Key Takeaways

-

Building a global banking platform costs between $50,000 and $200,000, depending on scope, but the architecture decisions made at day one determine whether that investment compounds or collapses under scale

-

Compliance, infrastructure, and third-party integrations are not secondary costs. They are the primary cost drivers, and underestimating them is where most enterprise builds go over budget

-

Hidden costs, API fees, legal retainers, fraud analysts, and scaling upgrades can add $57,000 to $145,000+ annually after launch, and most financial models don’t account for them upfront

-

The choice between extending legacy systems, using BaaS providers, or building proprietary infrastructure directly determines your time-to-market, recurring costs, and long-term competitive flexibility

-

A phased development approach, MVP first, enterprise features second, is the most capital-efficient path to global market entry without sacrificing system integrity

Building a global banking platform is one of the most important infrastructure choices a financial organization can make today. While the cost is a valid concern, it is rarely the best place to start. A more pressing question is whether your current system can meet the demands of the next three years.

Cross-border transactions, multi-currency accounts, embedded finance, and real-time compliance have become standard expectations in such platforms. At the same time, businesses operating across markets want financial infrastructure that can keep pace with their ambitions.

Traditional platforms were designed for a time when regulations were local, and technology updates took years. That time is gone. This is because a fintech company expanding into Europe or a company managing 40 currencies needs systems that can launch new markets in days, not quarters. Building at this scale involves managing technical architecture, regulatory requirements, security systems, and third-party integrations at the same time, with little room for costly mistakes.

Why Are Fintechs Focusing On Building Global Banking Platforms?

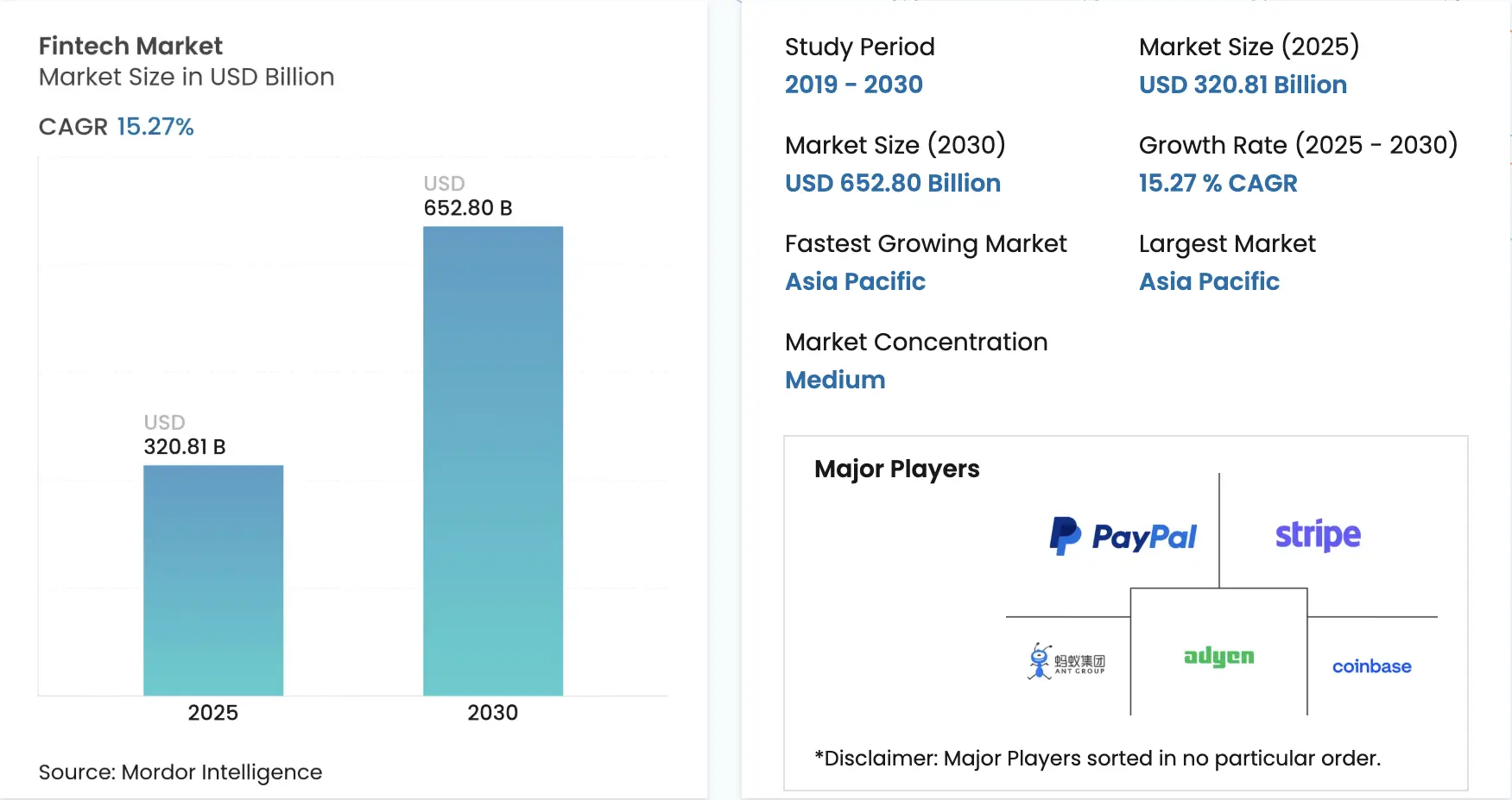

The global fintech market is expanding at a pace that makes platform scalability a strategic priority, not an afterthought. Estimated to reach USD 652.80 billion by 2030 at a 15.27% CAGR, the numbers reflect something more fundamental than market size. They reflect a structural shift in how financial services are built and delivered.

1. Faster Market Expansion

Fintechs want to enter new regions without rebuilding technology and operations from scratch each time. A global banking platform makes that possible because the core infrastructure carries over across markets.

Therefore, launch timelines shrink significantly. When competitors are moving fast, reusability is a competitive requirement.

2. Better Customer Reach

Fintech customers today are inherently cross-border. They work remotely, sell on global e-commerce platforms, freelance across time zones, and travel frequently.

These users need one account layer that works across currencies, countries, and payment rails without friction. Global platforms let fintechs serve that reality instead of working around it.

3. Lower Operating Complexity

Running separate systems for every country creates duplicate compliance workflows, fragmented support structures, and inconsistent product experiences. A unified platform centralizes identity, ledgering, payments, and risk controls in one place.

As a result, teams spend less time managing operational overhead and more time building product. That efficiency compounds as the business scales.

4. Stronger Revenue Potential

Global platforms unlock monetization paths that regional systems simply cannot support, including international transfers, multi-currency business accounts, card programs, and embedded finance services.

In addition, once a customer is onboarded, cross-regional upselling becomes far more executable. For fintechs, geographic expansion and revenue expansion move together rather than independently.

However, speed, reach, efficiency, and revenue scale are only achievable when the platform is architected correctly from the start. That is where the real cost conversation begins.

What Is A Global Banking Platform?

In the enterprise landscape, a global banking platform is far more than a simple mobile app. It represents a sophisticated ecosystem of interconnected financial services designed to operate across borders.

These platforms integrate core banking engines, multi-currency ledgers, and automated compliance layers into a unified architecture. For a business leader, this means having the infrastructure to manage cross-border liquidity and real-time settlements through a single technical interface.

Essentially, it is the digital spine that allows an organization to function as a financial institution on a global scale.

Cost Of Building a Banking Platform (At A Glance)

Investing in such a platform requires a clear understanding of the financial commitment involved.

While the scope of features impacts the final bill, most modern builds follow a predictable investment curve ranging between $50,000 and $200,000.

| Development Phase | Estimated Cost (USD) | Primary Focus |

| Foundational MVP | $50,000 – $85,000 | Core ledger, basic KYC, and essential API connectivity. |

| Mid-Market Scale | $85,000 – $145,000 | Multi-currency support, advanced security, and third-party integrations. |

| Global Enterprise System | $145,000 – $200,000 | Full regulatory automation, AI fraud detection, and high-concurrency architecture. |

Cost Range From MVP to Enterprise Systems

Starting with a Minimum Viable Product (MVP) allows an organization to test the market without committing maximum capital. At the entry level, the focus remains on the “Golden Path” of user experience.

This includes basic account creation, secure authentication, and a single-country regulatory hook. However, as the platform moves toward the enterprise tier, the cost increases to accommodate deep-tier infrastructure.

A full enterprise system demands high availability and disaster recovery protocols. These systems must handle thousands of transactions per second without latency. Consequently, the investment shifts toward microservices architecture and robust data encryption.

In addition, the integration of automated auditing tools ensures the platform remains compliant during rapid scaling. Therefore, the jump in cost reflects the transition from a functional tool to a resilient financial powerhouse.

| Feature Set | MVP Approach | Enterprise Approach |

| Architecture | Monolithic or simple Cloud | Distributed Microservices |

| Security | Basic SSL & MFA | Zero-Trust & Biometrics |

| Throughput | Limited concurrent users | Millions of transactions/hour |

| Scalability | Manual scaling | Auto-scaling AI orchestration |

Cost Differences by Region and Market

Geography plays a massive role in determining your total expenditure. For instance, launching in the European Union requires strict adherence to GDPR and PSD2 regulations.

These compliance frameworks necessitate specialized legal tech integrations that can drive up initial costs. In contrast, emerging markets may have lower entry barriers but require more localized payment gateway integrations.

Many countries now require financial data to stay within their borders, which adds to your server expenses.

| Factor | High-Regulation Markets (US/EU) | Emerging Markets (SEA/LATAM) |

| Compliance Cost | High (Strict licensing & audits) | Moderate (Easier entry) |

| Integration Complexity | High (Legacy bank connections) | Moderate (Mobile-first APIs) |

| Talent Acquisition | Premium pricing | Cost-optimized |

| Data Sovereignty | Extremely strict | Evolving/Flexible |

Why Costs Vary Across Banking Models

The specific business model you choose dictates the complexity of the underlying code. A Neobank focusing on retail customers requires a heavy emphasis on UI/UX and high-volume transaction processing.

Meanwhile, a B2B treasury platform must prioritize complex permissioning and bulk payment capabilities. These different requirements mean that developers must build entirely different logic sets for each model.

Furthermore, the choice between a “Banking-as-a-Service” (BaaS) approach and building a proprietary core affects the budget. Using a BaaS provider lowers the upfront build cost but leads to higher recurring operational fees.

| Model Type | Primary Cost Driver | Technical Focus |

| Retail Neobank | Customer Acquisition & UI | Mobile UX & Speed |

| B2B Treasury | Security & Permissions | Bulk processing & API |

| Crypto-Friendly | Blockchain Integration | Custody & Consensus |

| Wealth Management | Data Analytics | Predictive AI & Reporting |

Building a global banking platform is a strategic investment in future-ready infrastructure. By balancing regional needs with scalable architecture, enterprises can create high-impact financial solutions that drive long-term growth.

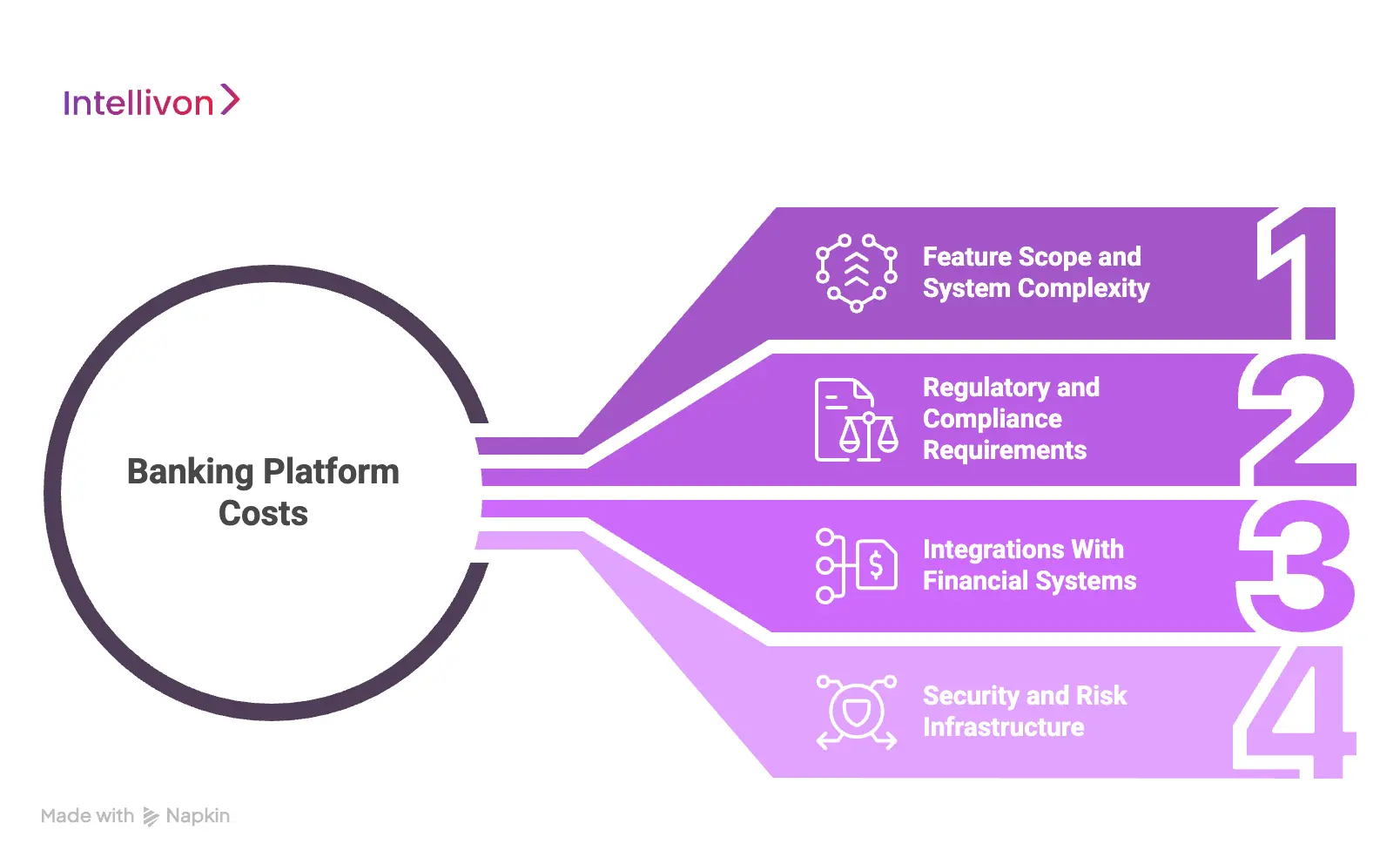

What Factors Affect Banking Platform Cost the Most?

Determining the final price tag of a financial ecosystem requires looking beyond the code. Several high-impact variables, from regional licensing to the depth of the tech stack, dictate whether a project stays within budget or scales in cost.

The following table highlights the core drivers that influence your capital allocation during the development lifecycle.

| Cost Driver | Influence Level | Primary Impact Area |

| Feature Scope | High | Development hours and UI/UX complexity. |

| Compliance | Critical | Legal tech, auditing, and regional licensing. |

| Integrations | Moderate | API middleware and third-party service fees. |

| Security | Essential | Encryption, fraud detection, and data safety. |

1. Feature Scope and System Complexity

Every added feature increases the logic required within the platform. A basic system might only handle peer-to-peer transfers, but an enterprise version often requires automated lending, currency exchange, and savings pots.

These layers require extensive testing to ensure data integrity remains intact across all modules. Therefore, a broader scope naturally extends the timeline and increases the engineering resources needed.

2. Regulatory and Compliance Requirements

Navigating the global financial landscape involves meeting strict legal standards. You must integrate Know Your Customer (KYC) and Anti-Money Laundering (AML) workflows into the onboarding process.

These systems are mandatory for maintaining a banking license. Consequently, the cost rises as you implement automated reporting tools that satisfy various regional regulators simultaneously.

3. Integrations With Financial Systems

A banking platform cannot exist in a vacuum. It must communicate with existing payment networks like SWIFT, SEPA, or local clearinghouses. Building these bridges involves complex API work and ensuring compatibility with legacy banking software.

In addition, you often pay for third-party services to handle card issuance or credit scoring. These external dependencies add both development time and ongoing operational costs.

4. Security and Risk Infrastructure

Protecting user capital is the most significant responsibility of any financial platform. This requires a multi-layered defense strategy, including end-to-end encryption and multi-factor authentication.

Advanced systems also utilize AI to monitor for suspicious patterns in real-time to prevent fraud. Investing heavily in this infrastructure at the start prevents the catastrophic financial and reputational costs associated with a data breach later.

Strategically managing these four pillars ensures your capital is spent on high-impact infrastructure rather than technical debt. Balancing these factors early in the development cycle is the most effective way to secure a strong return on your investment.

Why Is Banking Software Expensive to Build?

The high cost of financial software stems from the extreme precision required in every line of code. Unlike standard applications, banking systems have zero margin for error, as any glitch can lead to direct capital loss or legal penalties.

The following table breaks down the core investment areas that contribute to the premium pricing of these platforms.

| Cost Component | Description | Budget Priority |

| Licensing | Legal fees and regulatory permissions. | High (Non-negotiable) |

| Infrastructure | High-speed servers and redundant data paths. | High (Scalability) |

| Security | Defensive tech and automated risk monitoring. | Critical (Risk) |

| Ops Management | Ongoing audits and compliance staffing. | Moderate (Stability) |

1. Regulatory and Licensing Costs

Securing a digital banking license is often more expensive than the actual software development. Every jurisdiction requires a specific set of permissions to hold deposits or process payments. Furthermore, these licenses come with strict capital adequacy requirements, meaning you must prove you have liquid funds available.

- Legal Counsel: Expert fintech lawyers are necessary to navigate local and international finance laws.

- Compliance Tech: You must integrate third-party verification tools for “Know Your Business” (KYB) checks.

- Audit Readiness: Platforms need built-in reporting features to satisfy central bank inspections at any moment.

2. Real-Time Infrastructure Costs

Global banking requires an architecture that never sleeps and processes data in milliseconds. Building a system that maintains “Atomic Consistency”, ensuring a transaction is either 100% complete or 100% cancelled, is technically demanding. This level of reliability requires expensive, high-performance cloud environments and database management.

- High Availability: Using multiple server regions ensures the platform stays online during local outages.

- API Latency: Maintaining low-latency connections to global payment rails like SWIFT requires optimized code.

- Data Synchronization: Keeping balances accurate across different time zones and currencies in real-time is a complex engineering feat.

3. Security and Fraud Prevention Costs

Financial platforms are prime targets for cyberattacks, making top-tier security a mandatory expense rather than an optional feature.

Protecting sensitive data requires a layered approach that goes far beyond simple passwords. This involves continuous monitoring and the use of sophisticated AI to spot anomalies.

- End-to-End Encryption: Data must be scrambled at every point, from the user’s phone to the central database.

- AI Fraud Detection: Real-time algorithms analyze spending patterns to block suspicious activity instantly.

- Penetration Testing: Frequent “ethical hacking” sessions are required to find and fix vulnerabilities before criminals do.

4. Cost of Operating a Regulated System

The financial commitment does not end once the platform goes live. Operating a regulated system involves high recurring costs to ensure the business stays compliant with evolving laws. These costs are essential for maintaining the trust of both regulators and customers.

- Security Patches: Constant updates are needed to defend against newly discovered cyber threats.

- Compliance Officers: You need a dedicated team to monitor transactions and report suspicious activity.

- Data Residency: Storing financial data within specific national borders often requires renting local server space, which adds to the monthly bill.

While these expenses are significant, they represent the “trust tax” required to operate in the global financial market. Investing in these areas early protects your enterprise from future legal liabilities and system failures.

What Is the Cost Breakdown by System Components?

Building a global banking platform is a modular process where each component serves a distinct financial or regulatory function.

Understanding the specific cost allocation for these modules helps leaders prioritize their roadmap based on available capital.

The table below provides a realistic breakdown of the primary components required for a robust enterprise-grade system.

| System Component | Estimated Build Cost (USD) | Resource Intensity |

| Core Banking Ledger | $40,000 – $70,000 | Backend Engineering / Database Logic |

| Payment Rails | $30,000 – $50,000 | API Integration / Security Protocols |

| Compliance (KYC/AML) | $25,000 – $40,000 | Automation / 3rd Party Connectivity |

| Customer Interfaces | $35,000 – $60,000 | UI/UX Design / Frontend Development |

| Analytics & Reporting | $20,000 – $30,000 | Data Science / Business Intelligence |

1. Core Banking and Ledger Systems

The ledger is the absolute source of truth for every balance and transaction within the platform. Developing this requires specialized backend engineering to ensure double-entry bookkeeping remains flawless.

In addition, the core must handle interest calculations, fee structures, and account hierarchies. Because this component is the foundation of the entire system, it often commands the highest portion of the technical budget.

2. Payments and Transaction Processing

Moving money across borders involves connecting with various local and international payment rails. This module manages the logic for incoming and outgoing transfers, including currency conversion and settlement timing.

You must build secure “handshake” protocols with providers like SWIFT, FedNow, or regional UPI systems. Therefore, the cost reflects the complexity of maintaining high-speed connectivity while ensuring every transaction is fully traceable.

3. KYC, AML, and Compliance Systems

Regulatory tech ensures that your platform does not become a vehicle for financial crime. These systems automate the collection of identity documents and run them against global watchlists in real-time.

Implementing these features reduces the need for manual review teams, which saves operational costs in the long run. Consequently, investing in high-quality compliance automation is essential for maintaining the integrity of your banking license.

4. Customer Apps and Interfaces

The interface is how users interact with your financial ecosystem, requiring a focus on both security and simplicity. This includes developing native mobile applications and web dashboards that provide a seamless experience.

Developers must implement biometric logins, secure session management, and real-time push notifications for transaction alerts. A well-designed interface not only improves user retention but also reduces the burden on your customer support teams.

5. Analytics and Reporting Systems

Modern banking thrives on data-driven insights for both the institution and the end-user. This component aggregates transaction data to generate regulatory reports, tax statements, and internal business intelligence.

Advanced platforms also use this data to offer personalized financial advice or credit scoring through AI models. By investing in a dedicated analytics layer, you turn raw transaction logs into actionable strategic assets.

Allocating your budget across these five pillars ensures a balanced architecture that supports both user growth and regulatory stability. This modular approach allows for phased development, helping you manage cash flow while building toward a complete global solution.

How Much Does Infrastructure Cost Over Time?

Infrastructure is not a one-time purchase but a recurring operational commitment that evolves alongside your platform. For enterprise leaders, the goal is to transition from fixed capital expenditures to a flexible model that aligns costs with actual market demand.

The choice between hosting environments fundamentally changes your balance sheet, shifting the weight between upfront investment and monthly maintenance.

| Cost Variable | Cloud Infrastructure | On-Premise Servers |

| Upfront Capital | Minimal (Pay-as-you-go) | High (Hardware & Facility) |

| Scalability | Instant & Automated | Slow (Physical upgrades) |

| Maintenance | Included in Service Fee | Internal IT Staff Required |

| Data Control | Shared Responsibility | Absolute Ownership |

1. Cloud vs On-Premise Cost Differences

Cloud computing has become the global standard for banking due to its inherent flexibility and lower entry barriers. By utilizing providers like AWS or Azure, you avoid the massive costs of purchasing physical hardware.

However, as your transaction volume grows, monthly subscription fees can become a significant line item.

- Lower Barriers: Start development immediately without waiting for hardware delivery.

- Operational Shift: Move from large CapEx to predictable monthly OpEx.

- Shared Security: Benefit from the cloud provider’s billion-dollar investments in physical data center security.

2. Scaling Costs With User Growth

As your user base expands from thousands to millions, your infrastructure must adapt to handle increased database queries and API calls. Scaling costs often jump when you reach certain technical thresholds.

Planning for “elastic” infrastructure early prevents performance bottlenecks that could drive customers away during peak usage.

- Auto-Scaling: Automated systems add server capacity during peak hours and reduce it during lulls.

- Database Sharding: Dividing data across multiple servers to maintain speed as the volume increases.

- API Optimization: Reducing the cost per transaction through more efficient code and data caching.

3. High Availability and Failover Costs

In global finance, downtime is measured in lost revenue and eroded trust. Maintaining “five nines” (99.999%) availability requires redundant systems running in multiple geographic regions simultaneously. While this level of redundancy increases your hosting costs, it serves as a critical insurance policy against catastrophic system failures.

- Multi-Region Redundancy: Running identical setups in different countries to survive local outages.

- Instant Failover: Automated switches that redirect traffic to a healthy server in milliseconds.

- Disaster Recovery: Regular, encrypted backups stored in isolated environments to prevent total data loss.

4. Ongoing Maintenance and DevOps

A banking platform requires constant “pruning” to remain secure and efficient. This involves a dedicated DevOps team that manages continuous integration and deployment (CI/CD) pipelines.

They ensure that security patches are applied without disrupting service and that the system remains optimized for speed.

- Security Patching: Frequent updates to defend against newly discovered cyber threats.

- System Monitoring: 24/7 observation of health metrics to catch issues before they affect users.

- Technical Debt Management: Regularly refactoring code to ensure long-term stability and lower future costs.

Managing infrastructure is a balancing act between performance, reliability, and cost-efficiency. By prioritizing a cloud-native, scalable approach, enterprises can ensure their platform remains responsive to growth while maintaining a predictable expenditure profile.

Step-By-Step Development Of Global Banking Platforms Along With Costs

Building a financial ecosystem requires a disciplined, phase-gate approach to mitigate risk and ensure regulatory alignment. At Intellivon, we streamline this process by integrating advanced AI orchestration with robust banking logic, allowing enterprises to move from concept to market with precision.

The following breakdown illustrates our strategic seven-step roadmap and the associated investment for each critical milestone.

| Development Phase | Key Deliverable | Investment Range (USD) |

| 1. Strategic Discovery | Technical Blueprint & Roadmap | $5,000 – $8,000 |

| 2. Architecture Design | Scalable Microservices Schema | $8,000 – $12,000 |

| 3. Core Ledger Engineering | Immutable Source of Truth | $25,000 – $40,000 |

| 4. Compliance Integration | Automated KYC/AML Workflows | $15,000 – $25,000 |

| 5. Financial Connectivity | API & Payment Rail Bridges | $15,000 – $30,000 |

| 6. Security Hardening | Zero-Trust & Fraud Defense | $12,000 – $25,000 |

| 7. UI/UX & Market Launch | Native Apps & Production Go-Live | $20,000 – $40,000 |

Step 1: Strategic Discovery and Scoping

The foundation of a successful platform starts with identifying the specific market needs and legal hurdles. We map out the business objectives and technical requirements to ensure the project remains focused and within budget. This initial clarity prevents expensive pivots later in the development cycle.

- Stakeholder Alignment: Defining the core value proposition for your target audience.

- Feasibility Study: Assessing technical constraints and third-party dependency costs.

Step 2: Technical Architecture and Schema Design

We design the structural skeleton of the platform using a microservices approach. This ensures that different modules, like payments or lending, can scale independently without affecting the rest of the system. A well-designed architecture is essential for handling future user growth and technical complexity.

- Database Mapping: Designing for data integrity and high-speed retrieval.

- Orchestration Layer: Planning how different services will communicate securely.

Step 3: Core Ledger and Banking Logic Engineering

This step involves building the internal engine that tracks every cent moving through the system. We focus on creating an immutable ledger that ensures absolute accuracy in balance management and transaction history. This is the most critical technical component of the entire project.

- Transaction Atomicity: Ensuring payments either succeed fully or fail safely without data loss.

- Logic Engines: Coding the rules for interest, fees, and multi-currency conversions.

Step 4: Automated Compliance and Regulatory Integration

We bake regulatory requirements directly into the software to minimize manual oversight. By integrating automated KYC (Know Your Customer) and AML (Anti-Money Laundering) checks, we ensure your platform remains audit-ready and legally compliant in every jurisdiction.

- Sanction Screening: Real-time checking against global financial watchlists.

- Identity Verification: Document scanning and biometric matching for secure onboarding.

Step 5: Integration with Global Financial Ecosystems

No banking platform is an island. Instead, it must connect to the wider world of finance. We build secure bridges to payment networks like SWIFT, SEPA, or local clearinghouses. This allows your users to move money across borders with minimal friction and maximum speed.

- API Middleware: Creating stable connections with card issuers and banking partners.

- Webhooks: Setting up real-time notifications for transaction status updates.

Step 6: Security Hardening and Risk Infrastructure

Protecting capital is a non-negotiable priority. We implement a multi-layered security framework, including end-to-end encryption and AI-driven fraud detection. This step ensures that your platform is a fortress against both external attacks and internal vulnerabilities.

- Zero-Trust Models: Verifying every request, every time, regardless of the source.

- Anomaly Detection: Using AI to spot and block suspicious behavior instantly.

Step 7: UI/UX Development and Production Launch

The final step is crafting the user-facing interface and moving the system into a live environment. We focus on building intuitive mobile and web applications that make complex financial tasks feel simple. After rigorous stress testing, the platform is officially deployed to the market.

- Frontend Polish: Ensuring a seamless, high-performance experience across all devices.

- Post-Launch Monitoring: Providing 24/7 technical oversight to ensure stability during the initial rollout.

This detailed, seven-step methodology ensures that every dollar of your investment is directed toward building a secure, scalable, and market-ready asset. Partnering with Intellivon provides you with the strategic expertise needed to navigate this complexity with total confidence.

What Are the Hidden Costs in Banking Platforms?

Beyond the initial development and infrastructure, several “invisible” expenses can significantly impact the long-term profitability of a financial platform. These costs often remain hidden during the planning phase but surface as the platform matures and scales.

Understanding these ongoing commitments is vital for maintaining a healthy bottom line and avoiding sudden budget shortfalls.

| Hidden Cost Category | Nature of Expense | Estimated Annual/Volume Cost (USD) |

| API & Vendor Fees | Recurring / Volume-based | $12,000 – $25,000+ (per 10k users) |

| Legal & Compliance | Administrative / Retainer | $15,000 – $40,000 (annual) |

| Operational Support | Human Capital / Tools | $20,000 – $50,000 (annual) |

| Upgrades & Scaling | Technical Debt / Evolution | $10,000 – $30,000 (periodic) |

1. Third-Party API and Vendor Costs

Most global platforms rely on an ecosystem of specialized providers for essential services like SMS gateways and card networks. While using these vendors saves development time, they usually charge per transaction or per active user.

Over time, these small fees can aggregate into a massive monthly expense as your volume increases.

- KYC Providers: Expect to pay between $1.50 and $5.00 for every identity check performed during onboarding.

- Payment Gateways: Standard fees often range from 1% to 3% per transaction plus a fixed cent fee.

- Notification Services: Costs for sending mandatory security codes and transaction alerts can scale rapidly with user activity.

2. Compliance and Legal Overheads

Staying legal in the financial world is a continuous process rather than a one-time event. Laws change, and your platform must adapt to stay compliant with new anti-money laundering or data privacy rules.

This necessitates constant access to specialized legal counsel and regular independent audits.

- Annual Audits: Certified third-party audits can cost between $5,000 and $15,000, depending on depth.

- Regulatory Reporting: Costs associated with preparing and filing mandatory data with central banks often require dedicated software subscriptions.

- Legal Retainers: Keeping experts on hand to interpret shifting international finance laws is a necessary fixed expense.

3. Operational and Support Costs

Once a platform is live, you need a human infrastructure to manage the “exceptions” that software cannot handle. This includes everything from resolving transaction disputes to assisting users with account recovery.

Even with high levels of automation, a baseline of professional staff is required to maintain trust.

- Customer Success: Dedicated support for high-level technical or financial inquiries.

- Fraud Analysts: Experts who review transactions that the AI flags as suspicious to prevent false positives.

- Dispute Resolution: The manual work involved in investigating and reversing unauthorized charges or technical errors.

4. Upgrade and Scaling Costs

Technology ages rapidly in the fintech space, and staying relevant requires constant evolution.

You must periodically upgrade your core systems to support new features or to stay compatible with updated third-party APIs. Additionally, scaling into new countries often requires building specific “localizations” in the code.

- API Versioning: Rewriting code to match updates from your banking partners to avoid service breaks.

- Cloud Expansion: Increasing your server footprint to maintain speed in new geographic regions.

- Feature Evolution: Building new modules like “Crypto Wallets” or “Instant Lending” to remain competitive in a crowded market.

Accounting for these specific dollar figures allows for a more realistic ROI projection for investors. By identifying these costs early, enterprises can build a more resilient financial model that supports sustainable, long-term global growth.

How Do Integrations Impact Total Cost?

In the enterprise world, no platform operates in isolation. The “global” nature of a banking platform is defined by its ability to talk to other systems, central banks, payment networks, and identity databases. These connections, handled via APIs and middleware, often represent a significant portion of the total build cost.

The following table outlines the financial weight of these integrations and how they influence the overall project budget.

| Integration Type | Complexity Level | Estimated Cost (USD) |

| Core Banking (API) | High | $15,000 – $25,000 |

| Payment Networks | Moderate to High | $12,000 – $20,000 |

| Fraud & Risk Systems | Moderate | $8,000 – $15,000 |

| Data Synchronization | High | $10,000 – $18,000 |

1. Core Banking Integration Costs

Integrating with a core banking engine, whether it is a legacy system or a modern cloud-native provider, requires meticulous mapping of data fields. This process ensures that when a user initiates a transaction on your frontend, the ledger updates accurately in the backend.

- Middleware Development: Building a custom layer to translate your platform’s language to the core’s language.

- Database Alignment: Ensuring that account balances and transaction histories are perfectly mirrored without lag.

- Testing Cycles: Extensive “sandbox” testing to simulate thousands of scenarios before going live.

2. Payment Networks and Card Schemes

Connecting to global rails like SWIFT, Visa, or Mastercard requires adhering to strict communication protocols. Each network has its own set of rules for how data must be formatted and secured.

- Protocol Mapping: Configuring the system to handle ISO 20022 or other financial messaging standards.

- Certification Fees: Many card schemes charge for the right to integrate and test on their networks.

- Currency Logic: Building the engine that handles real-time exchange rates and cross-border settlement fees.

3. Fraud and Risk System Integration

To protect your capital, you must integrate third-party risk engines that analyze transactions in real-time. These systems provide a “score” for every action, helping you decide whether to approve or block a transfer instantly.

- Rule-Based Triggers: Setting up custom thresholds for suspicious activity based on your business model.

- Biometric Hooks: Integrating facial recognition or fingerprint data into the transaction flow for high-value transfers.

- Latency Management: Ensuring that the fraud check doesn’t slow down the user experience.

4. Data Sync Across Systems

A global platform often uses multiple specialized databases to handle different types of information. Keeping these systems in sync, so that a change in a user’s address in the KYC module is reflected in the reporting module, is a complex task.

- Event-Driven Architecture: Using tools to broadcast changes across the entire system in milliseconds.

- Consistency Checks: Automated scripts that run in the background to find and fix data discrepancies.

- Audit Trails: Maintaining a perfect chronological record of every data change for regulatory purposes.

Smart integration strategies prevent your platform from becoming a collection of disconnected silos. By investing in robust middleware and synchronized data paths, you create a seamless ecosystem that can scale across any financial network.

How Long Does It Take to Build a Platform?

Time-to-market is a critical metric for any enterprise looking to capture a competitive edge in the financial sector. While the desire to launch quickly is universal, banking infrastructure requires a realistic schedule to ensure that security protocols and regulatory requirements are fully met.

The following table compares development timelines based on the depth of the system and the speed of execution required for various market entries.

| Development Scope | Estimated Timeline | Strategic Purpose |

| Foundational MVP | 3 – 5 Months | Rapid market entry and investor validation. |

| Mid-Market System | 6 – 9 Months | Scaling features and regional expansion. |

| Enterprise Platform | 10 – 14+ Months | Full global orchestration and high-volume stability. |

1. MVP vs Full Platform Timelines

- MVP Focus: Speed, essential compliance, and primary payment rails.

- Full Platform Focus: Feature depth, international scalability, and ecosystem maturity.

2. Timeline Based on Complexity

- High Complexity: Multi-entity ledgers, cross-border settlements, and crypto-fiat gateways.

- Moderate Complexity: Domestic peer-to-peer transfers and basic interest-bearing accounts.

- Low Complexity: Digital wallets with limited third-party connectivity.

How Timeline Impacts Cost

In software development, time and budget are intrinsically linked. A longer timeline usually implies a higher cost due to the ongoing labor of specialized engineers, project managers, and compliance officers.

However, rushing a timeline can also lead to “technical debt”, shortcuts in code that require expensive fixes later.

- Labor Burn Rate: Monthly salaries for senior developers and architects accumulate as the project extends.

- Opportunity Cost: Delays in launching can result in lost market share or missed investment windows.

- Quality Assurance: Investing more time in the testing phase reduces the risk of post-launch failures, which are exponentially more expensive to fix.

Setting a realistic timeline is the first step toward a successful launch. By aligning your feature roadmap with a phased delivery schedule, you can manage your capital more effectively while ensuring your platform enters the market with a robust, high-performance foundation.

How Can You Reduce Banking Platform Costs?

High-level decision-makers often face the challenge of balancing innovation with fiscal responsibility. While the initial figures for a global platform can seem daunting, strategic planning can significantly optimize the budget. Reducing costs involves making smarter choices about how and when to deploy your capital.

The following table outlines actionable strategies to streamline your development budget without sacrificing system integrity.

| Optimization Strategy | Primary Benefit | Potential Savings |

| Phased Development | Managed Cash Flow | 20% – 30% (Initial Phase) |

| Pre-Built Infrastructure | Reduced Time-to-Market | $20,000 – $40,000 |

| Feature Prioritization | Focus on High-ROI Tasks | 15% – 25% |

| Minimal Engineering | Reduced Technical Debt | Long-term Stability |

1. Phased Development Strategy

Adopting a “crawl, walk, run” approach allows an enterprise to enter the market with a lean product while reserving capital for later improvements.

By launching an MVP first, you can gather real-world user data and generate revenue before funding advanced features. This strategy mitigates the risk of building complex modules that your market may not actually need or use.

- Capital Allocation: Direct funds toward essential core functions in the first six months.

- Feedback Loops: Use early user insights to refine the roadmap for the next development phase.

- Risk Mitigation: Limiting the initial scope reduces the financial impact if market conditions shift.

2. Using Pre-Built Infrastructure

Building every single component from scratch is rarely the most cost-effective path for a modern enterprise. Leveraging existing Banking-as-a-Service (BaaS) providers or white-label core engines can save thousands of development hours.

These pre-certified blocks handle the “heavy lifting” of ledger management and compliance, allowing your team to focus on the unique value proposition of your platform.

- Speed to Market: Reduce development time by 3 to 4 months by using verified API blocks.

- Lower Maintenance: The vendor handles the security patches and updates for the core engine.

- Proven Stability: Using a core used by other institutions reduces the likelihood of logic errors.

3. Prioritizing Core Features

It is easy for a project to suffer from “feature creep,” where non-essential ideas bloat the budget and delay the launch. To protect your investment, you must strictly categorize features into “must-haves” and “nice-to-haves.”

For a banking platform, this means prioritizing the transaction ledger, KYC, and security over aesthetic flourishes or secondary integrations.

- MVP Core: Focus solely on account creation, deposits, and basic transfers.

- Revenue-Driven Design: Prioritize features that directly contribute to transaction volume or user retention.

- Modular Expansion: Design the system so that new features can be “plugged in” as the budget allows.

4. Avoiding Over-Engineering

Engineers often want to build for every possible future scenario, which can lead to a system that is unnecessarily complex for its current needs.

Over-engineering drives up costs by requiring more senior talent and longer testing cycles. By focusing on “just enough” architecture, you keep the code clean and the budget predictable.

- Simplicity First: Use standard, well-documented technologies rather than experimental frameworks.

- Scalable Architecture: Build a system that can scale, without pre-paying for the scale you don’t have yet.

- Lower Debt: Simple code is easier to maintain, reducing the long-term cost of ownership for your IT department.

Strategic cost reduction is about focus, not compromise. By following these optimization paths, you ensure that every dollar invested contributes directly to a platform that is secure, compliant, and ready for global competition.

Conclusion

The financial commitment required to build a global banking platform is significant, but it represents a strategic pivot toward digital sovereignty. By understanding the architectural, regulatory, and operational variables involved, enterprise leaders can navigate these complexities with precision.

Ultimately, a well-funded, phased approach ensures that your infrastructure remains secure, compliant, and scalable. Investing in a robust foundation today creates a powerful vehicle for sustainable global growth and long-term market leadership.

Why Enterprises Choose Intellivon To Build Global Banking Platforms

Building a global banking platform is not merely a development task; it is the creation of a high-trust digital economy that must remain resilient under immense regulatory and transactional pressure.

While many firms can write code, Intellivon specializes in engineering the sophisticated AI-driven infrastructure required to turn complex financial visions into market-leading realities.

A. Deep Fintech & AI Orchestration Expertise

Apart from building enterprise-grade fintech apps, we design intelligent financial ecosystems that operate with surgical precision. Our deep understanding of the global fintech stack ensures your platform is both technologically superior and future-proof.

- AI-Driven Core Logic: We implement autonomous layers for real-time fraud detection and predictive liquidity management.

- Immutable Ledger Systems: Our architectures prioritize data integrity, ensuring every transaction is traceable and error-free.

- Intelligent Automation: We utilize AI to streamline complex back-office workflows, reducing operational overhead from day one.

B. Mastery of Global Regulatory Frameworks

The biggest barrier to entry in global banking is compliance. We treat regulatory alignment as a core feature of the build, not an afterthought, ensuring your platform is ready for international scrutiny.

- Automated Compliance Engines: Integrated KYC, AML, and KYB workflows that adapt to shifting regional laws.

- Audit-Ready Architecture: Every system we build includes automated reporting hooks designed for central bank transparency.

- Data Sovereignty Management: We design infrastructure that respects local data residency laws while maintaining global connectivity.

C. Strategic Execution with Accelerated Timelines

In the financial sector, a delayed launch is a lost opportunity. Intellivon utilizes a disciplined, sprint-based methodology to move you from architectural blueprint to live production without compromising on security.

- Phased MVP Delivery: We help you identify and launch the “Golden Path” features first to capture early market share.

- Zero-Debt Engineering: Our developers write clean, modular code that prevents expensive refactoring as you scale.

- Seamless Third-Party Connectivity: We provide pre-verified integrations for global payment rails like SWIFT, SEPA, and local clearinghouses.

D. Architected for Infinite Scalability

Most banking platforms face performance bottlenecks when user concurrency spikes. We anticipate this growth during the design phase, building a system that remains stable regardless of the load.

- Cloud-Native Microservices: Our architecture allows individual modules to scale independently based on real-time demand.

- High-Availability Networks: We implement multi-region failovers to ensure your services are available 24/7/365.

- Elastic Infrastructure: We leverage AI to optimize server resources, ensuring you only pay for the capacity you actually use.

Ready to architect your global financial future? Contact Intellivon today to discuss how our AI-driven approach can bring your global banking platform to life with precision, security, and speed.

FAQs

Q1. How much does it cost to build a global banking platform?

A1. Most enterprise-grade builds range from $50,000 to $200,000, depending on scope, geography, and regulatory complexity. Hidden costs, API fees, compliance overhead, and post-launch scaling routinely add another $57,000 to $145,000 annually.

Q2. What factors drive up the cost of a global banking platform the most?

A2. Compliance and licensing are the largest cost drivers, followed by security infrastructure, third-party integrations, and feature complexity. Underestimating these four areas is where most platform budgets break down before launch.

Q3. Should we build the platform from scratch or use a BaaS provider?

A3. BaaS lowers upfront cost but limits long-term differentiation and compounds operational fees at scale. Building proprietary infrastructure gives you full control. Most enterprises find the right balance through a hybrid model combining both approaches.

Q4. How do infrastructure costs change as the platform scales globally?

A4. Cloud infrastructure shifts from fixed capital expense to variable operational cost as user volume grows. Multi-region deployment, elastic scaling, and compliance localization each add recurring costs that compound significantly across new geographies and regulatory environments.