Modern fintech enterprises require quick financial movement to get payments across borders. However, some traditional banks still depend on outdated systems, which often involve several middlemen, leading to high costs. At the same time, deep inefficiencies slow down cash flow for growing businesses. Thus, enterprise leaders need to rethink their international transfer policies now.

A real-time cross-border payment platform can fix these problems. With digital verification, payments skip extra steps with the platform’s use. Transparency enables treasury teams to monitor capital with great accuracy. At the same time, improved systems simplify reconciliation across different regions. Consequently, businesses cut operational costs and boost international growth through better flexibility.

Intellivon creates high-performance payment platforms that tackle complex cross-border engineering issues. Our expertise includes AI-driven compliance and secure distributed ledgers. In this blog, we will discuss how we build these platforms for enterprises from the ground up.

Why Real-Time Cross-Border Infrastructure Matters Now

Real-time cross-border payment platforms utilize ISO 20022 messaging and Distributed Ledger Technology (DLT) to enable atomic settlement.

By removing sequential intermediary steps, these systems significantly reduce idle capital (with some estimates from J.P. Morgan suggesting a potential 10% reduction in liquidity costs) and eliminate settlement latency.

Real-time cross-border payments are expanding quickly. Growth is driven by RTP systems, blockchain networks, and emerging CBDC initiatives. However, they still represent a smaller segment within the broader $200B+ global cross-border payments market.

Adoption remains strongest in North America and Asia-Pacific. In these regions, projected CAGR ranges between 7% and 9%, reflecting steady enterprise investment and regulatory support.

Therefore, adopting a real-time infrastructure is now a strategic necessity to ensure total visibility and immediate capital access. Here is why:

1. Shift From SWIFT-Only to Multi-Rail Models

Companies are no longer relying solely on the SWIFT network. Instead, they use multiple payment rails to move money. This mix includes blockchain and local instant systems like SEPA.

Consequently, this approach offers much better reliability. It also allows firms to route payments based on current costs. Therefore, you avoid the risks of a single point of failure. This flexibility is essential for scaling a global business effectively.

2. Cost of Settlement Delays

Slow payments act like a hidden tax on your business. Money stuck in transit cannot be used for new projects.

This “dead capital” limits your ability to grow quickly. Furthermore, finance teams spend too much time on manual tracking. In contrast, fast payments build stronger trust with global partners.

Therefore, removing these delays directly helps your cash flow. This shift turns treasury management into a true competitive advantage.

3. Fintechs Replacing Correspondent Banking

The old banking model uses too many middleman banks. Each one charges a fee and causes more delays. However, fintech providers connect directly to local clearing systems. These platforms integrate easily with your existing software.

They also offer better exchange rates by finding direct liquidity. As a result, leaders are moving their high-volume payments to these tech-first partners. This transition offers the efficiency that old banks simply cannot match.

4. Regulatory Pressure Driving Infrastructure Rebuilds

Global regulators now require faster and clearer payment data. Specifically, the new ISO 20022 standard demands much more detail. Older banking systems often fail to handle this heavy data load. Modern platforms use AI tools for safety checks in milliseconds.

These tools perform compliance scans without slowing down the transfer. Thus, you stay safe while keeping your business moving fast. This setup is vital for a 24/7 global economy.

Adopting a modern cross-border infrastructure eliminates the financial friction inherent in legacy banking models. This strategic transition ensures your enterprise remains agile and compliant in an increasingly connected global market.

What Is A Real-Time Cross-Border Payment Platform?

A real-time cross-border payment platform is a digital infrastructure that settles international transactions instantly. Unlike traditional banking, which relies on a chain of intermediary banks, these platforms use a direct “point-to-point” model.

They utilize modern protocols like ISO 20022 and Distributed Ledger Technology to move funds and data simultaneously. Furthermore, it provides immediate finality, ensuring that the recipient receives the exact amount sent without hidden deductions.

Modern enterprises now benefit from this technology through dramatically improved cash flow management. Specifically, real-time rails allow for precise “just-in-time” payments to global suppliers or employees. This capability reduces the amount of idle capital trapped in transit across different time zones.

In addition, the platforms offer 24/7 availability, bypassing the limitations of traditional banking hours or public holidays. Therefore, businesses can operate with the same financial agility internationally as they do domestically.

Who Actually Needs a Real-Time Cross-Border Platform?

Organizations that handle high-frequency transactions or manage complex global workforces face the most friction. Therefore, implementing a real-time cross-border platform solution becomes a necessity for those seeking to maintain a competitive edge in a digital-first economy.

1. Global Fintechs Scaling Multi-Currency Products

Fintech companies must provide a seamless user experience to remain competitive. Customers now expect instant transfers regardless of the destination or currency.

Consequently, these firms require robust backend rails that support immediate multi-currency conversion. Using a real-time platform allows them to settle trades or wallet top-ups in seconds.

Therefore, they can scale their product offerings across borders without building individual bank relationships in every country.

2. Embedded Finance Providers Expanding Internationally

Embedded finance allows non-financial companies to offer banking-like services within their own apps. For instance, a software company might offer instant business loans to its international users.

These providers need reliable infrastructure to move capital across borders without manual intervention. Real-time platforms offer the necessary APIs to automate these complex workflows effectively.

As a result, companies can focus on their core product while the payment layer handles the heavy lifting of global settlement.

3. Marketplaces and Platforms Handling Global Payouts

Gig economy platforms and global marketplaces rely on keeping their sellers and creators satisfied. Delayed payouts can lead to high churn rates and a damaged brand reputation.

However, a real-time platform ensures that workers receive their earnings as soon as a task is completed. This immediate gratification builds significant trust and loyalty within the platform’s ecosystem.

Consequently, the marketplace gains a major advantage over competitors who still process payments in weekly or monthly batches.

4. Enterprises With Multi-Entity Treasury Operations

Large corporations often have dozens of legal entities spread across different continents. Managing internal liquidity between these subsidiaries is frequently a slow and expensive process.

Real-time platforms allow for instantaneous “inter-company” transfers to balance accounts as needed. Furthermore, this transparency helps treasury teams avoid taking out short-term loans to cover temporary local shortfalls.

Therefore, the entire organization operates with much higher capital efficiency and reduced financial risk.

Implementing a real-time cross-border payment platform allows various business models to eliminate the delays that once hampered global growth. This technology transforms the treasury function into a proactive tool for immediate international expansion.

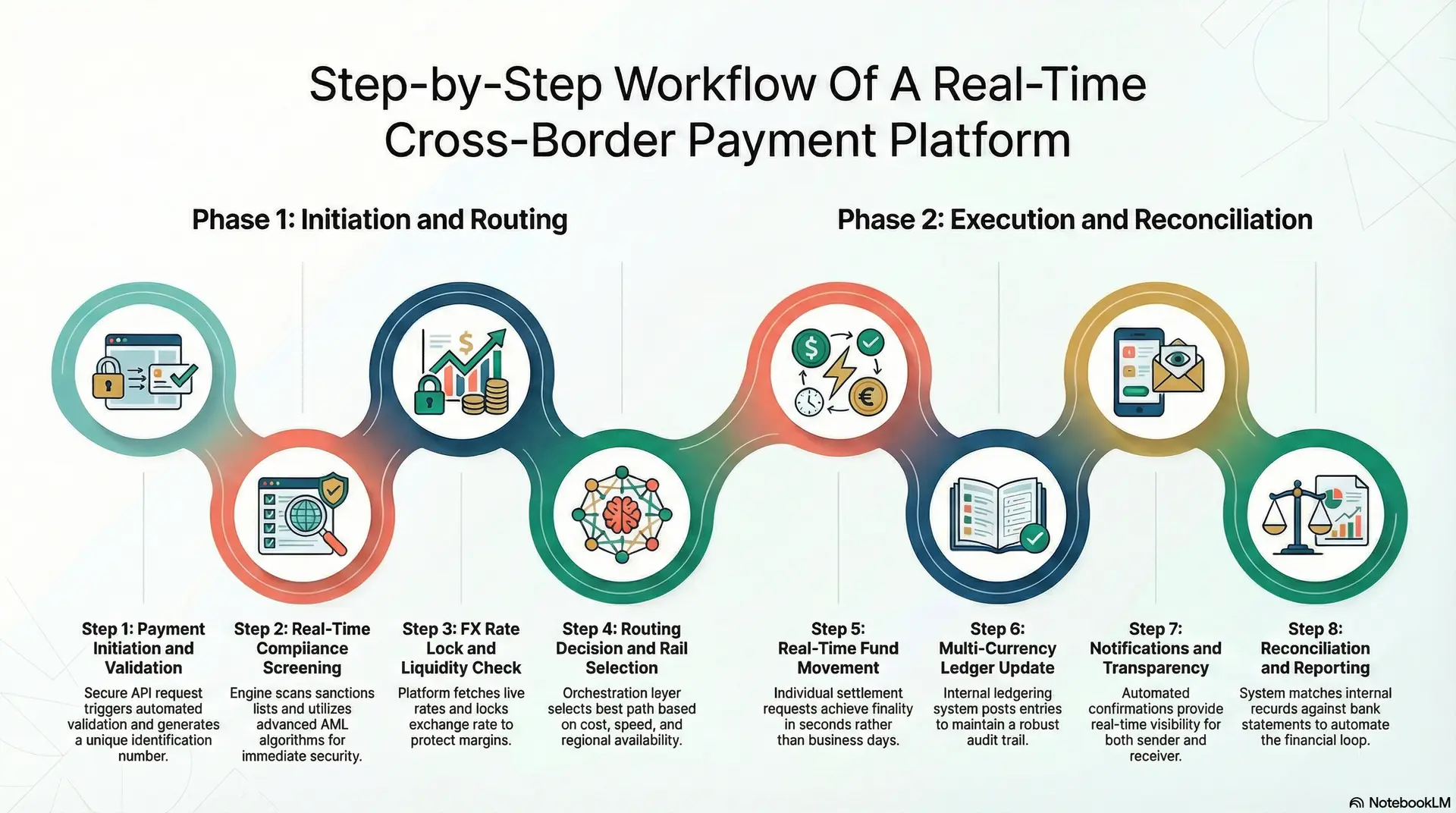

Step-by-Step Workflow Of A Real-Time Cross-Border Payment Platform

A real-time cross-border payment platform operates through a series of synchronized, high-speed digital handshakes. Unlike the manual, batch-based processing of the past, this modern workflow ensures that data and value move in parallel.

Specifically, the system utilizes API-driven communication to trigger actions across global banking rails instantly. Here is an example of a workflow of a real-time cross-border payment platform:

Step 1: Payment Initiation and Validation

The sequence begins with a secure API request from your enterprise software. Immediately, the platform validates all required fields like bank codes and destination currencies.

Furthermore, it generates a unique identification number for end-to-end tracking. This automated check prevents simple errors before they enter the processing pipeline. Therefore, only clean data proceeds to the core processing engine.

Step 2: Real-Time Compliance Screening

Security remains the primary focus during the screening phase. The engine scans global sanctions lists such as OFAC or the UN in real time. Simultaneously, advanced AML algorithms evaluate the transaction for potential high-risk patterns.

If the system detects an anomaly, it flags the request for expert review. Consequently, businesses maintain strict compliance without sacrificing operational velocity.

Step 3: FX Rate Lock and Liquidity Check

Next, the platform fetches a live FX rate from a primary liquidity provider. It verifies that sufficient funds exist in the destination currency to fulfill the request. Moreover, it locks the exchange rate for a set window to protect your margins.

This transparency removes the uncertainty of fluctuating intermediary fees. Thus, you ensure the exact amount reaches the global recipient.

Step 4: Routing Decision and Rail Selection

An intelligent orchestration layer evaluates the best path for the transfer. It considers variables like current network cost, speed, and regional availability. Specifically, the system selects between local clearing systems or blockchain-based payment rails.

If one path fails, cascading logic automatically identifies a secondary backup. Consequently, every payment follows the most reliable and efficient route possible.

Step 5: Real-Time Fund Movement

Value movement occurs immediately after the optimal rail is selected. The system debits the source account and sends a settlement request to the network. Unlike traditional batch processing, each transfer is treated as an individual, atomic event.

In addition, the platform receives a digital confirmation from the partner network. Therefore, settlement finality happens in seconds rather than business days.

Step 6: Multi-Currency Ledger Update

The internal ledgering system records every detail of the transaction. Specifically, it posts entries to maintain a perfect balance across all relevant accounts. Furthermore, the platform logs the FX rate and any applicable fees permanently.

This step creates a robust audit trail for the entire enterprise. Consequently, your global financial data remains accurate, synchronized, and easily accessible.

Step 7: Notifications and Transparency

Transparency enhances trust between your business and its global partners. The platform sends automated confirmations to both the sender and the receiver. Status tracking is also available through a secure customer portal or direct API.

Moreover, these updates happen the instant the transaction status changes. Therefore, everyone involved has real-time visibility into the movement of capital.

Step 8: Reconciliation and Reporting

The final stage automates the closing of the financial loop. The system matches internal records against external bank statements to ensure accuracy.

Additionally, it generates detailed reports for both treasury management and regulatory needs. This automation drastically reduces the administrative burden on your finance department. Thus, your team can focus on higher-value strategic growth initiatives.

Automating this eight-step workflow replaces fragmented manual steps with a unified digital standard. This architecture empowers enterprises to move capital as fast as their modern business operations.

Core Engines of a Real-Time Cross-Border Platform

The heart of a real-time cross-border platform resides in its modular engines. These components must work in perfect harmony to ensure transaction finality. Specifically, each engine handles a distinct part of the payment lifecycle autonomously. Furthermore, this decoupling allows for high scalability and easier maintenance.

Therefore, enterprises can upgrade individual parts without disrupting the entire system. Consequently, the architecture remains resilient under heavy global transaction loads. Here are the core engines of a real-time cross-border platform:

1. Multi-Rail Payment Orchestration Layer

The orchestration layer acts as the primary brain of the entire platform. It manages the complex logic of selecting the best payment route. Specifically, this engine evaluates multiple rails based on real-time network conditions. It considers factors such as current fees and estimated delivery times.

Furthermore, the layer remains rail-agnostic to ensure maximum flexibility for the business. Therefore, you can switch providers without rewriting your core integration code.

2. FX Conversion and Liquidity Engine

Global payments require instant access to competitive foreign exchange rates. This engine connects directly to multiple liquidity providers to fetch live pricing. Consequently, it calculates the most favorable conversion for every transaction automatically.

It also manages the internal liquidity pools needed for immediate settlement. Moreover, the system applies custom margins and spreads based on specific client profiles. Thus, you maintain tight control over your global currency exposure.

3. Real-Time Compliance and Sanctions Screening

Regulatory safety depends on high-speed data analysis. This engine uses AI to screen every transaction against international watchlists. Specifically, it performs fuzzy matching to identify potential risks with high accuracy.

Furthermore, it analyzes behavioral patterns to detect sophisticated money laundering attempts. This automated approach significantly reduces the rate of false positives. Therefore, your compliance team focuses only on truly suspicious activities.

4. Settlement and Reconciliation Core

The settlement core ensures that the actual transfer of value is finalized. It moves funds between accounts with atomic precision and digital certainty. In addition, the engine handles the complex task of reconciling internal records.

It matches every outbound payment with its corresponding network confirmation instantly. Consequently, the system identifies any discrepancies before they become financial liabilities. Therefore, your treasury stays balanced across every global currency account.

5. Ledger Architecture for Multi-Currency Flows

A robust ledger is the foundation of institutional financial integrity. This architecture utilizes a double-entry system to track every cent across borders. Specifically, it supports complex multi-currency sub-ledgers for various legal entities.

Furthermore, the records are immutable to prevent unauthorized modifications or data errors. This structure provides a “single source of truth” for your global finance team. Thus, you can generate accurate balance sheets for any jurisdiction at any time.

The integration of these core engines creates a powerful, high-performance financial gateway. This technical foundation allows your enterprise to scale global operations with absolute confidence and speed.

Architecture for Real-Time Processing In Cross-Border Payment Platforms

Building a real-time payment system requires a highly specialized technical blueprint. Specifically, the architecture must handle massive transaction volumes across multiple time zones. Therefore, engineering for speed and reliability is a core requirement for global scale.

To achieve this level of performance, you must focus on several foundational design principles.

1. Event-Driven System Design for Low Latency

Traditional request-response models often create bottlenecks in global payment processing. Instead, modern platforms use event-driven designs to trigger actions asynchronously.

This approach allows different services to communicate without waiting for a previous task to finish.

Consequently, the system can process compliance checks and FX locks simultaneously. Therefore, you achieve the low latency required for instant transaction finality.

2. API-First Infrastructure for Bank Integrations

Connectivity is the lifeblood of a successful cross-border payment ecosystem. Specifically, an API-first approach allows your platform to integrate seamlessly with various global banking partners.

These interfaces provide a standardized way to exchange data across different legacy environments. Furthermore, APIs simplify the onboarding of new payment rails as your business expands. Thus, you build a flexible network that grows alongside your international ambitions.

3. High Availability and Regional Failover

Global finance operates 24/7 without pauses for maintenance or localized outages. Therefore, your architecture must include robust regional failover capabilities to ensure constant uptime.

If a data center in one region fails, traffic shifts to another instantly. This redundancy protects your business from costly downtime during critical trading periods. In addition, it ensures that global payouts remain uninterrupted regardless of local infrastructure issues.

4. Retry Logic in Global Transfers

Network flickers are inevitable when communicating with banks halfway around the world. To prevent double-charging, the system implements strict idempotency keys for every request.

These keys ensure that the same payment is never processed more than once. Furthermore, intelligent retry logic manages temporary connection drops without requiring manual intervention.

Consequently, your financial records remain perfectly accurate even during unstable network conditions.

5. Observability and Transaction Traceability

Total visibility is essential for managing a complex global payment flow. Modern observability tools allow you to track every transaction through its entire lifecycle.

Specifically, you can monitor health metrics and identify potential delays before they impact users. This data helps your team optimize routing and improve overall system performance.

Therefore, you maintain a high standard of service while meeting strict audit requirements.

A well-engineered architecture ensures that your payment platform remains both fast and resilient. This technical foundation allows your organization to handle global capital movements with absolute precision and scale.

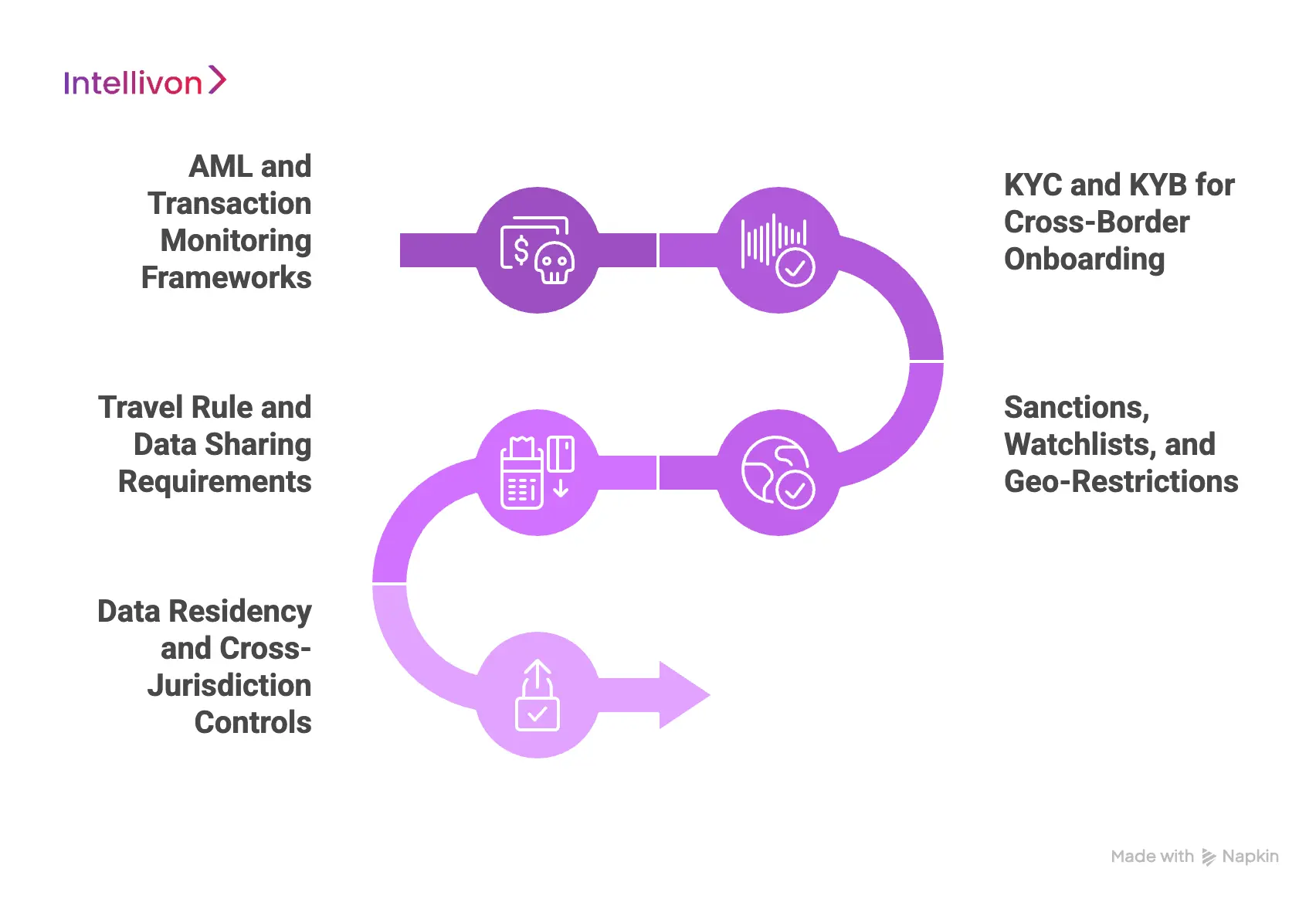

Global Regulations Your Cross-Border Payment Platform Must Support

Navigating the global regulatory landscape is a core challenge for any international payment initiative. Therefore, building trust with global regulators is just as important as the underlying technology itself.

To maintain institutional safety, your platform must integrate several key protective layers within its core architecture.

1. AML and Transaction Monitoring Frameworks

Anti-Money Laundering (AML) controls are the first line of defense against financial crime. Specifically, the system must monitor every transaction for suspicious volume or unusual geographic patterns.

Furthermore, advanced platforms utilize machine learning to identify complex layering techniques that manual reviews might miss. Consequently, this automated vigilance protects your organization from participating in illicit activities.

Therefore, you can maintain a high-velocity payment flow without compromising on security.

2. KYC and KYB for Cross-Border Onboarding

Verifying the identity of both individuals and businesses is a non-negotiable requirement. Know Your Customer (KYC) and Know Your Business (KYB) workflows ensure that you are dealing with legitimate entities.

In addition, these checks must be performed across various jurisdictions with different documentation standards. A modern platform automates this verification to ensure a smooth onboarding experience for global partners.

Thus, you build a verified network of trust before a single cent is ever transferred.

3. Sanctions, Watchlists, and Geo-Restrictions

Sanctions compliance is a dynamic field that requires instant updates to global watchlists. Your platform must screen participants against lists provided by bodies like OFAC, the UN, and the EU.

Specifically, the system should block transactions involving restricted regions or blacklisted individuals in real time. This automated enforcement prevents the severe legal penalties associated with sanctions violations.

Therefore, your business remains safely within the boundaries of international law at all times.

4. Travel Rule and Data Sharing Requirements

The Financial Action Task Force (FATF) Travel Rule requires that certain data accompany every significant transfer. Specifically, the originator and beneficiary information must travel with the payment to its destination.

Furthermore, this data sharing must be handled securely to protect sensitive user information. Consequently, your platform needs a secure messaging layer to facilitate this exchange between financial institutions.

This ensures that you meet the latest global standards for transparency in cross-border value movement.

5. Data Residency and Cross-Jurisdiction Controls

Managing data across borders introduces complex privacy and residency requirements. For instance, laws like the GDPR mandate specific protections for personal information within the European Union.

Your architecture must support data localization to ensure that sensitive records remain within their required jurisdictions. In addition, you must implement strict access controls to prevent unauthorized cross-border data leakage.

Consequently, you maintain the privacy of your users while satisfying the demands of local data authorities.

A rigorous approach to regulatory compliance transforms a potential liability into a significant competitive advantage. This strategic alignment ensures your platform is ready for the scrutiny of even the most demanding global financial institutions.

Designing a Real-Time FX and Liquidity Strategy

Successful global payment platforms rely on a sophisticated liquidity strategy. Therefore, a modern architecture requires a proactive approach to managing your global cash positions.

To build a reliable strategy, you must evaluate how your platform sources and manages its global capital.

1. Pre-Funding vs On-Demand Liquidity Models

Choosing the right funding model is the first step in your liquidity strategy. Specifically, this decision impacts how much capital your business must keep in foreign bank accounts.

- Pre-funding: You hold local currency in target accounts before any transactions occur. This ensures the fastest possible settlement because the funds are already available.

- On-Demand Liquidity: You source the required currency at the exact moment a payment is triggered. This approach frees up capital that would otherwise sit idle in various jurisdictions.

- Strategic Impact: Many modern platforms now utilize a hybrid of these two models. Consequently, you gain the speed of pre-funding alongside the capital efficiency of on-demand sourcing.

2. Managing Currency Volatility in Real Time

Currency values can shift significantly in the seconds it takes to process a transfer. Specifically, your platform must protect both the sender and the business from these sudden market moves.

- Dynamic Rate Locking: The system locks a specific exchange rate for a short execution window. This gives the sender absolute certainty about the final cost of their transfer.

- Automated Hedging: High-value transactions can trigger an automatic hedge to prevent financial loss. This process happens instantly in the background without any manual trade execution.

- Exposure Monitoring: Real-time dashboards track your total currency risk across all global corridors. Therefore, you can adjust your pricing strategy as international markets fluctuate throughout the day.

3. Partnering With Liquidity Providers

You must establish a network of reliable partners to source competitive exchange rates. Specifically, relying on a single provider creates a significant point of failure for your platform.

- Diverse Sourcing: Connecting to several providers forces competition and results in better pricing. Furthermore, it ensures your system remains operational if one partner faces technical issues.

- API Compatibility: Your partners must offer high-speed APIs for instantaneous rate fetching. This level of connectivity is essential for maintaining the “real-time” promise of your service.

- Corridor Reach: Choose partners who have deep expertise in specific regional or emerging markets. Consequently, you can offer more reliable and cost-effective services in difficult-to-reach geographies.

4. Optimizing Spread Without Increasing Risk

Managing the “spread” between buying and selling rates is vital for your platform’s profitability. Specifically, you must balance competitive pricing with the need to cover your own operational costs.

- Tiered Pricing: Apply different margins based on transaction volume or specific client profiles. This flexibility allows you to remain competitive while protecting your overall profit margins.

- Cost-Plus Models: Base your fees on the actual, live cost of the liquidity you source. Furthermore, this level of transparency builds significant long-term trust with your enterprise clients.

- Automated Selection: The platform should always pick the provider with the lowest current spread. Consequently, you capture the most value on every single transaction without increasing your risk.

A sophisticated liquidity strategy ensures your platform remains both profitable and reliable for global users. This strategic balance is critical for maintaining a strong competitive edge in the modern payment market. Intellivon’s experts will strategize this end-to-end to ensure your treasury operations are optimized for maximum capital efficiency.

Security Framework for Real-Time Cross-Border Global Payment Platforms

Protecting a real-time cross-border payment platform requires a multi-layered security strategy that goes beyond standard perimeter defenses.

To maintain institutional integrity, the following security pillars are essential for any high-performance global payment network:

1. Zero-Trust Architecture Principles

A Zero-Trust model operates on the assumption that threats can originate from both inside and outside the network. Specifically, no user or system is granted access to the real-time cross-border payment platform without continuous verification.

- Strict Verification: Every request must be authenticated and authorized based on a dynamic set of variables. This includes evaluating the user’s location, device health, and time of access.

- Least Privilege: Users and services are only granted the minimum level of access required to perform their specific tasks. This limits the “blast radius” in the event of a potential credential compromise.

- Continuous Monitoring: The system assumes a state of breach and constantly scans for anomalous behavior within the environment. Consequently, you maintain a high level of security even as your global network grows in complexity.

2. Tokenization and Encryption Standards

Protecting sensitive financial data is a critical requirement for a secure cross-border payment platform. Specifically, tokenization replaces sensitive data with unique, non-sensitive identifiers to prevent data exposure.

- Data at Rest and Transit: All transaction details must be protected using high-level encryption standards like AES-256 and TLS 1.3. This ensures that even if data is intercepted, it remains unreadable to unauthorized parties.

- Vaultless Tokenization: Modern platforms often use vaultless tokenization to improve system performance and reduce storage risks. This method allows the system to process payments without ever storing the actual account numbers.

- Compliance Alignment: These standards ensure that your architecture remains fully compliant with international mandates like PCI-DSS. Therefore, you reduce the risk of heavy fines and build deeper trust with your global financial partners.

3. Role-Based Access and Audit Logging

Maintaining a clear record of who did what is essential for the accountability of a real-time cross-border payment platform. Specifically, role-based access control (RBAC) ensures that only authorized personnel can access sensitive treasury functions.

- Granular Permissions: Access is granted based on specific job functions, such as compliance officer or system administrator. This prevents unauthorized individuals from triggering high-value international transfers.

- Immutable Logs: Every action taken within the system must be recorded in a permanent, tamper-proof audit trail. Furthermore, these logs should be stored in a separate, secure location to prevent deletion by a malicious actor.

- Audit Readiness: Having detailed logs simplifies the process of satisfying internal audits and external regulatory inquiries. Thus, your organization can demonstrate a high level of operational control to stakeholders and regulators alike.

4. Continuous Risk Monitoring With AI

Legacy fraud detection systems are often too slow to keep up with the speed of a real-time cross-border payment platform. Specifically, AI-driven monitoring tools are now required to identify and block fraudulent transactions as they happen.

- Behavioral Analysis: Machine learning models analyze thousands of data points to establish a “normal” baseline for user behavior. Consequently, any transaction that deviates from this pattern is instantly flagged for review or automatically blocked.

- Real-Time Scoring: Every payment receives a risk score in milliseconds based on factors like transaction size, destination, and velocity. This allows the system to make split-second decisions without introducing latency into the transfer.

- Adaptive Learning: The AI constantly learns from new fraud patterns discovered across the global network. Therefore, your security posture becomes stronger and more effective over time, protecting your enterprise from evolving cyber threats.

Implementing a rigorous security framework ensures that your real-time cross-border payment platform remains a safe environment for global commerce.

This proactive approach is the only way to protect your organization’s reputation and financial assets in a digital-first economy.

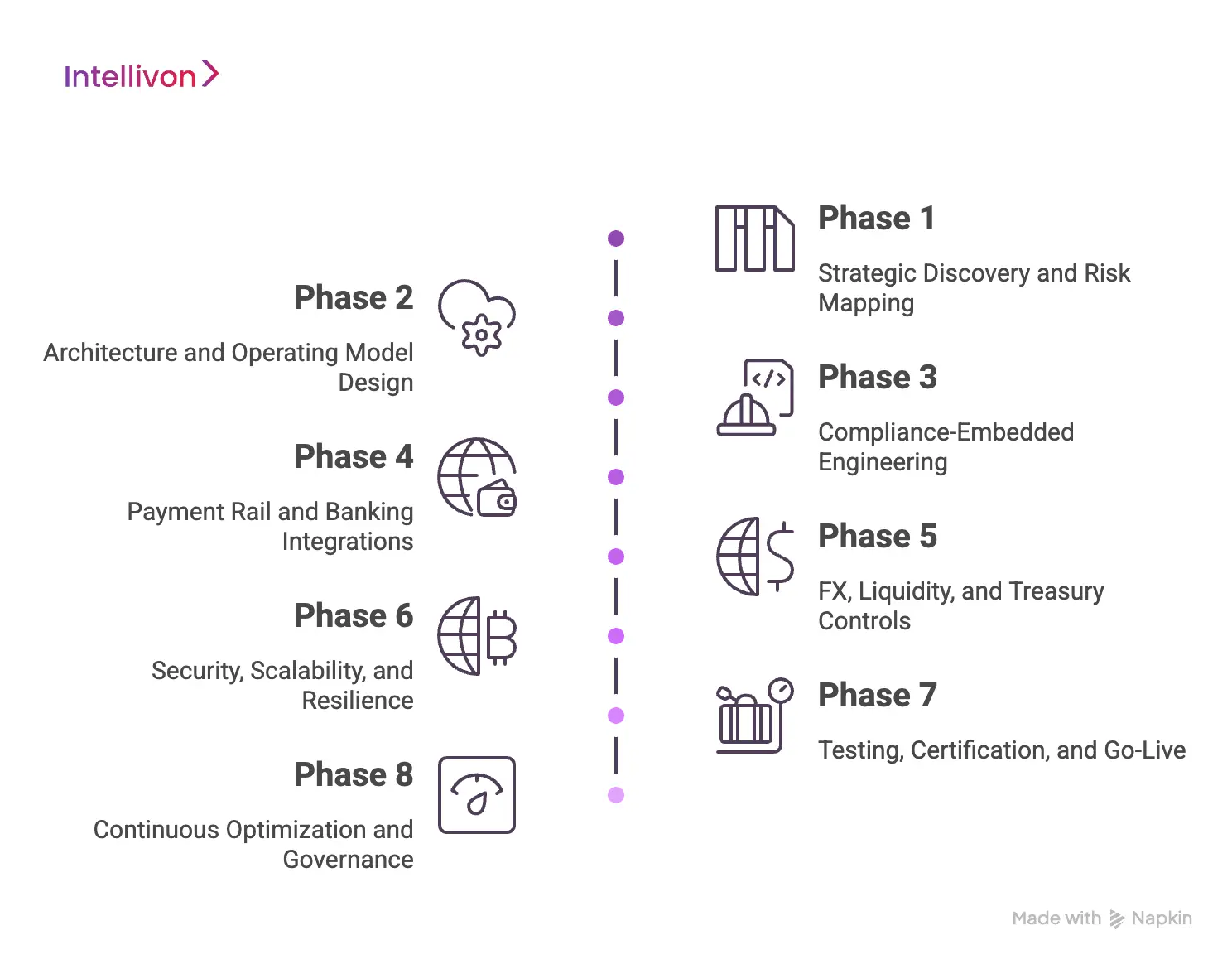

How We Develop A Real-Time Cross-Border Payment Platform

At Intellivon, we approach every real-time cross-border payment platform project with a focus on institutional-grade precision. Specifically, our engineering process balances high-speed performance with the strict safety requirements of global finance. Therefore, we ensure that your gateway is both a technical marvel and a regulatory fortress.

To deliver this level of excellence, our team executes a structured eight-phase roadmap designed for total operational success.

Phase 1: Strategic Discovery and Risk Mapping

The foundation of any global system begins with identifying specific business goals and operational constraints. Specifically, we must map the financial geography your business will serve.

- Corridor Definition: We identify the specific countries and currency pairs you need to support for your global operations.

- Regulatory Mapping: Consequently, we determine the compliance requirements for each jurisdiction, including licensing and data residency laws.

- Liquidity Assessment: Therefore, we evaluate your current treasury capabilities to decide which funding models will best support your transaction volume.

- Risk Profiling: In addition, we document potential exposure points and establish the necessary control requirements to protect your organization.

Phase 2: Architecture and Operating Model Design

With the strategy defined, the Intellivon technical team designs the blueprint for the system. This phase focuses on the logical flow of data and value.

- Orchestration Framework: We design how the system will intelligently route payments across various global networks.

- Ledger Structure: Specifically, we architect a double-entry accounting system that can handle complex multi-currency flows without errors.

- API Strategy: Furthermore, we define the standards for how your platform will communicate with external banks and liquidity providers.

- Governance Controls: Thus, we establish the internal approval workflows required for high-value international transfers.

Phase 3: Compliance-Embedded Engineering

Compliance is never an afterthought in our development process. Instead, it is built directly into the code. This specifically ensures that safety checks do not slow down the speed of settlement.

- Automated Screening: We build the layers responsible for scanning transactions against global sanctions lists in real time.

- Risk-Based Monitoring: Consequently, we configure the AI engines to flag suspicious patterns based on the sender’s specific risk profile.

- Identity Verification: Therefore, we integrate the necessary KYC and KYB workflows to ensure every participant in your network is verified.

- Reporting Automation: Furthermore, we embed the logic required to automatically generate the documents needed by global financial regulators.

Phase 4: Payment Rail and Banking Integrations

This phase involves the physical plumbing of the global gateway. In this phase, we connect your internal systems to the global financial grid.

- Domestic RTP Connections: We integrate with local instant payment systems like FedNow or SEPA to enable “local-speed” transfers.

- Global Rail Connectivity: In addition, we establish secure tunnels to the SWIFT network and other international settlement providers.

- Routing Logic: Consequently, we configure the “cascading” rules that tell the system how to pick the best path for every payment.

- Benchmark Testing: Therefore, we validate the latency and throughput of these connections to ensure they meet your performance standards.

Phase 5: FX, Liquidity, and Treasury Controls

Managing value is the primary function of a real-time cross-border payment platform. Specifically, this phase configures how your organization sources and tracks its global capital.

- Provider Integration: We connect to multiple liquidity providers to ensure you always have access to competitive exchange rates.

- Funding Models: Furthermore, we configure the system to support either pre-funding or on-demand liquidity based on your earlier strategy.

- Visibility Dashboards: Thus, we build the tools that give your treasury team a real-time view of your global cash positions.

- Margin Management: Consequently, we implement the rules for how the system applies spreads and fees to different transaction types.

Phase 6: Security, Scalability, and Resilience

A modern financial system must be indestructible and endlessly scalable. This phase ensures the infrastructure can handle the demands of 24/7 global finance.

- Cloud-Native Infrastructure: We deploy the system using modern cloud tools that allow for instant scaling as your volume grows.

- Failover Protocols: Therefore, we implement regional redundancy so the platform remains online even if a major data center goes dark.

- Data Protection: Furthermore, we configure the encryption and tokenization standards required to keep sensitive financial data safe.

- Stress Testing: Consequently, we conduct rigorous penetration testing to identify and fix any potential security vulnerabilities before launch.

Phase 7: Testing, Certification, and Go-Live

Before processing real money, the infrastructure must prove its reliability. This step involves simulating high-pressure scenarios in a controlled environment.

- Sandbox Testing: We run thousands of test transactions through your payment rails to ensure perfect data integrity.

- Scale Simulations: Thus, we test how the system handles sudden spikes in volume to prevent performance degradation.

- Reconciliation Audit: Therefore, we validate that every cent is accounted for across your internal ledgers and external bank statements.

- Phased Rollout: In addition, we execute a gradual production launch, starting with low-risk corridors before scaling to your entire network.

Phase 8: Continuous Optimization and Governance

The work on a global payment system is never truly finished. Specifically, we must constantly refine the system to improve speed and reduce costs.

- Metric Monitoring: We track the success rates and latency of every payment corridor to identify areas for improvement.

- Routing Refinement: Consequently, we adjust your rail selection logic based on changing network costs or provider performance.

- Margin Optimization: Furthermore, we fine-tune your FX strategies to capture more value as your transaction volume increases.

- Corridor Expansion: Therefore, we scale the platform into new geographies and currencies to support your ongoing global growth.

Our rigorous development path ensures that your organization builds a robust and future-proof gateway. Intellivon’s fintech develoers stands ready to build and scale your international payment capabilities with absolute certainty and technical expertise.

Cost To Build A Real-Time Cross-Border Payment Platform

At Intellivon, real-time cross-border payment platforms are built as regulated financial infrastructure, not as routing layers added to legacy systems. The focus stays on creating environments that operate reliably across currencies, jurisdictions, banking partners, and liquidity corridors. Every architectural decision considers settlement speed, FX exposure, compliance posture, reconciliation integrity, and long-term scalability from day one.

When budget constraints exist, scope can be adjusted with discipline. However, core foundations such as multi-currency ledger design, compliance automation, liquidity orchestration, and failover resilience are never compromised. As a result, enterprises avoid structural rework that typically surfaces after expansion into new corridors. Stability improves, and long-term operating margins remain protected.

Estimated Phase-Wise Cost Breakdown

| Phase | Description | Estimated Cost Range (USD) |

| Regulatory Discovery & Corridor Mapping | Jurisdiction review, licensing scope, payment flow design | $8,000 – $15,000 |

| Architecture & Ledger Design | Multi-currency ledger, settlement logic, audit controls | $15,000 – $30,000 |

| Payment Orchestration Engine | Rail selection logic, routing, cascading rules | $18,000 – $40,000 |

| FX & Liquidity Infrastructure | Rate integration, spread logic, liquidity tracking | $12,000 – $28,000 |

| Compliance & Monitoring Engine | AML screening, sanctions checks, reporting controls | $15,000 – $35,000 |

| Bank & Rail Integrations | RTP systems, SWIFT, and local clearing connectivity | $20,000 – $45,000 |

| Security & Governance Layer | Encryption, access control, and audit logging | $10,000 – $22,000 |

| Reconciliation & Reporting Systems | Automated reconciliation and finance dashboards | $8,000 – $18,000 |

| Testing & Performance Validation | Latency testing, failover simulations | $6,000 – $12,000 |

| Deployment & Optimization | Cloud deployment, monitoring, and scaling setup | $8,000 – $15,000 |

Total initial investment: $120,000 – $260,000

Ongoing maintenance and optimization: 15–20% annually

Costs vary depending on corridor count, compliance exposure, and integration depth.

Hidden Costs Enterprises Should Plan For

Even well-planned cross-border programs can experience budget pressure when indirect drivers are underestimated. Planning early prevents operational friction later.

- Expansion into new jurisdictions increases compliance scope

- Liquidity buffers may require capital allocation

- FX volatility can impact margin strategy

- Bank API limitations may require custom engineering

- Reconciliation complexity grows with transaction volume

- Regulatory reporting standards evolve over time

Because of this, effective cost planning must extend beyond the initial build.

Best Practices To Avoid Budget Overruns

Based on Intellivon’s experience delivering enterprise payment infrastructure, certain patterns consistently improve predictability.

- Define target corridors before selecting rails

- Design ledger logic before building routing layers

- Embed compliance into architecture, not workflows

- Plan liquidity strategy early in system design

- Use modular integrations to reduce rework

- Align treasury operations with payment execution

Enterprises that follow these principles typically avoid expensive infrastructure redesign when transaction scale increases.

Request a tailored proposal from Intellivon’s cross-border infrastructure specialists to receive a delivery roadmap aligned with your corridors, compliance exposure, and long-term global expansion strategy.

Monetization Models for Cross-Border Payment Platforms

Monetization of a real-time cross-border payment platform relies on four pillars: FX spreads, transaction fees, embedded finance, and treasury yield.

By automating spread management and offering high-value financial add-ons, enterprises can achieve significant ROI on their infrastructure investment. Consequently, these models transform the treasury from a cost center into a primary revenue driver.

1. FX Margin Optimization

The spread between the buy and sell rates of a currency represents a significant revenue opportunity. Specifically, the system must automatically capture the best available rates from liquidity providers while applying a strategic margin.

- Dynamic Spreads: The platform adjusts margins in real time based on market volatility and transaction volume. Consequently, you protect your profits during periods of high currency fluctuation.

- Tiered Margins: You can offer tighter spreads for high-volume enterprise clients while maintaining standard margins for retail-level transfers. Furthermore, this flexibility helps you remain competitive in various global corridors.

- Volume Discounts: As your transaction volume increases, your cost of liquidity decreases. Therefore, you can pass some savings to the user while still increasing your overall net margin.

2. Transaction Fee Structuring

Direct fees for processing transfers remain a stable and transparent source of income. Specifically, your fee structure should reflect the speed and complexity of the selected payment rail.

- Fixed vs. Percentage: You can choose between a flat fee for every transaction or a percentage-based model, depending on the target market. In addition, many platforms use a hybrid approach to capture value from both small and large transfers.

- Speed-Based Pricing: Users often pay a premium for “instant” settlement versus standard delivery times. This allows you to monetize the high performance of your real-time rails effectively.

- Transparent Surcharges: Clearly communicate any network or intermediary costs to build long-term trust with your users. Thus, you ensure that fee structures are viewed as fair and predictable.

3. Embedded Financial Services Revenue

Your platform can generate additional income by offering integrated financial products to its users. Specifically, these “embedded” services add significant value to the core payment experience.

- Integrated Lending: Offer short-term working capital loans to businesses based on their transaction history. Consequently, you earn interest income while helping your clients manage their own cash flows.

- Insurance Products: Provide automated insurance for high-value international shipments at the point of payment. Furthermore, this creates a seamless one-stop shop experience for global traders.

- Premium Insights: Monetize advanced data analytics and treasury reporting as a subscription-based service. Therefore, you turn your platform’s data into a recurring revenue stream.

4. Treasury Yield Strategies

Money held within your platform’s ecosystem can also be utilized to generate financial returns. Specifically, your treasury team can manage idle capital to capture interest in safe, liquid markets.

- Interest on Float: Earn interest on funds that are in transit or held in pre-funded local currency accounts. This “float” can represent a significant source of passive income as your transaction volume grows.

- Stablecoin Yields: For platforms utilizing blockchain rails, you can earn yield on digital assets held in treasury. In addition, these strategies must be managed with a strict focus on liquidity and safety.

- Cash Concentration: Automatically move idle balances into high-yield overnight accounts across different jurisdictions. Consequently, you ensure that every dollar in your system is working to improve your bottom line.

A well-rounded monetization strategy ensures that your real-time cross-border payment platform is both a technical success and a financial powerhouse.

By diversifying your income streams, you build a resilient business model capable of sustaining long-term global growth.

Enterprise Examples of Real-Time Cross-Border Platforms

Analyzing established industry leaders reveals the practical application of modern financial architecture. Specifically, these organizations have successfully moved away from legacy constraints to build proprietary global networks. Therefore, studying these models provides a clear blueprint for how to scale a modern international gateway.

Examining these specific implementations highlights the diverse strategies available for achieving global settlement.

1. Wise

Wise has pioneered a global infrastructure that avoids traditional international transfer fees by using a “peer-to-peer” banking model.

Specifically, they maintain a massive network of local accounts across multiple jurisdictions to facilitate internal netting.

- Local Clearing Access: They route payments through domestic systems like ACH or SEPA rather than using the global SWIFT network for every transfer.

- Capital Efficiency: By holding balances in dozens of currencies, they can settle transactions instantly without waiting for a cross-border wire.

- Strategic Impact: This model significantly reduces FX spreads and lowers the dependency on expensive intermediary corridors.

- Infrastructure Takeaway: Combining local account access with intelligent liquidity orchestration is the most effective way to reduce cost and latency.

2. Airwallex

Airwallex has developed a comprehensive payment stack designed specifically for the digital enterprise.

Specifically, they use a unified API layer to abstract the extreme complexity of diverse regional banking systems.

- Unified Connectivity: Their infrastructure allows businesses to access multiple global markets through a single, standardized integration.

- Automated FX: The platform features a real-time engine that handles currency conversion at the moment of payment.

- Treasury Visibility: Enterprises gain embedded visibility into their global cash positions across every entity and region.

- Infrastructure Takeaway: API-led abstraction is the essential foundation for any business seeking rapid international scalability.

3. Payoneer

Payoneer specializes in the infrastructure required for high-volume, multi-party payouts. Their system is designed to handle the unique compliance and ledgering needs of global marketplaces.

- Mass Payout Orchestration: The platform can execute thousands of individual payments to sellers in their local currencies simultaneously.

- Regulatory Onboarding: They have embedded the complex KYC and KYB processes needed to verify participants across disparate regions.

- Financial Integrity: Automated reconciliation tools ensure that every payout is perfectly matched with its corresponding internal record.

- Infrastructure Takeaway: Scalable payout engines must be supported by a highly robust ledger and a deep compliance layer.

4. Stripe

Stripe has transitioned from simple card processing into a full-scale treasury and settlement provider.

The platform allows companies to build and manage their own financial products programmatically.

- Platform-Led Finance: Businesses can offer their own branded banking services to their users through Stripe’s underlying rails.

- Embedded Value: This model integrates financial services—like business lending—directly into the payment flow.

- Real-Time Reporting: Developers can access status updates and financial data through sophisticated, developer-friendly APIs.

- Infrastructure Takeaway: The convergence of payments and treasury management represents the future of enterprise financial models.

5. Ripple

Ripple introduced a specialized model that uses digital assets to solve the problem of idle capital. Specifically, their technology aims to eliminate the need for pre-funded “nostro” accounts in foreign jurisdictions.

- On-Demand Liquidity: By using digital assets as a bridge, value can be moved across borders without holding local currency in advance.

- Reduced Lock-Up: This approach frees up significant amounts of capital that would otherwise be trapped in stagnant bank accounts.

- Network Alternative: It provides a genuine alternative to traditional correspondent banking for institutions seeking high-speed settlement.

- Infrastructure Takeaway: Digital liquidity models can dramatically improve capital efficiency for organizations with high cross-border volume.

What Enterprises Can Learn From These Models

The success of these platforms highlights several critical lessons for any organization building its own international gateway. Specifically, the common thread is the move toward total automation and the elimination of manual intermediaries.

- Local Rail Access: Utilizing domestic systems is the only way to avoid the risks and costs of the legacy SWIFT network.

- Strategic FX Engines: Real-time conversion tools are necessary for maintaining margin control and offering competitive pricing.

- Embedded Compliance: Safety checks must be part of the core code to ensure they never slow down the transaction velocity.

- Modern Ledger Design: The speed of your reconciliation process is directly determined by the quality of your underlying ledger architecture.

These enterprise examples prove that the shift toward real-time global finance is no longer optional. By adopting these proven strategies, your organization can build a platform that turns international payments into a strategic asset.

Conclusion

Adopting a real-time cross-border payment platform transforms the international treasury from a reactive cost center into a strategic growth driver. By integrating multi-rail orchestration with embedded compliance, enterprises eliminate settlement latency and unlock trapped capital.

This transition ensures your organization remains resilient and competitive within the modern global economy. Modernizing your financial infrastructure today provides the agility needed to scale operations across borders with absolute certainty and speed.

Build a Real-Time Cross-Border Platform With Intellivon

Intellivon designs and delivers real-time cross-border payment platforms built as regulated financial infrastructure, not as routing layers added onto legacy systems. By combining multi-rail orchestration, embedded compliance automation, FX intelligence, and resilient ledger architecture, we help enterprises move money globally without compromising speed, control, or regulatory integrity.

The result is a scalable, audit-ready cross-border environment that supports global expansion while protecting margins, liquidity stability, and operational visibility.

Why Partner With Intellivon?

Choosing the right partner to build cross-border infrastructure is a long-term strategic decision. We focus on the core pillars that define enterprise-grade global payment systems.

- Governance-First Architecture: Policy frameworks drive system behavior. As a result, approval workflows, audit controls, and compliance logic are embedded directly into the platform’s operational core.

- Multi-Rail Payment Orchestration: Global payments require flexibility. Therefore, we design intelligent routing engines that dynamically select optimal rails based on cost, speed, geography, and reliability.

- Embedded Compliance Infrastructure: Our systems integrate real-time AML screening, sanctions monitoring, and reporting automation from the architectural layer upward.

- FX and Liquidity Intelligence: Consequently, we build FX rate management and liquidity tracking engines that support margin control and real-time treasury visibility.

- Scalable Multi-Currency Ledger Design: We implement structured ledger systems that maintain financial clarity across currencies, corridors, and entities.

- Resilient Cloud-Native Deployment: High availability, failover readiness, and observability are built into the infrastructure from day one.

- Provider-Agnostic Integrations: Instead of limiting flexibility, we integrate domestic RTP systems, SWIFT networks, and local clearing rails seamlessly.

Book a strategy consultation with Intellivon to design a real-time cross-border payment platform aligned with your corridors, compliance exposure, and long-term international growth objectives.

FAQs

Q1. How long does it take to build a real-time cross-border payment platform?

A1. Timelines depend on corridor scope, compliance exposure, and integration depth.

In most enterprise environments, a production-ready platform takes between 4 and 8 months. Discovery and regulatory mapping typically require the first 4 to 6 weeks. Core infrastructure, rail integrations, and compliance automation follow.

However, expansion into multiple jurisdictions can extend delivery timelines. Therefore, defining corridors early significantly improves speed and predictability.

Q2. What is the average cost of building a cross-border payment platform?

A2. Initial build costs usually range from $120,000 to $260,000 for enterprise-grade infrastructure.

Costs vary based on multi-rail integrations, FX engine complexity, compliance automation, and ledger design requirements. In addition, ongoing maintenance typically represents 15–20% of the initial investment annually.

As a result, the total cost of ownership should always be evaluated beyond launch.

Q3. What technologies are required for real-time cross-border payments?

A3. A real-time platform requires multiple coordinated systems.

These include a multi-currency ledger, payment orchestration engine, FX rate integration, compliance monitoring layer, and banking API connectivity. Additionally, cloud-native infrastructure ensures scalability and failover resilience.

Without this layered architecture, latency increases, and reconciliation becomes difficult at scale.

Q4. How do real-time cross-border platforms manage compliance?

A4. Compliance must operate in real time alongside payment execution.

Platforms typically integrate AML screening, sanctions checks, transaction monitoring, and automated reporting into the transaction flow. Moreover, audit logs and access controls support regulatory transparency.

Embedding compliance into architecture reduces regulatory risk and prevents costly redesign later.

Q5. Should enterprises build or partner for cross-border infrastructure?

A5. The decision depends on internal expertise, licensing readiness, and long-term strategy.

Building in-house provides control but requires deep regulatory and treasury capabilities. On the other hand, partnering with an experienced infrastructure provider accelerates deployment and reduces integration risk.

Therefore, enterprises should evaluate total ownership cost, operational maturity, and expansion plans before deciding.