Key Takeaways

-

Traditional batch-processing infrastructure costs financial institutions an average of $1.8M to $2.2M per hour during outages. An always-on architecture eliminates that exposure entirely

-

A 24/7 payment system requires more than speed. It demands active-active redundancy, event-driven architecture, and zero-downtime failover, working together as a unified system

-

Integrating modern stablecoin and real-time rails with legacy core banking is achievable without a full rip-and-replace. The right orchestration layer bridges both worlds

-

Enterprise-grade always-on platforms typically cost between $50,000 and $150,000+ to build, with 15–25% of that reinvested annually in maintenance and uptime engineering

-

Always-on infrastructure is a direct revenue engine. The premium settlement services, API monetization, embedded finance, and cross-border fee optimization all become viable at this layer

Payment infrastructure has become the most consequential technology decision a financial institution makes in 2026. The financial system moves trillions of dollars every single day, yet a significant portion of that movement still depends on infrastructure built around scheduled windows, manual reconciliation, and tolerance for delay.

However, that tolerance has expired. Now, enterprises want instant payroll disbursement. At the same time, insurers need real-time claims settlement, and traders expect sub-second confirmation. The gap between what institutions promise and what their infrastructure delivers is becoming visible to the people who matter most: customers, auditors, and competitors.

The harder, more consequential question is how to build a payment infrastructure that genuinely never goes down, engineered resilience that holds during peak load, regional outages, and unexpected transaction surges simultaneously. That requires rethinking architecture from the ground up: how data flows, how failover is handled, and how compliance is embedded rather than bolted on.

Intellivon has built deep in this infrastructure layer, designing enterprise-grade payment systems where continuous availability is an operational requirement, and not an aspiration. This blog covers the full build, which includes architecture decisions, technology stack, compliance requirements, real-world failure points, and the strategic choices that determine whether a payment system truly operates at always-on standards or simply claims to.

Why Banks Are Moving to 24/7 Payments Now

Customer expectations have fundamentally shifted. A 2024 Forrester report found that 65% of U.S. banking customers want to complete any financial task through a mobile app. For tens of millions of users, that app is now the primary banking channel. Therefore, any unplanned downtime or after-hours unavailability erodes trust, accelerates churn, and hands a competitive edge to institutions that stay online.

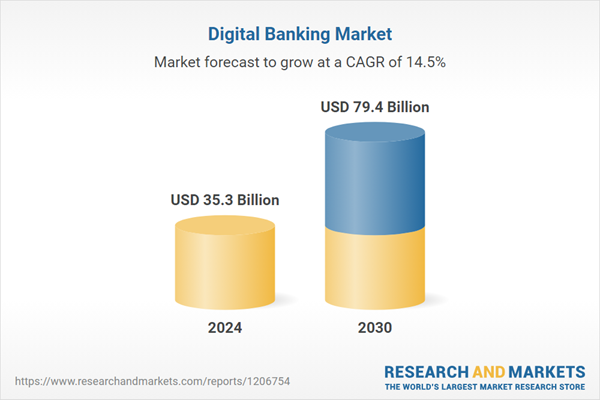

The market confirms the urgency. The global digital banking market is projected to grow from USD 35.3 billion in 2024 to USD 79.4 billion by 2030, at a 14.5% CAGR (Research and Markets). That trajectory rewards institutions whose systems are already built for scale, and puts pressure on those still operating within legacy constraints.

1. Market Demand Is Always-On

Banking behavior has shifted decisively toward digital-first and self-serve. Customers now expect to open accounts, move money, and resolve issues entirely on their own schedule, and not the bank’s. In addition, they no longer benchmark their experience against other banks.

They benchmark it against the best digital interaction they have had anywhere: a seamless checkout, an instant refund, a real-time notification. That bar keeps rising, and financial institutions are being measured against it whether they are ready or not.

2. Downtime Carries a Direct Financial Penalty

Given that baseline expectation, service interruptions carry immediate and quantifiable consequences. Financial services consistently record some of the highest outage costs across any industry.

According to New Relic, high-impact outages in financial services cost approximately $1.8 million per hour on average. A separate 2025 report placed the median higher, at $2.2 million per hour. Those figures go beyond technical disruption and reflect simultaneous hits to revenue, operational productivity, and customer confidence that take time to recover.

3. Availability Is a Retention Instrument

However, the cost of unavailability is not always measured in outage hours. A 24/7 platform functions as a retention strategy as much as a technical standard. Recent banking studies show customers are increasingly willing to move funds or switch providers after a single poor service experience.

Silent switching is growing more common, as customers quietly spread balances across institutions without formally leaving or filing a complaint. Therefore, service gaps on weekends, overnight, or during unexpected downtime directly erode wallet share over time, often without visible warning signals.

4. Competitive Pressure Has Become Structural

In addition to retention risk, there is a structural competitive shift that cannot be reversed. Digital-native competitors have permanently reset the baseline for speed, transparency, and availability. Seamless self-service and round-the-clock access are entry requirements.

As a result, 24/7 infrastructure has migrated out of the IT department’s remit and into the product experience itself. Institutions that treat it as a back-office concern are making a strategic miscalculation.

Building a 24/7 enterprise banking platform is therefore a strategic decision that directly determines how well an institution competes, retains customers, and weathers operational disruption, and not simply a technology upgrade.

What Always-On Payment Infrastructure Means

An always-on payment infrastructure represents a fundamental shift from batch processing to continuous, real-time value exchange. It is a resilient framework designed to eliminate maintenance windows and single points of failure.

For a financial institution, this means transactions are processed instantly, 24/7, regardless of volume spikes or regional outages. This architecture prioritizes high availability and fault tolerance, ensuring that the movement of capital remains as uninterrupted as the internet itself.

1. Real-Time vs Always-On Payment Systems

The distinction between real-time and always-on systems is subtle but critical for strategic planning. While real-time refers to the speed of the transaction, always-on refers to the absolute availability of the environment.

A system can be fast but still suffer from scheduled maintenance outages. Conversely, an always-on architecture ensures the “lights are always on,” even during core upgrades or database migrations.

Understanding this difference helps leaders prioritize investments in resilience alongside speed. Therefore, achieving true digital transformation requires moving beyond mere velocity toward a state of constant operational readiness.

| Feature | Real-Time Payments | Always-On Infrastructure |

| Primary Goal | Transaction speed and settlement. | System uptime and fault tolerance. |

| Core Metric | Milliseconds per transaction. | 99.999% availability (Five Nines). |

| Focus Area | Network rails and clearing. | Redundancy and cloud-native scaling. |

| Business Value | Improved liquidity and UX. | Market trust and risk mitigation. |

In conclusion, speed is a commodity, but availability is a competitive moat. Institutions must integrate both to meet modern consumer expectations. By merging these two concepts, you create a robust ecosystem that scales without friction. This dual approach transforms payment processing from a back-office function into a primary driver of enterprise growth.

2. Payment Orchestration vs Execution Layers

While they work together, orchestration and execution serve two different roles in a modern payment stack. Understanding their unique functions allows for a more resilient and flexible financial operation.

| Feature | Payment Orchestration | Execution Layers |

| Primary Role | Directs the flow and logic of the payment. | Performs the actual movement of money. |

| Intelligence | High: Uses rules to choose the best route. | Low: Follows specific technical instructions. |

| Flexibility | Connects to many banks and gateways. | Dedicated to one specific rail or network. |

| Business Value | Optimizes costs and success rates. | Ensures secure and final settlement. |

The orchestration layer acts as a smart manager that picks the best path for every transaction. In contrast, the execution layer is the specialized tool that finishes the job.

Therefore, a bank needs a strong manager to handle complexity and a reliable tool to guarantee results. Balancing both layers ensures that your system is both intelligent and indestructible.

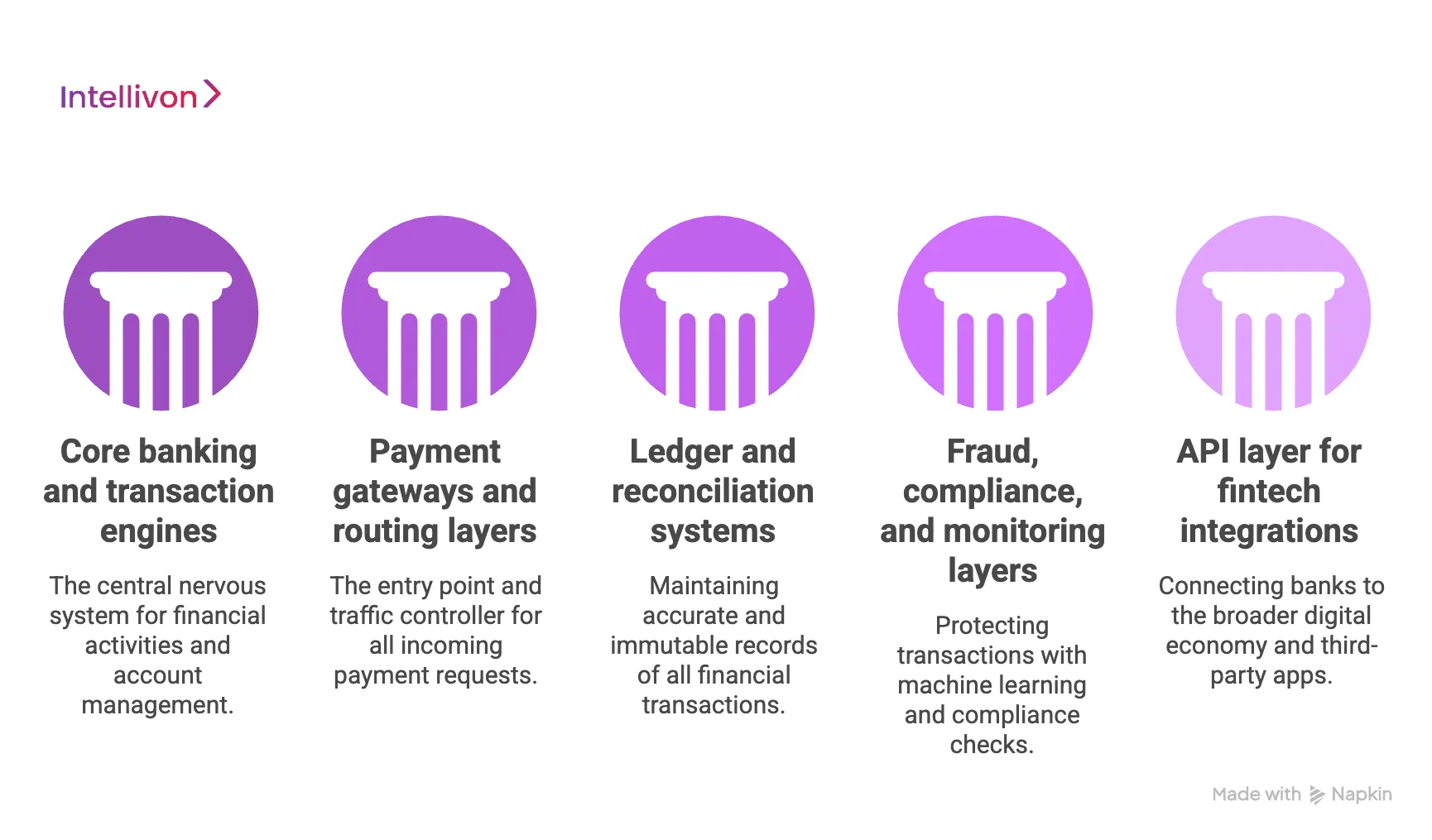

Key Systems Behind Always-On Payments

Building a resilient financial ecosystem requires a synchronized stack of specialized technologies working in perfect harmony. These components form the backbone of a system that never sleeps, ensuring security and speed at scale.

1. Core banking and transaction engines

The core banking engine serves as the central nervous system for all financial activities and account management. Unlike legacy systems that rely on end-of-day batch processing, modern engines use event-driven architectures to handle high-frequency data.

Therefore, they can process thousands of concurrent transactions without performance degradation or data inconsistency.

- Real-time Processing: Moves away from “bank hours” to offer immediate transaction finality.

- Horizontal Scalability: Allows the system to add more cloud resources during peak demand.

- High Availability: Utilizes multi-region deployments to prevent downtime during local server failures.

2. Payment gateways and routing layers

This layer acts as the entry point and traffic controller for every incoming payment request. It evaluates the best possible path for a transaction based on cost, speed, and current network health.

If one banking partner goes offline, the routing layer automatically shifts traffic to a secondary provider. This redundancy is what makes the payment infrastructure truly “always-on.”

- Smart Routing: Uses historical data to choose the provider with the highest success rate.

- Failover Protocols: Switches to backup connections instantly if a primary link fails.

- Unified Interface: Simplifies complex backend connections into a single, reliable point of entry.

3. Ledger and reconciliation systems

Maintaining an accurate record of every cent is the most critical task for any financial institution. Modern ledgers are immutable and distributed, meaning they provide a permanent and unchangeable audit trail.

Automating the reconciliation process in real-time eliminates the traditional “next-day” wait period for balancing books. This speed allows for better liquidity management and immediate error detection.

- Double-Entry Accuracy: Ensures every debit has a corresponding credit across all systems.

- Instant Reconciliation: Matches internal records with external bank statements as they happen.

- Audit Readiness: Provides a transparent history that is always ready for regulatory review.

4. Fraud, compliance, and monitoring layers

Security systems must work at the same speed as the payments they protect to be effective. These layers use machine learning to scan every transaction for suspicious patterns in milliseconds.

By integrating compliance checks directly into the flow, banks can stop illegal activity without slowing down legitimate users. Constant monitoring ensures that any system issues are identified before they impact the customer experience.

- Dynamic Risk Scoring: Evaluates the safety of a transaction based on user behavior and location.

- AML/KYC Integration: Automatically verifies identities against global watchlists in real-time.

- Proactive Alerting: Notifies engineers of potential system bottlenecks before they cause a crash.

5. API layer for fintech integrations

The API layer is the bridge that connects the bank to the broader digital economy and third-party apps. It allows for secure, standardized communication between different software platforms without exposing sensitive core data.

By offering well-documented APIs, an enterprise can easily partner with fintechs to launch new services quickly. This modularity ensures the system remains competitive in a rapidly evolving market.

- Developer Experience: Provides clear tools and sandboxes for external partners to build on.

- Secure Access: Uses modern tokens and encryption to protect every data exchange.

- Rate Limiting: Protects the core system from being overwhelmed by too many requests.

Strategic integration of these five pillars creates a platform that is both rigid in security and fluid in operation. Investing in this holistic architecture ensures your enterprise remains relevant in an era of instant expectations.

Architecture Blueprint for 24/7 Payments

Building a financial platform that never sleeps requires a move away from rigid, legacy frameworks toward fluid, distributed architectures. This blueprint focuses on decoupling dependencies to ensure that a failure in one component never halts the entire system.

1. Event-driven systems for real-time flows

Traditional request-response models often create bottlenecks when transaction volumes spike unexpectedly. Event-driven architecture solves this by using an asynchronous message bus to coordinate tasks across different services.

When a payment is initiated, it is published as an “event,” allowing downstream systems like fraud detection and ledger updates to react instantly. This decoupling ensures that the system remains responsive even if one sub-service is under heavy load.

- Message Brokers: Tools like Kafka or RabbitMQ manage the high-speed flow of data packets.

- Asynchronous Processing: Tasks happen in parallel rather than waiting in a linear queue.

- System Resilience: If a service goes offline, the message broker holds the data until the service recovers.

2. Active-active vs active-passive setups

For global payment systems, the choice of redundancy model dictates the true level of availability. An active-passive setup keeps a backup server idle until the primary one fails, which often results in a brief service gap.

In contrast, an active-active setup runs multiple data centers simultaneously, sharing the traffic load. This ensures that if one region goes dark, the other is already handling live traffic, resulting in a seamless transition for the user.

- Active-Active: Zero recovery time as all nodes are constantly processing data.

- Active-Passive: Lower cost but carries a risk of “warm-up” delays during a failover.

- Geographic Redundancy: Placing active nodes in different time zones to survive regional outages.

3. Designing zero-downtime failover systems

True zero-downtime is achieved when the system can detect a fault and reroute traffic before the user notices a delay. This involves implementing “circuit breakers” that automatically stop requests to a failing service to prevent a total system meltdown.

By using automated health checks and intelligent load balancing, the infrastructure can self-heal. These systems ensure that maintenance and upgrades happen in the background without interrupting the flow of capital.

- Circuit Breakers: Prevent a single slow service from dragging down the entire network.

- Blue-Green Deployment: Routes traffic to a new version of the software only after it passes health checks.

- Automated Health Checks: Constantly pings every service to ensure it is performing within set limits.

4. Data consistency across distributed systems

In a distributed payment environment, keeping balances accurate across different databases is a complex challenge. Banks must choose between “strong consistency,” where every node updates at the same time, and “eventual consistency,” which is faster but carries a short delay.

For payments, most architects use the Saga pattern or Two-Phase Commit protocols. These methods ensure that a transaction is either fully completed across all ledgers or completely rolled back, preventing “ghost” money.

- ACID Compliance: Guarantees that database transactions are processed reliably.

- Distributed Consensus: Algorithms like Raft or Paxos help servers agree on the current state of a ledger.

- Conflict Resolution: Intelligent logic that handles edge cases where two transactions hit the same account at once.

Transitioning to this architectural model is no longer optional for institutions looking to capture the modern market. By embracing decentralization, you replace fragile points of failure with a self-sustaining web of financial services.

Integrating With Existing Banking Systems

Modernizing a financial institution does not require a complete overhaul of the existing foundation. Instead, the goal is to build intelligent bridges that allow legacy systems to communicate with modern, high-speed networks.

This phased approach minimizes risk while unlocking new capabilities for digital-first customers.

1. Connecting to legacy core banking platforms

Most established banks rely on mainframe systems that were never built for the 24/7 internet age. To integrate these without a total “rip-and-replace,” architects use digital wrappers or “sidecar” databases.

These wrappers act as a translation layer, taking real-time requests and converting them into a format the old system understands. Therefore, the bank can offer modern mobile features while keeping its stable record-keeping core intact.

- Change Data Capture (CDC): Streams updates from the old database to a modern one in real-time.

- Shadow Core: Runs a parallel modern ledger for digital transactions to reduce the load on the mainframe.

- Data Virtualization: Provides a unified view of customer data without moving it from the legacy silos.

2. Integration with ACH, RTP, SWIFT rails

An always-on platform must be able to speak the “language” of various global payment networks. Whether it is the traditional batch processing of ACH or the instant settlement of RTP (Real-Time Payments), the system needs a unified gateway.

Modern infrastructure uses ISO 20022 messaging standards to ensure data remains rich and consistent across every rail. This allows for faster cross-border settlements through SWIFT without manual intervention.

- ISO 20022 Compliance: Standardizes financial data for global interoperability.

- Multi-Rail Support: Switches between payment networks based on the urgency of the transfer.

- Settlement Automation: Reduces human error by automating the clearing process across different time zones.

3. API-first approach for ecosystem expansion

Building an API-first architecture transforms a bank into a platform. By exposing secure endpoints, the institution can allow third-party fintechs to build specialized services on top of its regulated infrastructure.

This approach, often called “Banking as a Service” (BaaS), creates new revenue streams and reaches new demographics. It ensures that the bank remains at the center of the customer’s financial life, even if they use other apps for budgeting or investing.

- Sandbox Environments: Allows developers to test integrations safely before going live.

- Webhooks: Sends instant notifications to partner apps when a payment event occurs.

- Open Banking Compliance: Meets regulatory requirements while providing better data portability for users.

4. Middleware and orchestration layers

Middleware serves as the “glue” that binds disparate systems together, ensuring that data flows smoothly between the frontend and the legacy backend. An orchestration layer sits above this, managing the complex logic of a transaction’s journey.

For example, it might trigger a compliance check, a currency conversion, and a ledger update in a specific sequence. This layer ensures that even if one part of the process is slow, the user experience remains seamless.

- Enterprise Service Bus (ESB): Routes messages between different software applications within the bank.

- Workflow Automation: Defines the step-by-step rules for complex business processes.

- Protocol Translation: Converts modern JSON requests into legacy XML or COBOL formats.

5. Avoiding disruption during live integration

The biggest fear for an enterprise is a system crash during a major update. To prevent this, teams use “canary releases,” where a new feature is rolled out to a small group of users first. If no errors occur, the rollout expands to the rest of the database.

This incremental strategy ensures that the bank stays operational while it evolves. By maintaining strict version control on all APIs, the institution prevents breaking existing connections with corporate clients.

- Canary Deployments: Limits the blast radius of a potential bug during an update.

- Parallel Running: Keeps the old and new systems active simultaneously for a safety period.

- Rollback Strategy: Enables an instant return to the previous stable state if an issue is detected.

Successful integration is a balance between respecting the stability of the past and embracing the speed of the future. By focusing on modularity, an enterprise can evolve its infrastructure without ever turning the lights off.

Migration Strategy: Batch to Always-On Systems

Transitioning a legacy financial institution to a continuous processing model is a high-stakes operation that requires surgical precision. A successful migration balances the urgent need for modernization with the absolute necessity of maintaining service continuity and data integrity.

1. Phased vs big-bang migration approach

The choice between a phased rollout and a “big-bang” cutover is a decision that impacts every department from IT to customer support.

Therefore, the decision depends on the complexity of the existing architecture and the institution’s tolerance for risk.

| Feature | Phased Migration | Big-Bang Migration |

| Risk Profile | Low: Failures are isolated to small segments. | High: The entire operation is at risk if errors occur. |

| Complexity | High: Requires temporary bridges between old and new. | Low: No need for long-term hybrid maintenance. |

| Deployment Speed | Slower: Extended timeline for total adoption. | Faster: Immediate move to the new environment. |

| Testing Capability | High: Real-world testing in controlled waves. | Limited: Relies heavily on pre-launch simulation. |

2. Running parallel systems without risk

To ensure zero downtime, many enterprises choose to run the new always-on infrastructure alongside the legacy batch system. This “shadow mode” allows the modern engine to process transactions in the background without being the system of record.

Engineers can compare the outputs of both systems to verify accuracy. If the new system’s data matches the legacy output perfectly over a set period, the bank gains the confidence to flip the switch.

- Shadow Accounting: Both systems process the same data to check for discrepancies.

- Read-Only Integration: The new system reads from the old database without writing back.

- Traffic Mirroring: Copies of live traffic are sent to the new environment for stress testing.

3. Data sync during migration phases

Maintaining a “single source of truth” is the hardest part of a multi-stage migration. When data lives in two different systems, it must stay synchronized in real-time to prevent balance mismatches.

Using Change Data Capture (CDC) tools allows the legacy database to stream every update to the new distributed ledger instantly. This ensures that a customer checking their balance on a mobile app sees the same number as the backend core.

- Bi-Directional Sync: Updates in either system are reflected in the other to avoid lag.

- Conflict Resolution: Pre-defined rules handle cases where data changes simultaneously in both places.

- Data Integrity Audits: Continuous automated checks verify that both ledgers remain identical.

4. Risk mitigation during transition

The transition period is the most vulnerable time for any financial entity. To mitigate this, architects implement “feature toggles” that allow them to turn off a new module instantly if it behaves unexpectedly.

Comprehensive monitoring and observability tools provide real-time visibility into the health of the hybrid stack. Furthermore, having a clearly defined “point of no return” and a detailed rollback plan ensures that the team can revert to safety within seconds.

- Kill Switches: Instant deactivation of problematic features without a full code revert.

- Automated Rollbacks: System triggers a return to the previous state if error rates spike.

- Enhanced Observability: Real-time dashboards track performance across the hybrid environment.

5. Timeline for enterprise rollout

A typical enterprise-grade rollout follows a logical progression from discovery to full-scale adoption. Initial planning and proof-of-concept usually take three to six months.

This is followed by a “pilot phase” where internal employees or low-risk accounts are moved to the new rails.

The final global rollout can take another six to twelve months, depending on the number of regional regulatory requirements that must be met.

- Phase 1: Discovery: Analyzing dependencies and mapping legacy data structures.

- Phase 2: Pilot: Moving a small, controlled segment of live traffic to the new system.

- Phase 3: Scaling: Gradually increasing the volume until the legacy system is retired.

In conclusion, the migration to an always-on system is an evolutionary process rather than a singular event. By choosing a phased strategy and prioritizing data synchronization, you eliminate the fear of downtime.

Payment Rails Your Platform Infrastructure Must Support Globally

To build a truly global presence, your payment architecture must be polyglot. It should speak the language of local instant networks, traditional credit schemes, and emerging digital assets.

Providing this level of accessibility ensures that no matter where your customers or partners are located, capital moves without friction.

1. Real-time rails like RTP and FedNow

Domestic instant payment networks, such as RTP and the FedNow Service in the United States, are becoming the baseline for commercial expectations. These rails allow for the immediate movement of funds directly between bank accounts at any time of day.

Because these systems are credit-push only, they significantly reduce the risk of returns or fraud compared to older debit-based systems. Therefore, integrating these rails is essential for businesses that require immediate liquidity and instant confirmation of payment.

- Settlement Speed: Funds are available to the receiver in seconds, not days.

- Data Richness: Uses ISO 20022 standards to include detailed invoice information within the payment.

- Operational Efficiency: Eliminates the need for manual reconciliation of “pending” transactions.

2. Card networks like Visa and Mastercard

Despite the rise of account-to-account transfers, card networks remain the most widely used retail and corporate payment method globally. Your infrastructure must support secure tokenization and 3D Secure protocols to handle these transactions at scale.

By connecting directly to these networks, you can offer features like “push-to-card” for instant disbursements. This remains a critical pillar for any enterprise looking to maintain high authorization rates across diverse geographical regions.

- Global Reach: Accepted by millions of merchants in virtually every country.

- Consumer Protection: Built-in chargeback and dispute resolution mechanisms.

- Digital Wallets: Seamlessly integrates with Apple Pay, Google Pay, and Samsung Pay.

3. Cross-border rails like SWIFT

For large-scale international settlements, SWIFT remains the gold standard for secure financial messaging. While often criticized for being slower than local rails, the SWIFT gpi (Global Payments Innovation) initiative has significantly increased the speed and transparency of these transfers.

A modern infrastructure should automate the generation of these messages while providing real-time tracking of funds across correspondent banks. This ensures that treasury departments have a clear view of global cash positions.

- Ubiquity: Connects over 11,000 financial institutions worldwide.

- High Security: Utilizes a highly encrypted and private network for all transmissions.

- Tracking: Provides end-to-end visibility on where a payment is in the global chain.

4. Stablecoin and blockchain payments

The next frontier of “always-on” payments involves programmable money on distributed ledgers. Stablecoins, pegged to the US Dollar or Euro, allow for 24/7 global settlement without the volatility of traditional cryptocurrencies.

These assets move on public or private blockchains, bypassing the traditional correspondent banking system entirely. Therefore, an enterprise-grade platform should include a “fiat-to-crypto” rail to facilitate these high-speed, low-cost international transfers.

- Programmability: Uses smart contracts to automate escrow or conditional payments.

- 24/7 Availability: Blockchains do not have bank holidays or closing hours.

- Lower Fees: Significantly reduces the cost of intermediate banking fees for cross-border moves.

5. Multi-rail orchestration strategies

Supporting multiple rails lies in how you orchestrate them. A multi-rail strategy uses intelligent logic to route a payment based on the specific needs of the transaction.

For example, a high-value, non-urgent payment might go via ACH to save costs, while an urgent payroll disbursement is routed via RTP. This level of flexibility protects your business from network outages and allows you to optimize for both speed and expense.

- Least-Cost Routing: Automatically picks the cheapest available rail for every transaction.

- Network Redundancy: Shifts traffic to a backup rail if the primary network experiences downtime.

- Unified Reporting: Consolidates data from all different rails into a single, clean dashboard.

By supporting this diverse array of payment paths, your infrastructure becomes a universal adapter for the global economy. This versatility is the cornerstone of a future-proof financial strategy that can adapt to changing market demands.

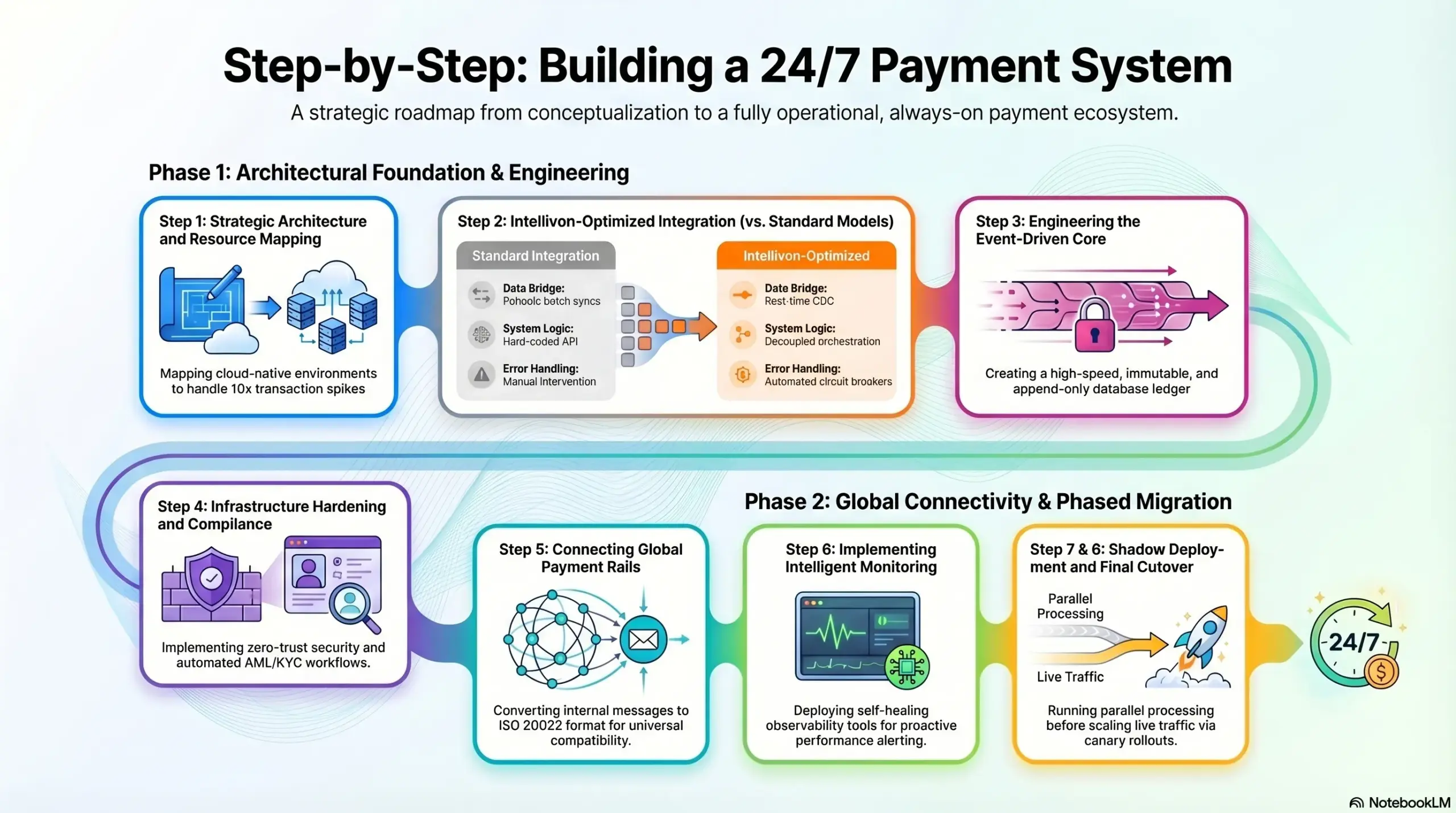

Step-by-Step: Building a 24/7 Payment System

Constructing a 24/7 payment system demands a strategic alignment of architecture, security, and global connectivity.

At Intellivon, we specialize in orchestrating these complex layers into a unified, high-performance platform. This detailed roadmap outlines the transition from conceptualization to a fully operational, always-on ecosystem.

Step 1: Strategic Architecture and Resource Mapping

The foundation begins with choosing between horizontal scalability and vertical depth. We analyze your existing data silos to determine how to decouple services without losing integrity.

This stage focuses on identifying the specific microservices, such as identity, ledger, and routing, that will form the core of your new infrastructure.

- Technology Audit: Assessing current technical debt to identify which legacy components can be “wrapped” versus replaced.

- Scalability Design: Mapping out cloud-native environments that can handle 10x spikes in transaction volume.

- Redundancy Planning: Designing the active-active geography to ensure that data centers in different regions back each other up.

Step 2: Selecting the Integration Model

Before a single line of code is written, you must decide how the new system will interact with the old one.

This decision dictates the speed of your rollout and the safety of your data. Therefore, choosing an optimized model is a prerequisite for zero-downtime operations.

| Component | Standard Integration | Intellivon-Optimized Integration |

| Data Bridge | Periodic batch syncs. | Real-time Change Data Capture (CDC). |

| System Logic | Hard-coded API connections. | Decoupled orchestration layer. |

| Vendor Access | Single gateway dependency. | Multi-rail, agnostic routing. |

| Error Handling | Manual intervention. | Automated circuit breakers. |

Step 3: Engineering the Event-Driven Core

With the strategy in place, the focus shifts to building the “brain” of the payment system. We implement an asynchronous message bus that allows different parts of the system to talk to each other without waiting for a response.

In addition, this decoupling ensures that if the compliance check takes an extra second, it won’t freeze the user’s mobile app interface.

- Immutable Ledger Development: Creating a high-speed, append-only database that ensures every transaction is permanent.

- Real-Time Fraud Logic: Integrating AI models that evaluate risk scores in the milliseconds between “swipe” and “settle.”

- API Gateway Security: Hardening the entry points with advanced encryption to protect sensitive financial data.

Step 4: Infrastructure Hardening and Compliance

Security must be baked into the architecture, not added as an afterthought. This step involves meeting stringent global standards like PCI-DSS and local data residency requirements.

We implement automated compliance workflows that scan every transaction for AML and KYC flags without adding latency to the user experience.

- Zero-Trust Security: Verifying every request, whether it comes from inside or outside the network.

- Data Masking: Ensuring sensitive PII (Personally Identifiable Information) is never stored in plain text.

- Automated Auditing: Generating real-time logs for regulatory bodies to ensure transparency at every step.

Step 5: Connecting Global Payment Rails

A system is only as good as the networks it can reach. In this phase, we build the bridges to domestic instant rails, international SWIFT messaging, and modern digital asset layers.

By using an API-first approach, we ensure that your platform can adopt new payment methods as soon as they go live.

- Rail Standardization: Converting all internal messages to ISO 20022 format for universal compatibility.

- Dynamic Routing Setup: Programming the logic that chooses the most cost-effective path for every individual payment.

- Liquidity Management: Automating the monitoring of treasury balances across different rails to ensure constant funding.

Step 6: Implementing Intelligent Monitoring

An always-on system requires a self-healing layer that can detect issues before they become outages. We deploy observability tools that track every millisecond of a transaction’s journey.

If a database begins to slow down, the system automatically triggers a circuit breaker to reroute traffic to a healthy node.

- Proactive Alerting: Notifying engineers of performance shifts before they impact the end user.

- Synthetic Testing: Running fake transactions through the system 24/7 to verify the health of every rail.

- Latency Tracking: Monitoring the speed of every third-party provider to ensure they meet their service level agreements.

Step 7: Shadow Deployment and Comparison

The move from the sandbox to the real world happens in a “shadow” environment. The new system processes live data but does not yet perform the final settlement.

This allows for a direct comparison of results against your legacy systems. Once the error rate hits zero over a sustained period, we gain the confidence needed for a live transition.

- Parallel Processing: Running both systems simultaneously to check for data parity.

- Data Consistency Checks: Verifying that balances match across both the old mainframe and the new ledger.

- Failover Simulation: Purposely shutting down nodes in the shadow environment to test the auto-recovery response.

Step 8: Phased Migration and Final Cutover

The final step is the gradual transition of live traffic. We begin with a small percentage of low-risk transactions, monitoring the system’s performance in real-time.

As trust grows, we scale the volume until the legacy system is no longer needed. This incremental strategy ensures that your business stays operational throughout the entire evolution.

- Canary Rollouts: Directing 1% of traffic to the new rails to monitor for any unforeseen edge cases.

- Traffic Scaling: Increasing the load in waves (e.g., 10%, 25%, 50%) as the system proves its stability.

- Decommissioning: Safely powering down the legacy batch systems once the new architecture is fully operational.

Building a 24/7 system is a high-reward investment that transforms your bank into a modern technology leader. By following this structured path, you eliminate the risks typically associated with large-scale financial migrations.

Cost to Build Always-On Payment Systems

Building an always-on payment infrastructure is not a fixed-cost initiative. The investment depends on how deeply the system integrates with core banking, payment rails, compliance layers, and real-time processing requirements.

Unlike traditional payment systems, always-on infrastructure requires continuous availability, fault tolerance, and multi-layer orchestration. As a result, costs are driven more by architecture, integrations, and uptime engineering than just feature development.

Key Cost Drivers in Enterprise Builds

Several factors directly influence the overall cost:

- Integration Complexity: Connecting with core banking systems, payment rails (ACH, RTP, SWIFT), and third-party services significantly impacts cost.

- Architecture Design: Event-driven, microservices-based systems with active-active setups require more engineering effort than monolithic builds.

- Real-Time Processing Requirements: Systems handling continuous transaction flows demand high-performance infrastructure and low-latency processing.

- Compliance & Security Layers: PCI-DSS, AML/KYC, fraud detection, and encryption layers add both development and operational overhead.

- Scalability & Uptime Engineering: Designing for 99.99%+ uptime requires redundancy, failover systems, and advanced monitoring.

Cost Breakdown by Modules and Complexity

| Component | Scope | Estimated Cost |

| Core Payment Engine | Transaction processing, routing, orchestration | $15,000 – $30,000 |

| Integration Layer | Core banking, APIs, payment rails integration | $10,000 – $25,000 |

| Ledger & Reconciliation | Real-time ledger, settlement, reporting | $8,000 – $20,000 |

| Fraud & Compliance Systems | AML/KYC, fraud detection, monitoring | $7,000 – $20,000 |

| API & Partner Access Layer | Developer APIs, fintech integrations | $5,000 – $15,000 |

| Monitoring & Observability | Logging, alerts, and uptime tracking | $3,000 – $10,000 |

Estimated Total Cost:

$50,000 – $150,000+ depending on system complexity and scale

Infrastructure and Cloud Cost Factors

Always-on systems require infrastructure that supports continuous uptime and real-time processing:

- Cloud hosting (AWS, Azure, GCP) with multi-region deployment

- Load balancing and auto-scaling for traffic spikes

- Database replication and distributed storage

- CDN and edge delivery for latency optimization

These costs are typically ongoing (monthly/annual) and scale with transaction volume and geographic reach.

Maintenance and Uptime Engineering Costs

Post-deployment, maintaining an always-on system requires continuous investment:

- 24/7 monitoring and incident response systems

- Performance tuning and infrastructure optimization

- Compliance updates and regulatory changes

- Security patching and threat monitoring

Most enterprises allocate 15–25% of the initial build cost annually for maintenance and uptime engineering.

Always-on payment infrastructure is not just a technology investment—it is a core financial system upgrade. The real cost lies in building a platform that can process transactions continuously, scale reliably, and integrate seamlessly across the banking ecosystem.

If you’re planning to build an always-on payment system, the right architecture decisions early on can significantly reduce long-term costs and risks.

Talk to Intellivon’s experts to get a tailored cost estimate and architecture roadmap based on your banking infrastructure and business goals.

How Banks Monetize Always-On Payments

Transitioning to a 24/7 infrastructure is a powerful engine for new revenue generation. By removing the constraints of traditional banking hours, institutions can offer high-velocity financial products that carry a premium price tag.

This shift allows a bank to move from a utility provider to a strategic value partner for its corporate and retail clients.

1. Premium real-time payment services

Corporations and high-net-worth individuals often prioritize certainty and speed over cost, especially for high-value transactions. Banks can monetize always-on systems by offering tiered service levels where instant settlement is a premium feature.

For example, a treasury department might pay a higher per-transaction fee to ensure a multi-million dollar supplier payment clears at 2:00 AM on a Saturday. Therefore, liquidity-as-a-service becomes a tangible product that directly improves the client’s cash flow management.

- Urgency-Based Pricing: Charging higher fees for instant settlement versus standard batch processing.

- SLA Guarantees: Offering contractually backed uptime and speed benchmarks for enterprise clients.

- Liquidity Buffering: Providing instant credit lines to cover real-time gaps in a client’s settlement account.

2. API monetization for fintech partners

An always-on API layer allows a bank to act as the regulated foundation for dozens of third-party fintech applications. By charging for API calls or taking a percentage of the volume flowing through these integrations, the bank creates a scalable, passive revenue stream.

This “Banking-as-a-Service” model allows the institution to profit from the innovation of others without needing to build every consumer-facing app itself.

- Subscription Tiers: Charging fintechs based on the volume of API requests or “calls” they make.

- Revenue Sharing: Taking a small commission on every transaction processed by a partner app.

- Premium Data Access: Offering enriched transaction data via API for a higher fee level.

3. Cross-border fee optimization models

International payments are traditionally slow and expensive due to the number of intermediary banks involved. An always-on system with direct rails or stablecoin support allows a bank to bypass these “toll booths.”

The bank can then capture more of the spread on currency exchange while still offering the customer a lower total cost than traditional SWIFT transfers. In addition, the ability to offer 24/7 FX rates provides a significant competitive advantage for global trading firms.

- Dynamic FX Spreads: Adjusting currency margins in real-time based on global market volatility.

- Direct Rail Savings: Keeping the “middleman” fees for the bank instead of passing them to correspondent partners.

- Instant Global Settlement: Charging for the unique ability to move money across borders in seconds rather than days.

4. Embedded finance revenue streams

Embedded finance places banking services directly into non-financial platforms, such as e-commerce checkouts or ride-sharing apps. Because these platforms operate around the clock, they require an always-on banking partner to handle instant driver payouts or point-of-sale financing.

By embedding its infrastructure into these high-traffic ecosystems, a bank can significantly increase its transaction volume and acquire new customers at a much lower cost.

- Transaction Volume Growth: Capturing a share of every purchase made on a partner’s platform.

- Lending Commissions: Earning interest or fees on “Buy Now, Pay Later” (BNPL) loans triggered at the point of sale.

- Integrated Insurance: Offering real-time micro-insurance products during the checkout process.

5. Data-driven financial products

The continuous flow of real-time transaction data is a goldmine for predictive analytics. Banks can use this data to offer highly personalized financial products, such as “just-in-time” loans or automated wealth management.

For instance, if the system detects a business client’s balance is likely to dip below zero based on upcoming scheduled payments, it can automatically offer a short-term credit facility. This proactive approach increases the “wallet share” and builds deeper institutional loyalty.

- Predictive Credit Scoring: Using real-time cash flow data to offer loans to clients who might fail traditional checks.

- Automated Wealth Management: Triggering investment moves based on instant changes in a client’s liquidity.

- Merchant Insights: Selling anonymized consumer spending trend reports to corporate retail clients.

Monetizing an always-on system requires a shift in mindset from charging for “storage” to charging for “movement and insight.” By leveraging these five revenue streams, an institution ensures that its technological evolution is matched by a robust and diversified bottom line

Conclusion

Building an always-on payment infrastructure is a strategic necessity in today’s instant economy. This shift ensures your institution remains competitive, resilient, and ready for future growth. By eliminating downtime, you protect your reputation and unlock new revenue streams.

Therefore, the transition from legacy batch processing to real-time systems is the most vital investment for modern finance. Embracing this evolution positions your enterprise as a leader in global capital movement.

Build Always-On Payment Platforms With Intellivon

Engineering a persistent, high-velocity financial ecosystem is a specialized discipline located at the intersection of high-frequency distributed systems and rigorous global regulation.

At Intellivon, we architect the high-trust digital rails that allow institutions to move capital with the same fluidity as information. Our approach turns the friction of traditional banking into a seamless, competitive advantage for your organization.

A. Converging Legacy Stability with Modern Velocity

We specialize in the critical “last mile” of digital banking: creating a harmonious bridge between rigid legacy mainframes and modern, continuous-settlement ledgers.

By deploying sophisticated orchestration layers, we ensure your new infrastructure communicates flawlessly with traditional clearing houses while leveraging the sub-second finality of a modern core.

This ensures your enterprise can modernize without risking the integrity of current operations.

B. Embedding Strategic Intelligence into the Payment Core

In an always-on environment, a platform must be proactive rather than reactive to maintain institutional margins. We integrate custom machine learning models directly into your routing engines to manage the variables that typically erode profitability in high-volume environments.

- Intelligent Liquidity Routing: Our AI monitors global network health and liquidity pools to execute transactions through the most stable and cost-effective channels.

- Predictive Anomaly Detection: We build proprietary safety nets that identify subtle pattern shifts in real-time, preventing fraud before it impacts the ledger.

- Automated Reconciliation Fabrics: We replace manual end-of-day matching with automated engines that sync transaction metadata with corporate records instantaneously.

C. Compliance-as-Code for Regulatory Resilience

The primary risk to global payment scaling is not technical failure, but a shifting regulatory landscape. Therefore, we treat compliance as a foundational engineering constraint.

From automated ISO 20022 message enrichment to jurisdictional logic adapters that update in real-time based on local mandates, we ensure your platform remains a “safe harbor” for capital across all borders.

D. High-Concurrency Engineering for Global Scale

Financial markets operate without pause, and your infrastructure must match that intensity. We utilize a high-concurrency tech stack optimized for low latency and high throughput.

This ensures your system handles massive disbursement cycles or sudden market spikes without a single millisecond of service degradation.

| Deployment Phase | Engineering Focus | Enterprise Value |

| Initial Integration | Digital wrapping of legacy cores. | Rapid modernization with zero system downtime. |

| Scaling Phase | Distribution of microservices. | Unlimited volume growth without performance loss. |

| Optimization Phase | AI-driven routing and settlement. | Maximized margins through autonomous cost reduction. |

By partnering with Intellivon, you are securing a technical moat that protects your treasury and scales your global influence. We don’t just provide software; we engineer the permanent foundations of modern commerce.

Are you ready to redefine your financial infrastructure?

Contact Intellivon today to begin architecting a 24/7 payment system that matches the scale of your global ambitions. Let’s turn your vision for an always-on enterprise into a production-ready reality.

FAQs

Q1. What is an always-on payment infrastructure?

A1. Always-on payment infrastructure enables banks to process transactions 24/7 without downtime. It uses real-time processing, resilient architecture, and failover systems to ensure continuous availability across payment rails, channels, and geographies.

Q2. How long does it take to build such a system?

A2. Most always-on payment systems take 4 to 9 months to build. Timelines depend on integration complexity, number of payment rails, compliance requirements, and whether you’re upgrading or replacing existing infrastructure.

Q3. What integrations are required for deployment?

A3. Banks must integrate with core banking systems, payment rails (ACH, RTP, SWIFT), card networks, KYC/AML tools, and fraud systems. API layers are also required for fintech and partner ecosystem connectivity.

Q4. How secure are always-on payment systems?

A4. These systems are built with PCI-DSS compliance, encryption, tokenization, and real-time fraud detection. Continuous monitoring and anomaly detection ensure security even during high transaction volumes.

Q5. How much does it cost to build always-on payments?

A5. The cost typically ranges from $50,000 to $150,000+, depending on system complexity, integrations, and scalability requirements. Infrastructure, compliance, and uptime engineering significantly impact the final investment.