

- Immutable Logs: Ensure that audit records cannot be altered or deleted, providing a secure history for internal and external auditors.

8. Product and Rule Configuration Engine

Market agility depends on being able to launch and tweak financial products without writing new code. This engine allows business teams to manage product logic directly.

- Dynamic Product Creation: Build new loan types, savings accounts, or credit products using a simple “building block” interface.

- Pricing and Rule Logic: Easily adjust interest rates, fees, or eligibility criteria in response to market changes or competitor moves.

- A/B Testing: Test different product versions on small groups of users before a full-scale market rollout.

9. Monitoring and Observability Systems

You cannot manage what you cannot see. Observability tools provide a deep look into the technical health of the banking platform.

- Uptime Monitoring: Constant checks to ensure that all services are responsive and performing at peak efficiency.

- Incident Alerts: Automatically notify the engineering team the moment a service shows signs of slowdown or failure.

- Performance Analytics: Analyze system response times to identify bottlenecks before they impact the user experience.

10. Sandbox and Developer Environments

Building a successful ecosystem requires making it easy for partners and developers to integrate with your platform safely.

- API Testing: A secure “playground” where developers can test their code against a simulated version of the bank without touching real money.

- Partner Onboarding: Streamlined tools that allow new fintech partners to connect their apps and start testing in minutes.

- Documentation: Clear, up-to-date guides that help external teams understand how to use your platform’s capabilities effectively.

These advanced capabilities ensure that a digital banking platform is not just a tool, but a flexible, secure foundation for the entire business. Investing in these features today prepares an enterprise for the unpredictable demands of tomorrow’s financial landscape.

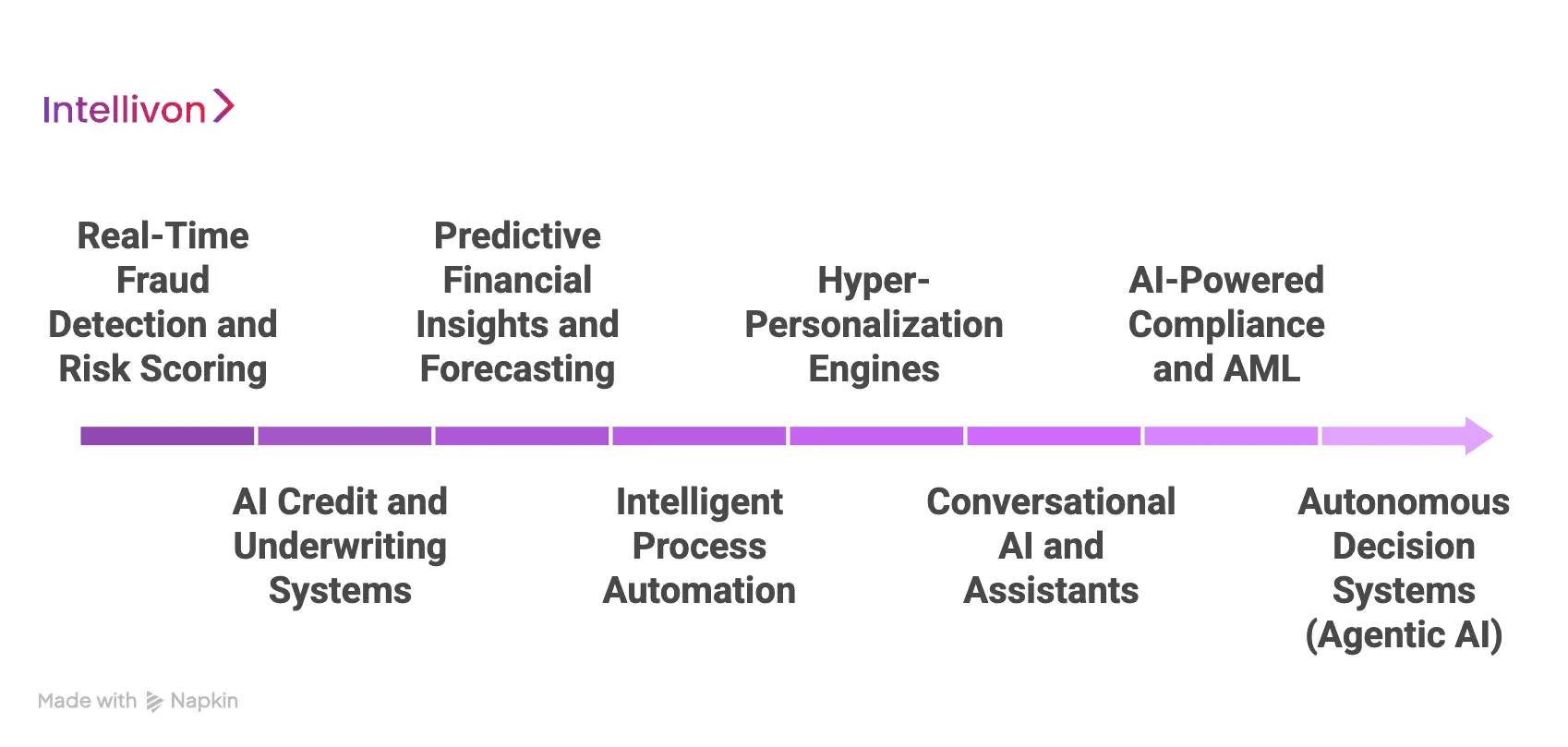

Advanced AI-Powered Banking Features

AI has moved from a speculative experiment to the core engine of modern financial infrastructure. These features allow a platform to move beyond simple automation into the realm of proactive, intelligent decision-making that evolves with every transaction.

1. Real-Time Fraud Detection and Risk Scoring

Legacy fraud systems rely on static rules that criminals eventually bypass. AI-driven detection analyzes billions of data points to identify subtle anomalies in milliseconds, stopping fraud before the money leaves the account.

- Behavioral Biometrics: Analyzes how a user interacts with their device to verify identity beyond passwords.

- Dynamic Risk Scoring: Assigns a risk level to every transaction based on location, frequency, and historical patterns.

- False Positive Reduction: Learns from past mistakes to ensure legitimate customers aren’t blocked unnecessarily.

2. AI Credit and Underwriting Systems

Traditional credit scoring often ignores a massive amount of relevant data, leading to missed opportunities. AI models ingest alternative data sources to provide a more accurate picture of a borrower’s true risk profile.

- Alternative Data Ingestion: Considers utility payments, rental history, and cash flow patterns to score the “unbanked.”

- Instant Decisioning: Automates the approval of loans and lines of credit without human intervention.

- Portfolio Monitoring: Continuously assesses the risk of existing loans to predict potential defaults before they occur.

3. Predictive Financial Insights and Forecasting

AI turns historical data into a roadmap for the future. By identifying patterns in spending and revenue, the platform acts as a proactive advisor for both the bank and the end user.

- Cash Flow Prediction: Alerts businesses to upcoming liquidity gaps several weeks in advance.

- Churn Analysis: Identifies customers who are likely to leave and suggests targeted interventions to keep them.

- Revenue Forecasting: Helps finance teams project future growth with higher accuracy using machine learning.

4. Intelligent Process Automation

While basic automation follows a set of steps, intelligent automation understands the context of a task. This allows the system to handle complex, unstructured data like legal documents or handwritten notes.

- Document Processing: Extracts data from invoices and contracts with near-perfect accuracy.

- Workflow Self-Correction: Identifies when a process has stalled and automatically reroutes it to resolve the bottleneck.

- Efficiency at Scale: Processes massive volumes of back-office work without needing to increase headcount.

5. Hyper-Personalization Engines

Generic offers are no longer effective in a competitive market. AI analyzes individual customer journeys to deliver the right message at the exact moment it is most likely to resonate.

- Micro-Segmentation: Groups customers by specific behaviors rather than just broad demographics.

- Next Best Action: Recommends the specific product or service that fits a user’s current life stage or business cycle.

- Contextual Notifications: Sends alerts that add real value, such as a reminder to save for a predicted upcoming bill.

6. Conversational AI and Assistants

Modern AI assistants go far beyond simple chatbots. They use natural language processing (NLP) to understand intent and can perform complex financial tasks on behalf of the user.

- Natural Dialogue: Handles complex, multi-turn conversations without getting lost or repeating questions.

- Task Execution: Allows users to move money, block cards, or open accounts entirely through voice or text.

- 24/7 Availability: Provides high-quality support at any time of day, reducing the burden on call centers.

7. AI-Powered Compliance and AML

The cost of compliance is rising, and human error is a significant risk. AI monitors every transaction against global watchlists and regulatory requirements in real-time.

- Pattern Recognition: Spots complex money-laundering schemes like “smurfing” that humans might miss.

- Automated SAR Filing: Drafts suspicious activity reports automatically, saving compliance officers hours of work.

- Regulatory Tracking: Scans for changes in global laws and suggests updates to internal policies.

8. Autonomous Decision Systems (Agentic AI)

Agentic AI represents the next frontier where the system executes them based on pre-set goals and constraints.

- Goal-Oriented Agents: Can be tasked with “optimizing corporate cash” and will move funds between accounts autonomously within set risk limits.

- Adaptive Logic: Changes its strategy in real-time based on new data or shifting market conditions.

- Self-Audit: Keeps a detailed log of why every autonomous decision was made for total transparency.

What to Evaluate in AI Banking Systems

Not all AI is created equal. When selecting an AI-driven platform, three specific areas determine whether the system will be a strategic asset or a liability.

- Explainability and Governance: You must be able to explain why an AI made a specific decision, especially in lending and compliance.

- Data Quality and Integration: AI is only as good as the data it consumes; the platform must have clean, unified data streams.

- Cost and Scalability: Ensure the AI models don’t become prohibitively expensive to run as your transaction volume increases.

These AI capabilities transform a digital banking platform from a passive storage system into an active, thinking partner. By integrating these tools, an enterprise ensures it remains at the cutting edge of efficiency and customer satisfaction.

Integration Capabilities Of Digital Banking Platforms

A digital banking platform is only as powerful as its ability to communicate with the broader financial world. These integration points act as the nervous system, connecting internal logic to external networks and business tools.

1. Core Banking System Integration

The most critical link for any digital layer is its connection to the legacy or modern core banking system (CBS). This integration ensures that the digital front-end reflects the actual state of the bank’s primary ledger.

- Bi-Directional Sync: Changes made in the digital app must update the core ledger instantly, and vice versa.

- Legacy Adapters: Specialized software layers that allow modern APIs to communicate with older, mainframe-based systems.

- Real-Time Visibility: Ensures that customer balances and transaction limits are always accurate across every channel.

2. Payment Networks and Card Schemes

To move money, the platform must be “plugged in” to the global financial infrastructure. This includes everything from domestic bank transfers to international credit card networks.

- Global Rails: Direct integration with networks like SWIFT for international wires or SEPA for European transfers.

- Card Processing: Connections to Visa, Mastercard, or local schemes for real-time card authorization and settlement.

- Digital Wallets: Built-in hooks for Apple Pay, Google Pay, and other modern mobile payment methods.

3. KYC, AML, and Fraud Detection Tools

Compliance is no longer a manual process. The platform must integrate with specialized third-party providers to verify identities and monitor for criminal activity.

- Automated Identity Verification: Real-time checks of passports, IDs, and facial biometrics during account opening.

- Watchlist Screening: Constant scanning against global sanctions lists and “Politically Exposed Person” (PEP) databases.

- Fraud Logic Sync: Feeding live transaction data into external AI fraud engines to catch suspicious patterns instantly.

4. ERP and Enterprise System Integration

For corporate banking, the platform must talk to the software businesses use to run their operations. This removes the need for manual data entry and reduces the risk of human error.

- Accounting Sync: Automatically pushing transaction data into tools like Xero, QuickBooks, or NetSuite.

- Treasury Management: Connecting directly with an enterprise’s internal treasury tools for automated cash positioning.

- Payroll Automation: Allowing businesses to execute massive payroll files directly from their ERP into the banking platform.

5. Third-Party Fintech Ecosystem Connectivity

Open banking has made it essential for platforms to connect with a wide variety of niche fintech services. This allows the bank to offer more value without building every feature from scratch.

- Wealth Management: Connecting to robo-advisors or investment platforms to show a user’s total net worth.

- Credit Scoring: Integrating with alternative credit data providers to offer better loan rates.

- Marketplace Apps: Allowing users to access third-party services directly inside the banking app.

Successful integration turns a standalone software product into a central hub for all financial activity. By mastering these connections, an enterprise ensures its platform is both useful today and adaptable for whatever new technology emerges tomorrow.

Real Examples of Digital Banking Platforms

Examining market leaders reveals how specific architectural choices translate into competitive advantages.

These examples demonstrate how different platforms prioritize specific features to capture distinct market segments.

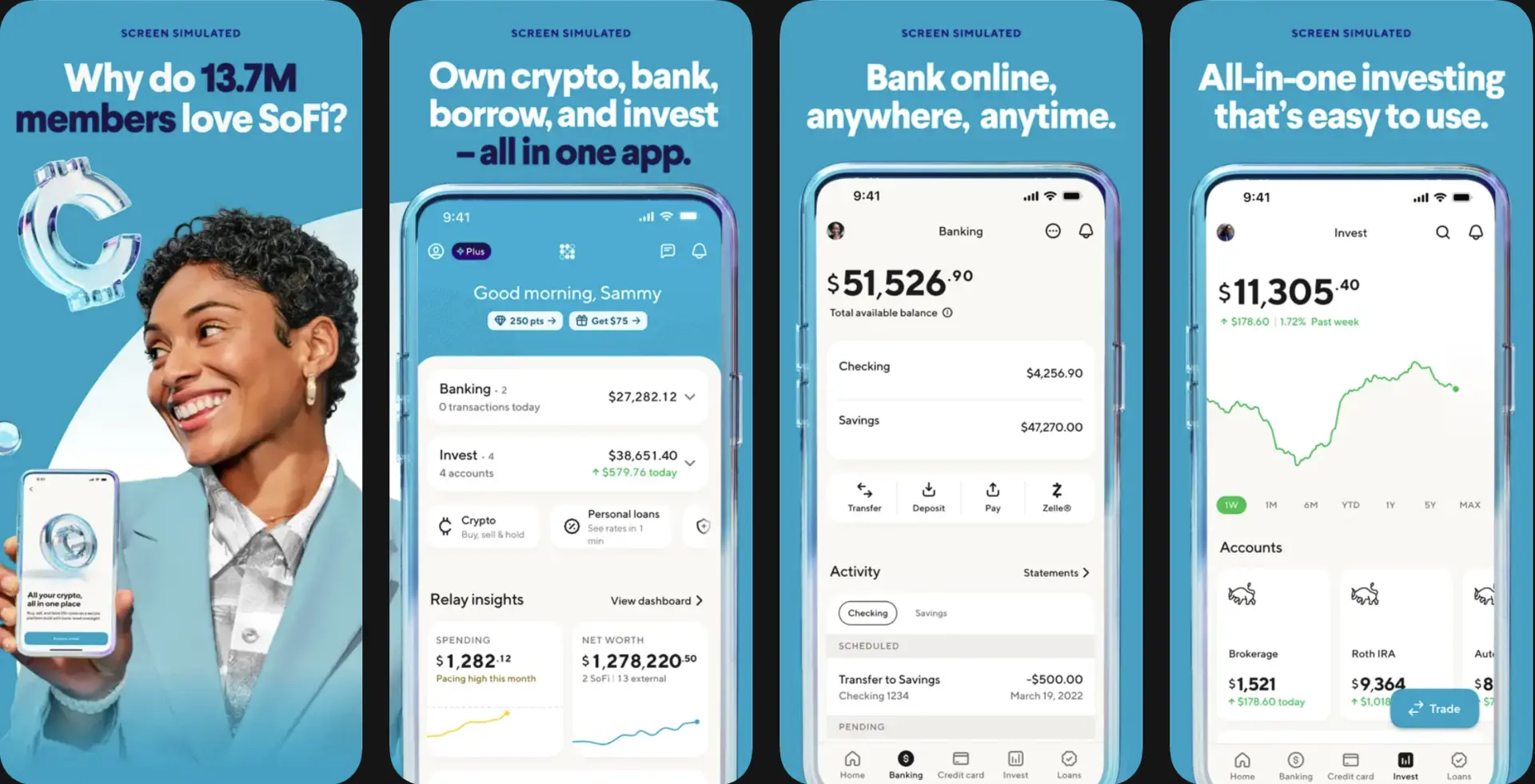

1. SoFi as a Platform Model

SoFi has evolved from a niche student lender into a comprehensive financial “super-app” by leveraging a robust internal platform. Their success stems from a unified data layer that allows them to cross-sell multiple products seamlessly.

- Unified Profile: A single customer identity links lending, investing, and checking accounts, creating a frictionless user journey.

- Vertical Integration: By acquiring Galileo, a payments processor, they gained control over their own infrastructure, reducing costs and increasing speed.

- Member Ecosystem: They use platform data to offer personalized financial advice and community benefits, driving high customer lifetime value.

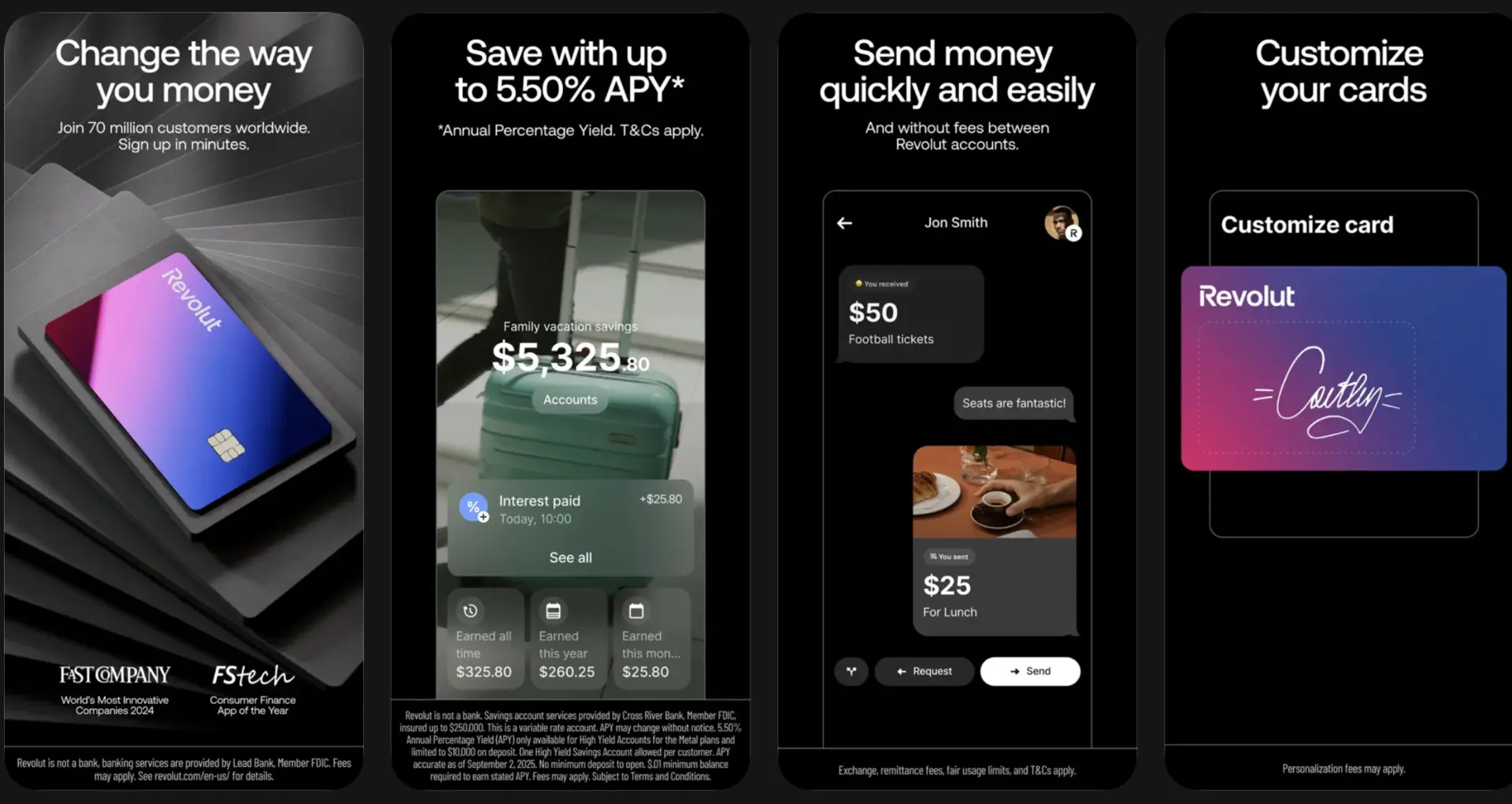

2. Revolut and Multi-Feature Banking

Revolut represents the “velocity” model of digital banking, constantly shipping new features to a global audience. Their platform is built for extreme modularity, allowing them to launch everything from crypto trading to travel insurance within a single interface.

- Global Multi-Currency: Their core engine handles real-time FX and local account details across dozens of countries.

- Aggressive Feature Deployment: A microservices-led architecture ensures that adding a new “hub” feature does not disrupt existing banking services.

- Granular Controls: Users have high-level programmatic control over their cards, including location-based security and disposable virtual cards.

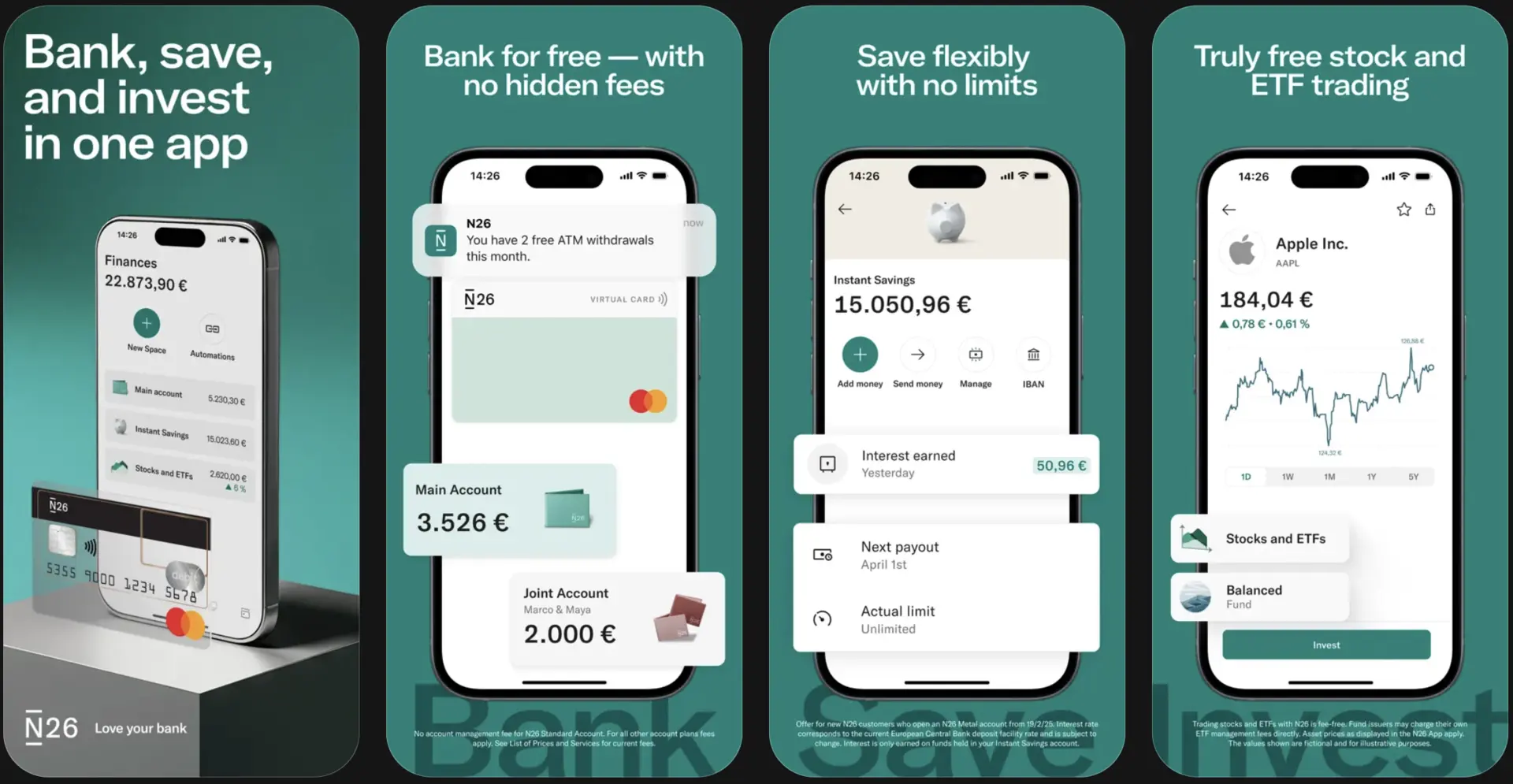

3. N26 and UX-First Approach

N26 focused on the “less is more” philosophy, proving that a superior user interface is a powerful defensive moat. Their platform prioritizes speed and clarity, removing the traditional friction points of legacy banking.

- Instant Interaction: Push notifications for every transaction and real-time balance updates are core platform requirements, not afterthoughts.

- Simplified Onboarding: They pioneered the use of integrated video and AI-assisted KYC to open fully functional accounts in under eight minutes.

- Spaces: A flexible ledger feature that allows users to create sub-accounts for specific goals with a simple drag-and-drop interface.

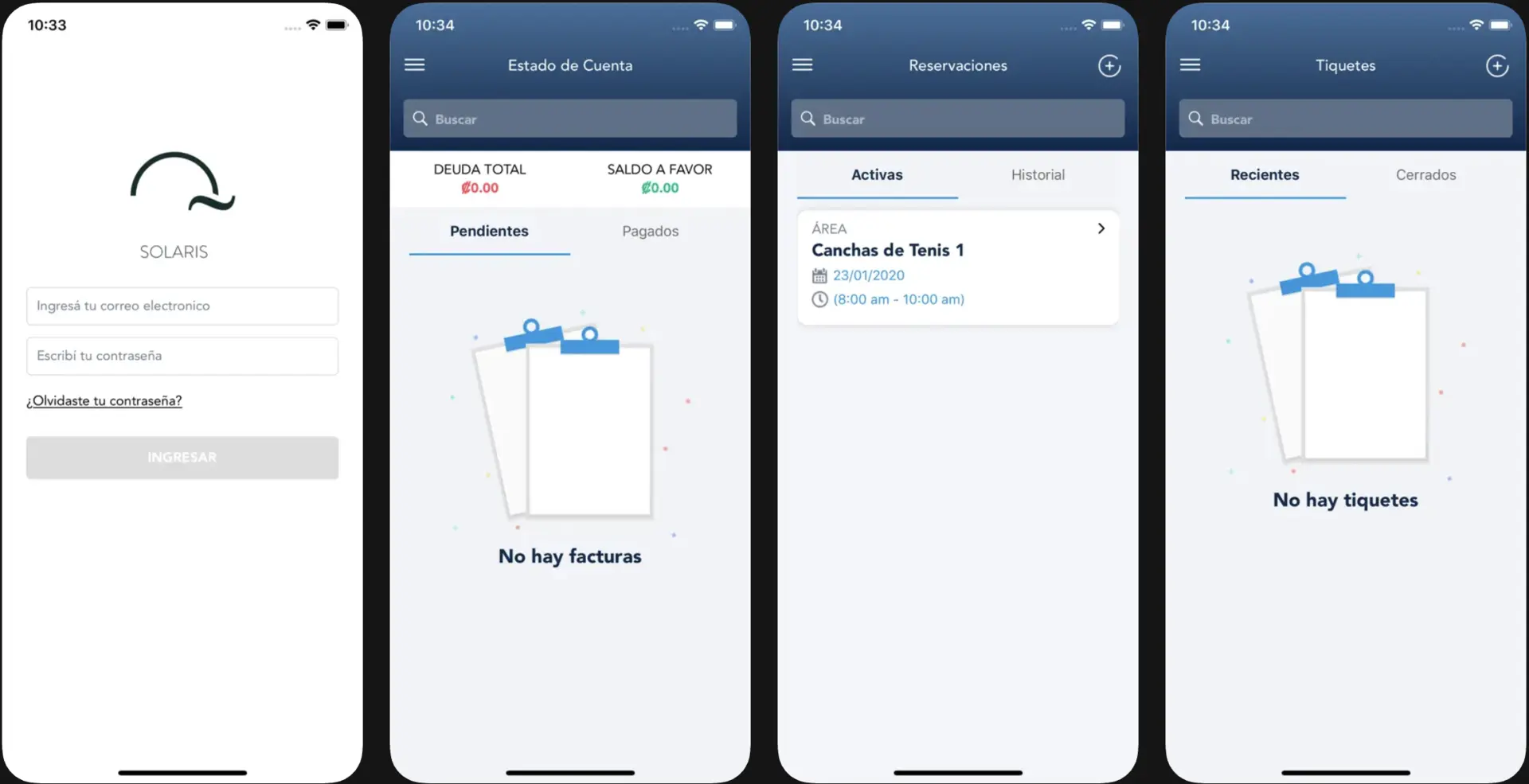

4. Solaris for Embedded Finance

Solaris operates entirely behind the scenes as a “tech company with a banking license.” Their platform is built specifically for other businesses to use, providing the regulatory and technical pipes for non-banks.

- BaaS Focus: They do not have a consumer-facing app; instead, their entire platform is a collection of well-documented APIs.

- Modular Compliance: Partners can pick and choose specific modules, such as digital identification or lending-as-a-service.

- Rapid Integration: Their platform is designed to let a corporate partner launch a fully compliant financial product in months instead of years.

These examples show that there is no “one-size-fits-all” digital banking platform. The most successful enterprises are those that choose an architecture aligned with their specific brand promise and target audience.

Conclusion

Investing in a digital banking platform is a strategic pivot toward long-term resilience and scalability. By moving beyond legacy constraints, enterprises can deliver the speed, security, and intelligence modern markets demand.

Intellivon provides the elite, AI-driven solutions needed to lead this transition. Contact us today to build your future-ready infrastructure.

Why Choose Intellivon For Building Digital Banking Platforms

Engineering an enterprise digital banking platform rests on designing a high-performance financial system that can handle real-time transactions, regulatory complexity, and global scale without failure.

At Intellivon, we build platform-grade banking infrastructure that connects data, payments, compliance, and user experience into a single, scalable system. Our approach focuses on turning architectural complexity into a long-term competitive advantage for your organization.

A. Bridging Legacy Banking Systems with Modern Platforms

Most enterprises evolve from legacy cores.

We specialize in building the integration layer that connects old and new systems seamlessly.

- Middleware that connects core banking, ERPs, and payment systems

- Gradual modernization without disrupting existing operations

- Real-time data synchronization across systems

This allows you to modernize without risking downtime or operational breaks.

B. Building Real-Time, Always-On Banking Infrastructure

Digital banking today operates in a 24/7, instant environment.

We design systems that support continuous transactions, settlements, and decision-making.

- Real-time payment orchestration across multiple rails

- High-availability systems with zero downtime architecture

- Event-driven systems for instant processing

This ensures your platform can scale with demand without performance bottlenecks.

C. Embedding Intelligence into Financial Workflows

Modern banking platforms must make decisions in real time.

We embed AI and automation directly into operational layers:

- Fraud detection models working at the transaction level

- Predictive insights for cash flow and liquidity

- Automated reconciliation and exception handling

This reduces manual effort while improving accuracy, speed, and financial control.

D. Architecture Built for Compliance and Global Scale

Compliance must be part of the system design.

We build platforms that are regulation-ready across regions:

- Built-in KYC, AML, and audit frameworks

- Configurable compliance rules for multiple jurisdictions

- Real-time reporting and audit trails

This ensures your platform remains operationally compliant as you expand globally.

E. Deep Integration Across the Financial Ecosystem

Enterprise banking platforms must connect with multiple systems and partners.

We design integration-ready architectures that connect:

- Payment networks (SWIFT, ACH, RTP, card rails)

- Fintech tools (KYC, fraud, analytics)

- Enterprise systems (ERP, treasury, accounting)

This creates a connected financial ecosystem, not a siloed platform.

F. Scalable Architecture That Grows With Your Business

We build systems that don’t need re-engineering every time you grow.

- Microservices-based architecture for modular scaling

- Cloud-native infrastructure for elasticity

- Observability and monitoring for system performance

This allows your platform to handle increasing transaction volumes without degradation.

System Milestones and Business Impact

| System Milestone | Intellivon’s Engineering Focus | Business Outcome |

| Launch Phase | Core platform with payments, accounts, and APIs | Faster go-to-market and early user adoption |

| Growth Phase | Integration, expansion, and system scaling | Seamless performance as volume increases |

| Mature Phase | AI-driven optimization and automation | Reduced costs and higher operational efficiency |

By partnering with Intellivon, you are creating a financial infrastructure layer that supports your long-term growth, innovation, and global expansion.

Ready to build a digital banking platform that actually scales with your business?

Talk to Intellivon’s experts today and start architecting a system designed for real-world enterprise demands.

FAQs

Q1. What defines a digital banking platform?

A1. A digital banking platform is a full-stack financial system that enables banks and enterprises to manage accounts, payments, lending, compliance, and customer experiences through a unified architecture.

Unlike standalone apps, it connects core banking systems, payment rails, data pipelines, and APIs into a single platform. This allows institutions to deliver real-time services, scale operations, and launch new financial products faster.

Q2. How is it different from online banking?

A2. Online banking is primarily a customer access layer that allows users to check balances, transfer money, and perform basic transactions through web or mobile interfaces.

A digital banking platform, however, is the underlying infrastructure that powers those experiences. It includes payments processing, compliance systems, integrations, and data layers, enabling banks to operate, innovate, and scale beyond just user interfaces.

Q3. What integrations are required?

A3. Enterprise digital banking platforms typically require integrations across multiple systems, including:

- Core banking systems for account and ledger management

- Payment networks such as SWIFT, ACH, RTP, and card schemes

- KYC, AML, and fraud detection tools

- ERP, treasury, and accounting systems

- Third-party fintech APIs for analytics, onboarding, and compliance

These integrations ensure the platform functions as a connected financial ecosystem, not a standalone system.

Q4. How long does development take?

A4. The development timeline depends on platform complexity, integrations, and compliance requirements.

- Basic platform (MVP): 3–6 months

- Mid-level enterprise platform: 6–12 months

- Fully integrated enterprise system: 12–18+ months

Timelines vary based on whether you build from scratch, use pre-built modules, or adopt a hybrid approach with a technology partner.

Q5. What is the cost to build one?

A5. The cost of building a digital banking platform varies based on features, integrations, and infrastructure requirements.

- Basic platform: $50,000 – $100,000

- Mid-level enterprise platform: $100,000 – $300,000

- Advanced enterprise system: $300,000+

Costs are primarily driven by real-time capabilities, compliance layers, integrations, and scalability requirements. For an accurate estimate, enterprises typically consult with experts to define scope and architecture before development begins.