Key Takeaways:

-

Agentic AI coordinates specialist agents across alert triage, KYC review, sanctions screening, and SAR drafting.

-

Stateful orchestration, RAG-grounded policy retrieval, confidence thresholds, and restricted tool calling are core requirements.

-

Human escalation, immutable audit records, and model validation ensure examiner-ready compliance at every action.

-

An agentic orchestration layer costs $60,000 to $250,000 with 5 to 9 months for deployment.

-

How Intellivon builds agentic AML systems around secure integrations, examiner-ready evidence, and human authorization for filings.

Banks run AML compliance at a massive scale. In practice, each alert demands multiple steps, which include entity research, sanctions screening, adverse media checks, and SAR drafting if needed. Agentic AI for AML compliance automation runs that full sequence autonomously, without a human hand-off at each step. As a result, compliance teams shift from processing alerts to making actual decisions about them.

But agentic AI deployed without a defined escalation architecture creates a compliance problem, not just a technical one. Without confidence thresholds, fallback routing, and audit trails in the agent design, autonomous decisions cannot pass the FFIEC model risk examination. Specifically, institutions that build escalation logic first report up to 87% reductions in manual monitoring effort. At the same time, analysts save an average of 115 minutes per day on alert reviews. That architecture also produces the auditable decision trail that examiners require.

Intellivon has built agentic compliance systems for financial institutions for over a decade. In all our builds, we ensure that escalation logic and audit trails go into the architecture on day one, and not after the build. This blog post covers agent framework selection, workflow design, escalation logic, FFIEC model risk obligations, and development cost.

What Is Agentic AI AML Compliance in Banking?

Agentic AI AML compliance is a controlled software layer that plans and executes multi-step anti-money laundering workflows through specialized software units. These autonomous AI agents in AML compliance banking systems handle deep evidence retrieval, use approved technical tools, route complex cases, and draft regulatory filings.

Crucially, these systems do not independently own regulatory accountability, meaning humans must review and sign off on all high-risk decisions.

Agentic Platform vs AI Copilot vs Transaction Monitoring

Financial institutions must distinguish between legacy data filters, human-guided assistants, and fully autonomous orchestration frameworks.

Understanding these technical differences allows technology leaders to deploy the right compliance infrastructure for their specific operational needs.

| System | Core Function | What It May Do | What Remains Outside Its Scope |

| Transaction Monitoring Platform | Generates or prioritizes alerts | Rules, ML scoring, graph detection | Full investigation orchestration |

| AML Copilot | Assists a human investigator | Summaries, evidence retrieval, SAR draft support | Multi-step autonomous task execution |

| Agentic AML Platform | Orchestrates controlled case tasks | Agent handoffs, tool use, research, validation, draft workflows | Unapproved filing, blocking, account closure |

Ultimately, agentic AI is a structural orchestration decision rather than a simple LLM feature. Consequently, this architectural shift explains why compliance leaders are urgently evaluating these platforms to solve systemic operational bottlenecks.

For a deeper breakdown of the assistant-led foundation, see our guide on How Can Banks Develop an AI AML Compliance Copilot Platform?.

Why Banks Are Moving From Assistance to Agentic AML Workflows

Financial institutions are rapidly evaluating agentic AML systems because compliance operations consist of heavily connected, repetitive tasks that can execute safely under deterministic programmatic boundaries. The core opportunity centers on accelerating multi-step investigation speeds, enforcing absolute evidence collection consistency, and unlocking frozen analyst capacity without introducing regulatory risk.

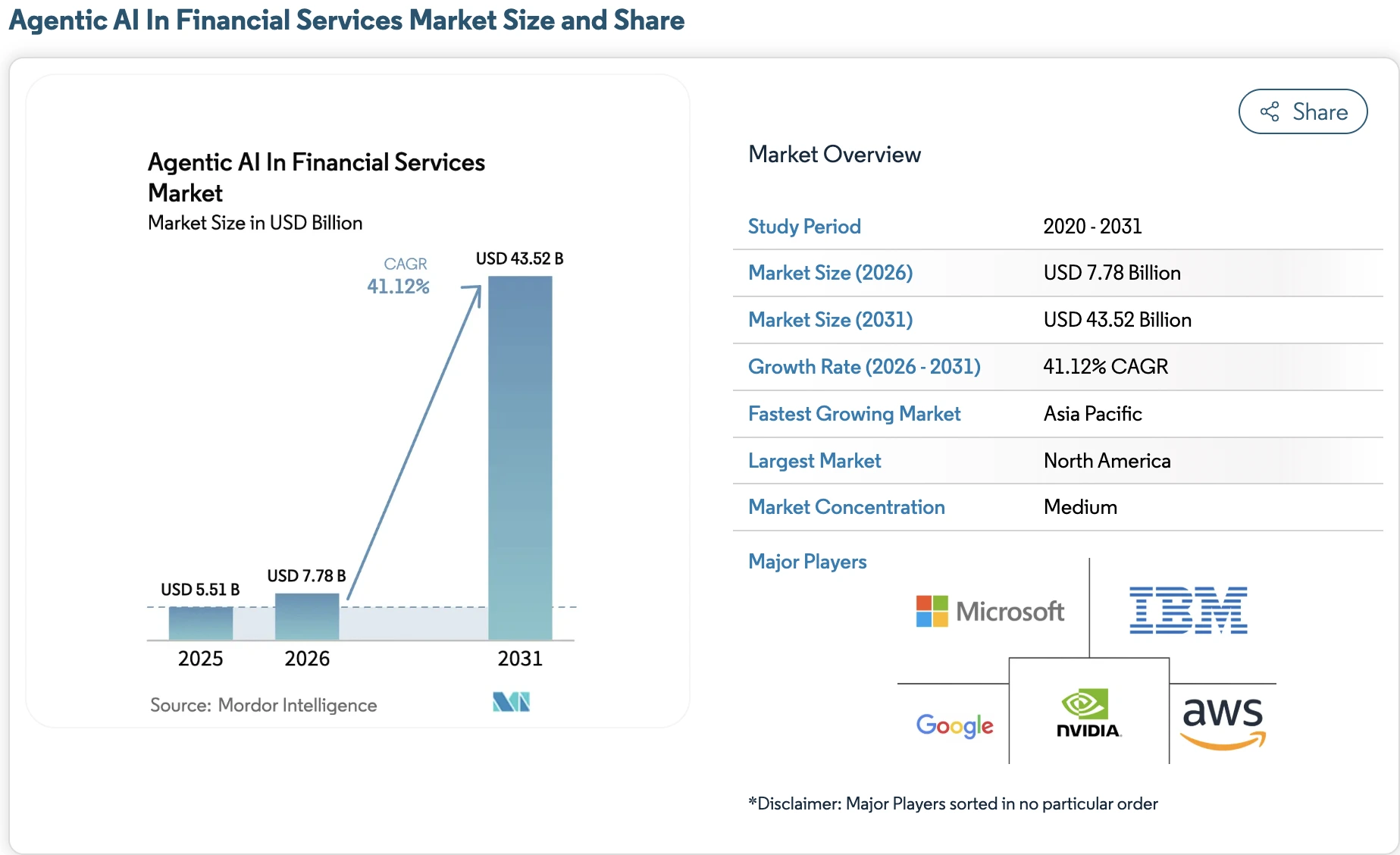

Mirroring this operational shift, the global market size for agentic AI in financial services is projected to reach 43.52 billion dollars by 2031, expanding at a compound annual growth rate (CAGR) of 41.12% from its 2026 valuation of 7.78 billion dollars. Consequently, shifting from passive assistance to active automation has become an essential infrastructure upgrade for modern banks.

1. The Market Signal Is AI Adoption, Not Autonomous Filing

Financial-services AI adoption has formally transitioned beyond simple experimentation into core production infrastructure. However, deploying a multi-agent framework is a highly targeted production decision focused entirely on workflow engineering rather than broad organizational transformation.

Therefore, banks must cleanly separate internal software efficiency gains from actual regulatory filing execution.

2. Where Agentic Value Appears First

Systemic performance improvements appear immediately across four specific, highly labor-intensive operational workflow categories.

- Alert enrichment and triage: Consolidating raw core banking transaction data, historical case notes, and primary account details.

- KYC/CDD and EDD case preparation: Processing complex business registration paperwork, beneficial ownership structures, and source-of-wealth records.

- Entity research, adverse media, and sanctions evidence: Scanning global watchlists, PEP databases, and open-source media archives for real-time risk markers.

- SAR narrative preparation and quality checks: Compiling multi-page investigative summaries that exactly match required regulatory structures.

For example, a live deployment scenario demonstrated a 50% total investigation time reduction and over 4 million Canadian dollars in annual savings for a 200-person financial intelligence unit.

What Must an AML Agent Prove Before It Acts?

An AML agent is defensible only when an institution can replay its actions from original evidence to final recommendation. To achieve this, platforms compile an Examiner Replay Packet, the technical record captured for each autonomous or semi-autonomous task before approval, escalation, disposition, or regulatory reporting.

Consequently, this record ensures complete regulatory auditability.

1. The Core Replay Packet Schema

Modern compliance software must preserve complete analytical lineage to satisfy model validation requirements. Therefore, the Examiner Replay Packet converts abstract deep learning inferences into an inspectable, componentized data schema.

| Evidence Object Retained Per Agent Task | What It Proves to Compliance and Examination Teams |

| Source event snapshot and transaction identifiers | The agent assessed the correct financial activity. |

| KYC/CDD, EDD, and customer-risk data version | Customer context was completely current at decision time. |

| Screening-list dataset and version timestamp | Sanctions, PEP, and adverse media lookups used approved data. |

| Agent role, task ID, and permitted tools | The agent acted strictly within its authorized operational scope. |

| Tool-call log and returned evidence | Each individual external API action can be completely reconstructed. |

| Policy/RAG document version and retrieved passages | The internal reasoning utilized officially approved bank procedures. |

| Model, prompt, workflow, and guardrail versions | Outputs can be identically reproduced and back-tested over time. |

| Confidence score and escalation rule triggered | Human review boundaries were actively and algorithmically enforced. |

| Human review, override, and approval record | Ultimate regulatory accountability remained assigned to a person. |

| SAR or case narrative output version | Final regulatory text maps directly back to cold evidence. |

This platform integration guarantees that every tool call, deterministic prompt variation, and retrieval-augmented generation (RAG) passage is hashed and preserved, which directly addresses the structural expectations outlined in the Federal Reserve, OCC, and FDIC Revised Guidance on Model Risk Management (2026).

2. The Action-Permission Matrix

Institutions must implement a strict, permissioned operational boundary that dictates exactly which compliance tasks can execute autonomously and which require immediate human intervention.

| Agent Action | Allow Automatically | Require Human Approval | Never Allow Autonomously |

| Retrieve transaction and KYC evidence | Yes | No | No |

| Screen using approved data integrations | Yes | For uncertain match disposition | No |

| Draft suspicious activity case narratives | Yes | Before final case disposition | No |

| Recommend formal SAR preparation | No | Yes | No |

| Submit final SAR or CTR filing | No | Yes | Yes, without authorized reviewer |

| Freeze, close, or restrict an account | No | Yes, under bank policy | Yes, without authorized control |

This matrix acts as an active execution guardrail within our deployment framework. For example, while an investigator agent can freely interact with the OFAC Sanctions List Data and Search Guidance to pull screening profiles, it cannot unilaterally execute risk-based actions.

As a result, the platform aligns perfectly with traditional FFIEC BSA/AML Examination Manual standards by keeping all final disposition authorities securely in human hands.

While conventional industry discussions focus on vague notions of auditability or high-level human review, this dual-layered architecture translates regulatory theory into an engineering reality. Technology leaders can treat these tables as a practical checklist for procurement, system validation, and examiner readiness.

Which AI Agents Should an AML Platform Include First?

A first-release deployment should not attempt to launch every conceivable compliance worker simultaneously. Instead, engineering teams must initially prioritize software units that gather evidence, automate repetitive data collection pipelines, and remain exceptionally easy for human teams to audit.

Specifically, institutions must reserve final legal determinations, direct transaction blocking, and adverse customer account actions entirely for authorized risk officers.

Consequently, a staged rollout mitigates initial operational risk while proving the core algorithmic reasoning engine.

1. Agent Roles for the First Controlled Release

A functional multi-agent framework splits labor across distinct, decoupled software modules. Therefore, this separation ensures that each component utilizes highly specific tool sets and data parameters.

| Agent Role | Primary Task | Tools/Data Required | Output | Human Gate |

| Alert Triage Agent | Prioritize incoming flags | Alert store, case rules, risk scores | Escalate or review recommendation | Closure approval |

| Entity Research Agent | Connect parties and ownership | KYC/KYB, registries, graph layer | Entity evidence summary | High-risk verification |

| Sanctions Screening Agent | Check named parties | Approved list integration | Match candidate report | Hit disposition |

| Adverse Media Agent | Gather relevant public-risk evidence | Search/provider API, RAG filters | Cited risk summary | Materiality decision |

| Case Documentation Agent | Assemble investigation history | Case store, evidence index | Review-ready case file | Analyst approval |

| SAR Drafting Agent | Draft narrative text only | Approved case facts, template rules | Narrative prose draft | Filing decision and submission |

At Intellivon, we configure these specialized roles into an integrated, message-driven network. For example, our custom AI agent KYC compliance automation banking pipelines feed structured entity profiles directly into the screening worker.

2. Agents to Defer Until Later Phases

While the temptation exists to automate the entire end-to-end legal filing pipeline, certain advanced operations carry excessive compliance risk for initial releases.

Therefore, technology leaders should defer the following capabilities until the core orchestration layer achieves stable, verified model performance:

- Autonomous alert disposition across broad typologies: Completely closing complex structuring or layering alerts without human oversight.

- Unreviewed sanctions clearance: Unilaterally dismissing potential watchlist matches generated by the core screening engine.

- Direct regulatory filing: Submitting an automated AI agent SAR filing automation banking payload directly to FinCEN systems without human sign-off.

- Automated customer restrictions: Freezing physical credit cards or blocking real-time payment transfers based solely on algorithmic flags.

- Multi-jurisdiction regulatory decisions: Adjusting live case logic across differing international legal requirements without legal counsel validation.

For a deeper breakdown of post-alert workflows, see our guide on How Do Fintech Companies Build AI AML Investigation Systems?.

Once these specific agent boundaries are programmatic facts, the underlying software architecture must guarantee that no sub-agent can bypass its approved permissions, data tools, or mandatory review gates. Consequently, this strict segregation of tasks naturally moves the development team toward the technical step-by-step assembly of the platform.

How Do Agentic AML Workflows Operate Across Five Bank Scenarios?

Agentic AML workflows become practical when each agent has a defined trigger, approved data sources, restricted tools, escalation rules, and a human approval boundary. In a bank, the strongest first-release scenarios are not open-ended investigations. They are controlled workflows for structuring alerts, mule-account activity, cross-border payments, customer-risk refreshes, and correspondent banking reviews.

Consequently, establishing these precise operational guardrails allows banks to safely deploy an agentic AI transaction monitoring platform without compromising regulatory integrity.

Scenario 1 — Cash Structuring Alert Investigation

This workflow isolates intentional transaction splitting designed to evade legal cash-reporting thresholds across multiple branches.

- Trigger & Triage: A core cash-monitoring alert fires. The alert triage agent immediately aggregates transaction histories and branch deposit timestamps.

- Pattern Analysis: A transaction pattern agent maps out repeated below-threshold amounts. Concurrently, the entity research agent links shared business structures or authorized account signatories.

- Lineage Compilation: The CDD agent compares current cash volumes against the declared source of wealth. A policy agent extracts exact procedural guidelines, and the case documentation agent exports a review-ready file to an analyst.

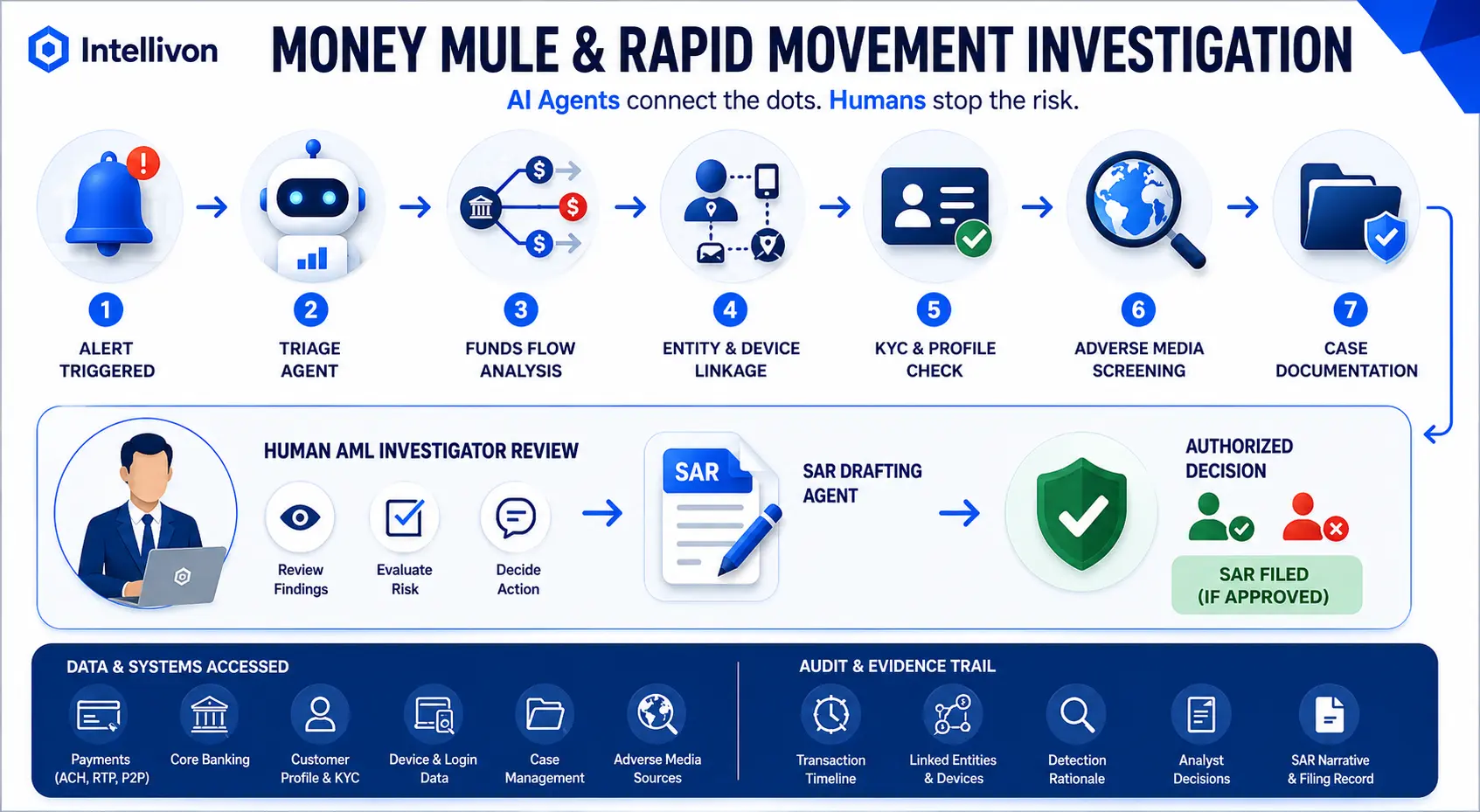

Scenario 2 — Rapid-Movement Payment Investigation

This workflow targets money mule behavior where funds clear and exit digital banking profiles within tight time frames.

- Trigger & Grouping: An automated ACH or real-time payment velocity flag triggers an investigation. The alert triage agent maps all interconnected peer-to-peer transfers.

- Linkage Resolution: A payment-flow agent isolates pass-through speeds. Simultaneously, an entity resolution agent flags matching login devices, phone numbers, or physical addresses used across separate customer accounts.

- Contextual Screening: The KYC review agent tracks profile variances, while the adverse media agent scans public scam registries. The case documentation agent builds a comprehensive fund-flow timeline for human validation.

Scenario 3 — Cross-Border Wire and Sanctions Screening Review

This scenario accelerates international payment compliance by verifying high-risk routing paths and clearing potential watchlist names.

- Trigger & Parsing: The platform intercepts an incoming SWIFT or ISO 20022 message. The screening agent parses originator, beneficiary, and intermediary fields.

- Watchlist Matching: A sanctions agent executes real-time matching against an approved, versioned list database. Concurrently, a funds-transfer risk agent evaluates jurisdiction risks.

- Evidence Gathering: The entity resolution agent checks historical false-positive logs, while a policy agent attaches matching compliance rules. This complete payload is pushed directly to a human reviewer.

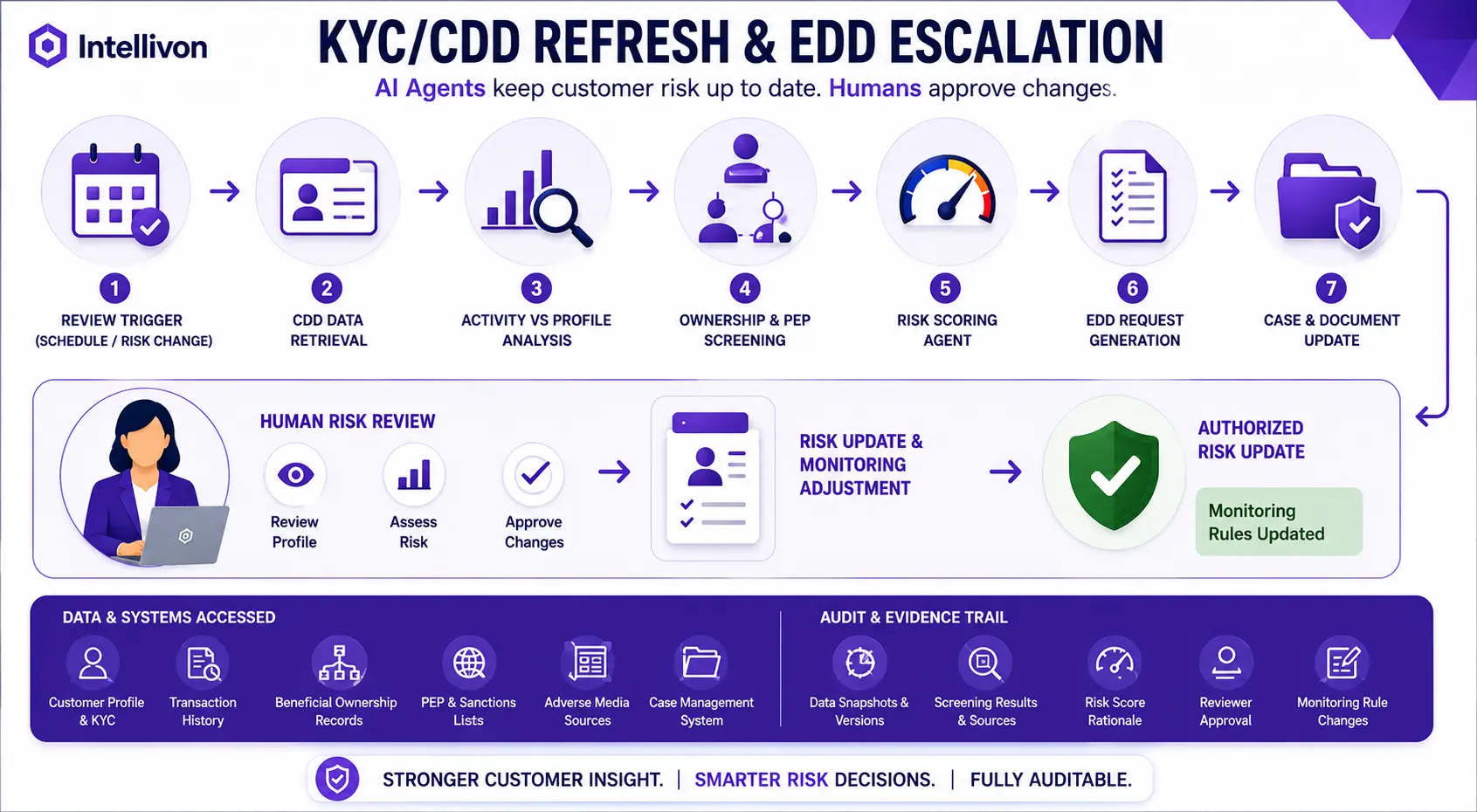

Scenario 4 — KYC/CDD Refresh and Enhanced Due Diligence Escalation

This workflow automates continuous customer risk reviews when corporate profiles or real-world behavior change post-onboarding.

- Trigger & Baselining: A periodic expiration date or transaction-variance event triggers. The CDD agent extracts the original customer baseline profile.

- Anomaly Verification: The transaction review agent checks actual account usage against stated business intents. If anomalies exist, the beneficial ownership agent scans registries for corporate structural shifts.

- Risk Scoring: PEP and adverse media agents search public databases. The risk-scoring engine calculates variance, flags an EDD escalation, and generates an automated customer documentation request.

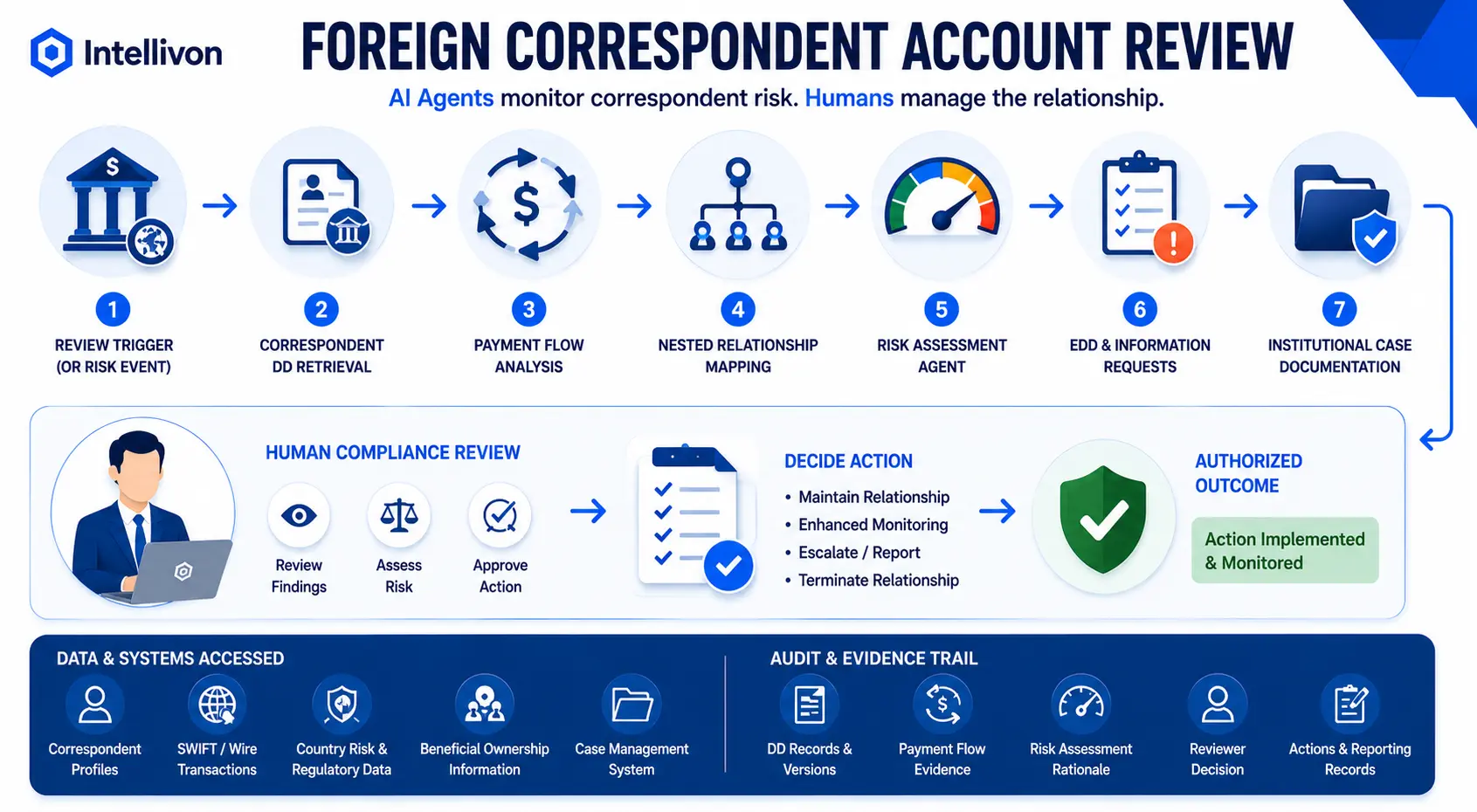

Scenario 5 — Foreign Correspondent and Nested Payment Relationship Review

This workflow evaluates institutional correspondent bank channels to discover unverified downstream banking networks.

- Trigger & Aggregation: A scheduled account review or a cross-border volume spike triggers. The correspondent due diligence agent aggregates the foreign bank’s AML baseline questionnaire.

- Corridor Analysis: The payment-flow agent reviews wire volumes, originating corridors, and nested activity. Simultaneously, the entity relationship agent isolates repeated downstream financial counterparties.

- Risk Evaluation: The risk agent checks actual transaction volumes against approved limits. If deviations occur, the EDD agent flags unverified downstream payment processors, publishing a structured file to the compliance officer.

The Shared Agentic AML Workflow Pattern

To connect these diverse scenarios back to a unified engineering architecture, banks utilize a repeatable, shared agentic pipeline that standardizes responsibilities.

| Shared Workflow Stage | Agent Responsibility | Human Responsibility | Evidence Retained |

| Trigger | Ingest alerts, scheduled reviews, or risk-change events. | Define and approve trigger logic parameters. | Event source data and original timestamp. |

| Evidence Retrieval | Pull approved transaction, customer, screening, and policy data. | Approve and authorize accessible data sources. | Retrieved records, query logs, and data versions. |

| Analysis | Identify patterns, relationships, mismatches, or possible hits. | Review material findings and contextual exceptions. | Scoring metrics, match logic, and data citations. |

| Recommendation | Propose escalation, EDD, case review, or SAR drafts. | Approve or override the automated outcome. | Confidence scores and recommendation records. |

| Regulatory Action | Draft supporting regulatory output text only. | Approve filings, restrictions, or relationship actions. | Final decision record and reviewer identity. |

| Monitoring | Track output quality, overrides, drift, and unresolved cases. | Approve workflow expansions or logic updates. | Test logs, regression metrics, and monitoring history. |

Our engineering teams at Intellivon focus on deploying custom frameworks that standardize this exact interaction loop across legacy core environments. This ensures that every automated step maps directly to an audited human decision node.

These operational workflows demonstrate exactly why an enterprise agentic AML platform requires far more than a basic LLM and a standard case-management connection. Each scenario demands approved data access, specialized agent roles, absolute human accountability, and evidence retained for granular replay.

Therefore, the underlying platform architecture must support controlled state, tool permissions, review gates, and immutable audit history across every active workflow.

What Architecture Supports a Multi-Agent AML Compliance System?

A bank-grade multi-agent AML platform needs separate, isolated layers for source data, event handling, evidence retrieval, agent orchestration, deterministic controls, human approval, reporting, and audit storage. Consequently, this modular separation prevents the underlying generative reasoning model from becoming an uncontrolled system of record or executing unauthorized payment actions.

By segregating execution capabilities from policy enforcement, engineering teams can safely scale multi-agent AML compliance system development within legacy core banking environments. Therefore, a structured architecture ensures absolute systemic safety and auditability.

1. Architecture Layers

Implementing a predictable agentic AI transaction monitoring platform requires translating complex regulatory workflows into decoupled, software-defined enterprise tiers.

| Architecture Layer | What It Does | Example Interfaces or Components | Evidence Retained |

| Source-System Integration | Pulls transaction, KYC, case, and screening inputs. | Core banking APIs, payment processors, SWIFT/ISO 20022. | Source ID, event version, timestamp. |

| Normalization & Identity | Standardizes records and links related entities. | Canonical data model, entity resolution, graph database. | Match reason, confidence, source links. |

| Event & Queue Layer | Starts tasks when an alert or review event occurs. | Event bus, message queues, workflow triggers. | Trigger source, queue path, retries. |

| Governed Knowledge | Retrieves SOPs and regulatory procedures. | RAG pipeline, approved document index. | Retrieved passage, document version. |

| Agent Orchestration | Delegates work and stores task state. | Stateful workflow graph, agent registry. | State checkpoints, handoffs, tool calls. |

| Deterministic Control | Applies non-negotiable compliance rules. | Policy engine, permission service, validation thresholds. | Rule ID, pass/fail result, escalation log. |

| Human Review Layer | Pauses actions requiring accountability. | Reviewer dashboard, interactive approval queues. | Approval, override reason, analyst identity. |

| Reporting & Audit Layer | Preserves case evidence and narratives. | Case store, immutable write-once logs, filing interface. | Replay packet and reporting history. |

By packaging every component inside a microservices agent deployment model, banks can seamlessly scale individual agent squads without taking down their primary banking lines.

2. Framework Selection Decision

When selecting an agentic AI architecture banking framework, technology leaders must choose software tools based on workflow complexity rather than industry hype.

- Linear Workflows: Use simple tool-calling patterns when compliance tasks are completely predictable, linear, and low-risk.

- Complex Graph Workflows: Use a multi-agent AML system design built on a stateful graph when tasks require pause-and-resume capabilities, manual approval gates, automated retries, and branching logic.

For complex graph workflows, engineering teams should evaluate LangGraph compliance workflows because the framework provides built-in LangGraph agent state management and controlled system interruptions.

While developers can use LangChain AML compliance libraries for basic retrieval or tool calling compliance API integrations, the framework itself must never be treated as the actual compliance control layer.

Furthermore, while the ReAct agent framework compliance pattern allows models to iterate through “Thought, Act, Observe” loops, this internal reasoning style requires strict tool restrictions and prompt injection controls.

This design choice prevents severe security vulnerabilities like excessive agency, aligning directly with top industry engineering standards.

Which AI Models Power Agentic Financial Crime Detection?

No single machine learning model can perform every anti-money laundering operation safely. Instead, banks must implement deterministic rules for mandated checks, supervised machine learning for behavioral prioritization, graph analytics for connected-party networks, and retrieval-grounded LLMs for evidence compilation.

Consequently, this multi-model approach ensures that deep language models handle contextual reasoning without gaining unauthorized operational agency or compromising transaction pipelines.

Therefore, mapping the correct model to its optimal operational task minimizes institutional risk.

1. Model-to-Task Mapping

Deploying an enterprise agentic AI financial crime detection platform requires a clear engineering alignment between software models and compliance duties.

| AML Task | Recommended Model or Control | Why It Fits | Output Requiring Review |

| Scenario Checks | Deterministic rules/policy engine | Auditables and reproducible | Alert or immediate hold |

| Behavioral Ranking | Supervised ML/anomaly models | Scores unusual patterns | Risk-prioritized queue |

| Layering Detection | Graph analytics and network vectors | Reveals hidden relationships | Network topology evidence |

| Evidence Extraction | Grounded RAG pipeline | Mitigates data hallucinations | Source-verified quotes |

| Narrative Drafting | Grounded generative AI LLM | Converts data into clean text | Human-approved narrative |

| Agent Validation | Critic agent plus automated tests | Checks output support | Pass or escalate outcome |

2. Model Requirements a CCO Should Demand

To pass upcoming regulatory examinations, Chief Compliance Officers must require specific, verifiable technical capabilities from their model infrastructure:

- Evidence Citation: Verifiable source footnotes for every single factual claim written within an automated case summary.

- Structured Schemas: Forced JSON or database outputs rather than relying entirely on unpredictable, free-form text blocks.

- Threshold Controls: Programmable agent confidence threshold compliance metrics that trigger immediate human-in-the-loop agent escalation when breached.

- Lineage Records: Complete, unalterable prompt, weight, and model type version histories for every transaction reviewed.

- Regression Testing: Standardized model benchmark execution against historically validated bank case sets to monitor analytical drift over time.

Ultimately, these core models can compile evidence and generate risk recommendations only from the specific enterprise systems that their underlying API integrations allow them to safely access. Consequently, technology leads must look next at mapping the physical systems the agent squads must integrate with to operate safely in production.

Which Banking Integrations Must AML Agents Access Securely?

Compliance agents require controlled read access to transactional, customer, screening, and case evidence before supporting compliance workflows. Conversely, write access must remain exceptionally narrow, explicitly logged, and structurally gated wherever actions alter filings, customer statuses, transaction outcomes, or database records.

Consequently, this strict segregation protects the bank’s core transactional perimeter.

1. Required Integration Map

Deploying a secure build AI agent AML compliance workflow demands a disciplined, layer-by-layer integration strategy across legacy and cloud-native systems.

| Integration | Data or Function Supplied | Agent Use | Required Control |

| Core Banking Ledger | Accounts, balances, transfer history. | Evidence assembly. | Read-only retrieval for initial release versions. |

| Payment Processors | ACH, wire, mobile wallet, RTP data. | Pattern review. | Event timestamp tracking and payload versioning. |

| SWIFT / ISO 20022 | Cross-border transaction text fields. | Counterparty analysis. | Automated schema validation and field mapping. |

| KYC / KYB Platforms | Legal identity and ownership records. | Customer context. | Role-based access controls and data minimization. |

| Sanctions Feed | Dynamic global watchlist entries. | Match evaluation. | Versioned list data; no open public scraping tools. |

| Adverse Media API | Public, source-linked risk articles. | Entity research. | Source provenance tracking and relevance scoring. |

| Case Management | Prior internal cases and dispositions. | History check. | Immutable user access logging and retention rules. |

| Blockchain Analytics | Public wallet risk metrics and asset flows. | Web3 investigation. | Vendor-verified evidence retention standards. |

Enforcing these programmatic interaction rules at the API gateway layer blocks malicious or unintentional system actions. For instance, configuring specialized agent core banking integration layers to run entirely on isolated, read-only replica databases keeps data clean.

This design ensures that agent payment processor integration tasks and agent SWIFT monitoring pipelines ingest transaction evidence without impacting live ledger balances. As a result, the bank protects its operational state while maintaining automated tracking velocity.

For a deeper breakdown of monitoring infrastructure and payment rails, see our guide on How Do You Build an AI Transaction Monitoring Platform Today?.

What Compliance Controls Must Govern Agentic AI AML Compliance?

Agentic AI AML compliance must be governed concurrently as an enterprise financial-crime workflow and a structured model-risk system. Banks require comprehensive model inventories, independent validation, granular permission controls, immutable evidence retention, and strict data privacy protections.

Crucially, human accountability must remain the absolute boundary before software agents can influence case dispositions or final regulatory reports.

1. Current Model Risk Guidance for US Banking Readers

United States financial regulators require institutions to anchor their deployment strategies within the April 2026 revised interagency model risk guidance.

Consequently, engineering teams must not center their risk frameworks on superseded guidance like SR 11-7 or SR 21-8. Instead, teams must address the modernized expectations detailed in Federal Reserve SR 26-2 and OCC Bulletin 2026-13, which specifically govern automated, generative systems.

- Model Inventory Expansion: Banks must catalog and track every individual prompt template, vector retrieval index, external tool integration, confidence threshold, and specific workflow graph version as independent model components.

- Validation & Monitoring: Independent validation teams must execute continuous regression testing against historical baseline datasets to catch drift in agent reasoning before it impacts live transaction monitoring queues.

- Third-Party Ingestion Controls: Production architectures must ingestion-test and log all external vendor API changes and open-source foundation model updates to guarantee absolute operational reproducibility over time.

2. BSA/AML and SAR Control Boundary

Under current federal regulations, a BSA compliance agent workflow can execute multi-step investigation data gathering, but it cannot own final filing authority.

While the system may compile background evidence and execute FinCEN filing agent automation routines to draft a narrative, a human officer must review the output.

- Mandatory Human Review: A qualified compliance reviewer must verify the source evidence, adjust the analytical reasoning text, and explicitly authorize the final submission (Source: FinCEN SAR Electronic Filing Instructions).

- SAR Confidentiality Guard: Institutions must implement tight role-based agent access control and isolated, encrypted software environments to completely shield sensitive filing logs from unauthorized internal or external entities.

- Lineage Ledger Retention: Every version of the generated narrative draft, alongside its exact source transaction links, must reside permanently within the Examiner Replay Packet to align with FFIEC BSA/AML Examination Manual audit standards.

3. Sanctions and Tool-Use Controls

To ensure continuous compliance with international regulations, agent frameworks must connect exclusively to approved, versioned sanctions datasets through secure provider APIs.

- Banned Web Scraping: Software teams must never design automated screening agents around OFAC’s public web search interface, as it lacks the programmatic structure required for auditable system execution (Source: OFAC Sanctions List Guidance).

- Escalation Thresholds: The platform must mandate a strict human-in-the-loop agent escalation path whenever a potential watchlist hit is identified, preventing autonomous clearance of true matches.

- Audit Logging: Every automated screening action must log the active list version, the specific match criteria utilized, the raw API outcome, and the subsequent human reviewer rationale.

4. LLM and Agent Security Controls

Deploying autonomous systems within a bank requires advanced software-level guardrails to preserve data safety and prevent malicious exploitation.

- Injection Filtering: Platforms must route external documents and adverse media search data through rigorous inbound input filters to block malicious prompt-injection vectors (Source: OWASP GenAI Security Project Top 10, 2025).

- Least-Privilege Tooling: System engineers must implement explicit tool allowlists, ensuring software units operate within tight, role-specific runtime boundaries to prevent excessive agency.

- PII Masking & Safety: Real-time data masking pipelines must strip sensitive customer data before transmitting payloads to external model endpoints, ensuring long-term agent data privacy and banking compliance.

- Output Validation: Deterministic parsing layers must scan and validate all generated agent outputs before allowing any downstream write action into core banking systems.

Compliance regulations cannot remain as static policy text inside an enterprise manual. Instead, the software engineering process must transform each requirement into deterministic system behaviors and reproducible test evidence, shifting focus toward production implementation.

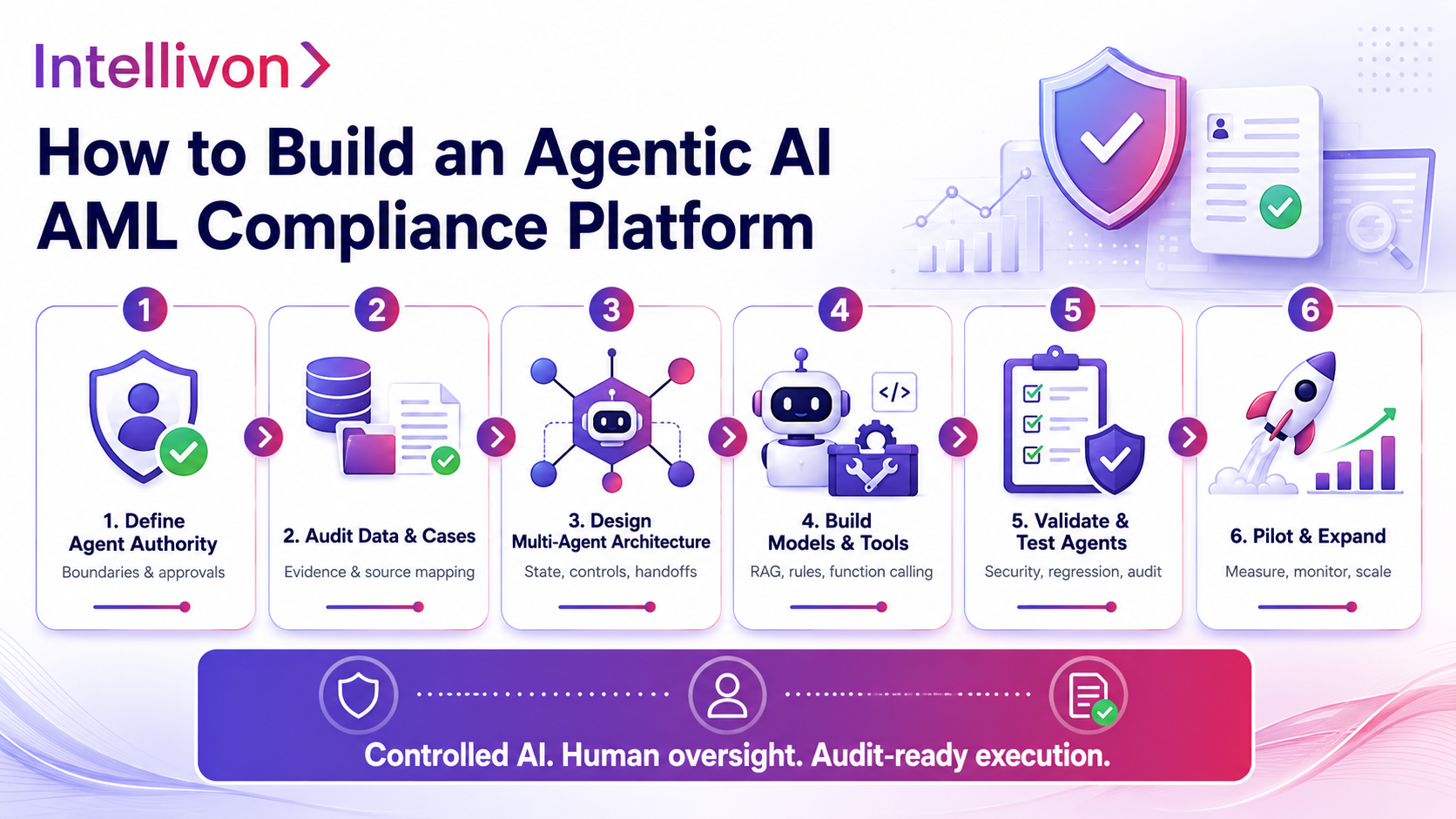

How to Build an Agentic AI AML Compliance Platform

Building an enterprise platform requires a structured engineering approach that balances generative reasoning with strict deterministic boundaries. To safely build agentic AI AML compliance platform systems, banks must transition through a disciplined six-step methodology.

This lifecycle guarantees that automated workflows enhance operational velocity without introducing model risk or compliance vulnerabilities.

Step 1: Define Agent Authority Before Selecting Models

Define exactly which tasks an agent may perform, which actions require immediate approval, and which actions remain prohibited. This prevents engineering teams from building excessive autonomy before compliance owners define acceptable control boundaries.

- Workflow Mapping: Maps the complete process from initial alert ingestion to final SAR submission to produce a comprehensive action-permission matrix.

- Access Controls: Programmatically defines user roles, system access levels, confidence thresholds, and deterministic escalation rules within the workflow engine.

- Intellivon Approach: We map agent permissions directly against live case operations, compliance policies, reviewer accountability, and examiner evidence requirements.

Authority determines exactly which data and transactional systems the platform must access securely.

Step 2: Audit Data, Cases, and Approved Knowledge Sources

Agents need traceable, usable evidence before they require sophisticated language reasoning. A data audit checks transaction fields, customer records, historical dispositions, investigation notes, internal policies, and screening sources before model work begins.

- Schema Verification: Defines target transaction schemas while verifying the completeness of KYC/CDD and beneficial ownership structures.

- Lineage Ingestion: Ingests historical case outcomes and reviewer labels to establish an empirical performance baseline.

- Intellivon Approach: We systematically identify missing evidence pathways and create a governed source map for every planned agent task.

Clean, audited evidence sources allow a controlled, resilient multi-agent architecture to be designed.

Step 3: Design the Multi-Agent Architecture and State Controls

The underlying platform must separate retrieval, reasoning, downstream actions, human approval loops, and immutable audit history. Each agent within the multi-agent system design receives a narrow task, approved tool keys, state checkpoints, fallback routing capabilities, and clear handoff rules.

- State Management: Implements an active agent registry and stateful workflow graphs using LangGraph to preserve session states.

- Interruption Gates: Configures a deterministic policy engine to enforce programmatic human interruption points and data preservation.

- Intellivon Approach: We design multi-agent orchestration entirely around structural traceability and controlled execution to prevent excessive agency.

Once workflow paths are completely controlled, advanced reasoning models can be introduced safely.

Step 4: Build Models, Tools, and Grounded Agent Outputs

Production-grade compliance platforms require a hybrid model stack rather than a single foundation model. Rules handle mandatory threshold checks, machine learning models prioritize behavior patterns, graph analytics connect entities, and grounded LLMs draft narratives using retrieved evidence.

- Function Calling: Builds tool-calling mechanics over approved bank APIs to facilitate secure, schema-forced data extraction.

- Grounded RAG: Routes text generation through a constrained RAG pipeline utilizing structural templates and automated hallucination checks.

- Intellivon Approach: We link all generated outputs back to physical transaction records and specific policy passages for rapid verification.

The integrated model layer now requires rigorous, production-grade compliance validation and security testing.

Step 5: Validate Agents Against Cases, Attacks, and Examiner Questions

Agent testing must prove both absolute operational accuracy and controlled programmatic behavior. A bank must rigorously test whether its agent squads retrieve correct facts, avoid unsupported claims, respect runtime permissions, escalate correctly, and preserve evidence.

- Sandbox Testing: Utilizes a version-controlled “golden-case” test set and executes intensive prompt-injection and data leakage testing.

- Regression Blocks: Runs automated regression tests after any prompt variation, foundation model upgrade, or sanctions watchlist update.

- Intellivon Approach: We test each capability independently in an isolated sandbox before evaluating the full end-to-end workflow graph.

Validated workflows can safely move into a measured production pilot before expanding wider operational autonomy.

Step 6: Pilot Controlled Workflows and Expand by Evidence

The first live production release should measure a highly restricted workflow, not attempt to automate the entire AML compliance program. Begin by deploying evidence retrieval, alert triage support, case file assembly, or initial SAR narrative drafting before increasing agent permissions.

- Baseline Tracking: Selects a limited pilot population to track baseline investigation times, quality assurance effort metrics, and human override rates.

- Rollback Paths: Establishes continuous production drift monitoring and an instantaneous rollback path if performance metrics deviate from expected thresholds.

- Intellivon Approach: We authorize workflow expansion only when the system demonstrates reliable output quality, controlled tool usage, and measurable operational value.

Pilot results provide the precise operational inputs needed to construct an honest, data-backed business case.

What Does Agentic AI AML Platform Development Cost?

Building an agentic AI AML compliance platform typically costs $60,000–$250,000 for a controlled agentic layer added to an existing AML environment, depending on workflow scope, integrations, agent autonomy, evidence controls, and model-validation requirements. This range covers an agentic AML orchestration and investigation layer. Crucially, it does not cover replacing the bank’s full transaction-monitoring infrastructure across all rails and jurisdictions. Therefore, technology leaders can scale operational capabilities without abandoning their depreciated core banking assets.

Development Phase Cost Breakdown

Deploying a secure, multi-agent financial crime detection system requires breaking down engineering investments across seven distinct delivery milestones.

| Development Phase | Estimated Cost Range | What Is Included |

| Workflow Scope & Authority Mapping | $5,000–$15,000 | Agent permissions, target workflows, review gates, success metrics. |

| Data, Case, & Knowledge Audit | $8,000–$22,000 | Data mapping, evidence quality review, SOP/RAG document planning. |

| Architecture & Secure Integration Design | $10,000–$30,000 | Orchestration, APIs, data flow, audit storage, security planning. |

| Multi-Agent Workflow & Model Build | $20,000–$70,000 | Agents, retrieval, tool calling, scoring, graph links, structured outputs. |

| Integrations & Reviewer Interface | $10,000–$45,000 | Core banking/case/screening connections, approval dashboard. |

| Compliance Controls & Validation | $8,000–$35,000 | Access controls, model testing, red teaming, replay packet verification. |

| Pilot Deployment, MLOps, & Monitoring | $7,000–$33,000 | Production pilot, monitoring, fallback routing, performance reporting. |

Ongoing Maintenance Cost

- Annual Budgeting: Institutions should allocate 18%–25% of the initial build cost annually for recurring operational upkeep.

- Operational Scope: This budget includes continuous model and prompt monitoring, automated agent regression tests, and sanctions list provider updates.

- Compliance Validation: Upkeep covers policy-index refreshes, integration API maintenance, regular security red-teaming, and generating updated validation evidence for examiners.

Planning an Agentic AML Build?

Download the Agent Authority and Examiner Replay Packet Checklist to map workflows, approval gates, integrations, and evidence requirements before requesting development estimates.

For a deeper breakdown of cost drivers in an adjacent controlled workflow, see our guide on What Does It Cost to Build an AI AML Compliance Copilot?.

The cheapest development path is not automatically the safest or most compliant first release. Consequently, buyers must evaluate whether custom agentic automation aligns appropriately with their present transaction volume and legacy software maturity.

Build Agentic AI AML Compliance With Intellivon

Agentic AI can help banks move complex AML investigations forward by coordinating evidence retrieval, customer-risk review, transaction analysis, case summarization, escalation preparation, and SAR drafting inside one controlled workflow.

Intellivon builds agentic AI AML compliance platforms that connect to your financial systems, give each agent defined permissions, preserve full audit evidence, and keep every material compliance decision with qualified reviewers.

1. Select AML Workflows Where Agents Can Act Safely

Agentic AI should begin with tasks that consume investigator time but do not transfer regulatory accountability to the system.

Intellivon helps financial institutions identify where AI agents can retrieve, assemble, compare, summarize, and route evidence while compliance officers continue to control case outcomes and reporting decisions.

- Map alert triage, KYC/CDD review, EDD, screening, investigation, and SAR workflows.

- Identify repeated manual tasks that delay analyst review and case progression.

- Separate agent-executable actions from human-controlled compliance decisions.

- Define which case types require mandatory analyst escalation from the start.

- Establish pilot KPIs for time saved, evidence quality, corrections, and approvals.

- Prioritize one measurable workflow before expanding agent authority.

2. Design Task-Specific AML Agents With Clear Boundaries

An agentic AML platform should not rely on one unrestricted AI system handling every compliance activity. Each agent needs a defined task, approved data access, permitted tools, output format, escalation trigger, and human approval requirement. Intellivon designs agent roles around real FinCrime workflows rather than broad automation claims.

Your controlled AML agent layer can include:

- An evidence retrieval agent that gathers approved case and transaction records.

- A KYC/CDD review agent that summarizes customer and ownership information.

- A transaction analysis agent that explains suspicious payment sequences and patterns.

- An adverse-media agent that extracts relevant findings with source references.

- A case summary agent that prepares investigator-ready chronologies and open questions.

- A SAR drafting agent that prepares narrative content for reviewer approval.

- A quality-control agent that checks missing evidence, unsupported claims, and approval steps.

Every agent should operate within documented access rules. It should also record what it reviewed, what it produced, and when a human decision became necessary.

3. Connect Agents to Evidence, Policies, and Case Systems

Agentic AI becomes useful only when it works with approved evidence inside your existing AML operations.

Intellivon connects agents to transaction monitoring outputs, customer records, investigation documents, regulatory guidance, and case-management workflows through secure, permissioned integrations.

- Connect transaction records, alert histories, and customer-risk profiles.

- Retrieve KYC, KYB, CDD, EDD, and beneficial ownership documentation.

- Integrate screening findings, adverse-media evidence, and investigation notes.

- Build governed access to FinCEN, FFIEC, FATF, OCC, and internal policy material.

- Route agent outputs into existing case-management and analyst review queues.

- Preserve source citations, document versions, model actions, and reviewer edits.

- Apply role-based access controls across every agent, tool, and retrieved record.

This architecture gives investigators faster access to relevant evidence without allowing agents to search unrestricted compliance data or operate beyond their assigned purpose.

4. Build Agentic SAR Support Without Losing Human Control

SAR preparation is one of the strongest agentic AI use cases, but it also requires the strictest controls. Intellivon develops workflows where agents organize approved evidence, draft clear narratives, identify missing facts, and prepare cases for review.

The final decision to escalate, approve, or file remains with authorized compliance professionals.

- Assemble transaction dates, amounts, parties, accounts, and jurisdictions.

- Organize suspicious patterns into a clear investigation chronology.

- Draft SAR narratives from permitted case evidence and approved guidance.

- Flag missing facts, conflicting records, or unsupported risk statements.

- Prevent filed SAR history from entering routine agent retrieval without approval.

- Require named human review before narrative approval or filing action.

- Retain every generated draft, correction, approval, and submission record.

Your AML team gains drafting support and stronger evidence visibility. Your institution retains accountability for every reporting decision.

5. Establish Governance Before Agents Enter Live FinCrime Workflows

An AML agent should never enter production because it performs well in a demonstration. Intellivon defines governance, validation, security, and monitoring controls before an agent influences live investigation work, so banking teams can assess whether automation remains accurate, confidential, and examination-ready.

- Test each agent against approved historical or synthetic investigation scenarios.

- Validate evidence retrieval, narrative completeness, and factual accuracy.

- Measure unsupported claims, missing citations, and reviewer correction rates.

- Run access-control, confidentiality, and prompt-injection testing.

- Restrict SAR-sensitive records through permissioned retrieval boundaries.

- Record agent decisions, tool calls, handoffs, and human overrides.

- Monitor prompt changes, model updates, policy revisions, and output drift.

- Maintain immutable audit evidence for internal governance and examination needs.

Agentic AI should expand only after the institution proves that agents support better investigation work without weakening compliance control.

6. Launch a Controlled Agentic AI AML Pilot

A successful first release does not attempt to automate every alert, investigation, or reporting workflow. It proves that defined AI agents can execute approved supporting tasks, reduce investigator administration, strengthen documentation quality, and escalate decisions correctly within a governed AML process.

With Intellivon, your agentic AI AML roadmap can include:

- Workflow selection for the first controlled agent deployment.

- Agent-role design across research, review, drafting, and quality checks.

- Secure integration planning for banking and compliance data sources.

- Permissioned tool access and human-approval boundary mapping.

- SAR confidentiality, audit trail, and validation-control design.

- Pilot KPI planning across investigator effort, quality, and security.

- A phased production roadmap aligned to budget and governance readiness.

Build controlled AI agents that move FinCrime investigations forward, strengthen evidence handling, and keep final compliance authority with your team.

Conclusion

Deploying agentic AI AML compliance is not a shortcut to unsupervised filing or opaque, unmonitored decision-making. Instead, it represents a highly governed software architecture that coordinates deep evidence retrieval, specialized agent roles, restrictive tool permissions, validation checks, and human escalation.

The optimal first release adds an agentic workflow layer directly to your existing compliance environment, measures a narrow set of outcomes, and preserves an Examiner Replay Packet for every single material action.

Consequently, this modular upgrade pattern maximizes immediate operational efficiency without introducing systemic regulatory risk or model drift. Therefore, banks must select a development partner that understands how to translate compliance authority into enforceable software controls, rather than simply connecting an LLM to a case queue.

Things To Know About Agentic AI AML Compliance Development

Q1. How Much Does It Cost to Build an Agentic AI AML Compliance Platform?

A1. Building an agentic AI AML compliance platform typically costs $60,000–$250,000 for a controlled layer on an existing AML stack. Costs rise with additional agent workflows, core-system integrations, evidence retention, approval controls, validation, security testing, and monitoring. However, replacing enterprise transaction monitoring requires a separate, larger investment and should not be included in this range.

Q2. How Long Does a Multi-Agent AML Compliance System Development Project Take?

A2. A controlled multi-agent AML first release typically takes 5–9 months to design, build, validate, and pilot. That timeline includes integrations, agent workflows, approval gates, model testing, security controls, and production monitoring. However, an evidence-retrieval or SAR-drafting pilot can launch sooner. Multi-rail or multi-jurisdiction execution requires longer implementation, testing, and compliance validation.

Q3. Can an AI Agent Draft or File SARs Without Human Review?

A3. An AI agent can retrieve approved evidence and draft a SAR narrative, but it should not file independently. Instead, a bank-grade workflow requires authorised human verification and filing approval before regulatory submission. The platform should preserve source evidence, narrative versions, reviewer edits, approval records, and filing decisions within an Examiner Replay Packet.

Q4. How Is an Autonomous AML Investigation Agent Different From Rule-Based Automation?

A4. Rule-based automation follows fixed logic, such as thresholds or predefined alert routes. In contrast, an autonomous AML investigation agent can plan tasks, retrieve context, use approved tools, connect evidence, and prepare recommendations. However, deterministic rules must still govern mandatory thresholds, permissions, escalation points, and prohibited actions. Agents operate inside those controls; they do not replace them.