Key Takeaways

-

Treasury fragmentation is structural. No dashboard fixes a broken data foundation underneath it.

-

A unified platform is six layers working as one: connectivity, payments, forecasting, risk, compliance, and a cash visibility engine that never sleeps.

-

Replacing your ERP is not required. A modern orchestration layer wraps existing systems and adds real-time capability without a rip-and-replace project.

-

Building a unified treasury platform starts between $50,000 and $150,000 for a focused MVP. Scope, integration depth, and entity complexity determine where the final number lands.

-

How Intellivon develops your unified treasury platform fast and at scale.

Enterprise finance functions were never designed. Instead, they grew gradually with one bank portal, one ERP module, and one spreadsheet workaround at a time. The result is a disjointed system making billion-dollar liquidity decisions based on two-day-old data.

The previous structure was created for a simpler time, where there were fewer banking relationships, fewer currencies, and fewer regulatory responsibilities. However, financial institutions now do not have the luxury to wait around for anomalies to show up and risk losing money or user trust.

This is why serious operators are looking beyond fixing existing systems. They are creating unified treasury platforms that handle cash visibility, payments, forecasting, and risk as a single workflow rather than treating them as four separate issues. According to Deloitte, 64% of enterprise treasurers see global cash visibility as their biggest challenge. This number has not changed because the tools have not improved.

At Intellivon, we develop enterprise-grade financial platforms for organizations ready to address this issue at the structural level. This blog draws on our experience and talks about how we build such platforms from the ground up.

Why Treasury Systems Are Fragmented in 2026

Treasury infrastructure across large enterprises remains deeply fragmented in 2026. Legacy ERP integrations, disconnected bank portals, and regional regulatory silos continue to block the kind of real-time cash visibility that modern finance demands.

Market data reflects a clear response, as enterprises are actively shifting toward unified treasury platforms that consolidate these layers into a single operational environment.

This shift is being accelerated by two converging pressures: economic fragmentation across global markets and growing AI-driven demands that require clean, centralized data to function effectively.

Three structural problems drive enterprise treasury fragmentation, and they tend to reinforce each other. They are:

- Legacy silos are the most visible. Large enterprises typically juggle multiple ERPs, treasury systems, and bank portals at once. Each runs on its own data model. Therefore, reconciliation becomes manual and slow, and decisions get delayed because the data is never truly unified.

- Geopolitical volatility adds another layer. Divergent interest rates (the US and UK near 3.75%, the ECB closer to 2.15%) force region-specific liquidity strategies. Managing those across fragmented systems amplifies risk rather than containing it.

- Regulatory complexity compounds both. Cross-border compliance requirements and currency controls block clean data flows between jurisdictions. What works operationally in one market rarely replicates cleanly in another.

The Shift Toward Unified Systems

Unified treasury platforms address these problems at the infrastructure level. They consolidate data from ERPs, banks, and payment systems into a single real-time environment.

However, the best platforms go further. Kyriba, FIS, and ION now embed AI forecasting and automated workflows directly into ERP ecosystems. The result is fewer portals, less manual intervention, and faster liquidity decisions.

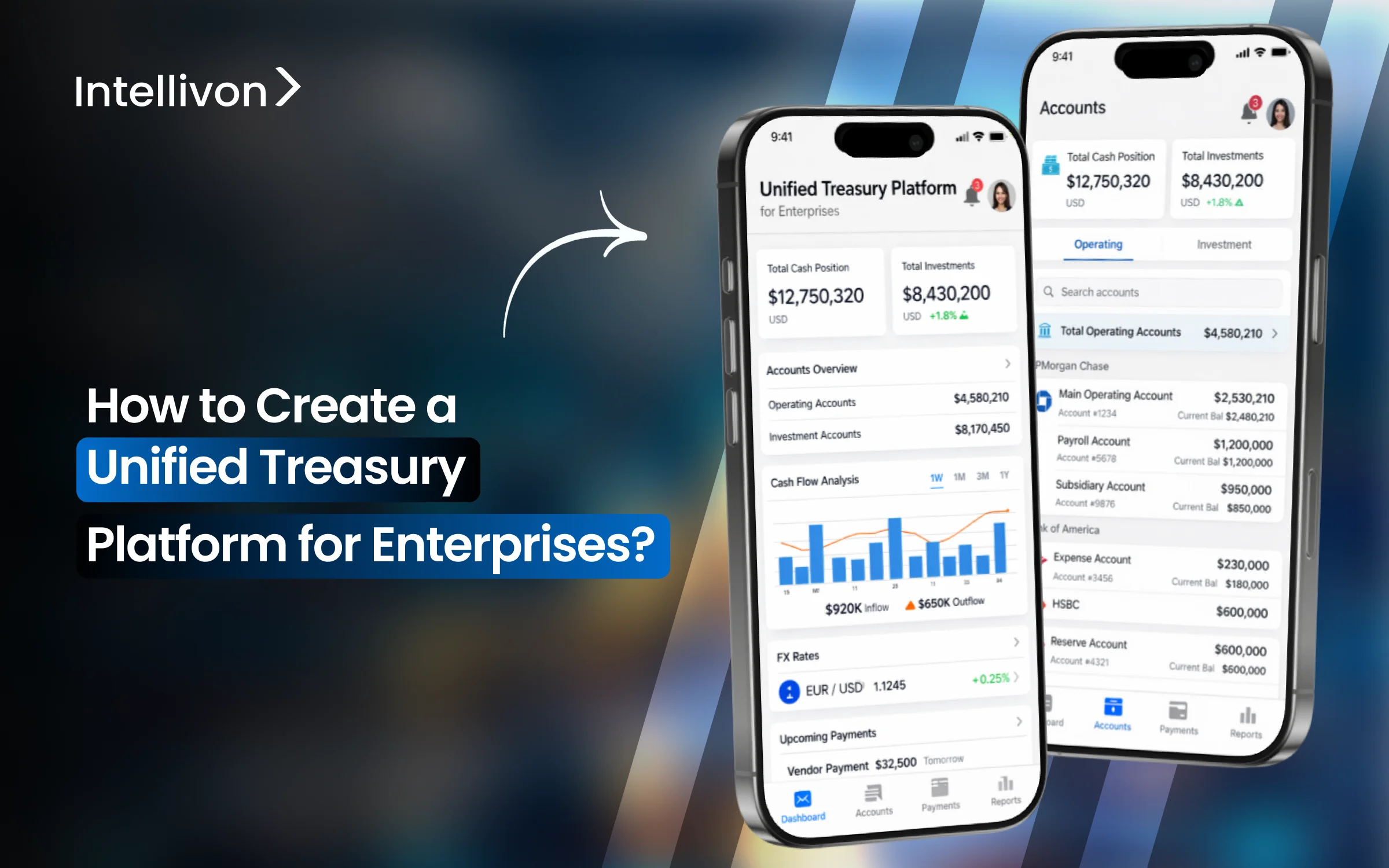

What Is a Unified Treasury Platform?

A unified treasury platform is a digital command center for all company money. It brings cash, investments, and debt into one clear view. Many businesses still use messy spreadsheets to track global accounts.

However, this platform connects directly to banks for instant updates. Consequently, leadership sees exactly how much capital is available right now. Therefore, the business moves funds faster and avoids costly financial mistakes.

Specifically, this system removes the guesswork from global finance. It monitors every transaction across different regions automatically. Furthermore, the software identifies hidden fees and idle cash balances.

Because everything is in one place, teams stop wasting time on manual data entry. Ultimately, this creates a faster and more secure way to grow a business.

Unified Platform vs TMS vs ERP Treasury

Enterprises often struggle to choose between specific financial tools. Standard ERP systems handle general accounting well. However, they usually lack deep treasury functionality.

Traditional Treasury Management Systems (TMS) offer more features for cash managers. Yet, these tools often exist as silos. Consequently, data stays trapped in separate environments. A unified platform solves this by merging these capabilities into a single architecture.

The following table compares these three distinct approaches:

| Feature | ERP Treasury | Traditional TMS | Unified Platform |

| Data Speed | Batch processing | Real-time or batch | Instant API-driven |

| Integration | Native to accounting | Requires complex APIs | Native cross-stack |

| Global Visibility | Limited/Fragmented | High but siloed | Complete & Centralized |

| Automation | Basic workflows | Intermediate | Advanced AI-driven |

| Cost Focus | Operational efficiency | Liquidity control | Strategic growth |

In conclusion, the choice depends on the scale of the business. ERPs are fine for simple reporting. A TMS serves specialized teams. However, a unified platform is the modern choice for scaling enterprises. It provides the agility needed for high-stakes investment. Therefore, it replaces manual effort with strategic, data-led clarity.

What Enterprises Actually Mean by “Unified”

True unification is often misunderstood in the corporate world. Many vendors promise a single solution but only deliver a combined interface. For a large business, being unified means more than just a shared login.

It requires a fundamental shift in how financial data moves. Therefore, leaders must distinguish between surface-level integration and deep structural synergy.

1. One UI vs. One Data Layer (The Critical Difference)

A single user interface (UI) is often just a superficial “skin” over old systems. It looks modern, but the underlying data remains messy and disconnected. In contrast, a single data layer ensures every department sees the identical numbers at the same time.

Consequently, teams avoid the tedious task of reconciling different reports at month-end. Specifically, this architecture allows for instant updates across the entire global organization.

| Comparison Point | Unified User Interface (UI) | Unified Data Layer |

| Primary Goal | Visual consistency | Data integrity and speed |

| Data Source | Multiple legacy databases | Single, centralized source |

| Accuracy | Prone to sync delays | Real-time “Single Source of Truth” |

| Maintenance | High (mapping multiple APIs) | Low (native data structure) |

| Decision Impact | Based on potentially old data | Based on live financial reality |

Without a shared data layer, a business still operates on delayed information. Therefore, a pretty interface cannot fix a broken foundation.

2. Operational Unification vs. Reporting Unification

Reporting unification only tells a leader what happened in the past. It gathers historical data into a neat chart for a board meeting. However, operational unification allows for immediate action within the same system.

It connects the “doing” with the “seeing” seamlessly. For example, a treasurer can move millions across borders with one click. This happens because the payment rails and the cash view are physically connected.

| Aspect | Reporting Unification | Operational Unification |

| Focus | Observation and Analysis | Execution and Action |

| Timeframe | Retrospective (Past) | Real-time (Present) |

| User Capability | View-only dashboards | Transact-and-track workflows |

| Efficiency | Manual execution required | Automated straight-through processing |

| Strategic Value | Identifying trends | Capitalizing on market movements |

Therefore, the platform becomes an active tool for execution, not just a passive ledger. Specifically, it moves the company from slow reporting to high-speed growth.

3. Why Most TMS Platforms Stop Halfway

Traditional Treasury Management Systems (TMS) were built for a different era. They focus heavily on niche financial tasks like hedge accounting.

Consequently, they often fail to connect with the broader business operations. These tools act as a specialized island for the finance team. Furthermore, they usually require manual uploads to sync with other departments.

Because they lack modern API connectivity, they cannot provide the “unified” experience promised. They solve part of the puzzle but leave the rest of the business in the dark.

4. The Shift from Tools to Infrastructure

Modern enterprises are moving away from buying isolated software tools. Instead, they are investing in financial infrastructure. A tool is something you use occasionally for a specific task. Infrastructure is the permanent foundation that powers everything you do.

Specifically, a unified treasury platform acts as the plumbing for your capital. It handles the heavy lifting of security, compliance, and connectivity automatically. Consequently, leadership can focus on growth rather than fixing broken data pipelines.

In conclusion, “unified” is a technical standard, not just a marketing term. It requires a clean data layer and operational control. Furthermore, it moves the company from slow reporting to high-speed execution. Therefore, choosing the right architecture is a strategic necessity for any scaling enterprise.

When Should You Build vs Buy vs Integrate

Choosing the right path for a treasury platform is a high-stakes capital decision. Most enterprises treat this as a simple software choice. However, the decision dictates how fast the business can react to global market shifts.

A wrong turn leads to millions in technical debt. Consequently, leadership must weigh long-term flexibility against immediate deployment speed.

1. Build vs. Buy: Where Enterprises Get It Wrong

Many organizations believe building a custom solution offers the ultimate control. They hire developers to replicate standard banking connections and ledger logic. Yet, they often underestimate the cost of maintaining global compliance and security updates.

Conversely, buying a generic SaaS product offers speed but can limit unique strategic workflows. Specifically, the mistake lies in failing to distinguish between core infrastructure and competitive advantage.

| Factor | Building Custom | Buying SaaS | Hybrid Approach |

| Time to Market | 12–24 months | 3–6 months | 6–9 months |

| Total Cost | High (Initial + Maintenance) | Moderate (Subscription) | Balanced ROI |

| Flexibility | Total (Unlimited) | Limited by vendor roadmap | High (Modular) |

| Security | Internal Responsibility | Vendor-guaranteed | Shared Responsibility |

| Integration | Custom-coded | Pre-built connectors | API-first orchestration |

Therefore, the goal is not just to own the code. The goal is to own the business logic while delegating the plumbing.

2. Best-of-Breed vs. Single Vendor Platforms

A best-of-breed strategy involves picking the top tool for every specific task. For example, a firm might use one tool for FX and another for cash positioning. While this offers depth, it often creates “integration hell.”

In contrast, a single vendor platform promises a smoother experience. However, it may lack the specialized features needed for complex global operations.

| Aspect | Best-of-Breed Strategy | Single Vendor Platform |

| Complexity | High (Managing 5+ vendors) | Low (Single point of contact) |

| Data Flow | Fragmented/Needs middleware | Seamless/Native |

| Expertise | Specialized in every niche | Generalist across all areas |

| Upgrade Cycle | Difficult to sync changes | Unified updates |

Furthermore, the “unified” approach is now bridging this gap. It provides the depth of specialized tools within a single, cohesive architecture.

3. Can You Unify Without Replacing ERP?

Replacing a core ERP is a multi-year nightmare that most leaders want to avoid. Fortunately, modern treasury platforms act as an orchestration layer above the ERP. They pull data from legacy systems and push processed instructions back.

This allows the business to modernize without a “rip and replace” strategy. Consequently, the ERP remains the system of record while the treasury platform becomes the system of action. Specifically, this preserves existing investments while adding much-needed agility.

4. When Custom Platforms Outperform SaaS

SaaS is excellent for standardizing common processes. However, if a business has a unique revenue model or complex cross-border flows, SaaS can become a bottleneck.

Custom-built platforms on top of robust AI infrastructure outperform off-the-shelf software in high-velocity environments.

Specifically, these platforms allow for proprietary risk models and automated settlement logic that competitors cannot copy. Therefore, for enterprises seeking a “moat,” a custom-built architecture is often the only logical choice.

In conclusion, the decision rests on whether the financial operation is a back-office function or a growth engine. If agility is the priority, integration and orchestration are the best paths. Furthermore, leveraging an expert partner ensures the foundation is built for the next decade.

Core Architecture of a Unified Treasury Platform

Building a resilient treasury ecosystem requires a multi-layered approach to data and execution. Each layer must communicate flawlessly to ensure capital remains mobile and secure.

For decision-makers, understanding this stack is vital for identifying technical bottlenecks. Consequently, a well-architected platform transforms raw banking data into a strategic asset.

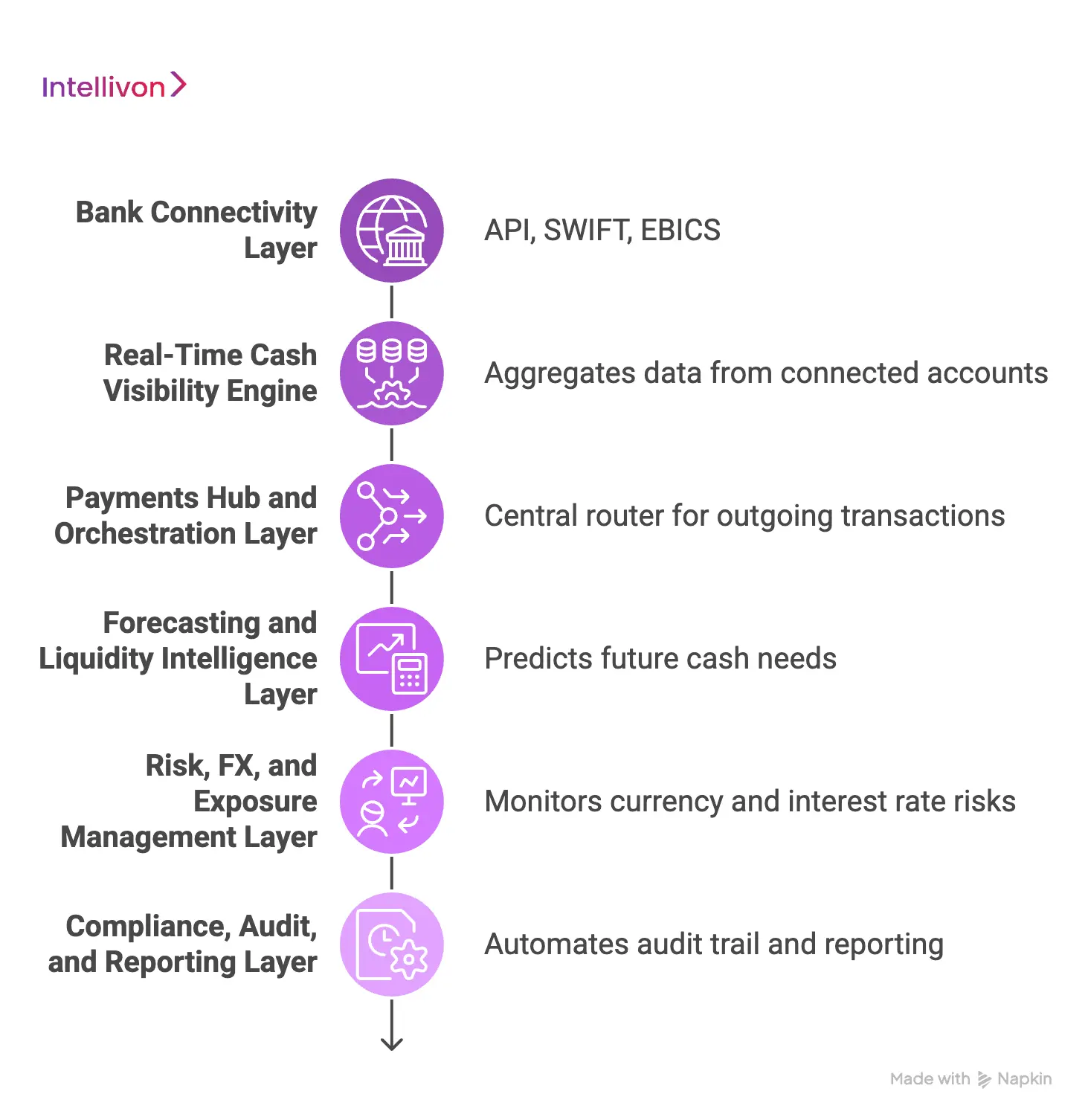

1. Bank Connectivity Layer (API, SWIFT, EBICS)

The foundation of any platform is its ability to talk to the global banking system. Historically, this meant slow, manual file uploads or expensive SWIFT setups.

Modern platforms now use a hybrid approach to maximize reach and speed. Specifically, they combine the security of SWIFT with the real-time speed of regional APIs.

| Connection Type | Speed | Reach | Primary Use Case |

| API | Instant | Regional/Modern Banks | Real-time balances and fintech |

| SWIFT (gpi) | Near Instant | Global (11,000+ institutions) | High-value international wires |

| EBICS | Batch | Primarily Europe (DACH) | High-volume corporate payments |

| Host-to-Host | High Speed | Direct Bank-to-Enterprise | Secure, high-volume recurring data |

2. Real-Time Cash Visibility Engine

Knowing the exact cash position at any moment is a competitive necessity. This engine aggregates data from every connected account across the globe. Therefore, it eliminates the “visibility gap” caused by time zone differences.

Furthermore, it automatically normalizes different currencies into a single reporting value. Consequently, leadership sees a live snapshot of global liquidity without waiting for manual bank reconciliations.

3. Payments Hub and Orchestration Layer

A unified payments hub acts as a central router for every outgoing transaction. It decides the best way to send it. Specifically, the orchestration layer evaluates cost, speed, and compliance for each payment.

If a faster rail like RTP (Real-Time Payments) is available, the system selects it automatically. Therefore, the business reduces transaction fees while ensuring vendors are paid on time.

4. Forecasting and Liquidity Intelligence Layer

Predicting future cash needs is where most enterprises struggle due to fragmented data. This layer uses historical patterns and current orders to project liquidity weeks or months in advance.

Specifically, it moves beyond static spreadsheets by incorporating AI-driven variables. Consequently, it identifies potential shortfalls before they happen. This allows the firm to move idle cash into yield-bearing investments rather than leaving it sitting in low-interest accounts.

5. Risk, FX, and Exposure Management Layer

Global operations bring constant exposure to currency and interest rate shifts. This layer monitors these risks in real-time by linking market feeds to internal balances. Specifically, it calculates “value at risk” for every currency pair automatically.

Therefore, the treasury team can execute hedges immediately when thresholds are breached. In addition, it provides a clear view of counterparty risk, ensuring the business is not over-exposed to a single financial institution.

6. Compliance, Audit, and Reporting Layer

Regulatory requirements like KYC, AML, and SOC2 are non-negotiable for enterprise finance. This layer automates the audit trail for every single movement of money.

Specifically, it provides granular permissions so only authorized users can approve high-value transfers. Furthermore, it generates “push-button” reports for tax and regulatory filings.

Because the data is immutable and centralized, the cost of year-end audits is significantly reduced.

In conclusion, these six layers represent the difference between a simple tool and a robust infrastructure. Furthermore, they provide the technical confidence needed to manage billions in global capital.

Therefore, investing in a complete stack is the only way to ensure long-term operational resilience.

The Missing Layer in Most Treasury Stacks

Most financial architectures suffer from a fundamental disconnect between vision and execution. Enterprises want total control, yet the technology is often a patchwork of legacy fixes.

Despite spending millions on premium software, data remains trapped in transit. Consequently, a “missing layer” exists between the bank and the balance sheet. Recognizing this gap is the first step toward achieving true capital agility.

1. Why ERPs, TMS, and Banks Don’t Talk Cleanly

Traditional financial systems were never designed for the era of instant, global data. ERPs focus on static accounting records, while banks use various messaging formats that vary by region.

- Data Structure Mismatch: ERPs often expect rigid, old-school data formats. Modern banking APIs provide rich, real-time data that legacy systems cannot digest.

- Sync Schedule Gaps: Banks move in real-time, but ERPs often process in batches. Consequently, the “current” balance in the ERP is almost always outdated.

- Regional Fragmentation: Different countries use different standards (like ISO 20022 vs. local formats). Therefore, a global firm ends up with a mess of incompatible data streams.

Specifically, this mismatch leads to “data friction,” where information must be manually cleaned or mapped. Therefore, the treasury team spends more time fixing broken records than analyzing market opportunities.

2. The Role of a Treasury Orchestration Layer

An orchestration layer acts as the intelligent translator for the entire financial stack. It sits above the banks, the ERP, and the TMS, pulling disparate data into a unified stream.

- Intelligent Routing: The layer decides the cheapest and fastest path for every payment. It evaluates local clearing vs. international wires automatically.

- Pre-execution Validation: It checks payments against compliance lists before they leave the building. Specifically, this prevents costly bank rejections and “frozen” funds.

- Native Connectivity: Instead of custom coding for every bank, the layer uses pre-built connectors. Consequently, adding a new banking partner takes days, not months.

Unlike a simple bridge, it actively manages the logic of how money moves. Therefore, the business gains the ability to add new banks or payment methods without rewriting its entire backend.

| Feature | Legacy Integration | Orchestration Layer |

| Data Mapping | Manual/Hard-coded | Automated/Dynamic |

| Speed of Change | Low (Requires IT) | High (Low-code/No-code) |

| Error Handling | Reactive (After failure) | Proactive (Validation first) |

| Visibility | Siloed by platform | Global and centralized |

3. How Leading Enterprises Unify Without Rip-and-Replace

The most successful firms avoid the high-risk “rip-and-replace” strategy. Instead, they adopt a modular approach by wrapping their existing systems in a modern layer.

- API Wrappers: Use modern APIs to “talk” to old software. This keeps the legacy ERP stable while giving it modern superpowers.

- Parallel Processing: Run the new treasury platform alongside the old system. Consequently, there is zero downtime during the transition.

- Phased Migration: Connect one region or one bank at a time. Therefore, the team can prove ROI on a small scale before a full global rollout.

Specifically, this preserves the stability of the core business while adding the agility of a startup. Consequently, the enterprise modernizes in weeks rather than years.

4. Turning Fragmented Systems into a Single Flow

Achieving a single flow requires moving from “batch” thinking to “stream” thinking. In a fragmented environment, data moves in chunks, leading to blind spots.

- Continuous Reconciliation: The system matches bank statements to invoices as they happen. This eliminates the “month-end crunch” for the finance team.

- Global Liquidity Pooling: Move money across entities automatically based on real-time needs. Specifically, this reduces the need for expensive short-term borrowing.

- Automated Accounting: Transactions are tagged and coded the moment they occur. Furthermore, the data flows directly into the general ledger without human intervention.

Ultimately, this transforms a collection of isolated tools into a high-performance financial engine. Furthermore, it provides the structural freedom to scale into new markets with confidence.

Must-Have Features in Enterprise Treasury Platforms

Selecting the right platform requires looking beyond basic functionality. For a global enterprise, the platform must act as a sophisticated nervous system that handles immense complexity without breaking.

Consequently, certain features are the baseline for survival in a volatile economy. Therefore, leadership must verify these core capabilities during the evaluation phase.

1. Multi-entity and Multi-currency Consolidation

Managing diverse subsidiaries across different regions is a significant operational hurdle. A platform must handle various accounting standards and tax jurisdictions within a single environment.

- Virtual Account Structures: Group different entities under one logical view without merging their physical bank accounts.

- Automatic FX Conversions: Convert all local balances into a functional currency in real-time. Specifically, this provides an instant global “net worth” view.

- Intercompany Tracking: Automatically record and reconcile loans and transfers between subsidiaries. Consequently, internal debt management becomes a background task rather than a manual project.

2. Real-time Global Cash Visibility

Visibility is the cornerstone of risk management. If a business cannot see its cash, it cannot deploy it effectively. A unified platform removes the “blind spots” created by delayed bank statements.

- Intraday Bank Reporting: Pull balance updates every few minutes via API rather than waiting for end-of-day files.

- Global Dashboarding: View every dollar across North America, EMEA, and APAC in one window. Furthermore, users can drill down into specific regional banks with one click.

- Idle Cash Identification: Automatically flag accounts with excess liquidity that could be earning interest. Specifically, this ensures that no capital sits unproductive.

3. AI-powered Cash Flow Forecasting

Traditional forecasting relies on manual guesswork and outdated data. AI transforms this into a predictive science by analyzing millions of historical data points.

- Pattern Recognition: The system identifies seasonal trends and payment behaviors of specific vendors. Therefore, it predicts outflows with much higher accuracy.

- Scenario Modeling: Run “what-if” simulations for market shocks or interest rate changes. Consequently, leadership can prepare for volatility before it strikes.

- Anomaly Alerts: Receive notifications when actual cash flows deviate significantly from the forecast. Specifically, this allows for immediate investigation of potential operational issues.

4. In-house Banking (IHB) Capabilities

In-house banking allows an enterprise to act as its own central bank. This reduces the need for external banking services and lowers transaction costs across the organization.

- Centralized Payment Factories: Process all subsidiary payments from a single hub to gain better terms from banks.

- Netting and Settlement: Offset internal receivables and payables so that only the “net” amount is moved externally. Specifically, this drastically reduces wire fees and FX costs.

- Internal Credit Lines: Provide liquidity to struggling subsidiaries from the central treasury. Consequently, the firm avoids expensive external borrowing.

5. Payment Fraud Detection Systems

As payment volumes grow, so does the risk of sophisticated cyber-attacks. A modern platform must include active defenses that sit within the payment workflow.

- Behavioral Analysis: Flag transactions that fall outside the normal pattern for a specific user or vendor.

- Sanction Screening: Automatically check every outgoing payment against global watchlists (OFAC, UN, etc.). Therefore, the business avoids massive regulatory fines.

- Multi-factor Approval: Require digital signatures from multiple executives for high-value movements. Specifically, this prevents “social engineering” attacks from succeeding.

6. ISO 20022-ready Data Architecture

The global banking system is shifting to the ISO 20022 standard for financial messaging. Platforms that do not support this rich data format will soon become obsolete.

- Enhanced Data Fields: Capture more information with every payment, such as original invoice numbers and detailed tax info. Consequently, reconciliation becomes fully automated.

- Global Interoperability: Ensure seamless communication with every major clearing system (SWIFT, SEPA, FedNow).

- Reduced Rejections: Richer data means fewer manual interventions and fewer failed payments. Therefore, the “straight-through processing” rate increases significantly.

7. Digital Assets and Stablecoin Readiness

The frontier of treasury involves programmable money and blockchain-based settlements. Even if not used today, a platform must be architected to handle digital assets tomorrow.

- Stablecoin Support: The ability to hold and move assets like USDC for near-instant cross-border settlement.

- Wallet Integration: Securely manage private keys alongside traditional bank account credentials. Specifically, this bridges the gap between Web2 and Web3 finance.

- Smart Contract Execution: Automate payments based on specific conditions being met in a supply chain. Ultimately, this represents the future of high-velocity enterprise commerce.

| Feature | Business Impact | Executive Value |

| IHB Capabilities | Reduces external bank fees | Maximizes internal ROI |

| AI Forecasting | Eliminates liquidity surprises | Improves strategic planning |

| Fraud Detection | Prevents capital loss | Ensures institutional security |

| ISO 20022 | Future-proofs connectivity | Automates reconciliation |

In conclusion, these features transform a treasury department from a manual reporting unit into a strategic command center. Furthermore, adopting this complete architectural stack ensures that the business can navigate global volatility with absolute confidence.

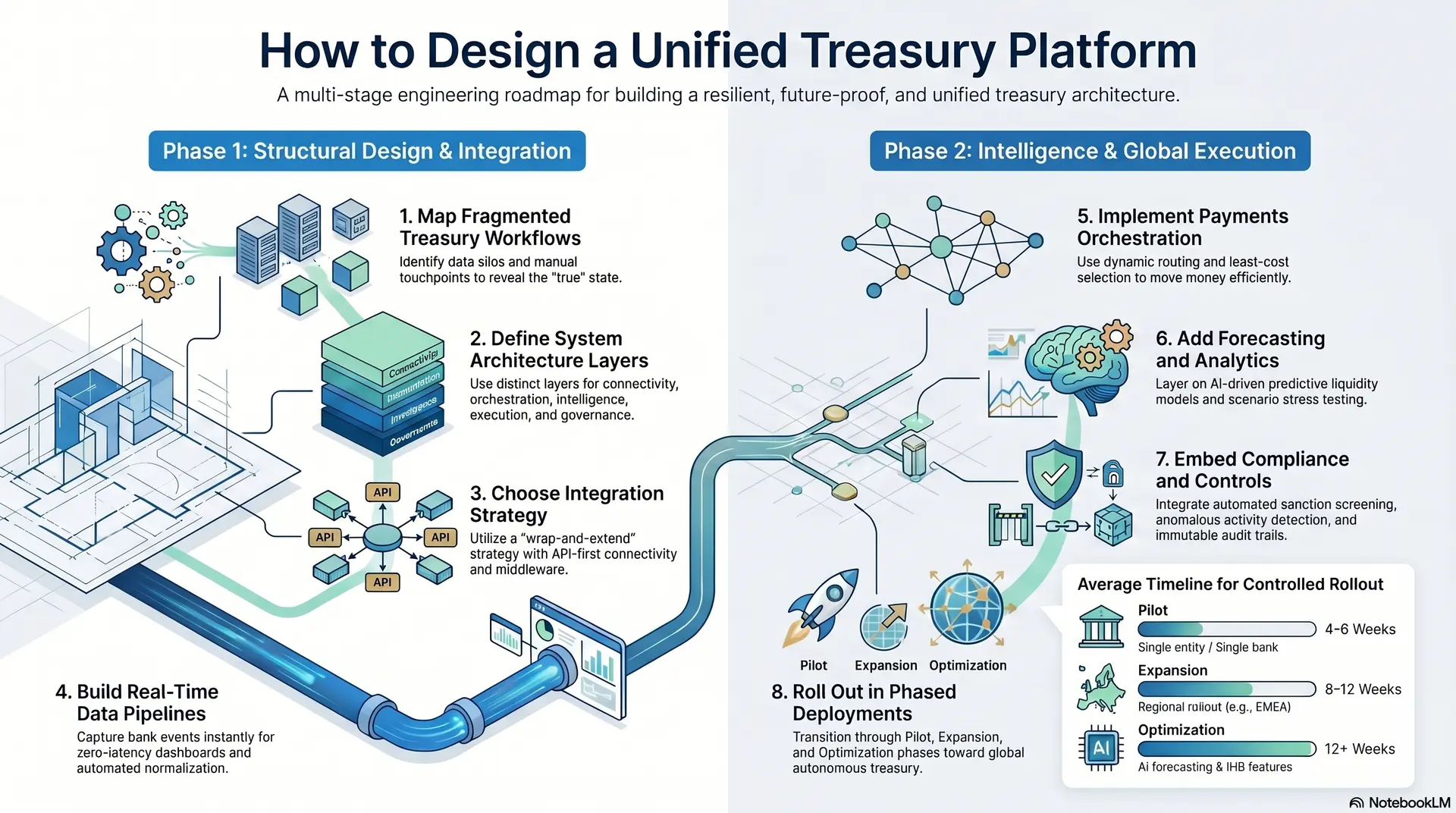

How to Design a Unified Treasury Platform

Designing a unified platform is not a software installation; it is an architectural overhaul. At Intellivon, we approach this as a multi-stage engineering project that aligns technical infrastructure with high-level financial strategy.

Consequently, the goal is to build a system that grows alongside the enterprise. Therefore, we follow a rigorous eight-step roadmap to ensure the final product is both resilient and future-proof.

Step 1: Map Fragmented Treasury Workflows

Before writing a single line of code, we identify where data currently gets stuck. Most enterprises operate with “ghost” spreadsheets and manual workarounds that hide operational risks.

- Identify Data Silos: We audit every department, from procurement to payroll, to see how they currently report cash.

- Document Manual Touchpoints: We pinpoint processes that require human intervention, as these are the primary sources of error.

- Analyze Latency: We measure the time it takes for a transaction to move from a local bank account to the central ledger.

Specifically, this mapping phase reveals the “true” state of the treasury. Consequently, it allows us to design a system that solves real-world bottlenecks rather than theoretical ones.

Step 2: Define System Architecture Layers

A robust platform requires a clean separation of concerns. We design the architecture in distinct layers to ensure that a change in one area (like a new bank) does not break the entire system.

| Layer | Responsibility | Key Component |

| Connectivity | Talking to the banks | APIs, SWIFT, H2H |

| Orchestration | Managing the logic | Business rules engine |

| Intelligence | Processing the data | AI/ML forecasting models |

| Execution | Moving the money | Payment hub |

| Governance | Securing the flow | IAM & Audit logs |

Therefore, the architecture remains modular and easy to scale. Furthermore, this layered approach allows for easier updates to security protocols without disrupting daily operations.

Step 3: Choose Integration Strategy

We help leaders decide whether to build, buy, or use a hybrid model. We typically recommend a “wrap-and-extend” strategy. This involves building a modern orchestration layer around existing ERP systems.

- API-First Connectivity: We prioritize RESTful APIs for real-time speed while maintaining SWIFT for global reach.

- Middleware Utilization: We deploy intelligent middleware to translate legacy data formats into modern standards like ISO 20022.

- ERP Preservation: Specifically, we ensure the current ERP remains the system of record to avoid a risky “rip-and-replace” scenario.

Step 4: Build Real-Time Data Pipelines

The heart of the platform is the data pipeline. We build high-throughput streams that ingest, clean, and normalize financial data the second it is generated.

- Event-Driven Ingestion: We use technologies like Kafka to capture bank events as they happen.

- Automated Data Normalization: The system automatically converts different currency formats and transaction codes into a unified standard.

- Zero-Latency Dashboards: Consequently, the executive view is always current. Therefore, there is no more waiting for “end-of-day” reports to see the global cash position.

Step 5: Implement Payments Orchestration

We transform the payment process from a manual task into an automated routing engine. This layer chooses the best path for every dollar leaving the organization.

- Dynamic Routing: The platform evaluates cost, speed, and success rates across multiple banking rails in real-time.

- Least-Cost Selection: Specifically, the system automatically routes domestic payments through local rails (like ACH or SEPA) instead of expensive international wires.

- Failover Protection: If one banking partner experiences an outage, the orchestrator reroutes the payment through an alternative channel instantly.

Step 6: Add Forecasting and Analytics

Once the data is flowing cleanly, we layer on AI-driven intelligence. This moves the treasury team from “tracking the past” to “predicting the future.”

- Predictive Liquidity Models: Our AI analyzes historical patterns to forecast cash needs with over 95% accuracy.

- Scenario Stress Testing: We build tools that allow leaders to simulate the impact of market crashes or supply chain disruptions.

- Investment Recommendations: Furthermore, the system flags excess liquidity and suggests short-term investment vehicles to maximize yield.

Step 7: Embed Compliance and Controls

Security is not an afterthought in our design process. We embed institutional-grade controls directly into the platform’s code.

- Automated Sanction Screening: Every payment is checked against global watchlists before execution.

- Anomalous Activity Detection: Specifically, our AI flags transactions that deviate from established patterns, preventing internal and external fraud.

- Immutable Audit Trails: We ensure every approval and movement of money is logged in a tamper-proof ledger. Consequently, year-end audits become a simple verification process rather than a months-long investigation.

Step 8: Roll Out in Phased Deployments

We avoid abrupt launches that can disrupt a global business. Instead, we follow a controlled rollout plan to ensure stability at every stage.

| Phase | Focus Area | Timeline (Avg) |

| Pilot | Single entity / Single bank | 4–6 Weeks |

| Expansion | Regional rollout (e.g., EMEA) | 8–12 Weeks |

| Optimization | AI forecasting & IHB features | 12+ Weeks |

| Full Maturity | Global autonomous treasury | Ongoing |

In conclusion, this structured approach ensures that the platform delivers immediate value while building long-term resilience. Furthermore, it allows the organization to adapt to the new system without overwhelming the finance team. Therefore, a phased rollout is the most secure path to a unified treasury.

Integration Strategy for Unified Treasury Platforms

A successful treasury platform lives or dies by its connectivity. For a global enterprise, integration is not a one-time setup but a permanent strategic capability. At Intellivon, we design integration layers that act as a universal translator for your entire financial ecosystem.

Consequently, the business gains the freedom to add new partners or regions without re-engineering the core. Therefore, a robust strategy must address the technical friction inherent in global finance.

1. Connecting Multiple ERPs and Subsidiaries

Large enterprises often grow through acquisitions, leaving them with a fragmented landscape of different ERP systems. We focus on creating a unified reporting and execution layer that sits above this complexity.

- Virtual Data Consolidation: We pull data from diverse systems like SAP, Oracle, and Microsoft Dynamics into a central warehouse.

- Entity Mapping: Each subsidiary maintains its local accounting rules, but the platform maps them to a single corporate standard.

- Decentralized Access, Centralized Control: Local teams manage their workflows, while the central treasury maintains oversight of all global balances.

Specifically, this approach allows the business to maintain operational continuity while achieving a “single pane of glass” view. Furthermore, it eliminates the need for expensive ERP consolidation projects.

2. Integrating Several Banking Partners

Managing a vast network of banking partners requires a sophisticated communication strategy. Each bank has its own technical requirements, security protocols, and data formats.

- Pre-Built Connector Libraries: We utilize a library of existing banking integrations to accelerate the onboarding process.

- Security Credential Management: The platform securely stores and manages digital certificates and API keys for every partner.

- Multi-Bank Reconciliation: Specifically, the system automatically matches statements from various banks against internal records. Consequently, the treasury team avoids the manual nightmare of logging into ten different portals every morning.

3. API vs. Host-to-Host vs. SWIFT Trade-offs

Choosing the right communication protocol is a balance between speed, reach, and cost. Most modern platforms use a hybrid model to ensure 100% global coverage.

| Connection Type | Speed | Technical Complexity | Best Use Case |

| Bank API | Real-time | Moderate (High variety) | Intraday visibility and instant payments |

| Host-to-Host (H2H) | High speed | High (Direct bank link) | High-volume recurring transactions |

| SWIFT (gpi) | Near real-time | High (Network fees) | Global reach for cross-border wires |

Therefore, we select the protocol that matches the specific needs of each region. Specifically, we use APIs for regional speed and SWIFT for global reliability.

4. Data Normalization Across Systems

Financial data is notoriously messy. A “payment” in one system might be labeled differently in another. We build normalization engines that ensure data is clean and comparable.

- Transaction Code Mapping: We translate proprietary bank codes into a standardized internal language.

- Currency Standardization: All local values are converted using live market rates for accurate global reporting.

- Metadata Enrichment: Furthermore, we attach internal project codes or invoice numbers to raw bank data. Consequently, the data becomes actionable intelligence rather than just a list of numbers.

5. Real-Time vs. Batch Integration Models

The shift from batch processing to real-time integration is the defining trend in modern treasury. However, some legacy processes still require scheduled updates.

- Real-Time (Streaming): Used for urgent payments and instant fraud detection. We prioritize this for high-velocity markets.

- Intraday (Scheduled): Useful for non-urgent balance updates that happen every few hours.

- End-of-Day (Batch): Still required for final ledger closing and official bank statements.

Specifically, we design a “hybrid sync” model. This ensures that the platform is always as fast as the market requires, but as stable as the accountants demand. Ultimately, this creates a reliable and high-performance environment for capital management.

In conclusion, a sophisticated integration strategy removes the technical barriers to global liquidity. Furthermore, it ensures that your treasury platform remains a flexible asset rather than a rigid burden. Therefore, investing in superior connectivity is a non-negotiable step for enterprise leaders.

Cost to Build a Unified Treasury Platform

There’s no single fixed cost for building a unified treasury platform, because what you’re really building is financial infrastructure, not just software.

The investment depends on how deeply you want to unify systems, how many banks and entities you operate across, and whether you’re building a visibility layer or full treasury orchestration.

However, based on enterprise implementations, here’s what a realistic cost range looks like.

Total Investment Range by Platform Scope

| Platform Scope | Timeline | Estimated Investment |

| MVP (Cash Visibility Layer) – 3–5 banks, basic dashboards | 3–5 months | $120,000 – $300,000 |

| Mid-Scale Platform – payments hub + forecasting + integrations | 6–9 months | $300,000 – $800,000 |

| Full Unified Treasury Platform – multi-entity, FX, risk, automation | 9–15 months | $800,000 – $2,000,000+ |

| Enterprise-Grade Infrastructure – global banks, real-time, compliance-heavy | 15–24 months | $2,000,000 – $5,000,000+ |

Note: These ranges assume an experienced fintech engineering team. Lower-cost teams may reduce upfront cost but often extend timelines and increase integration risk.

Cost Breakdown by Core Modules

| Module | % of Total Cost | Why It Matters |

| Bank Integrations & Connectivity | 20–30% | Most complex layer; varies by number of banks and formats |

| Cash Visibility & Data Layer | 15–20% | Real-time aggregation, normalization, and accuracy |

| Payments Hub & Orchestration | 15–20% | Routing, execution, approvals, fraud controls |

| Forecasting & Analytics Engine | 10–15% | AI models, historical data pipelines, scenario planning |

| FX & Risk Management | 5–10% | Exposure tracking, hedging workflows |

| Compliance & Reporting | 5–10% | Audit trails, regulatory reporting, controls |

| UI/UX & Dashboards | 5–10% | Decision-making interfaces for treasury teams |

Integration and Infrastructure Costs

Integration is where most treasury projects either succeed or fail—and it’s also where a large portion of the budget goes.

Key cost drivers include:

- Number of bank connections (APIs, SWIFT, host-to-host)

- ERP integrations (SAP, Oracle, NetSuite, custom systems)

- Data normalization across entities and currencies

- Real-time vs batch processing architecture

- Security layers (encryption, access controls, fraud detection)

In complex enterprise setups, integration alone can account for 30–40% of total cost.

Infrastructure and Ongoing Costs

Beyond development, treasury platforms require continuous investment to stay reliable and compliant.

Typical ongoing costs include:

- Cloud infrastructure and data processing

- Bank API maintenance and updates

- Compliance upgrades (ISO 20022, regional regulations)

- Monitoring, logging, and system resilience

- Feature expansion and scaling

Most enterprises allocate 15–25% of initial build cost annually for maintenance and upgrades.

Hidden Costs Enterprises Often Overlook

Most treasury budgets underestimate these factors:

- Manual workarounds due to incomplete integrations

- Consultant dependency during long implementations

- Rebuilding failed or underperforming systems

- Delays caused by poor data standardization

- Internal resource allocation (IT + treasury teams)

These hidden costs can increase total investment by 20–35% if not planned upfront.

What Actually Drives Cost the Most

If you’re evaluating a budget, focus on these three variables:

- Integration complexity (number of banks, ERPs, entities)

- Real-time vs batch architecture requirements

- Depth of automation and intelligence (AI, forecasting, risk)

Get a Custom Cost Estimate for Your Treasury Platform

At Intellivon, we assess your current treasury setup, integration landscape, and growth plans to give you a clear, realistic cost estimate before you commit to development.

Talk to our experts to get a tailored cost breakdown for your platform.

Where Treasury Platforms Are Headed Next

The landscape of corporate finance is shifting toward dynamic, autonomous systems. Enterprises must now prepare for a transition from manual monitoring to AI-orchestrated execution.

1. Rise of Agentic AI in Treasury

Unlike traditional automation, agentic AI pursues specific financial goals independently. This technology analyzes liquidity shortfalls and executes rebalancing across global accounts without human intervention.

- Self-Correcting Workflows: These agents identify payment failures and reroute them through alternative banks immediately.

- Predictive Negotiation: AI agents monitor market rates to suggest the optimal moment for large FX trades.

- Contextual Reasoning: The system distinguishes between harmless seasonal spikes and potential fraud attempts automatically.

Furthermore, this reduces the cognitive load on treasury teams. Consequently, specialists can focus on high-level capital allocation and risk strategy.

2. Real-Time Payments Replacing Batch Flows

Real-time payment (RTP) rails like FedNow are becoming the global standard for enterprise commerce. This eliminates the traditional “waiting period” for cross-border and domestic transfers.

| Feature | Legacy Batch Flow | Real-Time Payments (RTP) |

| Availability | Banking hours only | 24/7/365 |

| Settlement Speed | 1–3 business days | Seconds |

| Data Richness | Limited | High (ISO 20022-based) |

| Liquidity Impact | High capital lock-up | Immediate capital utility |

Specifically, businesses no longer need to hold massive cash buffers to cover pending transactions. Therefore, suppliers receive funds instantly, which strengthens supply chain resilience.

3. Stablecoins and Tokenized Liquidity

Leading enterprises are exploring blockchain-based assets to bypass the friction of traditional banking. Stablecoins offer a programmable way to move value across borders instantly.

- 24/7 Cross-Border Rails: Move capital between global regions on weekends without waiting for bank openings.

- Smart Contract Escrow: Release payments automatically once specific shipping or delivery conditions are met.

- Tokenized Yield: Deploy idle balances into tokenized money market funds for instant returns.

Consequently, modern platforms must manage both fiat and digital assets within a single workflow. This represents a fundamental shift in how enterprises define and move cash.

4. ISO 20022 Impact on Treasury Systems

The transition to ISO 20022 replaces thin, text-based messages with rich, structured data. This global standard is the essential fuel for future AI-driven finance.

- End-to-End Tracking: Every payment carries detailed metadata, such as invoice numbers and tax info.

- Automated Reconciliation: Systems match 100% of incoming payments to bills without manual intervention.

- Global Interoperability: A payment sent from London to Tokyo uses the same “language,” reducing rejections.

Therefore, richer data allows for much higher “straight-through processing” rates. Specifically, it enables machines to optimize workflows with far greater precision.

5. What Autonomous Treasury Looks Like

The final evolution is the “Autonomous Treasury,” where platforms handle daily operations independently within strict guardrails. This state ensures that global liquidity is always optimized without human effort.

- Zero-Touch Positioning: The system pools cash across 50+ countries based on predicted needs.

- Automated Hedge Execution: The platform executes currency hedges automatically when risk limits are breached.

- Autonomous Compliance: AI agents audit every transaction in real-time against global tax laws.

Ultimately, this allows the organization to scale financial operations without increasing headcount. Furthermore, it ensures the system never sleeps and never misses a detail.

In conclusion, the future belongs to those who view treasury as a high-tech infrastructure play. Adopting these technologies ensures long-term agility in an increasingly instant global economy.

Conclusion

Building a unified treasury platform transforms financial operations from a reactive cost center into a proactive growth engine. By centralizing data and automating execution, enterprises achieve the liquidity and agility required for global scale.

Investing in this infrastructure ensures long-term resilience, enabling leaders to capitalize on every market opportunity.

How Intellivon Can Help You Make A Unified Treasury Platform

Engineering a unified treasury platform requires building a financial infrastructure layer that can centralize liquidity, unify data flows, and enable real-time decision-making across the enterprise.

At Intellivon, we design unified treasury platforms that bring together cash visibility, payments, forecasting, and risk into a single, high-performance system. Our pre-vetted .NETMAUI developers build real-time unified treasury platforms tailored to your KPIs.

A. Bridging Fragmented Treasury Systems

Most enterprises operate across disconnected ERPs, bank portals, and legacy treasury tools that were never designed to work together.

We build the orchestration layer that connects and unifies your entire treasury ecosystem.

- Middleware connecting ERP, banking systems, and treasury tools

- Real-time data synchronization across entities and geographies

- Gradual integration without disrupting existing operations

This allows you to unify treasury operations without replacing your entire system stack.

B. Building a Centralized Cash Visibility Engine

Treasury decisions are only as strong as the visibility behind them. We design systems that provide a real-time, unified view of liquidity.

- Aggregation of balances across global bank accounts

- Multi-entity and multi-currency cash positioning

- Real-time dashboards for enterprise-wide visibility

This ensures treasury teams move from delayed reporting to real-time control.

C. Designing Intelligent Treasury Orchestration Layers

We move treasury from static workflows to dynamic, decision-driven systems.

- Rule-based and AI-driven cash flow orchestration

- Automated fund allocation and liquidity movement

- Event-driven workflows across treasury operations

This enables faster, more accurate treasury decisions at scale.

D. Enabling Real-Time Payments and Execution Control

Execution is where most treasury fragmentation exists. We build centralized payment hubs that unify and control transaction flows.

- Centralized payment initiation and approval systems

- Integration with global payment rails and banking networks

- Real-time monitoring and execution tracking

This ensures consistent, secure, and controlled transaction execution across the enterprise.

E. Embedding Forecasting and Liquidity Intelligence

We design platforms that go beyond visibility and enable predictive decision-making.

- AI-powered cash flow forecasting models

- Scenario analysis and liquidity planning tools

- Integration of historical and real-time financial data

This transforms treasury from reactive operations to a proactive financial strategy.

F. Integrating Compliance and Risk at the Core

Treasury systems must operate within strict regulatory and risk frameworks. We embed compliance into the system architecture from day one.

- Built-in audit trails and reporting frameworks

- Regulatory compliance aligned with global standards

- Risk monitoring across transactions and exposures

This ensures your treasury platform remains secure, compliant, and audit-ready at all times.

By partnering with Intellivon, you’re building a unified financial infrastructure layer that gives your enterprise real-time visibility, control, and scalability.

Ready to build a unified treasury platform that works across systems, entities, and real-world complexity?

Talk to Intellivon’s experts and get a tailored architecture and cost estimate for your platform.

FAQs

Q1. Do I need a standalone treasury platform if my ERP has a treasury module?

ERP treasury modules handle the basics. However, they lack real-time bank connectivity, advanced forecasting, and FX risk management. Once you operate across multiple entities or currencies, a standalone platform becomes necessary.

Q2. How much does a treasury platform actually cost annually?

Mid-market platforms typically range from $50,000 to $150,000 annually. Enterprise deployments can exceed that significantly. Licensing is often 40–60% of the total cost, which includes implementation, integration, and support add the rest.

Q3. What’s the typical ROI timeline on a treasury platform implementation?

Most enterprises see measurable ROI within 12 to 18 months. Faster visibility into idle cash and reduced reconciliation time delivers early returns. Full strategic ROI compounds over 24 to 36 months.

Q4. API-first vs. SWIFT vs. EBICS vs. host-to-host — which model should we use?

API-first delivers real-time data and suits modern banks. SWIFT covers global reach. EBICS is standard across Europe. Host-to-host works for legacy relationships. Therefore, most enterprises need a platform supporting all four.

Q5. How do we quantify the business case for treasury technology spend?

Model forecast accuracy improvement, reconciliation time saved, idle cash reduction, and fraud incident costs avoided. In addition, factor in audit readiness and M&A onboarding speed. Together, these build a defensible board-level ROI case.

Q7. What’s a reasonable number of pre-integrated banks and ERPs?

A credible enterprise platform should connect to at least 50 ERP systems and 100 banks at a minimum. However, connectivity quality matters more than quantity, and prioritizes depth of integration over breadth of logos.