Key Takeaways

- The core banking software market will reach $35.98 billion by 2035. The stack you build today determines whether you capture that growth or watch others do it.

- Legacy infrastructure actively costs money through reconciliation inefficiencies, manual compliance workflows, and blocked AI adoption.

- Fragmented integration is the real reason most AI initiatives in banking fail before they deliver value.

- Compliance built into the architecture from day one costs significantly less to maintain than compliance retrofitted after launch.

- A hybrid approach outperforms both custom-only and buy-only decisions. It compresses time-to-market without sacrificing the ability to differentiate.

- The technology partner you choose sets the ceiling on your platform’s growth. Architecture decisions made early are expensive to reverse later.

Banking has always relied on heavy infrastructure. What has changed is the cost of getting that infrastructure wrong. Institutions that built on inflexible, large systems are now spending more on maintenance than on innovation. Meanwhile, platforms designed with flexibility and real-time processing at their core are launching new financial products in weeks instead of quarters. The technology choices made at the design level are directly responsible for that difference.

The stack beneath an enterprise banking platform influences product speed, compliance status, integration skills, and ultimately, competitive edge. Every layer, from the core banking engine to the API gateway to the data infrastructure, either drives the business forward or holds it back. For entrepreneurs and investors looking to build or invest in this area, understanding what powers these platforms is essential.

At Intellivon, we build enterprise banking platforms across every layer of the stack, from cloud-native core systems and payment rails to AI infrastructure and compliance tools. This blog explains each of those layers and what they mean for the organizations that build on top of them.

Why Does the Enterprise Banking Tech Stack Matter Today?

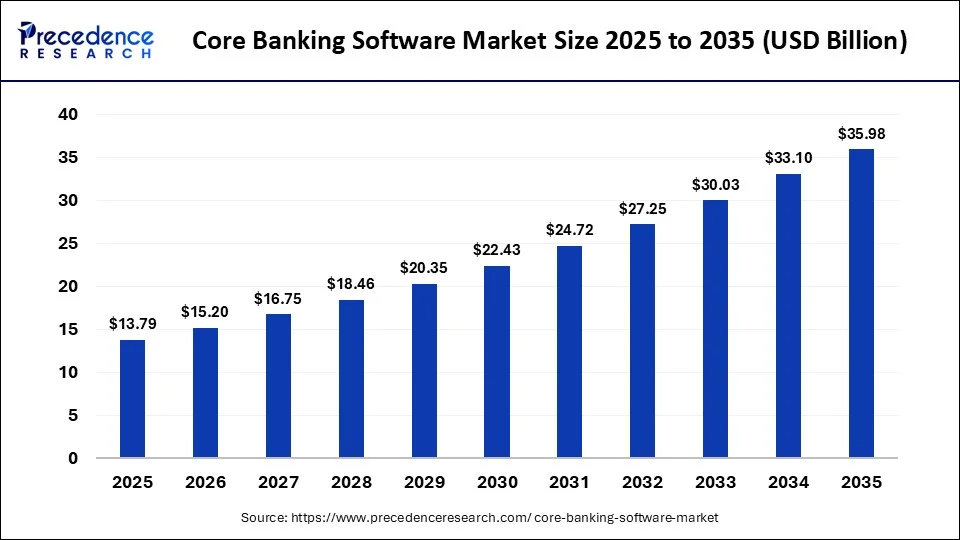

The global core banking software market sits between $14 and $15 billion in 2026, and the pressure driving that number is real. Digital mandates, AI adoption, and customer expectations for real-time service have made the underlying technology stack a direct determinant of business performance.

Institutions running fragmented legacy infrastructure are finding it harder to move quickly, stay compliant, and scale new capabilities. In contrast, platforms built on composable, cloud-native architectures are absorbing that same pressure without breaking stride.

The global core banking software market was valued at $13.79 billion in 2025. By 2026, that figure is expected to reach $15.20 billion, and projections place it at $35.98 billion by 2035, reflecting a compound annual growth rate of 10.07% over that period.

1. Tech Stack Fragmentation Risks

Legacy banking stacks built on monolithic cores and siloed ERPs create costly blind spots. Globally, firms lose an estimated $4.5 billion annually to reconciliation inefficiencies alone.

In 2026, 68% of banks report delayed decision-making due to disconnected data sources, which compounds liquidity risk in volatile rate environments.

2. Real-Time Compliance Pressures

Regulations like ISO 20022 and DORA now require near-instant reporting. However, fragmented stacks push 55% of enterprises into manual compliance workflows, carrying error rates between 12 and 15%.

Modern stacks with integrated API gateways reduce audit times by 40% and enable proactive KYC and AML through embedded RegTech.

3. Customer Experience Demands

Corporate customers expect seamless, omnichannel banking. Outdated infrastructure delivers fragmented portals instead, contributing to 27% abandonment rates in corporate payment flows.

Unified stacks with AI-driven personalization have demonstrated NPS improvements of up to 35 points.

4. Scalability for AI Innovation

Legacy infrastructure actively limits AI adoption. Only 22% of legacy stack users successfully scale generative AI pilots, compared to 78% on cloud-native platforms.

Composable data architectures and edge computing are projected to unlock $1.2 trillion in banking AI value by 2030.

Prioritizing tech stack modernization the linchpin for enterprise banks to thrive in 2026’s volatile landscape. Banks embracing cloud-native, API-first architectures gain a first-mover advantage in AI-driven services and regulatory resilience.

What Is an Enterprise Banking Tech Stack?

An enterprise banking tech stack is a multi-layered architectural foundation integrating core banking engines, middleware, and secure data pipelines. Beyond simple interfaces, it orchestrates real-time transaction processing, regulatory compliance automation, and distributed ledger synchronization.

At the same time, it serves as the resilient backbone enabling high-concurrency financial operations while ensuring absolute data integrity and institutional security.

A robust stack bridges the gap between legacy stability and modern innovation. For instance, the core layer manages the ledger while the integration layer connects to third-party fintech ecosystems.

This modularity allows your platform to evolve without requiring a total system overhaul. However, achieving this balance requires deep technical foresight and an understanding of global financial rails.

- Core Banking Engine: The central nervous system for ledger management and transactions.

- Middleware & APIs: The connective tissue for third-party integrations and service orchestration.

- Infrastructure Layer: Cloud-native environments ensuring 99.99% uptime and disaster recovery.

- Security & Compliance: Hardened layers for encryption, KYC, and AML monitoring.

Successful platforms treat security as a foundational element rather than a secondary feature. You must ensure that every component in the stack communicates through encrypted channels.

Furthermore, the use of containerization and automated DevOps pipelines ensures that updates occur without service interruptions. These strategic choices define whether your platform survives the rigors of the modern financial landscape.

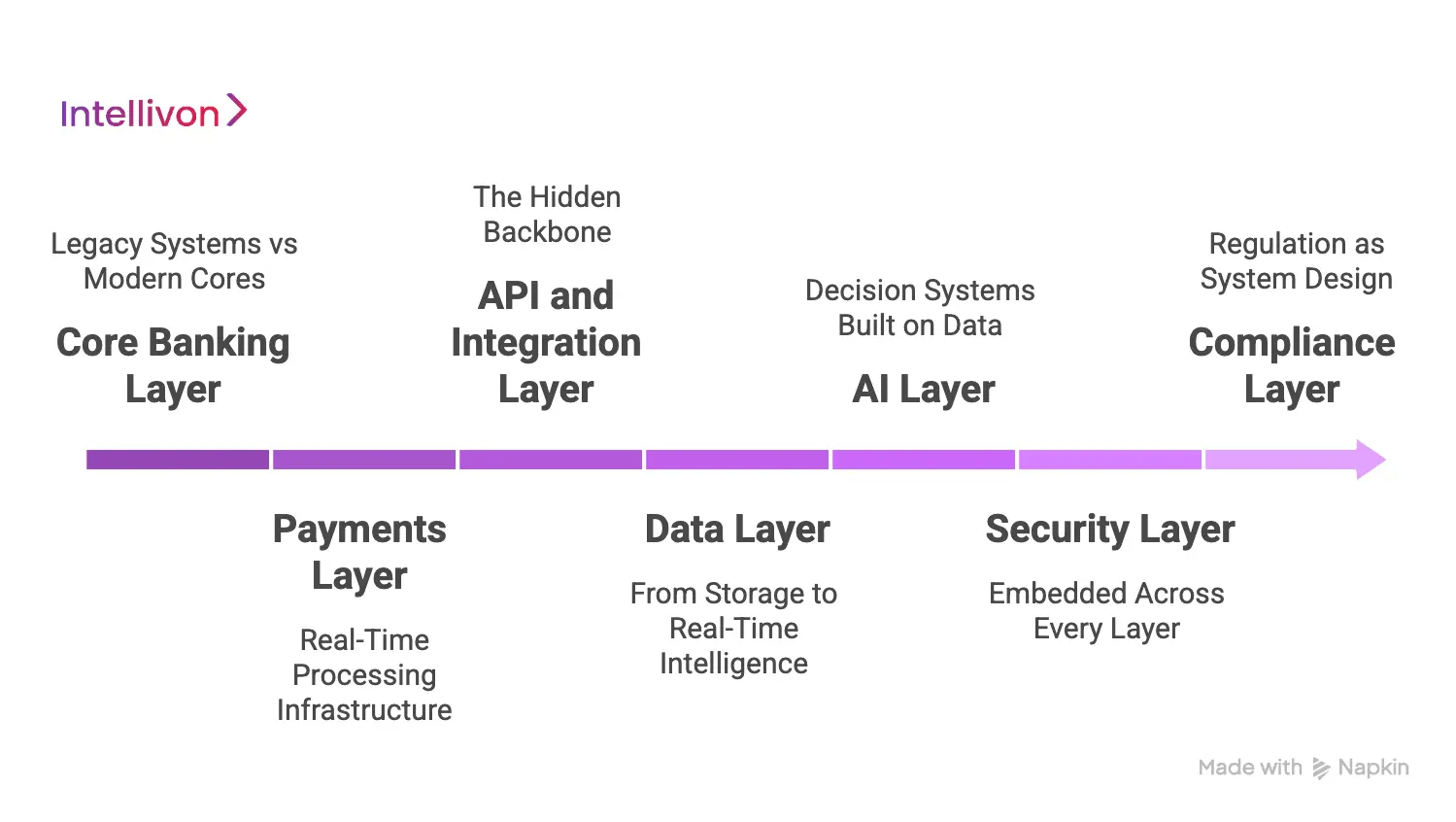

What Are the Core Layers of a Banking Tech Stack?

A high-performance banking architecture depends on a modular framework where every component serves a specific strategic purpose.

This structured approach ensures your platform can handle extreme transaction volumes while maintaining the agility required to launch new financial products.

1. Core Banking Layer: Legacy Systems vs Modern Cores

The core layer acts as the primary source of truth for all ledger balances and account data.

A. Modernization Pressure

Traditional institutions often rely on COBOL-based mainframes that lack the agility for modern digital demands. These legacy systems create significant technical debt and slow down the deployment of new financial products.

B. Modular Core Advantages

In contrast, modern modular cores utilize cloud-native microservices to allow for rapid iteration. This architecture enables developers to update specific features without risking the stability of the entire ledger system.

2. Payments Layer: Real-Time Processing Infrastructure

Global commerce now operates on a 24/7 cycle, necessitating infrastructure that supports instant settlements and high throughput.

A. High-Volume Settlement Engines

Modern platforms must interface directly with Real-Time Payment (RTP) networks and global card networks. Therefore, your payment engine must handle thousands of concurrent transactions per second without latency.

B. Concurrency Management

Properly managing concurrency ensures that double-spending or synchronization errors never occur. As a result, robust locking mechanisms and distributed transaction protocols are essential for maintaining financial accuracy at scale.

3. API and Integration Layer: The Hidden Backbone

This layer facilitates communication between internal services and external fintech ecosystems through structured gateways.

A. Orchestration and Gateways

Efficient middleware manages the flow of data between disparate systems like KYC providers and credit bureaus. Consequently, the orchestration layer must be resilient enough to handle third-party downtime gracefully.

B. Avoiding Integration Failures

Integrations often fail at scale due to poor rate limiting or incompatible data formats. However, utilizing standardized RESTful or gRPC interfaces helps maintain a predictable and reliable integration environment.

4. Data Layer: From Storage to Real-Time Intelligence

Data is the most valuable asset in banking, but only if it remains accessible and actionable in real-time.

A. Streaming Pipelines

Moving beyond static data warehouses, modern stacks utilize streaming pipelines like Kafka for real-time event processing. This allows the system to react to user behavior or market shifts instantly.

B. Data Availability

If data becomes a bottleneck, the entire user experience suffers. In addition, ensuring high availability through distributed databases prevents system-wide outages during peak traffic periods.

5. AI Layer: Decision Systems Built on Data

Artificial Intelligence provides the competitive edge needed for automated risk assessment and customer personalization.

A. Automated Fraud Detection

AI models analyze transaction patterns to identify anomalies before they result in financial loss. Therefore, these systems require low-latency access to historical data to make split-second decisions.

B. Pipeline Dependency

The effectiveness of any AI model depends entirely on the cleanliness of the data pipelines. Strategic investors must prioritize data hygiene to ensure that scoring models remain accurate and unbiased.

6. Security Layer: Embedded Across Every Layer

Security is not a perimeter fence but a continuous thread woven into every software component.

A. Zero-Trust Principles

Adopting zero-trust means the system never assumes a request is safe, even if it originates internally. Every interaction requires explicit authentication and authorization to minimize the blast radius of potential threats.

B. Continuous Monitoring

Encryption and identity management must be supplemented by real-time monitoring tools. These systems detect unauthorized access attempts and provide the forensic trail necessary for incident response.

7. Compliance Layer: Regulation as System Design

Regulatory requirements should be treated as functional specifications rather than afterthoughts.

A. Auditable Architectures

Standards like PCI DSS and GDPR require specific data handling procedures that must be baked into the code. This approach reduces the cost of audits and minimizes legal exposure.

B. Reporting Systems

Automated reporting tools ensure that your platform remains compliant across different jurisdictions. By automating these workflows, you allow your team to focus on innovation rather than manual paperwork.

Building a platform with these clearly defined layers ensures operational excellence and investor confidence. This structured approach transforms complex technical requirements into a scalable business engine ready for global expansion.

What Tech Stack Is Required for a Secure Banking Platform?

Selecting a technology stack is a high-stakes decision that impacts your platform’s security posture and its ability to scale under pressure.

This section outlines the specific tools and programming languages that have become the industry standard for building resilient financial systems.

1. Programming Languages: Java vs. Go vs. Rust

The choice of language dictates how efficiently your system handles concurrent transactions and manages memory safety. Each of these languages offers distinct advantages for specific parts of the banking ecosystem.

| Language | Primary Use Case | Strategic Advantage |

| Java (Spring Boot) | Core Banking / Back-office | Massive ecosystem, deep talent pool, and enterprise-grade libraries. |

| Go (Golang) | High-frequency Microservices | Superior concurrency handling and extremely fast execution speeds. |

| Rust | Security-Critical Modules | Memory safety without a garbage collector eliminates many common vulnerabilities. |

2. Database Architectures: SQL vs. NoSQL vs. NewSQL

Financial data requires a balance between the strict consistency of traditional databases and the massive scalability of modern distributed systems.

| Database Type | Example | Best For |

| Relational (SQL) | PostgreSQL | Ledger management where ACID compliance and data integrity are non-negotiable. |

| Non-Relational | MongoDB / Cassandra | User profiles, session data, and unstructured logging at high volumes. |

| NewSQL | CockroachDB | Distributed systems that require global consistency across multiple cloud regions. |

3. Infrastructure and Orchestration Tools

To maintain the high availability that enterprise banking demands, the infrastructure must be automated, self-healing, and easily replicated across different environments.

| Tool | Function | Business Impact |

| Kubernetes | Container Orchestration | Ensures 99.99% uptime by automatically managing service health and scaling. |

| Terraform | Infrastructure as Code | Allows for the rapid, error-free deployment of entire environments via scripts. |

| Kafka | Event Streaming | Powers real-time fraud detection by processing millions of events per second. |

Investing in these battle-tested technologies ensures that your platform is built on a foundation of reliability and security. By aligning your technical choices with these industry standards, you reduce operational risk and create a system that can evolve alongside the global financial market.

How Does a Banking Tech Stack Handle Real-Time Scale?

A banking platform tech stack must operate flawlessly whether ten people or ten million are logged in simultaneously. In the financial sector, scaling refers to the ability of the banking platform tech stack to manage massive activity bursts without experiencing crashes or performance lag.

1. Handling Peak Loads Across Payment Cycles

Financial movement occurs in waves rather than a steady stream. A high-performance banking platform tech stack remains elastic, expanding during busy periods and shrinking during quiet hours to optimize operational costs.

A. Payroll Spikes and Trading Windows

During monthly payroll cycles or significant market events, a system may experience a 1,000% increase in traffic within seconds.

Therefore, a sophisticated stack employs auto-scaling to provision digital resources automatically before users experience any latency. This prevents the friction that leads to customer frustration and diminished institutional trust.

B. Managing Resource Contention

High traffic volumes can lead to digital clogs where processes compete for the same resources. However, by isolating essential tasks, like fund transfers, from secondary tasks, like profile updates, the core business remains fluid. Consequently, the primary transaction engine stays fast even while background services manage a backlog.

| Event | Impact on System | The Business Strategy |

| Payday Waves | Massive rush of transfers. | System automatically scales server capacity. |

| Market Rush | High-concurrency balance checks. | Uses fast-access memory to show data instantly. |

| Holiday Sales | Persistent high-volume shopping. | Distributes workload across multiple data regions. |

2. Containerization and Orchestration in Banking

Containers act as standardized shipping units for software code. They ensure that a banking platform tech stack functions identically whether it is on a local testing machine or a massive global production server.

A. The Role of Kubernetes

Kubernetes functions as an automated foreman for digital infrastructure. It monitors software health 24/7 and replaces any failing part of the application instantly without manual intervention.

Furthermore, it supports blue-green deployments, allowing new features to be tested on small user groups before a full-scale rollout.

B. Orchestration Alternatives

While Kubernetes is the industry standard, managed versions exist that require less internal engineering overhead. These tools provide transparent dashboards for monitoring system health in real-time.

As a result, business leaders can make decisions based on actual performance data rather than technical guesswork.

| Tooling | Business Value | Operational Impact |

| Containers | Unified code packaging. | Faster updates and fewer bugs in production. |

| Kubernetes | Automated system management. | Keeps the platform online if a server fails. |

| Service Mesh | Internal traffic tracking. | Simplifies the process of finding hidden errors. |

3. Designing Always-On, Fault-Tolerant Systems

In the financial world, five minutes of downtime can result in massive revenue loss and regulatory penalties. A fault-tolerant banking platform tech stack is designed on the principle that hardware or software will eventually fail, necessitating a Plan B that activates in milliseconds.

A. Multi-Region and Redundancy

A strategic architecture is geographically distributed across multiple cities or countries. If a disaster affects a data center in one region, users are rerouted to a healthy center instantly.

In addition, transaction data is synchronized in real-time to ensure that no financial records are ever lost during a transition.

B. Failover Mechanisms

If a secondary feature, like a notification service, breaks, it should not hinder the ability of users to move money. This is known as graceful degradation.

By building the banking platform tech stack this way, core revenue is protected during technical incidents. This approach ensures the brand remains a symbol of institutional reliability.

| Resilience Strategy | Functional Purpose | ROI Benefit |

| Active-Active | Two engines running at once. | Zero downtime for the end user. |

| Circuit Breakers | Stops small errors from spreading. | Protects the main service during a crisis. |

| Self-Healing | System fixes itself. | Reduces the need for 24/7 manual support. |

Scale provides the foundation for growth. When a banking platform tech stack is built to handle millions of users effortlessly, the focus can shift from technical troubleshooting to market expansion. Investing in a self-healing architecture is the most reliable way to secure long-term institutional value.

What Is the Biggest Integration Problem in Banking Systems?

The most significant challenge in any banking platform tech stack is not building new features, but ensuring those features can talk to each other. When systems are isolated, the business suffers from delayed data, manual reconciliations, and a high risk of operational error.

1. Fragmented Systems and Data Silos

In most financial architectures, data is often trapped within specific departments or legacy modules. For instance, the credit scoring system might not have immediate access to the latest transaction data from the core ledger.

A. The Cost of Isolation

Silos create a disjointed view of the customer, leading to poor risk assessment and missed cross-selling opportunities. Consequently, the banking platform tech stack becomes a collection of independent islands rather than a unified engine.

This fragmentation requires expensive middleware to bridge the gaps, which often adds more complexity than it solves.

B. Operational Friction

When data must be manually moved or batch-processed between systems, real-time banking becomes impossible. Therefore, decision-makers face a choice: continue patching old silos or invest in a unified data architecture.

A modern approach ensures that every part of the stack sees the same truth at the same time.

| Problem | Business Impact | Technical Root Cause |

| Data Latency | Slow loan approvals. | Reliance on nightly batch processing. |

| Inconsistency | Incorrect balance displays. | Lack of a single source of truth. |

| Manual Work | High operational overhead. | Systems that cannot communicate via APIs. |

2. Why Integration Failures Block AI Adoption

AI is only as effective as the data it can access. If the banking platform tech stack is fragmented, the AI layer remains starved of the real-time context it needs to perform.

A. The AI Data Gap

Most AI models fail in banking because they are fed stale or incomplete data. For example, a fraud detection model cannot stop a suspicious transfer if it receives the transaction data ten minutes too late.

However, when integration is seamless, the AI can analyze patterns as they happen, providing a proactive shield for the institution.

B. Scaling Intelligence

To scale AI across the enterprise, the integration layer must support high-speed data streaming. Without this, AI remains a series of expensive experiments rather than a core business driver.

Strategic investors must prioritize a fluid integration layer to ensure their AI investments actually deliver a return on equity.

3. Modern Integration Patterns That Actually Work

To solve the integration crisis, leaders are moving away from rigid, point-to-point connections in favor of flexible, event-driven designs.

A. Event-Driven Architecture

An event-driven banking platform tech stack treats every action, like a deposit or a password change, as an event that is broadcast to the entire system.

Instead of one service asking another for data, services simply listen for relevant events. This decoupling allows the platform to be incredibly fast and highly modular.

B. Unified Orchestration Layers

A unified orchestration layer acts as a central brain that coordinates how different services interact. By using standardized API gateways and service meshes, the platform ensures that all internal and external integrations follow the same security and performance rules. As a result, adding a new partner or a new feature becomes a matter of days rather than months.

| Pattern | How it Works | Why it Wins |

| Event-Driven | Systems react to real-time triggers. | Absolute speed and modularity. |

| API-First | Everything is built as a pluggable service. | Easy to partner with other fintechs. |

| Service Mesh | Centralized control of all connections. | Hardened security and deep visibility. |

Solving the integration problem is the key to unlocking the full potential of a banking platform tech stack. By moving toward an event-driven, API-first model, an enterprise can finally achieve the agility required to lead in a data-driven market.

How Is AI Changing the Enterprise Banking Tech Stack?

Traditional banking systems were designed to record transactions, but modern stacks are designed to understand them. By embedding AI directly into the core layers, institutions can move from reactive processing to proactive financial management.

1. Real AI Use Cases in Banking Platforms

AI delivers measurable value by automating complex cognitive tasks that previously required manual intervention or rigid, rule-based logic.

A. Fraud and Risk Mitigation

AI models analyze thousands of data points in milliseconds to identify suspicious patterns that a human would likely miss. For instance, a banking platform tech stack can compare a current transaction against a customer’s multi-year history, location data, and global fraud trends simultaneously.

This reduces false positives, ensuring that legitimate customers are not inconvenienced while criminal activity is blocked instantly.

B. Hyper-Personalization at Scale

Beyond security, AI enables a level of personalization that mirrors a private banker for every user. By analyzing spending habits and cash flow patterns, the system can offer timely advice, such as identifying an upcoming bill that might cause an overdraft.

Consequently, the platform moves from being a static utility to a proactive financial partner, increasing customer lifetime value and engagement.

| Use Case | AI Application | Business Result |

| Fraud Detection | Real-time anomaly detection. | Reduced loss from unauthorized transactions. |

| Credit Scoring | Alternative data point analysis. | Faster loan approvals and lower default rates. |

| Personalization | Predictive cash flow modeling. | Higher adoption of secondary financial products. |

2. Limits of Legacy Systems for AI Workloads

Many legacy systems fail to support AI because they were built for batch processing rather than real-time data streaming. An outdated banking platform tech stack often treats data as a historical record rather than a live asset.

A. The Latency Bottleneck

Legacy databases often lock up during heavy read/write cycles, causing a delay in the data available to AI models. If an AI system receives information that is even a few seconds old, its ability to stop fraud or offer real-time advice is compromised.

Therefore, a modern stack must utilize high-speed data pipelines to feed the AI layer without interruption.

B. Rigid Data Structures

Older systems often store data in non-standard formats that require extensive cleaning before an AI can use it. This creates a data tax where a significant portion of the budget is spent on preparation rather than innovation.

However, a cloud-native banking platform tech stack uses standardized data lakes, ensuring that intelligence can be applied across the entire enterprise effortlessly.

3. Building AI Systems Without Compliance Risk

For enterprise leaders, the primary fear regarding AI is that a system makes a decision but cannot explain why. In a highly regulated industry, this lack of transparency is a major legal liability.

A. Explainability and RAG

To mitigate risk, a banking platform tech stack should incorporate Retrieval-Augmented Generation (RAG). This technology ensures that AI-driven responses or decisions are grounded in the institution’s own verified data and regulatory manuals.

By providing a clear audit trail of how a conclusion was reached, the system meets the high bars set by compliance officers and regulators.

B. Human-in-the-Loop Oversight

Strategic AI implementation always includes a human oversight layer for high-impact decisions. For example, while AI can flag a loan for approval, a human officer might provide the final sign-off for large enterprise credits.

This balanced approach uses technology to do the heavy lifting while maintaining the accountability required for institutional stability.

4. Emerging Role of Agentic AI in Banking

The next evolution of the banking platform tech stack is the shift from “Chatbot AI” to “Agentic AI.” Unlike simple assistants that answer questions, agentic systems are designed to complete complex, multi-step financial workflows autonomously.

A. Autonomous Financial Operations

Agentic AI can act as an invisible employee within the banking platform tech stack. For instance, an agent could monitor a corporate client’s fluctuating currency exposure and automatically execute a hedge based on pre-approved risk parameters.

It navigates the internal systems to solve it. This level of autonomy requires deep integration between the AI layer and the core execution engines.

B. Orchestrating Complex Workflows

In a typical banking environment, a single task like “onboarding a new corporate entity” involves KYC checks, document verification, and ledger setup across multiple systems.

Agentic AI can orchestrate this entire process, communicating with various APIs and resolving minor discrepancies without human help. As a result, operational costs drop significantly, and the speed of business increases.

This transformation turns the tech stack into a self-optimizing engine that grows more efficient with every transaction it processes.

| Agentic Feature | Description | Strategic Advantage |

| Workflow Autonomy | Executes multi-step financial tasks. | Drastically lower back-office headcount costs. |

| Self-Correction | Identifies and fixes data errors in-stream. | Higher data integrity and lower audit risk. |

| Predictive Execution | Moves funds based on predicted needs. | Optimized liquidity and capital efficiency. |

The move toward an intelligent banking platform tech stack is not just a technical upgrade; it is a fundamental shift in how value is created. By leveraging agentic systems and transparent AI, founders can build a platform that is not only faster but also significantly smarter than the competition.

How Do Neobanks Design Their Banking Tech Stack?

Neobanks represent the ultimate case study in how a modern banking platform tech stack can disrupt an entire industry. By discarding the physical and technical baggage of the past, these institutions have created a blueprint for financial agility that traditional banks are now racing to emulate.

1. Modular, API-First Architecture

The cornerstone of a neobank is the refusal to build everything in-house. Instead, they utilize a composable banking model where specialized third-party services are plugged into a central core via APIs.

A. The Composable Advantage

In this model, the banking platform tech stack acts as a sophisticated orchestrator. For example, a neobank might use one partner for card issuing, another for global currency exchange, and a third for identity verification.

This modularity means that if a better provider emerges, the neobank can swap them out without rebuilding its entire platform. Consequently, they can launch new features in weeks that would take a traditional bank years to develop.

B. API as the Product

For a neobank, the API is the fundamental foundation of the business. By adopting an API-first mindset, every internal function is built to be consumed by other services.

This creates a highly flexible environment where data flows freely between the mobile app, the ledger, and the analytics engine. Therefore, the institution can maintain a lean engineering team while delivering a broad range of high-end financial services.

| Component | Neobank Approach | Business Impact |

| Core Ledger | Cloud-native, real-time microservices. | Instant balance updates and 24/7 availability. |

| Integrations | Plug-and-play third-party APIs. | Rapid market entry and low R&D costs. |

| Front-End | Mobile-first, thin-client design. | Superior UX and high customer retention. |

2. Speed vs Stability Trade-Offs

The primary challenge for any neobank is balancing the need for rapid innovation with the absolute requirement for institutional stability. In the financial world, moving fast and breaking things is not a viable strategy when dealing with customer capital.

A. Agility with Stability

Neobanks solve this by using a high degree of automation within their banking platform tech stack. They utilize automated testing and deployment pipelines that catch errors before they reach the customer.

However, the trade-off is often technical complexity. Managing a web of hundreds of microservices requires a top-tier DevOps culture. As a result, while the neobank can move faster than a legacy competitor, it must invest heavily in observability tools to ensure the system remains stable under pressure.

B. Risk Management in High-Speed Environments

Stability in a neobank is achieved through isolation. If the rewards points service experiences a bug, it is architecturally prevented from affecting the fund transfer service.

This failure isolation allows the team to fix problems in real-time without taking the entire platform offline.

This strategic design ensures that even during rapid updates, the core promise of the bank is never compromised.

| Aspect | The Speed Priority | The Stability Requirement |

| Updates | Daily or weekly feature releases. | Rigorous automated compliance checks. |

| Infrastructure | Elastic scaling for viral growth. | Multi-region backups for disaster recovery. |

| Third-Parties | Fast integration of new fintech tools. | Deep due diligence on partner uptime and security. |

Designing a banking platform tech stack like a neobank requires a shift from owning infrastructure to orchestrating services. This approach allows an enterprise to remain agile, cost-effective, and ready to scale globally from day one. By prioritizing modularity, you ensure your platform can evolve as fast as the market demands.

Should You Build or Buy an Enterprise Banking Tech Stack?

A modern banking platform tech stack can be approached as a custom-engineered masterpiece or a high-performance utility. Understanding the strategic trade-offs between these paths is essential for maximizing ROI and minimizing time-to-market.

1. Custom Build: Control and Differentiation

Building a bespoke banking platform tech stack allows an enterprise to own its intellectual property entirely. This path is favored by organizations looking to introduce a unique financial product that off-the-shelf software cannot support.

A. Absolute Technical Sovereignty

With a custom build, every line of code is optimized for your specific business logic. There are no hidden limitations imposed by a third-party vendor’s roadmap.

However, this requires a significant upfront investment in engineering talent and a longer development cycle.

The primary advantage is the ability to pivot instantly as market conditions change, ensuring your platform always stays ahead of standardized competitors.

B. Tailored Security and Performance

Custom architectures allow for hardened security protocols specifically designed for your risk profile.

Therefore, you can optimize the data flow for the exact transaction types your users perform most.

Consequently, while the initial cost is higher, the long-term value of owning the underlying technology can lead to a much higher company valuation.

2. Platform Approach: Speed and Compliance

Buying a pre-built “bank-in-a-box” solution is the fastest way to enter the market. These platforms come with built-in regulatory frameworks and battle-tested engines that have already been audited.

A. Rapid Market Entry

A purchased banking platform tech stack allows you to launch in months rather than years. The vendor handles the complex maintenance and compliance updates, allowing your team to focus on marketing and customer acquisition.

However, the trade-off is a lack of differentiation. If you and your competitors use the same underlying engine, your only way to compete is through branding or price.

B. Vendor Dependency

When you buy a platform, you are tied to the vendor’s ecosystem. If their system goes down or they fall behind on innovation, your business suffers.

In addition, scaling costs can become unpredictable as seat licenses or transaction fees grow alongside your user base. While it is a safe starting point, it can eventually become a bottleneck for a truly ambitious enterprise.

3. Hybrid Models Used by Enterprises

The most successful global platforms increasingly utilize a hybrid approach. This strategy involves buying the non-differentiating “commodity” parts of the stack while building custom, proprietary layers for the features that actually drive revenue and user loyalty.

A. The Best of Both Worlds

In a hybrid banking platform tech stack, you might use a reliable third-party engine for basic ledger functions but build a custom, AI-driven orchestration layer on top of it.

This allows for rapid scaling without sacrificing the ability to innovate. It provides the compliance safety of a proven platform with the competitive edge of custom software.

| Strategic Factor | Custom Build | Platform (Buy) | Hybrid Model (Recommended) |

| Time to Market | Slow (12-24 months) | Very Fast (3-6 months) | Balanced (6-9 months) |

| Initial Cost | Very High | Moderate/Subscription | Strategic Allocation |

| Differentiation | Absolute | Low/Generic | High (on key features) |

| Compliance Risk | High (Internal) | Low (Vendor Managed) | Shared/Controlled |

| Long-term ROI | Maximum (IP Ownership) | Capped by Fees | High (Efficiency + IP) |

B. Why Hybrid with Custom Tech Wins

Ultimately, the hybrid model where you build your own proprietary “brain” on top of specialized infrastructure is the superior choice for serious investors.

It ensures that your core value proposition is unique while the “plumbing” remains standard and reliable. This approach minimizes risk while maximizing the potential for market disruption.

| Feature | Buy Only | Build Only | The Hybrid Advantage |

| Scalability | Limited by Vendor | Highly Complex | Elastic and Managed |

| Innovation | Wait for Roadmap | Total Freedom | Focused Innovation |

| Maintenance | Included | High Internal Effort | Optimized for Core Systems |

Choosing the right path in your banking platform tech stack journey is about balancing immediate needs with future growth.

By adopting a hybrid strategy that prioritizes custom development for your most valuable features, you create a resilient, scalable, and highly valuable financial institution.

What Is the Total Cost of an Enterprise Banking Tech Stack?

The cost of building a banking tech stack varies widely based on scope, integrations, and regulatory requirements.

For early-stage platforms or focused builds, the investment can start relatively lean. However, as complexity increases across payments, compliance, and scale, costs rise accordingly.

Cost Ranges Based on Platform Scope

Below is a realistic breakdown for lean to mid-scale banking tech stack builds:

| Platform Scope | Timeline | Investment Range |

| Prototype / MVP Layer (basic APIs + UI + limited flows) | 2–4 months | $10,000 – $25,000 |

| Functional MVP Platform (accounts, payments, integrations) | 4–7 months | $25,000 – $50,000 |

| Mid-Level Platform (multi-module + compliance-ready base) | 6–10 months | $50,000 – $80,000 |

Note: These ranges typically apply to non-regulated builds, internal tools, or early-stage fintech products. Enterprise-grade banking systems scale significantly beyond this.

Key Cost Drivers Across the Stack

Even within this range, costs are driven by architectural decisions:

- Integration Depth

- Number of APIs (banking, KYC, payments)

- Third-party dependencies

- Legacy system connections

- Payments Functionality

- Basic transfers vs multi-rail support

- Settlement and reconciliation logic

- Compliance Readiness

- KYC/AML workflows

- Data protection requirements

- Audit logging systems

- Data and Backend Complexity

- Real-time vs batch processing

- Data storage and pipelines

- Infrastructure Setup

- Cloud configuration

- Scalability and uptime requirements

Even in smaller builds, integration and compliance quickly become the largest cost drivers.

Five-Year Total Cost of Ownership

For platforms built in this range, long-term costs are often underestimated.

A typical breakdown looks like:

- Initial Development: 50–60%

- Maintenance & Iterations: 15–20%

- Infrastructure Costs: 10–15%

- Security & Compliance Updates: 10–15%

As the platform scales, additional investments are required to support:

- higher transaction volumes

- regulatory expansion

- system reliability

Most teams eventually reinvest to evolve this into a full-scale enterprise architecture.

Get a Clear Cost Breakdown for Your Platform

If you’re planning to build a banking platform, the right approach is to define what layer you’re building first.

At Intellivon, we help you map:

- architecture

- integrations

- compliance scope

before giving a realistic cost range.

Speak with our experts to get a tailored estimate based on your product scope and growth roadmap.

What Does Progressive Modernization Look Like in Banking?

Progressive modernization is the strategic alternative to risky, all-at-once migrations. It allows an enterprise to upgrade its banking platform tech stack incrementally, ensuring that the institution remains operational while moving toward a more agile, cloud-native future.

Modernization is no longer a choice between staying stagnant or risking a catastrophic failure. By using a phased approach, leaders can replace aging components of the banking platform tech stack while the business continues to generate revenue and serve customers.

1. Modernizing Without System Downtime

Modern engineering patterns allow for the “hot-swapping” of services while the system is live.

A. The Strangler Fig Pattern

This strategy involves building new functional modules around the edges of the legacy core. Over time, the new services “strangle” the old ones by taking over their responsibilities. Therefore, the banking platform tech stack evolves without a single moment of total system shutdown.

This minimizes operational risk and allows for a continuous feedback loop from real-world users.

B. Traffic Shifting and Shadow Testing

Before a new module goes live, it can run in “shadow mode,” where it processes real data but its results are not yet the source of truth.

This allows the team to compare the output of the new banking platform tech stack against the legacy system to ensure 100% accuracy. Consequently, when the actual switch happens, it is a non-event because the performance has already been validated.

2. Step-by-Step Transformation Approach

A successful modernization journey follows a logical sequence that prioritizes the most critical business needs while building a foundation for future growth.

A. Phase 1: Decoupling and API Enablement

The first step is to wrap the existing legacy core in a modern API layer. This allows the old system to communicate with new mobile apps and third-party fintech tools.

However, the core logic remains unchanged for now. This provides immediate value to the customer without the risk of moving the actual data ledger.

B. Phase 2: Microservices Migration

Once the API layer is stable, specific functions, like credit card processing or mortgage applications, are moved out of the monolith and into independent microservices.

In addition, these new services are built using the modern banking platform tech stack, benefiting from cloud scalability and automated testing. This step-by-step migration prevents the “all-or-nothing” pressure of traditional IT projects.

| Phase | Technical Focus | Business Value |

| Exposure | Creating APIs for legacy data. | Launches new digital channels quickly. |

| Separation | Moving non-core features to microservices. | Increases agility for specific products. |

| Re-platforming | Moving the core ledger to the cloud. | Drastically lowers infrastructure costs. |

3. Execution Models Used by Enterprises

Different organizations choose different paths based on their risk appetite and available capital. However, the goal remains the same: a resilient, high-performance banking platform tech stack.

A. The Parallel Run Model

In this model, the enterprise runs the old system and the new system side-by-side for a set period. Every transaction is processed by both, and the results are reconciled daily.

While this is more expensive in the short term, it provides the highest level of safety for institutions with zero tolerance for error.

As a result, the transition to the new banking platform tech stack happens only when the parallel results have been perfect for several months.

B.The Hollow-the-Core Strategy

This model focuses on stripping away all “non-banking” logic from the core ledger, such as customer communication, loyalty points, and reporting.

By moving these to a modern banking platform tech stack, the core ledger becomes much simpler and easier to eventually replace. This reduction in complexity makes the final step of modernization significantly safer and faster.

| Execution Model | Best For | Main Advantage |

| Strangler Fig | Complex Monoliths | Zero-downtime evolution. |

| Parallel Run | High-Value Ledgers | Maximum data integrity and safety. |

| Hollow-the-Core | Feature-Rich Platforms | Simplifies the path to full modernization. |

Modernizing a banking platform tech stack is a marathon and not a sprint. By choosing a progressive, step-by-step strategy, an enterprise can achieve the agility of a neobank while maintaining the stability of an established institution. This approach ensures that your technical infrastructure remains a growth enabler rather than a liability.

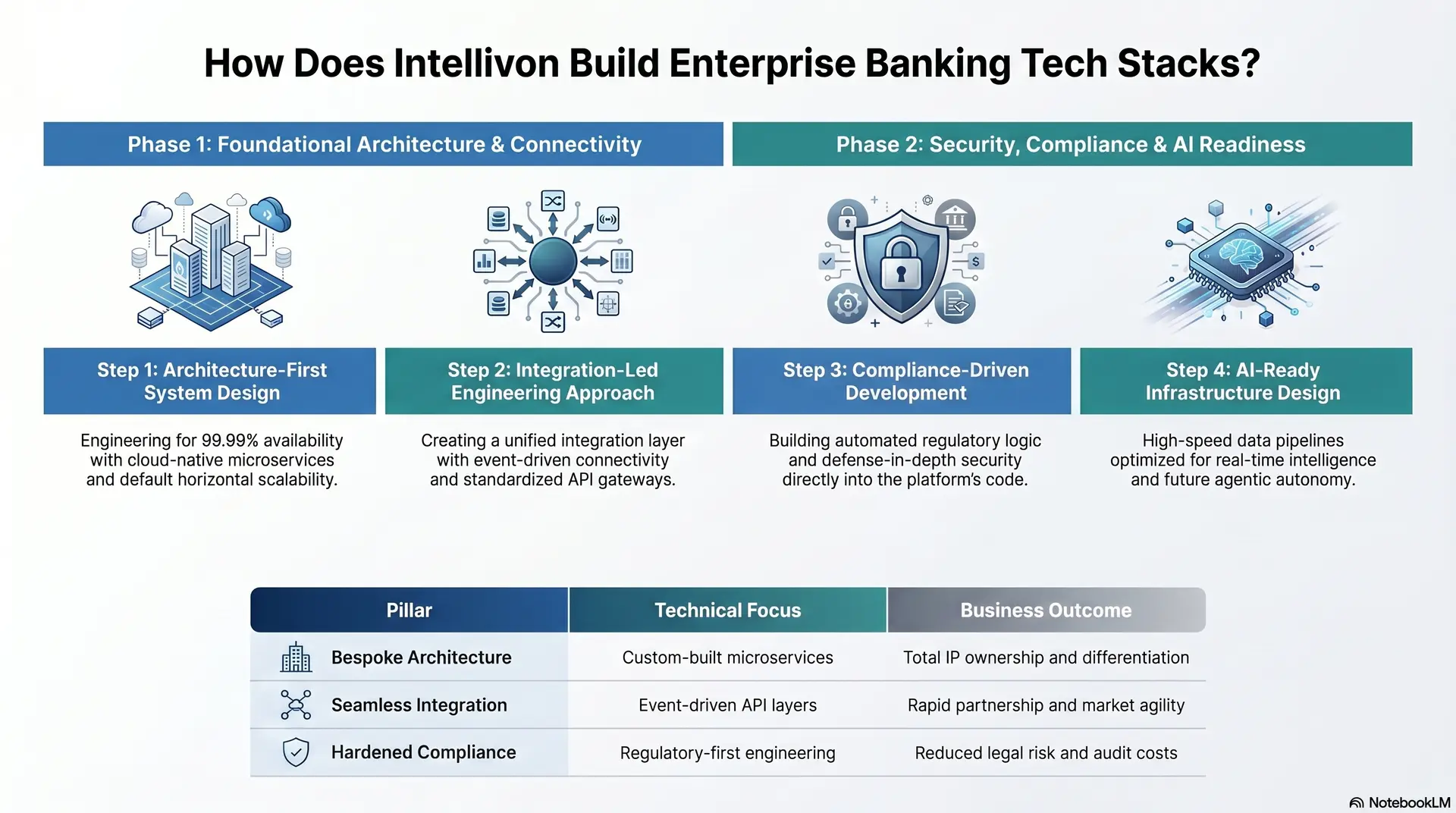

How Does Intellivon Build Enterprise Banking Tech Stacks?

Building a premium financial platform requires a strategic vision that anticipates the rigors of the global market. The approach at Intellivon centers on the belief that technical architecture should drive business value, not just support it.

By combining deep financial domain expertise with cutting-edge engineering, the result is a platform designed for absolute reliability and market dominance.

1. Architecture-First System Design

Before a single line of code is written, the structural integrity of the platform is meticulously planned. This ensures that the banking platform tech stack can handle massive transaction volumes while remaining flexible enough for future innovation.

A. Engineering for 99.99% Availability

Intellivon utilizes a cloud-native, microservices-driven architecture that eliminates single points of failure. This means every component is isolated and independently scalable.

Therefore, the system remains operational even during peak traffic surges or localized hardware failures. This architectural foresight protects the brand reputation of the institution from day one.

B. Horizontal Scalability by Default

The designs focus on horizontal scaling, allowing the banking platform tech stack to grow alongside the user base without requiring expensive system overhauls.

Consequently, resources are allocated dynamically, ensuring that the platform remains cost-effective during quiet hours while maintaining peak performance during demand spikes.

2. Integration-Led Engineering Approach

In a fragmented financial landscape, the ability to connect seamlessly with global ecosystems is a core competitive advantage. Our experts prioritize a unified integration layer that transforms disparate systems into a cohesive financial engine.

A. Event-Driven Connectivity

By implementing an event-driven banking platform tech stack, Intellivon ensures that data moves in real-time across the entire enterprise.

Whether it is syncing with a third-party KYC provider or a global payment rail, the integration is fluid and low-latency. This replaces slow, outdated batch processing with an instant data flow that powers a superior customer experience.

B. Standardized API Gateways

Every integration is managed through hardened, standardized API gateways. This approach ensures that adding new partners or features does not introduce security vulnerabilities or performance bottlenecks.

As a result, the platform becomes a plug-and-play hub for the latest fintech innovations, allowing the business to pivot and expand without technical friction.

3. Compliance-Driven Development

We build compliance directly into the code of the banking platform tech stack.

A. Embedded Regulatory Logic

From PCI DSS to GDPR and local banking mandates, the systems are designed to automate the heavy lifting of compliance. This includes automated audit trails, real-time AML monitoring, and zero-trust identity management.

Therefore, instead of manual reporting cycles, the platform provides a continuous, auditable state of compliance. This proactive design significantly reduces legal risk and lowers the cost of institutional oversight.

B. Security Across Every Layer

The security posture at Intellivon is built on the principle of defense-in-depth. Every transaction is encrypted, and every access request is verified.

By embedding security protocols at the database, application, and network levels, the banking platform tech stack becomes a fortified environment capable of withstanding the most sophisticated cyber threats.

4. AI-Ready Infrastructure Design

Intelligence is the next frontier of financial competition. Our experts ensure that every banking platform tech stack is built with the high-speed data pipelines required to power advanced AI and agentic workflows.

A. Real-Time Intelligence Pipelines

The infrastructure is optimized for Retrieval-Augmented Generation (RAG) and real-time scoring models. By providing the AI layer with instant access to clean, structured data, the platform enables autonomous fraud detection and hyper-personalized customer insights. This transforms the banking platform tech stack from a simple record-keeper into a proactive decision-making engine.

B. Preparing for Agentic Autonomy

We design with the future of Agentic AI in mind. The orchestration layers are built to support autonomous agents that can handle complex back-office workflows, such as corporate onboarding or automated treasury management.

Consequently, the enterprise gains a massive operational advantage, reducing headcount costs while increasing the speed and accuracy of high-value financial operations.

| Intellivon Pillar | Technical Focus | Business Outcome |

| Bespoke Architecture | Custom-built microservices. | Total IP ownership and differentiation. |

| Seamless Integration | Event-driven API layers. | Rapid partnership and market agility. |

| Hardened Compliance | Regulatory-first engineering. | Reduced legal risk and audit costs. |

| AI Integration | High-velocity data pipelines. | Future-proofed autonomous operations. |

The choice of a technical partner determines the ceiling of your business growth. At Intellivon, the goal is to build a banking platform tech stack that is not just a tool for today but a scalable engine for the future.

By prioritizing custom-grade engineering and AI readiness, Intellivon empowers leaders to launch with confidence and scale without limits.

Conclusion

An elite banking platform tech stack is the ultimate strategic asset for any modern institution. By prioritizing a modular, AI-ready architecture, leaders ensure long-term scalability and institutional resilience.

This investment secures a competitive edge, transforming technical infrastructure into a high-performance engine capable of driving sustainable growth and market dominance.

Build Your Enterprise Banking Platform With Intellivon

Building an enterprise banking platform involves designing a system that can handle real-time transactions, complex integrations, and evolving regulatory demands without breaking under scale.

B. Solving Integration Complexity at the Core

Banking platforms depend on multiple systems working together seamlessly. We build the integration layer that ensures everything, from core banking to third-party APIs, functions as a single system.

- API-first architecture for seamless system connectivity

- Middleware and orchestration layers for complex workflows

- Reliable integrations across payments, KYC, and financial systems

C. Building Compliance Into the Architecture

Compliance is a foundational requirement. We embed regulatory standards directly into the system design to reduce risk and avoid costly rework later.

- PCI DSS, GDPR, and SOC 2-aligned architecture

- Built-in audit trails and reporting mechanisms

- Secure data handling across all system layers

D. Designing AI-Ready Banking Infrastructure

Modern banking platforms must support intelligent decision-making. We build systems that can integrate AI capabilities without compromising performance or compliance.

- Real-time data pipelines for AI and analytics

- Infrastructure for fraud detection and risk scoring

- Controlled AI deployment with explainability and oversight

E. From MVP to Enterprise-Scale Platforms

Whether you’re starting with a focused MVP or building a full-scale banking platform, we align the architecture with your growth roadmap.

- Lean builds for early-stage platforms

- Scalable systems ready for enterprise expansion

- Clear upgrade paths from MVP to full infrastructure

Talk to Intellivon About Your Banking Platform

If you’re planning to build or modernize your platform, we can help you define the right architecture before you invest.

Connect with Intellivon’s experts to discuss your platform and get a clear path forward.

FAQs

Q1. How does a cloud-native banking platform handle peak traffic differently than a legacy system, like during payroll runs or market opens?

A1. Cloud-native platforms auto-scale compute resources in real time based on demand. Legacy systems run on fixed capacity, so peak events like payroll runs cause queuing delays. Cloud-native infrastructure absorbs those spikes without service degradation.

Q2. Is Kubernetes actually necessary for a fintech platform, or is it overkill?

A2. For platforms handling variable transaction loads across multiple services, Kubernetes earns its place. It automates deployment, scaling, and recovery. Smaller single-service platforms may not need it, but enterprise-grade banking infrastructure generally does.

Q3. Mambu vs. Thought Machine vs. Temenos — how do you actually decide which core banking platform to pick?

A3. Match the platform to your operating model. Mambu suits composable, fast-launch builds. Thought Machine fits institutions wanting ledger-level control. Temenos serves broad retail and corporate coverage. Product roadmap and migration reality should drive the decision.

Q4. Is building a custom core banking system ever worth it vs. buying a platform?

A4. Rarely at the start. Custom builds consume significant capital and time before generating value. Established platforms reduce infrastructure risk. Custom development makes sense only when your business model has needs that no existing platform can support.

Q5. How are fintechs actually automating AML and KYC in their stack — what tools are working?

A5. Fintechs are embedding tools like Sardine, Onfido, and ComplyAdvantage directly into onboarding flows. These run identity checks, sanctions screening, and behavioral monitoring in real time, replacing manual review queues with continuous, automated compliance coverage.

Q6. How is AI actually being used in enterprise banking platforms right now — not the hype, the real use cases?

A6. Fraud detection, credit decisioning, and compliance monitoring are the active use cases. AI models flag anomalous transactions in milliseconds, score loan applications without manual underwriting, and automate regulatory reporting. Generative AI is entering customer servicing workflows next.

Q7. Open banking and third-party integrations: what the API layer needs to support in 2026

A7. The API layer must handle consent management, token-based authentication, rate limiting, and real-time data exchange across partners. In 2026, BIAN-aligned APIs and event-driven architecture are the baseline for institutions operating in open banking ecosystems.